Auditing Report: Analysis of Account Selection and Audit Procedures

VerifiedAdded on 2020/03/16

|14

|2372

|205

Report

AI Summary

This auditing report provides a comprehensive analysis of financial accounts, detailing the selection of seven key accounts for audit, including accounts receivable, depreciation, repairs and maintenance, inventory, wages, cash at bank, and sales. The report offers rationales for each account selection based on fluctuations in financial data, such as percentage increases or decreases from the previous year. It outlines specific audit procedures recommended for each account, focusing on verifying the accuracy of financial statements and ensuring compliance with accounting standards. The report also includes a horizontal analysis of the income statement and balance sheet, providing context for the audit procedures and highlighting significant changes in financial performance and position. The analysis covers the audit planning process, including analytical review and preliminary judgment of materiality, to provide a comprehensive understanding of the audit process. References from various sources are provided to support the findings and recommendations within the report.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Authors Note:

Auditing

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING

Table of Contents

1. Audit planning:.......................................................................................................................3

1.1Analytical Review:................................................................................................................3

1.2Preliminary judgment of materiality:....................................................................................3

2. Selected First account:...........................................................................................................4

2.1 Rationale for selection:........................................................................................................4

2.2Assertion and explanation:....................................................................................................4

2.3 Recommended audit procedure:...........................................................................................4

3. Selected Second account:.......................................................................................................5

3.1Rationale for selection:.........................................................................................................5

3.2Assertion and explanation:....................................................................................................5

3.3 Recommended audit procedure:...........................................................................................5

4 Selected third account:............................................................................................................5

4.1 Rationale for selection:........................................................................................................6

4.2 Assertion and explanation:...................................................................................................6

4.3 Recommended audit procedure:...........................................................................................6

5. Selected fourth account:.........................................................................................................6

5.1 Rationale for selection:........................................................................................................6

5.2 Assertion and explanation:...................................................................................................7

5.3 Recommended audit procedure:...........................................................................................7

6. Selected Fifth account:...........................................................................................................7

6.1 Rationale for selection:........................................................................................................7

Table of Contents

1. Audit planning:.......................................................................................................................3

1.1Analytical Review:................................................................................................................3

1.2Preliminary judgment of materiality:....................................................................................3

2. Selected First account:...........................................................................................................4

2.1 Rationale for selection:........................................................................................................4

2.2Assertion and explanation:....................................................................................................4

2.3 Recommended audit procedure:...........................................................................................4

3. Selected Second account:.......................................................................................................5

3.1Rationale for selection:.........................................................................................................5

3.2Assertion and explanation:....................................................................................................5

3.3 Recommended audit procedure:...........................................................................................5

4 Selected third account:............................................................................................................5

4.1 Rationale for selection:........................................................................................................6

4.2 Assertion and explanation:...................................................................................................6

4.3 Recommended audit procedure:...........................................................................................6

5. Selected fourth account:.........................................................................................................6

5.1 Rationale for selection:........................................................................................................6

5.2 Assertion and explanation:...................................................................................................7

5.3 Recommended audit procedure:...........................................................................................7

6. Selected Fifth account:...........................................................................................................7

6.1 Rationale for selection:........................................................................................................7

2AUDITING

6.2 Assertion and explanation:...................................................................................................7

6.3 Recommended audit procedure:...........................................................................................7

7.1 Rationale for selection:........................................................................................................8

7.2 Assertion and explanation:...................................................................................................8

7.3 Recommended audit procedure:...........................................................................................8

8. Selected seventh account:......................................................................................................8

8.1 Rationale for selection:........................................................................................................9

8.2 Assertion and explanation:...................................................................................................9

8.3Recommended audit procedure:............................................................................................9

Reference..................................................................................................................................12

6.2 Assertion and explanation:...................................................................................................7

6.3 Recommended audit procedure:...........................................................................................7

7.1 Rationale for selection:........................................................................................................8

7.2 Assertion and explanation:...................................................................................................8

7.3 Recommended audit procedure:...........................................................................................8

8. Selected seventh account:......................................................................................................8

8.1 Rationale for selection:........................................................................................................9

8.2 Assertion and explanation:...................................................................................................9

8.3Recommended audit procedure:............................................................................................9

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING

1. Audit planning:

In this report, innovative methods have been implemented to select seven accounts for

the purpose of audit. The choosing of number of accounts is being done in a way that to

examine the objective of extraordinary fluctuations in particular pieces and aids to detect the

reason of the variations. The variations percentage in pieces along the variations in trail

balance is taken as a base.

