Comprehensive Audit Report on Azure Enterprises' Financial Statements

VerifiedAdded on 2023/06/05

|12

|2130

|226

Report

AI Summary

This report presents an audit assessment of Azure Enterprises' trial balance, focusing on areas requiring detailed examination and relevant audit procedures. It emphasizes the importance of adequate audit evidence in forming opinions on financial statements. The report includes an executive summary that highlights the significance of risk analysis in audit planning, covering aspects like client understanding, internal controls, IT environment, corporate governance, and closing processes. Trend analysis is used to identify significant accounts, such as cost of sales, other income, and depreciation, each discussed with appropriate audit procedures. The report also addresses fraud risk, emphasizing the need for professional skepticism and caution against relying solely on management's trustworthiness. It concludes that auditors must make thorough inquiries and critically assess evidence before forming opinions on financial statements, referencing ASA 315 and other relevant literature.

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To,

Respected Sir,

Audit Senior

Present report relates to audit assessment of the trial balance of Azure Enterprises as

requested by you. The report specifies the area which requires to be emphasized in more

detail along with the audit procedures required to be applied on same. It can be concluded

that adequate, appropriate audit evidence is necessary for forming an opinion on financial

statements.

Yours sincerely.

Respected Sir,

Audit Senior

Present report relates to audit assessment of the trial balance of Azure Enterprises as

requested by you. The report specifies the area which requires to be emphasized in more

detail along with the audit procedures required to be applied on same. It can be concluded

that adequate, appropriate audit evidence is necessary for forming an opinion on financial

statements.

Yours sincerely.

AUDIT PLANNING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Executive Summary

By comprehending the significance of risk analysis, an auditor can plan their inspection to

invest more time in the areas where the risks are maximum. In addition to this during the

period of planning, an auditor should assess about the client, their client’s internal controls,

information technology environment of their client, corporate governance of their client and

closing process of the client. Present report analyzes the trial balance of Azure Enterprises in

order to ascertain those accounts which require significant audit analysis. The accounts which

have been assessed to be significant on the basis of trend analysis have been explained along

with appropriate audit procedure. It can be concluded from the present analysis that an

auditor necessarily requires audit evidence along with management trustworthiness in order

to make a decision that whether fraud variant exists in books of accounts or not.

By comprehending the significance of risk analysis, an auditor can plan their inspection to

invest more time in the areas where the risks are maximum. In addition to this during the

period of planning, an auditor should assess about the client, their client’s internal controls,

information technology environment of their client, corporate governance of their client and

closing process of the client. Present report analyzes the trial balance of Azure Enterprises in

order to ascertain those accounts which require significant audit analysis. The accounts which

have been assessed to be significant on the basis of trend analysis have been explained along

with appropriate audit procedure. It can be concluded from the present analysis that an

auditor necessarily requires audit evidence along with management trustworthiness in order

to make a decision that whether fraud variant exists in books of accounts or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction................................................................................................................................6

Discussions.................................................................................................................................6

(a) Assessment of materiality set for Azure Enterprises........................................................6

(b) Analytical Review of Income Statement of Azure Ltd through trend analysis:...............7

(c) Accounts subject to significant audit testing....................................................................8

(d) Audit procedure of accounts require significant audit testing..........................................9

(e) Comment on suggestion relating to fraud risk................................................................10

Conclusion................................................................................................................................10

Introduction................................................................................................................................6

Discussions.................................................................................................................................6

(a) Assessment of materiality set for Azure Enterprises........................................................6

(b) Analytical Review of Income Statement of Azure Ltd through trend analysis:...............7

(c) Accounts subject to significant audit testing....................................................................8

(d) Audit procedure of accounts require significant audit testing..........................................9

(e) Comment on suggestion relating to fraud risk................................................................10

Conclusion................................................................................................................................10

INTRODUCTION

ASA 315 “Identifying and Assessing the Risk of Material Misstatement through

understanding the entity and its environment” specifies the responsibilities of Auditor

regarding determining and evaluation of risk of material misstatement in the financial

statement by comprehending the environment of any individual including individual’s

internal control (ASA 315. Understanding the Entity and Its Environment and assessing the

risk of material misstatement, 2017.). Present report revolves around audit procedure which

has been applied to assess the trial balance of Azure Enterprises. Further, trend analysis has

been applied in order to ascertain the accounts which require detail assessment. The report

ends up with discussion relating to variants which should be analyzed in order to ascertain an

indication of fraud in financial statements.

