Financial Performance Analysis of Betelgeuse Hotels and Summerlea Plc

VerifiedAdded on 2023/01/06

|11

|2653

|32

Report

AI Summary

This report presents a comprehensive financial analysis of two companies: Betelgeuse Hotels and Summerlea Plc. The first part focuses on the formulation of financial statements, including an income statement and balance sheet for Betelgeuse Hotels as of December 31, 2019. The income statement details revenues, expenses, and the calculation of net profit, while the balance sheet presents the company's assets, liabilities, and equity. The second part of the report analyzes Summerlea Plc through various financial ratios, including profitability (net profit margin, return on owner's equity), liquidity (acid test ratio), efficiency (account receivable collection period), and capital structure (interest cover ratio). The analysis compares and contrasts the financial performance of Summerlea Plc between 2018 and 2019, highlighting trends and providing interpretations of the calculated ratios to assess the company's financial health and operational efficiency. The report includes working notes for the calculations and concludes with a summary of the findings.

Statistics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Formulation of income statement and balance sheet...................................................................1

TASK 2............................................................................................................................................3

Calculation of financial ratios along with comparison and contrasting of them for year 2018

and 2019.......................................................................................................................................3

CONCLUSION................................................................................................................................5

REFRENCES...................................................................................................................................7

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Formulation of income statement and balance sheet...................................................................1

TASK 2............................................................................................................................................3

Calculation of financial ratios along with comparison and contrasting of them for year 2018

and 2019.......................................................................................................................................3

CONCLUSION................................................................................................................................5

REFRENCES...................................................................................................................................7

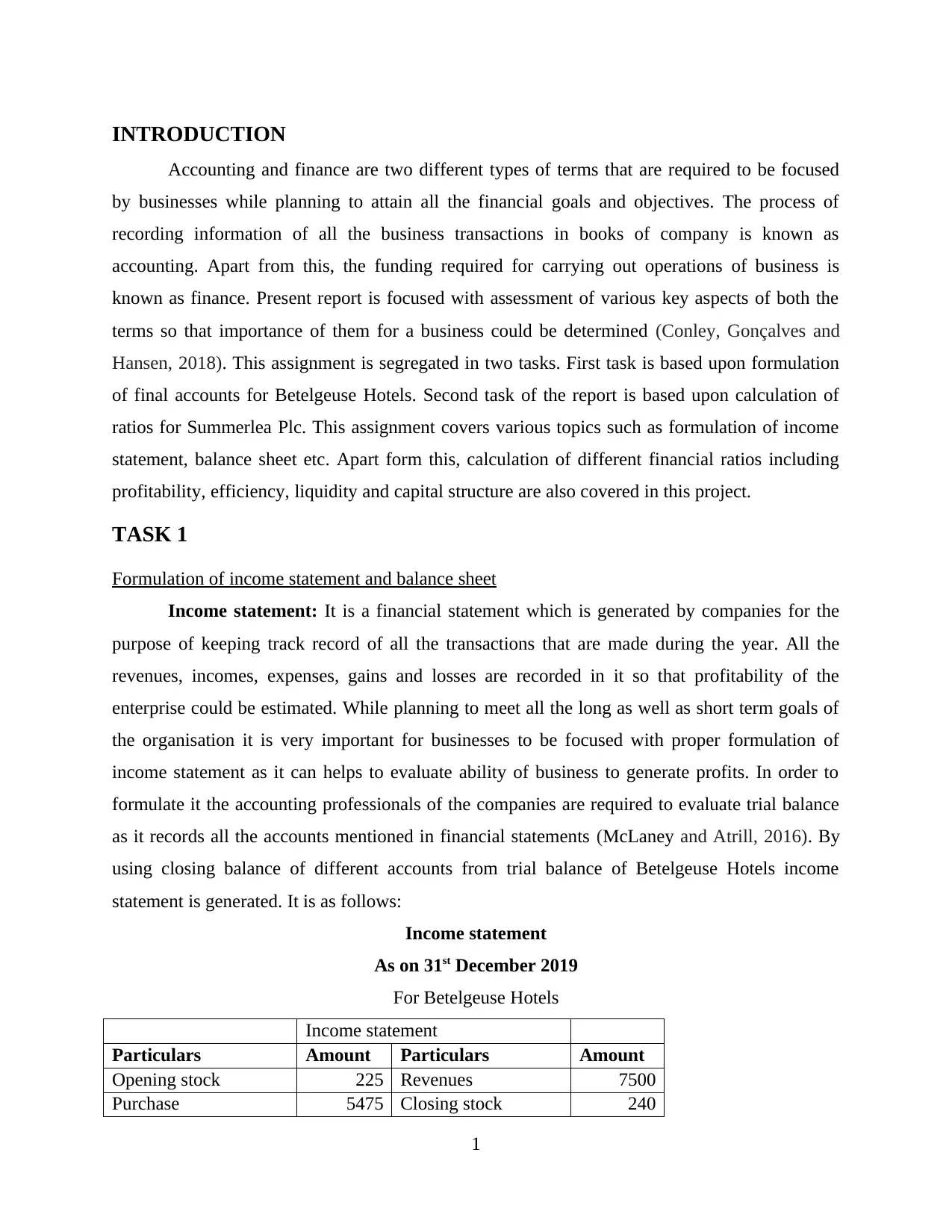

INTRODUCTION

Accounting and finance are two different types of terms that are required to be focused

by businesses while planning to attain all the financial goals and objectives. The process of

recording information of all the business transactions in books of company is known as

accounting. Apart from this, the funding required for carrying out operations of business is

known as finance. Present report is focused with assessment of various key aspects of both the

terms so that importance of them for a business could be determined (Conley, Gonçalves and

Hansen, 2018). This assignment is segregated in two tasks. First task is based upon formulation

of final accounts for Betelgeuse Hotels. Second task of the report is based upon calculation of

ratios for Summerlea Plc. This assignment covers various topics such as formulation of income

statement, balance sheet etc. Apart form this, calculation of different financial ratios including

profitability, efficiency, liquidity and capital structure are also covered in this project.

