Comprehensive Financial Analysis Report: Vivo Energy Mauritius Limited

VerifiedAdded on 2021/03/08

|34

|7457

|120

Report

AI Summary

This report presents a comprehensive financial analysis of Vivo Energy Mauritius Limited (VEML). It begins with an introduction to the company, its functional areas, and strategic integration. The core of the report involves a detailed examination of VEML's financial statements for 2018-2019, including a thorough analysis of the profit and loss statement, balance sheet, and key financial ratios such as current ratio, quick ratio, gearing ratio, return on capital employed, interest cover ratio, and net profit margin ratio. The report further delves into the budgeting process, evaluating various budgeting methods and the impact of technology. Additionally, the report explores organizational performance management, discussing performance measurement tools. Finally, it addresses capital budgeting decisions, evaluating sources of finance and investment appraisal techniques, including both discounted and non-discounted methods. The report concludes with a comprehensive reference section.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Anwar RADIM

Anwar RADIM

Anwar RADIM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Your assignment should meet the following requirements.

Please confirm this by ticking the boxes before submitting your assignment

I have filled the student information columns.

The contents of my assignment have been submitted to Turnitin and I have attached

Turnitin report screenshot in the last page.

I have strictly followed Harvard Referencing Style and Citations.

TO BE FILLED BY THE FACULTY

Faculty Name Mr. Shahid Wani

Contact No.

Email ID shahid@ebsedu.org

TO BE FILLED BY THE SUTDENT

Student Name Anwar RADIM

Student ID ONL2101012A01

Email ID radim.anwar@gmail.com

Turinitin Class ID 19578115

Turnitin Enrollment key CIQGM700

Course Master in Business Administration

Date Submitted 09/01/2021

ASSIGNMENT INFORMATION

Full/ Part Assignment Full

Date Assignment Issued 13/12/2020

Date Assignment Due 12/1/2021

Assignment IV by Dr. Vivek Mohan

TO BE FILLED BY THE ASSESSOR

Assessment types Marks Marks

Awarded

Understanding the concepts of financial analysis,

interpretation, and tools of financial decision making

40

Understanding Budgeting process and evaluating

organisational performance and tools

30

Understanding and evaluating the procurement and

utilization of funds

30

Overall Marks 100

Overall Grade

Please confirm this by ticking the boxes before submitting your assignment

I have filled the student information columns.

The contents of my assignment have been submitted to Turnitin and I have attached

Turnitin report screenshot in the last page.

I have strictly followed Harvard Referencing Style and Citations.

TO BE FILLED BY THE FACULTY

Faculty Name Mr. Shahid Wani

Contact No.

Email ID shahid@ebsedu.org

TO BE FILLED BY THE SUTDENT

Student Name Anwar RADIM

Student ID ONL2101012A01

Email ID radim.anwar@gmail.com

Turinitin Class ID 19578115

Turnitin Enrollment key CIQGM700

Course Master in Business Administration

Date Submitted 09/01/2021

ASSIGNMENT INFORMATION

Full/ Part Assignment Full

Date Assignment Issued 13/12/2020

Date Assignment Due 12/1/2021

Assignment IV by Dr. Vivek Mohan

TO BE FILLED BY THE ASSESSOR

Assessment types Marks Marks

Awarded

Understanding the concepts of financial analysis,

interpretation, and tools of financial decision making

40

Understanding Budgeting process and evaluating

organisational performance and tools

30

Understanding and evaluating the procurement and

utilization of funds

30

Overall Marks 100

Overall Grade

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Faculty Name

Summative Feedback by Faculty for further improvement

Assessment Brief/Task

The detailed requirements for this task are as follows:

Scenario:

You are to select a PLC that has a listing on any recognized stock exchange of your choice and agree

this with the module tutor. Once this is done, you are required to answer the following questions:

Assignment Task 1 (40 Marks):

1. Provide a brief introduction of your chosen organisation. 5 Marks

2. Critically examine the importance of various functional areas within organisations, emphasizing

Summative Feedback by Faculty for further improvement

Assessment Brief/Task

The detailed requirements for this task are as follows:

Scenario:

