Financial Analysis Report: The Unite Group plc Performance

VerifiedAdded on 2021/02/19

|14

|3059

|32

Report

AI Summary

This report provides a comprehensive financial analysis of The Unite Group plc, a leading student accommodation provider in the UK. It begins with an introduction to financial reporting and its importance, followed by a detailed calculation of various financial ratios, including profitability, liquidity, efficiency, and gearing ratios, for the years 2017 and 2018. The report then evaluates the company's performance and financial position based on these ratios, highlighting trends and improvements. Furthermore, the report analyzes the changes in lease accounting rules from IAS 17 to IFRS 16, discussing their implications. The analysis covers key financial metrics like net profit margin, current ratio, quick ratio, and debt-to-equity ratio. The conclusion summarizes the key findings, and the report includes references and an appendix for further information. The report emphasizes the company's financial health and strategic decisions based on the financial statements, including improvements in profitability, liquidity, and a shift in debt management.

Financial reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION......................................................................................................................................1

1. Calculation of Ratios...............................................................................................................1

2. Performance and position of The Unite Group plc.................................................................3

3. Analyse the change in Lease accounting rules........................................................................4

CONCLUSION................................................................................................................................7

REFERENCES ...............................................................................................................................8

APPENDEX ....................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION......................................................................................................................................1

1. Calculation of Ratios...............................................................................................................1

2. Performance and position of The Unite Group plc.................................................................3

3. Analyse the change in Lease accounting rules........................................................................4

CONCLUSION................................................................................................................................7

REFERENCES ...............................................................................................................................8

APPENDEX ....................................................................................................................................9

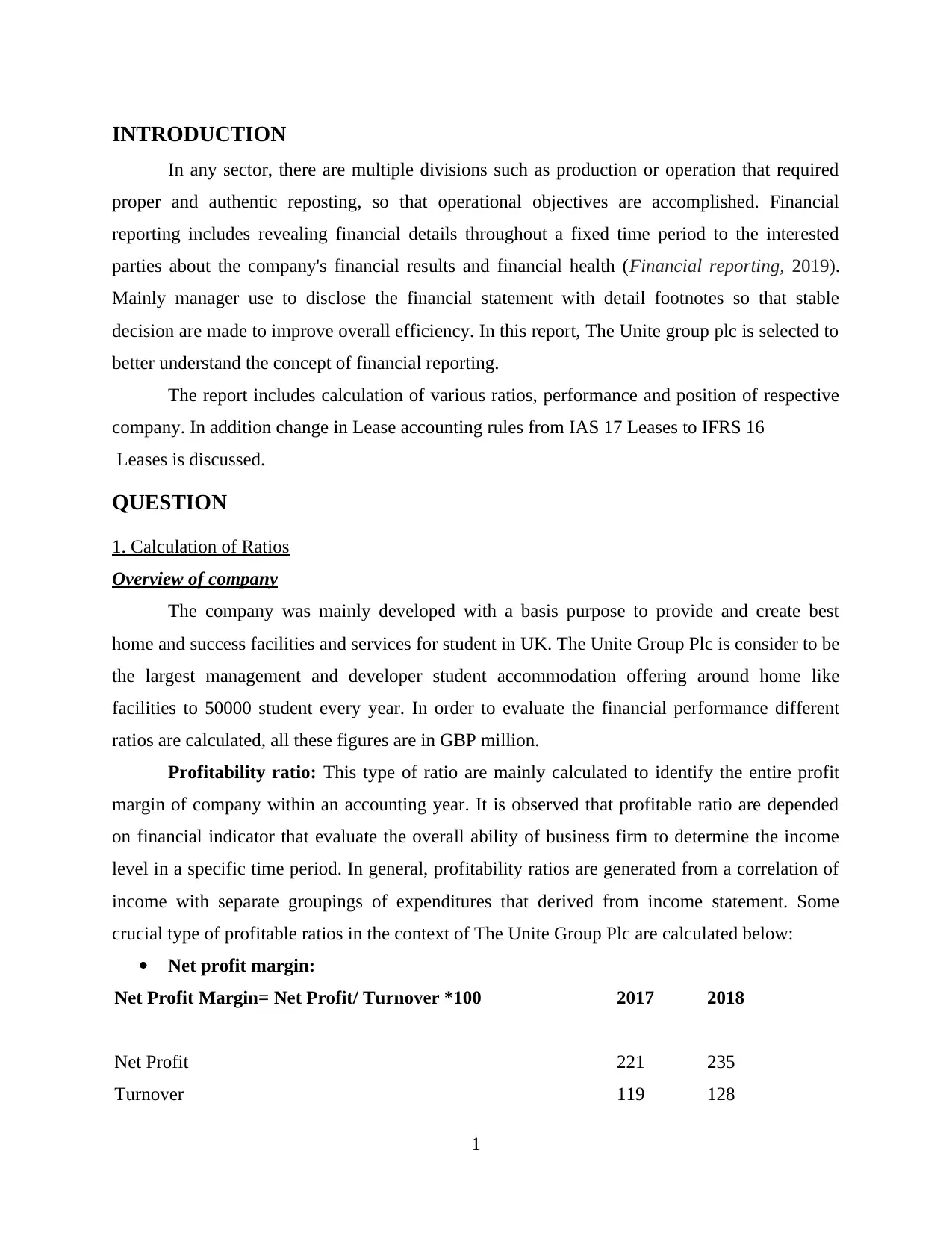

INTRODUCTION

In any sector, there are multiple divisions such as production or operation that required

proper and authentic reposting, so that operational objectives are accomplished. Financial

reporting includes revealing financial details throughout a fixed time period to the interested

parties about the company's financial results and financial health (Financial reporting, 2019).

