University Audit Report: DIPL Financial Risk Assessment and Mitigation

VerifiedAdded on 2020/02/24

|13

|2335

|71

Report

AI Summary

This report presents an audit analysis of Double Ink Printers Limited (DIPL), focusing on risk assessment and mitigation strategies. It begins with an executive summary outlining the importance of auditing in validating financial records and identifying potential fraud. The report then details the challenges faced by auditors, including the assessment of inherent and fraud risks. The analysis covers key areas such as purchase and inventory, revenue recognition, and cash receipts, while also addressing the impact of a new CEO and IT system implementation. The report identifies specific risk factors, such as changes in asset life assumptions and the introduction of a new IT system without proper testing, and proposes mitigation strategies. Furthermore, it highlights fraud risks related to segregation of duties and improper IT system implementation, suggesting measures to mitigate these risks through improved internal controls and auditor oversight. The report also includes references to relevant academic literature.

By student name

Professor

University

Date: 27 August 2017.

Professor

University

Date: 27 August 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Executive Summary

Auditing is a procedure by which the auditors can comment on the validity of the books of record

prepared by the company. Risk assessment and identification is an important part of audit. While

conducting the audit the auditor must apply all substantive and analytical methods to the best of his

ability. This will help in identification of the fraud and the risks and mitigation of the same. Professional

skepticm is an important attribute of any auditor. In the given case below, the company has certain

inherent risks and certain fraud risk factors might be present. They evaluation and mitigation of the

same is given below.

1 | P a g e

Executive Summary

Auditing is a procedure by which the auditors can comment on the validity of the books of record

prepared by the company. Risk assessment and identification is an important part of audit. While

conducting the audit the auditor must apply all substantive and analytical methods to the best of his

ability. This will help in identification of the fraud and the risks and mitigation of the same. Professional

skepticm is an important attribute of any auditor. In the given case below, the company has certain

inherent risks and certain fraud risk factors might be present. They evaluation and mitigation of the

same is given below.

1 | P a g e

2

Contents

Bried facts of the case……………………………………………………….3

Question no 1…………………………………………………………………...4

Question no 2…………………………………………………………………...10

Question no 3…………………………………………………………….....….12

Refrences.....……………………………………………………………….......14

2 | P a g e

Contents

Bried facts of the case……………………………………………………….3

Question no 1…………………………………………………………………...4

Question no 2…………………………………………………………………...10

Question no 3…………………………………………………………….....….12

Refrences.....……………………………………………………………….......14

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Brife facts of the case

Following are some of the brief points of the case study.

1. In the given case study of DIPL, the auditors of the company are faced with many challenges of

identification of major risk factors. Besides this, they are taking over from the old auditor ‘Jay

and Asssociates’, therefore the new auditors will also need to check the opening balances.

2. In case of the given company, there are many changes occurring, the new CEO is taking many

decisions that might affect the overall profitability of the company.

3. The work of the auditor is to identify the inherent risk factor in the company and help the

management in mitigation of the same. The major details about the performance of the

company, along with brife background information are given.

4. Along with it , there are details about the major functioning department of the company that

consists of Purchase and Inventory, ‘Print on Demand’ revenue and receivables, ‘E-book’

Revenue, cash receipts etc.

5. All the details regarding the management of these departments are given and the work of the

auditor is verifying the records properly and comment on the same.

3 | P a g e

Brife facts of the case

Following are some of the brief points of the case study.

1. In the given case study of DIPL, the auditors of the company are faced with many challenges of

identification of major risk factors. Besides this, they are taking over from the old auditor ‘Jay

and Asssociates’, therefore the new auditors will also need to check the opening balances.

2. In case of the given company, there are many changes occurring, the new CEO is taking many

decisions that might affect the overall profitability of the company.

3. The work of the auditor is to identify the inherent risk factor in the company and help the

management in mitigation of the same. The major details about the performance of the

company, along with brife background information are given.

4. Along with it , there are details about the major functioning department of the company that

consists of Purchase and Inventory, ‘Print on Demand’ revenue and receivables, ‘E-book’

Revenue, cash receipts etc.

5. All the details regarding the management of these departments are given and the work of the

auditor is verifying the records properly and comment on the same.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Question no 1

Audit of the financial statements has become one of the indispensable activity as this is the one

which gives reasonable assurance to the users of the financial statements that it has been prepared on

unbiased basis and is giving a true picture of the management and its accounts. While conducting or

starting the audit, auditor needs to know the business and its environment, the control procedures

being established within the organization, the industry in which it deals and several other in and outs

regarding the company. For the audit to be effective, the auditor needs to know and validate the

estimates and judgements being taken into consideration by the management as it has a huge bearing

on the results of the organization.Audit is conducted with the view to identify the material

misstatements, if any in the accounts prepared by identifying the risk areas. In the course of the audit,

the auditor also needs to check the materiality, the consistency and the going concern assumption of

the entity. He may use various procedures in path to checking of the books which includes substantive

and analytical audit procedures. Substantive audit procedures generally include vouching of the incomes

and expenses recorded in the profit and loss account using tools like inspection of the journal, ledgers,

invoices, bills, contracts, etc and observations of the activities like physical verification going on in the

organization. This also includes inquiry in the account balances and taking external confirmation from

the parties like banks, financial institutions and creditors. The main focus here is to ensure that proper

disclosures are made for related party disclosures, if any. Besides this, auditor also does recalculation

and reperformance of some of the activities like valuation of the inventory, actuarial valuation in acse of

employee benefits to ensure whether proper valuation techniques have been applied and the results

don’t vary much. One common example of substantive procedure is the preparation of the bank

reconciliation statement at the ned of every period to ensure that the bank and the cash books of the

company are reconciling(Bae 2017).