1.1Analytical Review:

The review in a systematic manner is displayed as the extraordinary variations in the

current year by utilising the dissimilar statistical and mathematical modus operandi through a

model of variations. The analysis of ratios is utilized to examine the extraordinary variations

in solidarity or liquidity ratio of a business along with the extraordinary variations in

prosperity in the institute (Knechel W.R. and Salterio 2016).

The sales have increased slight by 0.83% in the end of the year on 30th June 2017

from the figures of the previous year. Therefore, the profit of the business have increased in

the current year. The system of audit proficiently discovers the cause of the augmentation of

the profits in the system of audit that they will accomplish.

1.2Preliminary judgment of materiality:

At this point of time the materials has been settled in intriguing into the consideration

a particular percentage of the pieces sums to the full sum of the earnings, expenditures, assets

and liabilities that is related. The pieces are selected as per the earnings of the pieces and if

the earnings is not less than 5% of the aggregate income of the business then those pieces are

taken into consideration and acknowledged or else no tactics and time are being maltreatment

on those times (Junior et al. 2014).

1. Audit planning:

In this report, innovative methods have been implemented to select seven accounts for

the purpose of audit. The choosing of number of accounts is being done in a way that to

examine the objective of extraordinary fluctuations in particular pieces and aids to detect the

reason of the variations. The variations percentage in pieces along the variations in trail

balance is taken as a base.

1.1Analytical Review:

The review in a systematic manner is displayed as the extraordinary variations in the

current year by utilising the dissimilar statistical and mathematical modus operandi through a

model of variations. The analysis of ratios is utilized to examine the extraordinary variations

in solidarity or liquidity ratio of a business along with the extraordinary variations in

prosperity in the institute (Knechel W.R. and Salterio 2016).

The sales have increased slight by 0.83% in the end of the year on 30th June 2017

from the figures of the previous year. Therefore, the profit of the business have increased in

the current year. The system of audit proficiently discovers the cause of the augmentation of

the profits in the system of audit that they will accomplish.

1.2Preliminary judgment of materiality:

At this point of time the materials has been settled in intriguing into the consideration

a particular percentage of the pieces sums to the full sum of the earnings, expenditures, assets

and liabilities that is related. The pieces are selected as per the earnings of the pieces and if

the earnings is not less than 5% of the aggregate income of the business then those pieces are

taken into consideration and acknowledged or else no tactics and time are being maltreatment

on those times (Junior et al. 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING

2. Selected First account:

The account that have been selected for audit is Accounts Receivable.

2.1 Rationale for selection:

The Account receivable account is selected as thre has been 49% incresae in the balance.

2.2Assertion and explanation:

In the books of accounts there is an augmented in around 49% from the earlier year

where the receivable accounts and therefore this must be investigated appropriately in a way

to preserve the accounts balance.

2.3 Recommended audit procedure:

The ledger relating to receivables has augmented in the significant year that sums to

boost in 49% which is a positive aspect at the very present moment, this has its own concerns

and disadvantages at the very present moment. If there is enhancement in trade, which will

matches to the augment in the balance of receivable accounts that should be warranted. As

consequence, at the time when variation takes place in the balance of receivable accounts

beside with the augmentation in the trade from the earlier year’s the balance’s are observed

but this not augmented in the amount of the earnings will not be alteration with not a great

acceptance (Redmayne 2013). The examining and confirming the process of the trade is

being keeping with the credit. The total improvement of sale in credit will have to be verified

in a way to assure that paradigm procedure of sale is pursued in the business. The managing

the variations of any amount are done with aid of the Report as through a pattern procedure.

The payments by the customers are examined to discover the any sort of discrepancies in

relation to the structure and arrangement that should be charged by employee relating the

compensation in the way to steal from the business. Proper time limits are also permitted to

2. Selected First account:

The account that have been selected for audit is Accounts Receivable.