You are to select a PLC that has a listing on any recognized stock exchange of your choice and agree

this with the module tutor. Once this is done, you are required to answer the following questions:

Assignment Task 1 (40 Marks):

1. Provide a brief introduction of your chosen organisation. 5 Marks

2. Critically examine the importance of various functional areas within organisations, emphasizing

the significance of Finance as a critical functional area within your chosen organisation and

how a strategic integration can be achieved? 10 Marks

3. You are required to look into the financial statements of your chosen organisation for the year

2018-19 and explain the following: 25 Marks

a. Analyze and interpret the profit and loss statement, identify the major expenses &

incomes, compare with previous year, & recommend actions for the upcoming year.

You are also required to compare and interpret the P&L statement in the light of cash

flow statement.

b. Analyze the Balance sheet and critically discuss the financial position of your chosen

organisation and recommend future actions.

c. Explain, Calculate and interpret the following ratios for your chosen organisation for the

years 2018 and 2019:

Current ratio

Quick ratio

Gearing ratio

Return on capital employed

Interest cover ratio

Net profit margin ratio.

Assignment Task 2 (30 marks):

1. Explain the process and significance of budgeting process. Critically evaluate various methods

of budgeting and how they differ from each other? As a Finance Manager, which budgeting

approach would you employ and why? You are also required to examine the impact of

technology on the budgeting process and see how technology can be best used in the process to

enhance and speed up the budgeting process? 15 Marks

2. Explain why it is important for organisations to measure their performance. Discuss the

different types of performance management tools and techniques which can be deployed in

how a strategic integration can be achieved? 10 Marks

3. You are required to look into the financial statements of your chosen organisation for the year

2018-19 and explain the following: 25 Marks

a. Analyze and interpret the profit and loss statement, identify the major expenses &

incomes, compare with previous year, & recommend actions for the upcoming year.

You are also required to compare and interpret the P&L statement in the light of cash

flow statement.

b. Analyze the Balance sheet and critically discuss the financial position of your chosen

organisation and recommend future actions.

c. Explain, Calculate and interpret the following ratios for your chosen organisation for the

years 2018 and 2019:

Current ratio

Quick ratio

Gearing ratio

Return on capital employed

Interest cover ratio

Net profit margin ratio.

Assignment Task 2 (30 marks):

1. Explain the process and significance of budgeting process. Critically evaluate various methods

of budgeting and how they differ from each other? As a Finance Manager, which budgeting

approach would you employ and why? You are also required to examine the impact of

technology on the budgeting process and see how technology can be best used in the process to

enhance and speed up the budgeting process? 15 Marks

2. Explain why it is important for organisations to measure their performance. Discuss the

different types of performance management tools and techniques which can be deployed in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

large global companies for evaluating its suitability across a range of business and economic

environments. 15 Marks

Assignment Task 3 (30 marks):

1. Acquisition and utilization of funds are two of the major decisions taken by an organisation

which requires careful analysis. You are required to explain and evaluate various sources of

finance available to a business. Once this is done, you must examine and justify 15% Net Asset

Investment decision taken by your chosen organisation in order to upgrade the technology.

Which sources of finance do you believe would be appropriate for your chosen organisation

and why? 15 marks

2. Considering your organisation’s plans of making capital investments which is the need of the

hour as the organisation is facing a tough competition, the board of directors have approached

you for your expertise in regards to making a capital decision. You must critically evaluate the

investment appraisal techniques you would employ to help your organisation to reach a

decision. You are also required to explain the time value of money and hence compare and

contrast the discounted and non-discounted capital budgeting techniques. 15 Marks

Word count: Approx. 5500 words

Contents

1 TASK 1: Vivo Energy Mauritius Limited Financial Analysis...........................................9

1.1 Introduction.................................................................................................................9

1.2 Functional Areas........................................................................................................10

1.3 Financial Statement Analysis....................................................................................11

1.3.1 Profit and Loss Statement Analysis...................................................................11

1.3.2 Balance Sheet Statement Analysis.....................................................................13

1.3.3 Ratio Analysis....................................................................................................15

2 TASK 2: Budgeting and Organisational Performance Management...............................17

environments. 15 Marks

Assignment Task 3 (30 marks):

1. Acquisition and utilization of funds are two of the major decisions taken by an organisation

which requires careful analysis. You are required to explain and evaluate various sources of

finance available to a business. Once this is done, you must examine and justify 15% Net Asset

Investment decision taken by your chosen organisation in order to upgrade the technology.

