Audit and Assurance Report: Financial Analysis of DIPL's Performance

VerifiedAdded on 2020/03/02

|11

|2624

|227

Report

AI Summary

This report provides a detailed analysis of audit and assurance practices, focusing on the financial statements of DIPL. It begins by exploring the analytical approach, including financial ratios, and their interpretation. The report then delves into the inherent risks within DIPL's business operations, considering factors such as employee inexperience, environmental aspects, material misstatements, and CEO succession issues. Furthermore, it identifies and classifies various fraud risks, examining how pressure on the workforce and management can lead to fraudulent activities. The report also addresses the appropriateness of inventory valuation methods and assesses the potential for financial reporting risks. The analysis includes a review of liquidity, profitability, and solvency ratios, along with an examination of DIPL's financial performance. The report highlights areas of concern, such as declining profit margins and current ratios, and suggests improvements to mitigate risks and enhance financial performance. The report references multiple academic sources to support the findings and recommendations.

Running head: AUDIT AND ASSURANCE

Audit and Assurance

Name of Student:

Name of University:

Author’s Note:

Audit and Assurance

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT AND ASSURANCE

Question 1: Analytical Approach

The analytic approach to the economic declarations of the DIPL shows the method of the

dissemination of information from it. Analytic approach can be in the form of financial ratios.

With the help of analytic method of evaluation of financial announcements however,

several accountants as well as financial analysts can interpret the information for allowing the

arrival at crucial business decisions (Barr-Pulliam et al. 2017).

The case of the common sizing analytical way allows the assessment of the economic

announcements to a common reference point. This results in the possible contrast of the financial

statements in connection to the different timeframes or in relation to several entities. The

assessors can consider the several item lines shown in the economic report along with the

reporting method. For example, the way of registration of the items like assets, liabilities as well

as the owner’s equity in the economic reporting of the organisation along with the investigational

digression from the usual situation (Bayer and Cowell 2016). The method of benchmarking is

thought of as an analytic procedure and it should further be used for the audit plan assessment.

The variance of the actual fiscal declaration from the standard enables the recognition of the

deviation as well as helps in the evaluation of the reason of the recognised variance. Along with

this the analysis of the ratio could be adjudged as an effectual analytic method that can be used

for contrasting the financial declarations along with the audit plan assessment (Bepari and Mollik

2015).

Explanation:

Question 1: Analytical Approach

The analytic approach to the economic declarations of the DIPL shows the method of the

dissemination of information from it. Analytic approach can be in the form of financial ratios.

With the help of analytic method of evaluation of financial announcements however,

several accountants as well as financial analysts can interpret the information for allowing the

arrival at crucial business decisions (Barr-Pulliam et al. 2017).

The case of the common sizing analytical way allows the assessment of the economic

announcements to a common reference point. This results in the possible contrast of the financial

statements in connection to the different timeframes or in relation to several entities. The

assessors can consider the several item lines shown in the economic report along with the

reporting method. For example, the way of registration of the items like assets, liabilities as well

as the owner’s equity in the economic reporting of the organisation along with the investigational

digression from the usual situation (Bayer and Cowell 2016). The method of benchmarking is

thought of as an analytic procedure and it should further be used for the audit plan assessment.

The variance of the actual fiscal declaration from the standard enables the recognition of the

deviation as well as helps in the evaluation of the reason of the recognised variance. Along with

this the analysis of the ratio could be adjudged as an effectual analytic method that can be used

for contrasting the financial declarations along with the audit plan assessment (Bepari and Mollik

2015).

Explanation:

