Comparative Financial Analysis: Vodafone PLC and SingTel Optus

VerifiedAdded on 2023/06/05

|25

|4769

|87

Report

AI Summary

This report provides a detailed financial analysis of Vodafone PLC and SingTel Optus, focusing on key elements of their financial statements. It covers an in-depth analysis of items reported under owner’s equity, cash flow statements, other comprehensive income statements, and income statements. The analysis includes a comparative study of debt and equity positions, cash flow activities, and other comprehensive income items for both companies across multiple years (2013-2017 where data is available). Vodafone's performance is assessed based on called-up share capital, additional paid-in capital, treasury shares, accumulated losses, and other comprehensive income, while SingTel's analysis focuses on share capital, reserves, and other reserves. The report aims to provide readers with a comprehensive understanding of the financial health and performance of these two telecommunication giants.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Corporate Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CORPORATE ACCOUNTING

Executive summary:

There are five elements that consist of financial statements of an entity, these are; assets,

liabilities, revenue, expenditures and equity. It is important to have specific knowledge about

each of these elements to correctly prepare and present different statements in order to prepare

and present a complete set of financial statements for an entity operating in Australia. A

complete set of financial statements for an entity conducting business operations must have an

income statement, a statement of financial position, a statement to show the changes in equity

from previous year, a statement to record cash flows under three broad categories and notes to

accounts. Throughout this document an in-depth analysis of different items that are reported

under owner’s equity, in cash flow statements, in other comprehensive income statement and in

income statement of an entity shall be carried out for the benefit of the readers.

CORPORATE ACCOUNTING

Executive summary:

There are five elements that consist of financial statements of an entity, these are; assets,

liabilities, revenue, expenditures and equity. It is important to have specific knowledge about

each of these elements to correctly prepare and present different statements in order to prepare

and present a complete set of financial statements for an entity operating in Australia. A

complete set of financial statements for an entity conducting business operations must have an

income statement, a statement of financial position, a statement to show the changes in equity

from previous year, a statement to record cash flows under three broad categories and notes to

accounts. Throughout this document an in-depth analysis of different items that are reported

under owner’s equity, in cash flow statements, in other comprehensive income statement and in

income statement of an entity shall be carried out for the benefit of the readers.

2

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Equity:..............................................................................................................................................3

Cash flow statements:......................................................................................................................8

Other Comprehensive income statement:......................................................................................12

Accounting for corporate income tax:...........................................................................................14

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

CORPORATE ACCOUNTING

Contents

Executive summary:........................................................................................................................1

Introduction:....................................................................................................................................3

Equity:..............................................................................................................................................3

Cash flow statements:......................................................................................................................8

Other Comprehensive income statement:......................................................................................12

Accounting for corporate income tax:...........................................................................................14

Conclusion:....................................................................................................................................20

References:....................................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CORPORATE ACCOUNTING

Introduction:

Vodafone PLC and SingTel Optus are the two companies to be used to complete the exercise in

this document. A brief description about the two companies and their operations would provide

the point of references to the users of this document to understand the various elements discussed

here.

Vodafone PLC operates in Australia with the corporate identity of Vodafone Australia. The

company is worldwide telecom giant with its operations spreading to different countries in all

across the globe. Originated in United Kingdom, Vodafone PLC is now one of the largest

telecommunication companies in the world.

SingTel Optus, a telecommunication company in the country, is also one of the largest

telecommunication companies the country. Along with the market leader in the country, i.e.

Telstra Corporation, SingTel has been quite successful in capturing significant amount of market

share in the domestic market.

Equity:

(i) Components of owners’ equity and changes to these components over the years:

Called up share capital: Vodafone PLC has issued shares in the capital market to raise funds for

running business operations. The face value of shares issued and called up is represented in the

called up share capital account (Burks, 2015).

Share capital: It is the amount of face value of shares received by the company from the

shareholders. Amount of face value received by issuing ordinary shares in the market is

accumulated in share capital account.

CORPORATE ACCOUNTING

Introduction:

Vodafone PLC and SingTel Optus are the two companies to be used to complete the exercise in

this document. A brief description about the two companies and their operations would provide

the point of references to the users of this document to understand the various elements discussed

here.