In case the auditor is not able to make out the opinion on the financial statements post the

application of substantive procedures he would apply analysitical procedures which includes comparison

of the actual results of business from the expected or budgeted results, analysis of key financial ratios,

trend analysis, comparison with industry data and other non financial data points. The auditor also

needs to check on the SOX compliance being maintained in the entity, the governance, etc. and based

on all this he determoined the threshold limit for audit materiality. The results of all these procedures

and the level of internal control being practiced in the organization (strong or weak), the auditors

prepares the audit plan and determines the nature of sampling to be doen, the amount of time to be

4 | P a g e

Question no 1

Audit of the financial statements has become one of the indispensable activity as this is the one

which gives reasonable assurance to the users of the financial statements that it has been prepared on

unbiased basis and is giving a true picture of the management and its accounts. While conducting or

starting the audit, auditor needs to know the business and its environment, the control procedures

being established within the organization, the industry in which it deals and several other in and outs

regarding the company. For the audit to be effective, the auditor needs to know and validate the

estimates and judgements being taken into consideration by the management as it has a huge bearing

on the results of the organization.Audit is conducted with the view to identify the material

misstatements, if any in the accounts prepared by identifying the risk areas. In the course of the audit,

the auditor also needs to check the materiality, the consistency and the going concern assumption of

the entity. He may use various procedures in path to checking of the books which includes substantive

and analytical audit procedures. Substantive audit procedures generally include vouching of the incomes

and expenses recorded in the profit and loss account using tools like inspection of the journal, ledgers,

invoices, bills, contracts, etc and observations of the activities like physical verification going on in the

organization. This also includes inquiry in the account balances and taking external confirmation from

the parties like banks, financial institutions and creditors. The main focus here is to ensure that proper

disclosures are made for related party disclosures, if any. Besides this, auditor also does recalculation

and reperformance of some of the activities like valuation of the inventory, actuarial valuation in acse of

employee benefits to ensure whether proper valuation techniques have been applied and the results

don’t vary much. One common example of substantive procedure is the preparation of the bank

reconciliation statement at the ned of every period to ensure that the bank and the cash books of the

company are reconciling(Bae 2017).

In case the auditor is not able to make out the opinion on the financial statements post the

application of substantive procedures he would apply analysitical procedures which includes comparison

of the actual results of business from the expected or budgeted results, analysis of key financial ratios,

trend analysis, comparison with industry data and other non financial data points. The auditor also

needs to check on the SOX compliance being maintained in the entity, the governance, etc. and based

on all this he determoined the threshold limit for audit materiality. The results of all these procedures

and the level of internal control being practiced in the organization (strong or weak), the auditors

prepares the audit plan and determines the nature of sampling to be doen, the amount of time to be

4 | P a g e

5

given in checking of the critical areas and the extent to which a particular thing can be checked(DeZoort

& Harrison 2016).

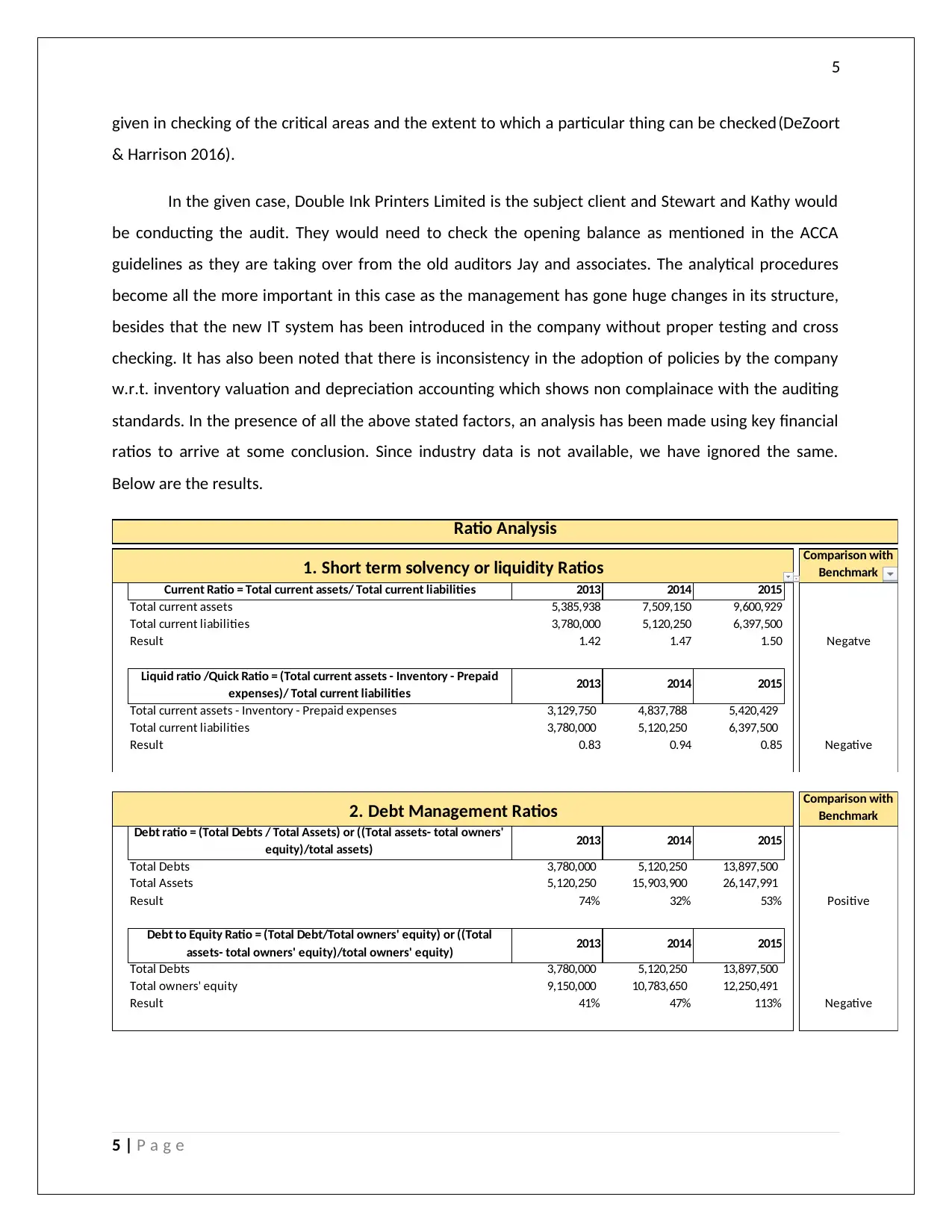

In the given case, Double Ink Printers Limited is the subject client and Stewart and Kathy would

be conducting the audit. They would need to check the opening balance as mentioned in the ACCA

guidelines as they are taking over from the old auditors Jay and associates. The analytical procedures

become all the more important in this case as the management has gone huge changes in its structure,

besides that the new IT system has been introduced in the company without proper testing and cross

checking. It has also been noted that there is inconsistency in the adoption of policies by the company

w.r.t. inventory valuation and depreciation accounting which shows non complainace with the auditing

standards. In the presence of all the above stated factors, an analysis has been made using key financial

ratios to arrive at some conclusion. Since industry data is not available, we have ignored the same.