2.1 Rationale for selection:

The Account receivable account is selected as thre has been 49% incresae in the balance.

2.2Assertion and explanation:

In the books of accounts there is an augmented in around 49% from the earlier year

where the receivable accounts and therefore this must be investigated appropriately in a way

to preserve the accounts balance.

2.3 Recommended audit procedure:

The ledger relating to receivables has augmented in the significant year that sums to

boost in 49% which is a positive aspect at the very present moment, this has its own concerns

and disadvantages at the very present moment. If there is enhancement in trade, which will

matches to the augment in the balance of receivable accounts that should be warranted. As

consequence, at the time when variation takes place in the balance of receivable accounts

beside with the augmentation in the trade from the earlier year’s the balance’s are observed

but this not augmented in the amount of the earnings will not be alteration with not a great

acceptance (Redmayne 2013). The examining and confirming the process of the trade is

being keeping with the credit. The total improvement of sale in credit will have to be verified

in a way to assure that paradigm procedure of sale is pursued in the business. The managing

the variations of any amount are done with aid of the Report as through a pattern procedure.

The payments by the customers are examined to discover the any sort of discrepancies in

relation to the structure and arrangement that should be charged by employee relating the

compensation in the way to steal from the business. Proper time limits are also permitted to

5AUDITING

the consumers are also examined besides the administering on the surroundings and they are

capable of bringing together the dues appropriately or not from the consumers and this are

reported as in accordance.

3. Selected Second account:

Account of Depreciation

3.1Rationale for selection:

The deprecation account is selected because the depreciation amount has increased by

127.59%

3.2Assertion and explanation:

In financial statement, a crucial component will be the account for depreciation. If

there is enhancements in 127.59% from the earlier year then this businesses depreciation

every year will be selected for the objective of auditing.

3.3 Recommended audit procedure:

Inspecting of the proper ways that should be completed in the business. Steadiness

must be present in the way to evaluate the depreciation and must be observed as alterations of

the ways that has done by the business in the way to supply depreciations in the current year

and if they did the modification then those alterations must be established.

4 Selected third account:

Accounts of Repairs and maintenance

the consumers are also examined besides the administering on the surroundings and they are

capable of bringing together the dues appropriately or not from the consumers and this are

reported as in accordance.

3. Selected Second account:

Account of Depreciation

3.1Rationale for selection:

The deprecation account is selected because the depreciation amount has increased by

127.59%

3.2Assertion and explanation:

In financial statement, a crucial component will be the account for depreciation. If

there is enhancements in 127.59% from the earlier year then this businesses depreciation

every year will be selected for the objective of auditing.

3.3 Recommended audit procedure:

Inspecting of the proper ways that should be completed in the business. Steadiness

must be present in the way to evaluate the depreciation and must be observed as alterations of

the ways that has done by the business in the way to supply depreciations in the current year

and if they did the modification then those alterations must be established.

4 Selected third account:

Accounts of Repairs and maintenance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING

4.1 Rationale for selection:

The repair and maintenance has been selected as it has declined by 78.61%.

4.2 Assertion and explanation:

As in common, maltreatment of the accounts are done in the lack of repairs and

maintenance. The cause for decline in the expenses should be evaluated appropriately so the

variations of the accounts in the current year may be observed.

4.3 Recommended audit procedure:

The agreements that are legally binding are being confirmed in case where in the

institution is Performing repair and maintenance associated tasks inside the business,

therefore the institute compensation are verified whether the compensation is been completed

in appropriate manner or not good with accords of the contract. A authentication procedure

must be enhanced that assures the administration pursues the procedure of the repair and

maintenance (Soh and Martinov-Bennie 2015). The agreement that is lawfully binding must

be given to the smallest possible trader when the other contractor is not concerned. There

must be no malpractice of the monetary sums in the name of the maintenance and repairs.

5. Selected fourth account:

In the way for the even execution of the institutions inventory has been chosen for the

significance.

5.1 Rationale for selection:

The inventory account is selected as there has been 4% incresae from the previous

year.

4.1 Rationale for selection:

The repair and maintenance has been selected as it has declined by 78.61%.

4.2 Assertion and explanation:

As in common, maltreatment of the accounts are done in the lack of repairs and

maintenance. The cause for decline in the expenses should be evaluated appropriately so the

variations of the accounts in the current year may be observed.