DISCUSSIONS

(a) Assessment of materiality set for Azure Enterprises

At the time of planning and reporting, the auditor takes a wide view of the client as a whole

and the diligence in which it functions. Further, information related to the client is achieved

in the early stages of every audit, and that information impels the planning of the audit. The

concept of materiality is applied by an auditor as planning as well as performing audit in

order to analyze the impact of ascertained misstatement if any in financial statement so that

appropriate opinion can be formed in auditor’s report. (Griffiths, 2016). According to

Beasley, et al. (2018) concept of materiality recognizes that transactions or accounts which

individually or in aggregate have significant impact on the true and fair opinion relating to

books of account of an organization.

It can be accessed from the Trial Balance that the total sales for the year ending 2016 of

Azure Enterprise of the year are 162499.99 which means that transactions which are

important or material will be done in expressions of thousands only. Hence, the figure which

is taken as a base by the auditor that is 15000 is correct since all the significant, as well as

crucial transaction, will be amounting to around 15000 or more than that. Moreover, if the

budget is modified than in that case the new base will ascertain the accounts and transactions

which involve deep inspection.

ASA 315 “Identifying and Assessing the Risk of Material Misstatement through

understanding the entity and its environment” specifies the responsibilities of Auditor

regarding determining and evaluation of risk of material misstatement in the financial

statement by comprehending the environment of any individual including individual’s

internal control (ASA 315. Understanding the Entity and Its Environment and assessing the

risk of material misstatement, 2017.). Present report revolves around audit procedure which

has been applied to assess the trial balance of Azure Enterprises. Further, trend analysis has

been applied in order to ascertain the accounts which require detail assessment. The report

ends up with discussion relating to variants which should be analyzed in order to ascertain an

indication of fraud in financial statements.

DISCUSSIONS

(a) Assessment of materiality set for Azure Enterprises

At the time of planning and reporting, the auditor takes a wide view of the client as a whole

and the diligence in which it functions. Further, information related to the client is achieved

in the early stages of every audit, and that information impels the planning of the audit. The

concept of materiality is applied by an auditor as planning as well as performing audit in

order to analyze the impact of ascertained misstatement if any in financial statement so that

appropriate opinion can be formed in auditor’s report. (Griffiths, 2016). According to

Beasley, et al. (2018) concept of materiality recognizes that transactions or accounts which

individually or in aggregate have significant impact on the true and fair opinion relating to

books of account of an organization.

It can be accessed from the Trial Balance that the total sales for the year ending 2016 of

Azure Enterprise of the year are 162499.99 which means that transactions which are

important or material will be done in expressions of thousands only. Hence, the figure which

is taken as a base by the auditor that is 15000 is correct since all the significant, as well as

crucial transaction, will be amounting to around 15000 or more than that. Moreover, if the

budget is modified than in that case the new base will ascertain the accounts and transactions

which involve deep inspection.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

