Detailed Financial Audit Assurance and Compliance Report Analysis

VerifiedAdded on 2020/03/13

|11

|2458

|30

Report

AI Summary

This report, focusing on audit assurance and compliance, begins with an application of analytical procedures to the financial information of DIPL, detailing how data from financial reports informs audit planning. It then identifies inherent risk factors arising from DIPL's business operations, examining how these risks can lead to material misstatements in financial reports. The report also identifies and explains key fraud risk factors related to misstatements stemming from fraudulent financial reporting, including asset loss and employee fraud. Financial ratios, such as the current and solvency ratios, are analyzed to assess DIPL's financial position. The study also highlights the impact of excessive workloads, employee pressure, and the nature of the business on the accuracy of financial reporting. This report is contributed by a student to be published on Desklib, a platform providing AI-based study tools for students; explore the content and enhance your understanding.

Running head: AUDIT ASSURANCE AND COMPLIANCE

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Audit Assurance and Compliance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT ASSURANCE AND COMPLIANCE

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................5

Reference List..................................................................................................................................8

List of Appendix............................................................................................................................10

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................3

Answer to Question 3:.....................................................................................................................5

Reference List..................................................................................................................................8

List of Appendix............................................................................................................................10

2AUDIT ASSURANCE AND COMPLIANCE

Answer to Question 1:

Application of analytical procedures to the financial report information of DIPL

The data sourced from the financial report of DIPL has been conducive in the

development of the audit plan. The planning process has been based on particular guideline

which has been undertaken as per the audit process. This has helped the assessor in considering

the audit cost and helps in the aversion of the misunderstanding of the clientele. DIPL has

considered the analytical approach with the dissemination of the information as per the financial

declarations. The primary process of the evaluation of the analytical approach has been

considered based on the specific approach for the financial declarations, financial analysts and

management accountants (Yasin and Nelson 2013).

The main consideration for the analytical approach has been further seen with the

reference point formed as per common sizing. Common sizing has been seen to be conducive in

the comparison of the financial statements as per different period in varied range of corporations.

The ratio analysis has been further compared based on the financial declarations in the planning

of the audit (Bell, Causholli and Knechel 2015).

Explanation of the way the results influence planning decisions for the audit

The various types of the decision of planning have been stated based on analytical

approach and disseminating information in the financial statements. For example the current

ratio of the various firms for DIPL has been considered as 1.42 in 2013, 1.46 in 2014 and 1.5 in

2015. The profitability factor has been considered as per the ratio, which is calculated as 0.068 in

2013, 0.60 in 2014 and 0.06 in 2015. The profitability and the profit margin of the company have

Answer to Question 1:

Application of analytical procedures to the financial report information of DIPL

The data sourced from the financial report of DIPL has been conducive in the

development of the audit plan. The planning process has been based on particular guideline

which has been undertaken as per the audit process. This has helped the assessor in considering

the audit cost and helps in the aversion of the misunderstanding of the clientele. DIPL has

considered the analytical approach with the dissemination of the information as per the financial

declarations. The primary process of the evaluation of the analytical approach has been

considered based on the specific approach for the financial declarations, financial analysts and

management accountants (Yasin and Nelson 2013).

The main consideration for the analytical approach has been further seen with the

reference point formed as per common sizing. Common sizing has been seen to be conducive in

the comparison of the financial statements as per different period in varied range of corporations.

The ratio analysis has been further compared based on the financial declarations in the planning

of the audit (Bell, Causholli and Knechel 2015).

Explanation of the way the results influence planning decisions for the audit

The various types of the decision of planning have been stated based on analytical

approach and disseminating information in the financial statements. For example the current

ratio of the various firms for DIPL has been considered as 1.42 in 2013, 1.46 in 2014 and 1.5 in

2015. The profitability factor has been considered as per the ratio, which is calculated as 0.068 in

2013, 0.60 in 2014 and 0.06 in 2015. The profitability and the profit margin of the company have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT ASSURANCE AND COMPLIANCE

been further able to reveal that the position of the net income which has been earned by the

company in compared to the net sales. Despite of this consideration, the assessor needs to

understand, if the expenses are low or high and the management team is having the necessity to

curtail the budget and time. The unfavourable and the favourable have been seen based on the

soundness in the financial position and audit assessment. Comparably in 2015 and 2013 the

solvency ratio of the company has been seen to be 0.62 and 0.21 (Lindeboom, van der Klaauw

and Vriend 2016).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The different level of the auditing factors has been considered based on the several

incidences of material misstatements in the financial announcements in a certain organisation.

