Financial Performance Analysis: Allegiance Coal Limited Audit Report

VerifiedAdded on 2021/06/16

|16

|3535

|21

Report

AI Summary

This report provides a comprehensive analysis of Allegiance Coal Limited, focusing on its operations within the Australian mining industry. It examines the company's business risks, including cash optimization, access to capital, joint ventures, and energy costs, and highlights concerns regarding liabilities, subsidiary financial results, and sales revenue. The report assesses Allegiance's financial performance, evaluating liquidity, profitability, and efficiency, and comments on its overall financial position. Additionally, it discusses relevant reporting requirements for Australian mining companies, such as the Offshore Minerals Act, Mineral Titles Act, Planning and Development Act, and Mineral Resources Development Act. The report concludes by evaluating the feasibility of conducting an audit of Allegiance Coal Limited, emphasizing the need for a thorough review of financial accounts to ensure the accuracy of the annual report.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

Executive Summary:........................................................................................................................2

1. Overview of the operations and industry of Allegiance Coal Limited:.......................................3

2. Four specific reporting requirements for the Australian mining companies:..............................4

3. Four significant business risks for Allegiance Coal Limited:.....................................................6

4. Three areas/accounts of concern for Allegiance Coal Limited:..................................................8

5. Comment on the financial performance of Allegiance Coal Limited:........................................9

5.1 Liquidity:.............................................................................................................................10

5.2 Profitability:.........................................................................................................................12

5.3 Efficiency:............................................................................................................................12

5.4 Overall financial position:...................................................................................................13

6. Evaluating of whether the audit work of Allegiance Coal Limited would be undertaken:.......13

References:....................................................................................................................................14

Table of Contents

Executive Summary:........................................................................................................................2

1. Overview of the operations and industry of Allegiance Coal Limited:.......................................3

2. Four specific reporting requirements for the Australian mining companies:..............................4

3. Four significant business risks for Allegiance Coal Limited:.....................................................6

4. Three areas/accounts of concern for Allegiance Coal Limited:..................................................8

5. Comment on the financial performance of Allegiance Coal Limited:........................................9

5.1 Liquidity:.............................................................................................................................10

5.2 Profitability:.........................................................................................................................12

5.3 Efficiency:............................................................................................................................12

5.4 Overall financial position:...................................................................................................13

6. Evaluating of whether the audit work of Allegiance Coal Limited would be undertaken:.......13

References:....................................................................................................................................14

2AUDITING AND ASSURANCE

Executive Summary:

The current report aims to deal with evaluating the current standing of Allegiance Coal

Limited in the mining industry of Australia. It has been evaluated that the revenue of this sector

has declined over the past five years despite the rise in output. With the surge in global

development, most of the Australian mining organisations invested in new projects leading to

increase in capital investments and mining volumes. However, the rising supply has resulted in

significant price fall in for various division products in the past five years. Moreover, the

organisation is prone to certain business risks like cash optimisation, access to capital, access to

energy and joint venture agreements. Significant concerns are inherent in its annual report in

terms of liabilities, sales revenue and financial results of its subsidiary. Based on the financial

analysis, it has been assessed that Allegiance is struggling to sustain in the market due to

negative profit level and inability to raise funds through debt. Even though the audit work of

Allegiance Limited could be undertaken, the auditor needs to have a thorough review of all the

accounts, income and expenses for ensuring the validity of the financial information in the

annual report.

Executive Summary:

The current report aims to deal with evaluating the current standing of Allegiance Coal

Limited in the mining industry of Australia. It has been evaluated that the revenue of this sector

has declined over the past five years despite the rise in output. With the surge in global

development, most of the Australian mining organisations invested in new projects leading to

increase in capital investments and mining volumes. However, the rising supply has resulted in

significant price fall in for various division products in the past five years. Moreover, the

organisation is prone to certain business risks like cash optimisation, access to capital, access to

energy and joint venture agreements. Significant concerns are inherent in its annual report in

terms of liabilities, sales revenue and financial results of its subsidiary. Based on the financial

analysis, it has been assessed that Allegiance is struggling to sustain in the market due to

negative profit level and inability to raise funds through debt. Even though the audit work of

