AF 304 Semester 2 Auditing Assignment: Las Vegas Group Corporation

VerifiedAdded on 2022/10/01

|18

|2481

|99

Report

AI Summary

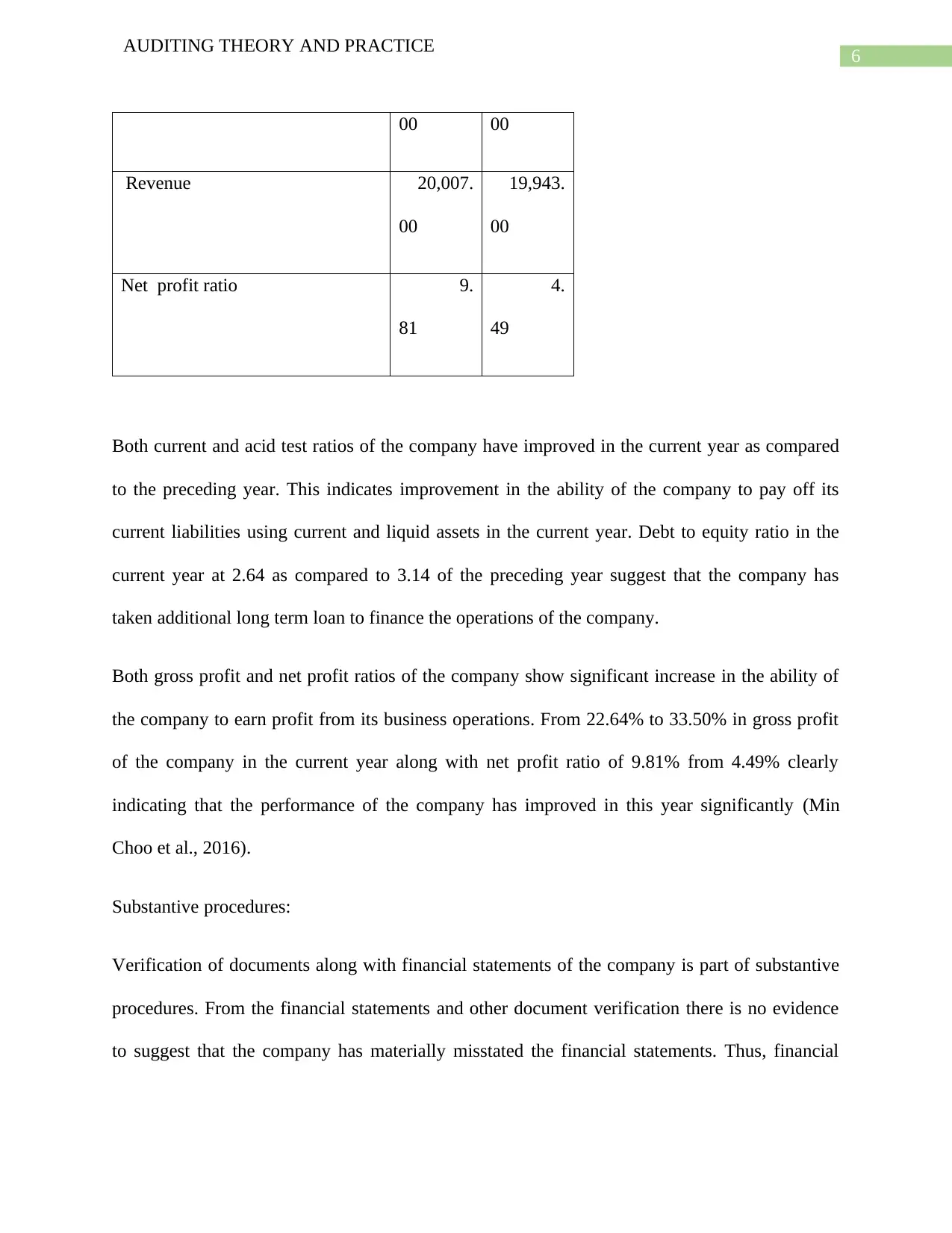

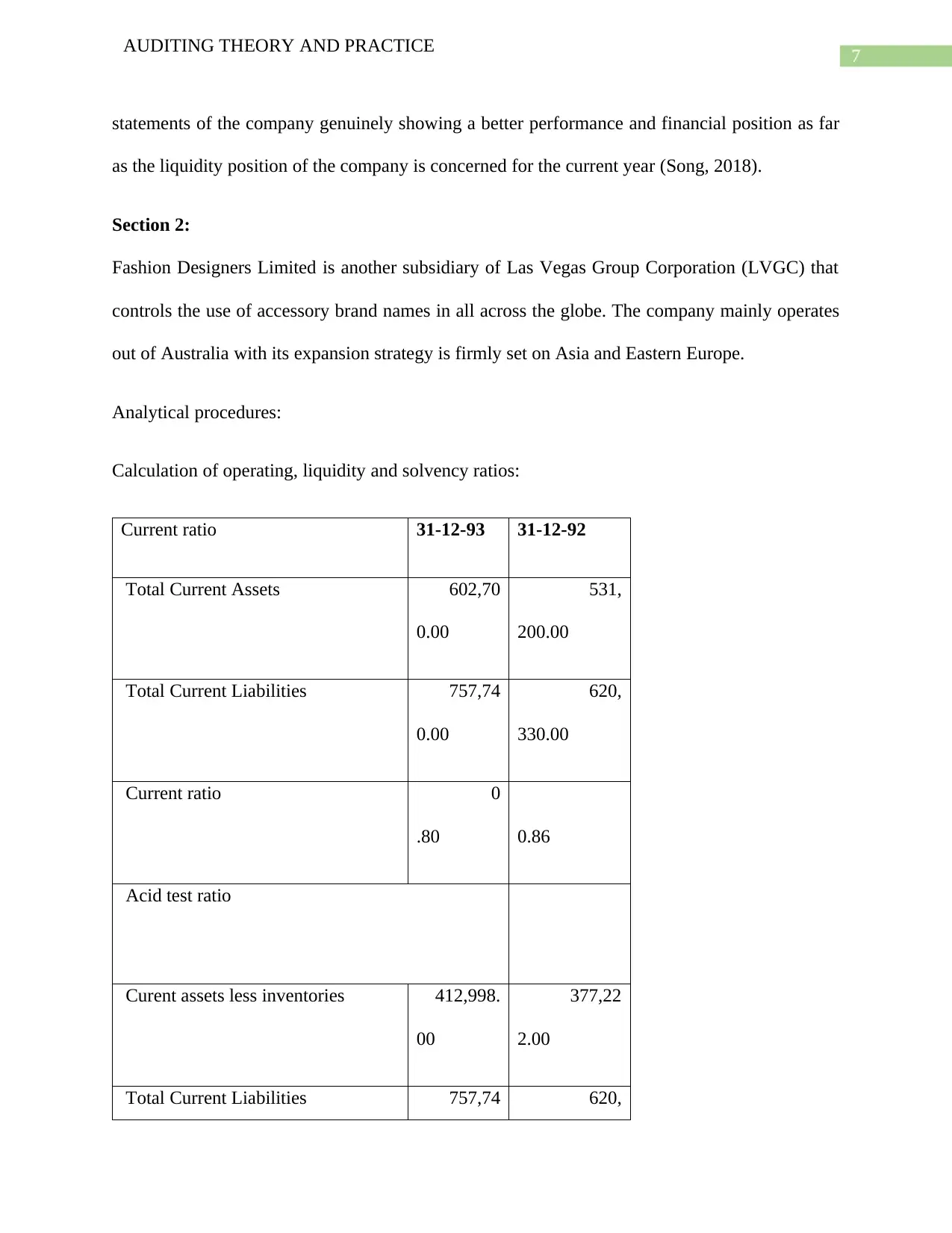

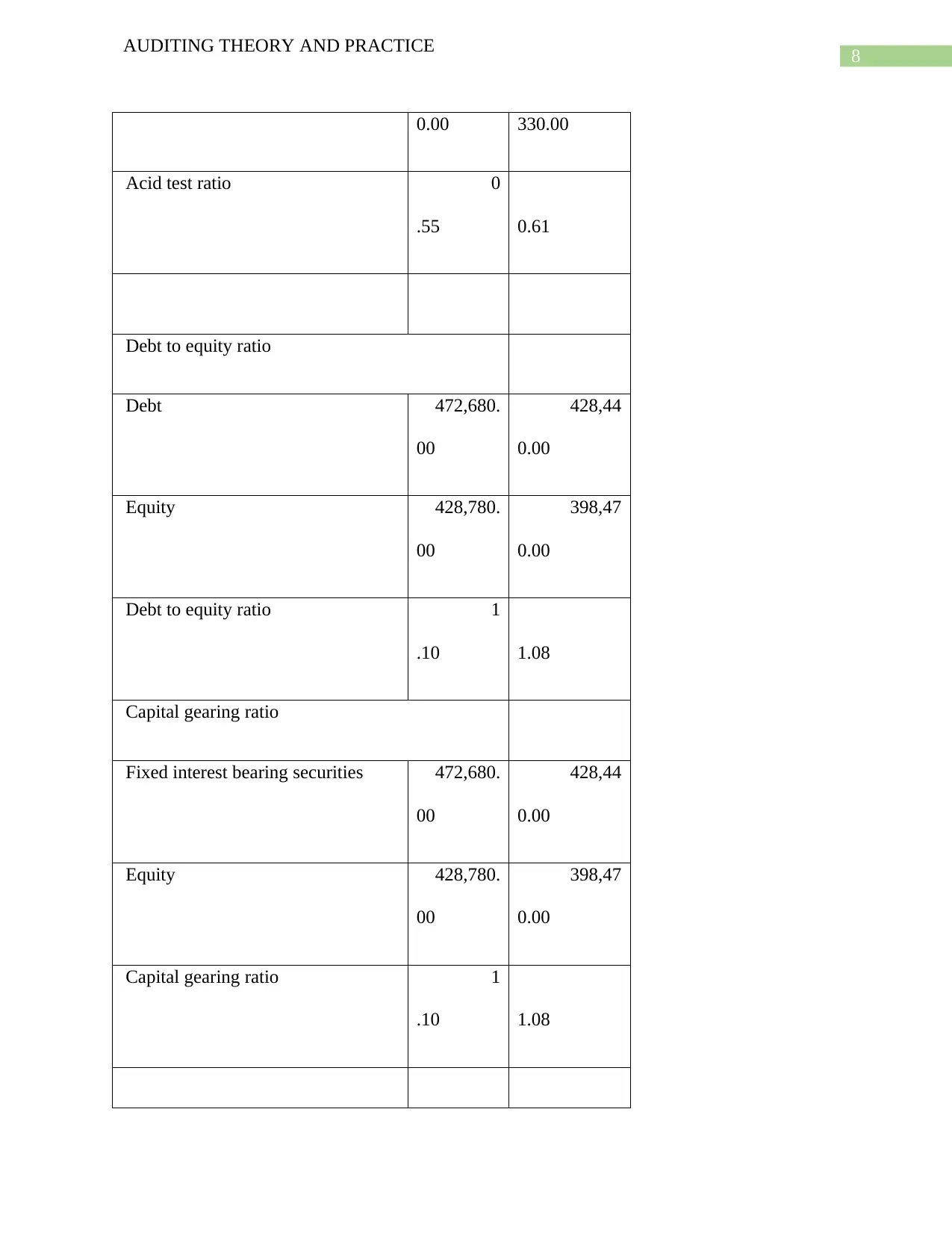