Below are the results.

Comparison with

Benchmark

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50 Negatve

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85 Negative

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

1. Short term solvency or liquidity Ratios

Ratio Analysis

Comparison with

Benchmark

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53% Positive

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113% Negative

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

2. Debt Management Ratios

5 | P a g e

given in checking of the critical areas and the extent to which a particular thing can be checked(DeZoort

& Harrison 2016).

In the given case, Double Ink Printers Limited is the subject client and Stewart and Kathy would

be conducting the audit. They would need to check the opening balance as mentioned in the ACCA

guidelines as they are taking over from the old auditors Jay and associates. The analytical procedures

become all the more important in this case as the management has gone huge changes in its structure,

besides that the new IT system has been introduced in the company without proper testing and cross

checking. It has also been noted that there is inconsistency in the adoption of policies by the company

w.r.t. inventory valuation and depreciation accounting which shows non complainace with the auditing

standards. In the presence of all the above stated factors, an analysis has been made using key financial

ratios to arrive at some conclusion. Since industry data is not available, we have ignored the same.

Below are the results.

Comparison with

Benchmark

2013 2014 2015

Total current assets 5,385,938 7,509,150 9,600,929

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 1.42 1.47 1.50 Negatve

2013 2014 2015

Total current assets - Inventory - Prepaid expenses 3,129,750 4,837,788 5,420,429

Total current liabilities 3,780,000 5,120,250 6,397,500

Result 0.83 0.94 0.85 Negative

Current Ratio = Total current assets/ Total current liabilities

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities

1. Short term solvency or liquidity Ratios

Ratio Analysis

Comparison with

Benchmark

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total Assets 5,120,250 15,903,900 26,147,991

Result 74% 32% 53% Positive

2013 2014 2015

Total Debts 3,780,000 5,120,250 13,897,500

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 41% 47% 113% Negative

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total owners'

equity)/total assets)

Debt to Equity Ratio = (Total Debt/Total owners' equity) or ((Total

assets- total owners' equity)/total owners' equity)

2. Debt Management Ratios

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

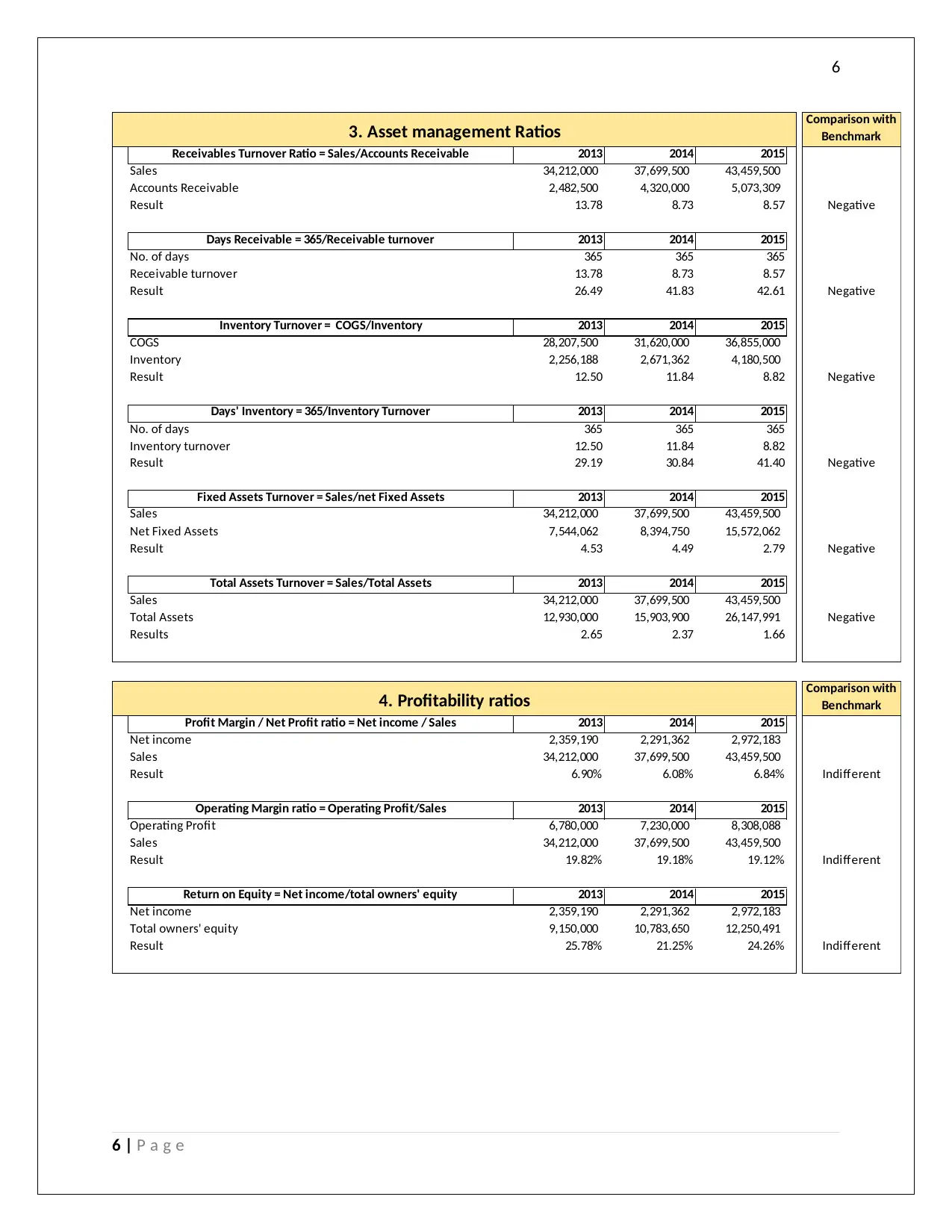

Comparison with

Benchmark

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57 Negative

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61 Negative

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82 Negative

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991 Negative

Results 2.65 2.37 1.66

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

3. Asset management Ratios

Comparison with

Benchmark

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84% Indifferent

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12% Indifferent

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26% Indifferent

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

4. Profitability ratios

6 | P a g e

Comparison with

Benchmark

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Accounts Receivable 2,482,500 4,320,000 5,073,309

