Audit Planning and Risk Assessment for GPSA: Financial Analysis Report

VerifiedAdded on 2020/04/01

|15

|3037

|406

Case Study

AI Summary

This case study presents an audit planning report for MYH, focusing on the financial analysis of GPSA. The report analyzes key financial areas including accounts receivables, current investments, property assets, intangible assets, and research and development capitalization. It identifies audit and business risks through ratio analysis, such as return on equity, times interest earned, current ratio, and debt to equity ratio. The report also assesses potential internal controls and weaknesses, particularly in sales and trade receivables, to mitigate identified risks. The analysis covers the years 2015, 2016 (audited), and 2017 (unaudited), providing a comprehensive overview of the company's financial health and the auditor's approach to risk management and internal control improvements. The report aims to support the audit partner in formulating the audit plan for the year ending June 30, 2017, and is intended for submission to the Board by the end of August 2017.

Audit Planning and Internal Control- A

Case STUDY

1

Case STUDY

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This management report is made for the audit partner of MYH John Richards to highlight

different domains of financial information to make the next audit plan for year ended on 30th

June, 2017. The client of MYH is GPSA who are engaged in different activities in the fields of

research and development of technologies related to medical equipments, production and

distribution of medical equipments, investment of surplus fund and investment in the property

market. Main concern for the audit planning is to find out the areas related to audit risks,

business risks and the implementation of tighter internal control. For this purpose my partner,

John Richards had asked for a management report on different areas of financial information like

accounts receivables, current investments property assets, intangible assets and capitalization of

research and development process. The financial controller has implemented some new IT

application for the company earlier which has taken shape with the staffs and now it runs

smoothly. Main objective of this report is to analyze different financial ratios as retrieved from

the financial report of the company for the last three years. The financial reports to be considered

has the credential of audited status for last two years- 2015 and 2016, while for 2017 the

financial ratios are of unaudited status. By analyzing those financial ratios, the present financial

condition of the company will be projected on the core areas of derivation of audit risks, business

risks and enhanced level of internal control to make the financial activities of the company more

professional and full proof.

2

This management report is made for the audit partner of MYH John Richards to highlight

different domains of financial information to make the next audit plan for year ended on 30th

June, 2017. The client of MYH is GPSA who are engaged in different activities in the fields of

research and development of technologies related to medical equipments, production and

distribution of medical equipments, investment of surplus fund and investment in the property

market. Main concern for the audit planning is to find out the areas related to audit risks,

business risks and the implementation of tighter internal control. For this purpose my partner,

John Richards had asked for a management report on different areas of financial information like

accounts receivables, current investments property assets, intangible assets and capitalization of

research and development process. The financial controller has implemented some new IT

application for the company earlier which has taken shape with the staffs and now it runs

smoothly. Main objective of this report is to analyze different financial ratios as retrieved from

the financial report of the company for the last three years. The financial reports to be considered

has the credential of audited status for last two years- 2015 and 2016, while for 2017 the

financial ratios are of unaudited status. By analyzing those financial ratios, the present financial

condition of the company will be projected on the core areas of derivation of audit risks, business

risks and enhanced level of internal control to make the financial activities of the company more

professional and full proof.

2

Table of Contents

Introduction.................................................................................................................................................4

Audit Risk.....................................................................................................................................................4

Accounts Receivables..............................................................................................................................4

Current investments................................................................................................................................5

Property assets........................................................................................................................................6

Intangible assets......................................................................................................................................7

Research and development capitalization...............................................................................................8

Business risk................................................................................................................................................8

Return on equity (ROE)............................................................................................................................9

Times interest earned..............................................................................................................................9

Current ratio............................................................................................................................................9

Debt to equity ratio...............................................................................................................................10

Potential Internal Controls........................................................................................................................10

Weaknesses in Internal Control for Sales and Trade Receivables..............................................................12

Conclusion.................................................................................................................................................12

References:................................................................................................................................................14

3

Introduction.................................................................................................................................................4

Audit Risk.....................................................................................................................................................4

Accounts Receivables..............................................................................................................................4

Current investments................................................................................................................................5

Property assets........................................................................................................................................6

Intangible assets......................................................................................................................................7

Research and development capitalization...............................................................................................8

Business risk................................................................................................................................................8

Return on equity (ROE)............................................................................................................................9

Times interest earned..............................................................................................................................9

Current ratio............................................................................................................................................9

Debt to equity ratio...............................................................................................................................10

Potential Internal Controls........................................................................................................................10

Weaknesses in Internal Control for Sales and Trade Receivables..............................................................12

