Comprehensive Financial Audit Report Analysis for DIPL

VerifiedAdded on 2020/03/04

|11

|1950

|376

Report

AI Summary

This report presents a comprehensive analysis of an audit conducted on DIPL's financial statements. It begins with an overview of the audit process, emphasizing the importance of both substantive and analytical audit procedures. The report then delves into the inherent risks associated with DIPL, including those related to non-routine transactions, the implementation of a new IT system, and changes in accounting policies. It identifies potential material misstatements arising from these risks. Furthermore, the report addresses fraud risks, particularly those linked to the IT system installation and the lack of segregation of duties within the company. The auditor's approach to mitigating these risks is discussed, highlighting the need for thorough document review, reconciliation, and the implementation of robust internal controls. The report concludes by emphasizing the auditor's role in providing assurance on the fairness of financial statements and the importance of addressing potential fraud.

By student name

Professor

University

Date: 18 August 2017.

Professor

University

Date: 18 August 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

Contents

Question no 1…………………………………………………………………...2

Question no 2…………………………………………………………………...6

Question no 3…………………………………………………………….....….8

Refrences.....……………………………………………………………….......10

1 | P a g e

2

Question no 1

The process of audit is integral to the business and viability of the financial statements prepared

by the entity. It gives the reasonable assurance to the management, users of the financial statements,

both internal and external that proper procedures have been followed while preparing it and utmost

care has been taken as it carries the decision making of many stakeholders. Audit is an independent

examination of the books of accounts of the entity, whether profit oriented or not, with the view to

express an opinion that it has been prepared on the unbiased basis and it follows the respective

financial reporting framework prescribed by various international bodies. The foremost responsibility of

the auditor is not to find out the frauds and errors committed by the management but to highlight the

key financial designs being followed by the entity and whether it is sufficient or not. There are various

audit procedures being followed by the auditor which mainly includes substantive audit procedures and

analytical audit procedures (Knechel & Salterio 2016). Substantive audit procedures are those, which

deal with checking of the various documents and supporting for financial transactions entered into in

the current financial year, this gives assurance that the consistency in maintaining the books of accounts

is being followed. This include vouching of incomes and expenses incurred and recorded in the books in

the mentioned period & verification of assets and liabilities as recorded in balance sheets at the end of

the period. But in case the view is not clear on the financials & the auditor wants to investigate further,

then he has to resort to the analytical procedures which includes analysis of key financial ratios, trend

analysis, comparison of the actual data of the company with the planned or forecasted data, budgetary

and variance analysis. The nature timing and extent of the audit procedures to be undertaken by the

auditors while performing the audit is determined by the results of these preliminary analytical

procedures. If the internal financial control were weak, more would be the risk and more would be audit

procedures red and vice versa. All this helps the auditor to comment on whether there are risks of any

material misstatements in the financial accounts prepared (Grenier 2017).

Further, in case of given case of DIPL, the new auditors are taking over from the old auditors, so

the extent of checking would be increased in order to validate the opening balances of the concern.

Besides this, audit planning as to what will be the critical areas to be checked, what will be auf=did

procedures, what is the time to be given to a particular area, what all needs to be discussed with the

management also depends on the results of the these analytical procedures. Moreover, since the

industry data is not available, we have just kept our discussion and analysis to the ratio analysis and the

trend for the last 3 years (Jones 2017).

2 | P a g e

Question no 1

The process of audit is integral to the business and viability of the financial statements prepared

by the entity. It gives the reasonable assurance to the management, users of the financial statements,

both internal and external that proper procedures have been followed while preparing it and utmost

care has been taken as it carries the decision making of many stakeholders. Audit is an independent

examination of the books of accounts of the entity, whether profit oriented or not, with the view to

express an opinion that it has been prepared on the unbiased basis and it follows the respective

financial reporting framework prescribed by various international bodies. The foremost responsibility of

the auditor is not to find out the frauds and errors committed by the management but to highlight the

key financial designs being followed by the entity and whether it is sufficient or not. There are various

audit procedures being followed by the auditor which mainly includes substantive audit procedures and

analytical audit procedures (Knechel & Salterio 2016). Substantive audit procedures are those, which

deal with checking of the various documents and supporting for financial transactions entered into in

the current financial year, this gives assurance that the consistency in maintaining the books of accounts

is being followed. This include vouching of incomes and expenses incurred and recorded in the books in

the mentioned period & verification of assets and liabilities as recorded in balance sheets at the end of

the period. But in case the view is not clear on the financials & the auditor wants to investigate further,

then he has to resort to the analytical procedures which includes analysis of key financial ratios, trend

analysis, comparison of the actual data of the company with the planned or forecasted data, budgetary

and variance analysis. The nature timing and extent of the audit procedures to be undertaken by the

auditors while performing the audit is determined by the results of these preliminary analytical

procedures. If the internal financial control were weak, more would be the risk and more would be audit

procedures red and vice versa. All this helps the auditor to comment on whether there are risks of any

material misstatements in the financial accounts prepared (Grenier 2017).