Allegiance Limited could be undertaken, the auditor needs to have a thorough review of all the

accounts, income and expenses for ensuring the validity of the financial information in the

annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

1. Overview of the operations and industry of Allegiance Coal Limited:

Operations of Allegiance Coal Limited:

Allegiance Coal Limited is listed on the Australian Stock Exchange with a ticker symbol

of AHQ. The organisation is involved in acquiring and exploring for metallurgical coal

tenements. The primary investment focus of Allegiance includes advanced, near producing

projects or production in nations having sound records of investment and minimised level of

political risk. The organisation considers the capital expenditure in its projects seriously for

assuring that they sit at the back end of the cost curve (Allegiancecoal.com.au 2018). Finally, it

is committed to the formation of effective working relationships with indigenous individuals,

with whom the organisation is associated for the projects.

Industry overview of the Australian mining industry:

Due to the huge supply of hydrocarbon, mineral and non-mineral reserves, the mining

companies in Australia extract, develop and sell these reserves. Since these resources are of

greater quality, they help in maintaining global price competitiveness of the mining division. The

sector is reliant mainly on export and nearly 70% of the overall revenues have been earned in

2017 from exports (Ibisworld.com.au 2018). This is due to the industrialisation of the global

nations like India and China driving demand for natural resources. However, the revenue of this

sector has declined over the past five years despite the rise in output. With the surge in global

development, most of the Australian mining organisations invested in new projects leading to

increase in capital investments and mining volumes. However, the rising supply has resulted in

significant price fall in for various division products in the past five years. Hence, it could be

1. Overview of the operations and industry of Allegiance Coal Limited:

Operations of Allegiance Coal Limited:

Allegiance Coal Limited is listed on the Australian Stock Exchange with a ticker symbol

of AHQ. The organisation is involved in acquiring and exploring for metallurgical coal

tenements. The primary investment focus of Allegiance includes advanced, near producing

projects or production in nations having sound records of investment and minimised level of

political risk. The organisation considers the capital expenditure in its projects seriously for

assuring that they sit at the back end of the cost curve (Allegiancecoal.com.au 2018). Finally, it

is committed to the formation of effective working relationships with indigenous individuals,

with whom the organisation is associated for the projects.

Industry overview of the Australian mining industry:

Due to the huge supply of hydrocarbon, mineral and non-mineral reserves, the mining

companies in Australia extract, develop and sell these reserves. Since these resources are of

greater quality, they help in maintaining global price competitiveness of the mining division. The

sector is reliant mainly on export and nearly 70% of the overall revenues have been earned in

2017 from exports (Ibisworld.com.au 2018). This is due to the industrialisation of the global

nations like India and China driving demand for natural resources. However, the revenue of this

sector has declined over the past five years despite the rise in output. With the surge in global

development, most of the Australian mining organisations invested in new projects leading to

increase in capital investments and mining volumes. However, the rising supply has resulted in

significant price fall in for various division products in the past five years. Hence, it could be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

said that the main success factors for the Australian mining industry include resource

availability, proximity to transport and effective controls related to cost.

2. Four specific reporting requirements for the Australian mining companies:

There are certain specific reporting requirements for the mining organisations in

Australia and they are elucidated briefly as follows:

Offshore Minerals Act 1999 and Mining Act:

According to this act, the offshore mining regulation needs to be restricted to the area,

which is outside the coastal waters of the state. In addition, it could be observed that a

corporation could not explore and recover minerals from the coastal waters, unless a licence or

special purpose content authorises such exploration or recovery. Any violation of this rule might

impose penalty on the organisation up to $30,000 (Legislation.nsw.gov.au 2018). The mining

companies need to consider the environmental concerns before exploration and recovery. In

other words, they need to ensure protection to the fisheries and scenic attractions in the areas of

exploration. Moreover, the Australian government often appoints inspectors to conduct

compliance inspection for examining stuffs utilised for mining or exploration purposes like

equipment and documents. These are carried out for assuring that the Australian mining

companies are abiding by the regulations laid down in the Act.

Mineral Titles Act 2010:

This particular act aims to develop a framework in order to grant and regulate mineral

titles, which authorise exploration, extraction and processing of minerals and related products. In

addition, another aim of this act is to help in commercialising activities conducted under mineral

said that the main success factors for the Australian mining industry include resource

availability, proximity to transport and effective controls related to cost.

