Financial Audit Report: Double Ink Printers Limited (DIPL) Analysis

VerifiedAdded on 2020/02/24

|12

|3097

|66

Report

AI Summary

This report presents an in-depth analysis of the audit conducted on Double Ink Printers Limited (DIPL). It begins by examining the analytical processes used in the audit plan, including the application of financial ratios like solvency, profit margin, and current ratio to assess DIPL's financial performance over three years. The report delves into the factors contributing to material misstatements in financial disclosures, identifying both systematic and unsystematic risks, such as employee-related issues, external environmental factors, and management integrity. It further explores risk factors associated with DIPL's financial reporting procedures, including employee involvement in fraudulent activities and the impact of new accounting software implementation. The analysis includes detailed tables of financial ratios and discusses the implications of these ratios on the company's financial health. The document concludes by examining the potential for fraudulent activities within the company and the challenges associated with management integrity.

Running head: AUDIT

Audit

Name of the Student:

Name of the University:

Author’s Note:

Audit

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................4

Answer to Question No 3...........................................................................................................7

Part A.....................................................................................................................................7

Part B....................................................................................................................................10

Reference List..........................................................................................................................11

AUDIT

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................4

Answer to Question No 3...........................................................................................................7

Part A.....................................................................................................................................7

Part B....................................................................................................................................10

Reference List..........................................................................................................................11

2

AUDIT

Answer to Question No 1

The analytical process that persists with the financial data of Double Ink Printers

Limited (DIPL) has been an influential factor for the construction of their audit plan. The

constructed plan could be regarded as a parameter that would become a key to be followed

during the preparation of the audit. These parameters have been helpful to the auditor in order

to keep track of the entire cost that would be required during the computation of the audit at

an efficient degree and this would aid in lowering the gap of understanding with the

customers. The analytical method for the financial declarations of DIPL specifies the process

of dissemination of the data (Audit & Australia 2015). These processes of assessment can be

undertaken making use of a variety of techniques. On the other hand, by taking assistance

analytical method of examining the financial declarations, various financial experts and the

accountants as well could interpret the data for attaining the decisions that would be

beneficial for the business.

The generalising of the analytical process assists in examining the financial

disclosures at a general reference point. As an outcome, the financial records can be

differentiated with reference to the numerous entities or with the time schedule. The auditors

try to think of several items that have been disclosed in the financial statement with respect to

the financial reporting technique (Sarens et al., 2013). An example can be drawn that like the

registration of the items that are inclusive of liabilities, assets and the equity stakeholders in

the reporting of the financial statements of DIPL along with investigating deviations from the

practical situation. It has been observed that benchmarking has been regarded as a process of

evaluation and this process can be used in a precise manner for the scrutiny and the

evaluation of the audit plan (Stevens 2014). The differentiation in the real financial

announcement from the benchmark aids in discovering the variances and is aids in assessing

the discovery of the factors of the recognised variances. Furthermore, the ratio analysis could

AUDIT

Answer to Question No 1

The analytical process that persists with the financial data of Double Ink Printers

Limited (DIPL) has been an influential factor for the construction of their audit plan. The

constructed plan could be regarded as a parameter that would become a key to be followed

during the preparation of the audit. These parameters have been helpful to the auditor in order

to keep track of the entire cost that would be required during the computation of the audit at

an efficient degree and this would aid in lowering the gap of understanding with the

customers. The analytical method for the financial declarations of DIPL specifies the process

of dissemination of the data (Audit & Australia 2015). These processes of assessment can be

undertaken making use of a variety of techniques. On the other hand, by taking assistance

analytical method of examining the financial declarations, various financial experts and the

accountants as well could interpret the data for attaining the decisions that would be

beneficial for the business.