Which sources of finance do you believe would be appropriate for your chosen organisation

and why? 15 marks

2. Considering your organisation’s plans of making capital investments which is the need of the

hour as the organisation is facing a tough competition, the board of directors have approached

you for your expertise in regards to making a capital decision. You must critically evaluate the

investment appraisal techniques you would employ to help your organisation to reach a

decision. You are also required to explain the time value of money and hence compare and

contrast the discounted and non-discounted capital budgeting techniques. 15 Marks

Word count: Approx. 5500 words

Contents

1 TASK 1: Vivo Energy Mauritius Limited Financial Analysis...........................................9

1.1 Introduction.................................................................................................................9

1.2 Functional Areas........................................................................................................10

1.3 Financial Statement Analysis....................................................................................11

1.3.1 Profit and Loss Statement Analysis...................................................................11

1.3.2 Balance Sheet Statement Analysis.....................................................................13

1.3.3 Ratio Analysis....................................................................................................15

2 TASK 2: Budgeting and Organisational Performance Management...............................17

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.1 Budgeting..................................................................................................................17

2.1.1 Budgeting Process..............................................................................................17

2.1.2 Significance of Budgeting..................................................................................18

2.1.3 Methods of Budgeting........................................................................................19

2.1.4 Impact of Technology on Budgeting..................................................................20

2.2 Performance Management.........................................................................................21

3 TASK 3: Capital Budgeting.............................................................................................24

3.1 Question 1: Source of finance...................................................................................24

3.1.1 Equity finance....................................................................................................24

3.1.2 Debt Finance......................................................................................................25

3.1.3 VEML Investment..............................................................................................26

3.2 Question 2: Investment Appraisal Techniques..........................................................26

3.2.1 Non-Discounted Techniques..............................................................................27

3.2.2 Discounted Techniques......................................................................................28

4 References........................................................................................................................30

5 Appendix..........................................................................................................................32

2.1.1 Budgeting Process..............................................................................................17

2.1.2 Significance of Budgeting..................................................................................18

2.1.3 Methods of Budgeting........................................................................................19

2.1.4 Impact of Technology on Budgeting..................................................................20

2.2 Performance Management.........................................................................................21

3 TASK 3: Capital Budgeting.............................................................................................24

3.1 Question 1: Source of finance...................................................................................24

3.1.1 Equity finance....................................................................................................24

3.1.2 Debt Finance......................................................................................................25

3.1.3 VEML Investment..............................................................................................26

3.2 Question 2: Investment Appraisal Techniques..........................................................26

3.2.1 Non-Discounted Techniques..............................................................................27

3.2.2 Discounted Techniques......................................................................................28

4 References........................................................................................................................30

5 Appendix..........................................................................................................................32

1 TASK 1: Vivo Energy Mauritius Limited Financial Analysis

1.1 Introduction

Vivo Energy Mauritius Limited (VEML) is a public limited company established in 2011.

The company acquired all shell’s operations within the country and is currently responsible

for the distribution and marketing of shell-related products to commercial customers and

retailers within Mauritius (Vivo Energy Mauritius n.d). VEML is part of the Vivo energy

group which is distributed and markets shell-related products across the African continent.

The company’s products are classified into two major category namely retail and

commercial offers. Retail products include shell fuels, lubricants, LPG, and card services.

Under the shell fuel category, the company supplies Shell fuel save diesel and unleaded fuel.

The lubricants supplied by VEML include Shell Helix, Shell Advance, and Shell Rimula. The

third product supplied by the company is liquified petroleum gas (LPG) under the brand

name shell gas. Last but not least, the company provides its customers with various card

services (Vivo Energy Mauritius n.d). The card services option offered by VEML includes

visa card, fleetman card, and Shell card.

