Audit & Assurance Report: Financial Statement Analysis of DIPL Ltd

VerifiedAdded on 2020/03/04

|8

|2168

|34

Report

AI Summary

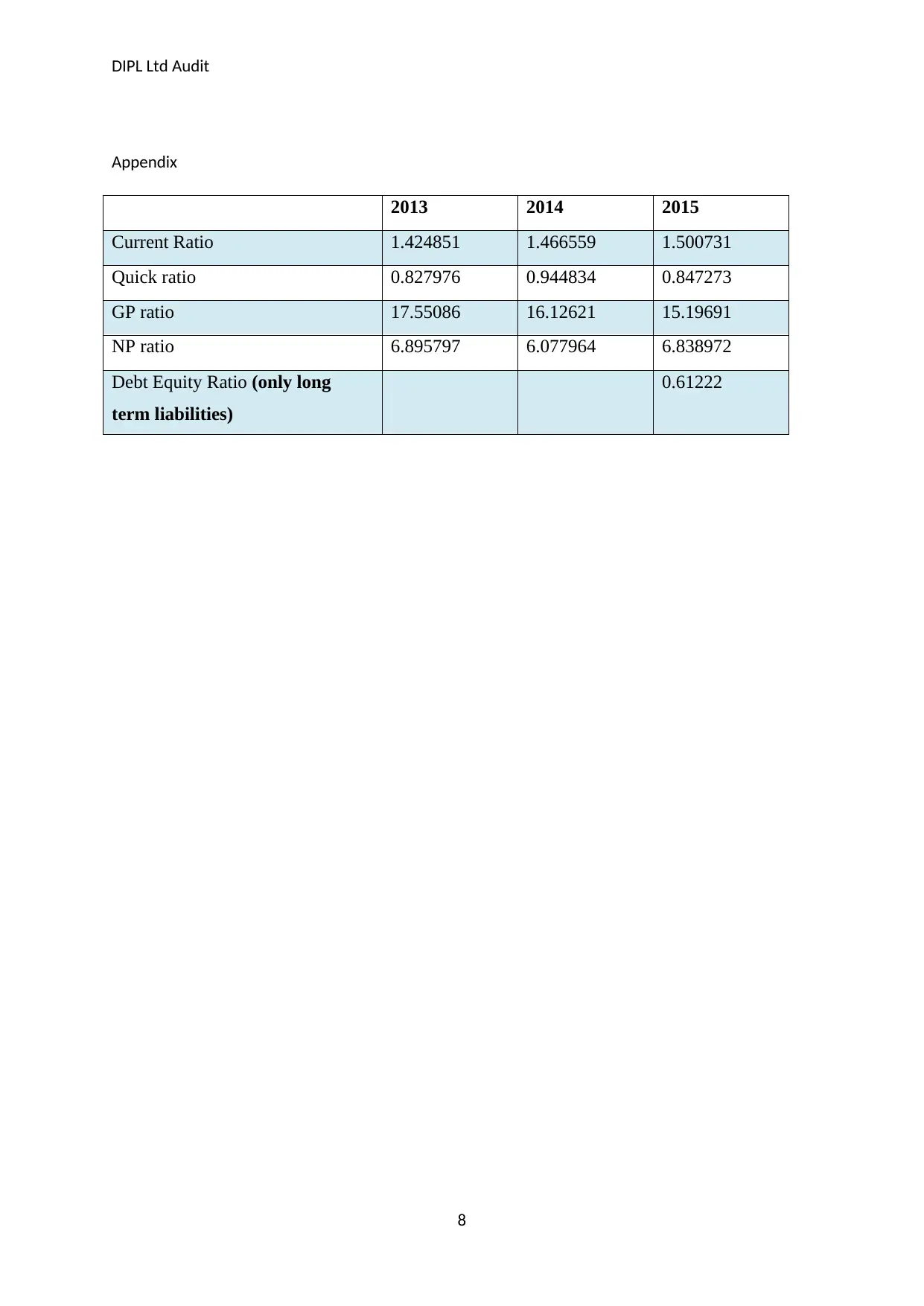

This report presents an audit and assurance analysis of DIPL Ltd, evaluating its financial performance from 2013 to 2015. It examines financial ratios like current, quick, gross profit, and net profit ratios, highlighting trends in liquidity, profitability, and solvency. The report identifies inherent risks, such as incorrect accounts receivable treatment and issues with a new IT system, and discusses two fraud risk factors: revenue recognition and IT technology variations. The auditor's reliance on management-provided materials and the impact of weak internal controls are also addressed. The analysis emphasizes the need for effective procedures to mitigate risks and ensure accurate financial reporting. The analysis also includes the use of analytical and substantive procedures. The report concludes with a call for improved cost control, better management of accounts receivable, and a review of inventory valuation procedures.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.