Financial Accounting Assignment: IAS 10, Share Capital, and Impairment

VerifiedAdded on 2021/02/19

|10

|2378

|40

Homework Assignment

AI Summary

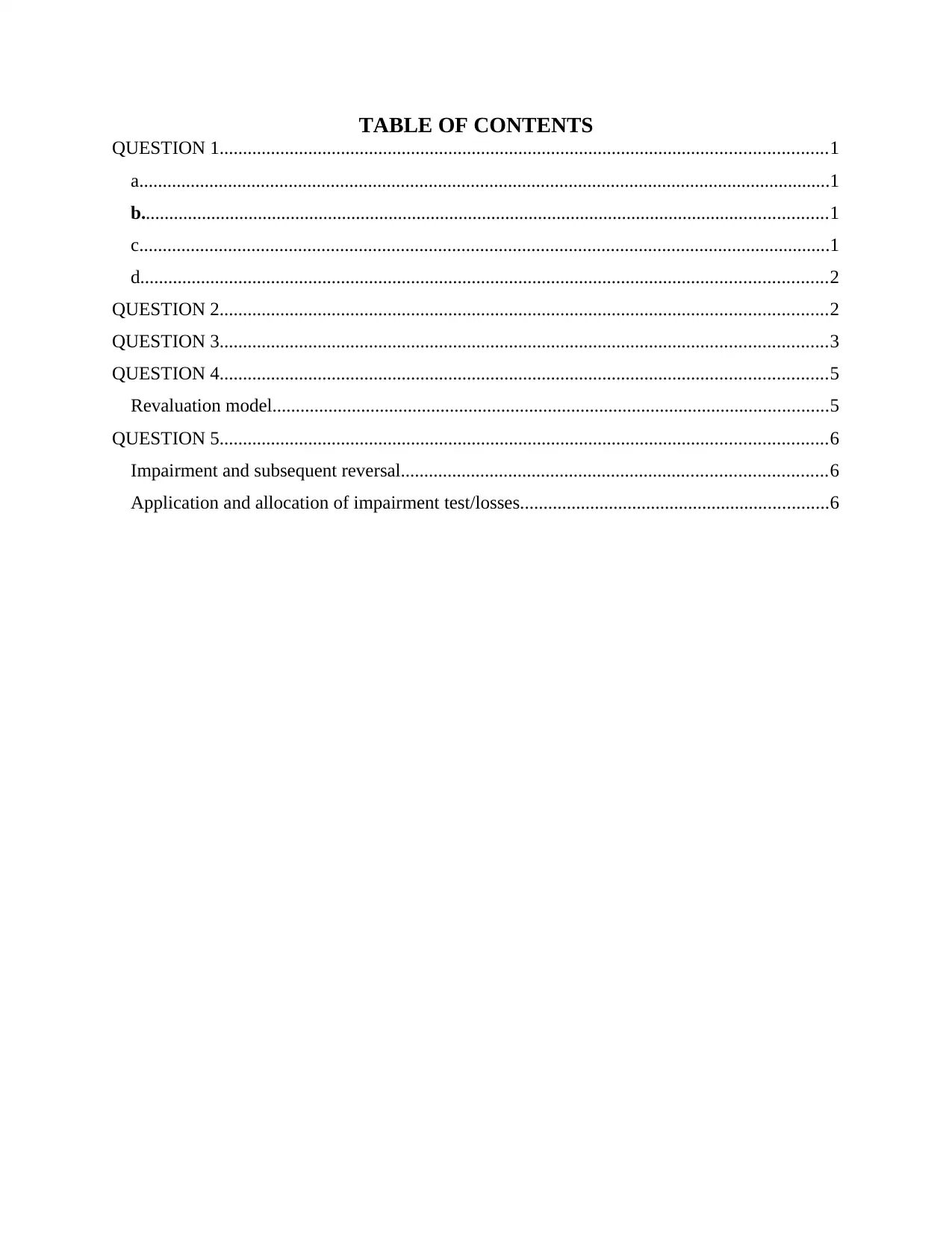