Conclusion.................................................................................................................................................12

References:................................................................................................................................................14

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

GPSA is engaged in different level of business with good profit. This report is meant for

detection of audit risks as per financial ratio analysis of the company by MYH, the audit firm of

GPSA. Before starting the audit, audit plan is required and this is to be made with the

consultation of Audit partner, Mr. Richards. As per his requirement, this management report is

made to highlight five accounting heads namely accounts receivables, current investments,

intangible assets, property assets, research and development capitalization. The report will

consist of discussion of audit risks of these five heads, relevant business risks as per ratio

analysis, general internal control for good business practice and internal control for sales and

receivables for GPSA (Myaccountingcourse, 2016). This report is required prior to proceeding

of audit plan for the financial year ended on 30th June 2017. The audit report of the company is to

be submitted to the Board at the end of August 2017. The audit report will obviously contain the

auditing process with the finalization of accounts along with the proposed internal control to be

implemented in order to make the business sustainable in long run (Myaccountingcourse, 2016).

Audit Risk

The audit risks for the company are to be detected are of the following heads with proper ratio

analysis, audit risk detection and steps to reduce audit risk:

Accounts Receivables

Ratio Analysis- As per days in accounts receivable ratio, the receivable ageing is getting

increased in respect of average turnover. The trend of this ratio for the company is observed as

upward which depicts that the blockage of blockage of working capital is there through this

loophole. The company has latest trend of 83 days of 2017 as days on accounts receivable. It

means that the company can recover receivable beyond 83 days which is to be justified by the

company policy of credit sales

4

GPSA is engaged in different level of business with good profit. This report is meant for

detection of audit risks as per financial ratio analysis of the company by MYH, the audit firm of

GPSA. Before starting the audit, audit plan is required and this is to be made with the

consultation of Audit partner, Mr. Richards. As per his requirement, this management report is

made to highlight five accounting heads namely accounts receivables, current investments,

intangible assets, property assets, research and development capitalization. The report will

consist of discussion of audit risks of these five heads, relevant business risks as per ratio

analysis, general internal control for good business practice and internal control for sales and

receivables for GPSA (Myaccountingcourse, 2016). This report is required prior to proceeding

of audit plan for the financial year ended on 30th June 2017. The audit report of the company is to

be submitted to the Board at the end of August 2017. The audit report will obviously contain the

auditing process with the finalization of accounts along with the proposed internal control to be

implemented in order to make the business sustainable in long run (Myaccountingcourse, 2016).

Audit Risk

The audit risks for the company are to be detected are of the following heads with proper ratio

analysis, audit risk detection and steps to reduce audit risk:

Accounts Receivables

Ratio Analysis- As per days in accounts receivable ratio, the receivable ageing is getting

increased in respect of average turnover. The trend of this ratio for the company is observed as

upward which depicts that the blockage of blockage of working capital is there through this

loophole. The company has latest trend of 83 days of 2017 as days on accounts receivable. It

means that the company can recover receivable beyond 83 days which is to be justified by the

company policy of credit sales

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit Risks- As per Audit risk classification, this is a Control risk. This trend is tending towards

accounts receivable ageing to 90 days which is not good for the business. If the trend is

continuing, the amount of doubtful debts can be increased and the profit of the company will be

drained out. It is to be controlled with some measures of internal control within GPSA to ensure

reduction of ageing of accounts receivable gradually to the objective of attaining 65 days on

order to increase the good debts and reduce the tendency to doubtful debts of the accounts

receivables (Financeformulas, 2015).

Audit Steps to reduce risks- To reduce audit risks for GPSA, the company should follow AASB

Standard 9 – Financial Instruments – Accounts Receivables (Aasb, 2014).

MYH should follow ASA 240 with the following steps to be taken to reduce risk:

to find out the real sales justified by dispatch of items;

to have proper exercise on ageing analysis of the receivables for

identification of doubtful debts;

proper verification of credit sales by the agreement of the company

and the customers to comply with the agreed terms of payments;

to ensure that returned goods are to be taken back into stock through

credit notes;

Cash sales, if any, is to be differentiated from credit sales (Auasb,

2006).

Current investments

Ratio Analysis- This financial component is derived from Quick Ratio and Current Ratio. As

current investments are component of current assets, it contributes to those ratios. Current ratio

of GPSA is found >1, which means current assets are > current liabilities. But the Quick ratio of

GPSA is featuring <1, which means components of current assets like cash, cash equivalent,

current investments and receivables are less than current liabilities for GPSA. Thos is ideal and

good sign for the organization so far liquidity of the company is concerned (Aafp, 2016).