The various types of the systematic and the unsystematic risk have been further seen to be based

on the financial declarations of the corporation. It has been further assessed that the risks has

been considered on both financial as well as non-financial factors. Nevertheless, an evaluator

needs to consider the detection of the various types of the risks. The risks may be further seen to

be linked with the risks interrelated to the omission and diverse errors as per the diversified

nature of the operation of business for DIPL (Giard et al. 2016).

As per the given scenario it has been seen that several transactions were omitted by the

accountants otherwise by the management of the DIPL. This can be further sequentially based on

the different types of the inconsistencies in the planning and the sales activities. The various

types of the depictions of the financial declarations has been further associated to the

accomplishment of the profit from the revenue acquired from the sales. The present analysis has

been further able to reveal that the position of the net income which has been earned by the

company in compared to the net sales. Despite of this consideration, the assessor needs to

understand, if the expenses are low or high and the management team is having the necessity to

curtail the budget and time. The unfavourable and the favourable have been seen based on the

soundness in the financial position and audit assessment. Comparably in 2015 and 2013 the

solvency ratio of the company has been seen to be 0.62 and 0.21 (Lindeboom, van der Klaauw

and Vriend 2016).

Answer to Question 2:

Identification of inherent risk factors that arise from nature of business operations of DIPL

The different level of the auditing factors has been considered based on the several

incidences of material misstatements in the financial announcements in a certain organisation.

The various types of the systematic and the unsystematic risk have been further seen to be based

on the financial declarations of the corporation. It has been further assessed that the risks has

been considered on both financial as well as non-financial factors. Nevertheless, an evaluator

needs to consider the detection of the various types of the risks. The risks may be further seen to

be linked with the risks interrelated to the omission and diverse errors as per the diversified

nature of the operation of business for DIPL (Giard et al. 2016).

As per the given scenario it has been seen that several transactions were omitted by the

accountants otherwise by the management of the DIPL. This can be further sequentially based on

the different types of the inconsistencies in the planning and the sales activities. The various

types of the depictions of the financial declarations has been further associated to the

accomplishment of the profit from the revenue acquired from the sales. The present analysis has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT ASSURANCE AND COMPLIANCE

been able to specify about the IT implementation process which has been able to state about the

different types of the concerns associated to the particular issues. DIPL corporation being short

on staff has found it difficult to handle the various types of the execution process related to the

installation process and carrying of the reconciliation and the testing process of the new

arrangement by the year end (Duncan and Whittington 2014).

The main considerations of the cash receipt have been depicted by the finance

professionals and the inherent risks associated to the concerns. The staff member has been

further able to handle the various types the associated issues which are seen to be related to the

appropriate sequence for account receivables (De George, Ferguson and Spear 2013).

Risk and way it might affect the risk of material misstatement in the financial report

The various types of the inherent risk as per material misstatements are listed below as

follows:

Excessive pressure on employees and management- The excusive workload on the staff

members has been seen to be the main cause for the deteriorating bookkeeping. The identified

attributed encountered for the poor liquidity has been based on the various types ofthe opeatin

outcomes and issues pertaining to cash flow.

Risks of errors or else incorrect misrepresentation- The intricacies identified and the erros in

the financial statement has been simultaneously misstated.

Integrity of the entire management- The management of DIPL has been essentially seen to

lack the various types of the considerations related to reputational loss for business and

community.

been able to specify about the IT implementation process which has been able to state about the

different types of the concerns associated to the particular issues. DIPL corporation being short

on staff has found it difficult to handle the various types of the execution process related to the

installation process and carrying of the reconciliation and the testing process of the new

arrangement by the year end (Duncan and Whittington 2014).

The main considerations of the cash receipt have been depicted by the finance

professionals and the inherent risks associated to the concerns. The staff member has been

further able to handle the various types the associated issues which are seen to be related to the

appropriate sequence for account receivables (De George, Ferguson and Spear 2013).

Risk and way it might affect the risk of material misstatement in the financial report

The various types of the inherent risk as per material misstatements are listed below as

follows:

Excessive pressure on employees and management- The excusive workload on the staff

members has been seen to be the main cause for the deteriorating bookkeeping. The identified

attributed encountered for the poor liquidity has been based on the various types ofthe opeatin

outcomes and issues pertaining to cash flow.