2AUDIT AND ASSURANCE

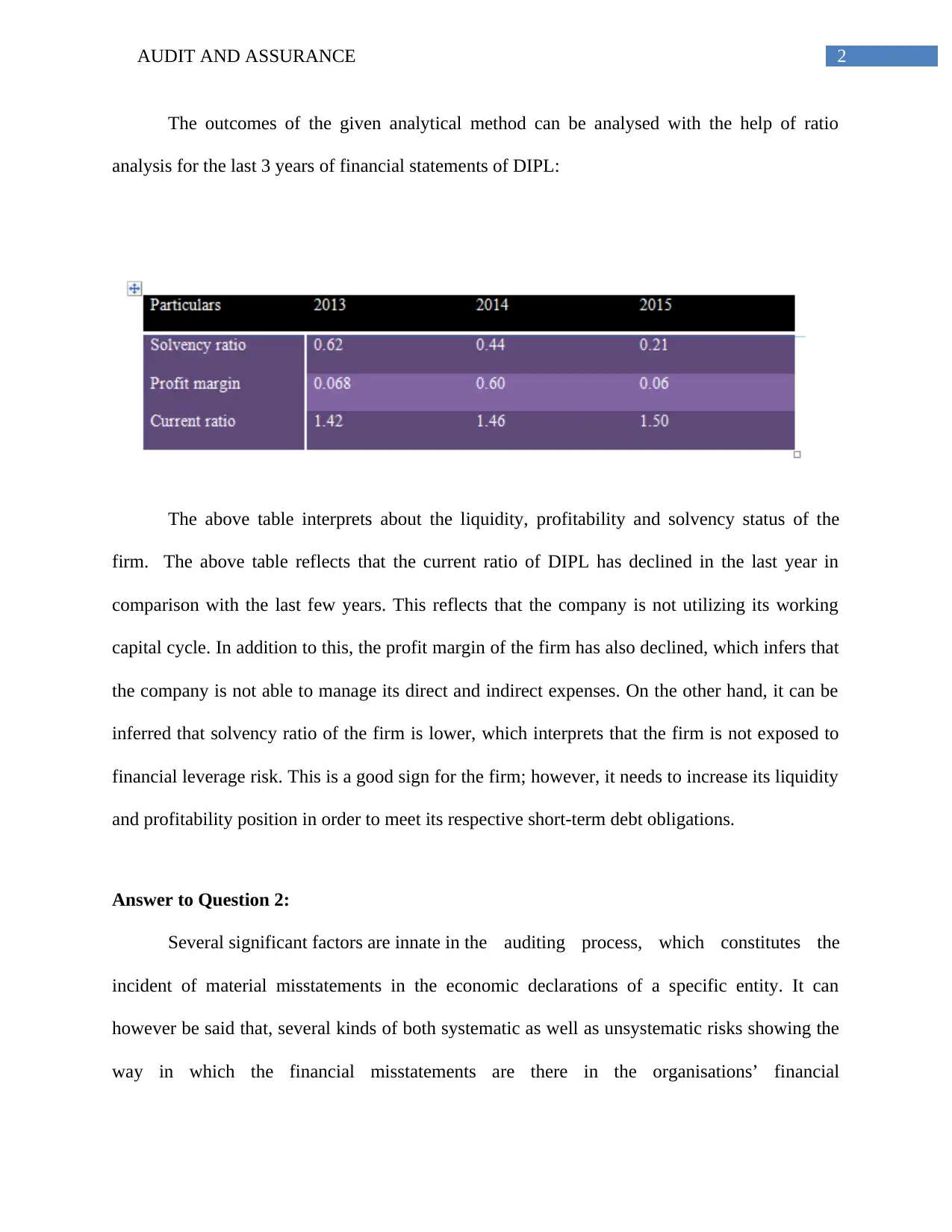

The outcomes of the given analytical method can be analysed with the help of ratio

analysis for the last 3 years of financial statements of DIPL:

The above table interprets about the liquidity, profitability and solvency status of the

firm. The above table reflects that the current ratio of DIPL has declined in the last year in

comparison with the last few years. This reflects that the company is not utilizing its working

capital cycle. In addition to this, the profit margin of the firm has also declined, which infers that

the company is not able to manage its direct and indirect expenses. On the other hand, it can be

inferred that solvency ratio of the firm is lower, which interprets that the firm is not exposed to

financial leverage risk. This is a good sign for the firm; however, it needs to increase its liquidity

and profitability position in order to meet its respective short-term debt obligations.

Answer to Question 2:

Several significant factors are innate in the auditing process, which constitutes the

incident of material misstatements in the economic declarations of a specific entity. It can

however be said that, several kinds of both systematic as well as unsystematic risks showing the

way in which the financial misstatements are there in the organisations’ financial

The outcomes of the given analytical method can be analysed with the help of ratio

analysis for the last 3 years of financial statements of DIPL:

The above table interprets about the liquidity, profitability and solvency status of the

firm. The above table reflects that the current ratio of DIPL has declined in the last year in

comparison with the last few years. This reflects that the company is not utilizing its working

capital cycle. In addition to this, the profit margin of the firm has also declined, which infers that

the company is not able to manage its direct and indirect expenses. On the other hand, it can be

inferred that solvency ratio of the firm is lower, which interprets that the firm is not exposed to

financial leverage risk. This is a good sign for the firm; however, it needs to increase its liquidity

and profitability position in order to meet its respective short-term debt obligations.