Result 13.78 8.73 8.57 Negative

2013 2014 2015

No. of days 365 365 365

Receivable turnover 13.78 8.73 8.57

Result 26.49 41.83 42.61 Negative

2013 2014 2015

COGS 28,207,500 31,620,000 36,855,000

Inventory 2,256,188 2,671,362 4,180,500

Result 12.50 11.84 8.82 Negative

2013 2014 2015

No. of days 365 365 365

Inventory turnover 12.50 11.84 8.82

Result 29.19 30.84 41.40 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Net Fixed Assets 7,544,062 8,394,750 15,572,062

Result 4.53 4.49 2.79 Negative

2013 2014 2015

Sales 34,212,000 37,699,500 43,459,500

Total Assets 12,930,000 15,903,900 26,147,991 Negative

Results 2.65 2.37 1.66

Inventory Turnover = COGS/Inventory

Days' Inventory = 365/Inventory Turnover

Fixed Assets Turnover = Sales/net Fixed Assets

Total Assets Turnover = Sales/Total Assets

Receivables Turnover Ratio = Sales/Accounts Receivable

Days Receivable = 365/Receivable turnover

3. Asset management Ratios

Comparison with

Benchmark

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Sales 34,212,000 37,699,500 43,459,500

Result 6.90% 6.08% 6.84% Indifferent

2013 2014 2015

Operating Profit 6,780,000 7,230,000 8,308,088

Sales 34,212,000 37,699,500 43,459,500

Result 19.82% 19.18% 19.12% Indifferent

2013 2014 2015

Net income 2,359,190 2,291,362 2,972,183

Total owners' equity 9,150,000 10,783,650 12,250,491

Result 25.78% 21.25% 24.26% Indifferent

Profit Margin / Net Profit ratio = Net income / Sales

Operating Margin ratio = Operating Profit/Sales

Return on Equity = Net income/total owners' equity

4. Profitability ratios

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

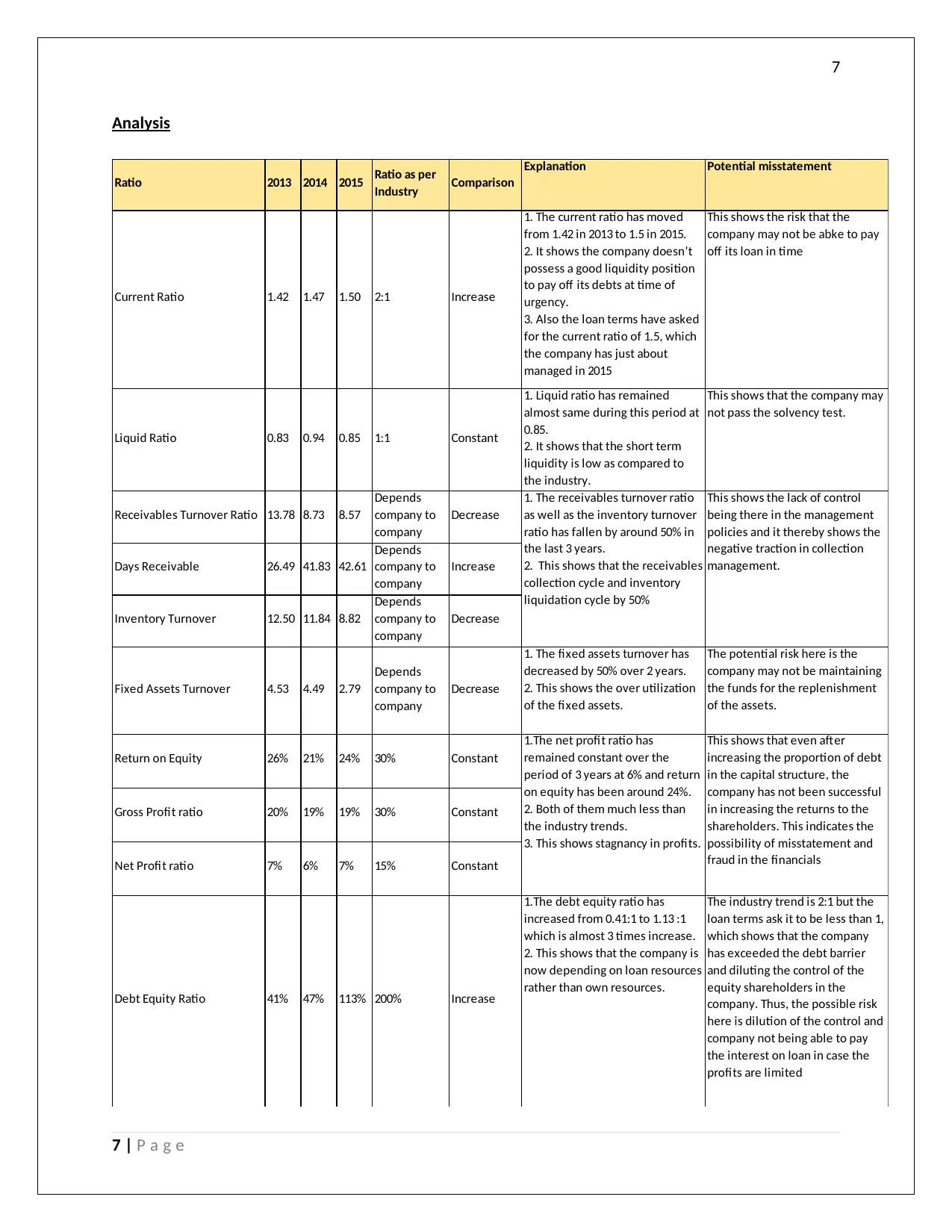

Analysis

Ratio 2013 2014 2015 Ratio as per

Industry Comparison

Explanation Potential misstatement

Current Ratio 1.42 1.47 1.50 2:1 Increase

1. The current ratio has moved

from 1.42 in 2013 to 1.5 in 2015.