Risks of errors or else incorrect misrepresentation- The intricacies identified and the erros in

the financial statement has been simultaneously misstated.

Integrity of the entire management- The management of DIPL has been essentially seen to

lack the various types of the considerations related to reputational loss for business and

community.

5AUDIT ASSURANCE AND COMPLIANCE

Unusual pressure on management- In several occasions the incentives for the management are

based on the incentives acquired for the pecuniary declarations and misstatements.

Nature of business- DIPL has been seen to be majorly contributing for the competitive

circumstances. The various types of the aforementioned facets has been seen to be associated the

differ type the consideration which is further seen to be related to the inherent risks of the audit

planning and the audit structure (Laili and Khairi 2013).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Asset Loss The identified risks have been seen to be associated to the various

degrees of the losses resulting in the fraud of the assets. The

dissatisfaction of the workforce has been further related to the different

types of considerations which have been further seen to be based on the

expectations of fraud risks. In addition to this, the expectations of the

investors has been seen in terms of the different types of types of the

consideration which has been taken into the consideration from the

various types the associated risk which are seen to be related to the

performance based targets and high amount of risk of fraud. The various

types of the other considerations of the risk of fraud has been further seen

to be associated to different types of the consideration made for the

different financial outcomes in averting the guarantees generated

Unusual pressure on management- In several occasions the incentives for the management are

based on the incentives acquired for the pecuniary declarations and misstatements.

Nature of business- DIPL has been seen to be majorly contributing for the competitive

circumstances. The various types of the aforementioned facets has been seen to be associated the

differ type the consideration which is further seen to be related to the inherent risks of the audit

planning and the audit structure (Laili and Khairi 2013).

Answer to Question 3:

A) Identification and explanation of two key fraud risk factors relating to

misstatements arising from fraudulent financial reporting

Asset Loss The identified risks have been seen to be associated to the various

degrees of the losses resulting in the fraud of the assets. The

dissatisfaction of the workforce has been further related to the different

types of considerations which have been further seen to be based on the

expectations of fraud risks. In addition to this, the expectations of the

investors has been seen in terms of the different types of types of the

consideration which has been taken into the consideration from the

various types the associated risk which are seen to be related to the

performance based targets and high amount of risk of fraud. The various

types of the other considerations of the risk of fraud has been further seen

to be associated to different types of the consideration made for the

different financial outcomes in averting the guarantees generated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT ASSURANCE AND COMPLIANCE