2. Four specific reporting requirements for the Australian mining companies:

There are certain specific reporting requirements for the mining organisations in

Australia and they are elucidated briefly as follows:

Offshore Minerals Act 1999 and Mining Act:

According to this act, the offshore mining regulation needs to be restricted to the area,

which is outside the coastal waters of the state. In addition, it could be observed that a

corporation could not explore and recover minerals from the coastal waters, unless a licence or

special purpose content authorises such exploration or recovery. Any violation of this rule might

impose penalty on the organisation up to $30,000 (Legislation.nsw.gov.au 2018). The mining

companies need to consider the environmental concerns before exploration and recovery. In

other words, they need to ensure protection to the fisheries and scenic attractions in the areas of

exploration. Moreover, the Australian government often appoints inspectors to conduct

compliance inspection for examining stuffs utilised for mining or exploration purposes like

equipment and documents. These are carried out for assuring that the Australian mining

companies are abiding by the regulations laid down in the Act.

Mineral Titles Act 2010:

This particular act aims to develop a framework in order to grant and regulate mineral

titles, which authorise exploration, extraction and processing of minerals and related products. In

addition, another aim of this act is to help in commercialising activities conducted under mineral

5AUDITING AND ASSURANCE

titles by authorising the formation and switch over of title interests. Furthermore, this act deals

with the authorisation of other activities associated with minerals and mineral-related products to

be carried out in the absence of mineral titles (Legislation.nt.gov.au 2018). The entities are

needed to conduct preliminary exploration of land for finding out whether the land is potential

enough for future exploration of minerals and other related products. Such exploration might

constitute of investigating the geographical characteristics or air-borne geo-scientific survey with

prior approval. For such exploration, the mining companies could not use metal detectors;

instead, hand-held and non-mechanical tools could be used.

Planning and Development Act 2007:

The aim of this act is to provide planning and land system contributing to the sustainable

and orderly development of the act. This system is formulated in accordance with effective

financial principles. Thus, it becomes necessary for the Australian mining companies to ensure

sustainable development while carrying out their mining operations. According to this act,

sustainable development indicates the sound integration of environmental, economic and social

considerations in the processes of decision-making, which could be accomplished with inter-

generational equity principle and precautionary principle (Legislation.act.gov.au 2018). The first

principle states that the present generation is required to ensure health, productivity and diversity

for the upcoming generations. On the other hand, the second principle states that if there is

possibility of serious environmental damage, lack of overall economic certainty need not be used

as a cause to postpone measures for restricting environmental degradation. Hence, the mining

companies need to take into account these principles while performing their exploration and

recovery work.

titles by authorising the formation and switch over of title interests. Furthermore, this act deals

with the authorisation of other activities associated with minerals and mineral-related products to

be carried out in the absence of mineral titles (Legislation.nt.gov.au 2018). The entities are

needed to conduct preliminary exploration of land for finding out whether the land is potential

enough for future exploration of minerals and other related products. Such exploration might

constitute of investigating the geographical characteristics or air-borne geo-scientific survey with

prior approval. For such exploration, the mining companies could not use metal detectors;

instead, hand-held and non-mechanical tools could be used.

Planning and Development Act 2007:

The aim of this act is to provide planning and land system contributing to the sustainable

and orderly development of the act. This system is formulated in accordance with effective

financial principles. Thus, it becomes necessary for the Australian mining companies to ensure

sustainable development while carrying out their mining operations. According to this act,

sustainable development indicates the sound integration of environmental, economic and social

considerations in the processes of decision-making, which could be accomplished with inter-

generational equity principle and precautionary principle (Legislation.act.gov.au 2018). The first

principle states that the present generation is required to ensure health, productivity and diversity

for the upcoming generations. On the other hand, the second principle states that if there is

possibility of serious environmental damage, lack of overall economic certainty need not be used

as a cause to postpone measures for restricting environmental degradation. Hence, the mining

companies need to take into account these principles while performing their exploration and

recovery work.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

Mineral Resources Development Act 1995:

This act aims for the progress of mineral resources which is consistent with effective

environmental, economic and land use management. The mining companies of the nation need to

use effective equipment and machinery for extracting and processing minerals. The intention

would be to ensure the environmental protection and limit land or soil erosion (Mrt.tas.gov.au

2018). The Tasmanian Mineral Resources is involved in administering the approval of ongoing

works, exploration and special exploration licences, production licences, retention licences along

with mining leases for ensuring the safety of the overall community.