2. It shows the company doesn’t

possess a good liquidity position

to pay off its debts at time of

urgency.

3. Also the loan terms have asked

for the current ratio of 1.5, which

the company has just about

managed in 2015

This shows the risk that the

company may not be abke to pay

off its loan in time

Liquid Ratio 0.83 0.94 0.85 1:1 Constant

1. Liquid ratio has remained

almost same during this period at

0.85.

2. It shows that the short term

liquidity is low as compared to

the industry.

This shows that the company may

not pass the solvency test.

Receivables Turnover Ratio 13.78 8.73 8.57

Depends

company to

company

Decrease

Days Receivable 26.49 41.83 42.61

Depends

company to

company

Increase

Inventory Turnover 12.50 11.84 8.82

Depends

company to

company

Decrease

Fixed Assets Turnover 4.53 4.49 2.79

Depends

company to

company

Decrease

1. The fixed assets turnover has

decreased by 50% over 2 years.

2. This shows the over utilization

of the fixed assets.

The potential risk here is the

company may not be maintaining

the funds for the replenishment

of the assets.

Return on Equity 26% 21% 24% 30% Constant

Gross Profit ratio 20% 19% 19% 30% Constant

Net Profit ratio 7% 6% 7% 15% Constant

Debt Equity Ratio 41% 47% 113% 200% Increase

1.The debt equity ratio has

increased from 0.41:1 to 1.13 :1

which is almost 3 times increase.

2. This shows that the company is

now depending on loan resources

rather than own resources.

The industry trend is 2:1 but the

loan terms ask it to be less than 1,

which shows that the company

has exceeded the debt barrier

and diluting the control of the

equity shareholders in the

company. Thus, the possible risk

here is dilution of the control and

company not being able to pay

the interest on loan in case the

profits are limited

1. The receivables turnover ratio

as well as the inventory turnover

ratio has fallen by around 50% in

the last 3 years.

2. This shows that the receivables

collection cycle and inventory

liquidation cycle by 50%

This shows the lack of control

being there in the management

policies and it thereby shows the

negative traction in collection

management.

1.The net profit ratio has

remained constant over the

period of 3 years at 6% and return

on equity has been around 24%.

2. Both of them much less than

the industry trends.

3. This shows stagnancy in profits.

This shows that even after

increasing the proportion of debt

in the capital structure, the

company has not been successful

in increasing the returns to the

shareholders. This indicates the

possibility of misstatement and

fraud in the financials

7 | P a g e

Analysis

Ratio 2013 2014 2015 Ratio as per

Industry Comparison

Explanation Potential misstatement

Current Ratio 1.42 1.47 1.50 2:1 Increase

1. The current ratio has moved

from 1.42 in 2013 to 1.5 in 2015.

2. It shows the company doesn’t

possess a good liquidity position

to pay off its debts at time of

urgency.

3. Also the loan terms have asked

for the current ratio of 1.5, which

the company has just about

managed in 2015

This shows the risk that the

company may not be abke to pay

off its loan in time

Liquid Ratio 0.83 0.94 0.85 1:1 Constant

1. Liquid ratio has remained

almost same during this period at

0.85.

2. It shows that the short term

liquidity is low as compared to

the industry.

This shows that the company may

not pass the solvency test.

Receivables Turnover Ratio 13.78 8.73 8.57

Depends

company to

company

Decrease

Days Receivable 26.49 41.83 42.61

Depends

company to

company

Increase

Inventory Turnover 12.50 11.84 8.82

Depends

company to

company

Decrease

Fixed Assets Turnover 4.53 4.49 2.79

Depends

company to

company

Decrease

1. The fixed assets turnover has

decreased by 50% over 2 years.

2. This shows the over utilization

of the fixed assets.

The potential risk here is the

company may not be maintaining

the funds for the replenishment

of the assets.

Return on Equity 26% 21% 24% 30% Constant

Gross Profit ratio 20% 19% 19% 30% Constant

Net Profit ratio 7% 6% 7% 15% Constant

Debt Equity Ratio 41% 47% 113% 200% Increase

1.The debt equity ratio has

increased from 0.41:1 to 1.13 :1

which is almost 3 times increase.

2. This shows that the company is

now depending on loan resources

rather than own resources.

The industry trend is 2:1 but the

loan terms ask it to be less than 1,

which shows that the company

has exceeded the debt barrier

and diluting the control of the

equity shareholders in the

company. Thus, the possible risk

here is dilution of the control and

company not being able to pay

the interest on loan in case the

profits are limited

1. The receivables turnover ratio

as well as the inventory turnover

ratio has fallen by around 50% in

the last 3 years.

2. This shows that the receivables

collection cycle and inventory

liquidation cycle by 50%

This shows the lack of control

being there in the management

policies and it thereby shows the

negative traction in collection

management.

1.The net profit ratio has

remained constant over the

period of 3 years at 6% and return

on equity has been around 24%.

2. Both of them much less than

the industry trends.