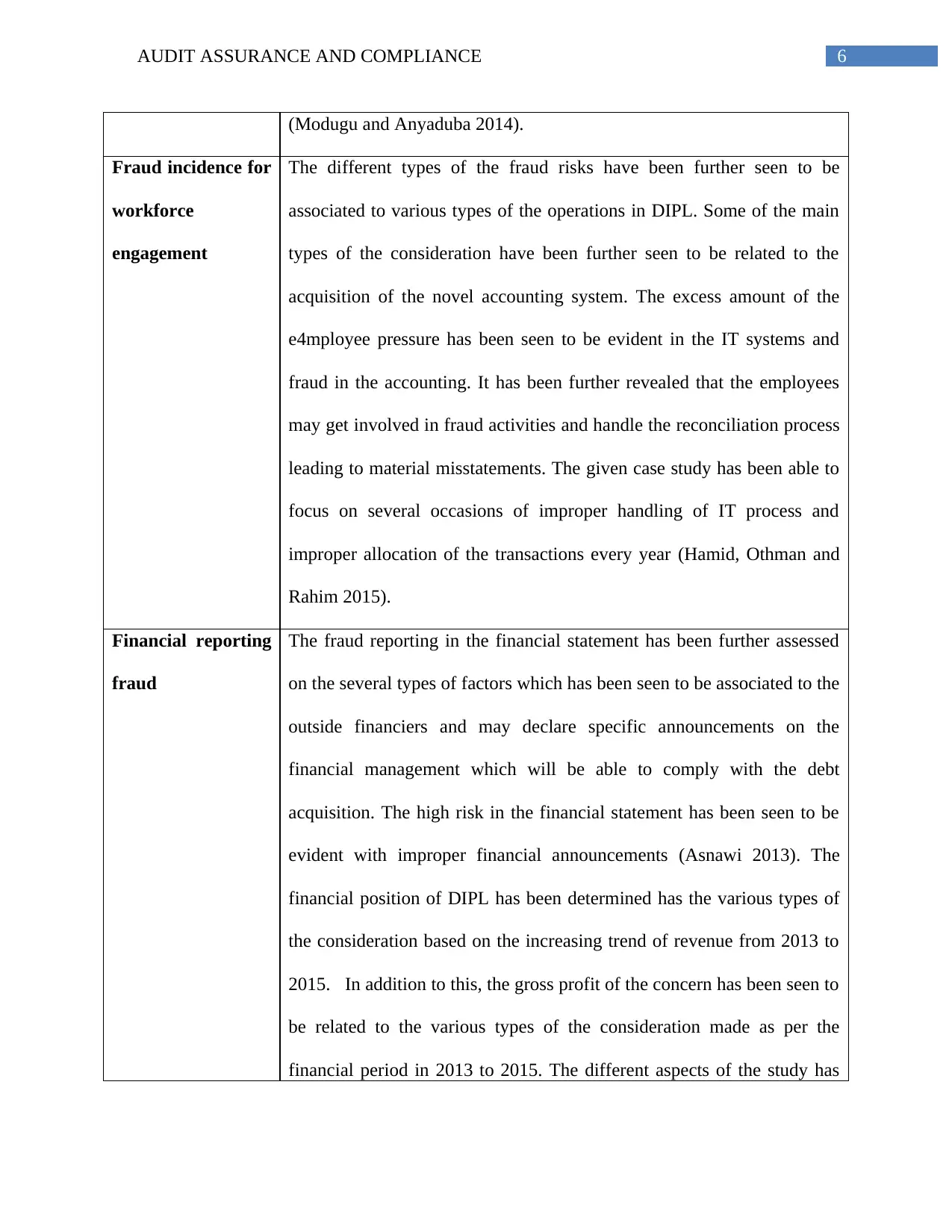

(Modugu and Anyaduba 2014).

Fraud incidence for

workforce

engagement

The different types of the fraud risks have been further seen to be

associated to various types of the operations in DIPL. Some of the main

types of the consideration have been further seen to be related to the

acquisition of the novel accounting system. The excess amount of the

e4mployee pressure has been seen to be evident in the IT systems and

fraud in the accounting. It has been further revealed that the employees

may get involved in fraud activities and handle the reconciliation process

leading to material misstatements. The given case study has been able to

focus on several occasions of improper handling of IT process and

improper allocation of the transactions every year (Hamid, Othman and

Rahim 2015).

Financial reporting

fraud

The fraud reporting in the financial statement has been further assessed

on the several types of factors which has been seen to be associated to the

outside financiers and may declare specific announcements on the

financial management which will be able to comply with the debt

acquisition. The high risk in the financial statement has been seen to be

evident with improper financial announcements (Asnawi 2013). The

financial position of DIPL has been determined has the various types of

the consideration based on the increasing trend of revenue from 2013 to

2015. In addition to this, the gross profit of the concern has been seen to

be related to the various types of the consideration made as per the

financial period in 2013 to 2015. The different aspects of the study has

(Modugu and Anyaduba 2014).

Fraud incidence for

workforce

engagement

The different types of the fraud risks have been further seen to be

associated to various types of the operations in DIPL. Some of the main

types of the consideration have been further seen to be related to the

acquisition of the novel accounting system. The excess amount of the

e4mployee pressure has been seen to be evident in the IT systems and

fraud in the accounting. It has been further revealed that the employees

may get involved in fraud activities and handle the reconciliation process

leading to material misstatements. The given case study has been able to

focus on several occasions of improper handling of IT process and

improper allocation of the transactions every year (Hamid, Othman and

Rahim 2015).

