Advanced Accounting Assignment 1: Financial Audit of Comvita Limited

VerifiedAdded on 2023/06/03

|7

|1811

|276

Report

AI Summary

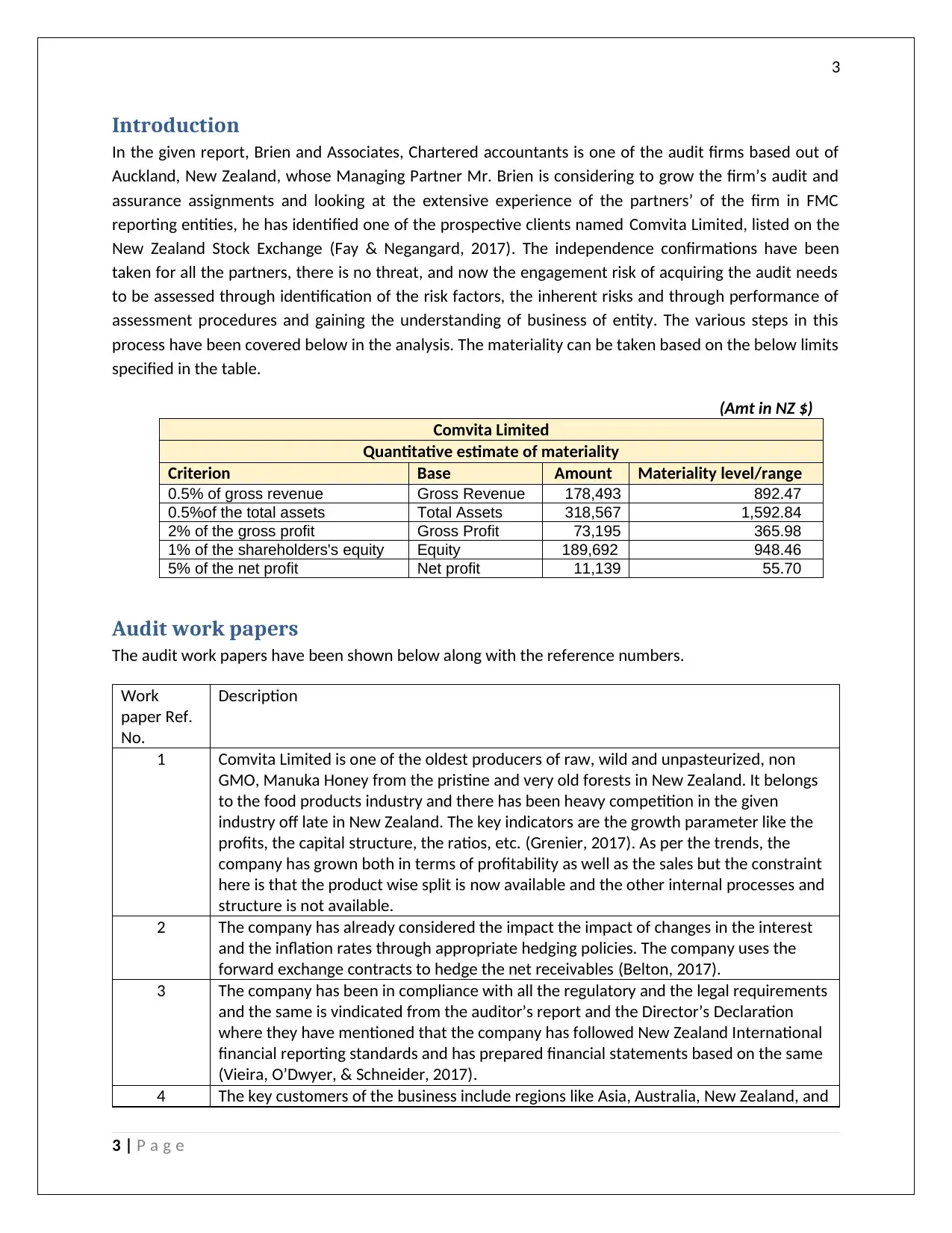

This report presents an analysis of the audit engagement for Comvita Limited, a company listed on the New Zealand Stock Exchange. The report begins with an introduction outlining the context of the audit, including the firm's interest in acquiring the client and the importance of assessing engagement risk. The report proceeds to detail the materiality levels based on various financial metrics of Comvita Limited. The core of the report consists of audit workpapers that summarize key aspects of the company's business, including its industry, key indicators, compliance with regulations, key customers, competitors, management structure, related party transactions, financing sources, investments, and accounting policies. Each workpaper provides a concise description of the relevant information and identifies areas of potential risk. The report highlights the company's strengths, such as its experienced management and compliance with financial reporting standards, while also acknowledging potential risks stemming from competition, internal control weaknesses, and the use of accounting estimates and judgments. Finally, the report concludes by referencing relevant literature and emphasizing the need for a thorough understanding of the business and its risks to ensure a successful audit engagement.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.