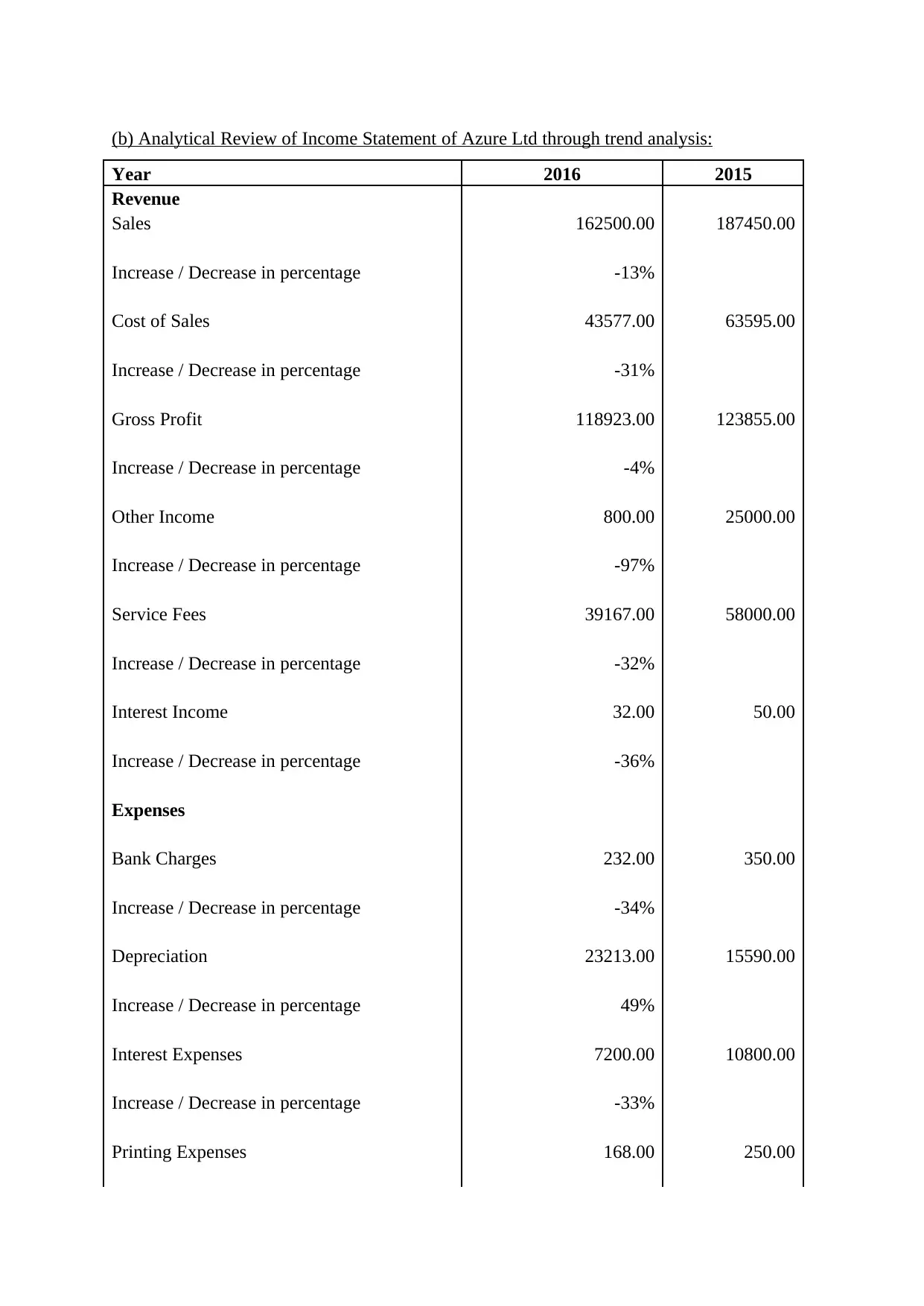

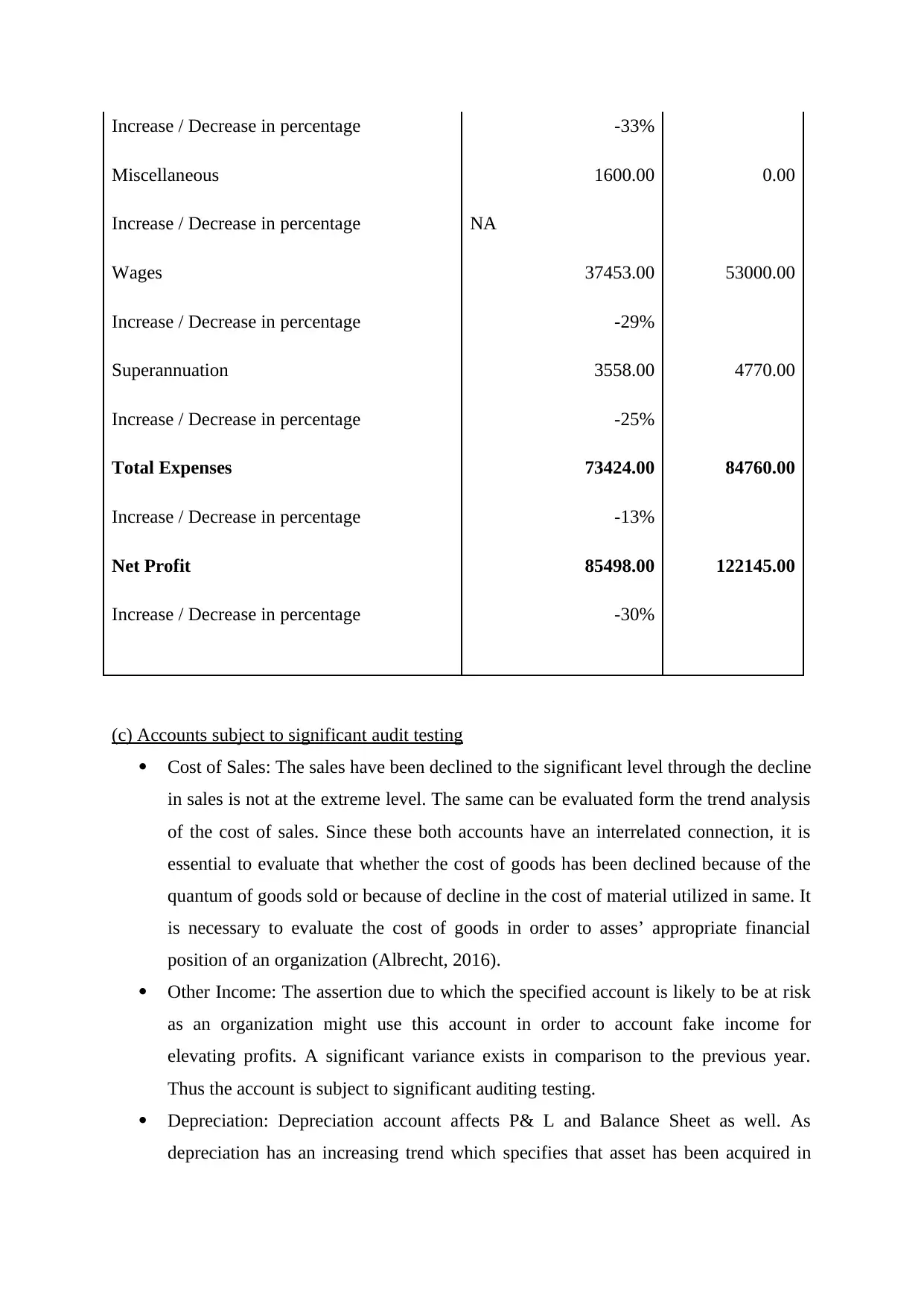

(b) Analytical Review of Income Statement of Azure Ltd through trend analysis:

Year 2016 2015

Revenue

Sales 162500.00 187450.00

Increase / Decrease in percentage -13%

Cost of Sales 43577.00 63595.00

Increase / Decrease in percentage -31%

Gross Profit 118923.00 123855.00

Increase / Decrease in percentage -4%

Other Income 800.00 25000.00

Increase / Decrease in percentage -97%

Service Fees 39167.00 58000.00

Increase / Decrease in percentage -32%

Interest Income 32.00 50.00

Increase / Decrease in percentage -36%

Expenses

Bank Charges 232.00 350.00

Increase / Decrease in percentage -34%

Depreciation 23213.00 15590.00

Increase / Decrease in percentage 49%

Interest Expenses 7200.00 10800.00

Increase / Decrease in percentage -33%

Printing Expenses 168.00 250.00

Year 2016 2015

Revenue

Sales 162500.00 187450.00

Increase / Decrease in percentage -13%

Cost of Sales 43577.00 63595.00

Increase / Decrease in percentage -31%

Gross Profit 118923.00 123855.00

Increase / Decrease in percentage -4%

Other Income 800.00 25000.00

Increase / Decrease in percentage -97%

Service Fees 39167.00 58000.00

Increase / Decrease in percentage -32%

Interest Income 32.00 50.00

Increase / Decrease in percentage -36%

Expenses

Bank Charges 232.00 350.00

Increase / Decrease in percentage -34%

Depreciation 23213.00 15590.00

Increase / Decrease in percentage 49%

Interest Expenses 7200.00 10800.00

Increase / Decrease in percentage -33%

Printing Expenses 168.00 250.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Increase / Decrease in percentage -33%