Financial reporting

fraud

The fraud reporting in the financial statement has been further assessed

on the several types of factors which has been seen to be associated to the

outside financiers and may declare specific announcements on the

financial management which will be able to comply with the debt

acquisition. The high risk in the financial statement has been seen to be

evident with improper financial announcements (Asnawi 2013). The

financial position of DIPL has been determined has the various types of

the consideration based on the increasing trend of revenue from 2013 to

2015. In addition to this, the gross profit of the concern has been seen to

be related to the various types of the consideration made as per the

financial period in 2013 to 2015. The different aspects of the study has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT ASSURANCE AND COMPLIANCE

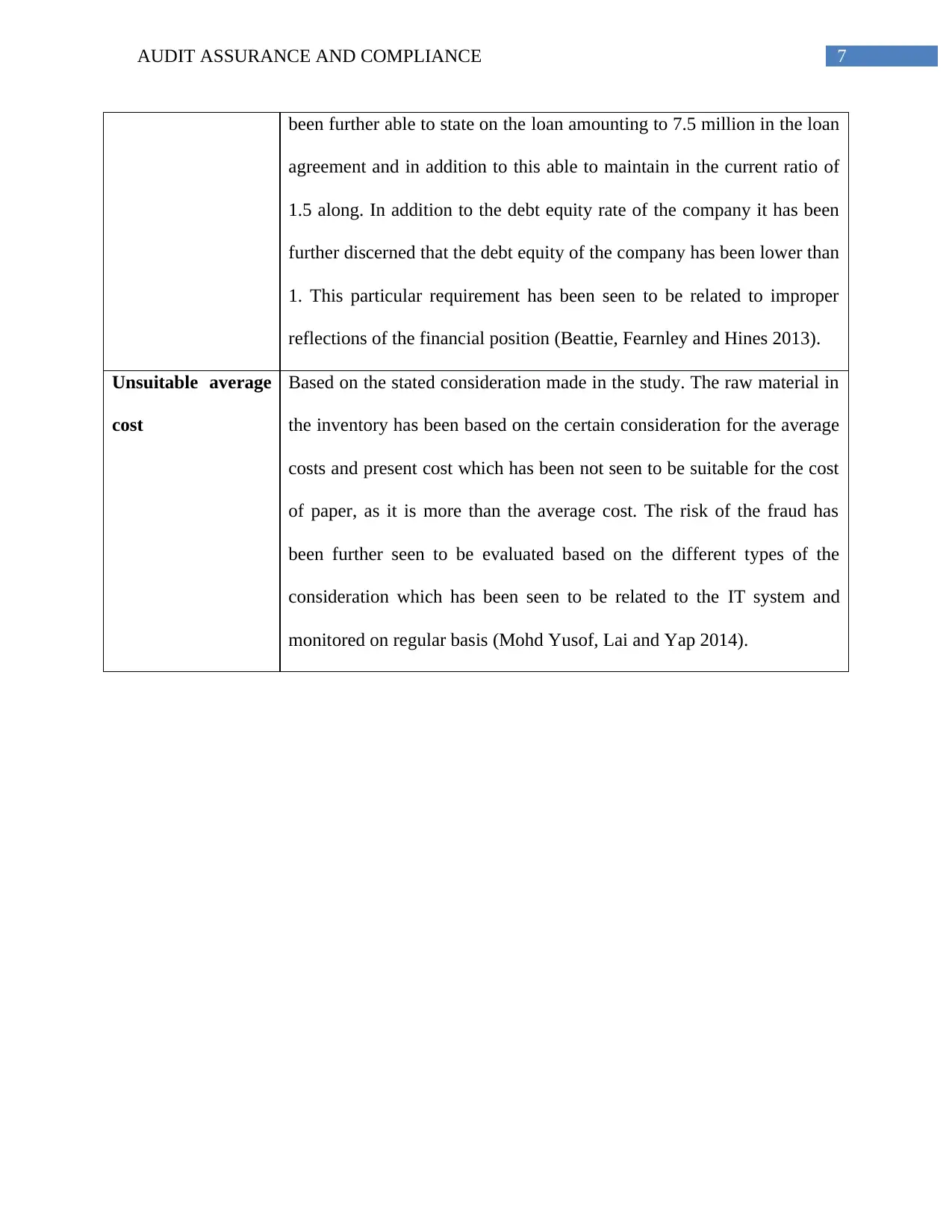

been further able to state on the loan amounting to 7.5 million in the loan

agreement and in addition to this able to maintain in the current ratio of

1.5 along. In addition to the debt equity rate of the company it has been

further discerned that the debt equity of the company has been lower than

1. This particular requirement has been seen to be related to improper

reflections of the financial position (Beattie, Fearnley and Hines 2013).