Answer to Question 2:

Several significant factors are innate in the auditing process, which constitutes the

incident of material misstatements in the economic declarations of a specific entity. It can

however be said that, several kinds of both systematic as well as unsystematic risks showing the

way in which the financial misstatements are there in the organisations’ financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT AND ASSURANCE

announcements. Additionally the identified risks may be due to financial as well as non-financial

factors which can subsequently prevent a specific entity in reflecting a just view of the economic

announcements. Based on the information from Devos and Zackrisson (2015), the detected risks

may be associated with several risks of omission connected with risks of several unimaginable

errors of a specific bookkeeper. Hence it can be said that it is the business risk for the DIPL’s

business operations.

Apart from this, the employees at DIPL are inexperienced and do not possess the

requisite proficiency that has escalated the total inherent risk of the organisation. Additionally,

such a lack of experience can result in the committing of errors or mistakes, thereby increasing

the inherent risks. This is due to the fact that the employees constitute a significant segment of

the company and it is not feasible for the firm to ensure its business success as well as its growth

in the future without the effective contributions from the employees. The other significant factors

contributing towards the inherent risk can be categorised into several segments like the external

as well as the ecological or environmental aspects as well as the materialistic misstatements in

the previous time points as well as the false exercises. The environmental aspects directing the

method towards the inherent risk comprises rapid alternations where the matters could arise

connected to the valuation of inventory, intense competition in the market as well as the lack of

sufficient money. Apart from this, there is the chance of materialistic misstatements that can

direct the DIPL towards the inherent risk in the years to come.

The analytical process of the current case of the DIPL shows the fact that the issues as

well as the complexities related to the CEO succession constitutes the inherent risks also. In core

it can be said that the succession of CEO is different as the candidates are individuals (Graham

2015). Hence, the commencement of the procedure, without complying to the strategy, delayed

announcements. Additionally the identified risks may be due to financial as well as non-financial

factors which can subsequently prevent a specific entity in reflecting a just view of the economic

announcements. Based on the information from Devos and Zackrisson (2015), the detected risks

may be associated with several risks of omission connected with risks of several unimaginable

errors of a specific bookkeeper. Hence it can be said that it is the business risk for the DIPL’s

business operations.

Apart from this, the employees at DIPL are inexperienced and do not possess the

requisite proficiency that has escalated the total inherent risk of the organisation. Additionally,

such a lack of experience can result in the committing of errors or mistakes, thereby increasing

the inherent risks. This is due to the fact that the employees constitute a significant segment of

the company and it is not feasible for the firm to ensure its business success as well as its growth

in the future without the effective contributions from the employees. The other significant factors

contributing towards the inherent risk can be categorised into several segments like the external

as well as the ecological or environmental aspects as well as the materialistic misstatements in

the previous time points as well as the false exercises. The environmental aspects directing the

method towards the inherent risk comprises rapid alternations where the matters could arise

connected to the valuation of inventory, intense competition in the market as well as the lack of

sufficient money. Apart from this, there is the chance of materialistic misstatements that can

direct the DIPL towards the inherent risk in the years to come.

The analytical process of the current case of the DIPL shows the fact that the issues as

well as the complexities related to the CEO succession constitutes the inherent risks also. In core

it can be said that the succession of CEO is different as the candidates are individuals (Graham

2015). Hence, the commencement of the procedure, without complying to the strategy, delayed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT AND ASSURANCE

initiation of the process, ineffective connection of the CEO as well as staff attrition may result in

an inherent risk.

The analysis of the case provided implies that the implementation procedure of the IT

system has caused certain issues. DIPL has a shortage of employees for managing the

implementation process as well as installation along with the reconciliation conduction as well as

the testing which should be primarily before the new arrangement at the period end.

Additionally, the initial assessment disclosed that numerous transactions carried out were

recorded in a suitable manner. Thus the results in material misstatements because of the inherent

factors that is an error of deletion in a specific economic announcement.