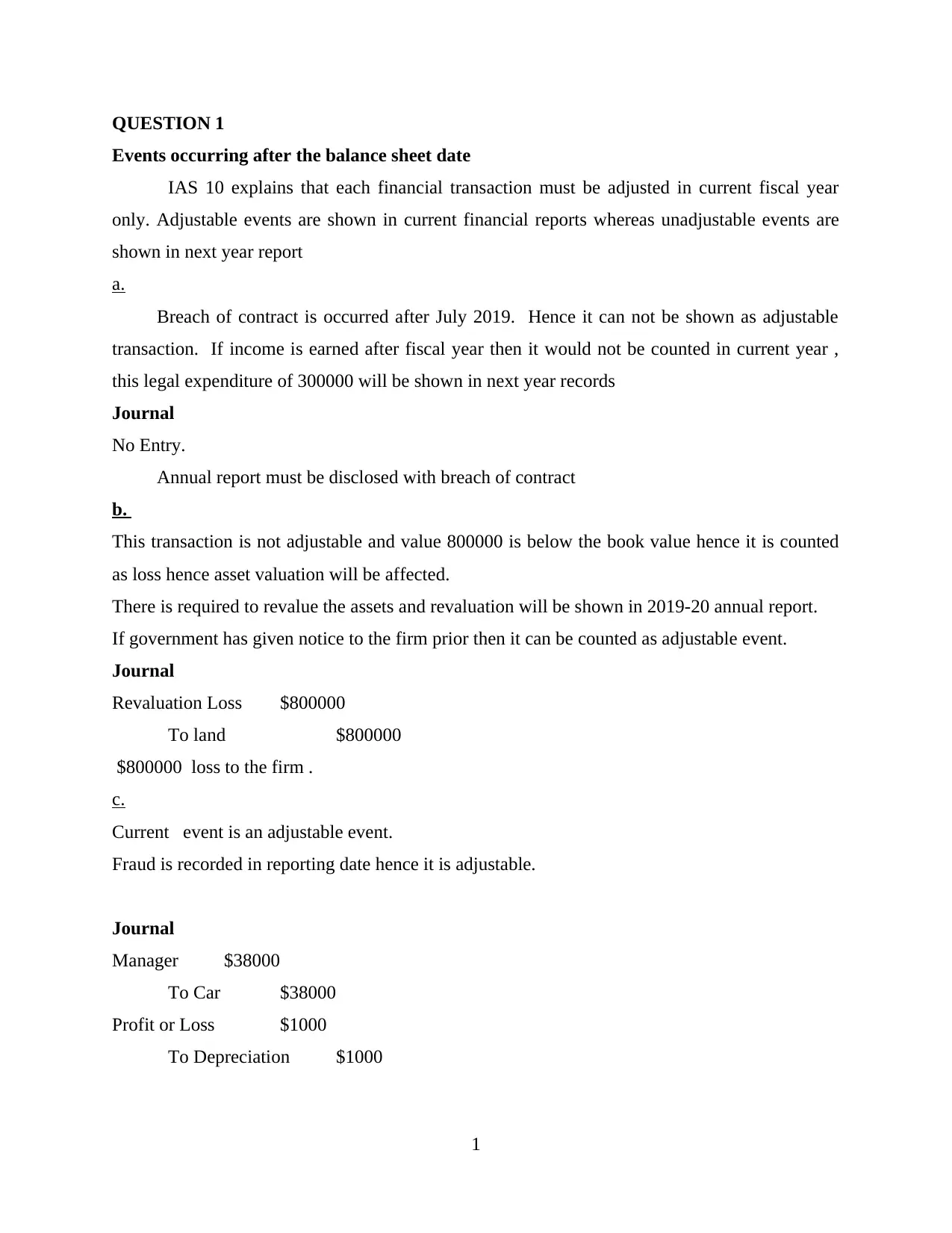

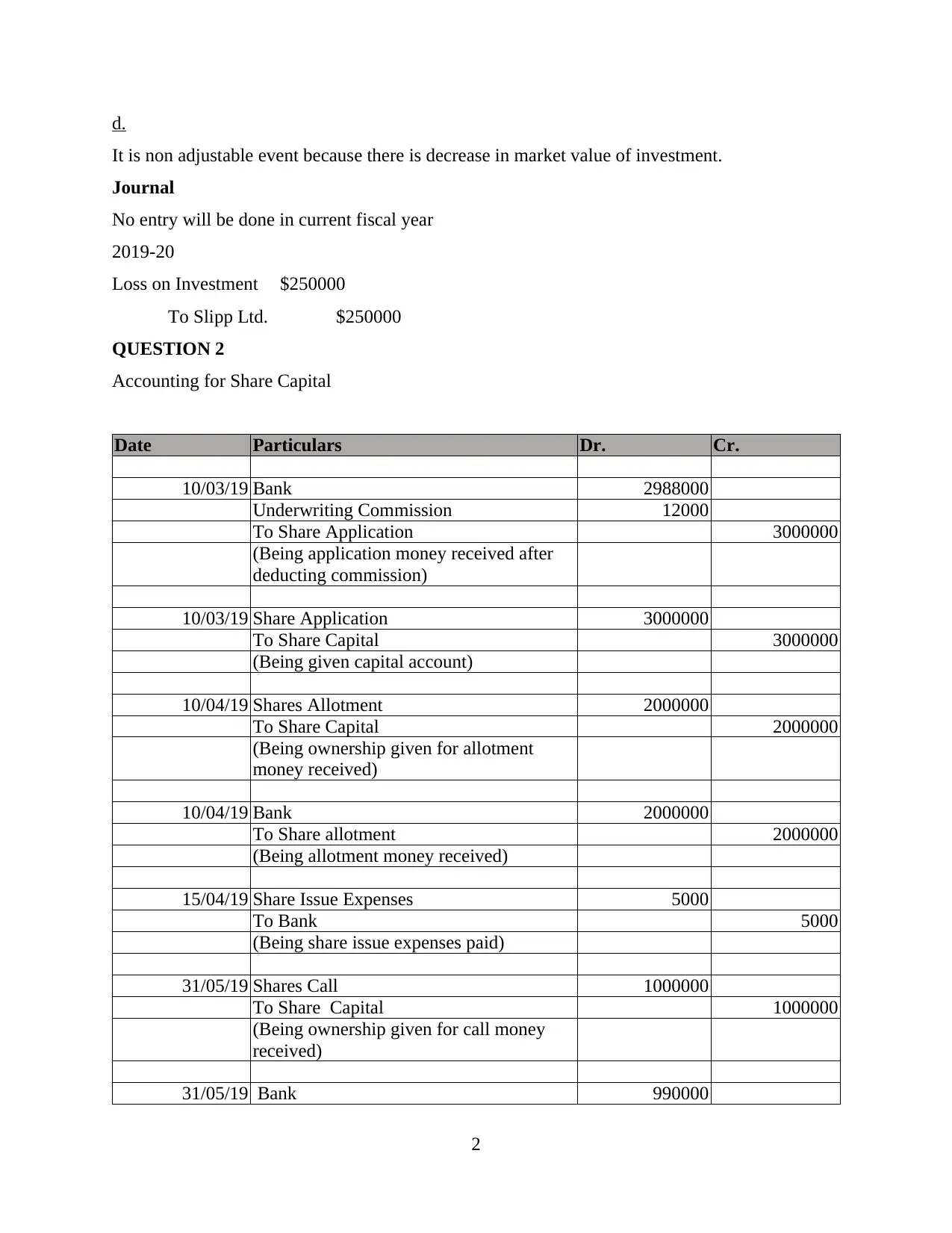

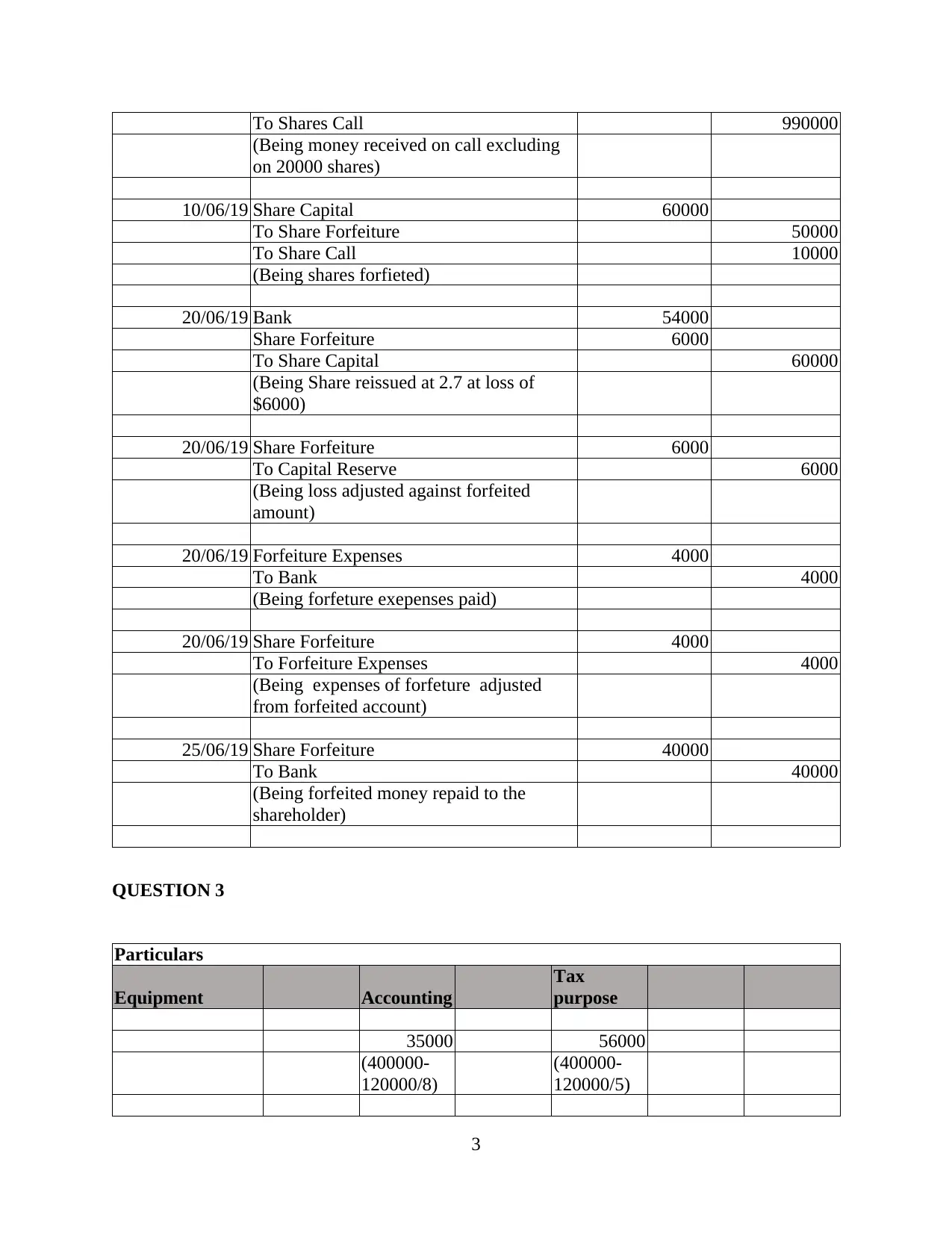

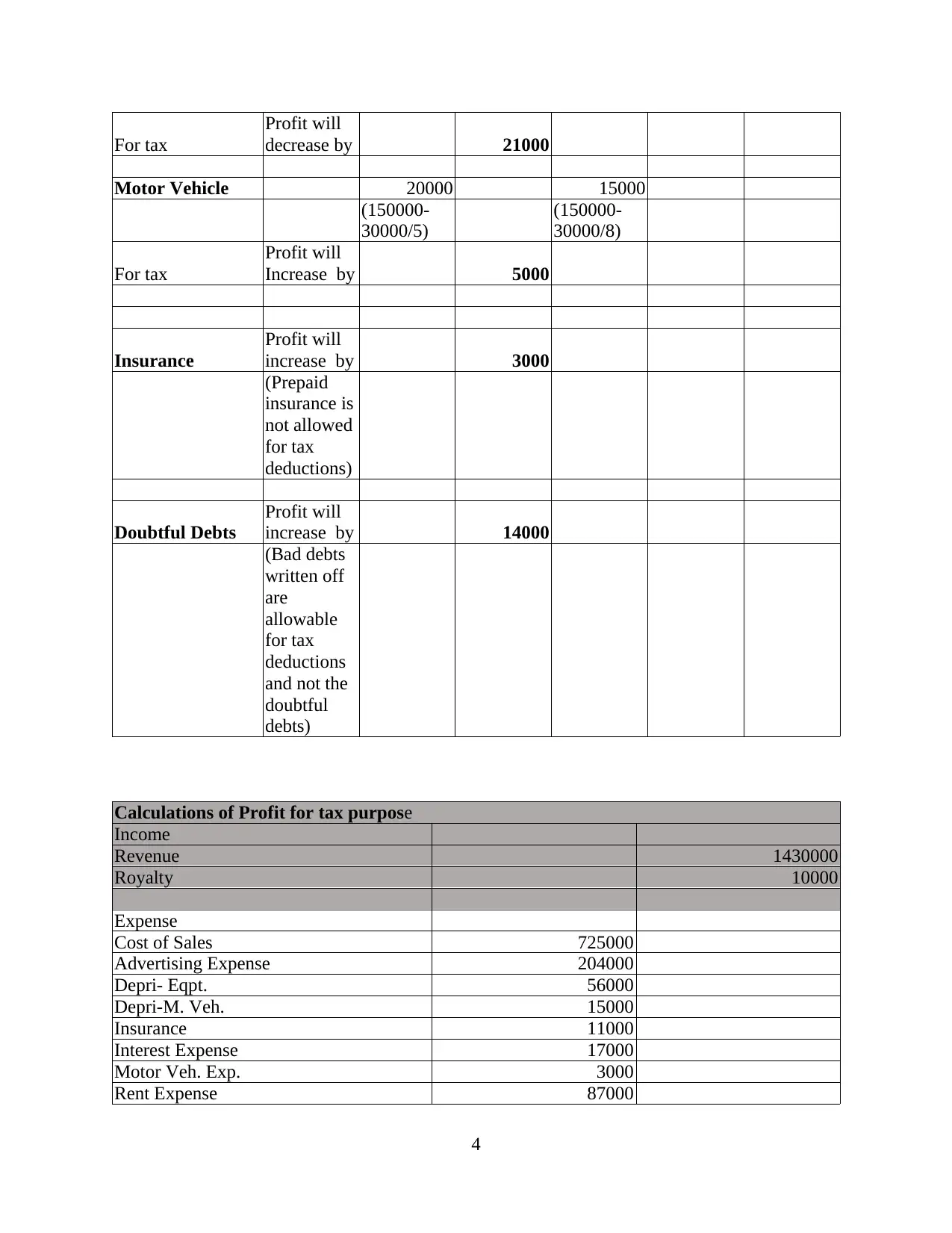

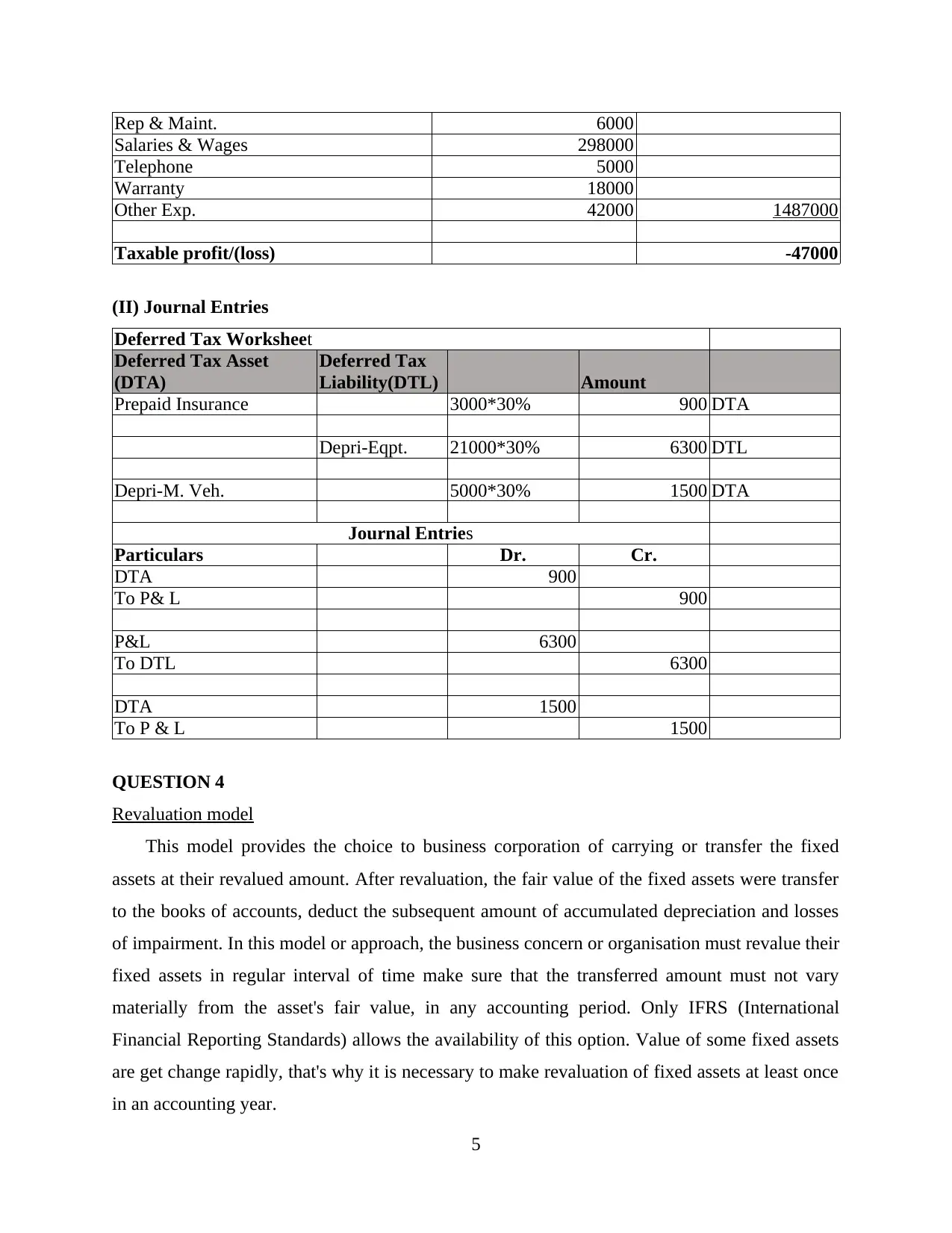