3. This shows stagnancy in profits.

This shows that even after

increasing the proportion of debt

in the capital structure, the

company has not been successful

in increasing the returns to the

shareholders. This indicates the

possibility of misstatement and

fraud in the financials

7 | P a g e

8

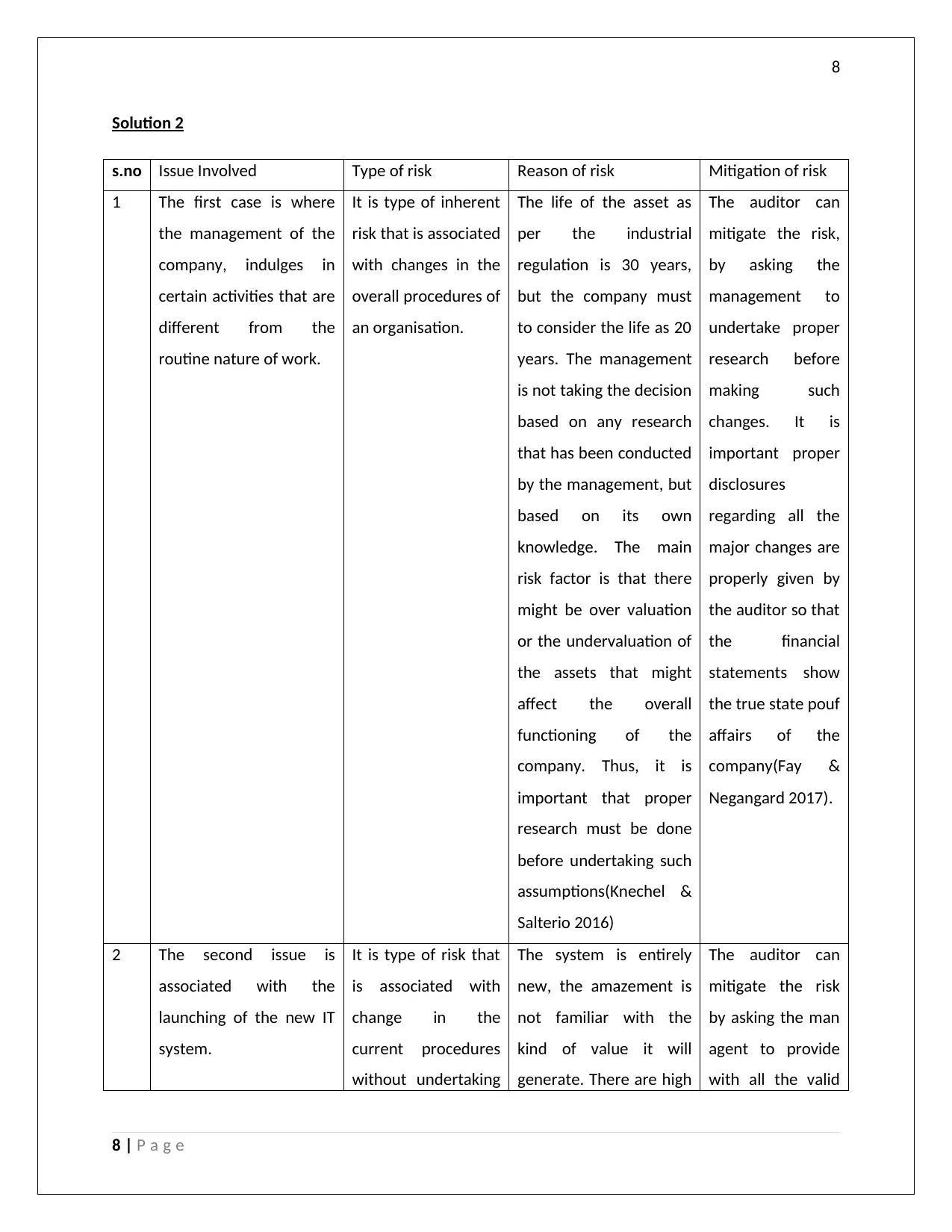

Solution 2

s.no Issue Involved Type of risk Reason of risk Mitigation of risk

1 The first case is where

the management of the

company, indulges in

certain activities that are

different from the

routine nature of work.

It is type of inherent

risk that is associated

with changes in the

overall procedures of

an organisation.

The life of the asset as

per the industrial

regulation is 30 years,

but the company must

to consider the life as 20

years. The management

is not taking the decision

based on any research

that has been conducted

by the management, but

based on its own

knowledge. The main

risk factor is that there

might be over valuation

or the undervaluation of

the assets that might

affect the overall

functioning of the

company. Thus, it is

important that proper

research must be done

before undertaking such

assumptions(Knechel &

Salterio 2016)

The auditor can

mitigate the risk,

by asking the

management to

undertake proper

research before

making such

changes. It is

important proper

disclosures

regarding all the

major changes are

properly given by

the auditor so that

the financial

statements show

the true state pouf

affairs of the

company(Fay &

Negangard 2017).

2 The second issue is

associated with the

launching of the new IT

system.

It is type of risk that

is associated with

change in the

current procedures

without undertaking

The system is entirely

new, the amazement is

not familiar with the

kind of value it will

generate. There are high

The auditor can

mitigate the risk

by asking the man

agent to provide

with all the valid

8 | P a g e

Solution 2

s.no Issue Involved Type of risk Reason of risk Mitigation of risk

1 The first case is where

the management of the

company, indulges in

certain activities that are

different from the

routine nature of work.

It is type of inherent

risk that is associated

with changes in the

overall procedures of

an organisation.

The life of the asset as

per the industrial

regulation is 30 years,

but the company must

to consider the life as 20

years. The management

is not taking the decision

based on any research

that has been conducted

by the management, but

based on its own

knowledge. The main

risk factor is that there

might be over valuation

or the undervaluation of

the assets that might

affect the overall

functioning of the

company. Thus, it is

important that proper

research must be done

before undertaking such

assumptions(Knechel &

Salterio 2016)

The auditor can

mitigate the risk,

by asking the

management to

undertake proper

research before

making such

changes. It is

important proper

disclosures

regarding all the

major changes are

properly given by

the auditor so that

the financial

statements show

the true state pouf

affairs of the

company(Fay &

Negangard 2017).

2 The second issue is

associated with the

launching of the new IT

system.