5

accounts receivable ageing to 90 days which is not good for the business. If the trend is

continuing, the amount of doubtful debts can be increased and the profit of the company will be

drained out. It is to be controlled with some measures of internal control within GPSA to ensure

reduction of ageing of accounts receivable gradually to the objective of attaining 65 days on

order to increase the good debts and reduce the tendency to doubtful debts of the accounts

receivables (Financeformulas, 2015).

Audit Steps to reduce risks- To reduce audit risks for GPSA, the company should follow AASB

Standard 9 – Financial Instruments – Accounts Receivables (Aasb, 2014).

MYH should follow ASA 240 with the following steps to be taken to reduce risk:

to find out the real sales justified by dispatch of items;

to have proper exercise on ageing analysis of the receivables for

identification of doubtful debts;

proper verification of credit sales by the agreement of the company

and the customers to comply with the agreed terms of payments;

to ensure that returned goods are to be taken back into stock through

credit notes;

Cash sales, if any, is to be differentiated from credit sales (Auasb,

2006).

Current investments

Ratio Analysis- This financial component is derived from Quick Ratio and Current Ratio. As

current investments are component of current assets, it contributes to those ratios. Current ratio

of GPSA is found >1, which means current assets are > current liabilities. But the Quick ratio of

GPSA is featuring <1, which means components of current assets like cash, cash equivalent,

current investments and receivables are less than current liabilities for GPSA. Thos is ideal and

good sign for the organization so far liquidity of the company is concerned (Aafp, 2016).

5

Audit Risks- As per Audit Risk classification, this is a Detection Risk. The risk is demanding

proper detection of financial instruments in the form of current investments. This is to be ensured

my MYH because failure of proper detection of current investment of GPSA with the salient

features of those investments. This is to be done to ensure as its real identity as a component of

current assets. GPSA should comply with AASB Standard 9 for the accounting treatment of

those current investments (Aasb, 2014).

Audit Steps to reduce risks- Following steps are to be taken for reduction of this risk as per the

guideline provided by ASA 545 by MYH to ensure Fair value measurement and subsequent

disclosure:

verification of proper documentation of current investments,

proper listing of the current investments with the date of maturity

and the amount to be repaid after the maturity,

Identification of any mortgage against those investments with the

detection of risk (Auasb, 2006).

Property assets

Ratio Analysis- Property assets are part of long-term assets and are derivable from the

consolidated financial statement of the company. It is always observed that the valuation of such

assets can be made from Return on total assets ratio. The consideration of total assets are done by

(opening value + closing value of assets)/2. Through the schedule of total assets with opening

and closing values of assets, property assets can be derived.

Audit Risks- Applicable type of audit risk for this component of financial instrument is detection

risk. Proper evaluation of property assets are to be made with the opening and closing value to

derive the addition during the year with consideration of anticipated depreciation or appreciation

of value of those assets. GPSA should follow AASB Standard 116- Property, Plant and Assets to

ensure proper treatment of those property assets which are with the company (Aasb, 2014).

6

proper detection of financial instruments in the form of current investments. This is to be ensured

my MYH because failure of proper detection of current investment of GPSA with the salient

features of those investments. This is to be done to ensure as its real identity as a component of

current assets. GPSA should comply with AASB Standard 9 for the accounting treatment of

those current investments (Aasb, 2014).

Audit Steps to reduce risks- Following steps are to be taken for reduction of this risk as per the

guideline provided by ASA 545 by MYH to ensure Fair value measurement and subsequent

disclosure:

verification of proper documentation of current investments,

proper listing of the current investments with the date of maturity

and the amount to be repaid after the maturity,

Identification of any mortgage against those investments with the

detection of risk (Auasb, 2006).

Property assets

Ratio Analysis- Property assets are part of long-term assets and are derivable from the

consolidated financial statement of the company. It is always observed that the valuation of such

assets can be made from Return on total assets ratio. The consideration of total assets are done by

(opening value + closing value of assets)/2. Through the schedule of total assets with opening

and closing values of assets, property assets can be derived.

Audit Risks- Applicable type of audit risk for this component of financial instrument is detection

risk. Proper evaluation of property assets are to be made with the opening and closing value to

derive the addition during the year with consideration of anticipated depreciation or appreciation

of value of those assets. GPSA should follow AASB Standard 116- Property, Plant and Assets to

ensure proper treatment of those property assets which are with the company (Aasb, 2014).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit steps to reduce risks- As these types of assets are generating revenue in the form of

revenue other than turnover as specified by the company operation of renting those to medical

practitioners, proper verification of rent agreements is to be done to assess the revenue earned

from those assets (Auasb, 2006). Moreover the valuation of the assets as per standard norms is to

be verified with effective guidance of AASB through AASB 15- revenue from contract with

customers. MYH should ensure the auditing procedure of these assets as per ASA Standard 240

and 545 for fair value measurement with subsequent disclosure (Auasb, 2013).