The generalising of the analytical process assists in examining the financial

disclosures at a general reference point. As an outcome, the financial records can be

differentiated with reference to the numerous entities or with the time schedule. The auditors

try to think of several items that have been disclosed in the financial statement with respect to

the financial reporting technique (Sarens et al., 2013). An example can be drawn that like the

registration of the items that are inclusive of liabilities, assets and the equity stakeholders in

the reporting of the financial statements of DIPL along with investigating deviations from the

practical situation. It has been observed that benchmarking has been regarded as a process of

evaluation and this process can be used in a precise manner for the scrutiny and the

evaluation of the audit plan (Stevens 2014). The differentiation in the real financial

announcement from the benchmark aids in discovering the variances and is aids in assessing

the discovery of the factors of the recognised variances. Furthermore, the ratio analysis could

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT

be attuned as an effectual technique of evaluation that can be exploited for the explanation of

the financial declarations that is attached with the evaluation of the audit plan.

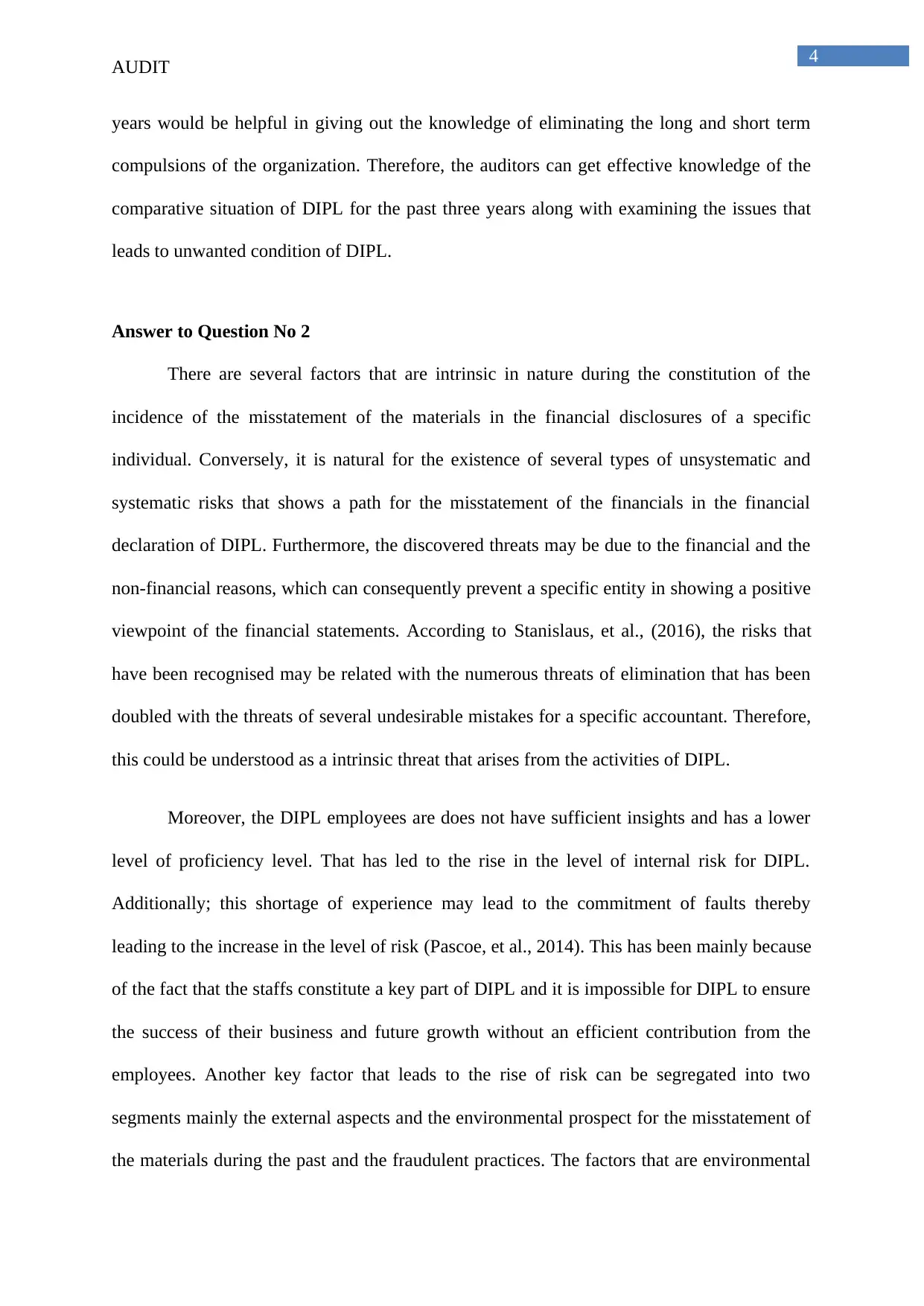

Explanation to the Case Study

The end result of the decision planning related with the planning of the audit is

persuaded mostly through the results of the analytical process in order to publicize the data

from the financial statements. The tables given below provide the financial ratios that have

been constructed with respect to the case study.

