Comprehensive Audit Program for Aeris Environmental Ltd Report

VerifiedAdded on 2023/04/21

|10

|1207

|171

Report

AI Summary

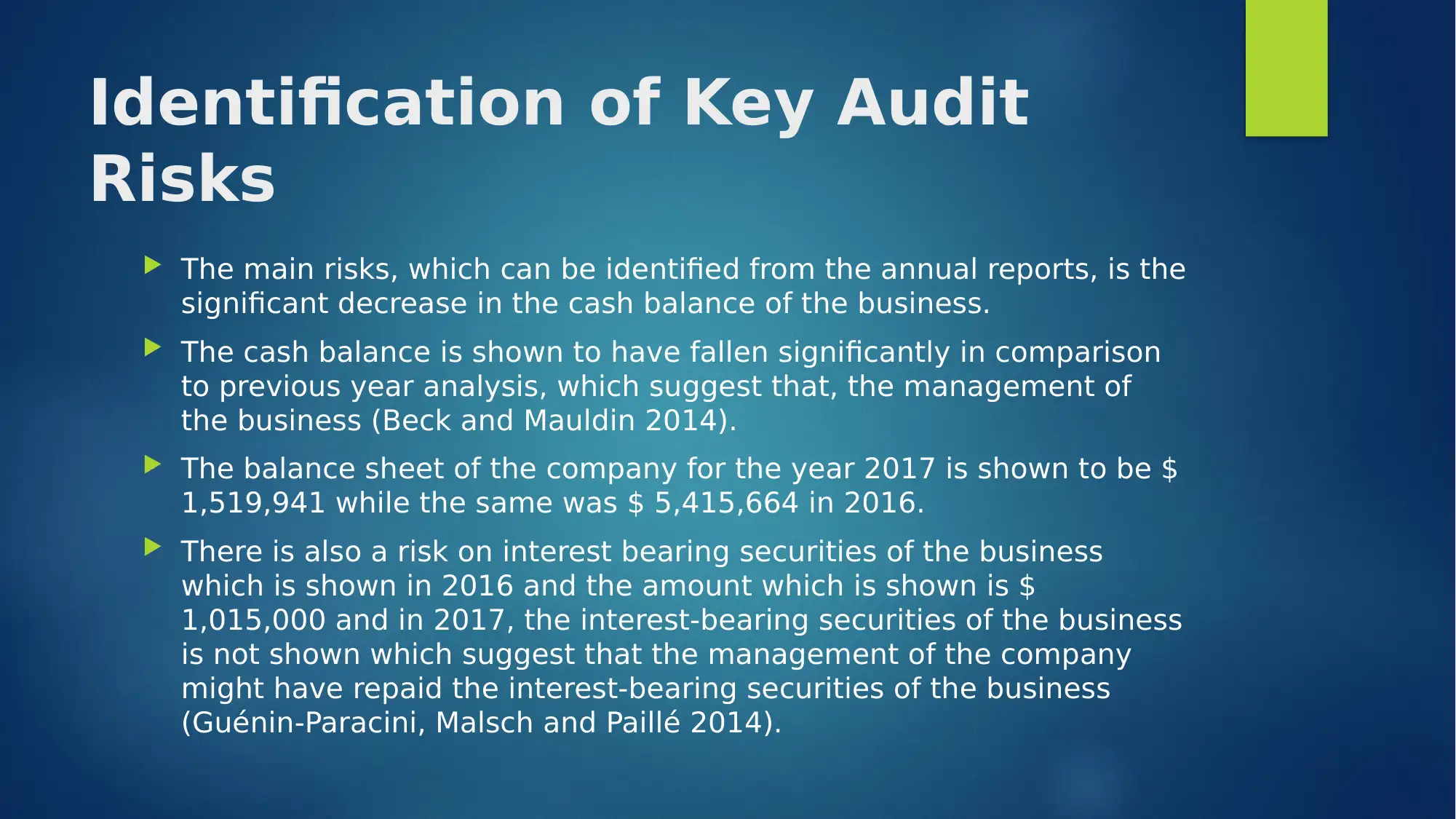

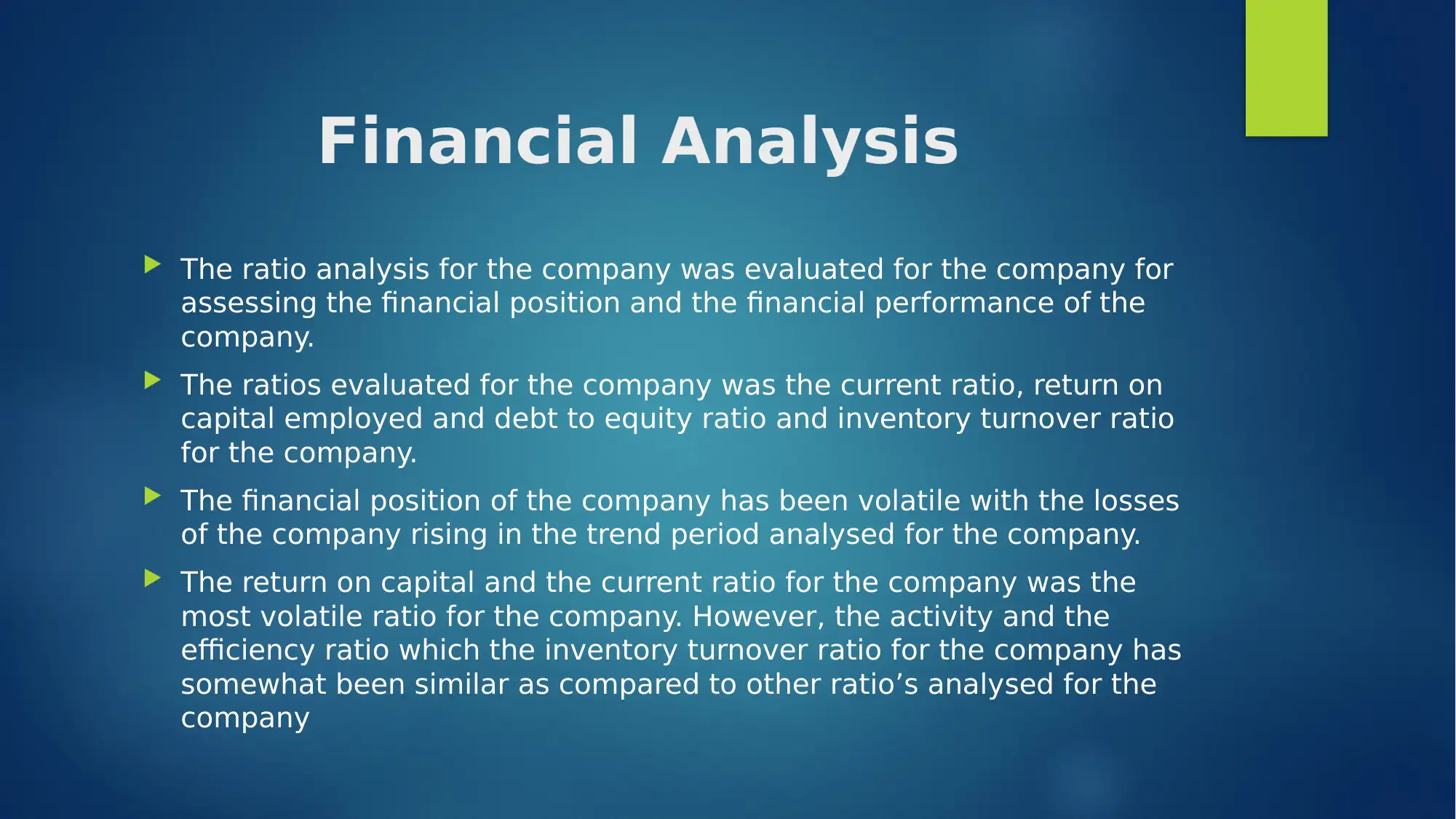

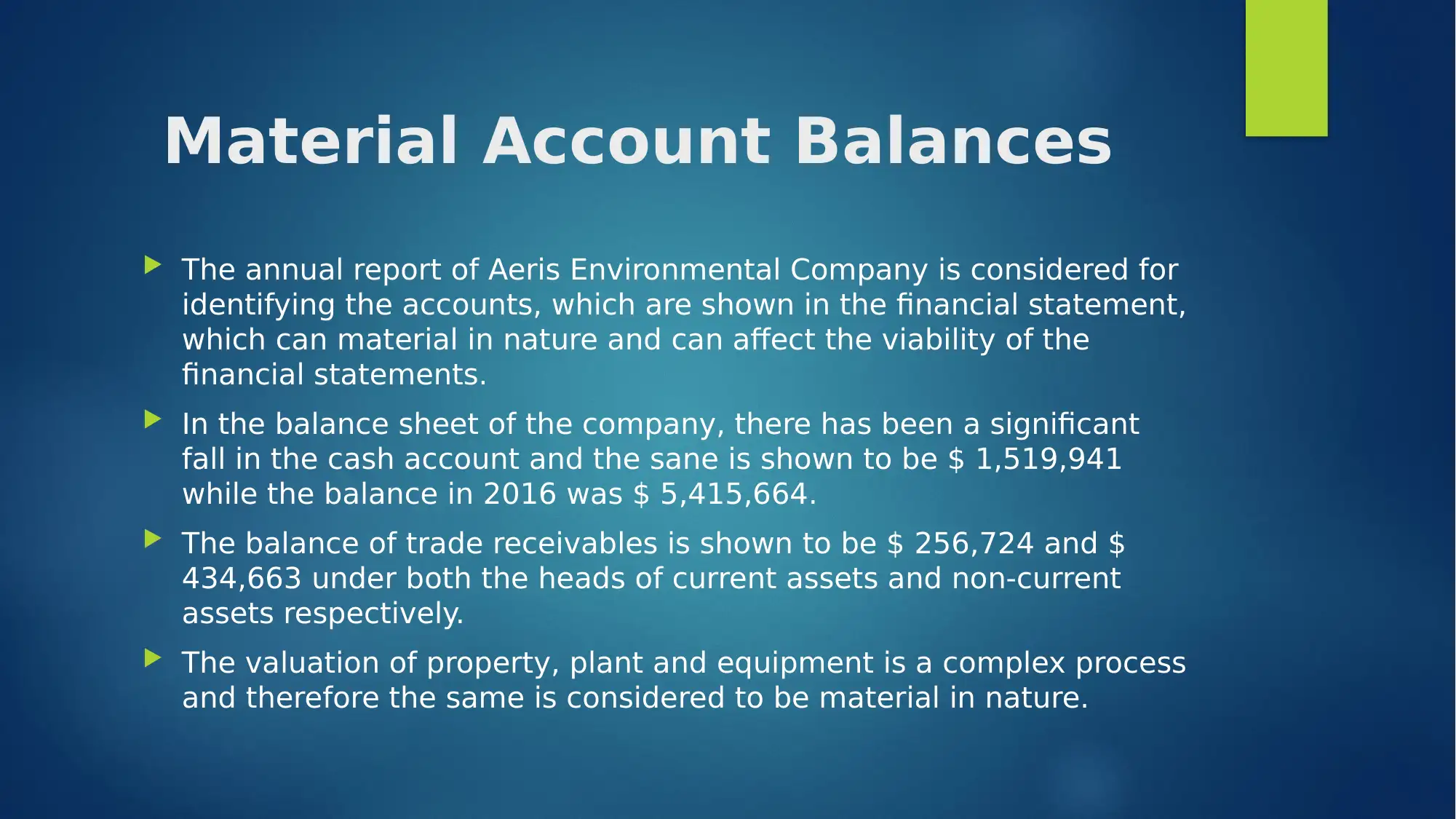

This report provides a detailed audit program for Aeris Environmental Ltd, examining the company's financial statements and key accounts. It identifies significant decreases in cash balance and other potential risks, such as interest-bearing securities. The report includes a comprehensive financial analysis using ratio analysis to assess the company's financial position and performance, highlighting volatile trends in profitability and efficiency ratios. It focuses on material account balances like cash, trade receivables, and property, plant, and equipment, along with key assertions for each. The audit steps cover verification of cash books, ledgers, and internal controls, as well as an outline of the sampling plan based on risk assessment and materiality. The document references several auditing sources and provides a thorough framework for auditing Aeris Environmental Ltd's financial activities. This report is designed to help students understand audit procedures, risk assessment, and financial statement analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.