Financial Auditing Analysis: CSL Limited Case Study Assignment

VerifiedAdded on 2021/05/30

|11

|2218

|21

Homework Assignment

AI Summary

This assignment focuses on the auditing analysis of CSL Limited, a biotechnology company. It involves filling in a table with information extracted from CSL's annual report, including the balance date, audit report details (date, auditor, opinion type), and explanations for any modifications. The assignment also requires the calculation of audit and non-audit fees, a breakdown of the industry, and financial data such as operating revenue, profit, equity, assets, and liabilities. Furthermore, the discussion factor section delves into inherent risk, the nature of the client's business, results of previous audits, initial versus repeat audits, quantity of non-routine transactions, estimates and judgments required for accounts, and potential fraud risks. The analysis concludes with an assessment of the overall inherent risk level, considering factors such as foreign exchange risk, intricate business accounting, and global operations. The assignment highlights various aspects of the audit process and provides a comprehensive overview of CSL Limited's financial standing and risk profile, referencing relevant auditing standards and academic sources.

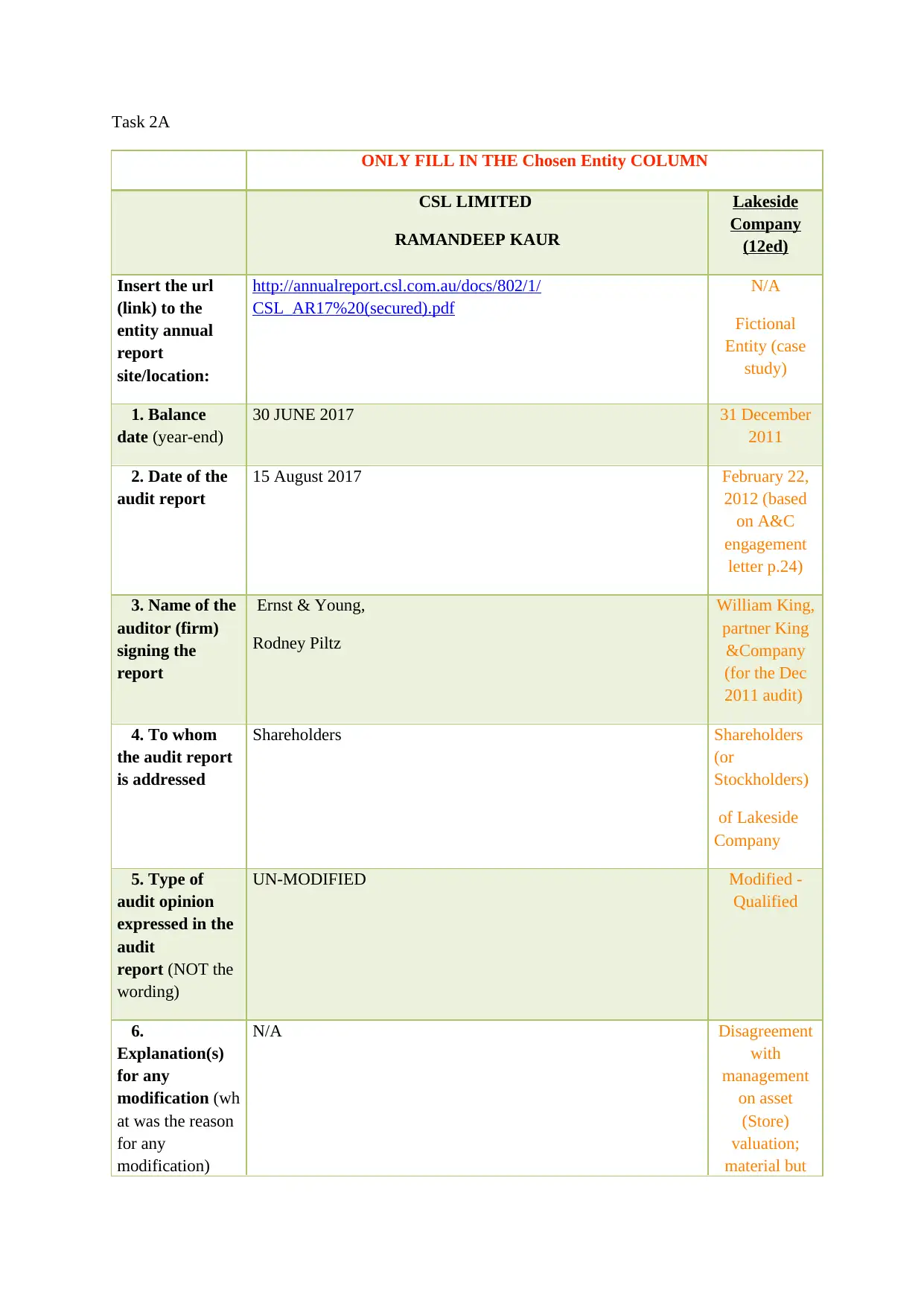

Task 2A

ONLY FILL IN THE Chosen Entity COLUMN

CSL LIMITED

RAMANDEEP KAUR

Lakeside

Company

(12ed)