TASK 1

Formulation of income statement and balance sheet

Income statement: It is a financial statement which is generated by companies for the

purpose of keeping track record of all the transactions that are made during the year. All the

revenues, incomes, expenses, gains and losses are recorded in it so that profitability of the

enterprise could be estimated. While planning to meet all the long as well as short term goals of

the organisation it is very important for businesses to be focused with proper formulation of

income statement as it can helps to evaluate ability of business to generate profits. In order to

formulate it the accounting professionals of the companies are required to evaluate trial balance

as it records all the accounts mentioned in financial statements (McLaney and Atrill, 2016). By

using closing balance of different accounts from trial balance of Betelgeuse Hotels income

statement is generated. It is as follows:

Income statement

As on 31st December 2019

For Betelgeuse Hotels

Income statement

Particulars Amount Particulars Amount

Opening stock 225 Revenues 7500

Purchase 5475 Closing stock 240

1

Accounting and finance are two different types of terms that are required to be focused

by businesses while planning to attain all the financial goals and objectives. The process of

recording information of all the business transactions in books of company is known as

accounting. Apart from this, the funding required for carrying out operations of business is

known as finance. Present report is focused with assessment of various key aspects of both the

terms so that importance of them for a business could be determined (Conley, Gonçalves and

Hansen, 2018). This assignment is segregated in two tasks. First task is based upon formulation

of final accounts for Betelgeuse Hotels. Second task of the report is based upon calculation of

ratios for Summerlea Plc. This assignment covers various topics such as formulation of income

statement, balance sheet etc. Apart form this, calculation of different financial ratios including

profitability, efficiency, liquidity and capital structure are also covered in this project.

TASK 1

Formulation of income statement and balance sheet

Income statement: It is a financial statement which is generated by companies for the

purpose of keeping track record of all the transactions that are made during the year. All the

revenues, incomes, expenses, gains and losses are recorded in it so that profitability of the

enterprise could be estimated. While planning to meet all the long as well as short term goals of

the organisation it is very important for businesses to be focused with proper formulation of

income statement as it can helps to evaluate ability of business to generate profits. In order to

formulate it the accounting professionals of the companies are required to evaluate trial balance

as it records all the accounts mentioned in financial statements (McLaney and Atrill, 2016). By

using closing balance of different accounts from trial balance of Betelgeuse Hotels income

statement is generated. It is as follows:

Income statement

As on 31st December 2019

For Betelgeuse Hotels

Income statement

Particulars Amount Particulars Amount

Opening stock 225 Revenues 7500

Purchase 5475 Closing stock 240

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

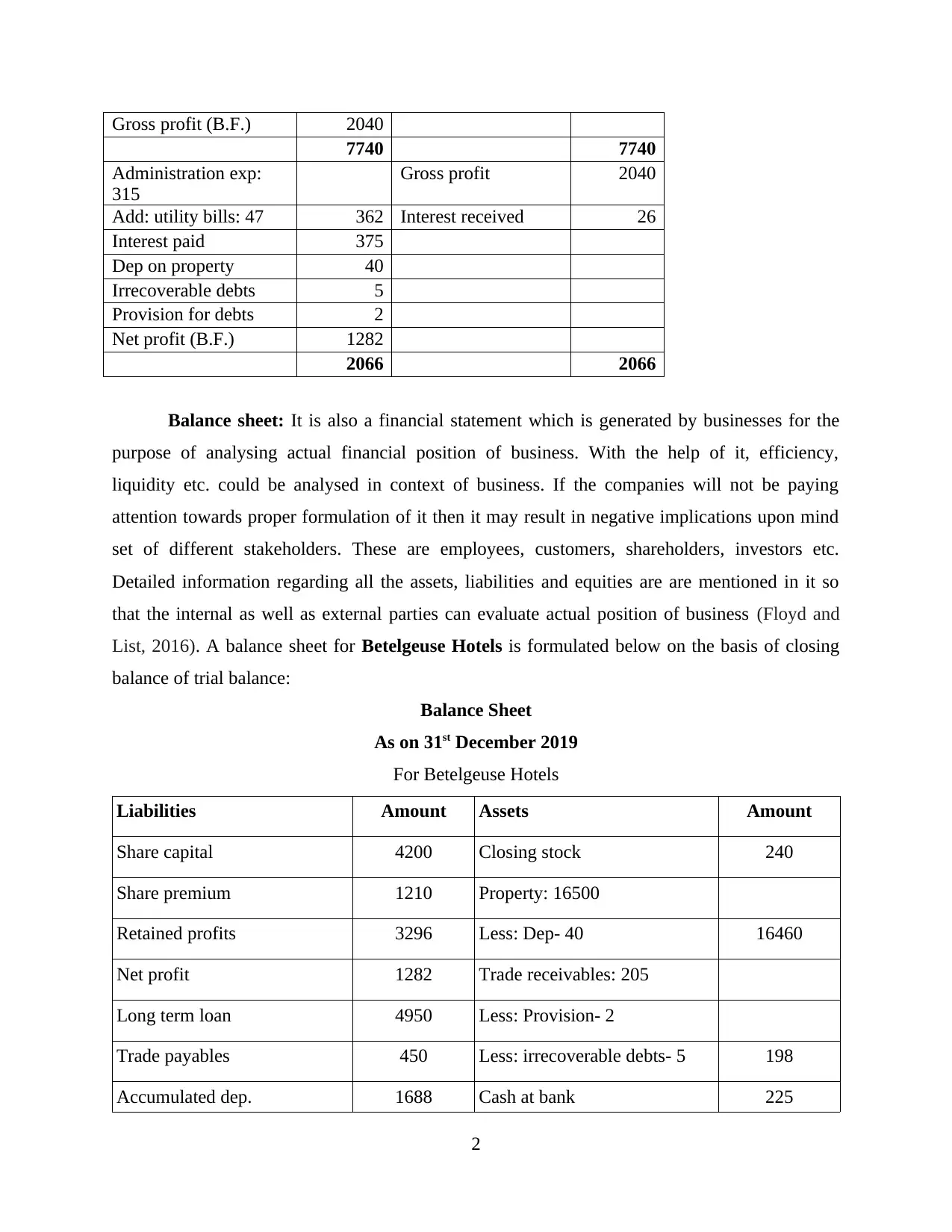

Gross profit (B.F.) 2040

7740 7740

Administration exp:

315

Gross profit 2040

Add: utility bills: 47 362 Interest received 26

Interest paid 375

Dep on property 40

Irrecoverable debts 5

Provision for debts 2

Net profit (B.F.) 1282

2066 2066

Balance sheet: It is also a financial statement which is generated by businesses for the

purpose of analysing actual financial position of business. With the help of it, efficiency,

liquidity etc. could be analysed in context of business. If the companies will not be paying

attention towards proper formulation of it then it may result in negative implications upon mind

set of different stakeholders. These are employees, customers, shareholders, investors etc.

Detailed information regarding all the assets, liabilities and equities are are mentioned in it so

that the internal as well as external parties can evaluate actual position of business (Floyd and

List, 2016). A balance sheet for Betelgeuse Hotels is formulated below on the basis of closing

balance of trial balance:

Balance Sheet

As on 31st December 2019

For Betelgeuse Hotels

Liabilities Amount Assets Amount

Share capital 4200 Closing stock 240

Share premium 1210 Property: 16500

Retained profits 3296 Less: Dep- 40 16460

Net profit 1282 Trade receivables: 205

Long term loan 4950 Less: Provision- 2

Trade payables 450 Less: irrecoverable debts- 5 198

Accumulated dep. 1688 Cash at bank 225

2

7740 7740

Administration exp:

315

Gross profit 2040

Add: utility bills: 47 362 Interest received 26

Interest paid 375

Dep on property 40

Irrecoverable debts 5

Provision for debts 2

Net profit (B.F.) 1282

2066 2066

Balance sheet: It is also a financial statement which is generated by businesses for the

purpose of analysing actual financial position of business. With the help of it, efficiency,

liquidity etc. could be analysed in context of business. If the companies will not be paying

attention towards proper formulation of it then it may result in negative implications upon mind

set of different stakeholders. These are employees, customers, shareholders, investors etc.

Detailed information regarding all the assets, liabilities and equities are are mentioned in it so

that the internal as well as external parties can evaluate actual position of business (Floyd and

List, 2016). A balance sheet for Betelgeuse Hotels is formulated below on the basis of closing

balance of trial balance:

Balance Sheet

As on 31st December 2019

For Betelgeuse Hotels

Liabilities Amount Assets Amount

Share capital 4200 Closing stock 240

Share premium 1210 Property: 16500

Retained profits 3296 Less: Dep- 40 16460

Net profit 1282 Trade receivables: 205

Long term loan 4950 Less: Provision- 2

Trade payables 450 Less: irrecoverable debts- 5 198

Accumulated dep. 1688 Cash at bank 225

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

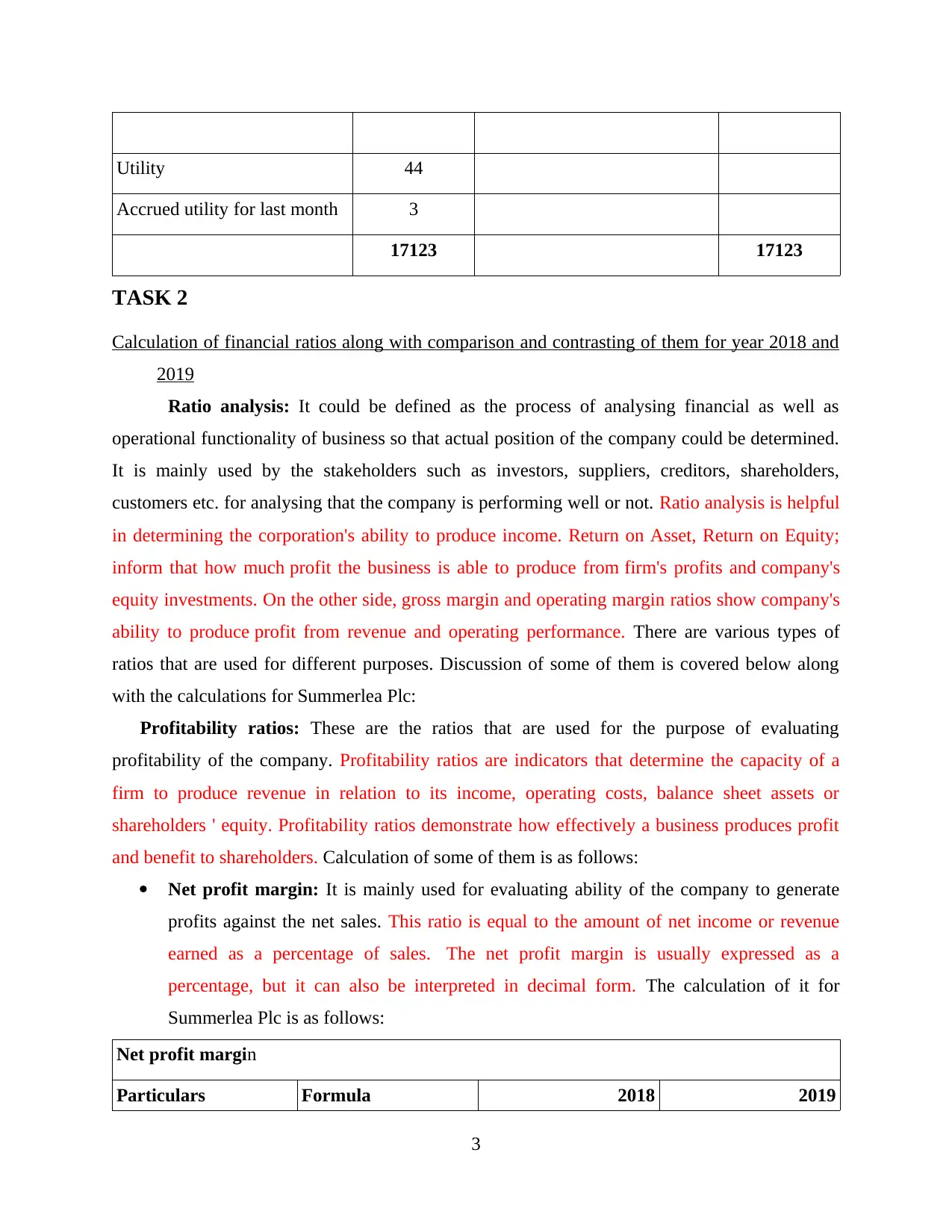

Utility 44

Accrued utility for last month 3

17123 17123

TASK 2

Calculation of financial ratios along with comparison and contrasting of them for year 2018 and

2019

Ratio analysis: It could be defined as the process of analysing financial as well as

operational functionality of business so that actual position of the company could be determined.

It is mainly used by the stakeholders such as investors, suppliers, creditors, shareholders,

customers etc. for analysing that the company is performing well or not. Ratio analysis is helpful

in determining the corporation's ability to produce income. Return on Asset, Return on Equity;

inform that how much profit the business is able to produce from firm's profits and company's

equity investments. On the other side, gross margin and operating margin ratios show company's

ability to produce profit from revenue and operating performance. There are various types of

ratios that are used for different purposes. Discussion of some of them is covered below along

with the calculations for Summerlea Plc:

Profitability ratios: These are the ratios that are used for the purpose of evaluating

profitability of the company. Profitability ratios are indicators that determine the capacity of a

firm to produce revenue in relation to its income, operating costs, balance sheet assets or

shareholders ' equity. Profitability ratios demonstrate how effectively a business produces profit

and benefit to shareholders. Calculation of some of them is as follows:

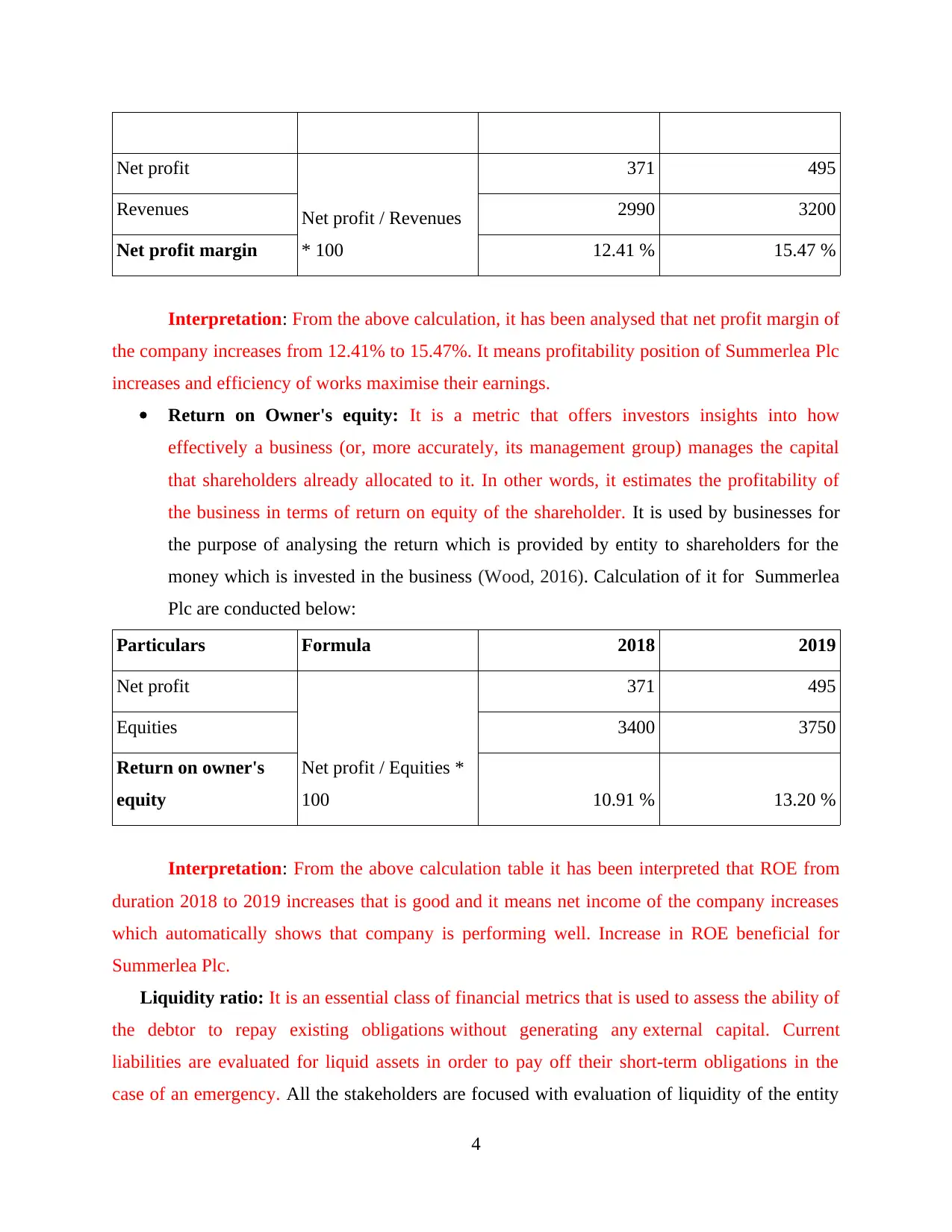

Net profit margin: It is mainly used for evaluating ability of the company to generate

profits against the net sales. This ratio is equal to the amount of net income or revenue

earned as a percentage of sales. The net profit margin is usually expressed as a

percentage, but it can also be interpreted in decimal form. The calculation of it for

Summerlea Plc is as follows:

Net profit margin

Particulars Formula 2018 2019

3

Accrued utility for last month 3

17123 17123

TASK 2

Calculation of financial ratios along with comparison and contrasting of them for year 2018 and

2019

Ratio analysis: It could be defined as the process of analysing financial as well as

operational functionality of business so that actual position of the company could be determined.