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The table that has been computed above has revealed that the current ratio of DIPL

has grown over the last three years. Furthermore, the margin profit has been noticed to be

changing for the last few years. By taking assistance of the ratios computed above, the net

profit margin of DIPL can be contrasted with the total profit that has been created (Wang et

al., 2015). Conversely, this could be of significant value to the auditor in gaining an

indication of whether the expenses are higher or are lower and if the administration of DIPL

has the requirement to decrease the budget and the total expenditure of the same. The

alterations in the ratio whether positive or adverse can be exploited as a preferential reason

for examining the authenticity and the preciseness of the financial situation of DIPL. For

instance, the solvency ratio that has been constructed in the table above assists in

understanding the positive and the adverse patterns in the entire financial condition of DIPL

(Brown et al., 2015). In a comparable manner, the comparison of the ratios for the last three

AUDIT

be attuned as an effectual technique of evaluation that can be exploited for the explanation of

the financial declarations that is attached with the evaluation of the audit plan.

Explanation to the Case Study

The end result of the decision planning related with the planning of the audit is

persuaded mostly through the results of the analytical process in order to publicize the data

from the financial statements. The tables given below provide the financial ratios that have

been constructed with respect to the case study.

Particulars 2013 2014 2015

Solvency ratio 0.62 0.44 0.21

Profit margin 0.068 0.60 0.06

Current ratio 1.42 1.46 1.50

The table that has been computed above has revealed that the current ratio of DIPL

has grown over the last three years. Furthermore, the margin profit has been noticed to be

changing for the last few years. By taking assistance of the ratios computed above, the net

profit margin of DIPL can be contrasted with the total profit that has been created (Wang et

al., 2015). Conversely, this could be of significant value to the auditor in gaining an

indication of whether the expenses are higher or are lower and if the administration of DIPL

has the requirement to decrease the budget and the total expenditure of the same. The

alterations in the ratio whether positive or adverse can be exploited as a preferential reason

for examining the authenticity and the preciseness of the financial situation of DIPL. For

instance, the solvency ratio that has been constructed in the table above assists in

understanding the positive and the adverse patterns in the entire financial condition of DIPL

(Brown et al., 2015). In a comparable manner, the comparison of the ratios for the last three

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT

years would be helpful in giving out the knowledge of eliminating the long and short term

compulsions of the organization. Therefore, the auditors can get effective knowledge of the

comparative situation of DIPL for the past three years along with examining the issues that

leads to unwanted condition of DIPL.

Answer to Question No 2

There are several factors that are intrinsic in nature during the constitution of the

incidence of the misstatement of the materials in the financial disclosures of a specific

individual. Conversely, it is natural for the existence of several types of unsystematic and

systematic risks that shows a path for the misstatement of the financials in the financial

declaration of DIPL. Furthermore, the discovered threats may be due to the financial and the

non-financial reasons, which can consequently prevent a specific entity in showing a positive

viewpoint of the financial statements. According to Stanislaus, et al., (2016), the risks that

have been recognised may be related with the numerous threats of elimination that has been

doubled with the threats of several undesirable mistakes for a specific accountant. Therefore,

this could be understood as a intrinsic threat that arises from the activities of DIPL.

Moreover, the DIPL employees are does not have sufficient insights and has a lower

level of proficiency level. That has led to the rise in the level of internal risk for DIPL.