Insert the url

(link) to the

entity annual

report

site/location:

http://annualreport.csl.com.au/docs/802/1/

CSL_AR17%20(secured).pdf

N/A

Fictional

Entity (case

study)

1. Balance

date (year-end)

30 JUNE 2017 31 December

2011

2. Date of the

audit report

15 August 2017 February 22,

2012 (based

on A&C

engagement

letter p.24)

3. Name of the

auditor (firm)

signing the

report

Ernst & Young,

Rodney Piltz

William King,

partner King

&Company

(for the Dec

2011 audit)

4. To whom

the audit report

is addressed

Shareholders Shareholders

(or

Stockholders)

of Lakeside

Company

5. Type of

audit opinion

expressed in the

audit

report (NOT the

wording)

UN-MODIFIED Modified -

Qualified

6.

Explanation(s)

for any

modification (wh

at was the reason

for any

modification)

N/A Disagreement

with

management

on asset

(Store)

valuation;

material but

ONLY FILL IN THE Chosen Entity COLUMN

CSL LIMITED

RAMANDEEP KAUR

Lakeside

Company

(12ed)

Insert the url

(link) to the

entity annual

report

site/location:

http://annualreport.csl.com.au/docs/802/1/

CSL_AR17%20(secured).pdf

N/A

Fictional

Entity (case

study)

1. Balance

date (year-end)

30 JUNE 2017 31 December

2011

2. Date of the

audit report

15 August 2017 February 22,

2012 (based

on A&C

engagement

letter p.24)

3. Name of the

auditor (firm)

signing the

report

Ernst & Young,

Rodney Piltz

William King,

partner King

&Company

(for the Dec

2011 audit)

4. To whom

the audit report

is addressed

Shareholders Shareholders

(or

Stockholders)

of Lakeside

Company

5. Type of

audit opinion

expressed in the

audit

report (NOT the

wording)

UN-MODIFIED Modified -

Qualified

6.

Explanation(s)

for any

modification (wh

at was the reason

for any

modification)

N/A Disagreement

with

management

on asset

(Store)

valuation;