Miscellaneous 1600.00 0.00

Increase / Decrease in percentage NA

Wages 37453.00 53000.00

Increase / Decrease in percentage -29%

Superannuation 3558.00 4770.00

Increase / Decrease in percentage -25%

Total Expenses 73424.00 84760.00

Increase / Decrease in percentage -13%

Net Profit 85498.00 122145.00

Increase / Decrease in percentage -30%

(c) Accounts subject to significant audit testing

Cost of Sales: The sales have been declined to the significant level through the decline

in sales is not at the extreme level. The same can be evaluated form the trend analysis

of the cost of sales. Since these both accounts have an interrelated connection, it is

essential to evaluate that whether the cost of goods has been declined because of the

quantum of goods sold or because of decline in the cost of material utilized in same. It

is necessary to evaluate the cost of goods in order to asses’ appropriate financial

position of an organization (Albrecht, 2016).

Other Income: The assertion due to which the specified account is likely to be at risk

as an organization might use this account in order to account fake income for

elevating profits. A significant variance exists in comparison to the previous year.

Thus the account is subject to significant auditing testing.

Depreciation: Depreciation account affects P& L and Balance Sheet as well. As

depreciation has an increasing trend which specifies that asset has been acquired in

Miscellaneous 1600.00 0.00

Increase / Decrease in percentage NA

Wages 37453.00 53000.00

Increase / Decrease in percentage -29%

Superannuation 3558.00 4770.00

Increase / Decrease in percentage -25%

Total Expenses 73424.00 84760.00

Increase / Decrease in percentage -13%

Net Profit 85498.00 122145.00

Increase / Decrease in percentage -30%

(c) Accounts subject to significant audit testing

Cost of Sales: The sales have been declined to the significant level through the decline

in sales is not at the extreme level. The same can be evaluated form the trend analysis

of the cost of sales. Since these both accounts have an interrelated connection, it is

essential to evaluate that whether the cost of goods has been declined because of the

quantum of goods sold or because of decline in the cost of material utilized in same. It

is necessary to evaluate the cost of goods in order to asses’ appropriate financial

position of an organization (Albrecht, 2016).

Other Income: The assertion due to which the specified account is likely to be at risk

as an organization might use this account in order to account fake income for

elevating profits. A significant variance exists in comparison to the previous year.

Thus the account is subject to significant auditing testing.

Depreciation: Depreciation account affects P& L and Balance Sheet as well. As

depreciation has an increasing trend which specifies that asset has been acquired in

the present year. Thus, assertions are required to access whether appropriate

accounting treatment, as well as disclosure, have been provided relating to same or

not.

(d) Audit procedure of accounts require significant audit testing

Cost of sales:

The first step in auditing process of the cost of sales is operating an analytical test of

the cost of sale through the product line, division or other business section by

reference to details of units’ transmitted and average unit costs.

Subsequently, investigation of vital variations between the predicted and posted

amounts should be performed.

After this, the intensifying the vouching test of expense transaction to test linked cost

of sales transaction by tracing units costs employed to assuage inventory to costs

records tested in the inspection of stock.

Thus, as per assertions of Knechel, and Salterio, (2016) the audit procedure should be

followed rigorously from time to time so that the assessment can be done that is

whether the cost of sales has augmented or declined.

Other Income:

The first step in auditing procedure of other income is to comprehend the internal

controls and transaction cycle of income. The same will comprises meeting with

administration and learning about the accounting of other income procedure,

process and controls which the organization has implemented to guard against

loss. As per the study of Bailey, Collins and Abbott (2017), this procedure is

frequently known as design and implementation testing.