Mainly manager use to disclose the financial statement with detail footnotes so that stable

decision are made to improve overall efficiency. In this report, The Unite group plc is selected to

better understand the concept of financial reporting.

The report includes calculation of various ratios, performance and position of respective

company. In addition change in Lease accounting rules from IAS 17 Leases to IFRS 16

Leases is discussed.

QUESTION

1. Calculation of Ratios

Overview of company

The company was mainly developed with a basis purpose to provide and create best

home and success facilities and services for student in UK. The Unite Group Plc is consider to be

the largest management and developer student accommodation offering around home like

facilities to 50000 student every year. In order to evaluate the financial performance different

ratios are calculated, all these figures are in GBP million.

Profitability ratio: This type of ratio are mainly calculated to identify the entire profit

margin of company within an accounting year. It is observed that profitable ratio are depended

on financial indicator that evaluate the overall ability of business firm to determine the income

level in a specific time period. In general, profitability ratios are generated from a correlation of

income with separate groupings of expenditures that derived from income statement. Some

crucial type of profitable ratios in the context of The Unite Group Plc are calculated below:

Net profit margin:

Net Profit Margin= Net Profit/ Turnover *100 2017 2018

Net Profit 221 235

Turnover 119 128

1

In any sector, there are multiple divisions such as production or operation that required

proper and authentic reposting, so that operational objectives are accomplished. Financial

reporting includes revealing financial details throughout a fixed time period to the interested

parties about the company's financial results and financial health (Financial reporting, 2019).

Mainly manager use to disclose the financial statement with detail footnotes so that stable

decision are made to improve overall efficiency. In this report, The Unite group plc is selected to

better understand the concept of financial reporting.

The report includes calculation of various ratios, performance and position of respective

company. In addition change in Lease accounting rules from IAS 17 Leases to IFRS 16

Leases is discussed.

QUESTION

1. Calculation of Ratios

Overview of company

The company was mainly developed with a basis purpose to provide and create best

home and success facilities and services for student in UK. The Unite Group Plc is consider to be

the largest management and developer student accommodation offering around home like

facilities to 50000 student every year. In order to evaluate the financial performance different

ratios are calculated, all these figures are in GBP million.

Profitability ratio: This type of ratio are mainly calculated to identify the entire profit

margin of company within an accounting year. It is observed that profitable ratio are depended

on financial indicator that evaluate the overall ability of business firm to determine the income

level in a specific time period. In general, profitability ratios are generated from a correlation of

income with separate groupings of expenditures that derived from income statement. Some

crucial type of profitable ratios in the context of The Unite Group Plc are calculated below:

Net profit margin:

Net Profit Margin= Net Profit/ Turnover *100 2017 2018

Net Profit 221 235

Turnover 119 128

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

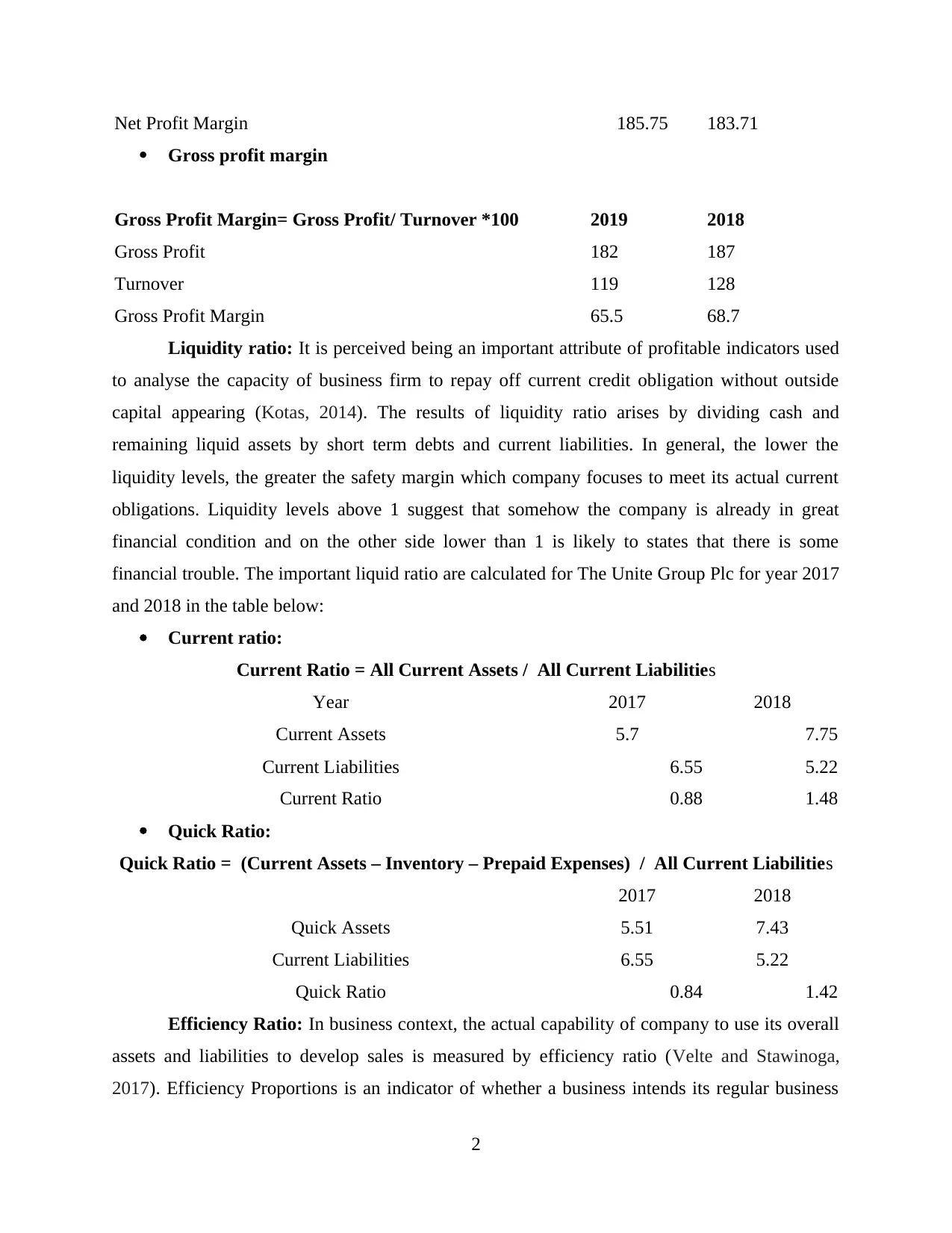

Net Profit Margin 185.75 183.71

Gross profit margin

Gross Profit Margin= Gross Profit/ Turnover *100 2019 2018

Gross Profit 182 187

Turnover 119 128

Gross Profit Margin 65.5 68.7

Liquidity ratio: It is perceived being an important attribute of profitable indicators used

to analyse the capacity of business firm to repay off current credit obligation without outside

capital appearing (Kotas, 2014). The results of liquidity ratio arises by dividing cash and

remaining liquid assets by short term debts and current liabilities. In general, the lower the

liquidity levels, the greater the safety margin which company focuses to meet its actual current

obligations. Liquidity levels above 1 suggest that somehow the company is already in great

financial condition and on the other side lower than 1 is likely to states that there is some

financial trouble. The important liquid ratio are calculated for The Unite Group Plc for year 2017

and 2018 in the table below:

Current ratio:

Current Ratio = All Current Assets / All Current Liabilities

Year 2017 2018

Current Assets 5.7 7.75

Current Liabilities 6.55 5.22

Current Ratio 0.88 1.48

Quick Ratio:

Quick Ratio = (Current Assets – Inventory – Prepaid Expenses) / All Current Liabilities

2017 2018

Quick Assets 5.51 7.43

Current Liabilities 6.55 5.22

Quick Ratio 0.84 1.42

Efficiency Ratio: In business context, the actual capability of company to use its overall

assets and liabilities to develop sales is measured by efficiency ratio (Velte and Stawinoga,

2017). Efficiency Proportions is an indicator of whether a business intends its regular business

2

Gross profit margin

Gross Profit Margin= Gross Profit/ Turnover *100 2019 2018

Gross Profit 182 187

Turnover 119 128

Gross Profit Margin 65.5 68.7

Liquidity ratio: It is perceived being an important attribute of profitable indicators used

to analyse the capacity of business firm to repay off current credit obligation without outside

capital appearing (Kotas, 2014). The results of liquidity ratio arises by dividing cash and

remaining liquid assets by short term debts and current liabilities. In general, the lower the

liquidity levels, the greater the safety margin which company focuses to meet its actual current

obligations. Liquidity levels above 1 suggest that somehow the company is already in great

financial condition and on the other side lower than 1 is likely to states that there is some

financial trouble. The important liquid ratio are calculated for The Unite Group Plc for year 2017

and 2018 in the table below:

Current ratio:

Current Ratio = All Current Assets / All Current Liabilities

Year 2017 2018

Current Assets 5.7 7.75

Current Liabilities 6.55 5.22

Current Ratio 0.88 1.48

Quick Ratio:

Quick Ratio = (Current Assets – Inventory – Prepaid Expenses) / All Current Liabilities

2017 2018

Quick Assets 5.51 7.43

Current Liabilities 6.55 5.22

Quick Ratio 0.84 1.42

Efficiency Ratio: In business context, the actual capability of company to use its overall

assets and liabilities to develop sales is measured by efficiency ratio (Velte and Stawinoga,

2017). Efficiency Proportions is an indicator of whether a business intends its regular business