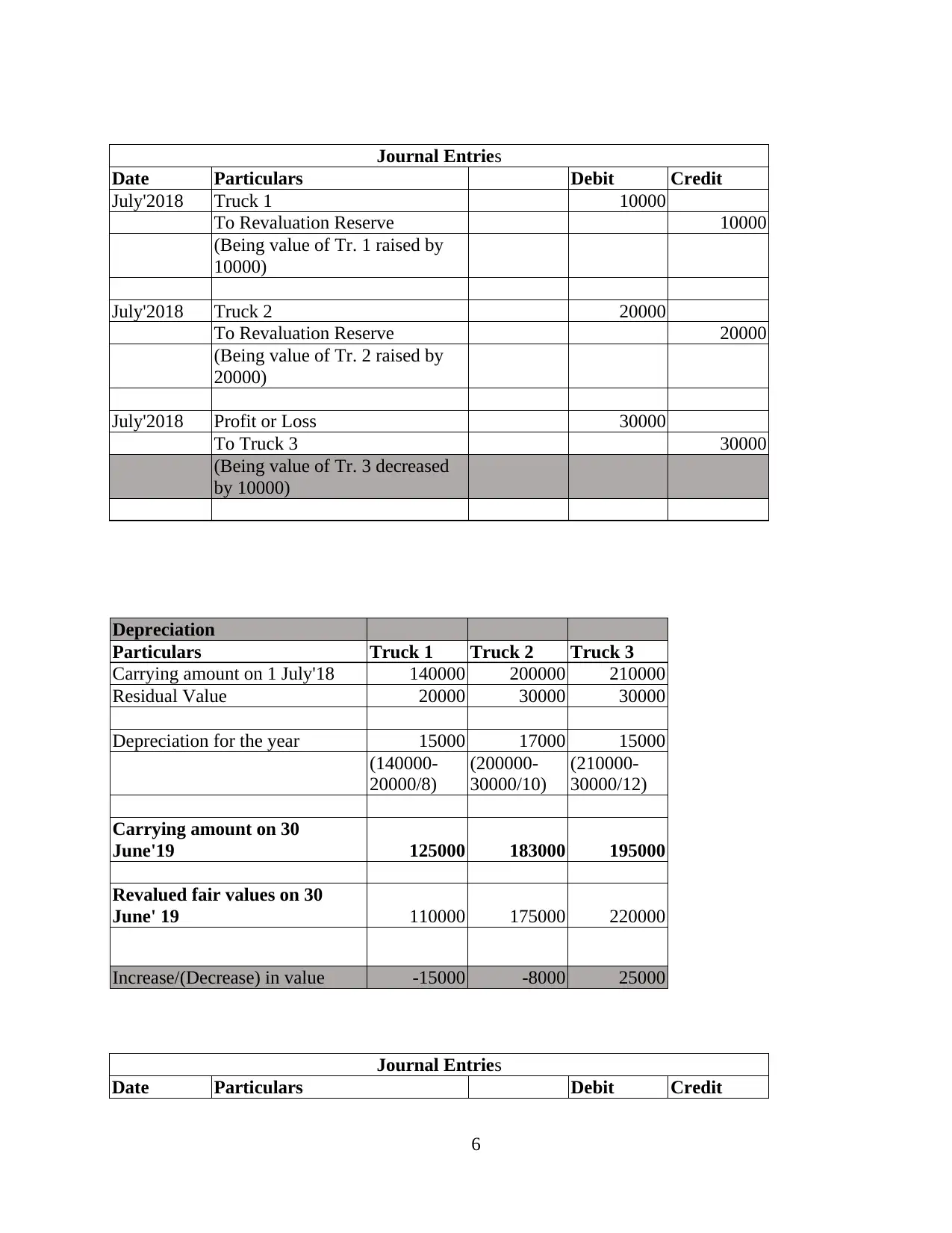

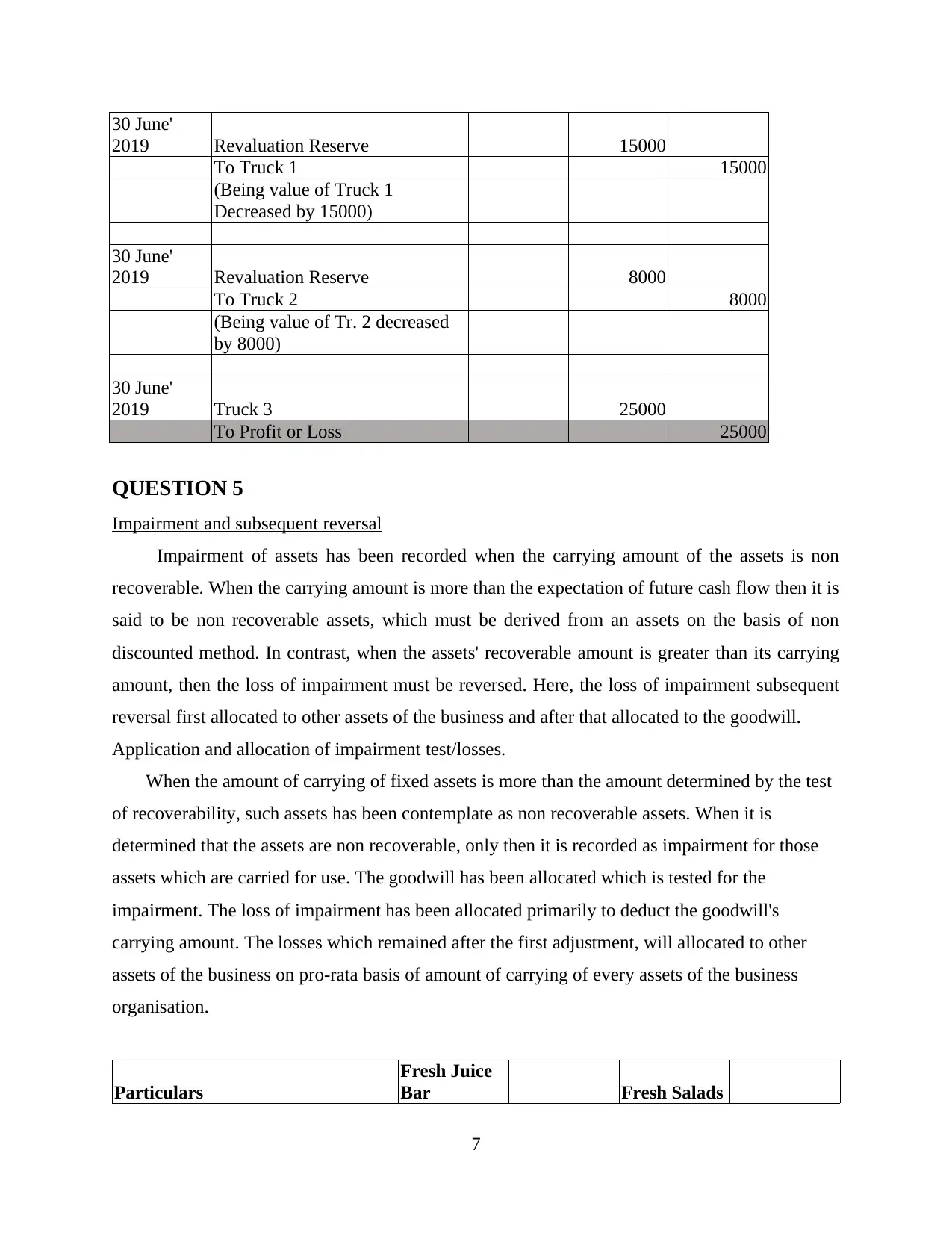

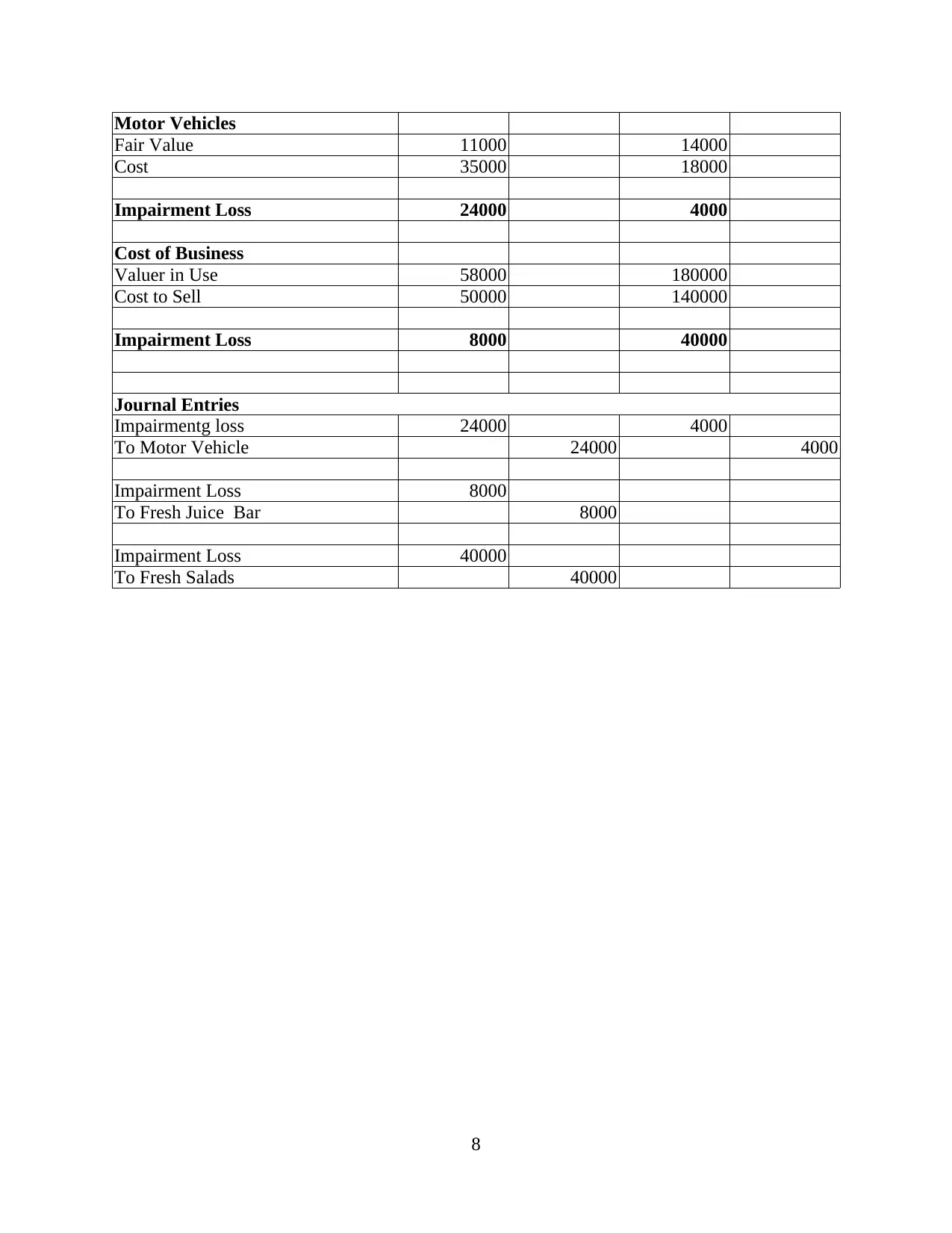

This financial accounting assignment solution addresses several key areas of financial reporting. It begins with an analysis of events occurring after the balance sheet date, as per IAS 10, determining whether transactions are adjustable or non-adjustable and providing corresponding journal entries. The solution then delves into accounting for share capital, including journal entries for share applications, allotments, share issue expenses, share calls, forfeitures, and reissuance of shares. A detailed explanation and calculations are provided for the deferred tax worksheet. The assignment also covers the revaluation model for fixed assets, including journal entries for increases and decreases in asset values, and discusses impairment and subsequent reversal of assets, explaining the application and allocation of impairment tests and losses. The solution encompasses a range of financial accounting principles and practical applications, making it a valuable resource for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.