Further, along with execution of investigation of administration, auditors must

also review flowcharts related to invoice flow, ask for duplicates of vital contracts

as well as document any alteration to the income process that has to arise as the

last audit.

The procedure will get finish by mapping the internal control activities that were

recognized when learning about the internal control system to specific

administration assertion of incomes.

Depreciation:

accounting treatment, as well as disclosure, have been provided relating to same or

not.

(d) Audit procedure of accounts require significant audit testing

Cost of sales:

The first step in auditing process of the cost of sales is operating an analytical test of

the cost of sale through the product line, division or other business section by

reference to details of units’ transmitted and average unit costs.

Subsequently, investigation of vital variations between the predicted and posted

amounts should be performed.

After this, the intensifying the vouching test of expense transaction to test linked cost

of sales transaction by tracing units costs employed to assuage inventory to costs

records tested in the inspection of stock.

Thus, as per assertions of Knechel, and Salterio, (2016) the audit procedure should be

followed rigorously from time to time so that the assessment can be done that is

whether the cost of sales has augmented or declined.

Other Income:

The first step in auditing procedure of other income is to comprehend the internal

controls and transaction cycle of income. The same will comprises meeting with

administration and learning about the accounting of other income procedure,

process and controls which the organization has implemented to guard against

loss. As per the study of Bailey, Collins and Abbott (2017), this procedure is

frequently known as design and implementation testing.

Further, along with execution of investigation of administration, auditors must

also review flowcharts related to invoice flow, ask for duplicates of vital contracts

as well as document any alteration to the income process that has to arise as the

last audit.

The procedure will get finish by mapping the internal control activities that were

recognized when learning about the internal control system to specific

administration assertion of incomes.

Depreciation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For auditing the depreciation expense, the auditor must evaluate the rationality of

depreciation which individual offers to group or class of assets. The rate must be

consistency to the ability which fixed assets can provide to the inflow of economic.

Further, the inspection should evaluate the depreciation rate also which is offered by

tax authority and their comprehending.

Subsequently, the auditor should review the depreciation expenses which are

calculated by accountants in their depreciation program. After reviewing the

depreciation rate, auditors must contrast their outcomes with their client’s outcomes.

The difference must be inspected accurately.

(e) Comment on suggestion relating to fraud risk

Misstatements in the financial statement can occur from either deception or fault (Guénin et

al., 2014.). The distinctive factor among deception as well as the fault is whether the

underlying action that results in the misstatement of the financial statement is deliberated or

accidental. Professional skepticism can be referred as an attitude which comprises

questioning mind, being alert in scenarios which provide hint of possible misstatement due to

fraud or error as well as critical assessment of audit evidence. An auditor requires application

of skepticism in order to evaluate evidence and risk throughout the audit procedure. assessing

administration’s procedure for recognizing and reacting to the risks of deception in the

individual, comprising any particular risks of deception that administration has recognized or

that have been brought to its concentration, or classes of transactions, account balances or

revelations for which a risk of deception is expected to exist (McKee, 2014).

The suggestion of an audit partner is not appropriate as the decision is to take after

considering the above specified enquiries. Moreover, mere trustworthy of client staff cannot

be treated as adequate audit evidence for an opinion, as application of professional skepticism

is necessary for auditor to attain appropriate evidence.

CONCLUSION

It can be concluded from the above study that the auditor is required to make enquiries of

administration concerning prior to making a decision whether fraud risk shall be taken into

consideration or not. Further, administration evaluation of the risk that the financial statement

might be materially misstated because of deception, comprising the nature, level and rate of

such evaluations can be specified as base taken by the auditor in order to provide opinion on

financial statements of an organization.

depreciation which individual offers to group or class of assets. The rate must be

consistency to the ability which fixed assets can provide to the inflow of economic.

Further, the inspection should evaluate the depreciation rate also which is offered by

tax authority and their comprehending.

Subsequently, the auditor should review the depreciation expenses which are

calculated by accountants in their depreciation program. After reviewing the

depreciation rate, auditors must contrast their outcomes with their client’s outcomes.

The difference must be inspected accurately.