Also, the company offers various commercial products. Products supplied to

commercial customers include Shell diesel, Shell oil, shell Rimula, Shell Gadus, Shell Tellus,

and Shell gas. Vivo Energy Mauritius Limited has only been in operation for 8 years and as

of 31st December 2019, the company had 119 employees. The total number of service stations

within the country amounted to 49 in 2019. The company had 49,923 metric tonnes of fuel

and 4,175 metric tonnes of LPG storage (Vivo Energy Mauritius Limited 2020).

1.1 Introduction

Vivo Energy Mauritius Limited (VEML) is a public limited company established in 2011.

The company acquired all shell’s operations within the country and is currently responsible

for the distribution and marketing of shell-related products to commercial customers and

retailers within Mauritius (Vivo Energy Mauritius n.d). VEML is part of the Vivo energy

group which is distributed and markets shell-related products across the African continent.

The company’s products are classified into two major category namely retail and

commercial offers. Retail products include shell fuels, lubricants, LPG, and card services.

Under the shell fuel category, the company supplies Shell fuel save diesel and unleaded fuel.

The lubricants supplied by VEML include Shell Helix, Shell Advance, and Shell Rimula. The

third product supplied by the company is liquified petroleum gas (LPG) under the brand

name shell gas. Last but not least, the company provides its customers with various card

services (Vivo Energy Mauritius n.d). The card services option offered by VEML includes

visa card, fleetman card, and Shell card.

Also, the company offers various commercial products. Products supplied to

commercial customers include Shell diesel, Shell oil, shell Rimula, Shell Gadus, Shell Tellus,

and Shell gas. Vivo Energy Mauritius Limited has only been in operation for 8 years and as

of 31st December 2019, the company had 119 employees. The total number of service stations

within the country amounted to 49 in 2019. The company had 49,923 metric tonnes of fuel

and 4,175 metric tonnes of LPG storage (Vivo Energy Mauritius Limited 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Functional Areas

There are various functional areas within any organisation. The number and size of these

areas vary across organisations with the most common functional areas being Finance,

operations, marketing, and human resource. Each of these areas is important to the successful

running of a company. The operations function ensures that the inputs are translated into

goods and services that are of quality and meet the demand in the market. The marketing

function is another critical function because it ensures that customers are made aware of an

organisation’s products. Also, marketing helps in identifying different customers’ needs

thereby enabling a company to supply products that satisfy customers. The human resource

function is significant to an organisation because it ensures the right talent are hired and

retained. Employees play a major role in the success of a company and hence the importance

of this functional area.

Another critical functional area in an organisation is finance. This area is significant

to an organisation because it manages all the finances of an organisation. The finance

function carries out the planning and budgeting process ensuring the achievement of strategic

goals. The area also a source for finances needed for expansion and day-to-day running of an

organisation. And last but not least, finance provides useful information used by management

in the decision-making process. Therefore, finance is a key functional area within an

organisation.

Strategic integration can be achieved at VEML by integrated the different functional

areas. The company buys, stores, markets and distribute petroleum product. Therefore, by

establishing an integrated model, controls can improve, and efficiency increased thereby

improving its performance. Integrating the operation, marketing, and financing functions will

ensure smooth flow of processes thereby increasing efficiency.

There are various functional areas within any organisation. The number and size of these

areas vary across organisations with the most common functional areas being Finance,

operations, marketing, and human resource. Each of these areas is important to the successful

running of a company. The operations function ensures that the inputs are translated into

goods and services that are of quality and meet the demand in the market. The marketing

function is another critical function because it ensures that customers are made aware of an

organisation’s products. Also, marketing helps in identifying different customers’ needs

thereby enabling a company to supply products that satisfy customers. The human resource

function is significant to an organisation because it ensures the right talent are hired and

retained. Employees play a major role in the success of a company and hence the importance

of this functional area.

Another critical functional area in an organisation is finance. This area is significant

to an organisation because it manages all the finances of an organisation. The finance

function carries out the planning and budgeting process ensuring the achievement of strategic

goals. The area also a source for finances needed for expansion and day-to-day running of an

organisation. And last but not least, finance provides useful information used by management

in the decision-making process. Therefore, finance is a key functional area within an

organisation.