It is mainly used by the stakeholders such as investors, suppliers, creditors, shareholders,

customers etc. for analysing that the company is performing well or not. Ratio analysis is helpful

in determining the corporation's ability to produce income. Return on Asset, Return on Equity;

inform that how much profit the business is able to produce from firm's profits and company's

equity investments. On the other side, gross margin and operating margin ratios show company's

ability to produce profit from revenue and operating performance. There are various types of

ratios that are used for different purposes. Discussion of some of them is covered below along

with the calculations for Summerlea Plc:

Profitability ratios: These are the ratios that are used for the purpose of evaluating

profitability of the company. Profitability ratios are indicators that determine the capacity of a

firm to produce revenue in relation to its income, operating costs, balance sheet assets or

shareholders ' equity. Profitability ratios demonstrate how effectively a business produces profit

and benefit to shareholders. Calculation of some of them is as follows:

Net profit margin: It is mainly used for evaluating ability of the company to generate

profits against the net sales. This ratio is equal to the amount of net income or revenue

earned as a percentage of sales. The net profit margin is usually expressed as a

percentage, but it can also be interpreted in decimal form. The calculation of it for

Summerlea Plc is as follows:

Net profit margin

Particulars Formula 2018 2019

3

Net profit

Net profit / Revenues

* 100

371 495

Revenues 2990 3200

Net profit margin 12.41 % 15.47 %

Interpretation: From the above calculation, it has been analysed that net profit margin of

the company increases from 12.41% to 15.47%. It means profitability position of Summerlea Plc

increases and efficiency of works maximise their earnings.

Return on Owner's equity: It is a metric that offers investors insights into how

effectively a business (or, more accurately, its management group) manages the capital

that shareholders already allocated to it. In other words, it estimates the profitability of

the business in terms of return on equity of the shareholder. It is used by businesses for

the purpose of analysing the return which is provided by entity to shareholders for the

money which is invested in the business (Wood, 2016). Calculation of it for Summerlea

Plc are conducted below:

Particulars Formula 2018 2019

Net profit

Net profit / Equities *

100

371 495

Equities 3400 3750

Return on owner's

equity 10.91 % 13.20 %

Interpretation: From the above calculation table it has been interpreted that ROE from

duration 2018 to 2019 increases that is good and it means net income of the company increases

which automatically shows that company is performing well. Increase in ROE beneficial for

Summerlea Plc.

Liquidity ratio: It is an essential class of financial metrics that is used to assess the ability of

the debtor to repay existing obligations without generating any external capital. Current

liabilities are evaluated for liquid assets in order to pay off their short-term obligations in the

case of an emergency. All the stakeholders are focused with evaluation of liquidity of the entity

4

Net profit / Revenues

* 100

371 495

Revenues 2990 3200

Net profit margin 12.41 % 15.47 %

Interpretation: From the above calculation, it has been analysed that net profit margin of

the company increases from 12.41% to 15.47%. It means profitability position of Summerlea Plc

increases and efficiency of works maximise their earnings.

Return on Owner's equity: It is a metric that offers investors insights into how

effectively a business (or, more accurately, its management group) manages the capital

that shareholders already allocated to it. In other words, it estimates the profitability of

the business in terms of return on equity of the shareholder. It is used by businesses for

the purpose of analysing the return which is provided by entity to shareholders for the

money which is invested in the business (Wood, 2016). Calculation of it for Summerlea

Plc are conducted below:

Particulars Formula 2018 2019

Net profit

Net profit / Equities *

100

371 495

Equities 3400 3750

Return on owner's

equity 10.91 % 13.20 %

Interpretation: From the above calculation table it has been interpreted that ROE from

duration 2018 to 2019 increases that is good and it means net income of the company increases

which automatically shows that company is performing well. Increase in ROE beneficial for

Summerlea Plc.

Liquidity ratio: It is an essential class of financial metrics that is used to assess the ability of

the debtor to repay existing obligations without generating any external capital. Current

liabilities are evaluated for liquid assets in order to pay off their short-term obligations in the

case of an emergency. All the stakeholders are focused with evaluation of liquidity of the entity

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

so that they can analyse ability of the firm to repay the debts. There are various types of this ratio

and one of this calculated below:

Acid test ratio: It is used by business entities for the purpose of evaluating ability of

firm to meet their short term obligations with the help of core current assets. This

ratio also calculated by the organization to identify their ability to pay their

obligation in case of any emergency. Short term debt should be paying off with their

short term assets which include the debtors, cash in hand or cash at bank. This ratio

is calculated below for Summerlea Plc:

Acid test ratio

Particulars Formula 2018 2019

Liquid assets

Liquid assets / current

liabilities

750 650

Current liabilities 520 385

Acid test ratio 1.44 1.69

Interpretation: From the above calculation of acid test ratio, in 2018 it was 1.44 times

and in 2019 it was 1.69 times. Both year ratios are higher than its ideal ratio that is 1:1. In order

to maintain their liquidity managers need to build some strategy where they have to effectively

use their resources. Higher the liquidity position means, company able to meet their current

obligation with the help of liquid assets.