Vodafone PLC operates in Australia with the corporate identity of Vodafone Australia. The

company is worldwide telecom giant with its operations spreading to different countries in all

across the globe. Originated in United Kingdom, Vodafone PLC is now one of the largest

telecommunication companies in the world.

SingTel Optus, a telecommunication company in the country, is also one of the largest

telecommunication companies the country. Along with the market leader in the country, i.e.

Telstra Corporation, SingTel has been quite successful in capturing significant amount of market

share in the domestic market.

Equity:

(i) Components of owners’ equity and changes to these components over the years:

Called up share capital: Vodafone PLC has issued shares in the capital market to raise funds for

running business operations. The face value of shares issued and called up is represented in the

called up share capital account (Burks, 2015).

Share capital: It is the amount of face value of shares received by the company from the

shareholders. Amount of face value received by issuing ordinary shares in the market is

accumulated in share capital account.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CORPORATE ACCOUNTING

Additional paid up share capital: Vodafone PLC has issued share over the face value and the

amount received in excess of the face value form issue shares has been accumulated in the

additional paid up share capital account.

Treasury shares: The amount of stock that an entity has brought back from the capital market is

accumulated in treasury shares. Vodafone PLC has balance in treasury shares (Floyd, 2016).

Reserves: SingTel Optus has accumulated balance in reserves. This is the accumulated amount

set aside from profit and loss account of the company to meet specific future obligations.

Accumulated losses: The amount of loss accumulated from the business activities of Vodafone

over the years is stated under accumulated losses in the Balance sheet of the company (Chen,

2015).

Accumulated other comprehensive income: Vodafone PLC has showed accumulated income

from other comprehensive income. This is the amount of income in other comprehensive income

statement.

Other reserves: SingTel has reported other reserves under owners’ equity in the Balance Sheet. It

is the free reserves that has been accumulated from balance of profit and loss account after

making all provisions and declaration of dividend (Heidari and Felden, 2015).