material but

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not pervasive

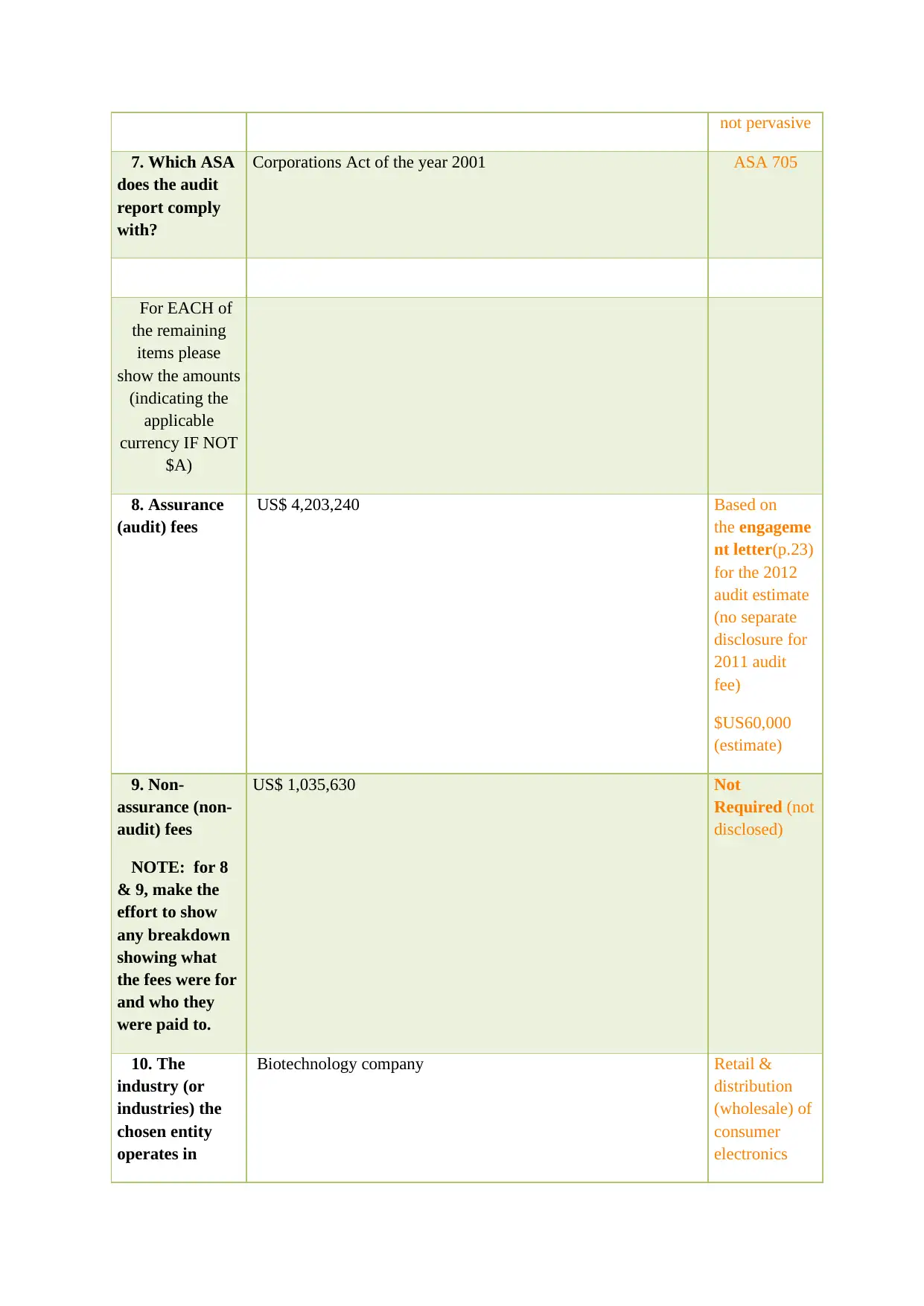

7. Which ASA

does the audit

report comply

with?

Corporations Act of the year 2001 ASA 705

For EACH of

the remaining

items please

show the amounts

(indicating the

applicable

currency IF NOT

$A)

8. Assurance

(audit) fees

US$ 4,203,240 Based on

the engageme

nt letter(p.23)

for the 2012

audit estimate

(no separate

disclosure for

2011 audit

fee)

$US60,000

(estimate)

9. Non-

assurance (non-

audit) fees

NOTE: for 8

& 9, make the

effort to show

any breakdown

showing what

the fees were for

and who they

were paid to.

US$ 1,035,630 Not

Required (not

disclosed)

10. The

industry (or

industries) the

chosen entity

operates in

Biotechnology company Retail &

distribution

(wholesale) of

consumer

electronics

7. Which ASA

does the audit

report comply

with?

Corporations Act of the year 2001 ASA 705

For EACH of

the remaining

items please

show the amounts

(indicating the

applicable

currency IF NOT

$A)

8. Assurance

(audit) fees

US$ 4,203,240 Based on

the engageme

nt letter(p.23)

for the 2012

audit estimate

(no separate

disclosure for

2011 audit

fee)

$US60,000

(estimate)

9. Non-

assurance (non-

audit) fees

NOTE: for 8

& 9, make the

effort to show

any breakdown

showing what

the fees were for

and who they

were paid to.

US$ 1,035,630 Not

Required (not

disclosed)