Unsuitable average

cost

Based on the stated consideration made in the study. The raw material in

the inventory has been based on the certain consideration for the average

costs and present cost which has been not seen to be suitable for the cost

of paper, as it is more than the average cost. The risk of the fraud has

been further seen to be evaluated based on the different types of the

consideration which has been seen to be related to the IT system and

monitored on regular basis (Mohd Yusof, Lai and Yap 2014).

been further able to state on the loan amounting to 7.5 million in the loan

agreement and in addition to this able to maintain in the current ratio of

1.5 along. In addition to the debt equity rate of the company it has been

further discerned that the debt equity of the company has been lower than

1. This particular requirement has been seen to be related to improper

reflections of the financial position (Beattie, Fearnley and Hines 2013).

Unsuitable average

cost

Based on the stated consideration made in the study. The raw material in

the inventory has been based on the certain consideration for the average

costs and present cost which has been not seen to be suitable for the cost

of paper, as it is more than the average cost. The risk of the fraud has

been further seen to be evaluated based on the different types of the

consideration which has been seen to be related to the IT system and

monitored on regular basis (Mohd Yusof, Lai and Yap 2014).

8AUDIT ASSURANCE AND COMPLIANCE

Reference List

Asnawi, M. (2013) ‘The impact of audit rate, perceived probability of audit on tax compliance

decision’, Journal of Indonesian Economy and Business, 28(2), pp. 292–307. doi:

10.1017/CBO9781107415324.004.

Beattie, V., Fearnley, S. and Hines, T. (2013) ‘Perceptions of factors affecting audit quality in

the post-SOX UK regulatory environment’, Accounting and Business Research, 43(1), pp. 56–

81. doi: 10.1080/00014788.2012.703079.

Bell, T. B., Causholli, M. and Knechel, W. R. (2015) ‘Audit Firm Tenure, Non-Audit Services,

and Internal Assessments of Audit Quality’, Journal of Accounting Research, 53(3), pp. 461–

509. doi: 10.1111/1475-679X.12078.

Duncan, B. and Whittington, M. (2014) ‘Compliance with Standards, Assurance and Audit: Does

this Equal Security?’, in Security of Information and Networks (SIN), 2014 Proceedings of the

7th International Conference on, pp. 77–84. doi: 10.1145/2659651.2659711.

De George, E. T., Ferguson, C. B. and Spear, N. A. (2013) ‘How much does IFRS cost? IFRS

adoption and audit fees’, Accounting Review, 88(2), pp. 429–462. doi: 10.2308/accr-50317.

Giard, M., Laprugne-Garcia, E., Caillat-Vallet, E., Russell, I., Verjat-Trannoy, D., Ertzscheid, M.

A., Vernier, N., Laland, C. and Savey, A. (2016) ‘Compliance with standard precautions: Results

of a French national audit’, American Journal of Infection Control, 44(1), pp. 8–13. doi:

10.1016/j.ajic.2015.07.034.

Hamid, K. C. A., Othman, S. and Rahim, M. A. (2015) ‘Independence and Financial Knowledge

Reference List

Asnawi, M. (2013) ‘The impact of audit rate, perceived probability of audit on tax compliance

decision’, Journal of Indonesian Economy and Business, 28(2), pp. 292–307. doi:

10.1017/CBO9781107415324.004.

Beattie, V., Fearnley, S. and Hines, T. (2013) ‘Perceptions of factors affecting audit quality in

the post-SOX UK regulatory environment’, Accounting and Business Research, 43(1), pp. 56–

81. doi: 10.1080/00014788.2012.703079.

Bell, T. B., Causholli, M. and Knechel, W. R. (2015) ‘Audit Firm Tenure, Non-Audit Services,

and Internal Assessments of Audit Quality’, Journal of Accounting Research, 53(3), pp. 461–

509. doi: 10.1111/1475-679X.12078.

Duncan, B. and Whittington, M. (2014) ‘Compliance with Standards, Assurance and Audit: Does

this Equal Security?’, in Security of Information and Networks (SIN), 2014 Proceedings of the

7th International Conference on, pp. 77–84. doi: 10.1145/2659651.2659711.

De George, E. T., Ferguson, C. B. and Spear, N. A. (2013) ‘How much does IFRS cost? IFRS

adoption and audit fees’, Accounting Review, 88(2), pp. 429–462. doi: 10.2308/accr-50317.