The DIPL staff members need to follow a suitable sequence for registering the receivable

accounts as well as ledgers connected to the accounts receivable. Along with this, the

reconciliation of the bank, is required to be properly recorded as well (Milonas et al. 2016).

Further, it can be said that the revenue registration found from the e-book and considering the

textbook reprinting in the future could possibly result in several inherent risks due to complexity

associated with the procedure. Thus the inventory valuation applicable to the raw materials at an

average cost is not at all suitable as the average cost is not apt, as the average cost is much below

the existing paper cost.

The discerned inherent risks can be adjudged as the susceptibility of a particular assertion

in connection to the materialistic misstatements and are shown briefly as follows:

Increasing burden on the employees as well as the management:

initiation of the process, ineffective connection of the CEO as well as staff attrition may result in

an inherent risk.

The analysis of the case provided implies that the implementation procedure of the IT

system has caused certain issues. DIPL has a shortage of employees for managing the

implementation process as well as installation along with the reconciliation conduction as well as

the testing which should be primarily before the new arrangement at the period end.

Additionally, the initial assessment disclosed that numerous transactions carried out were

recorded in a suitable manner. Thus the results in material misstatements because of the inherent

factors that is an error of deletion in a specific economic announcement.

The DIPL staff members need to follow a suitable sequence for registering the receivable

accounts as well as ledgers connected to the accounts receivable. Along with this, the

reconciliation of the bank, is required to be properly recorded as well (Milonas et al. 2016).

Further, it can be said that the revenue registration found from the e-book and considering the

textbook reprinting in the future could possibly result in several inherent risks due to complexity

associated with the procedure. Thus the inventory valuation applicable to the raw materials at an

average cost is not at all suitable as the average cost is not apt, as the average cost is much below

the existing paper cost.

The discerned inherent risks can be adjudged as the susceptibility of a particular assertion

in connection to the materialistic misstatements and are shown briefly as follows:

Increasing burden on the employees as well as the management:

5AUDIT AND ASSURANCE

It is because of the increasing burden of work on the DIPL staff, that it has resulted in the

inaccurate bookkeeping. As a result, several attributes have occurred that include the propensity

in encountering the cash flow, operating results as well as the poor liquidity.

Risk of errors due to incorrect representation:

Intricacy as well as dependability is inherent because of the risk related with the errors as

well wrong interpretation in a simultaneous manner.

Overall management integrity:

According to the case study, the DIPL’s management possess the lack of integrity it is

desired that it will be ready for any possible loss in the business community.

Abnormal pressure on the management:

Occasionally it so happens that there exist incentives for the management. As a result

financial announcements have several misstatements (Nalewaik and Mills 2016).

Nature of the business entity:

DIPL contributes to the major growth in economic as well as circumstances of

competitive nature. Additionally, these aspects might have an influence on the underlying risks

of the business entities for the audit planning assessment in a suitable fashion.

It is because of the increasing burden of work on the DIPL staff, that it has resulted in the

inaccurate bookkeeping. As a result, several attributes have occurred that include the propensity

in encountering the cash flow, operating results as well as the poor liquidity.

Risk of errors due to incorrect representation:

Intricacy as well as dependability is inherent because of the risk related with the errors as

well wrong interpretation in a simultaneous manner.

Overall management integrity:

According to the case study, the DIPL’s management possess the lack of integrity it is

desired that it will be ready for any possible loss in the business community.

Abnormal pressure on the management:

Occasionally it so happens that there exist incentives for the management. As a result

financial announcements have several misstatements (Nalewaik and Mills 2016).

Nature of the business entity:

DIPL contributes to the major growth in economic as well as circumstances of

competitive nature. Additionally, these aspects might have an influence on the underlying risks

of the business entities for the audit planning assessment in a suitable fashion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT AND ASSURANCE

Answer to question 3:

Answer to part A:

According to Saad (2014), the risks of fraud, could probably result in severe losses of the

assets because of several fraudulent activities. The motivational lack in the workforce due to the

additional pressure of work on the staff could probably influence them to get involved in several

fraudulent activities. With this, the expectations form several groups of investors in the reporting

of specific financial results or particularly in case of the management in achieving the suitable

targets of performance had a chance of resulting in significantly increased fraud risks. Further,

strong amount of pressure is exerted on the management of the corporation in order to announce

specific economic results in a bid to avert the generation of the guarantees.