3. Four significant business risks for Allegiance Coal Limited:

The four significant business risks that could be identified in the context of Allegiance

Coal Limited are summarised as follows:

Cash optimisation:

The unpredicted volatility of the market and the change in the prices of the mineral

products result in uncertainty, which signifies risk (Boskou, Kirkos and Spathis 2018).

Allegiance Coal Limited is confronted with rising challenge to plan for the long-term due to the

limited visibility of demand and price. Such change could place the balance sheet statement of

the organisation in risk, which might eventually lead to material misstatement. In this case, cash

could be used for managing the liquidity of the balance sheet with the help of sustainable cost

minimisations; however, they need not dissolve value. Such minimisations need to raise

concentration on working capital along with enhancing the effectiveness of capital.

Access to capital:

Mineral Resources Development Act 1995:

This act aims for the progress of mineral resources which is consistent with effective

environmental, economic and land use management. The mining companies of the nation need to

use effective equipment and machinery for extracting and processing minerals. The intention

would be to ensure the environmental protection and limit land or soil erosion (Mrt.tas.gov.au

2018). The Tasmanian Mineral Resources is involved in administering the approval of ongoing

works, exploration and special exploration licences, production licences, retention licences along

with mining leases for ensuring the safety of the overall community.

3. Four significant business risks for Allegiance Coal Limited:

The four significant business risks that could be identified in the context of Allegiance

Coal Limited are summarised as follows:

Cash optimisation:

The unpredicted volatility of the market and the change in the prices of the mineral

products result in uncertainty, which signifies risk (Boskou, Kirkos and Spathis 2018).

Allegiance Coal Limited is confronted with rising challenge to plan for the long-term due to the

limited visibility of demand and price. Such change could place the balance sheet statement of

the organisation in risk, which might eventually lead to material misstatement. In this case, cash

could be used for managing the liquidity of the balance sheet with the help of sustainable cost

minimisations; however, they need not dissolve value. Such minimisations need to raise

concentration on working capital along with enhancing the effectiveness of capital.

Access to capital:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

The mining companies often encounter significant issues when it comes to raising capital.

As pointed out by Carson, Fargher and Zhang (2016), the overall capital that the mining

companies had raised in 2015 was 10% lower year-over-year (YOY). In addition, the loan

funding to the sector has been falling as well. Allegiance has obtained such loans previously and

it has been engaged in reusing them for improving its current infrastructure rather than investing

in new projects. Even though it has guaranteed security for backing the debt, it has been faced

difficulties for obtaining further bank loans. As a result, certain amount of interest expense needs

to be included in the income statement out of the debt security and any inaccurate estimation

could eventually lead to material misstatement. Thus, Allegiance is required to look for

alternative sources of finance along with realigning portfolios for overcoming this challenge.

Joint ventures:

If the joint venture agreements are managed effectively, it could result in providing

greater value to the stakeholders (Fuhrmann et al. 2017). These ventures could improve the

portfolio values and in few instances, they could enable in providing access to reserves and

capabilities. This denotes that risks could arise in relation to reserves and any wrong estimation

would result in loss of time and money for the organisation. As observed from the annual report

of Allegiance in 2017, it has entered into joint venture agreement with JOGMEC, from which it

has realised $31,590 from this venture and it is depicted under cash flow from investing

activities. This amount, if wrongly estimated, could result in material misstatement for the

organisation.

Access to energy:

The mining companies often encounter significant issues when it comes to raising capital.