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

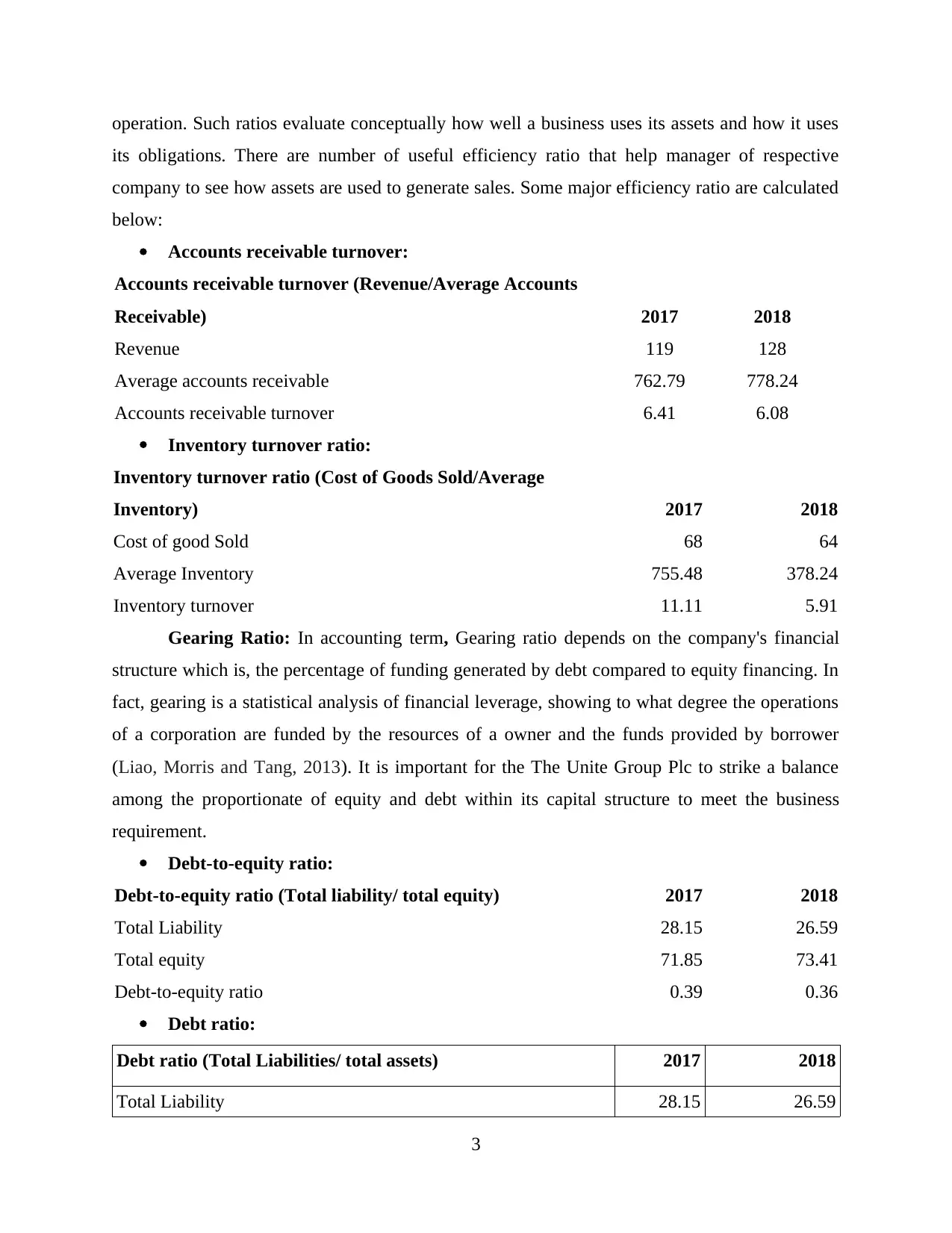

operation. Such ratios evaluate conceptually how well a business uses its assets and how it uses

its obligations. There are number of useful efficiency ratio that help manager of respective

company to see how assets are used to generate sales. Some major efficiency ratio are calculated

below:

Accounts receivable turnover:

Accounts receivable turnover (Revenue/Average Accounts

Receivable) 2017 2018

Revenue 119 128

Average accounts receivable 762.79 778.24

Accounts receivable turnover 6.41 6.08

Inventory turnover ratio:

Inventory turnover ratio (Cost of Goods Sold/Average

Inventory) 2017 2018

Cost of good Sold 68 64

Average Inventory 755.48 378.24

Inventory turnover 11.11 5.91

Gearing Ratio: In accounting term, Gearing ratio depends on the company's financial

structure which is, the percentage of funding generated by debt compared to equity financing. In

fact, gearing is a statistical analysis of financial leverage, showing to what degree the operations

of a corporation are funded by the resources of a owner and the funds provided by borrower

(Liao, Morris and Tang, 2013). It is important for the The Unite Group Plc to strike a balance

among the proportionate of equity and debt within its capital structure to meet the business

requirement.

Debt-to-equity ratio:

Debt-to-equity ratio (Total liability/ total equity) 2017 2018

Total Liability 28.15 26.59

Total equity 71.85 73.41

Debt-to-equity ratio 0.39 0.36

Debt ratio:

Debt ratio (Total Liabilities/ total assets) 2017 2018

Total Liability 28.15 26.59

3

its obligations. There are number of useful efficiency ratio that help manager of respective

company to see how assets are used to generate sales. Some major efficiency ratio are calculated

below:

Accounts receivable turnover:

Accounts receivable turnover (Revenue/Average Accounts

Receivable) 2017 2018

Revenue 119 128

Average accounts receivable 762.79 778.24

Accounts receivable turnover 6.41 6.08

Inventory turnover ratio:

Inventory turnover ratio (Cost of Goods Sold/Average

Inventory) 2017 2018

Cost of good Sold 68 64

Average Inventory 755.48 378.24

Inventory turnover 11.11 5.91

Gearing Ratio: In accounting term, Gearing ratio depends on the company's financial

structure which is, the percentage of funding generated by debt compared to equity financing. In

fact, gearing is a statistical analysis of financial leverage, showing to what degree the operations

of a corporation are funded by the resources of a owner and the funds provided by borrower

(Liao, Morris and Tang, 2013). It is important for the The Unite Group Plc to strike a balance

among the proportionate of equity and debt within its capital structure to meet the business

requirement.