4.3 Recommended audit procedure:

The agreements that are legally binding are being confirmed in case where in the

institution is Performing repair and maintenance associated tasks inside the business,

therefore the institute compensation are verified whether the compensation is been completed

in appropriate manner or not good with accords of the contract. A authentication procedure

must be enhanced that assures the administration pursues the procedure of the repair and

maintenance (Soh and Martinov-Bennie 2015). The agreement that is lawfully binding must

be given to the smallest possible trader when the other contractor is not concerned. There

must be no malpractice of the monetary sums in the name of the maintenance and repairs.

5. Selected fourth account:

In the way for the even execution of the institutions inventory has been chosen for the

significance.

5.1 Rationale for selection:

The inventory account is selected as there has been 4% incresae from the previous

year.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING

5.2 Assertion and explanation:

To operate and function the institutions inventory is essential for this functioning’s

and the operation’s that in turn nominated for the objective of auditing for the regulation of

the administrating on the inventories.

5.3 Recommended audit procedure:

For the objective of regulating of inventory systems like LIFO, average cost method,

FIFO are utilized that aids the auditor to be acquainted with the vital role through the

structure of administration around the earth. The auditor mechanism is to test out the modes

that is allotted in the inventory to the administration are pursued properly in the year or not.

6. Selected Fifth account:

The significance of the wages towards the institutions

6.1 Rationale for selection:

The wages account is selected as there has been 9% decline in amount.

6.2 Assertion and explanation:

The procedure of the audit must assess the worker’s wages as a proper and separate

account. The debt obligations of the institutions as wage’s of the worker should be

compensated on due time with the least amount for the rate of wages that they must be

worthy of so as to operate and function for the long term (Hay et al. 2016).

6.3 Recommended audit procedure:

An appropriate register must be maintained and preserved to verify and assess the

turnout of the hands along with the appropriate wages that are arranged on time or not.

Hence, the register that is utilized for the objective of attendance is preserved and maintained

5.2 Assertion and explanation:

To operate and function the institutions inventory is essential for this functioning’s

and the operation’s that in turn nominated for the objective of auditing for the regulation of

the administrating on the inventories.

5.3 Recommended audit procedure:

For the objective of regulating of inventory systems like LIFO, average cost method,

FIFO are utilized that aids the auditor to be acquainted with the vital role through the

structure of administration around the earth. The auditor mechanism is to test out the modes

that is allotted in the inventory to the administration are pursued properly in the year or not.

6. Selected Fifth account:

The significance of the wages towards the institutions

6.1 Rationale for selection:

The wages account is selected as there has been 9% decline in amount.

6.2 Assertion and explanation:

The procedure of the audit must assess the worker’s wages as a proper and separate

account. The debt obligations of the institutions as wage’s of the worker should be

compensated on due time with the least amount for the rate of wages that they must be

worthy of so as to operate and function for the long term (Hay et al. 2016).

6.3 Recommended audit procedure:

An appropriate register must be maintained and preserved to verify and assess the

turnout of the hands along with the appropriate wages that are arranged on time or not.

Hence, the register that is utilized for the objective of attendance is preserved and maintained

8AUDITING

by the institution and for the ways of compensating are also evaluates any discrepancies. This

is also verified whether the compensation is made in the way of direct transfer through the

account of bank or cash. If the compensation of cash are made then this should be pursued to

procedure of bank transfers.

7. Selected sixth account:

Cash at bank and in hand for its vulnerabilities reasons

7.1 Rationale for selection:

The cash and bank is selected as there has been 10% decline.

7.2 Assertion and explanation:

A crucial component for committing fraud is cash at bank and cash handlings are due

to this huge value and liquidity. Therefore, the administration thus chooses for the objective

of auditing is assuring the handling of cash, bank transfers or cash resources.

7.3 Recommended audit procedure:

The routine authentication of cash has to be displayed by the administration also

checks to evaluate whether the arrangement is paradigm for the administration or not. The

cyclic resolution may be there as the inspections are must for the auditors to inspect the

statements to help the regulation of the administration over the transactions and dealings

related to cash (Australia 2016).