Additionally; this shortage of experience may lead to the commitment of faults thereby

leading to the increase in the level of risk (Pascoe, et al., 2014). This has been mainly because

of the fact that the staffs constitute a key part of DIPL and it is impossible for DIPL to ensure

the success of their business and future growth without an efficient contribution from the

employees. Another key factor that leads to the rise of risk can be segregated into two

segments mainly the external aspects and the environmental prospect for the misstatement of

the materials during the past and the fraudulent practices. The factors that are environmental

AUDIT

years would be helpful in giving out the knowledge of eliminating the long and short term

compulsions of the organization. Therefore, the auditors can get effective knowledge of the

comparative situation of DIPL for the past three years along with examining the issues that

leads to unwanted condition of DIPL.

Answer to Question No 2

There are several factors that are intrinsic in nature during the constitution of the

incidence of the misstatement of the materials in the financial disclosures of a specific

individual. Conversely, it is natural for the existence of several types of unsystematic and

systematic risks that shows a path for the misstatement of the financials in the financial

declaration of DIPL. Furthermore, the discovered threats may be due to the financial and the

non-financial reasons, which can consequently prevent a specific entity in showing a positive

viewpoint of the financial statements. According to Stanislaus, et al., (2016), the risks that

have been recognised may be related with the numerous threats of elimination that has been

doubled with the threats of several undesirable mistakes for a specific accountant. Therefore,

this could be understood as a intrinsic threat that arises from the activities of DIPL.

Moreover, the DIPL employees are does not have sufficient insights and has a lower

level of proficiency level. That has led to the rise in the level of internal risk for DIPL.

Additionally; this shortage of experience may lead to the commitment of faults thereby

leading to the increase in the level of risk (Pascoe, et al., 2014). This has been mainly because

of the fact that the staffs constitute a key part of DIPL and it is impossible for DIPL to ensure

the success of their business and future growth without an efficient contribution from the

employees. Another key factor that leads to the rise of risk can be segregated into two

segments mainly the external aspects and the environmental prospect for the misstatement of

the materials during the past and the fraudulent practices. The factors that are environmental

5

AUDIT

in nature helping in discovering the internal risks comprises of the swift modifications where

the problems could be related to the valuation of the inventory, rise in the degree of

competition in the economy and the deficiency in the amount of capital (Stute et al., 2014).

Furthermore, there exists a probability of misstatement of the materials, which could be

influential for directing DIPL in the past of risk for the future years to come.

The assessment of the current case study that is related to DIPL explains the fact that

the problems and the convolutions that are associated to the progression of the CEO consists

of the internal threats as well (Christopher 2015). In this respect, the changes in the CEO can

be modified to be dissimilar as the nominees are entities. Therefore, the progress of the

procedure without any alignment to the plan, delayed instigation of the method, inefficient

initiation of the CEO and rise in the level of employee attrition may lead to such risks.

The examination of the given case study has given out the answer that the

introduction procedure if the IT mechanism has been the cause for the rise of specific

problems. There has been a scarcity of employees in DIPL for handling the method of

installation and execution while undertaking the examination and the reconciliation before

implementation of the fresh arrangement during the completion of the accounting year

(Harrison 2015). Furthermore, the primary evaluation has discovered that numerous

transactions that were undertaken were not maintained in a precise manner. Therefore, this

has led to the misstatement of the documents because of the inherent reasons, which has been

discovered to be an omission error within a specific financial declaration.

The DIPL employees are required to pursue a suitable series for the registration of the

values of the accounts receivable and the ledgers related with the accounts receivable.

Furthermore, the reconciliation of the bank is required to be maintained in an effective

manner as well (Gurran et al., 2013). Along with this, the revenue registration that is obtained

AUDIT

in nature helping in discovering the internal risks comprises of the swift modifications where

the problems could be related to the valuation of the inventory, rise in the degree of

competition in the economy and the deficiency in the amount of capital (Stute et al., 2014).

Furthermore, there exists a probability of misstatement of the materials, which could be

influential for directing DIPL in the past of risk for the future years to come.

The assessment of the current case study that is related to DIPL explains the fact that

the problems and the convolutions that are associated to the progression of the CEO consists

of the internal threats as well (Christopher 2015). In this respect, the changes in the CEO can

be modified to be dissimilar as the nominees are entities. Therefore, the progress of the

procedure without any alignment to the plan, delayed instigation of the method, inefficient

initiation of the CEO and rise in the level of employee attrition may lead to such risks.