It is type of risk that

is associated with

change in the

current procedures

without undertaking

The system is entirely

new, the amazement is

not familiar with the

kind of value it will

generate. There are high

The auditor can

mitigate the risk

by asking the man

agent to provide

with all the valid

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

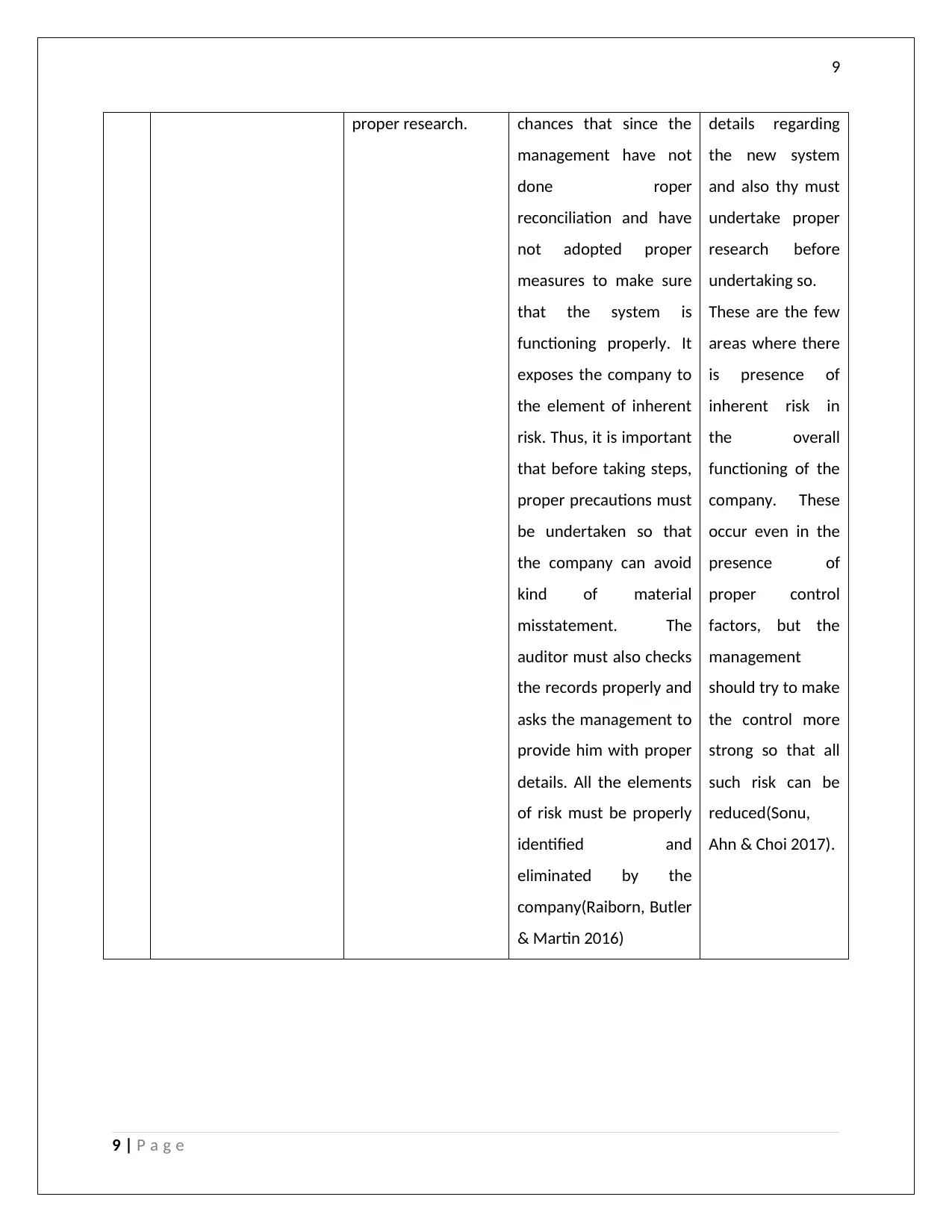

proper research. chances that since the

management have not

done roper

reconciliation and have

not adopted proper

measures to make sure

that the system is

functioning properly. It

exposes the company to

the element of inherent

risk. Thus, it is important

that before taking steps,

proper precautions must

be undertaken so that

the company can avoid

kind of material

misstatement. The

auditor must also checks

the records properly and

asks the management to

provide him with proper

details. All the elements

of risk must be properly

identified and

eliminated by the

company(Raiborn, Butler

& Martin 2016)

details regarding

the new system

and also thy must

undertake proper

research before

undertaking so.

These are the few

areas where there

is presence of

inherent risk in

the overall

functioning of the

company. These

occur even in the

presence of

proper control

factors, but the

management

should try to make

the control more

strong so that all

such risk can be

reduced(Sonu,

Ahn & Choi 2017).

9 | P a g e

proper research. chances that since the

management have not

done roper

reconciliation and have

not adopted proper

measures to make sure

that the system is

functioning properly. It

exposes the company to

the element of inherent

risk. Thus, it is important

that before taking steps,

proper precautions must

be undertaken so that

the company can avoid

kind of material

misstatement. The

auditor must also checks

the records properly and

asks the management to

provide him with proper

details. All the elements

of risk must be properly

identified and

eliminated by the

company(Raiborn, Butler

& Martin 2016)

details regarding

the new system

and also thy must

undertake proper

research before

undertaking so.

These are the few

areas where there

is presence of

inherent risk in

the overall

functioning of the

company. These

occur even in the

presence of

proper control

factors, but the

management

should try to make

the control more

strong so that all

such risk can be

reduced(Sonu,

Ahn & Choi 2017).