Efficiency ratio: These ratios are compare what actually company owns to its revenue or

profit results and notify investors about the capacity of a firm to use what someone has to

produce as much revenue as possible for owners and investors. This ratio is used to contrast the

net revenues of a business with its total average assets. In business entities accounting

professionals calculate different types of ratios to determine the efficiency of business to

generate revenues and collect owed amount from clients. One of them is calculated below for

Summerlea Plc:

Account receivable collection period ratio: It is used by businesses for the purpose

of evaluating the time period which will be taken by the debtors to make payment of

outstanding amount (Mburayi and Wall, 2018). It calculation for Summerlea Plc is

as follows:

5

and one of this calculated below:

Acid test ratio: It is used by business entities for the purpose of evaluating ability of

firm to meet their short term obligations with the help of core current assets. This

ratio also calculated by the organization to identify their ability to pay their

obligation in case of any emergency. Short term debt should be paying off with their

short term assets which include the debtors, cash in hand or cash at bank. This ratio

is calculated below for Summerlea Plc:

Acid test ratio

Particulars Formula 2018 2019

Liquid assets

Liquid assets / current

liabilities

750 650

Current liabilities 520 385

Acid test ratio 1.44 1.69

Interpretation: From the above calculation of acid test ratio, in 2018 it was 1.44 times

and in 2019 it was 1.69 times. Both year ratios are higher than its ideal ratio that is 1:1. In order

to maintain their liquidity managers need to build some strategy where they have to effectively

use their resources. Higher the liquidity position means, company able to meet their current

obligation with the help of liquid assets.

Efficiency ratio: These ratios are compare what actually company owns to its revenue or

profit results and notify investors about the capacity of a firm to use what someone has to

produce as much revenue as possible for owners and investors. This ratio is used to contrast the

net revenues of a business with its total average assets. In business entities accounting

professionals calculate different types of ratios to determine the efficiency of business to

generate revenues and collect owed amount from clients. One of them is calculated below for

Summerlea Plc:

Account receivable collection period ratio: It is used by businesses for the purpose

of evaluating the time period which will be taken by the debtors to make payment of

outstanding amount (Mburayi and Wall, 2018). It calculation for Summerlea Plc is

as follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

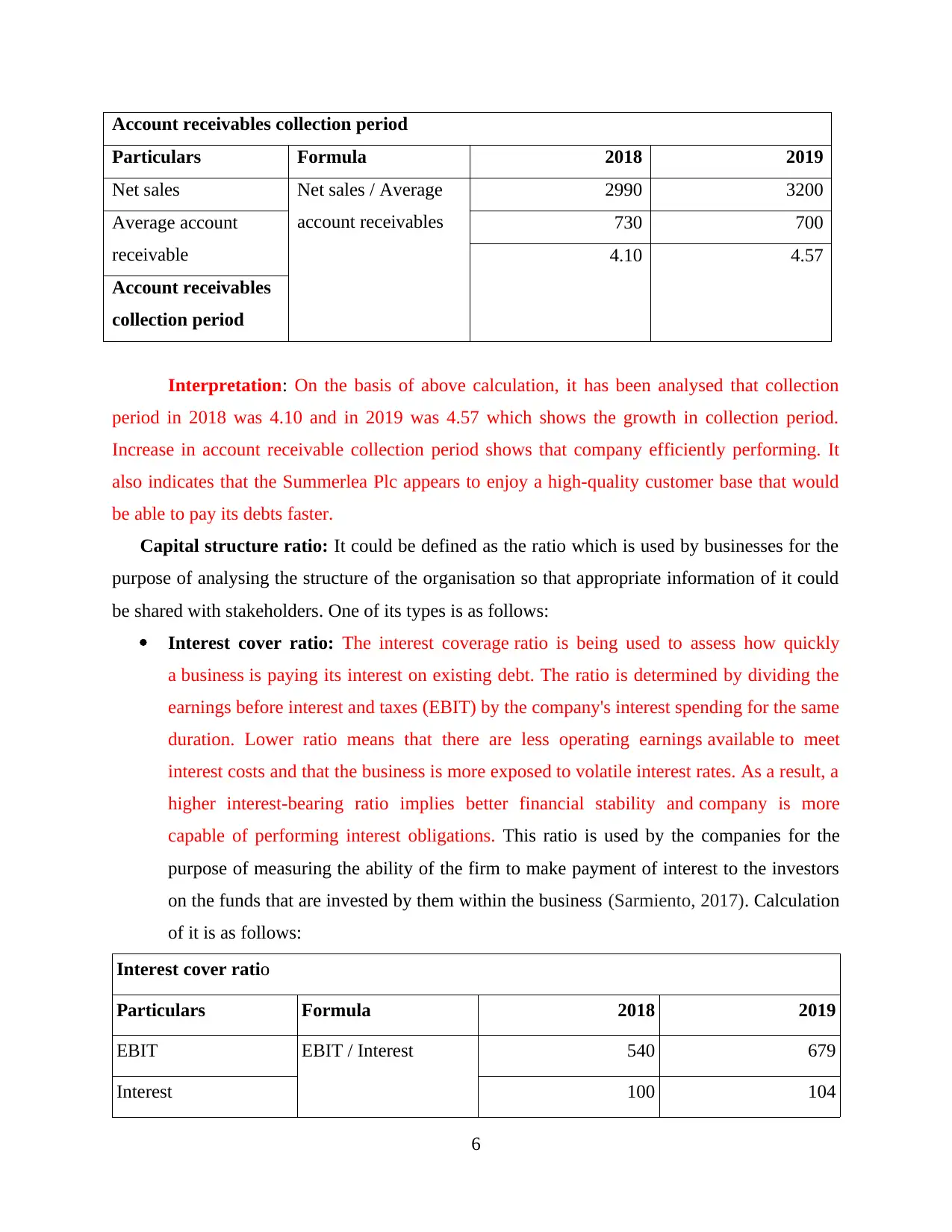

Account receivables collection period

Particulars Formula 2018 2019

Net sales Net sales / Average

account receivables

2990 3200

Average account

receivable

730 700

4.10 4.57

Account receivables

collection period

Interpretation: On the basis of above calculation, it has been analysed that collection

period in 2018 was 4.10 and in 2019 was 4.57 which shows the growth in collection period.

Increase in account receivable collection period shows that company efficiently performing. It

also indicates that the Summerlea Plc appears to enjoy a high-quality customer base that would

be able to pay its debts faster.