Further, in case of given case of DIPL, the new auditors are taking over from the old auditors, so

the extent of checking would be increased in order to validate the opening balances of the concern.

Besides this, audit planning as to what will be the critical areas to be checked, what will be auf=did

procedures, what is the time to be given to a particular area, what all needs to be discussed with the

management also depends on the results of the these analytical procedures. Moreover, since the

industry data is not available, we have just kept our discussion and analysis to the ratio analysis and the

trend for the last 3 years (Jones 2017).

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

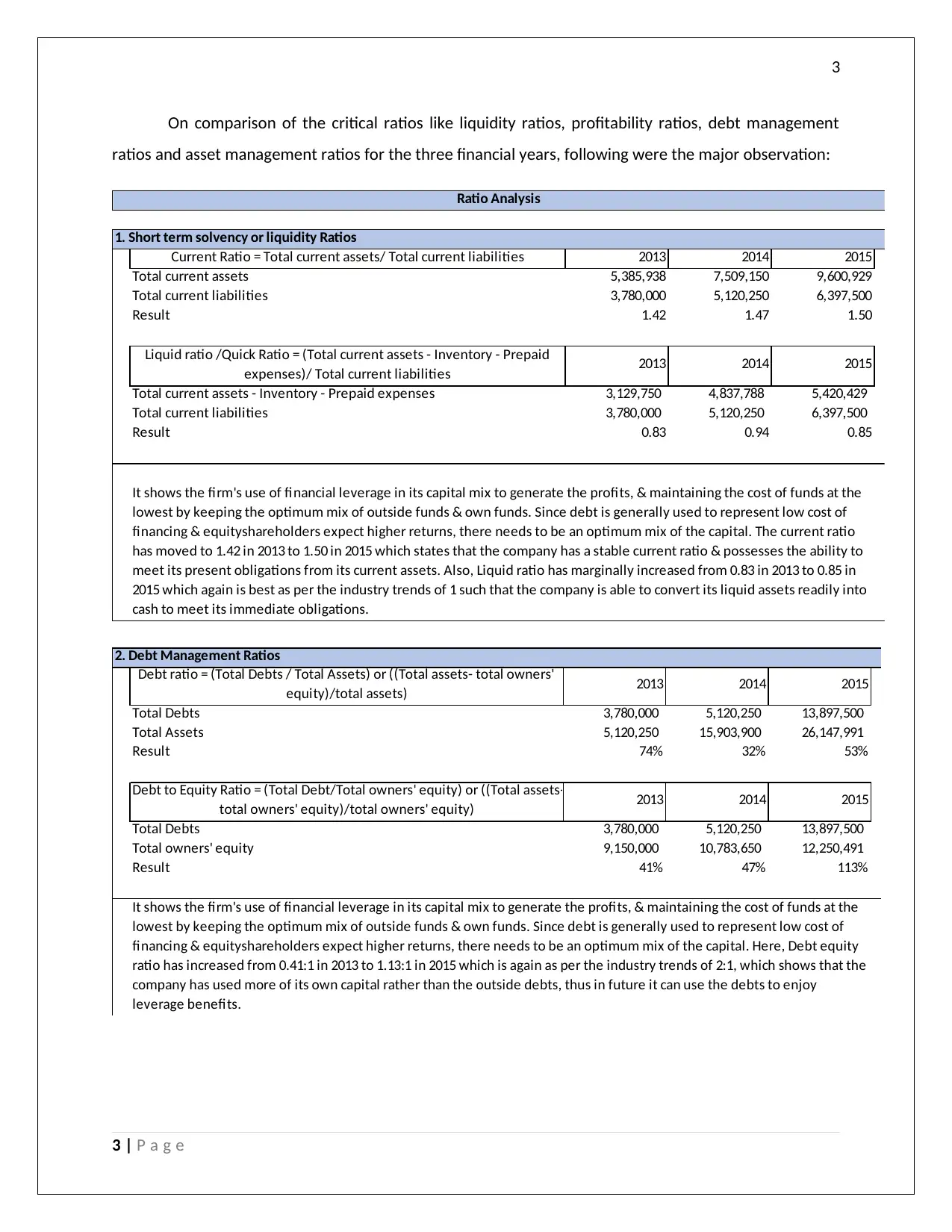

On comparison of the critical ratios like liquidity ratios, profitability ratios, debt management

ratios and asset management ratios for the three financial years, following were the major observation:

1. Short term solvency or liquidity Ratios

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

Ratio Analysis

It shows the firm's use of financial leverage in its capital mix to generate the profits, & maintaining the cost of funds at the

lowest by keeping the optimum mix of outside funds & own funds. Since debt is generally used to represent low cost of

financing & equityshareholders expect higher returns, there needs to be an optimum mix of the capital. The current ratio

has moved to 1.42 in 2013 to 1.50 in 2015 which states that the company has a stable current ratio & possesses the ability to

meet its present obligations from its current assets. Also, Liquid ratio has marginally increased from 0.83 in 2013 to 0.85 in

2015 which again is best as per the industry trends of 1 such that the company is able to convert its liquid assets readily into

cash to meet its immediate obligations.