10. The

industry (or

industries) the

chosen entity

operates in

Biotechnology company Retail &

distribution

(wholesale) of

consumer

electronics

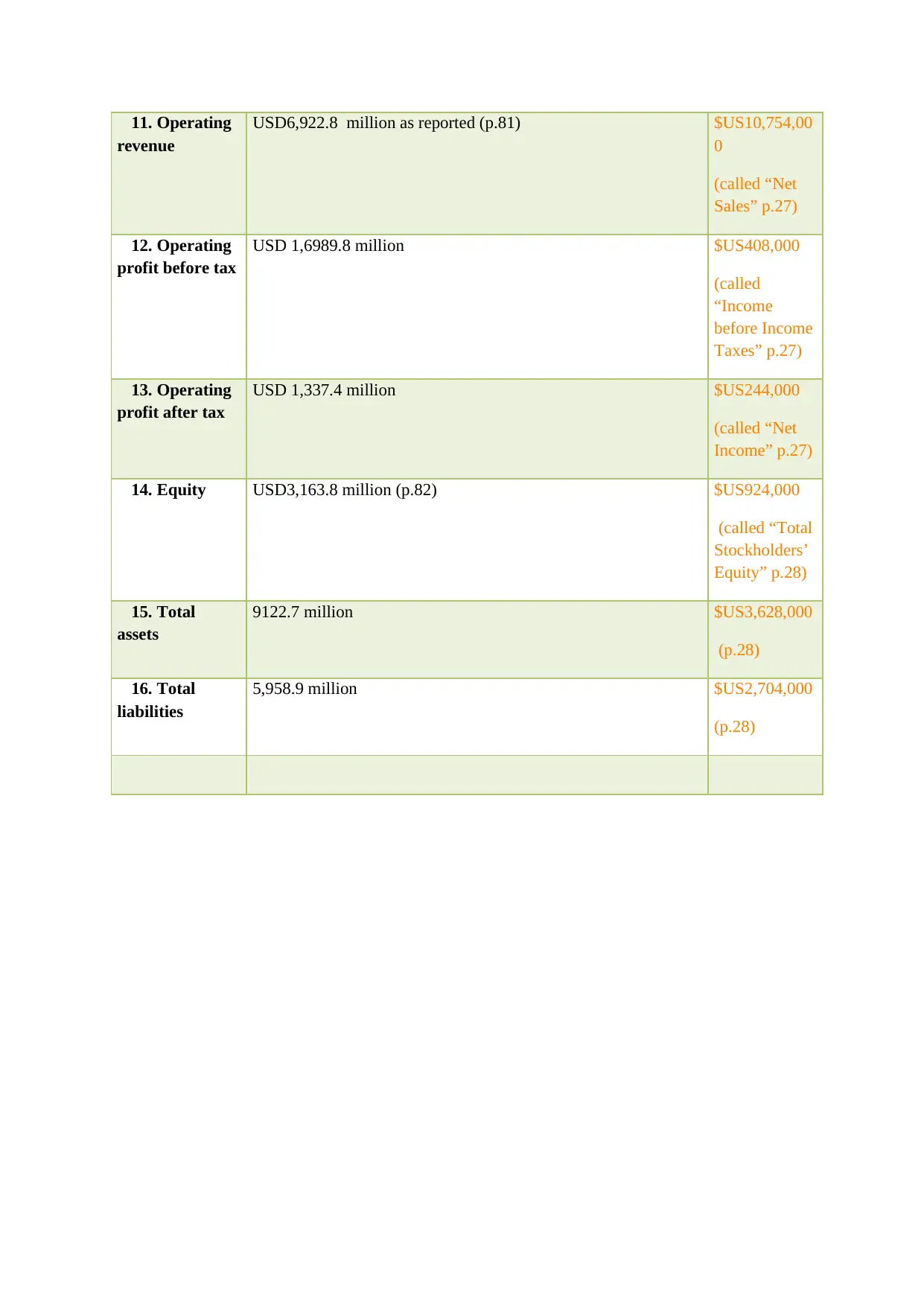

11. Operating

revenue

USD6,922.8 million as reported (p.81) $US10,754,00

0

(called “Net

Sales” p.27)

12. Operating

profit before tax

USD 1,6989.8 million $US408,000

(called

“Income

before Income

Taxes” p.27)

13. Operating

profit after tax

USD 1,337.4 million $US244,000

(called “Net

Income” p.27)

14. Equity USD3,163.8 million (p.82) $US924,000

(called “Total

Stockholders’

Equity” p.28)

15. Total

assets

9122.7 million $US3,628,000

(p.28)

16. Total

liabilities

5,958.9 million $US2,704,000

(p.28)

revenue

USD6,922.8 million as reported (p.81) $US10,754,00

0

(called “Net

Sales” p.27)

12. Operating

profit before tax

USD 1,6989.8 million $US408,000

(called

“Income

before Income

Taxes” p.27)

13. Operating

profit after tax

USD 1,337.4 million $US244,000

(called “Net

Income” p.27)

14. Equity USD3,163.8 million (p.82) $US924,000

(called “Total

Stockholders’

Equity” p.28)

15. Total

assets

9122.7 million $US3,628,000

(p.28)