The main types of risks identified in the context of DIPL’s business operations are briefly

classified as follows:

Types of risk Identification

Engagement of the total workforce in fraudulent

activities

The case study provided conforming to the

operations of the DIPL states that the board has put

immense pressure on the company in acquiring an

innovative system of accounting. Such additional

staff pressure in performing the new information

installation process for accounting may result in

fraud. This implies that the staff may be involved in

fraudulent activities for managing the behaviours as

well as the reconciliation process in an effective

fashion, and also the materialistic misstatements.

Answer to question 3:

Answer to part A:

According to Saad (2014), the risks of fraud, could probably result in severe losses of the

assets because of several fraudulent activities. The motivational lack in the workforce due to the

additional pressure of work on the staff could probably influence them to get involved in several

fraudulent activities. With this, the expectations form several groups of investors in the reporting

of specific financial results or particularly in case of the management in achieving the suitable

targets of performance had a chance of resulting in significantly increased fraud risks. Further,

strong amount of pressure is exerted on the management of the corporation in order to announce

specific economic results in a bid to avert the generation of the guarantees.

The main types of risks identified in the context of DIPL’s business operations are briefly

classified as follows:

Types of risk Identification

Engagement of the total workforce in fraudulent

activities

The case study provided conforming to the

operations of the DIPL states that the board has put

immense pressure on the company in acquiring an

innovative system of accounting. Such additional

staff pressure in performing the new information

installation process for accounting may result in

fraud. This implies that the staff may be involved in

fraudulent activities for managing the behaviours as

well as the reconciliation process in an effective

fashion, and also the materialistic misstatements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT AND ASSURANCE

The provide case shows, that the ineffective

management of the process execution connected to

the implementation of the information technology

for the accounting results system in incorrect

allotment of several transactions at the period end.

This results in severe loss due to the material

misstatements as well as fraudulent risks (DeFond

and Zhang 2014).

Way pertaining to economic reporting Another risk of fraud that may confront the DIPL’s

business operations may take the risk related to the

financial reporting fraud into account. At the time

of certain situations, it has been found that there is

additional expectation from the management or

from the external financers. This form of

expectation is to achieve the particular targets of

the performance of different goals to qualify for

obtaining debt. There is enhanced risk of incorrect

declarations of a financial nature. Based on the

DIPL’s balance sheet statement the net revenue of

the organisation has increased. Gross and net

income has also increased. Current assets have also

escalated. Due to the failure of the organisation in

maintaining the standard yardsticks, the

organisation became ineligible in acquiring funds.

The provide case shows, that the ineffective

management of the process execution connected to

the implementation of the information technology

for the accounting results system in incorrect

allotment of several transactions at the period end.

This results in severe loss due to the material

misstatements as well as fraudulent risks (DeFond

and Zhang 2014).

Way pertaining to economic reporting Another risk of fraud that may confront the DIPL’s

business operations may take the risk related to the

financial reporting fraud into account. At the time

of certain situations, it has been found that there is

additional expectation from the management or

from the external financers. This form of

expectation is to achieve the particular targets of

the performance of different goals to qualify for

obtaining debt. There is enhanced risk of incorrect

declarations of a financial nature. Based on the

DIPL’s balance sheet statement the net revenue of

the organisation has increased. Gross and net

income has also increased. Current assets have also

escalated. Due to the failure of the organisation in

maintaining the standard yardsticks, the

organisation became ineligible in acquiring funds.

8AUDIT AND ASSURANCE

Answer to Part B:

Depending on the provided case study, it can be stated that the evaluation method

associated with the inventory valuation of several raw materials at specific average costs is not

appropriate. This is because the existing cost of paper is higher considerably that the average

cost. The risk connected with the financial reporting could have been recognised by the

dissection of the financial statements on part of the assessors. Benchmarking is thought of as an

analytic process and could be utilised for the audit plan assessment. The real financial

declaration from the yardstick helps in the recognising of the deviation and helps in the

evaluation of the recognised variance.