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

2. Debt Management Ratios

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

It shows the firm's use of financial leverage in its capital mix to generate the profits, & maintaining the cost of funds at the

lowest by keeping the optimum mix of outside funds & own funds. Since debt is generally used to represent low cost of

financing & equityshareholders expect higher returns, there needs to be an optimum mix of the capital. Here, Debt equity

ratio has increased from 0.41:1 in 2013 to 1.13:1 in 2015 which is again as per the industry trends of 2:1, which shows that the

company has used more of its own capital rather than the outside debts, thus in future it can use the debts to enjoy

leverage benefits.

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total assets-

total owners' equity)/total owners' equity)

3 | P a g e

On comparison of the critical ratios like liquidity ratios, profitability ratios, debt management

ratios and asset management ratios for the three financial years, following were the major observation:

1. Short term solvency or liquidity Ratios

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85

Ratio Analysis

It shows the firm's use of financial leverage in its capital mix to generate the profits, & maintaining the cost of funds at the

lowest by keeping the optimum mix of outside funds & own funds. Since debt is generally used to represent low cost of

financing & equityshareholders expect higher returns, there needs to be an optimum mix of the capital. The current ratio

has moved to 1.42 in 2013 to 1.50 in 2015 which states that the company has a stable current ratio & possesses the ability to

meet its present obligations from its current assets. Also, Liquid ratio has marginally increased from 0.83 in 2013 to 0.85 in

2015 which again is best as per the industry trends of 1 such that the company is able to convert its liquid assets readily into

cash to meet its immediate obligations.

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

2. Debt Management Ratios

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53%

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113%

It shows the firm's use of financial leverage in its capital mix to generate the profits, & maintaining the cost of funds at the

lowest by keeping the optimum mix of outside funds & own funds. Since debt is generally used to represent low cost of

financing & equityshareholders expect higher returns, there needs to be an optimum mix of the capital. Here, Debt equity

ratio has increased from 0.41:1 in 2013 to 1.13:1 in 2015 which is again as per the industry trends of 2:1, which shows that the

company has used more of its own capital rather than the outside debts, thus in future it can use the debts to enjoy

leverage benefits.

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total assets-

total owners' equity)/total owners' equity)