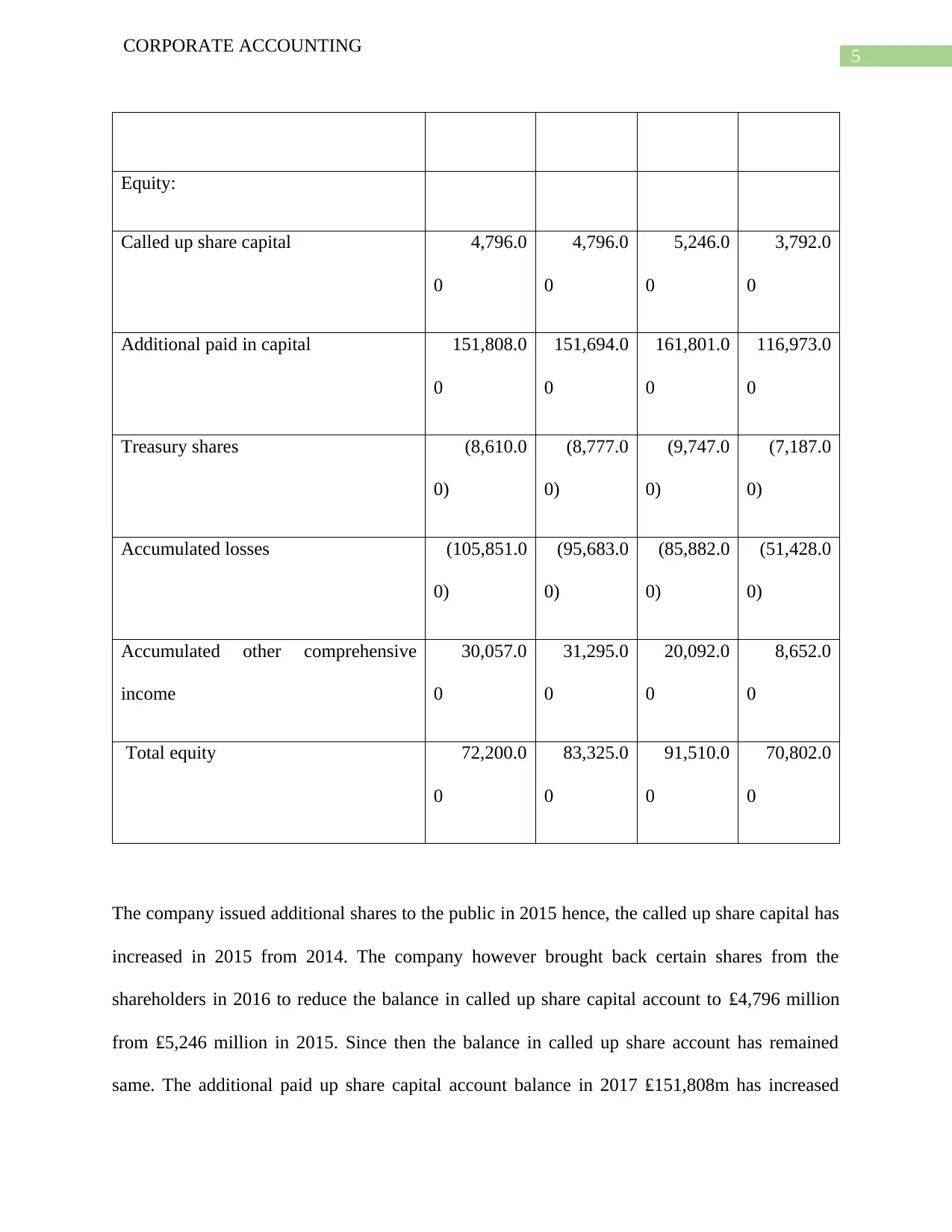

Changes in the items of equity of Vodafone PLC can be seen in the following table:

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

CORPORATE ACCOUNTING

Additional paid up share capital: Vodafone PLC has issued share over the face value and the

amount received in excess of the face value form issue shares has been accumulated in the

additional paid up share capital account.

Treasury shares: The amount of stock that an entity has brought back from the capital market is

accumulated in treasury shares. Vodafone PLC has balance in treasury shares (Floyd, 2016).

Reserves: SingTel Optus has accumulated balance in reserves. This is the accumulated amount

set aside from profit and loss account of the company to meet specific future obligations.

Accumulated losses: The amount of loss accumulated from the business activities of Vodafone

over the years is stated under accumulated losses in the Balance sheet of the company (Chen,

2015).

Accumulated other comprehensive income: Vodafone PLC has showed accumulated income

from other comprehensive income. This is the amount of income in other comprehensive income

statement.

Other reserves: SingTel has reported other reserves under owners’ equity in the Balance Sheet. It

is the free reserves that has been accumulated from balance of profit and loss account after

making all provisions and declaration of dividend (Heidari and Felden, 2015).

Changes in the items of equity of Vodafone PLC can be seen in the following table:

Vodafone

Amount in ₤' Million

Year 2017 2016 2015 2014

5

CORPORATE ACCOUNTING

Equity:

Called up share capital 4,796.0

0

4,796.0

0

5,246.0

0

3,792.0

0

Additional paid in capital 151,808.0

0

151,694.0

0

161,801.0

0

116,973.0

0

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.0

0

31,295.0

0

20,092.0

0

8,652.0

0

Total equity 72,200.0

0

83,325.0

0

91,510.0

0

70,802.0

0

The company issued additional shares to the public in 2015 hence, the called up share capital has

increased in 2015 from 2014. The company however brought back certain shares from the

shareholders in 2016 to reduce the balance in called up share capital account to ₤4,796 million

from ₤5,246 million in 2015. Since then the balance in called up share account has remained

same. The additional paid up share capital account balance in 2017 ₤151,808m has increased

CORPORATE ACCOUNTING

Equity:

Called up share capital 4,796.0

0

4,796.0

0

5,246.0

0

3,792.0

0

Additional paid in capital 151,808.0

0

151,694.0

0

161,801.0

0

116,973.0

0

Treasury shares (8,610.0

0)

(8,777.0

0)

(9,747.0

0)

(7,187.0

0)

Accumulated losses (105,851.0

0)

(95,683.0

0)

(85,882.0

0)

(51,428.0

0)

Accumulated other comprehensive

income

30,057.0

0

31,295.0

0

20,092.0

0

8,652.0

0

Total equity 72,200.0

0

83,325.0

0

91,510.0

0

70,802.0

0

The company issued additional shares to the public in 2015 hence, the called up share capital has

increased in 2015 from 2014. The company however brought back certain shares from the

shareholders in 2016 to reduce the balance in called up share capital account to ₤4,796 million

from ₤5,246 million in 2015. Since then the balance in called up share account has remained

same. The additional paid up share capital account balance in 2017 ₤151,808m has increased

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CORPORATE ACCOUNTING

from ₤151,694m of 2016 due to adjustment made to the account (Chen, Miao and Shevlin,

2015).