Debt-to-equity ratio:

Debt-to-equity ratio (Total liability/ total equity) 2017 2018

Total Liability 28.15 26.59

Total equity 71.85 73.41

Debt-to-equity ratio 0.39 0.36

Debt ratio:

Debt ratio (Total Liabilities/ total assets) 2017 2018

Total Liability 28.15 26.59

3

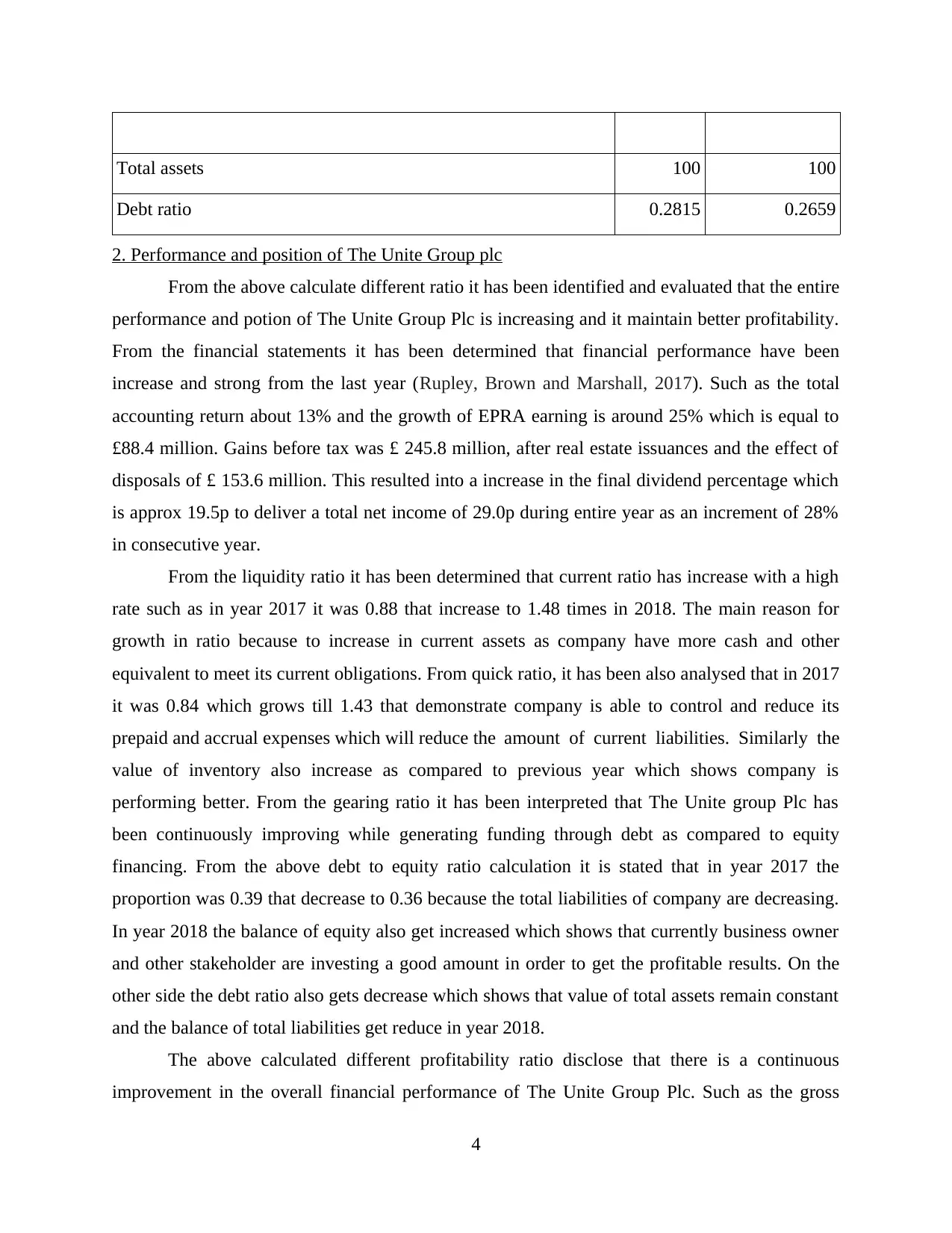

Total assets 100 100

Debt ratio 0.2815 0.2659

2. Performance and position of The Unite Group plc

From the above calculate different ratio it has been identified and evaluated that the entire

performance and potion of The Unite Group Plc is increasing and it maintain better profitability.

From the financial statements it has been determined that financial performance have been

increase and strong from the last year (Rupley, Brown and Marshall, 2017). Such as the total

accounting return about 13% and the growth of EPRA earning is around 25% which is equal to

£88.4 million. Gains before tax was £ 245.8 million, after real estate issuances and the effect of

disposals of £ 153.6 million. This resulted into a increase in the final dividend percentage which

is approx 19.5p to deliver a total net income of 29.0p during entire year as an increment of 28%

in consecutive year.

From the liquidity ratio it has been determined that current ratio has increase with a high

rate such as in year 2017 it was 0.88 that increase to 1.48 times in 2018. The main reason for

growth in ratio because to increase in current assets as company have more cash and other

equivalent to meet its current obligations. From quick ratio, it has been also analysed that in 2017

it was 0.84 which grows till 1.43 that demonstrate company is able to control and reduce its

prepaid and accrual expenses which will reduce the amount of current liabilities. Similarly the

value of inventory also increase as compared to previous year which shows company is

performing better. From the gearing ratio it has been interpreted that The Unite group Plc has

been continuously improving while generating funding through debt as compared to equity

financing. From the above debt to equity ratio calculation it is stated that in year 2017 the

proportion was 0.39 that decrease to 0.36 because the total liabilities of company are decreasing.