Intangible assets

Ratio Analysis- It is not possible to identify the component of intangible assets from the given

ratio analysis, but as it is a component of total assets, ROA is to be considered for deriving the

same with schedule of intangible assets of the company.

Audit risks- The identified audit risk related to this component is inherent risk. There may be

some material misstatement related to the valuation of these assets. GPSA should follow the

guideline of AASB Standard 138 meant for treatment of Intangible Assets (Aasb, 2015).

Audit steps to reduce risks- To ensure mitigation of audit risks, auditor should follow the

guideline of ASA 545 for valuation of intangible assets as this standard demands fair value

measurement of the intangible assets with subsequent disclosure (Auasb, 2006).

Research and development capitalization

Ratio Analysis- GPSA has taken loan for $ 5 million during this year for research and

development. The banker had put the criterion of debt to equity ratio should be below 1.2;

otherwise the bank may recover the loan amount at any time. The company is positioned at 1.11

7

revenue other than turnover as specified by the company operation of renting those to medical

practitioners, proper verification of rent agreements is to be done to assess the revenue earned

from those assets (Auasb, 2006). Moreover the valuation of the assets as per standard norms is to

be verified with effective guidance of AASB through AASB 15- revenue from contract with

customers. MYH should ensure the auditing procedure of these assets as per ASA Standard 240

and 545 for fair value measurement with subsequent disclosure (Auasb, 2013).

Intangible assets

Ratio Analysis- It is not possible to identify the component of intangible assets from the given

ratio analysis, but as it is a component of total assets, ROA is to be considered for deriving the

same with schedule of intangible assets of the company.

Audit risks- The identified audit risk related to this component is inherent risk. There may be

some material misstatement related to the valuation of these assets. GPSA should follow the

guideline of AASB Standard 138 meant for treatment of Intangible Assets (Aasb, 2015).

Audit steps to reduce risks- To ensure mitigation of audit risks, auditor should follow the

guideline of ASA 545 for valuation of intangible assets as this standard demands fair value

measurement of the intangible assets with subsequent disclosure (Auasb, 2006).

Research and development capitalization

Ratio Analysis- GPSA has taken loan for $ 5 million during this year for research and

development. The banker had put the criterion of debt to equity ratio should be below 1.2;

otherwise the bank may recover the loan amount at any time. The company is positioned at 1.11