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

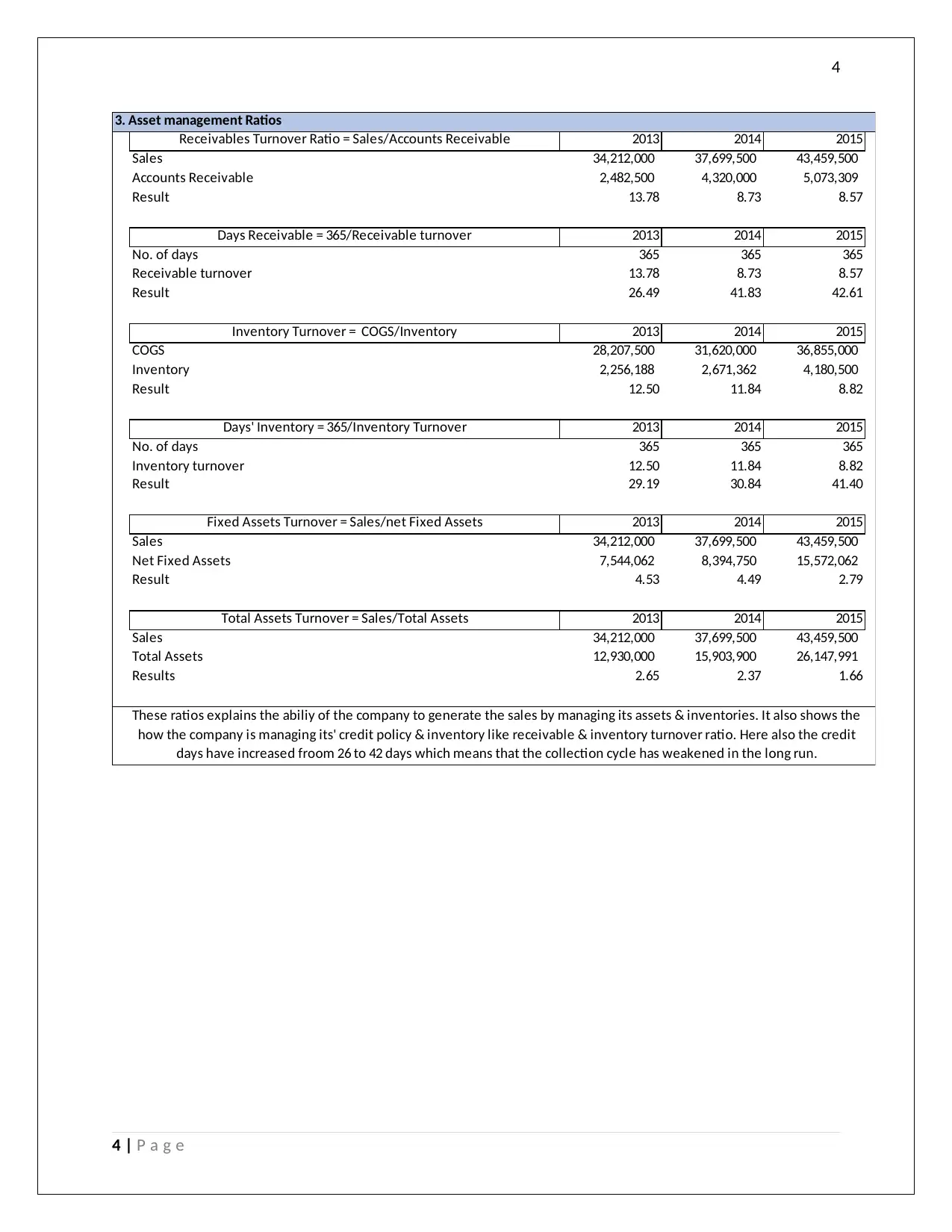

3. Asset management Ratios

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

These ratios explains the abiliy of the company to generate the sales by managing its assets & inventories. It also shows the

how the company is managing its' credit policy & inventory like receivable & inventory turnover ratio. Here also the credit

days have increased froom 26 to 42 days which means that the collection cycle has weakened in the long run.

4 | P a g e

3. Asset management Ratios

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991

Results 2.65 2.37 1.66

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

These ratios explains the abiliy of the company to generate the sales by managing its assets & inventories. It also shows the

how the company is managing its' credit policy & inventory like receivable & inventory turnover ratio. Here also the credit

days have increased froom 26 to 42 days which means that the collection cycle has weakened in the long run.