The examination of the given case study has given out the answer that the

introduction procedure if the IT mechanism has been the cause for the rise of specific

problems. There has been a scarcity of employees in DIPL for handling the method of

installation and execution while undertaking the examination and the reconciliation before

implementation of the fresh arrangement during the completion of the accounting year

(Harrison 2015). Furthermore, the primary evaluation has discovered that numerous

transactions that were undertaken were not maintained in a precise manner. Therefore, this

has led to the misstatement of the documents because of the inherent reasons, which has been

discovered to be an omission error within a specific financial declaration.

The DIPL employees are required to pursue a suitable series for the registration of the

values of the accounts receivable and the ledgers related with the accounts receivable.

Furthermore, the reconciliation of the bank is required to be maintained in an effective

manner as well (Gurran et al., 2013). Along with this, the revenue registration that is obtained

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT

from the e-book and allowing for the textbook printing on the coming years could lead to

several intrinsic threats due to the intricacy linked with the procedure. Therefore the

inventory valuation that is in relation to the raw material at an aggregate cost is not ideal as

the aggregate cost is lower than the current paper cost (Arntz-Gray 2016). The intrinsic costs

that have been disclosed can be adjusted as the vulnerability of a distinct affirmation in

accordance to the misstatement of the materials and they have been explained below:

Rise in the pressure on the management and the employees

It has been noticed that due to the increase in the work pressure of the employees who

are working in DIPL, there has been fraudulent accounting within the company (Bunker

2015). As an outcome the numerous qualities have occurred that are inclusive of the

inclination in differentiating cash flows, improper liquidity and operational outcomes.

Misrepresentation

The increasing pressure of work on the employees of DIPL has led to the ineffective

accounting. It is due to this effect that several aspects have taken place that is inclusive of the

tendency in meeting the cash slow statements, operational outcomes and inadequate liquidity.

Overall management integrity

According to the case study, the administration of DIPL has ineffective integrity and

is predicted to be aware of fall in the brand image within the society of business (Alzeban, &

Gwilliam 2014).

AUDIT

from the e-book and allowing for the textbook printing on the coming years could lead to

several intrinsic threats due to the intricacy linked with the procedure. Therefore the

inventory valuation that is in relation to the raw material at an aggregate cost is not ideal as

the aggregate cost is lower than the current paper cost (Arntz-Gray 2016). The intrinsic costs

that have been disclosed can be adjusted as the vulnerability of a distinct affirmation in

accordance to the misstatement of the materials and they have been explained below:

Rise in the pressure on the management and the employees

It has been noticed that due to the increase in the work pressure of the employees who

are working in DIPL, there has been fraudulent accounting within the company (Bunker

2015). As an outcome the numerous qualities have occurred that are inclusive of the

inclination in differentiating cash flows, improper liquidity and operational outcomes.

Misrepresentation

The increasing pressure of work on the employees of DIPL has led to the ineffective

accounting. It is due to this effect that several aspects have taken place that is inclusive of the

tendency in meeting the cash slow statements, operational outcomes and inadequate liquidity.

Overall management integrity

According to the case study, the administration of DIPL has ineffective integrity and

is predicted to be aware of fall in the brand image within the society of business (Alzeban, &

Gwilliam 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT

Overall management integrity

In accordance with the provided case study, the DIPL administration has the

integration deficiency and it is anticipated to be prepared for any sort of reputation loss in the

organizational society.

Abnormal burden on the management

It has been observed that frequently there has been a survival of remunerations for the

administration. As an outcome, it may lead to financial reporting misstatement.

Nature of business entity

DIPL has sustained to expansion for the key competitive and economic situations.

Furthermore, these aspects may have an impact on the intrinsic threats of the business for the

evaluation of the framework of audit planning in a suitable manner.

Answer to Question No 3

Part A

The data with respect to DIPL has been obtained taking the assistance of the provided

case study and this data has been influential for the disclosure of the potentiality for the

implementation of a precise construction of the financial report procedure of DIPL. The

various significant risk factors that are linked with the utilisation of the practices have been

shown in the table below:

AUDIT

Overall management integrity

In accordance with the provided case study, the DIPL administration has the

integration deficiency and it is anticipated to be prepared for any sort of reputation loss in the

organizational society.