The balance in treasury stock has reduced to ₤8,610m in 2017 from ₤8,777m in 2016.

Accumulated losses of ₤105,851m of 2017 has increased after every year. This is because the

company has incurred losses from business operations. In 2014 the accumulated losses were only

₤51,428m.

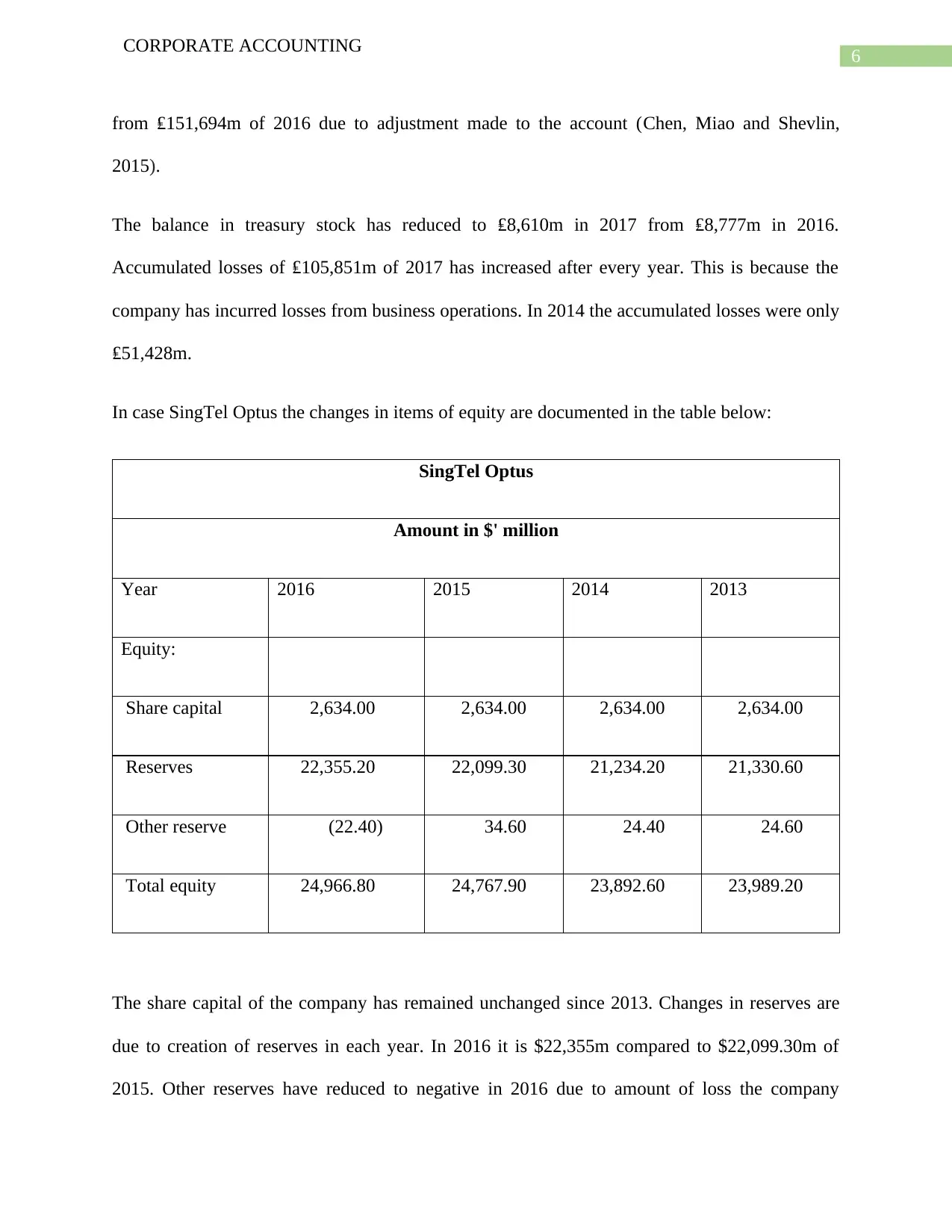

In case SingTel Optus the changes in items of equity are documented in the table below:

SingTel Optus

Amount in $' million

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

The share capital of the company has remained unchanged since 2013. Changes in reserves are

due to creation of reserves in each year. In 2016 it is $22,355m compared to $22,099.30m of

2015. Other reserves have reduced to negative in 2016 due to amount of loss the company

CORPORATE ACCOUNTING

from ₤151,694m of 2016 due to adjustment made to the account (Chen, Miao and Shevlin,

2015).