As pointed out by Carson, Fargher and Zhang (2016), the overall capital that the mining

companies had raised in 2015 was 10% lower year-over-year (YOY). In addition, the loan

funding to the sector has been falling as well. Allegiance has obtained such loans previously and

it has been engaged in reusing them for improving its current infrastructure rather than investing

in new projects. Even though it has guaranteed security for backing the debt, it has been faced

difficulties for obtaining further bank loans. As a result, certain amount of interest expense needs

to be included in the income statement out of the debt security and any inaccurate estimation

could eventually lead to material misstatement. Thus, Allegiance is required to look for

alternative sources of finance along with realigning portfolios for overcoming this challenge.

Joint ventures:

If the joint venture agreements are managed effectively, it could result in providing

greater value to the stakeholders (Fuhrmann et al. 2017). These ventures could improve the

portfolio values and in few instances, they could enable in providing access to reserves and

capabilities. This denotes that risks could arise in relation to reserves and any wrong estimation

would result in loss of time and money for the organisation. As observed from the annual report

of Allegiance in 2017, it has entered into joint venture agreement with JOGMEC, from which it

has realised $31,590 from this venture and it is depicted under cash flow from investing

activities. This amount, if wrongly estimated, could result in material misstatement for the

organisation.

Access to energy:

8AUDITING AND ASSURANCE

According to Heenetigala and Armstrong (2017), energy consumption could account for

15% to 40% of the overall operating budget of a mining firm. At the time of selecting energy

price, cost is of utmost significance. Allegiance Cost Limited is no exception to this issue as

well. If cost is overstated or understated, material misstatement might arise in the income

statement of the organisation.

4. Three areas/accounts of concern for Allegiance Coal Limited:

The three most significant areas or accounts of concern for Allegiance Coal Limited

constitute of the following:

Liabilities:

Significant concern is inherent in the liability stated in the balance sheet statement of the

organisation. This is because the overall liability base of Allegiance Coal Limited might be

understated, since it has not recognised or disclosed any provision in its financial statements. In

addition, the disclosures related to contingencies might not adequately disclose the exact net

amount to be recovered from the tax authority. Furthermore, it has been identified that the

organisation does not have any long-term borrowings, which is another concern to carry out its

audit work.

Financial results of subsidiary:

There is high chance that the financial results of the subsidiary, Telkwa Coal Limited

might be manipulated. The aim might be to impact the market value of the shares prior to the

sale of the transaction (Simnett, Carson and Vanstraelen 2016). Thus, it could be stated that the

organisation might not have estimated properly the overall worth of the subsidiary.

According to Heenetigala and Armstrong (2017), energy consumption could account for

15% to 40% of the overall operating budget of a mining firm. At the time of selecting energy

price, cost is of utmost significance. Allegiance Cost Limited is no exception to this issue as

well. If cost is overstated or understated, material misstatement might arise in the income

statement of the organisation.

4. Three areas/accounts of concern for Allegiance Coal Limited:

The three most significant areas or accounts of concern for Allegiance Coal Limited

constitute of the following:

Liabilities:

Significant concern is inherent in the liability stated in the balance sheet statement of the

organisation. This is because the overall liability base of Allegiance Coal Limited might be

understated, since it has not recognised or disclosed any provision in its financial statements. In

addition, the disclosures related to contingencies might not adequately disclose the exact net

amount to be recovered from the tax authority. Furthermore, it has been identified that the

organisation does not have any long-term borrowings, which is another concern to carry out its

audit work.

Financial results of subsidiary:

There is high chance that the financial results of the subsidiary, Telkwa Coal Limited

might be manipulated. The aim might be to impact the market value of the shares prior to the

sale of the transaction (Simnett, Carson and Vanstraelen 2016). Thus, it could be stated that the

organisation might not have estimated properly the overall worth of the subsidiary.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Sales revenue:

It has been observed that the sales revenue of the organisation is significantly lower in

both 2016 and 2017. The organisation currently realises sales revenue based on estimates in

respect of its exploration sites. Such estimate could be biased and it might not be dependent on

realistic assumptions in relation to the sales price. As a result, the impact of provisional pricing

and any revisions in future might not be revealed adequately in the financial statements (Soh and

Martinov-Bennie 2015).