16. Total

liabilities

5,958.9 million $US2,704,000

(p.28)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

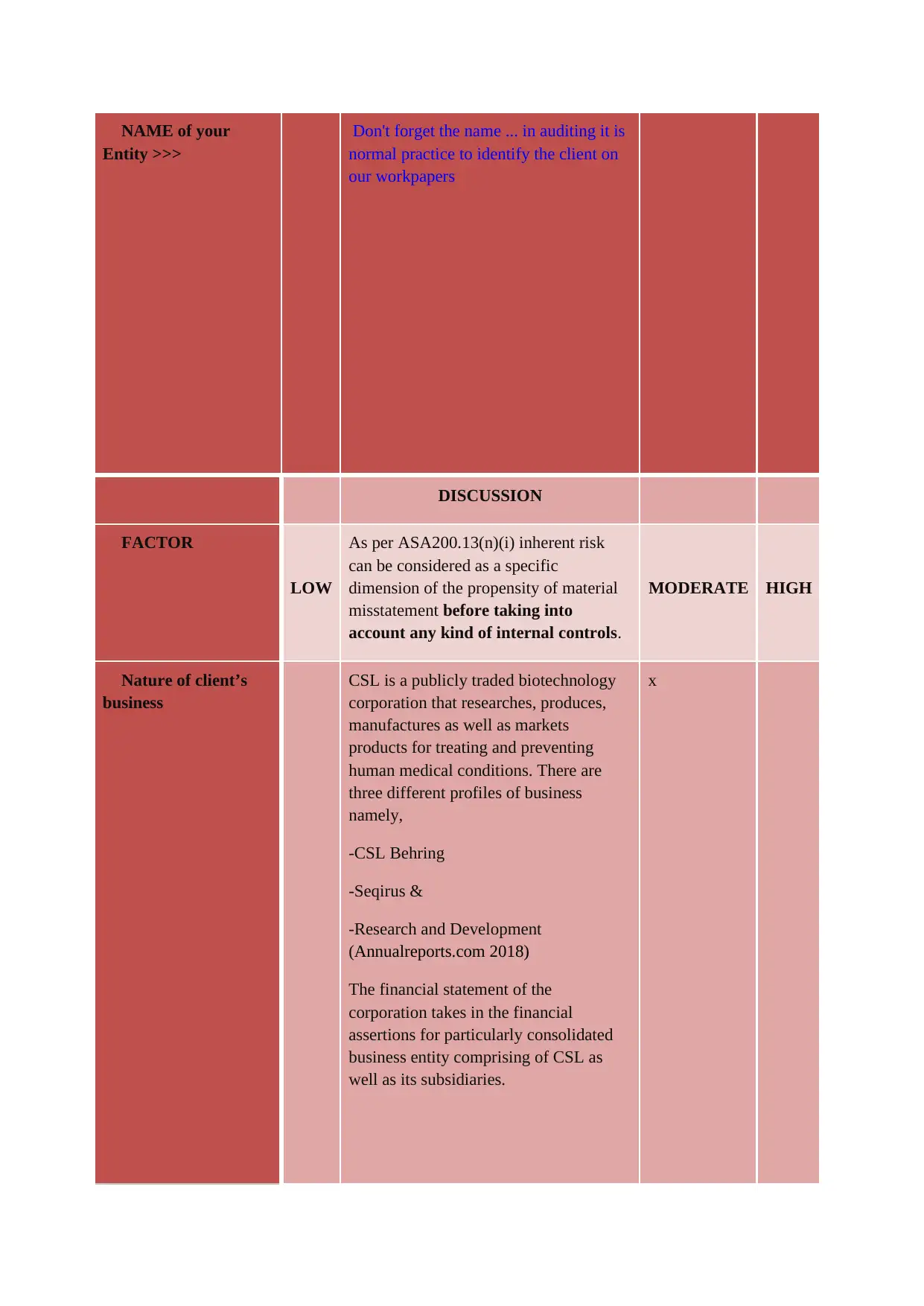

NAME of your

Entity >>>

Don't forget the name ... in auditing it is

normal practice to identify the client on

our workpapers

DISCUSSION

FACTOR

LOW

As per ASA200.13(n)(i) inherent risk

can be considered as a specific

dimension of the propensity of material

misstatement before taking into

account any kind of internal controls.

MODERATE HIGH

Nature of client’s

business

CSL is a publicly traded biotechnology

corporation that researches, produces,

manufactures as well as markets

products for treating and preventing

human medical conditions. There are

three different profiles of business

namely,

-CSL Behring

-Seqirus &

-Research and Development

(Annualreports.com 2018)

The financial statement of the

corporation takes in the financial

assertions for particularly consolidated

business entity comprising of CSL as

well as its subsidiaries.

x

Entity >>>

Don't forget the name ... in auditing it is

normal practice to identify the client on

our workpapers

DISCUSSION

FACTOR

LOW

As per ASA200.13(n)(i) inherent risk

can be considered as a specific

dimension of the propensity of material

misstatement before taking into

account any kind of internal controls.

MODERATE HIGH

Nature of client’s

business

CSL is a publicly traded biotechnology

corporation that researches, produces,

manufactures as well as markets

products for treating and preventing

human medical conditions. There are

three different profiles of business

namely,

-CSL Behring

-Seqirus &

-Research and Development

(Annualreports.com 2018)

The financial statement of the

corporation takes in the financial

assertions for particularly consolidated

business entity comprising of CSL as

well as its subsidiaries.

x

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Results of previous

audits

Prior audit report reveals that there are

internal as well as external auditors

reviewing the functionalities of the

business (Annualreports.com 2018). The

external auditor reviews as well as

monitors firm’s performance along with

independence of particularly external

auditors. External auditors attend the

annual general meeting and are also

available for answering all the questions

from particularly the shareholders

pertinent to the process of audit. The

internal assessors also monitors overall

performance of the firm. For the year

2015, PricewaterhouseCoopers was the

internal auditor of the firm. Analysis of

prior audit report reflects that the

financial statements of the firm along

with related notes conform to IFRS

Accounting Standards as is necessary for

the Corporation Act, particular corporate

regulations as well as CSL Group

Accounting Policies. Also, the

statements provide a true as well as fair

view of the company’s financial position

as on the pertinent balance date along

with performance of the firm CSL for the

relatable period as necessary by the

Corporations Act (Annualreports.com

2018). In addition to this, the financial

records of the firm are also maintained as

per the directives of the Corporation Act.