The balance in treasury stock has reduced to ₤8,610m in 2017 from ₤8,777m in 2016.

Accumulated losses of ₤105,851m of 2017 has increased after every year. This is because the

company has incurred losses from business operations. In 2014 the accumulated losses were only

₤51,428m.

In case SingTel Optus the changes in items of equity are documented in the table below:

SingTel Optus

Amount in $' million

Year 2016 2015 2014 2013

Equity:

Share capital 2,634.00 2,634.00 2,634.00 2,634.00

Reserves 22,355.20 22,099.30 21,234.20 21,330.60

Other reserve (22.40) 34.60 24.40 24.60

Total equity 24,966.80 24,767.90 23,892.60 23,989.20

The share capital of the company has remained unchanged since 2013. Changes in reserves are

due to creation of reserves in each year. In 2016 it is $22,355m compared to $22,099.30m of

2015. Other reserves have reduced to negative in 2016 due to amount of loss the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CORPORATE ACCOUNTING

incurred I its business operations in 2016 and the same was transferred to the reserves resulted in

negative other reserves balance (Graham et. al. 2017).

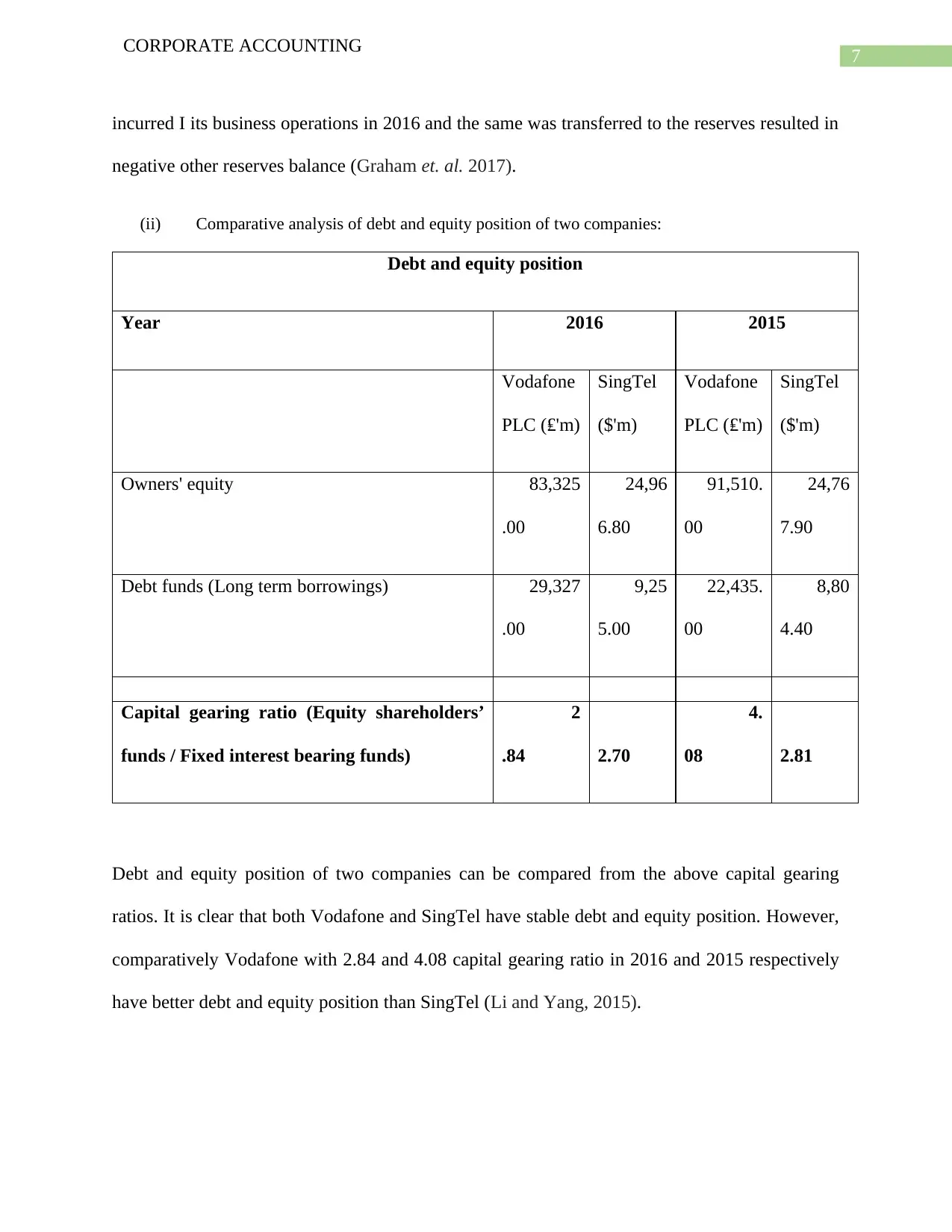

(ii) Comparative analysis of debt and equity position of two companies:

Debt and equity position

Year 2016 2015

Vodafone

PLC (₤'m)

SingTel

($'m)

Vodafone

PLC (₤'m)

SingTel

($'m)

Owners' equity 83,325

.00

24,96

6.80

91,510.

00

24,76

7.90

Debt funds (Long term borrowings) 29,327

.00

9,25

5.00

22,435.

00

8,80

4.40

Capital gearing ratio (Equity shareholders’

funds / Fixed interest bearing funds)

2

.84 2.70

4.

08 2.81

Debt and equity position of two companies can be compared from the above capital gearing

ratios. It is clear that both Vodafone and SingTel have stable debt and equity position. However,

comparatively Vodafone with 2.84 and 4.08 capital gearing ratio in 2016 and 2015 respectively

have better debt and equity position than SingTel (Li and Yang, 2015).

CORPORATE ACCOUNTING

incurred I its business operations in 2016 and the same was transferred to the reserves resulted in

negative other reserves balance (Graham et. al. 2017).

(ii) Comparative analysis of debt and equity position of two companies:

Debt and equity position

Year 2016 2015

Vodafone

PLC (₤'m)

SingTel

($'m)

Vodafone

PLC (₤'m)