Abnormal burden on the management

It has been observed that frequently there has been a survival of remunerations for the

administration. As an outcome, it may lead to financial reporting misstatement.

Nature of business entity

DIPL has sustained to expansion for the key competitive and economic situations.

Furthermore, these aspects may have an impact on the intrinsic threats of the business for the

evaluation of the framework of audit planning in a suitable manner.

Answer to Question No 3

Part A

The data with respect to DIPL has been obtained taking the assistance of the provided

case study and this data has been influential for the disclosure of the potentiality for the

implementation of a precise construction of the financial report procedure of DIPL. The

various significant risk factors that are linked with the utilisation of the practices have been

shown in the table below:

8

AUDIT

Risk Type Explanation

Workforce engagement in fraudulent

activities

After the examination of the data that has

been observed from the case study of DIPL,

it can be cited that the significant counterfeits

of risk is in association to the employees of

DIPL as they have the probability to be

related to the activities. The significant

factors that is related with the threat is the

dissatisfaction among the employees of

DIPL. In accordance to the case study, there

have been an surveillance that there have

been a huge strain from the management side

so that the new accounting concept can be

introduced. It has been noticed that the

introduction of the new accounting process

creates a massive stress in the employees,

there is a rise in the level of threat as the

staffs may be related with various fake

practices (Morse & Deutsch 2016). Hence, in

order to perform as a remedy for the method

of reconciliation, the DIPL staffs improvise

several false practices and these methods

may lead to the misstatement of the financial

reports. With respect to the case study that is

under consideration. due to inefficient use of

AUDIT

Risk Type Explanation

Workforce engagement in fraudulent

activities

After the examination of the data that has

been observed from the case study of DIPL,

it can be cited that the significant counterfeits

of risk is in association to the employees of

DIPL as they have the probability to be

related to the activities. The significant

factors that is related with the threat is the

dissatisfaction among the employees of

DIPL. In accordance to the case study, there

have been an surveillance that there have

been a huge strain from the management side

so that the new accounting concept can be

introduced. It has been noticed that the

introduction of the new accounting process

creates a massive stress in the employees,

there is a rise in the level of threat as the

staffs may be related with various fake

practices (Morse & Deutsch 2016). Hence, in

order to perform as a remedy for the method

of reconciliation, the DIPL staffs improvise

several false practices and these methods

may lead to the misstatement of the financial

reports. With respect to the case study that is

under consideration. due to inefficient use of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT

the new software of accounts, the accountants

of the organization has not been able to

maintain in a precise process the primary

accounting and the financial transactions for

the current financial year. Additionally, the

fraud risks can be understood in the process

of selecting the succession of the CEO of

DIPL. It is because f this event that there has

been a rise in the internal risks of the firm.

Processes related to financial reporting There have been various risks that have been

observed with respect to the process of

financial reporting of DIPL. In this condition,

if the employees have significant financial

predictions from the performance of DIPL,

there is a rising chance of alterations in the

financial reports that has tried to influence

the stakeholders that the firm has been

undergoing efficient activities and rise in the

financial revenue (Bunker 2014). Hence it

can be stated that the fraud risk in the

construction of the financial reports id the

significant threats of DIPL.

AUDIT

the new software of accounts, the accountants

of the organization has not been able to

maintain in a precise process the primary

accounting and the financial transactions for

the current financial year. Additionally, the

fraud risks can be understood in the process

of selecting the succession of the CEO of

DIPL. It is because f this event that there has

been a rise in the internal risks of the firm.

Processes related to financial reporting There have been various risks that have been

observed with respect to the process of

financial reporting of DIPL. In this condition,

if the employees have significant financial

predictions from the performance of DIPL,

there is a rising chance of alterations in the

financial reports that has tried to influence

the stakeholders that the firm has been

undergoing efficient activities and rise in the

financial revenue (Bunker 2014). Hence it

can be stated that the fraud risk in the

construction of the financial reports id the

significant threats of DIPL.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT

Part B

According to the DIPL case study, there have been a key shortage in the raw material

valuation of DIP, that is dependent on the computation of the average cost. The main reason

has been the rise in the paper cost that is a value more than the average cost. Thus it can be

said that it is not a precise method. The fundamental threat related with the implementation of

the new system of accounting can be understood by taking help of understanding the various

performance phase inside the firm. Moreover, the examination and the scrutiny of the

financial reports of DIPL is helpful to the management to find out the fraud risks that is

linked with the construction of the financial reports. The analysis of the ratios and the other

financial techniques would be helpful for the identification of the precise results. Hence, it is

important for the DIPL management to conclude the evaluation and the investigation within a

stipulated time period.