Giard, M., Laprugne-Garcia, E., Caillat-Vallet, E., Russell, I., Verjat-Trannoy, D., Ertzscheid, M.

A., Vernier, N., Laland, C. and Savey, A. (2016) ‘Compliance with standard precautions: Results

of a French national audit’, American Journal of Infection Control, 44(1), pp. 8–13. doi:

10.1016/j.ajic.2015.07.034.

Hamid, K. C. A., Othman, S. and Rahim, M. A. (2015) ‘Independence and Financial Knowledge

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT ASSURANCE AND COMPLIANCE

on Audit Committee with Non-compliance of Financial Disclosure: A Study of Listed

Companies Issued with Public Reprimand in Malaysia’, Procedia - Social and Behavioral

Sciences, 172, pp. 754–761. doi: 10.1016/j.sbspro.2015.01.429.

Laili, N. H. and Khairi, K. F. (2013) ‘IFRS Compliance and Audit Quality Among Big 3

Auditors: The Case of Goodwill Impairment’, SSRN Electronic Journal. doi:

10.2139/ssrn.2358336.

Lindeboom, M., van der Klaauw, B. and Vriend, S. (2016) ‘Audit rates and compliance: A field

experiment in care provision’, Journal of Economic Behavior and Organization, 131, pp. 160–

173. doi: 10.1016/j.jebo.2015.08.016.

Modugu, K. P. and Anyaduba, J. O. (2014) ‘Impact of tax audit on tax compliance in Nigeria’,

International Journal of Business and Social Science, 5(9), pp. 207–215.

Mohd Yusof, N. A., Lai, M. L. and Yap, B. W. (2014) ‘Tax non-compliance among SMCs in

Malaysia: tax audit evidence’, Journal of Applied Accounting Research, 15(2), pp. 215–234. doi:

10.1108/JAAR-02-2013-0016.

Yasin, F. M. and Nelson, S. P. (2013) ‘Audit Committee and Internal Audit: Implications on

Audit Quality’, International Journal of Economics, Management and Accounting International

Journal of Economics Management and Accounting, 20(122), pp. 187–218. doi:

10.1108/02686909310036223.

on Audit Committee with Non-compliance of Financial Disclosure: A Study of Listed

Companies Issued with Public Reprimand in Malaysia’, Procedia - Social and Behavioral

Sciences, 172, pp. 754–761. doi: 10.1016/j.sbspro.2015.01.429.

Laili, N. H. and Khairi, K. F. (2013) ‘IFRS Compliance and Audit Quality Among Big 3

Auditors: The Case of Goodwill Impairment’, SSRN Electronic Journal. doi:

10.2139/ssrn.2358336.

Lindeboom, M., van der Klaauw, B. and Vriend, S. (2016) ‘Audit rates and compliance: A field

experiment in care provision’, Journal of Economic Behavior and Organization, 131, pp. 160–

173. doi: 10.1016/j.jebo.2015.08.016.

Modugu, K. P. and Anyaduba, J. O. (2014) ‘Impact of tax audit on tax compliance in Nigeria’,

International Journal of Business and Social Science, 5(9), pp. 207–215.

Mohd Yusof, N. A., Lai, M. L. and Yap, B. W. (2014) ‘Tax non-compliance among SMCs in

Malaysia: tax audit evidence’, Journal of Applied Accounting Research, 15(2), pp. 215–234. doi:

10.1108/JAAR-02-2013-0016.

Yasin, F. M. and Nelson, S. P. (2013) ‘Audit Committee and Internal Audit: Implications on

Audit Quality’, International Journal of Economics, Management and Accounting International

Journal of Economics Management and Accounting, 20(122), pp. 187–218. doi:

10.1108/02686909310036223.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT ASSURANCE AND COMPLIANCE