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

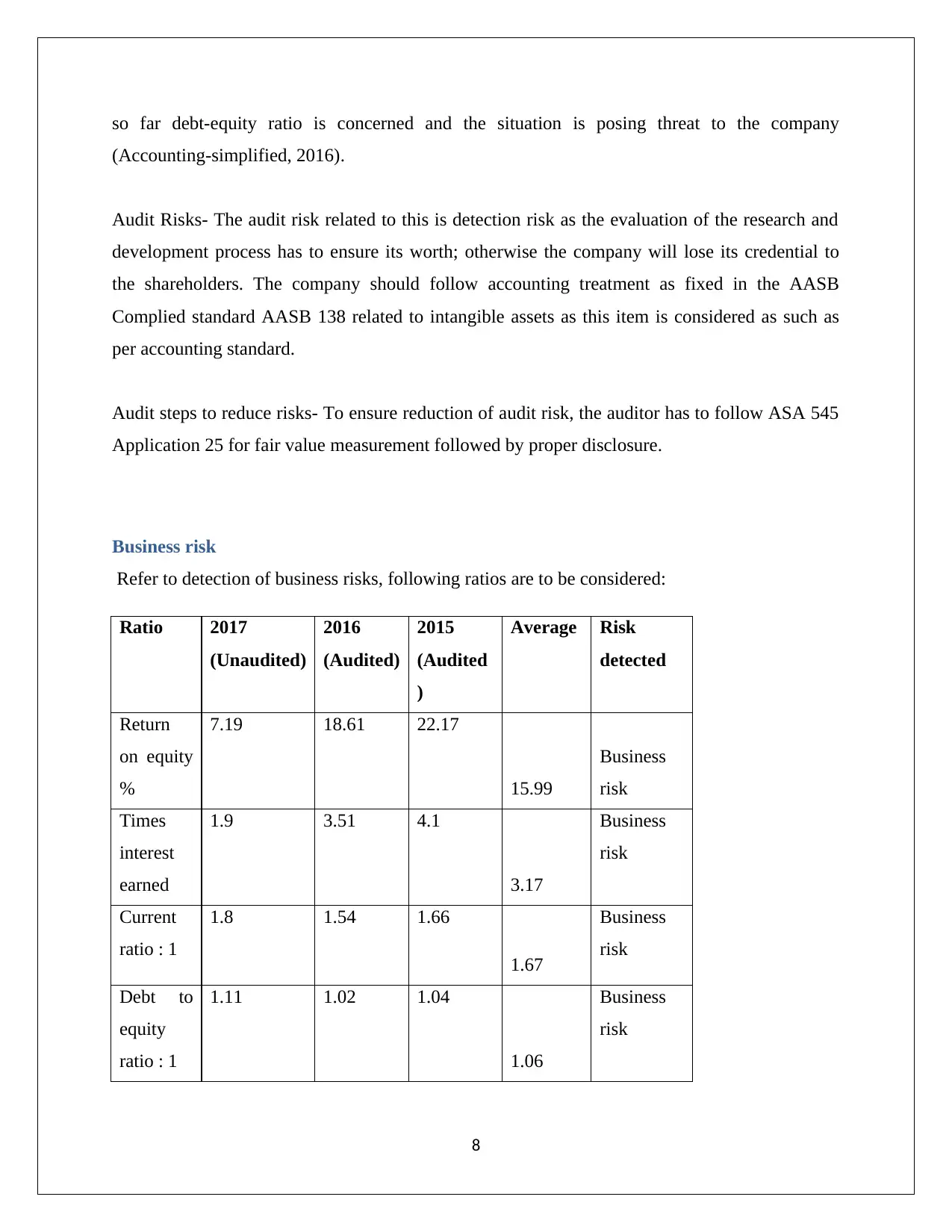

so far debt-equity ratio is concerned and the situation is posing threat to the company

(Accounting-simplified, 2016).

Audit Risks- The audit risk related to this is detection risk as the evaluation of the research and

development process has to ensure its worth; otherwise the company will lose its credential to

the shareholders. The company should follow accounting treatment as fixed in the AASB

Complied standard AASB 138 related to intangible assets as this item is considered as such as

per accounting standard.

Audit steps to reduce risks- To ensure reduction of audit risk, the auditor has to follow ASA 545

Application 25 for fair value measurement followed by proper disclosure.

Business risk

Refer to detection of business risks, following ratios are to be considered:

Ratio 2017

(Unaudited)

2016

(Audited)

2015

(Audited

)

Average Risk

detected

Return

on equity

%

7.19 18.61 22.17

15.99

Business

risk

Times

interest

earned

1.9 3.51 4.1

3.17

Business

risk

Current

ratio : 1

1.8 1.54 1.66

1.67

Business

risk

Debt to

equity

ratio : 1

1.11 1.02 1.04

1.06

Business

risk

8

(Accounting-simplified, 2016).

Audit Risks- The audit risk related to this is detection risk as the evaluation of the research and

development process has to ensure its worth; otherwise the company will lose its credential to

the shareholders. The company should follow accounting treatment as fixed in the AASB

Complied standard AASB 138 related to intangible assets as this item is considered as such as

per accounting standard.

Audit steps to reduce risks- To ensure reduction of audit risk, the auditor has to follow ASA 545

Application 25 for fair value measurement followed by proper disclosure.

Business risk

Refer to detection of business risks, following ratios are to be considered:

Ratio 2017

(Unaudited)

2016

(Audited)

2015

(Audited

)

Average Risk

detected

Return

on equity

%

7.19 18.61 22.17

15.99

Business

risk

Times

interest

earned

1.9 3.51 4.1

3.17

Business

risk

Current

ratio : 1

1.8 1.54 1.66

1.67

Business

risk

Debt to

equity

ratio : 1

1.11 1.02 1.04

1.06

Business

risk

8

Return on equity (ROE)

ROE of GPSA is decreasing in steady rate during 2015 to 2017. As the components of

calculation of ROE are net income and average assets, it is observed that the rate of deployment

of net income for acquisition of assets are getting declined which pose risk to the business.

Times interest earned

This ratio is derived from EBIT/ interest expenses. As the company had taken fresh loan from

bankers for their research and development, interest expenses increased which makes the ratio of

2017 at 1.9. Moreover as one of the competitors had announced their achievement for same

machinery with subsequent patent, this investment causes great risk to the business

Current ratio

Current ratio shows the strength of the company so far its financial liquidity is concerned. As the

present ratio stands at 1.8, it depicts that the current assets are 1.8 times than current liabilities.