Furthermore, different non-audit services

of the company are also reviewed by

specifically the Audit as well as Risk

Management Committee to make certain

maintenance of impartiality along with

objectivity of the assessor as per 307C of

Corporation Act of the year 2001

(Annualreports.com 2018).

Key judgements also states that

impairment assessment procedure calls

for the need to make significant

judgements. Ascertaining whether

x

audits

Prior audit report reveals that there are

internal as well as external auditors

reviewing the functionalities of the

business (Annualreports.com 2018). The

external auditor reviews as well as

monitors firm’s performance along with

independence of particularly external

auditors. External auditors attend the

annual general meeting and are also

available for answering all the questions

from particularly the shareholders

pertinent to the process of audit. The

internal assessors also monitors overall

performance of the firm. For the year

2015, PricewaterhouseCoopers was the

internal auditor of the firm. Analysis of

prior audit report reflects that the

financial statements of the firm along

with related notes conform to IFRS

Accounting Standards as is necessary for

the Corporation Act, particular corporate

regulations as well as CSL Group

Accounting Policies. Also, the

statements provide a true as well as fair

view of the company’s financial position

as on the pertinent balance date along

with performance of the firm CSL for the

relatable period as necessary by the

Corporations Act (Annualreports.com

2018). In addition to this, the financial

records of the firm are also maintained as

per the directives of the Corporation Act.

Furthermore, different non-audit services

of the company are also reviewed by

specifically the Audit as well as Risk

Management Committee to make certain

maintenance of impartiality along with

objectivity of the assessor as per 307C of

Corporation Act of the year 2001

(Annualreports.com 2018).

Key judgements also states that

impairment assessment procedure calls

for the need to make significant

judgements. Ascertaining whether

x

goodwill has also become impaired and

needs approximation of recoverable

amount of particularly cash generating

sections utilizing discounted flow of cash

methodology. The enumeration process

utilizes projections of cash flow founded

on operatingbudgets and strategic

business plan.

Any surplus of the fair value of

particularly purchase consideration of a

particular acquired business specifically

over the fair value of particular net assets

is registered as goodwill. Again,

intellectual property that is acquired

distinctly or in a combination is

preliminarily enumerated at cost that is

the fair value at the acquirement date.

Further, costs borne for development or

acquirement of software also contribute

towards future benefits and are

capitalised. Also, economic lives of

intangible assets are analysed to be either

finite or else indefinite.

Initial versus repeat

audits

x The auditor of the company has been

changed from PricewaterhouseCooper to

Ernst & Young (Annualreports.com

2018). The change of auditor calls for

higher degree of transparency in the

association between firm’s board as well

as their external assessors. As per

Corporation Act, there is need for the

companies to change their partiner in

audit in every five years that can be

extended to even 7 years. However, there

are stringent rules regarding altering

needs approximation of recoverable

amount of particularly cash generating

sections utilizing discounted flow of cash

methodology. The enumeration process

utilizes projections of cash flow founded

on operatingbudgets and strategic

business plan.

Any surplus of the fair value of

particularly purchase consideration of a

particular acquired business specifically

over the fair value of particular net assets

is registered as goodwill. Again,

intellectual property that is acquired

distinctly or in a combination is

preliminarily enumerated at cost that is

the fair value at the acquirement date.

Further, costs borne for development or

acquirement of software also contribute

towards future benefits and are

capitalised. Also, economic lives of

intangible assets are analysed to be either

finite or else indefinite.

Initial versus repeat

audits

x The auditor of the company has been

changed from PricewaterhouseCooper to

Ernst & Young (Annualreports.com

2018). The change of auditor calls for

higher degree of transparency in the

association between firm’s board as well

as their external assessors. As per

Corporation Act, there is need for the

companies to change their partiner in

audit in every five years that can be

extended to even 7 years. However, there

are stringent rules regarding altering

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

audit corporations. Auditor independence

can be maintained by the rotation of the

auditor. This can also considerably

improve overall integrity as well as

quality of auditing and corporate

governance. Acquaintance with audit

partner can lead to personal association

and higher likelihood of scams

(Annualreports.com 2018).