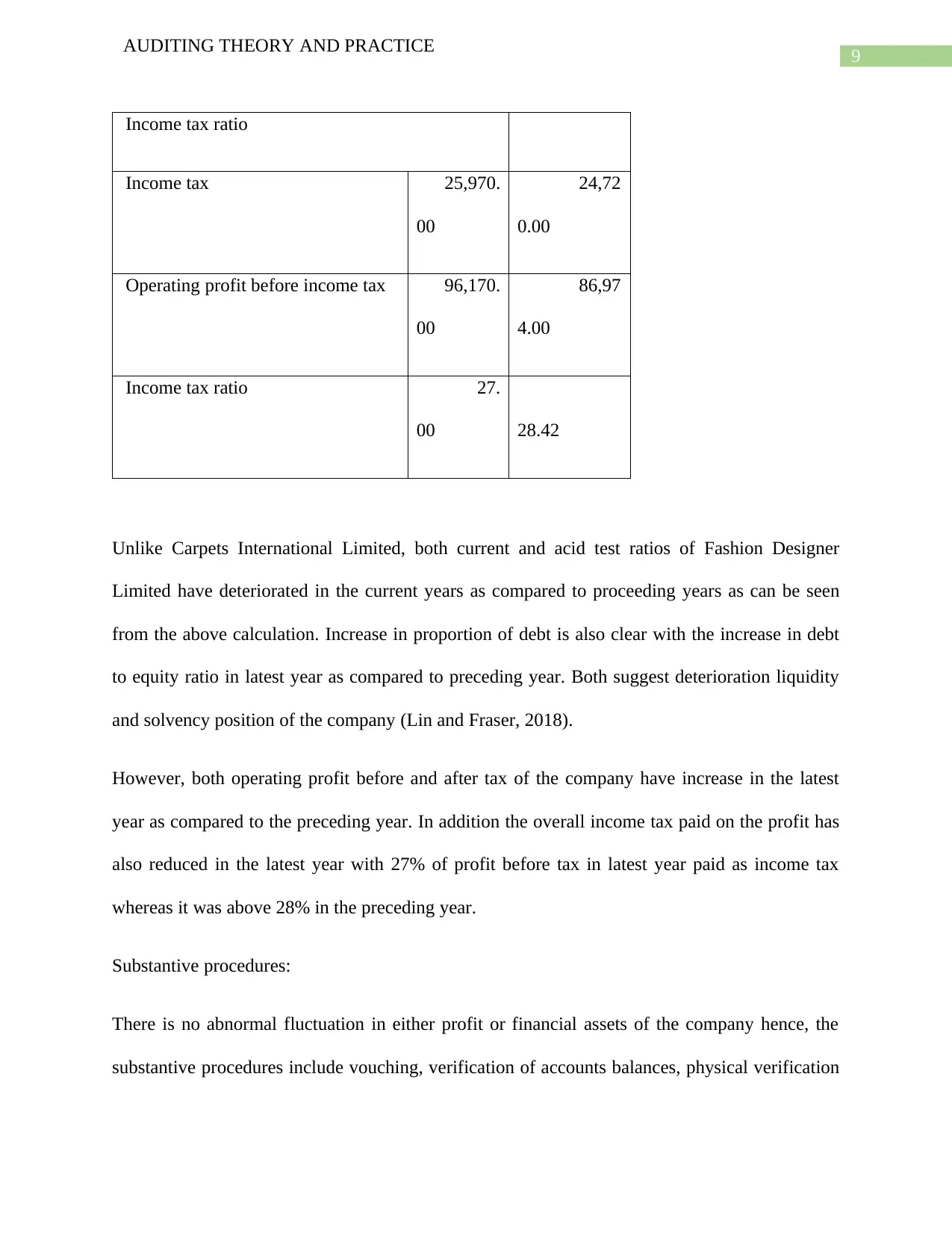

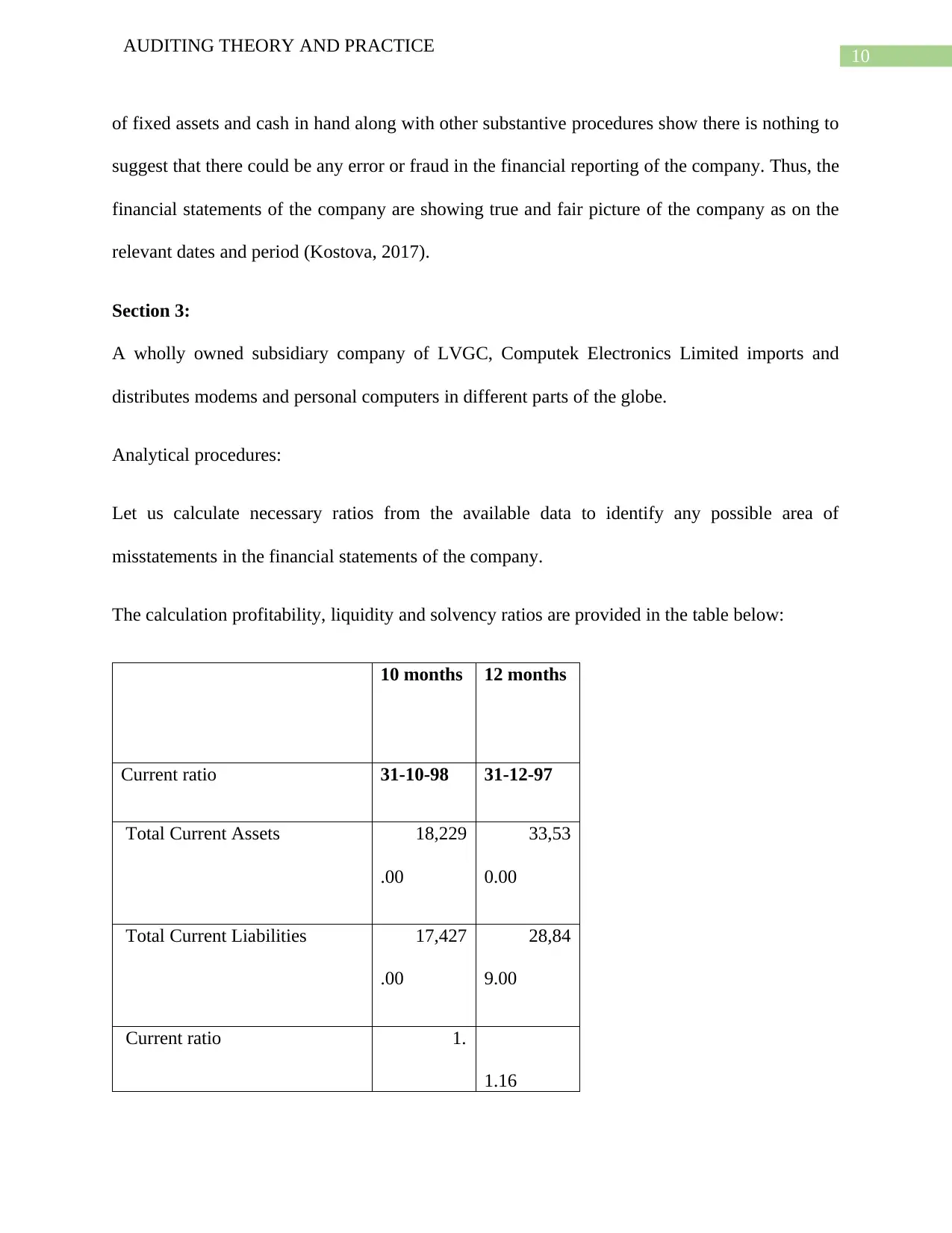

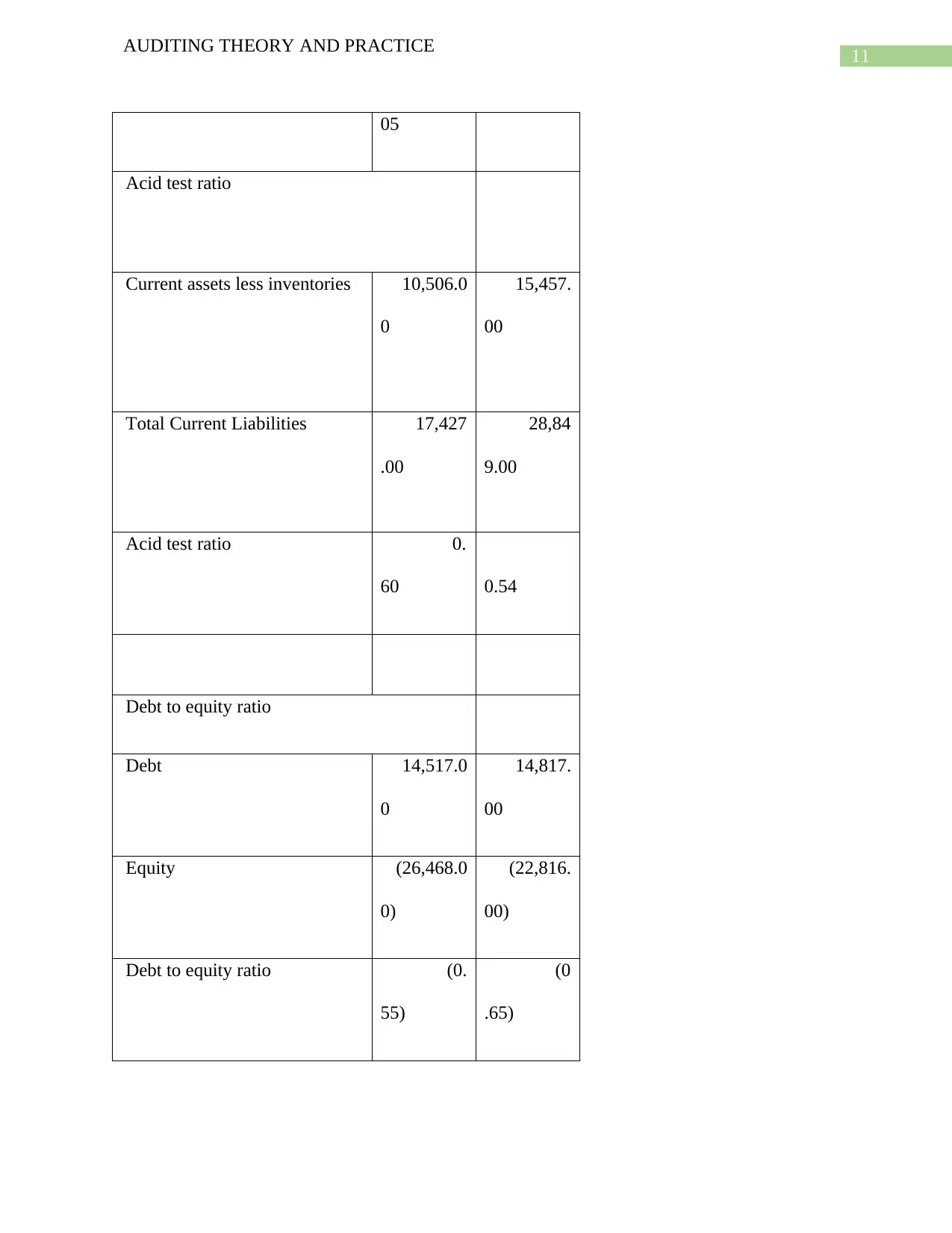

This report presents an analysis of audit reports for five subsidiary companies of the Las Vegas Group Corporation, a multinational corporation operating in various countries. The report begins with an introduction to audit reports and their importance in providing an independent opinion on financial statements. It then proceeds to analyze the audit reports of Carpet International Limited, Fashion Designers Limited, Computek Electronics Limited, Enron Electronics Limited, and General Machinery Company Limited. The analysis includes the application of analytical procedures such as ratio analysis (current ratio, acid test ratio, debt-to-equity ratio, and profitability ratios) to assess the financial performance and position of each subsidiary. Based on the findings from analytical procedures, the report evaluates the effectiveness of substantive procedures, including verification of documents and account balances. The report concludes by summarizing the key findings of the audit and emphasizing the limitations of an audit in providing absolute assurance. The report highlights the importance of considering the audit report and financial statements with this understanding.

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.