SingTel

($'m)

Owners' equity 83,325

.00

24,96

6.80

91,510.

00

24,76

7.90

Debt funds (Long term borrowings) 29,327

.00

9,25

5.00

22,435.

00

8,80

4.40

Capital gearing ratio (Equity shareholders’

funds / Fixed interest bearing funds)

2

.84 2.70

4.

08 2.81

Debt and equity position of two companies can be compared from the above capital gearing

ratios. It is clear that both Vodafone and SingTel have stable debt and equity position. However,

comparatively Vodafone with 2.84 and 4.08 capital gearing ratio in 2016 and 2015 respectively

have better debt and equity position than SingTel (Li and Yang, 2015).

8

CORPORATE ACCOUNTING

Cash flow statements:

(iii) Both companies have reported cash flows under three broad categories these are cash flow

from operating activities, investing actives and financing activities. Before getting into

changes in these items let’s have a brief understanding of different items reported under three

broad categories of both the companies (Leuz and Wysocki, 2016).

Operating activities: Both Vodafone and SingTel have reported cash received from

customers and cash paid to suppliers and employees. Cash received from customers are the

revenue received from providing telecommunication services to the customers. Payment of

cash to suppliers is the amount paid to suppliers for using the services and operating platform

of suppliers. Payment to employees is the amount paid as salaries and wages to employees

and workers for their services. Without the services of the employees it would not have been

possible to provide services to the customers (Christensen et. al. 2015)). SingTel unlike

Vodafone has used indirect method to present its cash flow from operating activities thus, the

following items have been reported under the cash flow from operating activities of the

company:

Profit before tax: It is the amount of profit earned from business before tax.

Adjustments for depreciation and amortization: Since the depreciation and amortization costs are

not cash expenses hence, these are added back to the profit before tax of the company (Cuccia,

2018).

Adjustment for share of results in associates and joint ventures: The deduction for share of

results in joint ventures and associates is because such profit or loss is generally not received in

cash.