(e) Comment on suggestion relating to fraud risk

Misstatements in the financial statement can occur from either deception or fault (Guénin et

al., 2014.). The distinctive factor among deception as well as the fault is whether the

underlying action that results in the misstatement of the financial statement is deliberated or

accidental. Professional skepticism can be referred as an attitude which comprises

questioning mind, being alert in scenarios which provide hint of possible misstatement due to

fraud or error as well as critical assessment of audit evidence. An auditor requires application

of skepticism in order to evaluate evidence and risk throughout the audit procedure. assessing

administration’s procedure for recognizing and reacting to the risks of deception in the

individual, comprising any particular risks of deception that administration has recognized or

that have been brought to its concentration, or classes of transactions, account balances or

revelations for which a risk of deception is expected to exist (McKee, 2014).

The suggestion of an audit partner is not appropriate as the decision is to take after

considering the above specified enquiries. Moreover, mere trustworthy of client staff cannot

be treated as adequate audit evidence for an opinion, as application of professional skepticism

is necessary for auditor to attain appropriate evidence.

CONCLUSION

It can be concluded from the above study that the auditor is required to make enquiries of

administration concerning prior to making a decision whether fraud risk shall be taken into

consideration or not. Further, administration evaluation of the risk that the financial statement

might be materially misstated because of deception, comprising the nature, level and rate of

such evaluations can be specified as base taken by the auditor in order to provide opinion on

financial statements of an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Albrecht, C., Holland, D.V., Sanders, M.L. and Albrecht, C.C., 2016. The debilitating effects

of fraud in organizations. In Crime and Corruption in Organizations .Pp. 183-206.

Routledge.

Allen, R.D., Hermanson, D.R., Kozloski, T.M. and Ramsay, R.J., 2006. Auditor risk

assessment: Insights from the academic literature. Accounting Horizons, 20(2), pp.157-177.

ASA 315. Understanding the Entity and Its Environment and assessing risk of material

misstatement. 2017. [PDF]. Available through <

https://www.auasb.gov.au/admin/file/content102/c3/ASA_315_28-04-06.pdf>. [Accessed on

14th September 2018]

Bailey, C., Collins, D.L. and Abbott, L.J., 2017. The Impact of Enterprise Risk Management

on the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of

Practice & Theory, 37(3), pp.25-46.

Beasley, M.S., Blay, A.D., Lewellen, C. and McAllister, M., 2018. The Association Between

Board Risk Oversight and the Risk of Material Misstatement.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Guénin-Paracini, H., Malsch, B. and Paillé, A.M., 2014. Fear and risk in the audit

process. Accounting, Organizations and Society, 39(4), pp.264-288.

McKee, T.E., 2014. Evaluating financial fraud risk during audit planning. The CPA

Journal, 84(10), p.28.

Albrecht, C., Holland, D.V., Sanders, M.L. and Albrecht, C.C., 2016. The debilitating effects

of fraud in organizations. In Crime and Corruption in Organizations .Pp. 183-206.

Routledge.

Allen, R.D., Hermanson, D.R., Kozloski, T.M. and Ramsay, R.J., 2006. Auditor risk

assessment: Insights from the academic literature. Accounting Horizons, 20(2), pp.157-177.

ASA 315. Understanding the Entity and Its Environment and assessing risk of material

misstatement. 2017. [PDF]. Available through <

https://www.auasb.gov.au/admin/file/content102/c3/ASA_315_28-04-06.pdf>. [Accessed on

14th September 2018]

Bailey, C., Collins, D.L. and Abbott, L.J., 2017. The Impact of Enterprise Risk Management

on the Audit Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of

Practice & Theory, 37(3), pp.25-46.

Beasley, M.S., Blay, A.D., Lewellen, C. and McAllister, M., 2018. The Association Between

Board Risk Oversight and the Risk of Material Misstatement.

Griffiths, P., 2016. Risk-based auditing. Routledge.

Guénin-Paracini, H., Malsch, B. and Paillé, A.M., 2014. Fear and risk in the audit

process. Accounting, Organizations and Society, 39(4), pp.264-288.

McKee, T.E., 2014. Evaluating financial fraud risk during audit planning. The CPA

Journal, 84(10), p.28.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.