Strategic integration can be achieved at VEML by integrated the different functional

areas. The company buys, stores, markets and distribute petroleum product. Therefore, by

establishing an integrated model, controls can improve, and efficiency increased thereby

improving its performance. Integrating the operation, marketing, and financing functions will

ensure smooth flow of processes thereby increasing efficiency.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1.3 Financial Statement Analysis

Financial statement analysis looks into the company’s performance through its profit

and loss statement, balance sheet statement, and ratio analysis.

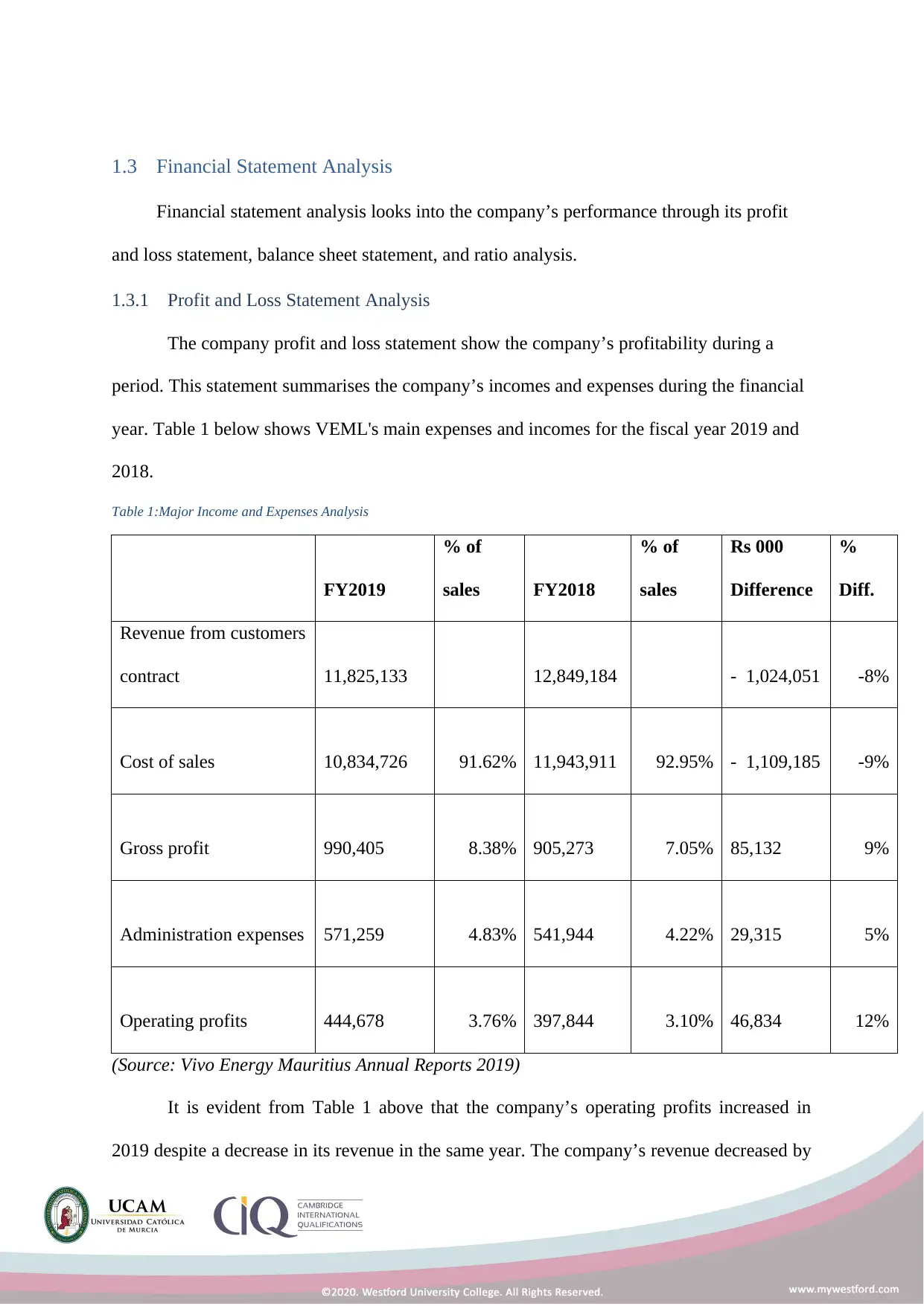

1.3.1 Profit and Loss Statement Analysis

The company profit and loss statement show the company’s profitability during a

period. This statement summarises the company’s incomes and expenses during the financial

year. Table 1 below shows VEML's main expenses and incomes for the fiscal year 2019 and

2018.