4 | P a g e

5

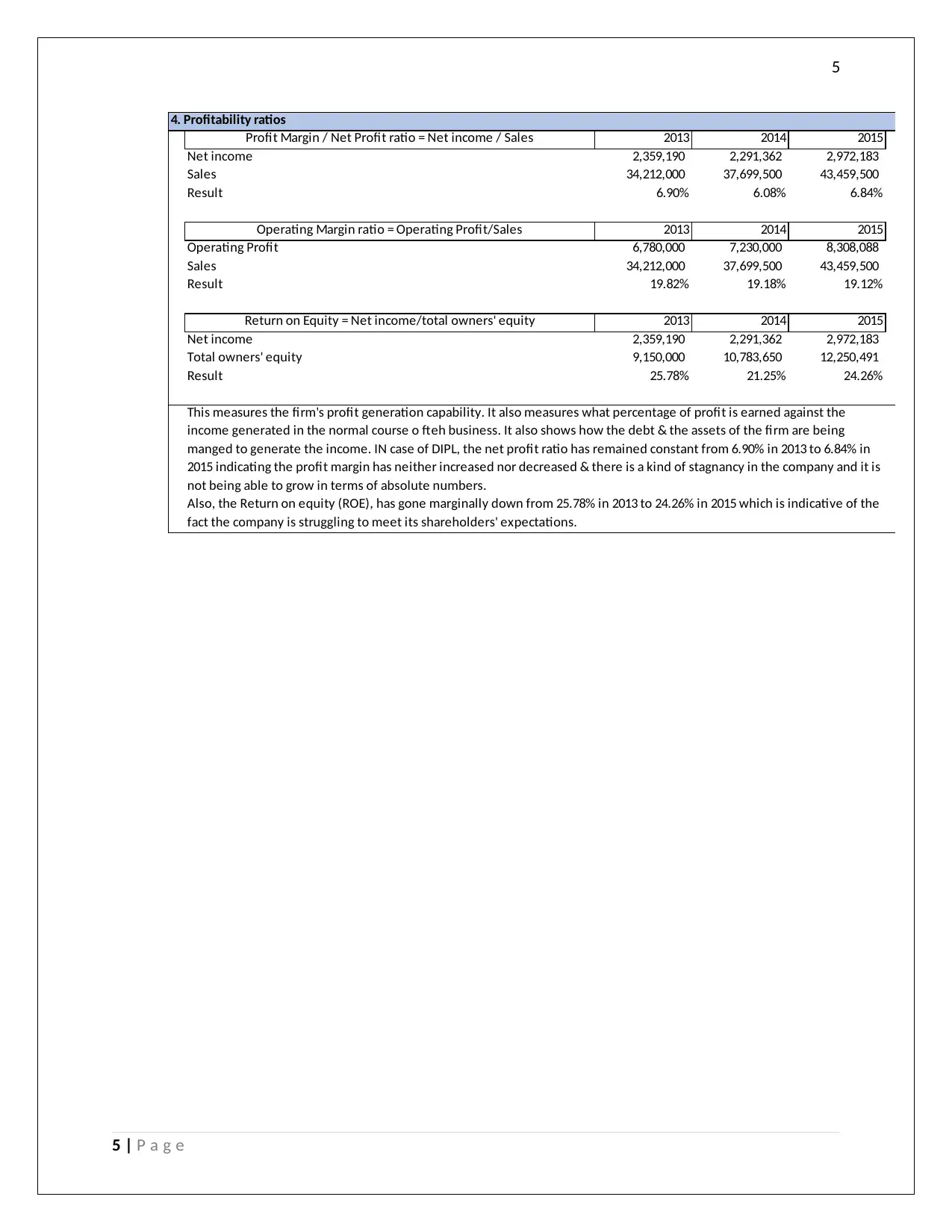

4. Profitability ratios

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

This measures the firm's profit generation capability. It also measures what percentage of profit is earned against the

income generated in the normal course o fteh business. It also shows how the debt & the assets of the firm are being

manged to generate the income. IN case of DIPL, the net profit ratio has remained constant from 6.90% in 2013 to 6.84% in

2015 indicating the profit margin has neither increased nor decreased & there is a kind of stagnancy in the company and it is

not being able to grow in terms of absolute numbers.

Also, the Return on equity (ROE), has gone marginally down from 25.78% in 2013 to 24.26% in 2015 which is indicative of the

fact the company is struggling to meet its shareholders' expectations.

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

5 | P a g e

4. Profitability ratios

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84%

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12%

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26%

This measures the firm's profit generation capability. It also measures what percentage of profit is earned against the

income generated in the normal course o fteh business. It also shows how the debt & the assets of the firm are being

manged to generate the income. IN case of DIPL, the net profit ratio has remained constant from 6.90% in 2013 to 6.84% in

2015 indicating the profit margin has neither increased nor decreased & there is a kind of stagnancy in the company and it is

not being able to grow in terms of absolute numbers.

Also, the Return on equity (ROE), has gone marginally down from 25.78% in 2013 to 24.26% in 2015 which is indicative of the

fact the company is struggling to meet its shareholders' expectations.