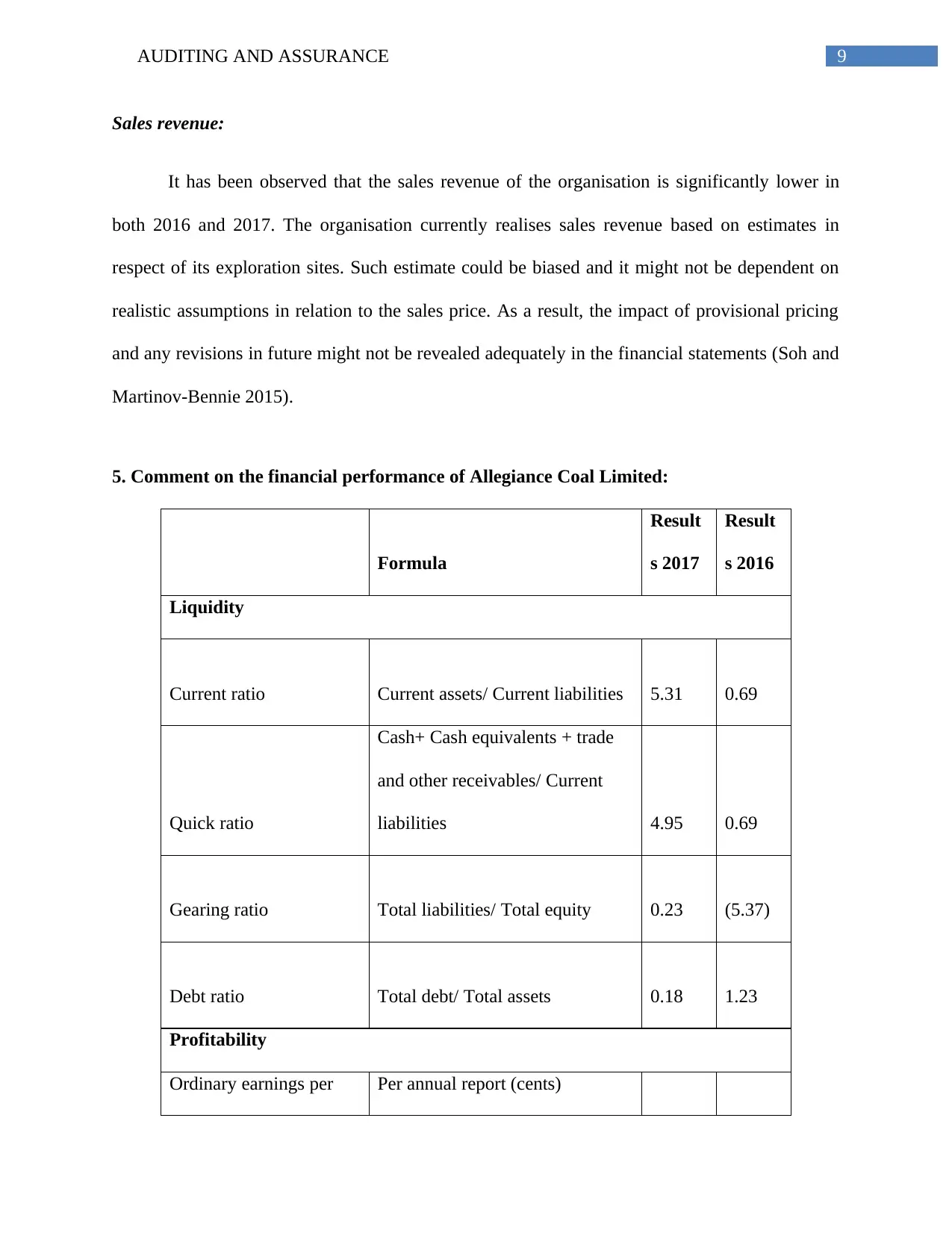

5. Comment on the financial performance of Allegiance Coal Limited:

Formula

Result

s 2017

Result

s 2016

Liquidity

Current ratio Current assets/ Current liabilities 5.31 0.69

Quick ratio

Cash+ Cash equivalents + trade

and other receivables/ Current

liabilities 4.95 0.69

Gearing ratio Total liabilities/ Total equity 0.23 (5.37)

Debt ratio Total debt/ Total assets 0.18 1.23

Profitability

Ordinary earnings per Per annual report (cents)

Sales revenue:

It has been observed that the sales revenue of the organisation is significantly lower in

both 2016 and 2017. The organisation currently realises sales revenue based on estimates in

respect of its exploration sites. Such estimate could be biased and it might not be dependent on

realistic assumptions in relation to the sales price. As a result, the impact of provisional pricing

and any revisions in future might not be revealed adequately in the financial statements (Soh and

Martinov-Bennie 2015).