Table 1:Major Income and Expenses Analysis

FY2019

% of

sales FY2018

% of

sales

Rs 000

Difference

%

Diff.

Revenue from customers

contract 11,825,133 12,849,184 - 1,024,051 -8%

Cost of sales 10,834,726 91.62% 11,943,911 92.95% - 1,109,185 -9%

Gross profit 990,405 8.38% 905,273 7.05% 85,132 9%

Administration expenses 571,259 4.83% 541,944 4.22% 29,315 5%

Operating profits 444,678 3.76% 397,844 3.10% 46,834 12%

(Source: Vivo Energy Mauritius Annual Reports 2019)

It is evident from Table 1 above that the company’s operating profits increased in

2019 despite a decrease in its revenue in the same year. The company’s revenue decreased by

Financial statement analysis looks into the company’s performance through its profit

and loss statement, balance sheet statement, and ratio analysis.

1.3.1 Profit and Loss Statement Analysis

The company profit and loss statement show the company’s profitability during a

period. This statement summarises the company’s incomes and expenses during the financial

year. Table 1 below shows VEML's main expenses and incomes for the fiscal year 2019 and

2018.

Table 1:Major Income and Expenses Analysis

FY2019

% of

sales FY2018

% of

sales

Rs 000

Difference

%

Diff.

Revenue from customers

contract 11,825,133 12,849,184 - 1,024,051 -8%

Cost of sales 10,834,726 91.62% 11,943,911 92.95% - 1,109,185 -9%

Gross profit 990,405 8.38% 905,273 7.05% 85,132 9%

Administration expenses 571,259 4.83% 541,944 4.22% 29,315 5%

Operating profits 444,678 3.76% 397,844 3.10% 46,834 12%

(Source: Vivo Energy Mauritius Annual Reports 2019)

It is evident from Table 1 above that the company’s operating profits increased in

2019 despite a decrease in its revenue in the same year. The company’s revenue decreased by

8% in 2019 compared to the previous. Similarly, the cost of sales decreased to Rs.

10,834,726,000 in 2019 from Rs. 11,943,911,000 (Vivo Energy Mauritius Limited 2020).

The gross profit increased by 9% in 2019 from 2018. The increase in gross profit despite the

increase in revenue is due to a high rate of decrease in the cost of sales. The company’s cost

of sales accounted for 92.95% of sales in 2018 and 91.62% in 2019.