The current assets include inventories which are consisting of good and obsolete inventories also.

Moreover, the accounts receivable is also a component of current assets which contains doubtful

debts as the company has days in accounts receivable of 83 days. Most of the customers are of

credit sales with specific terms and conditions and thus recovery of such receivable in full is

problematic for the company (Myaccountingcourse, 2016).

Debt to equity ratio

Debt to equity ratio shows 1.11 in 2017. This is due to the new introduction of loan by bankers

for the research and development of the company. Due to the standing agreement of the bank, if

this ratio reaches 1.2, the bank will immediate recover the money from the company. Hence this

ration is posing business risk and to be controlled with justified decision by Board.

9

ROE of GPSA is decreasing in steady rate during 2015 to 2017. As the components of

calculation of ROE are net income and average assets, it is observed that the rate of deployment

of net income for acquisition of assets are getting declined which pose risk to the business.

Times interest earned

This ratio is derived from EBIT/ interest expenses. As the company had taken fresh loan from

bankers for their research and development, interest expenses increased which makes the ratio of

2017 at 1.9. Moreover as one of the competitors had announced their achievement for same

machinery with subsequent patent, this investment causes great risk to the business

Current ratio

Current ratio shows the strength of the company so far its financial liquidity is concerned. As the

present ratio stands at 1.8, it depicts that the current assets are 1.8 times than current liabilities.

The current assets include inventories which are consisting of good and obsolete inventories also.

Moreover, the accounts receivable is also a component of current assets which contains doubtful

debts as the company has days in accounts receivable of 83 days. Most of the customers are of

credit sales with specific terms and conditions and thus recovery of such receivable in full is

problematic for the company (Myaccountingcourse, 2016).

Debt to equity ratio

Debt to equity ratio shows 1.11 in 2017. This is due to the new introduction of loan by bankers

for the research and development of the company. Due to the standing agreement of the bank, if

this ratio reaches 1.2, the bank will immediate recover the money from the company. Hence this

ration is posing business risk and to be controlled with justified decision by Board.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