5. Comment on the financial performance of Allegiance Coal Limited:

Formula

Result

s 2017

Result

s 2016

Liquidity

Current ratio Current assets/ Current liabilities 5.31 0.69

Quick ratio

Cash+ Cash equivalents + trade

and other receivables/ Current

liabilities 4.95 0.69

Gearing ratio Total liabilities/ Total equity 0.23 (5.37)

Debt ratio Total debt/ Total assets 0.18 1.23

Profitability

Ordinary earnings per Per annual report (cents)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

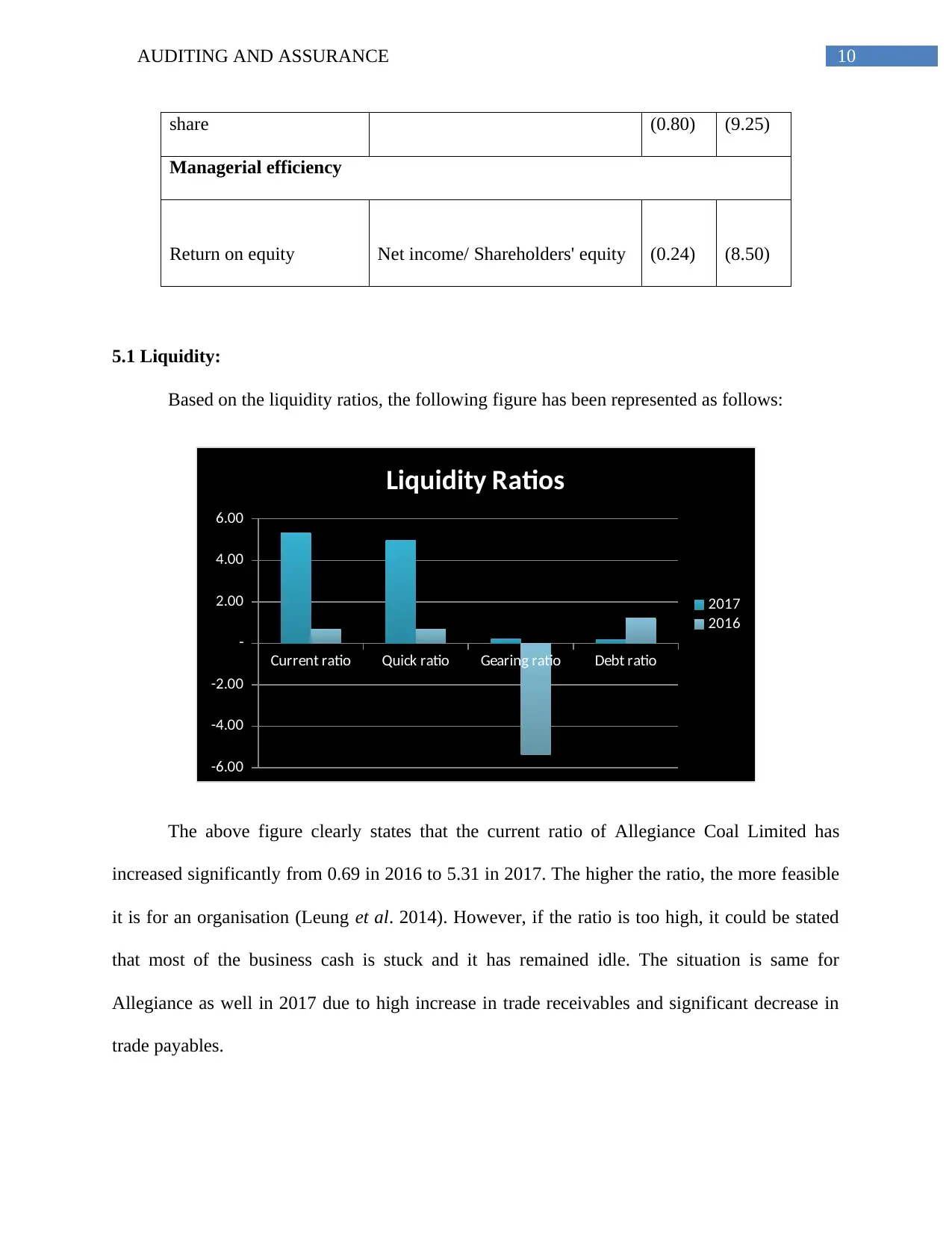

share (0.80) (9.25)