8. Selected seventh account:

Sales account is chosen for auditing

by the institution and for the ways of compensating are also evaluates any discrepancies. This

is also verified whether the compensation is made in the way of direct transfer through the

account of bank or cash. If the compensation of cash are made then this should be pursued to

procedure of bank transfers.

7. Selected sixth account:

Cash at bank and in hand for its vulnerabilities reasons

7.1 Rationale for selection:

The cash and bank is selected as there has been 10% decline.

7.2 Assertion and explanation:

A crucial component for committing fraud is cash at bank and cash handlings are due

to this huge value and liquidity. Therefore, the administration thus chooses for the objective

of auditing is assuring the handling of cash, bank transfers or cash resources.

7.3 Recommended audit procedure:

The routine authentication of cash has to be displayed by the administration also

checks to evaluate whether the arrangement is paradigm for the administration or not. The

cyclic resolution may be there as the inspections are must for the auditors to inspect the

statements to help the regulation of the administration over the transactions and dealings

related to cash (Australia 2016).

8. Selected seventh account:

Sales account is chosen for auditing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING

8.1 Rationale for selection:

There has been 0.83% increase in sales but it is selected because it forms an important

component of the financial statement

8.2 Assertion and explanation:

The assertions that is tested by auditing of sales is the existence and completeness of

the transaction. It is tested by performing audit procedure whether sales have actually taken

place during the year and the sales have been recorded (Houghton and Campbell 2013).

8.3Recommended audit procedure:

The auditor evaluates the regulations of the business has been made for the cycle of

sales to ascertain the strength and credibility of this. If these are of good strength, an auditor

must diminish the sum of the dealings examination he should do. The programs for the cash

receipts must be made and a procedure for audit and purposes for the audit must be made.

8.1 Rationale for selection:

There has been 0.83% increase in sales but it is selected because it forms an important

component of the financial statement

8.2 Assertion and explanation:

The assertions that is tested by auditing of sales is the existence and completeness of

the transaction. It is tested by performing audit procedure whether sales have actually taken

place during the year and the sales have been recorded (Houghton and Campbell 2013).

8.3Recommended audit procedure:

The auditor evaluates the regulations of the business has been made for the cycle of

sales to ascertain the strength and credibility of this. If these are of good strength, an auditor

must diminish the sum of the dealings examination he should do. The programs for the cash

receipts must be made and a procedure for audit and purposes for the audit must be made.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING

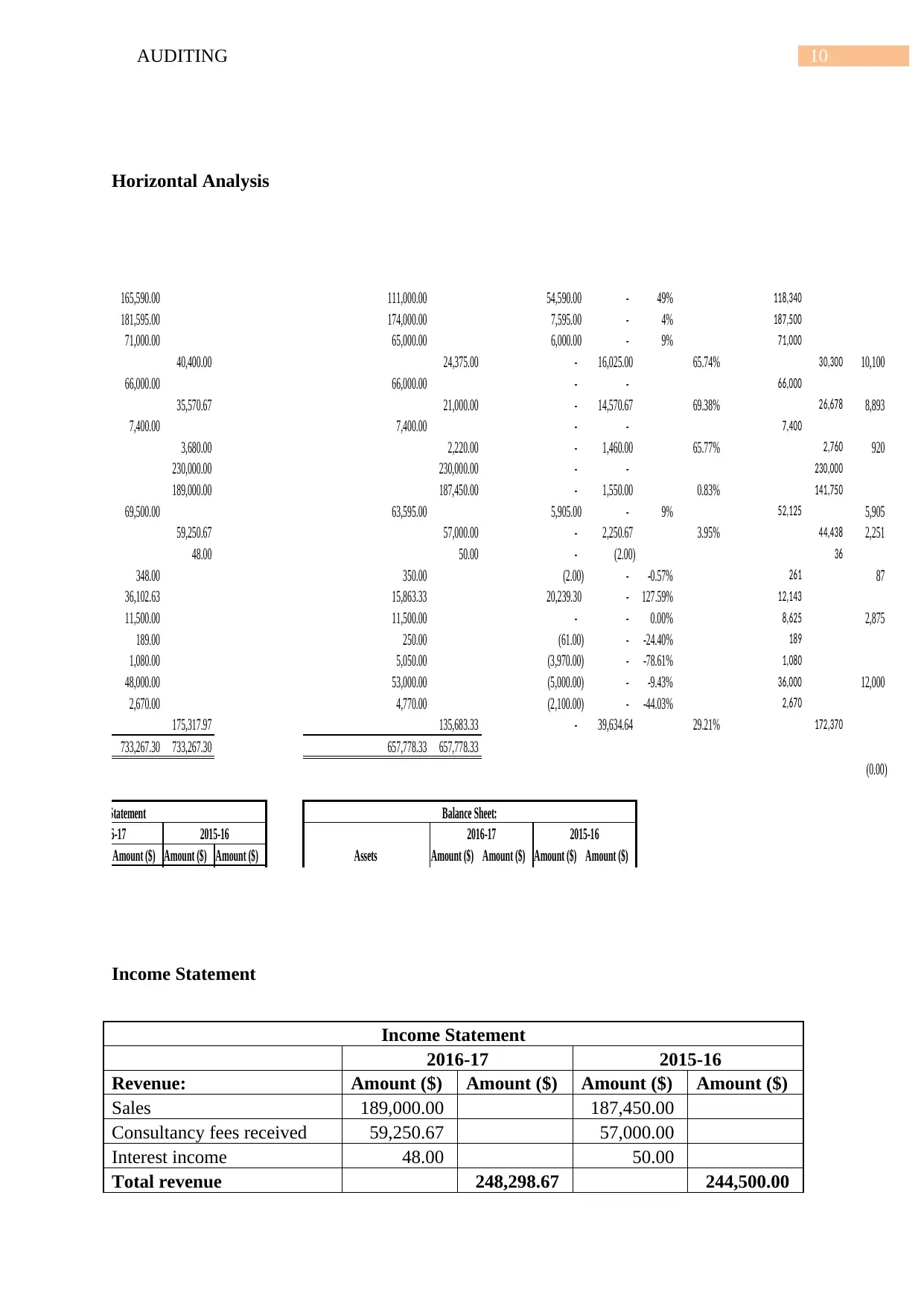

Horizontal Analysis

165,590.00 111,000.00 54,590.00 - 49% 118,340

181,595.00 174,000.00 7,595.00 - 4% 187,500

71,000.00 65,000.00 6,000.00 - 9% 71,000

40,400.00 24,375.00 - 16,025.00 65.74% 30,300 10,100

66,000.00 66,000.00 - - 66,000

35,570.67 21,000.00 - 14,570.67 69.38% 26,678 8,893

7,400.00 7,400.00 - - 7,400

3,680.00 2,220.00 - 1,460.00 65.77% 2,760 920

230,000.00 230,000.00 - - 230,000

189,000.00 187,450.00 - 1,550.00 0.83% 141,750

69,500.00 63,595.00 5,905.00 - 9% 52,125 5,905

59,250.67 57,000.00 - 2,250.67 3.95% 44,438 2,251

48.00 50.00 - (2.00) 36

348.00 350.00 (2.00) - -0.57% 261 87

36,102.63 15,863.33 20,239.30 - 127.59% 12,143

11,500.00 11,500.00 - - 0.00% 8,625 2,875

189.00 250.00 (61.00) - -24.40% 189

1,080.00 5,050.00 (3,970.00) - -78.61% 1,080

48,000.00 53,000.00 (5,000.00) - -9.43% 36,000 12,000

2,670.00 4,770.00 (2,100.00) - -44.03% 2,670

175,317.97 135,683.33 - 39,634.64 29.21% 172,370

733,267.30 733,267.30 657,778.33 657,778.33

(0.00)

Income Statement Balance Sheet:

2016-17 2015-16

Assets

2016-17 2015-16

Amount ($) Amount ($) Amount ($) Amount ($) Amount ($) Amount ($) Amount ($)

Income Statement

Income Statement

2016-17 2015-16

Revenue: Amount ($) Amount ($) Amount ($) Amount ($)

