McPherson Ltd Financial Report: Analysis, Valuation & Strategies

VerifiedAdded on 2023/04/20

|11

|1928

|208

Report

AI Summary

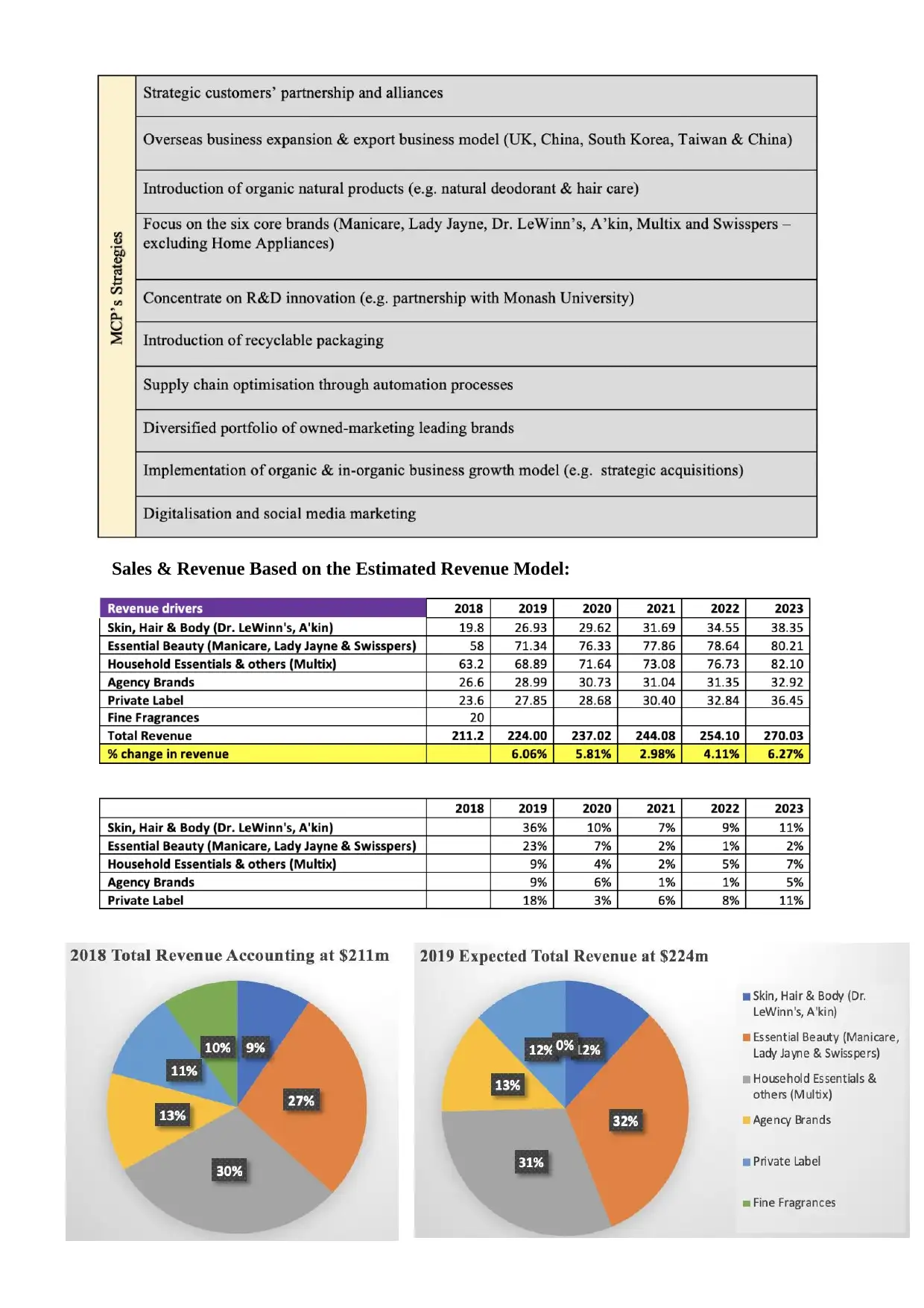

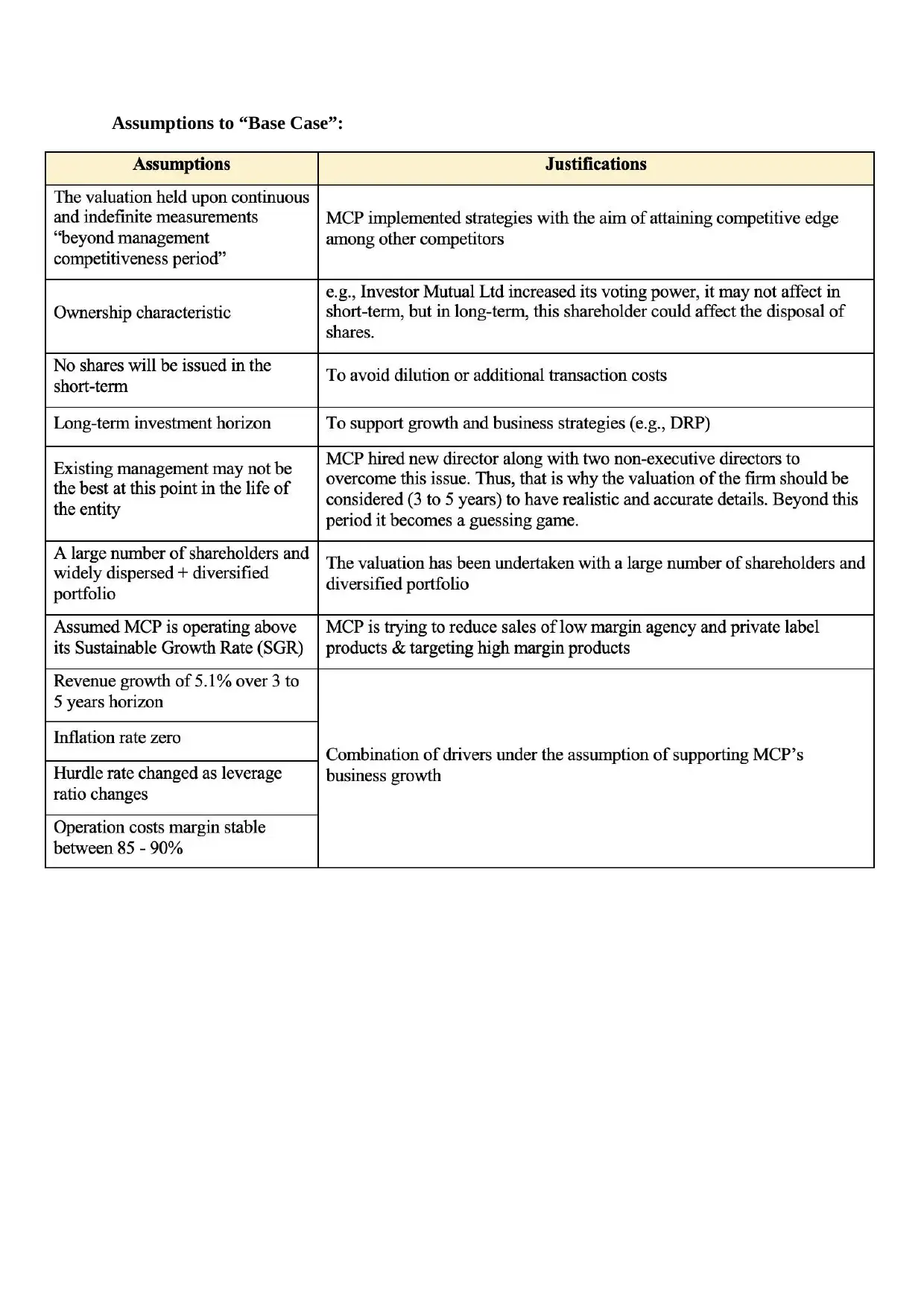

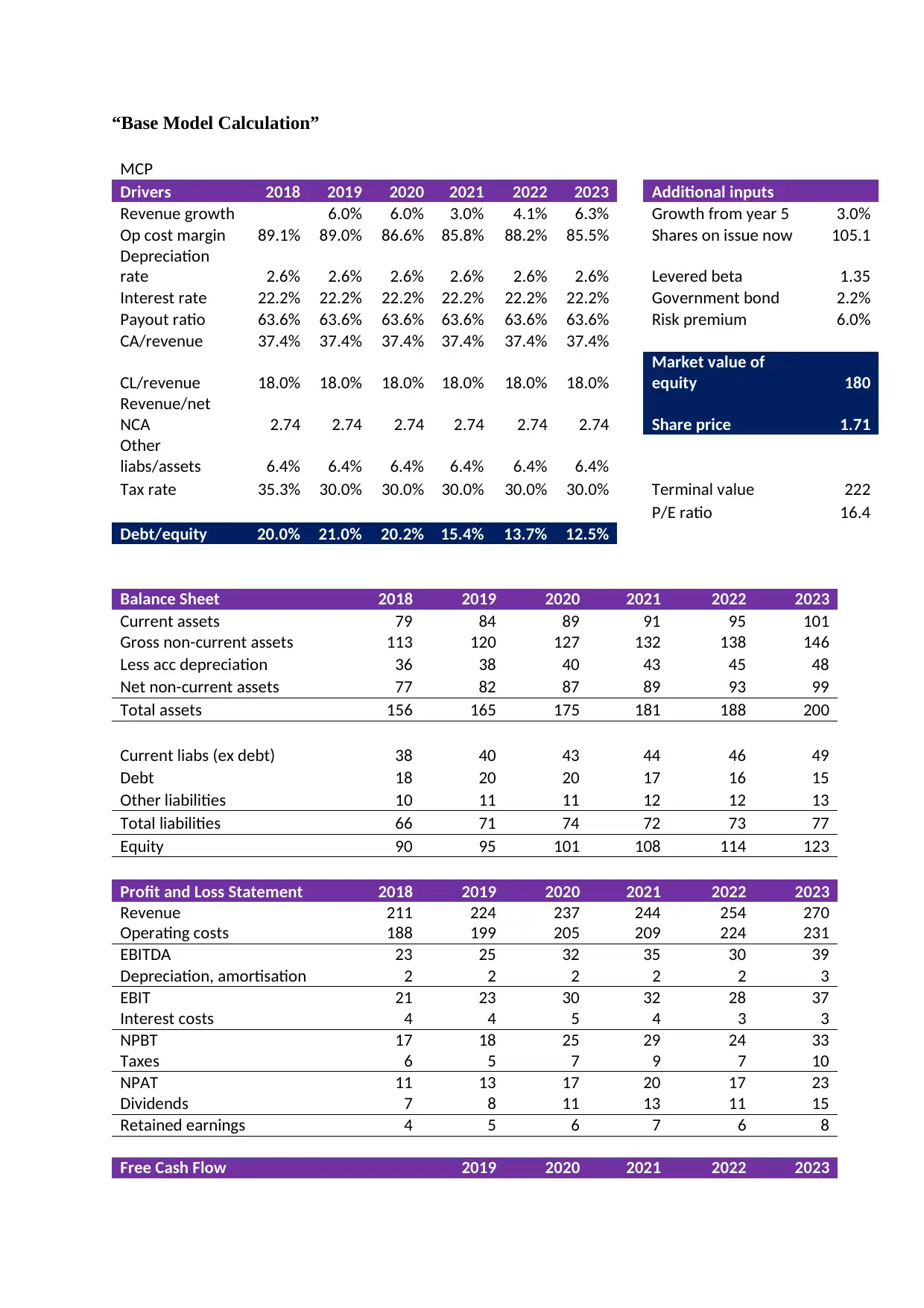

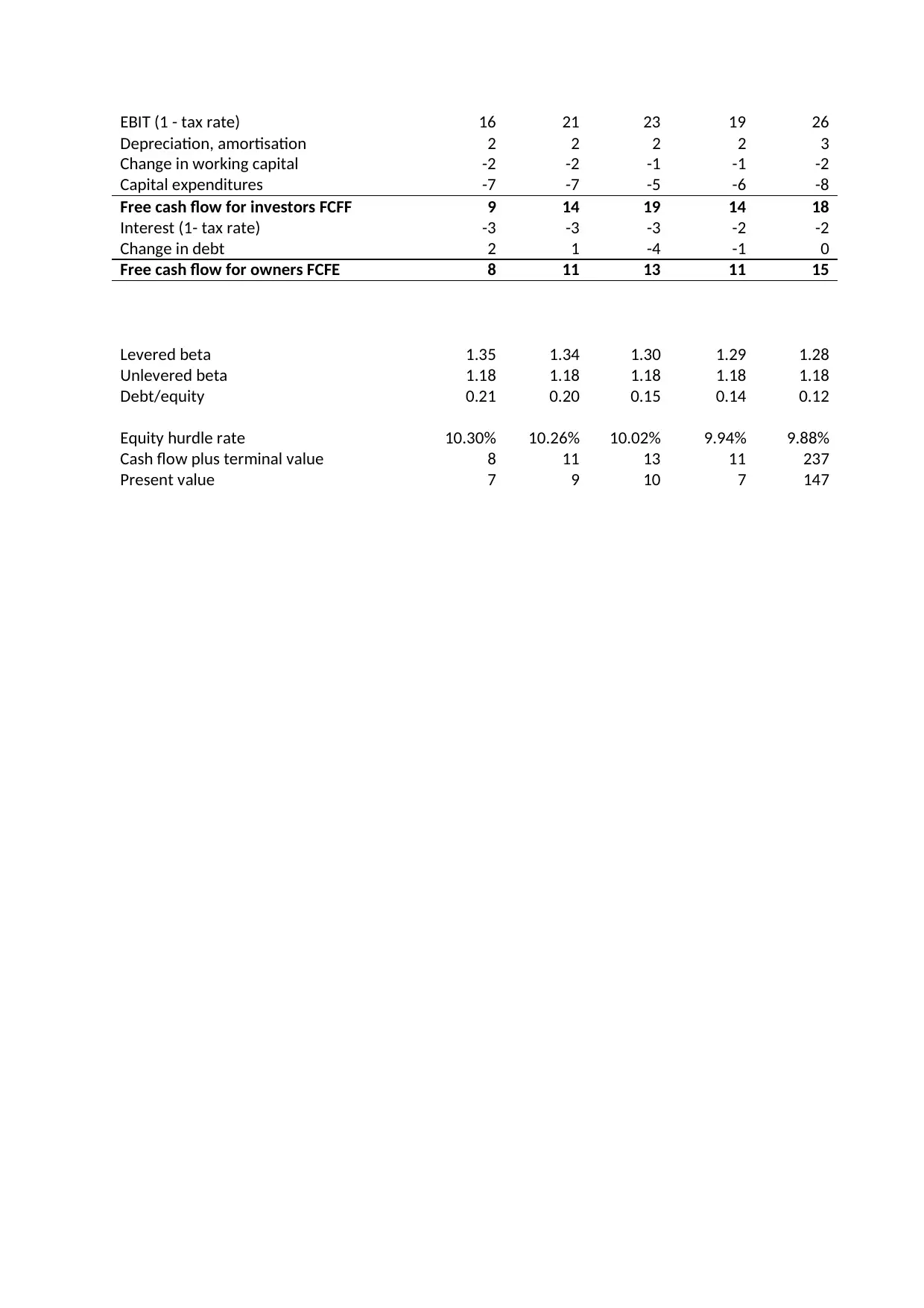

This report provides a financial analysis and valuation of McPherson Ltd (MCP), an Australian Stock Exchange-listed company involved in the marketing and distribution of health and beauty products. The analysis focuses on a 'base case' scenario, examining the company's business strategies, sales revenue based on estimated models, and recent market communications. Key strategies include focusing on core brand performance and increasing global revenue. The report assesses the company's financial health, noting its undervalued share price compared to estimated value, along with concerns about debt and acquisitions. It also considers the impact of new directors and shareholder interest changes. The analysis includes forecasted balance sheets and profit and loss statements, concluding that McPherson's Limited is well-positioned for future growth despite current financial questions. The company will manage to recover and reduce its debt to equity ratio in 2021.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.