CORPORATE ACCOUNTING

Cash flow statements:

(iii) Both companies have reported cash flows under three broad categories these are cash flow

from operating activities, investing actives and financing activities. Before getting into

changes in these items let’s have a brief understanding of different items reported under three

broad categories of both the companies (Leuz and Wysocki, 2016).

Operating activities: Both Vodafone and SingTel have reported cash received from

customers and cash paid to suppliers and employees. Cash received from customers are the

revenue received from providing telecommunication services to the customers. Payment of

cash to suppliers is the amount paid to suppliers for using the services and operating platform

of suppliers. Payment to employees is the amount paid as salaries and wages to employees

and workers for their services. Without the services of the employees it would not have been

possible to provide services to the customers (Christensen et. al. 2015)). SingTel unlike

Vodafone has used indirect method to present its cash flow from operating activities thus, the

following items have been reported under the cash flow from operating activities of the

company:

Profit before tax: It is the amount of profit earned from business before tax.

Adjustments for depreciation and amortization: Since the depreciation and amortization costs are

not cash expenses hence, these are added back to the profit before tax of the company (Cuccia,

2018).

Adjustment for share of results in associates and joint ventures: The deduction for share of

results in joint ventures and associates is because such profit or loss is generally not received in

cash.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CORPORATE ACCOUNTING

Exceptional items of non-cash: Non-cash exceptional items have to be added and deducted as the

case may be depending on whether the item is revenue or expenditures as these have no effect on

cash of the company (Phillips, 2016).

Interest and investment income: Interest from investment income is deducted for the obvious

reason that such income is considered in calculating cash flow from investing activities.

Finance costs: Finance cost will be considered in calculating cash flow from financing activities

hence have to be added back to profit before tax as it not an operating item.

Other non-cash items: All other non-cash items have to be adjusted as these have no effect on

movement of cash (Papanastasopoulos, 2018).

Changes in working capital: The changes in working capital, i.e. total cash assets less total cash

liabilities of the company is added or deducted from adjusted profit before tax after all the above

adjustments. In case increase in working capital it is deduced from the adjusted profit and in case

of reduction the same is added to the adjusted profit.

Income tax payment: The amount paid as income tax is deducted from the resultant amount after

adjustments of changes in working capital (Penman, S.H., 2016).

Changes in items:

SingTel Optus:

Profit before tax in case of SingTel has increased to $4,580.8 million from $4,463 million.

Depreciation and amortization cost has decreased from 2015 to $2,148.8m in 2016. Share of

results (negative) in associates and joint ventures have increased to $2,026.6m in 2016. Non-cash

exception item for 2016 is ($2.4) million is much less than of ($57.7m) of 2015. Fiancé cost of

CORPORATE ACCOUNTING

Exceptional items of non-cash: Non-cash exceptional items have to be added and deducted as the

case may be depending on whether the item is revenue or expenditures as these have no effect on

cash of the company (Phillips, 2016).

Interest and investment income: Interest from investment income is deducted for the obvious

reason that such income is considered in calculating cash flow from investing activities.

Finance costs: Finance cost will be considered in calculating cash flow from financing activities

hence have to be added back to profit before tax as it not an operating item.

Other non-cash items: All other non-cash items have to be adjusted as these have no effect on

movement of cash (Papanastasopoulos, 2018).

Changes in working capital: The changes in working capital, i.e. total cash assets less total cash

liabilities of the company is added or deducted from adjusted profit before tax after all the above

adjustments. In case increase in working capital it is deduced from the adjusted profit and in case

of reduction the same is added to the adjusted profit.

Income tax payment: The amount paid as income tax is deducted from the resultant amount after

adjustments of changes in working capital (Penman, S.H., 2016).

Changes in items:

SingTel Optus:

Profit before tax in case of SingTel has increased to $4,580.8 million from $4,463 million.

Depreciation and amortization cost has decreased from 2015 to $2,148.8m in 2016. Share of

results (negative) in associates and joint ventures have increased to $2,026.6m in 2016. Non-cash

exception item for 2016 is ($2.4) million is much less than of ($57.7m) of 2015. Fiancé cost of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CORPORATE ACCOUNTING

2016 added back to the profit is $359.6m whereas in 2015 the company only added back

$309.2m. The company has used $2,740m in 2016 on investing activities. In 2015 it invested

$3,556.9m on investment activities. The company in 2016 used net of $2,043.5m to repayment

its debts and borrowings along with payment of dividend compared to $2,310.6m it used in 2015

(Karadag, 2015).