Quantity of non-

routine transactions

Non-routine transactions refer to

recurring actions that are carried out in

usual course of the specific business. For

instance, cash disbursements can a,so be

regarded as non-routine transaction that

take place periodically but are not part of

the scheduled flow of transactions. Cash

was registered to be USD 556 million

that again increased to approximately

USD 844 million (Annualreports.com

2018).

x

Quantity of

estimates and

judgement required

for accounts

Analysis of the annual report of the firm

CSL reveals that important judgements

as well as estimates are presented for

business combinations (page 88 note 1b),

tax (page 90 Note 3), people cost (page

93 note 5), inventories (page 92 note 4),

intangible assets (page 96 note 7) and

trade receivables as well as payables

(page 109 note 5). Reports reveal that no

business combination has taken place

during the financial year 2017. Income

tax expenditure of the firm is recorded to

be USD 352.4 million in 2017

(Annualreports.com 2018). Here current

tax assets/liabilities re the specific

amounts to be recovered from authorities

of tax (Arens et al. 2016). However,

deferred tax liabilities are identified for

x

can be maintained by the rotation of the

auditor. This can also considerably

improve overall integrity as well as

quality of auditing and corporate

governance. Acquaintance with audit

partner can lead to personal association

and higher likelihood of scams

(Annualreports.com 2018).

Quantity of non-

routine transactions

Non-routine transactions refer to

recurring actions that are carried out in

usual course of the specific business. For

instance, cash disbursements can a,so be

regarded as non-routine transaction that

take place periodically but are not part of

the scheduled flow of transactions. Cash

was registered to be USD 556 million

that again increased to approximately

USD 844 million (Annualreports.com

2018).

x

Quantity of

estimates and

judgement required

for accounts

Analysis of the annual report of the firm

CSL reveals that important judgements

as well as estimates are presented for

business combinations (page 88 note 1b),

tax (page 90 Note 3), people cost (page

93 note 5), inventories (page 92 note 4),

intangible assets (page 96 note 7) and

trade receivables as well as payables

(page 109 note 5). Reports reveal that no

business combination has taken place

during the financial year 2017. Income

tax expenditure of the firm is recorded to

be USD 352.4 million in 2017

(Annualreports.com 2018). Here current

tax assets/liabilities re the specific

amounts to be recovered from authorities

of tax (Arens et al. 2016). However,

deferred tax liabilities are identified for

x

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

particularly taxable temporary variances.

In this case, judgements as well as

assumptions that include matters namely

availability along with timing of

deductions of tax and application of

principles to associated transactions are

subject to both risks as well as

uncertainty. Inventories stand at USD

2578. 8 million in 2017 while at USD

2152 million in 2016. Raw materials,

work in progress as well as finished

products are taken into account. Key

judgement in this regard include

regulatory approvals as well as future

demand for the products of the group

that affect analysis of recoverability of

particularly carrying value.

Potential for

fraudulent financial

reporting &

misappropriation of

assets (fraud risk

factors, see ASA 240)

There subsists probability for fraud in

the enumeration of software

development costs (Arens et al. 2016).

This mainly external direct costs of

different materials, specific service as

well payroll and payroll associated costs

of time spent of the workforces on the

particular project. In particular, it is the

managers of the firm that make use of

judgement on the total amount to allot

for the time spent by the employees

towards development of software. Also

software cycle can alter fast and

therefore it is intangible asset that is

significant to asset position of the entire

group (Knechel and Salterio 2016).

x

List any other

factors (can you see any

illustrations in your

client’s annual report of

the examples in ASA

315, Appendix 2 and

ASA 570.A2?)

1. CSL faces the foreign exchange risk as

the entire group has international

operations. Essentially, these risks can be

related to upcoming business

transactions, firm’s assets/liabilities that

are necessarily denominated in different

currencies along with net investments in

different foreign functionalities (Leung

x

In this case, judgements as well as

assumptions that include matters namely

availability along with timing of

deductions of tax and application of

principles to associated transactions are

subject to both risks as well as

uncertainty. Inventories stand at USD

2578. 8 million in 2017 while at USD

2152 million in 2016. Raw materials,

work in progress as well as finished

products are taken into account. Key

judgement in this regard include

regulatory approvals as well as future

demand for the products of the group

that affect analysis of recoverability of

particularly carrying value.

Potential for

fraudulent financial

reporting &

misappropriation of

assets (fraud risk

factors, see ASA 240)

There subsists probability for fraud in

the enumeration of software

development costs (Arens et al. 2016).

This mainly external direct costs of

different materials, specific service as

well payroll and payroll associated costs

of time spent of the workforces on the

particular project. In particular, it is the

managers of the firm that make use of

judgement on the total amount to allot

for the time spent by the employees

towards development of software. Also

software cycle can alter fast and

therefore it is intangible asset that is

significant to asset position of the entire

group (Knechel and Salterio 2016).

x

List any other

factors (can you see any

illustrations in your

client’s annual report of

the examples in ASA

315, Appendix 2 and

ASA 570.A2?)