Managerial efficiency

Return on equity Net income/ Shareholders' equity (0.24) (8.50)

5.1 Liquidity:

Based on the liquidity ratios, the following figure has been represented as follows:

Current ratio Quick ratio Gearing ratio Debt ratio

-6.00

-4.00

-2.00

-

2.00

4.00

6.00

Liquidity Ratios

2017

2016

The above figure clearly states that the current ratio of Allegiance Coal Limited has

increased significantly from 0.69 in 2016 to 5.31 in 2017. The higher the ratio, the more feasible

it is for an organisation (Leung et al. 2014). However, if the ratio is too high, it could be stated

that most of the business cash is stuck and it has remained idle. The situation is same for

Allegiance as well in 2017 due to high increase in trade receivables and significant decrease in

trade payables.

share (0.80) (9.25)

Managerial efficiency

Return on equity Net income/ Shareholders' equity (0.24) (8.50)

5.1 Liquidity:

Based on the liquidity ratios, the following figure has been represented as follows:

Current ratio Quick ratio Gearing ratio Debt ratio

-6.00

-4.00

-2.00

-

2.00

4.00

6.00

Liquidity Ratios

2017

2016

The above figure clearly states that the current ratio of Allegiance Coal Limited has

increased significantly from 0.69 in 2016 to 5.31 in 2017. The higher the ratio, the more feasible

it is for an organisation (Leung et al. 2014). However, if the ratio is too high, it could be stated

that most of the business cash is stuck and it has remained idle. The situation is same for

Allegiance as well in 2017 due to high increase in trade receivables and significant decrease in

trade payables.

11AUDITING AND ASSURANCE

Quick ratio, on the other hand, is a better measure of liquidity, since it excludes the

amount of inventory while evaluating the overall business performance (Moroney and Trotman

2016). In case of Allegiance, the same trend is observed as in case of current ratio, since the

organisation has extended its receivable terms. As a result, large amount of cash has remained

with the debtors.

The gearing ratio of the organisation has improved highly in 2017; however, it could be

observed that equity is used for funding majority of its business operations and projects. This is

because it has failed to obtain short-term debts from banks because of the significantly lower net

income and revenue earning capacity. As a result, it needs to pay greater dividends to its

shareholders for retaining them in order to fund its business operations and upcoming capital

projects.

Finally, it could be observed that the debt ratio of the organisation has declined

significantly from 1.23 in 2016 to 0.18 in 2017. This is because of the significant increase in

non-current assets, especially exploration and evaluation along with significant decline in short-

term borrowings. Hence, it could be inferred that Allegiance Coal Limited is going through a

poor liquidity position in the Australian market.

Quick ratio, on the other hand, is a better measure of liquidity, since it excludes the

amount of inventory while evaluating the overall business performance (Moroney and Trotman

2016). In case of Allegiance, the same trend is observed as in case of current ratio, since the

organisation has extended its receivable terms. As a result, large amount of cash has remained

with the debtors.

The gearing ratio of the organisation has improved highly in 2017; however, it could be

observed that equity is used for funding majority of its business operations and projects. This is

because it has failed to obtain short-term debts from banks because of the significantly lower net

income and revenue earning capacity. As a result, it needs to pay greater dividends to its

shareholders for retaining them in order to fund its business operations and upcoming capital

projects.

Finally, it could be observed that the debt ratio of the organisation has declined

significantly from 1.23 in 2016 to 0.18 in 2017. This is because of the significant increase in

non-current assets, especially exploration and evaluation along with significant decline in short-

term borrowings. Hence, it could be inferred that Allegiance Coal Limited is going through a

poor liquidity position in the Australian market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.