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

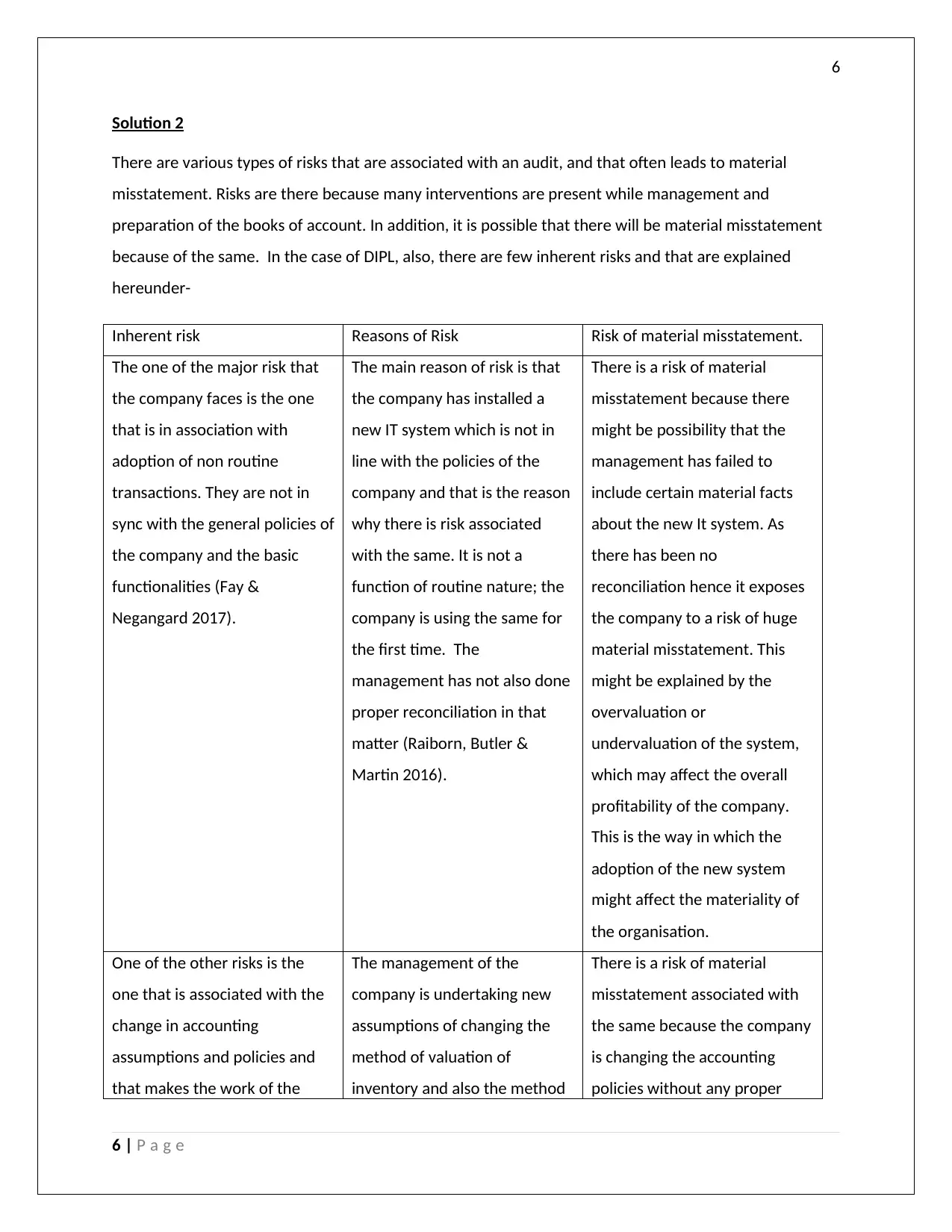

Solution 2

There are various types of risks that are associated with an audit, and that often leads to material

misstatement. Risks are there because many interventions are present while management and

preparation of the books of account. In addition, it is possible that there will be material misstatement

because of the same. In the case of DIPL, also, there are few inherent risks and that are explained

hereunder-

Inherent risk Reasons of Risk Risk of material misstatement.

The one of the major risk that

the company faces is the one

that is in association with

adoption of non routine

transactions. They are not in

sync with the general policies of

the company and the basic

functionalities (Fay &

Negangard 2017).

The main reason of risk is that

the company has installed a

new IT system which is not in

line with the policies of the

company and that is the reason

why there is risk associated

with the same. It is not a

function of routine nature; the

company is using the same for

the first time. The

management has not also done

proper reconciliation in that

matter (Raiborn, Butler &

Martin 2016).

There is a risk of material

misstatement because there

might be possibility that the

management has failed to

include certain material facts

about the new It system. As

there has been no

reconciliation hence it exposes

the company to a risk of huge

material misstatement. This

might be explained by the

overvaluation or

undervaluation of the system,

which may affect the overall

profitability of the company.

This is the way in which the

adoption of the new system

might affect the materiality of

the organisation.

One of the other risks is the

one that is associated with the

change in accounting

assumptions and policies and

that makes the work of the

The management of the

company is undertaking new

assumptions of changing the

method of valuation of

inventory and also the method

There is a risk of material

misstatement associated with

the same because the company

is changing the accounting

policies without any proper

6 | P a g e

Solution 2

There are various types of risks that are associated with an audit, and that often leads to material

misstatement. Risks are there because many interventions are present while management and

preparation of the books of account. In addition, it is possible that there will be material misstatement

because of the same. In the case of DIPL, also, there are few inherent risks and that are explained

hereunder-

Inherent risk Reasons of Risk Risk of material misstatement.

The one of the major risk that

the company faces is the one

that is in association with

adoption of non routine

transactions. They are not in

sync with the general policies of

the company and the basic

functionalities (Fay &

Negangard 2017).

The main reason of risk is that

the company has installed a

new IT system which is not in

line with the policies of the

company and that is the reason

why there is risk associated

with the same. It is not a

function of routine nature; the

company is using the same for

the first time. The

management has not also done

proper reconciliation in that

matter (Raiborn, Butler &

Martin 2016).

There is a risk of material

misstatement because there

might be possibility that the

management has failed to

include certain material facts

about the new It system. As

there has been no

reconciliation hence it exposes

the company to a risk of huge

material misstatement. This

might be explained by the

overvaluation or

undervaluation of the system,

which may affect the overall

profitability of the company.

This is the way in which the

adoption of the new system

might affect the materiality of

the organisation.

One of the other risks is the

one that is associated with the

change in accounting

assumptions and policies and

that makes the work of the

The management of the

company is undertaking new

assumptions of changing the

method of valuation of

inventory and also the method

There is a risk of material

misstatement associated with

the same because the company

is changing the accounting

policies without any proper

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

auditor difficult. of depreciation. The new CEO

wants to calculate depreciation

by considering life of the asset

to be 30 years whereas the

industry standards say that the

life will be 20 years. It is not

based on any research and is

only based on the experience of

the individual. So there are high

chances of inherent risk

involved in the same because it

is not in the hands of the

individual but in the hands of

the management (DeZoort &

Harrison 2016).

research and that might have

some material effects on the

books of account of the

company. It is thus important

on part of the management to

ascertain that all the necessary

disclosures are properly given.

All the details are properly

recorded and before making

any changes in the accounting

estimates that might affect the

overall materiality of the

company. The management

must conduct research and

analysis on his part and then

take such important decisions

in regard with the functioning

of the company. All risks of

material misstatement must be

avoided by the company and

the auditor must properly verify

all avenues to do the same.

Solution 3

7 | P a g e

auditor difficult. of depreciation. The new CEO

wants to calculate depreciation

by considering life of the asset

to be 30 years whereas the

industry standards say that the

life will be 20 years. It is not

based on any research and is

only based on the experience of

the individual. So there are high

chances of inherent risk

involved in the same because it

is not in the hands of the

individual but in the hands of

the management (DeZoort &

Harrison 2016).

research and that might have

some material effects on the

books of account of the

company. It is thus important

on part of the management to

ascertain that all the necessary

disclosures are properly given.