Vodafone PLC:

The net cash generated by the company from operating activities in 2016 is ₤10,481m in net

compared to ₤9,715 in 2015. Thus, a significant improvement by the company in generation cash

flow from operating activities. The increase is mainly due to increase in cash received from

customers. Cash flow used in investing activities of Vodafone for 2016 is ₤10,151m is lower

than ₤10,327m of 2015. The decrease is mainly due to increase in acquisition of interests in

subsidiaries during 2016. The company unlike past has generated cash flow from financing

activities in 2016. In 2016 the company has generated ₤2,960m in cash inflows from financing

activities. In 2015 the company used ₤2,418m in financing activities (Finocchiaro et. al. 2018).

(iv) Comparative analysis of three broad cash flows:

The table below contains comparative analysis of three broad categories of cash flows of the two

companies.

Change

SingTel ($'million) 2,016.00 2,015.00

Increase /

(Decrease)

Cash flow from operating activities 4,647.70 5,786.60 (1,138.90)

Cash flow from investing activities (2,740.00) 3,556.90 (6,296.90)

Cash flow from financing activities (2,043.50) 2,310.60 (4,354.10)

CORPORATE ACCOUNTING

2016 added back to the profit is $359.6m whereas in 2015 the company only added back

$309.2m. The company has used $2,740m in 2016 on investing activities. In 2015 it invested

$3,556.9m on investment activities. The company in 2016 used net of $2,043.5m to repayment

its debts and borrowings along with payment of dividend compared to $2,310.6m it used in 2015

(Karadag, 2015).

Vodafone PLC:

The net cash generated by the company from operating activities in 2016 is ₤10,481m in net

compared to ₤9,715 in 2015. Thus, a significant improvement by the company in generation cash

flow from operating activities. The increase is mainly due to increase in cash received from

customers. Cash flow used in investing activities of Vodafone for 2016 is ₤10,151m is lower

than ₤10,327m of 2015. The decrease is mainly due to increase in acquisition of interests in

subsidiaries during 2016. The company unlike past has generated cash flow from financing

activities in 2016. In 2016 the company has generated ₤2,960m in cash inflows from financing

activities. In 2015 the company used ₤2,418m in financing activities (Finocchiaro et. al. 2018).

(iv) Comparative analysis of three broad cash flows:

The table below contains comparative analysis of three broad categories of cash flows of the two

companies.

Change

SingTel ($'million) 2,016.00 2,015.00

Increase /

(Decrease)

Cash flow from operating activities 4,647.70 5,786.60 (1,138.90)

Cash flow from investing activities (2,740.00) 3,556.90 (6,296.90)

Cash flow from financing activities (2,043.50) 2,310.60 (4,354.10)

11

CORPORATE ACCOUNTING

Vodafone PLC (₤'m) 2016 2015

Cash flow from operating activities 10,481.00 9,715.00 766.00

Cash flow from investing activites (10,151.00) (10,327.00) 176.00

Cash flow from financing activities 2,960.00 (2,418.00) 5,378.00

(v) Comparative analysis between two companies:

2016

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 10,481.00 4,647.70

Cash flow from investing activities (10,151.00) (2,740.00)

Cash flow from financing activities 2,960.00 (2,043.50)

2015

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 9,715.00 5,786.60

Cash flow from investing activities (10,327.00) 3,556.90

Cash flow from financing activities (2,418.00) 2,310.60

CORPORATE ACCOUNTING

Vodafone PLC (₤'m) 2016 2015

Cash flow from operating activities 10,481.00 9,715.00 766.00

Cash flow from investing activites (10,151.00) (10,327.00) 176.00

Cash flow from financing activities 2,960.00 (2,418.00) 5,378.00

(v) Comparative analysis between two companies:

2016

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 10,481.00 4,647.70

Cash flow from investing activities (10,151.00) (2,740.00)

Cash flow from financing activities 2,960.00 (2,043.50)

2015

Vodafone PLC

(₤'m)

SingTel

($'million)

Cash flow from operating activities 9,715.00 5,786.60

Cash flow from investing activities (10,327.00) 3,556.90

Cash flow from financing activities (2,418.00) 2,310.60

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.