1. CSL faces the foreign exchange risk as

the entire group has international

operations. Essentially, these risks can be

related to upcoming business

transactions, firm’s assets/liabilities that

are necessarily denominated in different

currencies along with net investments in

different foreign functionalities (Leung

x

et al. 2014).

2. CSL carries out intricate business

accounting that includes calculations of

taxes for respective governments and

abiding by tax rules. Essentially, it can

be considered as a great risk as company

need to be adaptable to alterations in

local legislation exerting influence on the

entire business community.

3. Multiple locations of operations and

global expansion of operations can

enhance productivity on one hand and

increase intricacies of regulatory as well

as legal burden (Messier et al. 2015).

Locations in different multiple

worldwide locations can aid and firms to

refer to opportunities generated by

convergence of both worldwide audit as

well as accounting standards.

4. The company is listed under ASX and

has the need to follow all the listing rules

of ASX and abide by 8 principles of

ASX Corporate Governance issued by

the Corporate Governance Council.

Adherence to this principles can help in

enhancement of materiality of the firm

(William Jr et al. 2016).

Conclusion: Overall

inherent risk level

We considered the risk of auditing as

moderate.

The above mentioned study helps in

understanding nature of business of the

company. Prior audit reports of the

company are also reviewed in detail to

present comparative study and identify

changes in mechanisms of audit and

results of audit. Review on initial as

against repeated audit is also presented

and justification of auditor rotation for

averting material misstatements is also

presented. Non routine transaction that is

x

2. CSL carries out intricate business

accounting that includes calculations of

taxes for respective governments and

abiding by tax rules. Essentially, it can

be considered as a great risk as company

need to be adaptable to alterations in

local legislation exerting influence on the

entire business community.

3. Multiple locations of operations and

global expansion of operations can

enhance productivity on one hand and

increase intricacies of regulatory as well

as legal burden (Messier et al. 2015).

Locations in different multiple

worldwide locations can aid and firms to

refer to opportunities generated by

convergence of both worldwide audit as

well as accounting standards.

4. The company is listed under ASX and

has the need to follow all the listing rules

of ASX and abide by 8 principles of

ASX Corporate Governance issued by

the Corporate Governance Council.

Adherence to this principles can help in

enhancement of materiality of the firm

(William Jr et al. 2016).

Conclusion: Overall

inherent risk level

We considered the risk of auditing as

moderate.

The above mentioned study helps in

understanding nature of business of the

company. Prior audit reports of the

company are also reviewed in detail to

present comparative study and identify

changes in mechanisms of audit and

results of audit. Review on initial as

against repeated audit is also presented

and justification of auditor rotation for

averting material misstatements is also

presented. Non routine transaction that is

x

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identified in the present case include the

cash transactions. Again capital

development cost is also anon-routine

transaction that has the need of

comprehending capitalised rate as well

as timing. Different quantity of estimate

is also mentioned in the current study at

hand for diverse accounts. Moving

further, the study presents potential risk

areas for the company and potential areas

of risk.

As the business transactions in the case

of CSL are complex, certain inherent

risks have higher likelihood of

occurrence.

Therefore, inherent risks are involved in

managing currency fluctuation and

interest rate risk, adherence to listing

rules, undertaking intricate business

accounting (that is to say, tax

calculation), difficulties in convergence

of audit as well as accounting standards

in global operations.

cash transactions. Again capital

development cost is also anon-routine

transaction that has the need of

comprehending capitalised rate as well

as timing. Different quantity of estimate

is also mentioned in the current study at

hand for diverse accounts. Moving

further, the study presents potential risk

areas for the company and potential areas

of risk.

As the business transactions in the case

of CSL are complex, certain inherent

risks have higher likelihood of

occurrence.

Therefore, inherent risks are involved in

managing currency fluctuation and

interest rate risk, adherence to listing

rules, undertaking intricate business

accounting (that is to say, tax

calculation), difficulties in convergence

of audit as well as accounting standards

in global operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Annualreports.com. (2018). [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_CSL_2016.pdf [Accessed 6

May 2018].

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and Assurance

Services 6e. Wiley.

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2015. Auditing & Assurance Services: A Systematic

Approach. Qing hua da xue chu ban she.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Annualreports.com. (2018). [online] Available at:

http://www.annualreports.com/HostedData/AnnualReports/PDF/ASX_CSL_2016.pdf [Accessed 6

May 2018].

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Leung, P., Coram, P., Cooper, B.J. and Richardson, P., 2014. Modern Auditing and Assurance

Services 6e. Wiley.

Messier, W.F., Glover, S.M. and Prawitt, D.F., 2015. Auditing & Assurance Services: A Systematic

Approach. Qing hua da xue chu ban she.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.