In year 2018 the balance of equity also get increased which shows that currently business owner

and other stakeholder are investing a good amount in order to get the profitable results. On the

other side the debt ratio also gets decrease which shows that value of total assets remain constant

and the balance of total liabilities get reduce in year 2018.

The above calculated different profitability ratio disclose that there is a continuous

improvement in the overall financial performance of The Unite Group Plc. Such as the gross

4

Debt ratio 0.2815 0.2659

2. Performance and position of The Unite Group plc

From the above calculate different ratio it has been identified and evaluated that the entire

performance and potion of The Unite Group Plc is increasing and it maintain better profitability.

From the financial statements it has been determined that financial performance have been

increase and strong from the last year (Rupley, Brown and Marshall, 2017). Such as the total

accounting return about 13% and the growth of EPRA earning is around 25% which is equal to

£88.4 million. Gains before tax was £ 245.8 million, after real estate issuances and the effect of

disposals of £ 153.6 million. This resulted into a increase in the final dividend percentage which

is approx 19.5p to deliver a total net income of 29.0p during entire year as an increment of 28%

in consecutive year.

From the liquidity ratio it has been determined that current ratio has increase with a high

rate such as in year 2017 it was 0.88 that increase to 1.48 times in 2018. The main reason for

growth in ratio because to increase in current assets as company have more cash and other

equivalent to meet its current obligations. From quick ratio, it has been also analysed that in 2017

it was 0.84 which grows till 1.43 that demonstrate company is able to control and reduce its

prepaid and accrual expenses which will reduce the amount of current liabilities. Similarly the

value of inventory also increase as compared to previous year which shows company is

performing better. From the gearing ratio it has been interpreted that The Unite group Plc has

been continuously improving while generating funding through debt as compared to equity

financing. From the above debt to equity ratio calculation it is stated that in year 2017 the

proportion was 0.39 that decrease to 0.36 because the total liabilities of company are decreasing.

In year 2018 the balance of equity also get increased which shows that currently business owner

and other stakeholder are investing a good amount in order to get the profitable results. On the

other side the debt ratio also gets decrease which shows that value of total assets remain constant

and the balance of total liabilities get reduce in year 2018.

The above calculated different profitability ratio disclose that there is a continuous

improvement in the overall financial performance of The Unite Group Plc. Such as the gross

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profit ratio in year 2017 was 65.5 which increase to 68.7 in next year. The main reasons for

improvement in profit is that company has develop different ways to provide best and best

services to Student in UK that increase overall profit. Management has also worked to reduce the

expenses and any other promotional additional cost by focusing on digital promotion. On the

other side it has been also determined that net profit have slightly decrease in year 2018 as

compared to 2017 which was 185.75%. There can be different reason for the decrease in net

profit margin can be increase in total expenses or reduction in sales for the year. From the

efficiency ratio it has been determined that company is capable to generate funds from its total

assets.

From the financial statements it has been determined that total revenue of The Unite

Group Plc has also increased in year 2018 as it is £m128.7 which was £m 119.3 in 2017 because

rent amount increased by company in year. Profit before tax in year 2018 is £m245.8 which

increase because company has reduce its cost of good sold and financial costs. The total profit of

the year in year 2017 was £m 223.8 which increase to £m237.3 in year 2018 as Net financing

costs and Share of joint venture profit. The consolidated balance sheet shows that overall

performance of The Unite Group Plc has increased such as in year 2017 the total assets was £m

2431.6 which grows to £m2849.5. The main reason of increase in volume of assets is growth in

investment property, joint venture investment, growth in inventories, increase in cash and cash

equivalent. On the other side, the total liabilities in year 2017 was £m (677.4) that reduces to

(750.7) in year 2018 that shows that company have reduces the borrowing current tax liability

also reduce and interest rate swaps which shows company financial performance is good.

3. Analyse the change in Lease accounting rules

In accounting term, lease is defined as a transaction in which an legal agreements is

singed by lessee with lessor in order to use or take the assets of lessor for which lessee make an

equivalent payment or a set of payment within specific time period.

According to IAS 17, leases demonstrate the accounting disclosure and policies that are

relevant to leases for both parties lessor and lessees. In 2003 it was reissued again and implies to

the entire year starting after 1st January 2005 (IAS 17, 2019.). The main objective of the

accounting standard is to provide suitable and authentic policies that are applied to finance and

operation lease. The finance lease are those which includes all kind of rewards and risk that are

being transferred to owner of particular assets but not the title. On the other side operating leases

5

improvement in profit is that company has develop different ways to provide best and best

services to Student in UK that increase overall profit. Management has also worked to reduce the

expenses and any other promotional additional cost by focusing on digital promotion. On the

other side it has been also determined that net profit have slightly decrease in year 2018 as

compared to 2017 which was 185.75%. There can be different reason for the decrease in net

profit margin can be increase in total expenses or reduction in sales for the year. From the

efficiency ratio it has been determined that company is capable to generate funds from its total

assets.