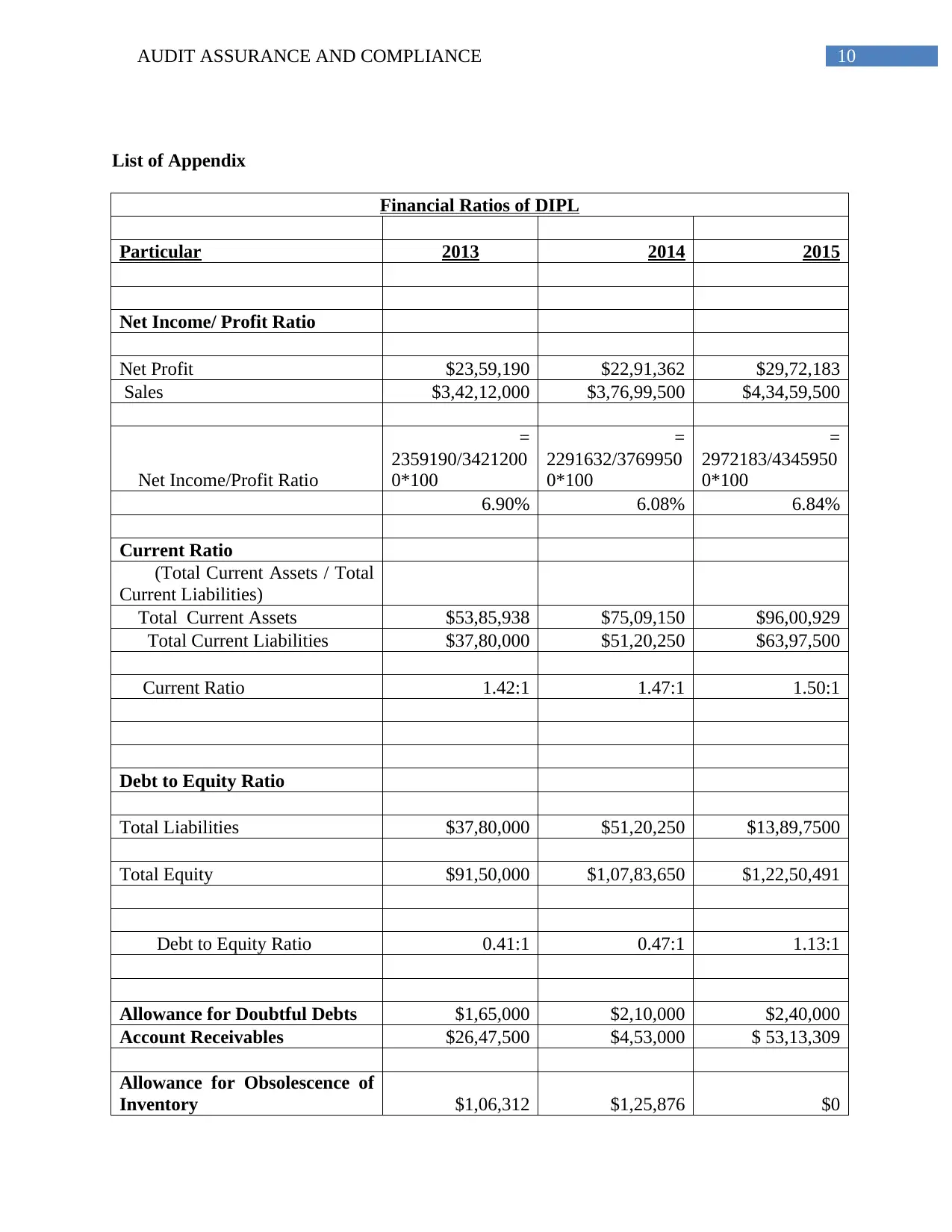

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

List of Appendix

Financial Ratios of DIPL

Particular 2013 2014 2015

Net Income/ Profit Ratio

Net Profit $23,59,190 $22,91,362 $29,72,183

Sales $3,42,12,000 $3,76,99,500 $4,34,59,500

Net Income/Profit Ratio

=

2359190/3421200

0*100

=

2291632/3769950

0*100

=

2972183/4345950

0*100

6.90% 6.08% 6.84%

Current Ratio

(Total Current Assets / Total

Current Liabilities)

Total Current Assets $53,85,938 $75,09,150 $96,00,929

Total Current Liabilities $37,80,000 $51,20,250 $63,97,500

Current Ratio 1.42:1 1.47:1 1.50:1

Debt to Equity Ratio

Total Liabilities $37,80,000 $51,20,250 $13,89,7500

Total Equity $91,50,000 $1,07,83,650 $1,22,50,491

Debt to Equity Ratio 0.41:1 0.47:1 1.13:1

Allowance for Doubtful Debts $1,65,000 $2,10,000 $2,40,000

Account Receivables $26,47,500 $4,53,000 $ 53,13,309

Allowance for Obsolescence of

Inventory $1,06,312 $1,25,876 $0

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.