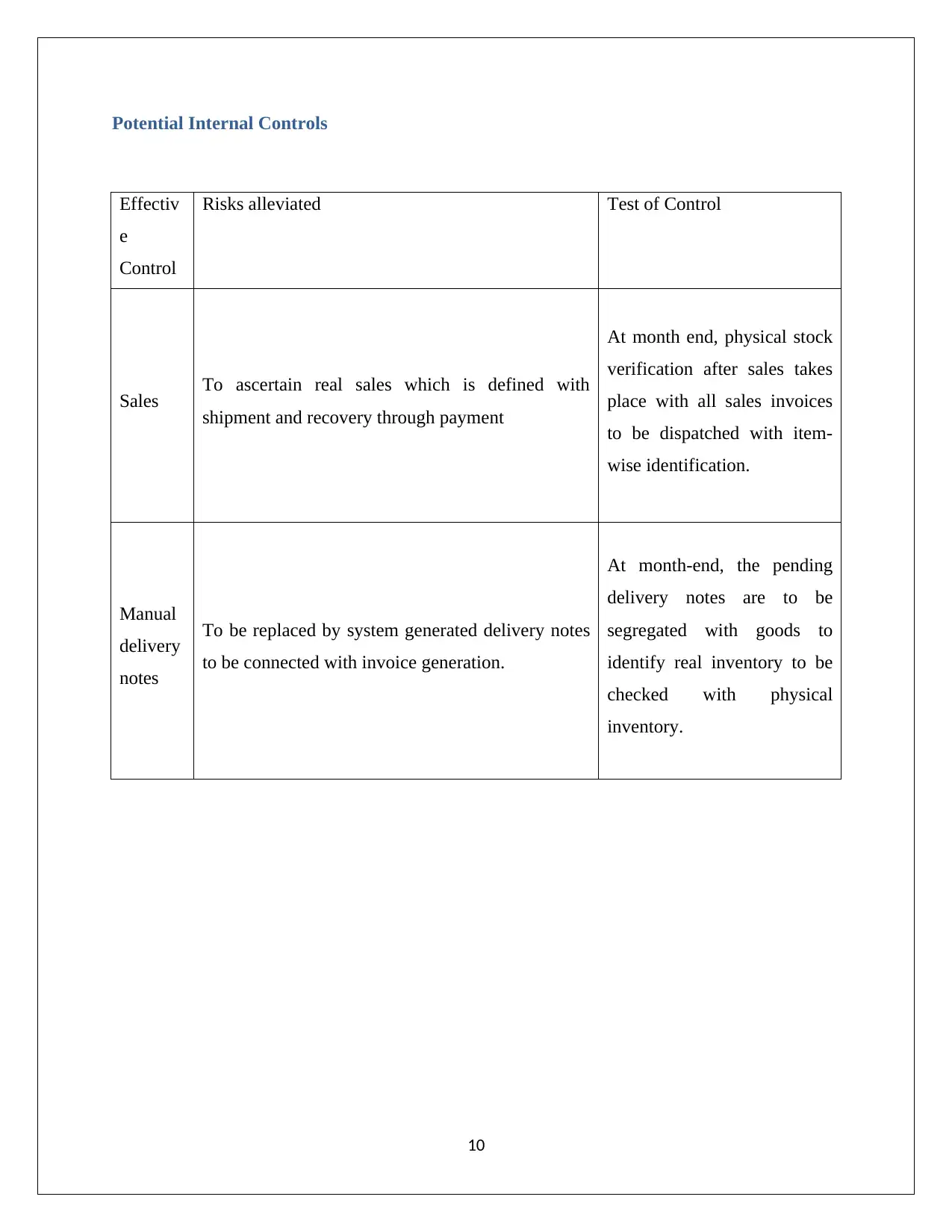

Potential Internal Controls

Effectiv

e

Control

Risks alleviated Test of Control

Sales To ascertain real sales which is defined with

shipment and recovery through payment

At month end, physical stock

verification after sales takes

place with all sales invoices

to be dispatched with item-

wise identification.

Manual

delivery

notes

To be replaced by system generated delivery notes

to be connected with invoice generation.

At month-end, the pending

delivery notes are to be

segregated with goods to

identify real inventory to be

checked with physical

inventory.

10

Effectiv

e

Control

Risks alleviated Test of Control

Sales To ascertain real sales which is defined with

shipment and recovery through payment

At month end, physical stock

verification after sales takes

place with all sales invoices

to be dispatched with item-

wise identification.

Manual

delivery

notes

To be replaced by system generated delivery notes

to be connected with invoice generation.