From the financial statements it has been determined that total revenue of The Unite

Group Plc has also increased in year 2018 as it is £m128.7 which was £m 119.3 in 2017 because

rent amount increased by company in year. Profit before tax in year 2018 is £m245.8 which

increase because company has reduce its cost of good sold and financial costs. The total profit of

the year in year 2017 was £m 223.8 which increase to £m237.3 in year 2018 as Net financing

costs and Share of joint venture profit. The consolidated balance sheet shows that overall

performance of The Unite Group Plc has increased such as in year 2017 the total assets was £m

2431.6 which grows to £m2849.5. The main reason of increase in volume of assets is growth in

investment property, joint venture investment, growth in inventories, increase in cash and cash

equivalent. On the other side, the total liabilities in year 2017 was £m (677.4) that reduces to

(750.7) in year 2018 that shows that company have reduces the borrowing current tax liability

also reduce and interest rate swaps which shows company financial performance is good.

3. Analyse the change in Lease accounting rules

In accounting term, lease is defined as a transaction in which an legal agreements is

singed by lessee with lessor in order to use or take the assets of lessor for which lessee make an

equivalent payment or a set of payment within specific time period.

According to IAS 17, leases demonstrate the accounting disclosure and policies that are

relevant to leases for both parties lessor and lessees. In 2003 it was reissued again and implies to

the entire year starting after 1st January 2005 (IAS 17, 2019.). The main objective of the

accounting standard is to provide suitable and authentic policies that are applied to finance and

operation lease. The finance lease are those which includes all kind of rewards and risk that are

being transferred to owner of particular assets but not the title. On the other side operating leases

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are those in which outcome in expense is recognised by the lessee in the context of the assets

remaining identified by the lessor. In company The Unite Group Plc there are some cases that

would lead to classify a lease into finance lease which includes:

The tenant has the option of buying the property at a rate that is supposed to be

substantially less than the market value at the day upon which choice is exercisable that it

is fairly certain that the option will be exercised at the end of the lease.

At the time of inception of lease the fair value of the marginal lease payment sum is least

substantially entire market value of the leased assets.

Profit and losses arising in variations throughout the fair market value of the remaining

rent to the lessee.

As per the accounting standard of IAS 17 there are different ways of accounting for both

lessees and lessors which are included within the annual financial statements of respective

company. These are discussed below:

Accounting by lessees

Monetary contracts must be registered as assets and liabilities at the lesser market value

of the assets as well as the current value of the fixed rental payments at the end of the

term of the lease (Mio, 2016).

The depreciation valuation strategy must be compatible with those of owned property of

assets held within financial leases. When there is no sensible assurance that perhaps the

lessee will acquire possession when lease end. Then all those asset are needed to be

depreciated over less time period or as per the existence of such asset.

Accounting by lessors:

The tenant must consider financial income on the basis of a trend representing a

continuous regular profit on the financial rent net profit of the lessor.

In the context of operating lease the assets hold must be shown on the balance sheet of

the lessor as per the nature of assets. Contract profits must be treated according to

straight-line framework throughout the term of the lease.

According to IFRS 16, a single tenant accounting framework that require lessees to

identify each assets and liabilities that are for leases in which underlying assets have a lower

value. IFRS 16 lays down guidelines for the identification, assessment, reporting and recording

of rentals, with the goal of maintaining that leaseholders and leasing companies have important

6

remaining identified by the lessor. In company The Unite Group Plc there are some cases that

would lead to classify a lease into finance lease which includes:

The tenant has the option of buying the property at a rate that is supposed to be

substantially less than the market value at the day upon which choice is exercisable that it

is fairly certain that the option will be exercised at the end of the lease.

At the time of inception of lease the fair value of the marginal lease payment sum is least

substantially entire market value of the leased assets.

Profit and losses arising in variations throughout the fair market value of the remaining

rent to the lessee.

As per the accounting standard of IAS 17 there are different ways of accounting for both

lessees and lessors which are included within the annual financial statements of respective

company. These are discussed below:

Accounting by lessees

Monetary contracts must be registered as assets and liabilities at the lesser market value

of the assets as well as the current value of the fixed rental payments at the end of the

term of the lease (Mio, 2016).

The depreciation valuation strategy must be compatible with those of owned property of

assets held within financial leases. When there is no sensible assurance that perhaps the

lessee will acquire possession when lease end. Then all those asset are needed to be

depreciated over less time period or as per the existence of such asset.

Accounting by lessors:

The tenant must consider financial income on the basis of a trend representing a

continuous regular profit on the financial rent net profit of the lessor.

In the context of operating lease the assets hold must be shown on the balance sheet of

the lessor as per the nature of assets. Contract profits must be treated according to

straight-line framework throughout the term of the lease.

According to IFRS 16, a single tenant accounting framework that require lessees to

identify each assets and liabilities that are for leases in which underlying assets have a lower

value. IFRS 16 lays down guidelines for the identification, assessment, reporting and recording

of rentals, with the goal of maintaining that leaseholders and leasing companies have important

6

information that accurately reflects these transactions (IFRS 16, 2019). In a similar financial

setting, the rate of interest a lessee will have to charge to invest over a comparable period,

though with a similar protection, the resources needed to purchase a property of equivalent value

to the correct-of-use asset. It is also stated that a lessee can select the account for lease payment

that is an expenses according to straight-line method across the lease term. There are mainly two

kind of leases such as:

Contracts with such a term of the lease for around 12 months or lower and without

leasing rights in which decision is taken by asset class.

Leases in which the underlying assets have a reduced value when new value is

determined.

There are separate ways of accounting for lessees and lessors as per the IFRS 16 in order

to record the finance and operating lease that much be included with financial statements. These

are discussed below:

Accounting by lessees:

The correct use of an assets is regarded as an investment property in which lessee counts

its fair value under the section IAS 40.