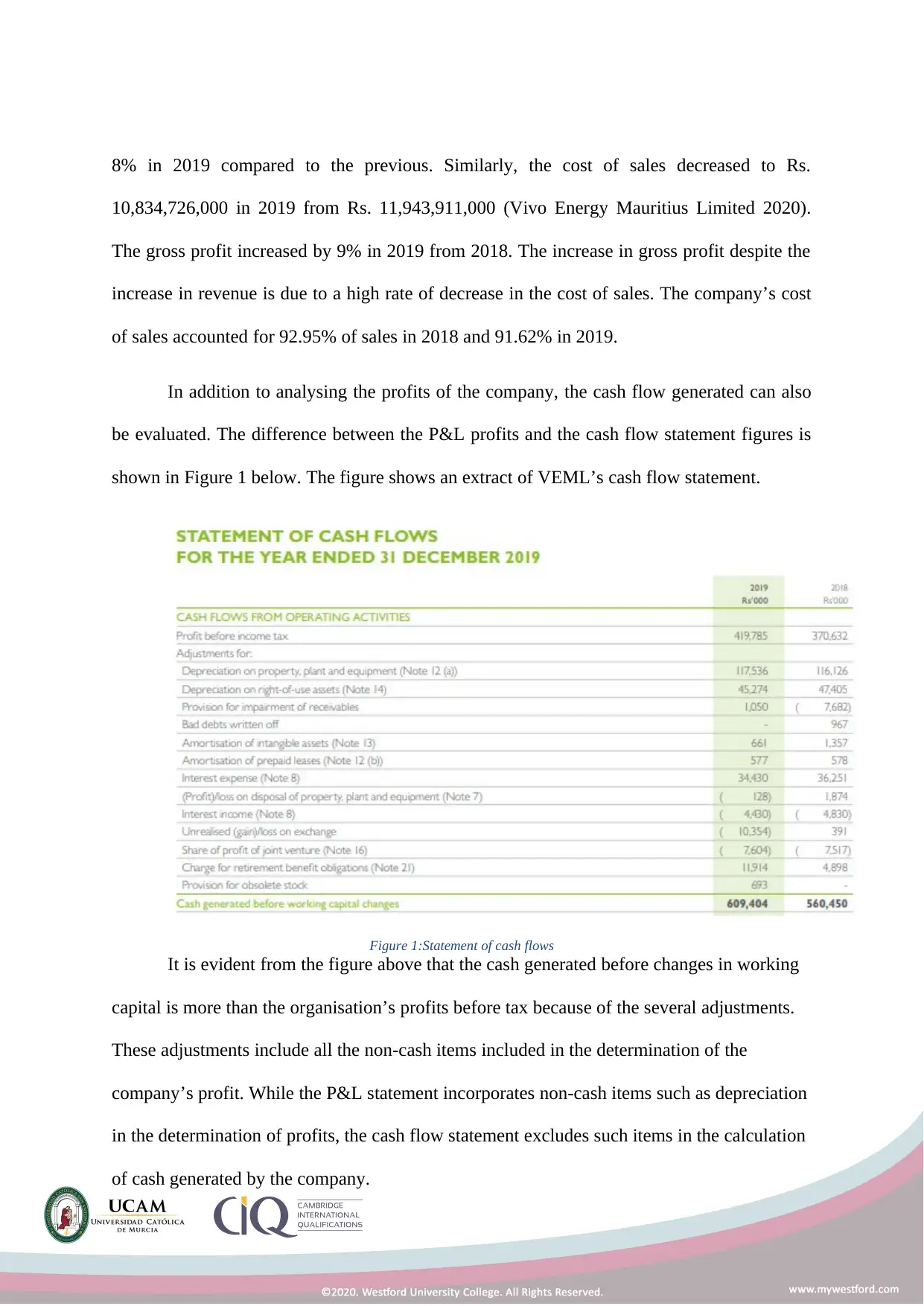

In addition to analysing the profits of the company, the cash flow generated can also

be evaluated. The difference between the P&L profits and the cash flow statement figures is

shown in Figure 1 below. The figure shows an extract of VEML’s cash flow statement.

Figure 1:Statement of cash flows

It is evident from the figure above that the cash generated before changes in working

capital is more than the organisation’s profits before tax because of the several adjustments.

These adjustments include all the non-cash items included in the determination of the

company’s profit. While the P&L statement incorporates non-cash items such as depreciation

in the determination of profits, the cash flow statement excludes such items in the calculation

of cash generated by the company.

10,834,726,000 in 2019 from Rs. 11,943,911,000 (Vivo Energy Mauritius Limited 2020).

The gross profit increased by 9% in 2019 from 2018. The increase in gross profit despite the

increase in revenue is due to a high rate of decrease in the cost of sales. The company’s cost

of sales accounted for 92.95% of sales in 2018 and 91.62% in 2019.

In addition to analysing the profits of the company, the cash flow generated can also

be evaluated. The difference between the P&L profits and the cash flow statement figures is

shown in Figure 1 below. The figure shows an extract of VEML’s cash flow statement.

Figure 1:Statement of cash flows

It is evident from the figure above that the cash generated before changes in working

capital is more than the organisation’s profits before tax because of the several adjustments.

These adjustments include all the non-cash items included in the determination of the

company’s profit. While the P&L statement incorporates non-cash items such as depreciation

in the determination of profits, the cash flow statement excludes such items in the calculation

of cash generated by the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.