Answer to Part B:

Depending on the provided case study, it can be stated that the evaluation method

associated with the inventory valuation of several raw materials at specific average costs is not

appropriate. This is because the existing cost of paper is higher considerably that the average

cost. The risk connected with the financial reporting could have been recognised by the

dissection of the financial statements on part of the assessors. Benchmarking is thought of as an

analytic process and could be utilised for the audit plan assessment. The real financial

declaration from the yardstick helps in the recognising of the deviation and helps in the

evaluation of the recognised variance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT AND ASSURANCE

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

References:

Barr-Pulliam, D., Nkansa, P., Walker, K., appreciate helpful comments from Helen, W., Brown-

Liburd, A.G. and Stefaniak, C., 2017. From Compliance to Strategy: Using the Three Lines of

Defense Model to Evaluate and Motivate Internal Audit Contributions to Accounting Research.

Bayer, R. and Cowell, F., 2016. Tax compliance by firms and audit policy. Research in

Economics, 70(1), pp.38-52.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bryce, M., Ali, M.J. and Mather, P.R., 2015. Accounting quality in the pre-/post-IFRS adoption

periods and the impact on audit committee effectiveness—Evidence from Australia. Pacific-

Basin Finance Journal, 35, pp.163-181.

Cason, T.N., Friesen, L. and Gangadharan, L., 2016. Regulatory performance of audit

tournaments and compliance observability. European Economic Review, 85, pp.288-306.

DeFond, M. and Zhang, J., 2014. A review of archival auditing research. Journal of Accounting

and Economics, 58(2), pp.275-326.

Devos, K. and Zackrisson, M., 2015. Tax compliance and the public disclosure of tax

information: An Australia/Norway comparison. eJournal of Tax Research, 13(1), p.108.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT AND ASSURANCE

Gani, I., Wijeweera, A. and Eddie, I., 2017. Audit Committee Compliance and Company

Performance Nexus: Evidence from ASX Listed Companies. Business and Economic

Research, 7(2), pp.135-145.

Graham, L., 2015. Internal Control Audit and Compliance: Documentation and Testing Under

the New COSO Framework. John Wiley & Sons.

Gray, S.E., Sekendiz, B., Norton, K., Dietrich, J., Keyzer, P., Coyle, I.R. and Finch, C., 2016.

The development and application of an observational audit tool for use in Australian fitness

facilities. Journal of Fitness Research, 5(1), p.29.

Milonas, A., Hutchinson, A., Charlesworth, D., Doric, A., Green, J. and Considine, J., 2016. Post

resuscitation management of cardiac arrest patients in the critical care environment: A

retrospective audit of compliance with evidence based guidelines. Australian Critical Care.

Mumford, V., Greenfield, D., Hogden, A., Debono, D., Gospodarevskaya, E., Forde, K.,

Westbrook, J. and Braithwaite, J., 2014. Disentangling quality and safety indicator data: a

longitudinal, comparative study of hand hygiene compliance and accreditation outcomes in 96

Australian hospitals. BMJ open, 4(9), p.e005284.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

Gani, I., Wijeweera, A. and Eddie, I., 2017. Audit Committee Compliance and Company

Performance Nexus: Evidence from ASX Listed Companies. Business and Economic

Research, 7(2), pp.135-145.

Graham, L., 2015. Internal Control Audit and Compliance: Documentation and Testing Under

the New COSO Framework. John Wiley & Sons.

Gray, S.E., Sekendiz, B., Norton, K., Dietrich, J., Keyzer, P., Coyle, I.R. and Finch, C., 2016.

The development and application of an observational audit tool for use in Australian fitness

facilities. Journal of Fitness Research, 5(1), p.29.

Milonas, A., Hutchinson, A., Charlesworth, D., Doric, A., Green, J. and Considine, J., 2016. Post

resuscitation management of cardiac arrest patients in the critical care environment: A

retrospective audit of compliance with evidence based guidelines. Australian Critical Care.

Mumford, V., Greenfield, D., Hogden, A., Debono, D., Gospodarevskaya, E., Forde, K.,

Westbrook, J. and Braithwaite, J., 2014. Disentangling quality and safety indicator data: a

longitudinal, comparative study of hand hygiene compliance and accreditation outcomes in 96

Australian hospitals. BMJ open, 4(9), p.e005284.

Nalewaik, A. and Mills, A., 2016. Project Performance Review: Capturing the Value of Audit,

Oversight, and Compliance for Project Success. CRC Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.