Originally, the correct-of-use property is assessed at the value of the rent obligation

including the additional actual costs that the tenant sustained. Modifications could also be

needed for rent rewards, compensation at or before start-up and reconstruction

responsibilities (Mukhlisin, Hudaib and Azid, 2015).

Accounting by lessors:

In the term of lease the financial life of an assets is defined but the title is not given to the

lessees.

The tenant shall have the opportunity to buy the property at a rate that is estimated to be

substantially lower than the book value at the period upon which right is exercisable it is

fairly certain at the beginning of the contract that the option would be executed

(Mullinova and Simonyants, 2016).

CONCLUSION

In the end of this report financial reporting is a systematic process of developing essential

financial statements so that decision are made by external and internal interested parties. These

statements are beneficial in to calculate the different ratio so that overall performance and

7

setting, the rate of interest a lessee will have to charge to invest over a comparable period,

though with a similar protection, the resources needed to purchase a property of equivalent value

to the correct-of-use asset. It is also stated that a lessee can select the account for lease payment

that is an expenses according to straight-line method across the lease term. There are mainly two

kind of leases such as:

Contracts with such a term of the lease for around 12 months or lower and without

leasing rights in which decision is taken by asset class.

Leases in which the underlying assets have a reduced value when new value is

determined.

There are separate ways of accounting for lessees and lessors as per the IFRS 16 in order

to record the finance and operating lease that much be included with financial statements. These

are discussed below:

Accounting by lessees:

The correct use of an assets is regarded as an investment property in which lessee counts

its fair value under the section IAS 40.

Originally, the correct-of-use property is assessed at the value of the rent obligation

including the additional actual costs that the tenant sustained. Modifications could also be

needed for rent rewards, compensation at or before start-up and reconstruction

responsibilities (Mukhlisin, Hudaib and Azid, 2015).

Accounting by lessors:

In the term of lease the financial life of an assets is defined but the title is not given to the

lessees.

The tenant shall have the opportunity to buy the property at a rate that is estimated to be

substantially lower than the book value at the period upon which right is exercisable it is

fairly certain at the beginning of the contract that the option would be executed

(Mullinova and Simonyants, 2016).

CONCLUSION

In the end of this report financial reporting is a systematic process of developing essential

financial statements so that decision are made by external and internal interested parties. These

statements are beneficial in to calculate the different ratio so that overall performance and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profitability can be determined within an accounting year. In case if a systemic framework ion

term of lease is more reflective upon the time period where the rented asset's usage profit is

decreased. It is observed that leases are mainly classified on the basis of substances of the

dealing instead of the form.

8

term of lease is more reflective upon the time period where the rented asset's usage profit is

decreased. It is observed that leases are mainly classified on the basis of substances of the

dealing instead of the form.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Liao, L., Morris, R .D. and Tang, Q., 2013. Information asymmetry of fair value accounting

during the financial crisis. Journal of Contemporary Accounting & Economics. 9(2).

pp.221-236.

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Mukhlisin, M., Hudaib, M. and Azid, T., 2015. The need for Shariah harmonization in financial

reporting standardization: The case of Indonesia. International Journal of Islamic and

Middle Eastern Finance and Management. 8(4). pp.455-471.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches,

(1), pp.83-88.

Rupley, K. H., Brown, D. and Marshall, S., 2017. Evolution of corporate reporting: From stand-

alone corporate social responsibility reporting to integrated reporting. Research in

accounting regulation. 29(2). pp.172-176.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of empirical research,

limitations and future research implications. Journal of Management Control. 28(3).

pp.275-320.

Online

Financial reporting. 2019. [Online] Available Through:

<https://www.edupristine.com/blog/financial-reporting>.

IAS 17. 2019. [Online] Available Through:

<https://www.iasplus.com/en/standards/ias/ias17>.

IFRS 16. 2019. [Online] Available Through:

<https://www.iasplus.com/en/standards/ifrs/ifrs-16>.

9

Books and Journals:

Kotas, R., 2014. Management accounting for hotels and restaurants. Routledge.

Liao, L., Morris, R .D. and Tang, Q., 2013. Information asymmetry of fair value accounting

during the financial crisis. Journal of Contemporary Accounting & Economics. 9(2).

pp.221-236.

Mio, C. ed., 2016. Integrated reporting: A new accounting disclosure. Springer.

Mukhlisin, M., Hudaib, M. and Azid, T., 2015. The need for Shariah harmonization in financial

reporting standardization: The case of Indonesia. International Journal of Islamic and

Middle Eastern Finance and Management. 8(4). pp.455-471.

Mullinova, S. and Simonyants, N., 2016. Reflection of a deferred tax liability in the credit union

reporting according to IFRS (IAS) 12" Income taxes". Modern European Researches,

(1), pp.83-88.

Rupley, K. H., Brown, D. and Marshall, S., 2017. Evolution of corporate reporting: From stand-

alone corporate social responsibility reporting to integrated reporting. Research in

accounting regulation. 29(2). pp.172-176.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of empirical research,

limitations and future research implications. Journal of Management Control. 28(3).

pp.275-320.

Online

Financial reporting. 2019. [Online] Available Through:

<https://www.edupristine.com/blog/financial-reporting>.

IAS 17. 2019. [Online] Available Through:

<https://www.iasplus.com/en/standards/ias/ias17>.

IFRS 16. 2019. [Online] Available Through:

<https://www.iasplus.com/en/standards/ifrs/ifrs-16>.

9

APPENDEX

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.