Capital structure ratio: It could be defined as the ratio which is used by businesses for the

purpose of analysing the structure of the organisation so that appropriate information of it could

be shared with stakeholders. One of its types is as follows:

Interest cover ratio: The interest coverage ratio is being used to assess how quickly

a business is paying its interest on existing debt. The ratio is determined by dividing the

earnings before interest and taxes (EBIT) by the company's interest spending for the same

duration. Lower ratio means that there are less operating earnings available to meet

interest costs and that the business is more exposed to volatile interest rates. As a result, a

higher interest-bearing ratio implies better financial stability and company is more

capable of performing interest obligations. This ratio is used by the companies for the

purpose of measuring the ability of the firm to make payment of interest to the investors

on the funds that are invested by them within the business (Sarmiento, 2017). Calculation

of it is as follows:

Interest cover ratio

Particulars Formula 2018 2019

EBIT EBIT / Interest 540 679

Interest 100 104

6

Particulars Formula 2018 2019

Net sales Net sales / Average

account receivables

2990 3200

Average account

receivable

730 700

4.10 4.57

Account receivables

collection period

Interpretation: On the basis of above calculation, it has been analysed that collection

period in 2018 was 4.10 and in 2019 was 4.57 which shows the growth in collection period.

Increase in account receivable collection period shows that company efficiently performing. It

also indicates that the Summerlea Plc appears to enjoy a high-quality customer base that would

be able to pay its debts faster.

Capital structure ratio: It could be defined as the ratio which is used by businesses for the

purpose of analysing the structure of the organisation so that appropriate information of it could

be shared with stakeholders. One of its types is as follows:

Interest cover ratio: The interest coverage ratio is being used to assess how quickly

a business is paying its interest on existing debt. The ratio is determined by dividing the

earnings before interest and taxes (EBIT) by the company's interest spending for the same

duration. Lower ratio means that there are less operating earnings available to meet

interest costs and that the business is more exposed to volatile interest rates. As a result, a

higher interest-bearing ratio implies better financial stability and company is more

capable of performing interest obligations. This ratio is used by the companies for the

purpose of measuring the ability of the firm to make payment of interest to the investors

on the funds that are invested by them within the business (Sarmiento, 2017). Calculation

of it is as follows:

Interest cover ratio

Particulars Formula 2018 2019

EBIT EBIT / Interest 540 679

Interest 100 104

6

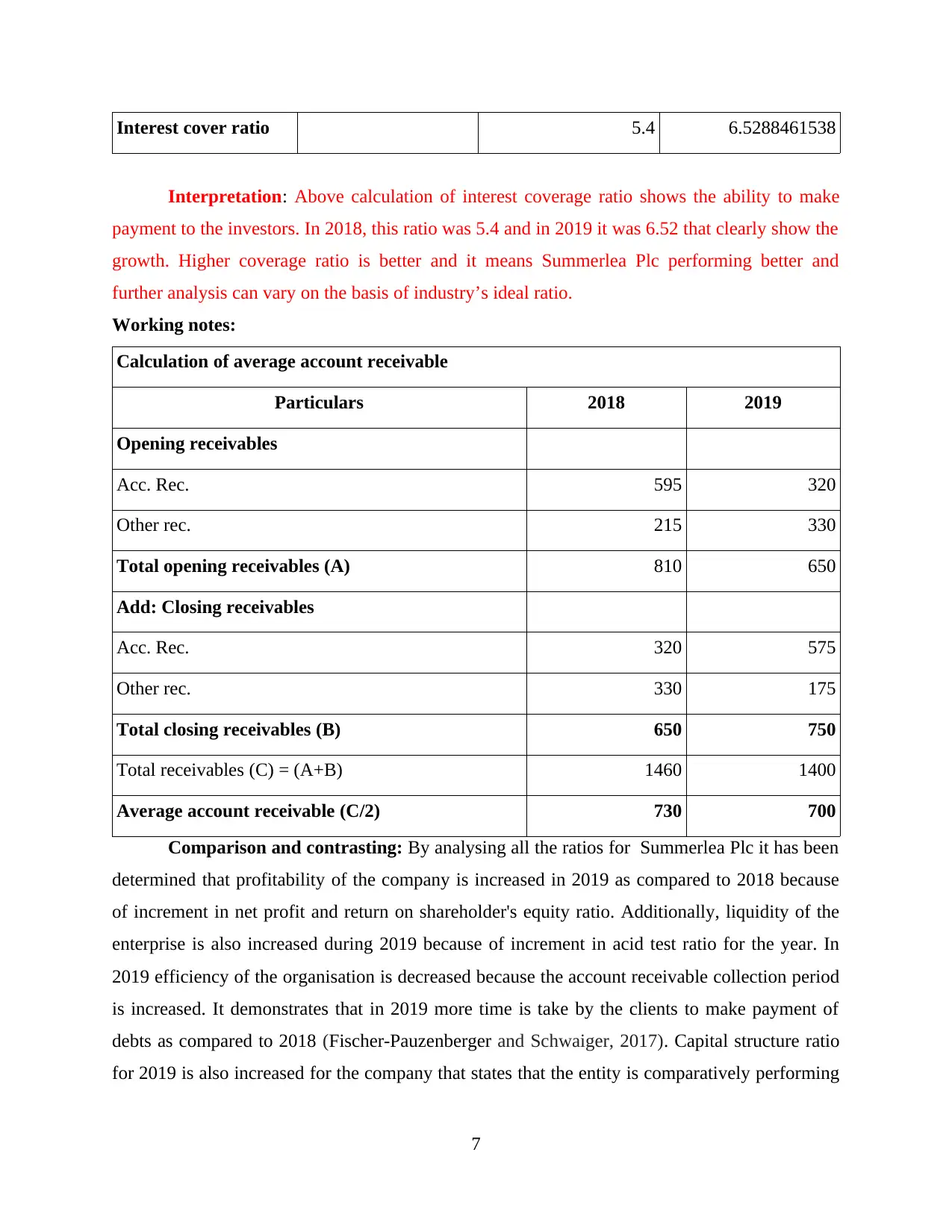

Interest cover ratio 5.4 6.5288461538

Interpretation: Above calculation of interest coverage ratio shows the ability to make

payment to the investors. In 2018, this ratio was 5.4 and in 2019 it was 6.52 that clearly show the

growth. Higher coverage ratio is better and it means Summerlea Plc performing better and

further analysis can vary on the basis of industry’s ideal ratio.