At month-end, the pending

delivery notes are to be

segregated with goods to

identify real inventory to be

checked with physical

inventory.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

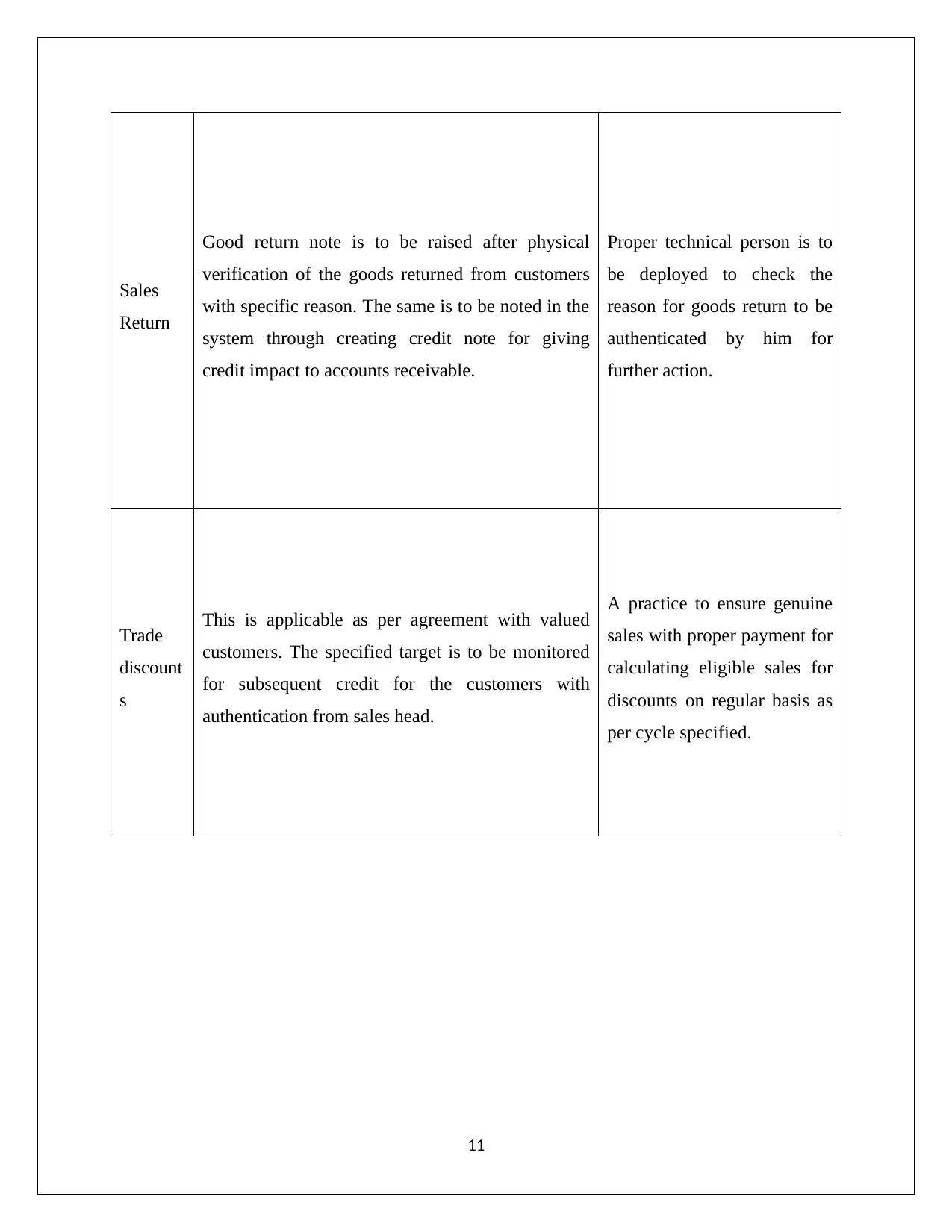

Sales

Return

Good return note is to be raised after physical

verification of the goods returned from customers

with specific reason. The same is to be noted in the

system through creating credit note for giving

credit impact to accounts receivable.

Proper technical person is to

be deployed to check the

reason for goods return to be

authenticated by him for

further action.

Trade

discount

s

This is applicable as per agreement with valued

customers. The specified target is to be monitored

for subsequent credit for the customers with

authentication from sales head.

A practice to ensure genuine

sales with proper payment for

calculating eligible sales for

discounts on regular basis as

per cycle specified.

11

Return

Good return note is to be raised after physical

verification of the goods returned from customers

with specific reason. The same is to be noted in the

system through creating credit note for giving

credit impact to accounts receivable.

Proper technical person is to

be deployed to check the

reason for goods return to be

authenticated by him for

further action.

Trade

discount

s

This is applicable as per agreement with valued

customers. The specified target is to be monitored

for subsequent credit for the customers with

authentication from sales head.

A practice to ensure genuine

sales with proper payment for

calculating eligible sales for

discounts on regular basis as

per cycle specified.

11

Weaknesses in Internal Control for Sales and Trade Receivables

Basic weaknesses found in internal control:

For Sales:

Lack of priority for generating genuine sales

Non compliance of strict dispatch schedule

Lack of control in goods return system

Inventory management

Lack of proper control to stop fictitious sales by sales team

For Trade Receivables:

Most of the sales are credit sales

Recovery of receivables are not strictly maintained as per payment terms

Receivables ageing analysis is getting high with more blockage of working capital

Regular follow up of receivables are not done on routine basis

Sales made are not followed up for steady payment practice

Conclusion

With the above report, I will conclude that different financial areas of business of GPSA needs

to be taken under the scanner in the form of accounts receivables, sales, property assets,

intangible assets and capitalization of research and development. The financial ratios of the

company are the basic resources for this primary management report related to auditing with

basic objective of detection of audit risks and subsequent steps to avoid audit risks, detection of

business risks of the company, prescribed internal control in different areas with the basic

weaknesses of internal control in the areas of trades receivables and sales. This report has

12

Basic weaknesses found in internal control:

For Sales:

Lack of priority for generating genuine sales

Non compliance of strict dispatch schedule

Lack of control in goods return system

Inventory management

Lack of proper control to stop fictitious sales by sales team

For Trade Receivables:

Most of the sales are credit sales

Recovery of receivables are not strictly maintained as per payment terms

Receivables ageing analysis is getting high with more blockage of working capital

Regular follow up of receivables are not done on routine basis

Sales made are not followed up for steady payment practice

Conclusion

With the above report, I will conclude that different financial areas of business of GPSA needs

to be taken under the scanner in the form of accounts receivables, sales, property assets,

intangible assets and capitalization of research and development. The financial ratios of the

company are the basic resources for this primary management report related to auditing with

basic objective of detection of audit risks and subsequent steps to avoid audit risks, detection of

business risks of the company, prescribed internal control in different areas with the basic

weaknesses of internal control in the areas of trades receivables and sales. This report has

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.