All the details are properly

recorded and before making

any changes in the accounting

estimates that might affect the

overall materiality of the

company. The management

must conduct research and

analysis on his part and then

take such important decisions

in regard with the functioning

of the company. All risks of

material misstatement must be

avoided by the company and

the auditor must properly verify

all avenues to do the same.

Solution 3

7 | P a g e

8

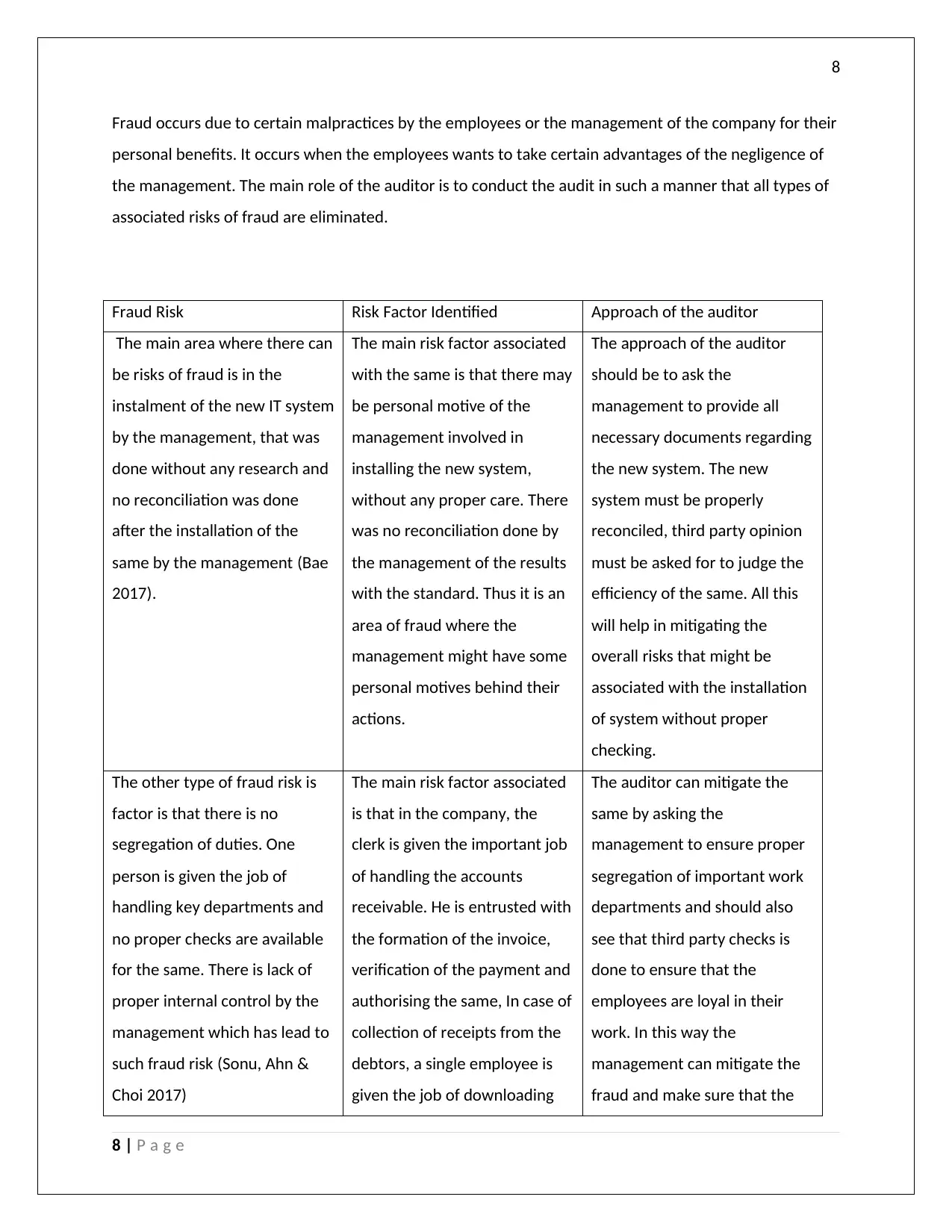

Fraud occurs due to certain malpractices by the employees or the management of the company for their

personal benefits. It occurs when the employees wants to take certain advantages of the negligence of

the management. The main role of the auditor is to conduct the audit in such a manner that all types of

associated risks of fraud are eliminated.

Fraud Risk Risk Factor Identified Approach of the auditor

The main area where there can

be risks of fraud is in the

instalment of the new IT system

by the management, that was

done without any research and

no reconciliation was done

after the installation of the

same by the management (Bae

2017).

The main risk factor associated

with the same is that there may

be personal motive of the

management involved in

installing the new system,

without any proper care. There

was no reconciliation done by

the management of the results

with the standard. Thus it is an

area of fraud where the

management might have some

personal motives behind their

actions.