Working notes:

Calculation of average account receivable

Particulars 2018 2019

Opening receivables

Acc. Rec. 595 320

Other rec. 215 330

Total opening receivables (A) 810 650

Add: Closing receivables

Acc. Rec. 320 575

Other rec. 330 175

Total closing receivables (B) 650 750

Total receivables (C) = (A+B) 1460 1400

Average account receivable (C/2) 730 700

Comparison and contrasting: By analysing all the ratios for Summerlea Plc it has been

determined that profitability of the company is increased in 2019 as compared to 2018 because

of increment in net profit and return on shareholder's equity ratio. Additionally, liquidity of the

enterprise is also increased during 2019 because of increment in acid test ratio for the year. In

2019 efficiency of the organisation is decreased because the account receivable collection period

is increased. It demonstrates that in 2019 more time is take by the clients to make payment of

debts as compared to 2018 (Fischer-Pauzenberger and Schwaiger, 2017). Capital structure ratio

for 2019 is also increased for the company that states that the entity is comparatively performing

7

Interpretation: Above calculation of interest coverage ratio shows the ability to make

payment to the investors. In 2018, this ratio was 5.4 and in 2019 it was 6.52 that clearly show the

growth. Higher coverage ratio is better and it means Summerlea Plc performing better and

further analysis can vary on the basis of industry’s ideal ratio.

Working notes:

Calculation of average account receivable

Particulars 2018 2019

Opening receivables

Acc. Rec. 595 320

Other rec. 215 330

Total opening receivables (A) 810 650

Add: Closing receivables

Acc. Rec. 320 575

Other rec. 330 175

Total closing receivables (B) 650 750

Total receivables (C) = (A+B) 1460 1400

Average account receivable (C/2) 730 700

Comparison and contrasting: By analysing all the ratios for Summerlea Plc it has been

determined that profitability of the company is increased in 2019 as compared to 2018 because

of increment in net profit and return on shareholder's equity ratio. Additionally, liquidity of the

enterprise is also increased during 2019 because of increment in acid test ratio for the year. In

2019 efficiency of the organisation is decreased because the account receivable collection period

is increased. It demonstrates that in 2019 more time is take by the clients to make payment of

debts as compared to 2018 (Fischer-Pauzenberger and Schwaiger, 2017). Capital structure ratio

for 2019 is also increased for the company that states that the entity is comparatively performing

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

better in 2019. Apart from this, it has also been analysed that the company is performing all the

operations in systematic manner in 2019 if it will be compared with 2018.

CONCLUSION

From the above project report it has been concluded that accounting and finance are two

main elements that are required to be taken in to consideration by businesses while planning to

improve profitability. In order to analyse that all the long as well as short term goals of the

business are attained or not the top level executives are required to formulate financial statements

in systematic manner. It can help to determine actual position of business. While determining

financial strength of the company different types of ratios could be calculated. Some of them are

profitability, efficiency, capital structure, liquidity etc.

8

operations in systematic manner in 2019 if it will be compared with 2018.

CONCLUSION

From the above project report it has been concluded that accounting and finance are two

main elements that are required to be taken in to consideration by businesses while planning to

improve profitability. In order to analyse that all the long as well as short term goals of the

business are attained or not the top level executives are required to formulate financial statements

in systematic manner. It can help to determine actual position of business. While determining

financial strength of the company different types of ratios could be calculated. Some of them are

profitability, efficiency, capital structure, liquidity etc.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFRENCES

Books and Journals:

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research. 56(4). pp.1139-1203.

McLaney, E. and Atrill, P., 2016. Accounting and finance an introduction. Pearson Education

Limited.

Floyd, E. and List, J. A., 2016. Using field experiments in accounting and finance. Journal of

Accounting Research. 54(2). pp.437-475.

Wood, D. A., 2016. Comparing the publication process in accounting, economics, finance,

management, marketing, psychology, and the natural sciences. Accounting Horizons.

30(3). pp.341-361.

Mburayi, L. and Wall, T., 2018. Sustainability in the professional accounting and finance

curriculum: an exploration. Higher Education, Skills and Work-Based Learning.

Fischer-Pauzenberger, C. and Schwaiger, W. S., 2017, November. The OntoREA© accounting

and finance model: ontological conceptualization of the accounting and finance domain.

In International Conference on Conceptual Modeling (pp. 506-519). Springer, Cham.

Sarmiento, C. P., 2017. Student perceptions of online homework in mathematics of accounting

and finance. Advanced Science Letters. 23(2). pp.1122-1125.

9

Books and Journals:

Conley, T., Gonçalves, S. and Hansen, C., 2018. Inference with dependent data in accounting

and finance applications. Journal of Accounting Research. 56(4). pp.1139-1203.

McLaney, E. and Atrill, P., 2016. Accounting and finance an introduction. Pearson Education

Limited.

Floyd, E. and List, J. A., 2016. Using field experiments in accounting and finance. Journal of

Accounting Research. 54(2). pp.437-475.

Wood, D. A., 2016. Comparing the publication process in accounting, economics, finance,

management, marketing, psychology, and the natural sciences. Accounting Horizons.

30(3). pp.341-361.

Mburayi, L. and Wall, T., 2018. Sustainability in the professional accounting and finance

curriculum: an exploration. Higher Education, Skills and Work-Based Learning.

Fischer-Pauzenberger, C. and Schwaiger, W. S., 2017, November. The OntoREA© accounting

and finance model: ontological conceptualization of the accounting and finance domain.

In International Conference on Conceptual Modeling (pp. 506-519). Springer, Cham.

Sarmiento, C. P., 2017. Student perceptions of online homework in mathematics of accounting

and finance. Advanced Science Letters. 23(2). pp.1122-1125.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.