AUDIT

Part B

According to the DIPL case study, there have been a key shortage in the raw material

valuation of DIP, that is dependent on the computation of the average cost. The main reason

has been the rise in the paper cost that is a value more than the average cost. Thus it can be

said that it is not a precise method. The fundamental threat related with the implementation of

the new system of accounting can be understood by taking help of understanding the various

performance phase inside the firm. Moreover, the examination and the scrutiny of the

financial reports of DIPL is helpful to the management to find out the fraud risks that is

linked with the construction of the financial reports. The analysis of the ratios and the other

financial techniques would be helpful for the identification of the precise results. Hence, it is

important for the DIPL management to conclude the evaluation and the investigation within a

stipulated time period.

11

AUDIT

Reference List

Alzeban, A., & Gwilliam, D. (2014). Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), 74-86.

Arntz-Gray, J. (2016). Plan, Do, Check, Act: The need for independent audit of the internal

responsibility system in occupational health and safety. Safety Science, 84, 12-23.

Audit, A. I., & Australia, I. (2015). SUBMISSION: AUSTRALIAN INFRASTRUCTURE

AUDIT.

Brown, A., Santilli, M., & Scott, B. (2015). The internal audit of clinical areas: a pilot of the

internal audit methodology in a health service emergency department. International

Journal for Quality in Health Care, mzv085.

Bunker, R. (2014). How is the compact city faring in Australia?. Planning Practice &

Research, 29(5), 449-460.

Bunker, R. (2015). Can We Plan Too Much?–The Case of the 2010 Metropolitan Strategy for

Adelaide. Australian Journal of Public Administration, 74(3), 381-389.

Christopher, J. (2015). Internal audit: Does it enhance governance in the Australian public

university sector?. Educational Management Administration & Leadership, 43(6),

954-971.

Gurran, N., Norman, B., & Hamin, E. (2013). Climate change adaptation in coastal Australia:

an audit of planning practice. Ocean & coastal management, 86, 100-109.

Harrison, M. (2015). Implementing the 2014 changes to internal audit. Governance

Directions, 67(1), 38.

AUDIT

Reference List

Alzeban, A., & Gwilliam, D. (2014). Factors affecting the internal audit effectiveness: A

survey of the Saudi public sector. Journal of International Accounting, Auditing and

Taxation, 23(2), 74-86.

Arntz-Gray, J. (2016). Plan, Do, Check, Act: The need for independent audit of the internal

responsibility system in occupational health and safety. Safety Science, 84, 12-23.

Audit, A. I., & Australia, I. (2015). SUBMISSION: AUSTRALIAN INFRASTRUCTURE

AUDIT.

Brown, A., Santilli, M., & Scott, B. (2015). The internal audit of clinical areas: a pilot of the

internal audit methodology in a health service emergency department. International

Journal for Quality in Health Care, mzv085.

Bunker, R. (2014). How is the compact city faring in Australia?. Planning Practice &

Research, 29(5), 449-460.

Bunker, R. (2015). Can We Plan Too Much?–The Case of the 2010 Metropolitan Strategy for

Adelaide. Australian Journal of Public Administration, 74(3), 381-389.

Christopher, J. (2015). Internal audit: Does it enhance governance in the Australian public

university sector?. Educational Management Administration & Leadership, 43(6),

954-971.

Gurran, N., Norman, B., & Hamin, E. (2013). Climate change adaptation in coastal Australia:

an audit of planning practice. Ocean & coastal management, 86, 100-109.

Harrison, M. (2015). Implementing the 2014 changes to internal audit. Governance

Directions, 67(1), 38.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.