The approach of the auditor

should be to ask the

management to provide all

necessary documents regarding

the new system. The new

system must be properly

reconciled, third party opinion

must be asked for to judge the

efficiency of the same. All this

will help in mitigating the

overall risks that might be

associated with the installation

of system without proper

checking.

The other type of fraud risk is

factor is that there is no

segregation of duties. One

person is given the job of

handling key departments and

no proper checks are available

for the same. There is lack of

proper internal control by the

management which has lead to

such fraud risk (Sonu, Ahn &

Choi 2017)

The main risk factor associated

is that in the company, the

clerk is given the important job

of handling the accounts

receivable. He is entrusted with

the formation of the invoice,

verification of the payment and

authorising the same, In case of

collection of receipts from the

debtors, a single employee is

given the job of downloading

The auditor can mitigate the

same by asking the

management to ensure proper

segregation of important work

departments and should also

see that third party checks is

done to ensure that the

employees are loyal in their

work. In this way the

management can mitigate the

fraud and make sure that the

8 | P a g e

Fraud occurs due to certain malpractices by the employees or the management of the company for their

personal benefits. It occurs when the employees wants to take certain advantages of the negligence of

the management. The main role of the auditor is to conduct the audit in such a manner that all types of

associated risks of fraud are eliminated.

Fraud Risk Risk Factor Identified Approach of the auditor

The main area where there can

be risks of fraud is in the

instalment of the new IT system

by the management, that was

done without any research and

no reconciliation was done

after the installation of the

same by the management (Bae

2017).

The main risk factor associated

with the same is that there may

be personal motive of the

management involved in

installing the new system,

without any proper care. There

was no reconciliation done by

the management of the results

with the standard. Thus it is an

area of fraud where the

management might have some

personal motives behind their

actions.

The approach of the auditor

should be to ask the

management to provide all

necessary documents regarding

the new system. The new

system must be properly

reconciled, third party opinion

must be asked for to judge the

efficiency of the same. All this

will help in mitigating the

overall risks that might be

associated with the installation

of system without proper

checking.

The other type of fraud risk is

factor is that there is no

segregation of duties. One

person is given the job of

handling key departments and

no proper checks are available

for the same. There is lack of

proper internal control by the

management which has lead to

such fraud risk (Sonu, Ahn &

Choi 2017)

The main risk factor associated

is that in the company, the

clerk is given the important job

of handling the accounts

receivable. He is entrusted with

the formation of the invoice,

verification of the payment and

authorising the same, In case of

collection of receipts from the

debtors, a single employee is

given the job of downloading

The auditor can mitigate the

same by asking the

management to ensure proper

segregation of important work

departments and should also

see that third party checks is

done to ensure that the

employees are loyal in their

work. In this way the

management can mitigate the

fraud and make sure that the

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

the receipts, verifying the

payments, and entering them

in the books of the company

and also verify the same. This

leads to a major disability on

part of the accounts

maintenance and

establishment of proper

control.

employees are doing their work

effectively. And also proper

internal control measures must

be established that will be very

helpful for the organisation,

and also for the auditor. It will

reduce the overall chances of

risk on part of the

management.

References

9 | P a g e

the receipts, verifying the

payments, and entering them

in the books of the company

and also verify the same. This

leads to a major disability on

part of the accounts

maintenance and

establishment of proper

control.

employees are doing their work

effectively. And also proper

internal control measures must

be established that will be very

helpful for the organisation,

and also for the auditor. It will

reduce the overall chances of

risk on part of the

management.

References

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

10 | P a g e

Bae, SH 2017, 'The Association Between Corporate Tax Avoidance And Audit Efforts: Evidence From

Korea', Journal of Applied Business Research, vol 33, no. 1, pp. 153-172.

DeZoort, FT & Harrison, PD 2016, 'Understanding Auditors sense of Responsibility for detecting fraud

within organization', Journal of Business Ethics, pp. 1-18.

Fay, R & Negangard, EM 2017, 'Manual journal entry testing : Data analytics and the risk of fraud',

Journal of Accounting Education, vol 38, pp. 37-49.

Grenier, J 2017, 'Encouraging Professional Skepticism in the Industry Specialization Era', Journal of

Business Ethics, vol 142, no. 2, pp. 241-256.

Jones, P 2017, Statistical Sampling and Risk Analysis in Auditing, Routledge, NY.

Knechel, WB & Salterio, SE 2016, Auditing:Assurance and Risk, 4th edn, Routledge, New York.

Raiborn, C, Butler, JB & Martin, K 2016, 'The internal audit function: A prerequisite for Good

Governance', Journal of Corporate Accounting and Finance, vol 28, no. 2, pp. 10-21.

Sonu, CH, Ahn, H & Choi, A 2017, 'Audit fee pressure and audit risk: evidence from the financial crisis of

2008', Asia-Pacific Journal of Accounting & Economics , vol 24, no. 1-2, pp. 127-144.

10 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.