Sales 189,000.00 187,450.00

Consultancy fees received 59,250.67 57,000.00

Interest income 48.00 50.00

Total revenue 248,298.67 244,500.00

Horizontal Analysis

165,590.00 111,000.00 54,590.00 - 49% 118,340

181,595.00 174,000.00 7,595.00 - 4% 187,500

71,000.00 65,000.00 6,000.00 - 9% 71,000

40,400.00 24,375.00 - 16,025.00 65.74% 30,300 10,100

66,000.00 66,000.00 - - 66,000

35,570.67 21,000.00 - 14,570.67 69.38% 26,678 8,893

7,400.00 7,400.00 - - 7,400

3,680.00 2,220.00 - 1,460.00 65.77% 2,760 920

230,000.00 230,000.00 - - 230,000

189,000.00 187,450.00 - 1,550.00 0.83% 141,750

69,500.00 63,595.00 5,905.00 - 9% 52,125 5,905

59,250.67 57,000.00 - 2,250.67 3.95% 44,438 2,251

48.00 50.00 - (2.00) 36

348.00 350.00 (2.00) - -0.57% 261 87

36,102.63 15,863.33 20,239.30 - 127.59% 12,143

11,500.00 11,500.00 - - 0.00% 8,625 2,875

189.00 250.00 (61.00) - -24.40% 189

1,080.00 5,050.00 (3,970.00) - -78.61% 1,080

48,000.00 53,000.00 (5,000.00) - -9.43% 36,000 12,000

2,670.00 4,770.00 (2,100.00) - -44.03% 2,670

175,317.97 135,683.33 - 39,634.64 29.21% 172,370

733,267.30 733,267.30 657,778.33 657,778.33

(0.00)

Income Statement Balance Sheet:

2016-17 2015-16

Assets

2016-17 2015-16

Amount ($) Amount ($) Amount ($) Amount ($) Amount ($) Amount ($) Amount ($)

Income Statement

Income Statement

2016-17 2015-16

Revenue: Amount ($) Amount ($) Amount ($) Amount ($)

Sales 189,000.00 187,450.00

Consultancy fees received 59,250.67 57,000.00

Interest income 48.00 50.00

Total revenue 248,298.67 244,500.00

11AUDITING

Expenditures:

Cost of sales 69,500.00 63,595.00

Interest expenses 11,500.00 11,500.00

Depreciation 36,102.63 15,863.33

Bank charges 348.00 350.00

Printing 189.00 250.00

Repairs and Maintenance 1,080.00 5,050.00

Wages 48,000.00 53,000.00

Superannuation 2,670.00 4,770.00

Total Expenses 169,389.63 154,378.33

Net income 78,909.03 90,121.67

Balance Sheet

Balance Sheet:

Assets

2016-17 2015-16

Amount

($)

Amount

($)

Amount

($)

Amount

($)

Non-current assets

Machinery 71,000.00 65,000.00

Motor Vehicles 66,000.00 66,000.00

Furniture 7,400.00 7,400.00

144,400.00 138,400.00

Current Assets

Cash at Bank 72,292.67 80,000.00

Accounts receivable 165,590.00 111,000.00

Inventory 181,595.00 174,000.00

419,477.67 365,000.00

Total Assets 563,877.67 503,400.00

Liabilities and owners' equity

Non-current liabilities

Bank Loan 230,000.00 230,000.00 -

Expenditures:

Cost of sales 69,500.00 63,595.00

Interest expenses 11,500.00 11,500.00

Depreciation 36,102.63 15,863.33

Bank charges 348.00 350.00

Printing 189.00 250.00

Repairs and Maintenance 1,080.00 5,050.00

Wages 48,000.00 53,000.00

Superannuation 2,670.00 4,770.00

Total Expenses 169,389.63 154,378.33

Net income 78,909.03 90,121.67

Balance Sheet

Balance Sheet:

Assets

2016-17 2015-16

Amount

($)

Amount

($)

Amount

($)

Amount

($)

Non-current assets

Machinery 71,000.00 65,000.00

Motor Vehicles 66,000.00 66,000.00

Furniture 7,400.00 7,400.00

144,400.00 138,400.00

Current Assets

Cash at Bank 72,292.67 80,000.00

Accounts receivable 165,590.00 111,000.00

Inventory 181,595.00 174,000.00

419,477.67 365,000.00

Total Assets 563,877.67 503,400.00

Liabilities and owners' equity

Non-current liabilities

Bank Loan 230,000.00 230,000.00 -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.