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

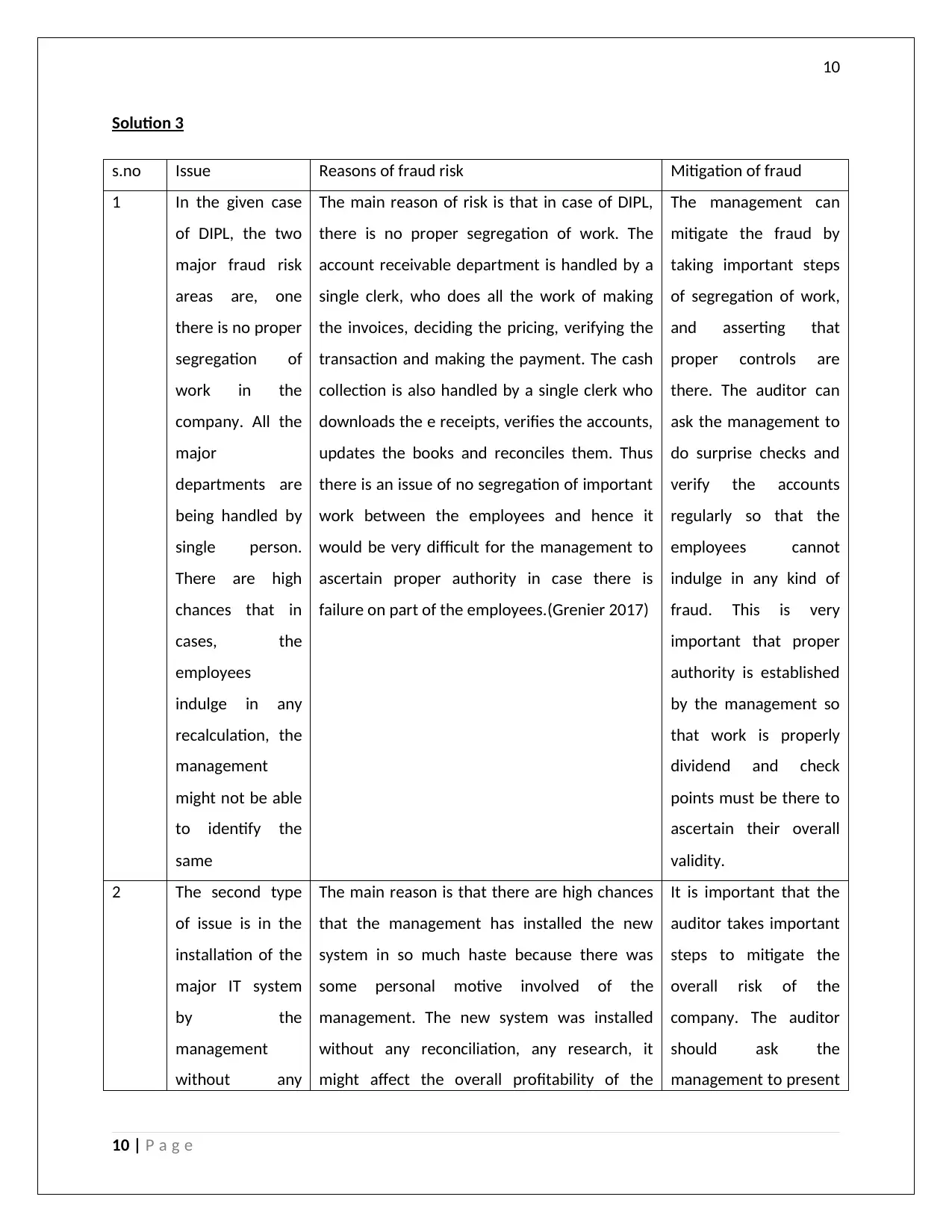

Solution 3

s.no Issue Reasons of fraud risk Mitigation of fraud

1 In the given case

of DIPL, the two

major fraud risk

areas are, one

there is no proper

segregation of

work in the

company. All the

major

departments are

being handled by

single person.

There are high

chances that in

cases, the

employees

indulge in any

recalculation, the

management

might not be able

to identify the

same

The main reason of risk is that in case of DIPL,

there is no proper segregation of work. The

account receivable department is handled by a

single clerk, who does all the work of making

the invoices, deciding the pricing, verifying the

transaction and making the payment. The cash

collection is also handled by a single clerk who

downloads the e receipts, verifies the accounts,

updates the books and reconciles them. Thus

there is an issue of no segregation of important

work between the employees and hence it

would be very difficult for the management to

ascertain proper authority in case there is

failure on part of the employees.(Grenier 2017)

The management can

mitigate the fraud by

taking important steps

of segregation of work,

and asserting that

proper controls are

there. The auditor can

ask the management to

do surprise checks and

verify the accounts

regularly so that the

employees cannot

indulge in any kind of

fraud. This is very

important that proper

authority is established

by the management so

that work is properly

dividend and check

points must be there to

ascertain their overall

validity.

2 The second type

of issue is in the

installation of the

major IT system

by the

management

without any

The main reason is that there are high chances

that the management has installed the new

system in so much haste because there was

some personal motive involved of the

management. The new system was installed

without any reconciliation, any research, it

might affect the overall profitability of the

It is important that the

auditor takes important

steps to mitigate the

overall risk of the

company. The auditor

should ask the

management to present

10 | P a g e

Solution 3

s.no Issue Reasons of fraud risk Mitigation of fraud

1 In the given case

of DIPL, the two

major fraud risk

areas are, one

there is no proper

segregation of

work in the

company. All the

major

departments are

being handled by

single person.

There are high

chances that in

cases, the

employees

indulge in any

recalculation, the

management

might not be able

to identify the

same

The main reason of risk is that in case of DIPL,

there is no proper segregation of work. The

account receivable department is handled by a

single clerk, who does all the work of making

the invoices, deciding the pricing, verifying the

transaction and making the payment. The cash

collection is also handled by a single clerk who

downloads the e receipts, verifies the accounts,

updates the books and reconciles them. Thus

there is an issue of no segregation of important

work between the employees and hence it

would be very difficult for the management to

ascertain proper authority in case there is

failure on part of the employees.(Grenier 2017)

The management can

mitigate the fraud by

taking important steps

of segregation of work,

and asserting that

proper controls are

there. The auditor can

ask the management to

do surprise checks and

verify the accounts

regularly so that the

employees cannot

indulge in any kind of

fraud. This is very

important that proper

authority is established

by the management so

that work is properly

dividend and check

points must be there to

ascertain their overall

validity.

2 The second type

of issue is in the

installation of the

major IT system

by the

management

without any

The main reason is that there are high chances

that the management has installed the new

system in so much haste because there was

some personal motive involved of the

management. The new system was installed

without any reconciliation, any research, it

might affect the overall profitability of the

It is important that the

auditor takes important

steps to mitigate the

overall risk of the

company. The auditor

should ask the

management to present

10 | P a g e

11

proper research. company hampering its growth and

development. There might be undervaluation

or overvaluation of the new system which

might have risk of material misstatement on the

books of the company (Jones 2017).

them with important

documents regarding

the company, to make

take expert opinion

before installing the

new system. It should

also reconcile the

overall cost and profit

to see the profitability

of the system and

should also check its

effect on the financials

of the company. The

management should

provide the auditor

with all the support and

documents. In case the

auditor finds any

discrepancies, he can

modify the audit report

and give a disclaimer

opinion. These are the

few ways in which the

auditor can mitigate the

overall risk of fraud that

is associated with the

company.

11 | P a g e

proper research. company hampering its growth and

development. There might be undervaluation

or overvaluation of the new system which

might have risk of material misstatement on the

books of the company (Jones 2017).

them with important

documents regarding

the company, to make

take expert opinion

before installing the

new system. It should

also reconcile the

overall cost and profit

to see the profitability

of the system and

should also check its

effect on the financials

of the company. The

management should

provide the auditor

with all the support and

documents. In case the

auditor finds any

discrepancies, he can

modify the audit report

and give a disclaimer

opinion. These are the

few ways in which the

auditor can mitigate the

overall risk of fraud that

is associated with the

company.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.