Audit Assurance and Compliance Report: DIPL Financial Analysis

VerifiedAdded on 2020/03/01

|9

|2489

|42

Report

AI Summary

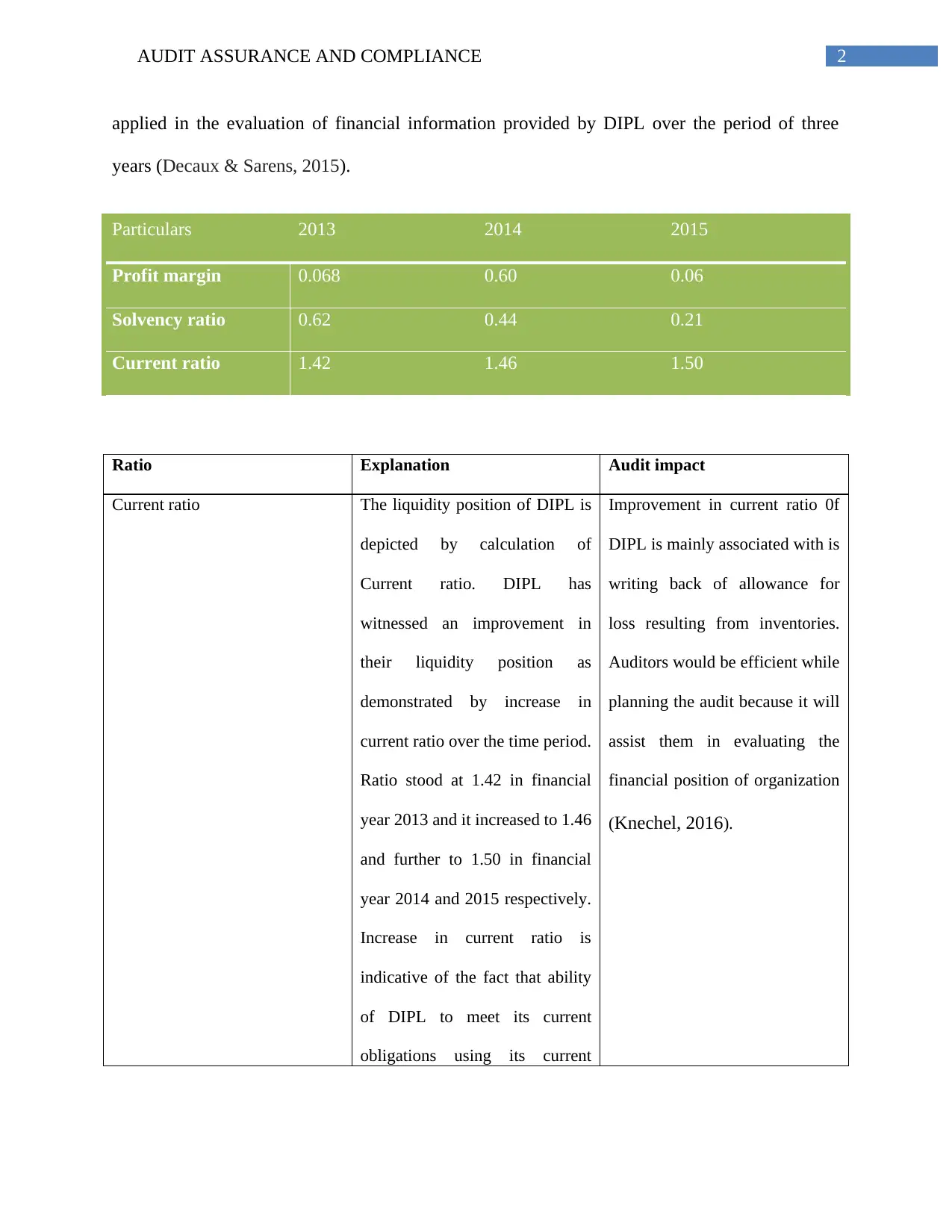

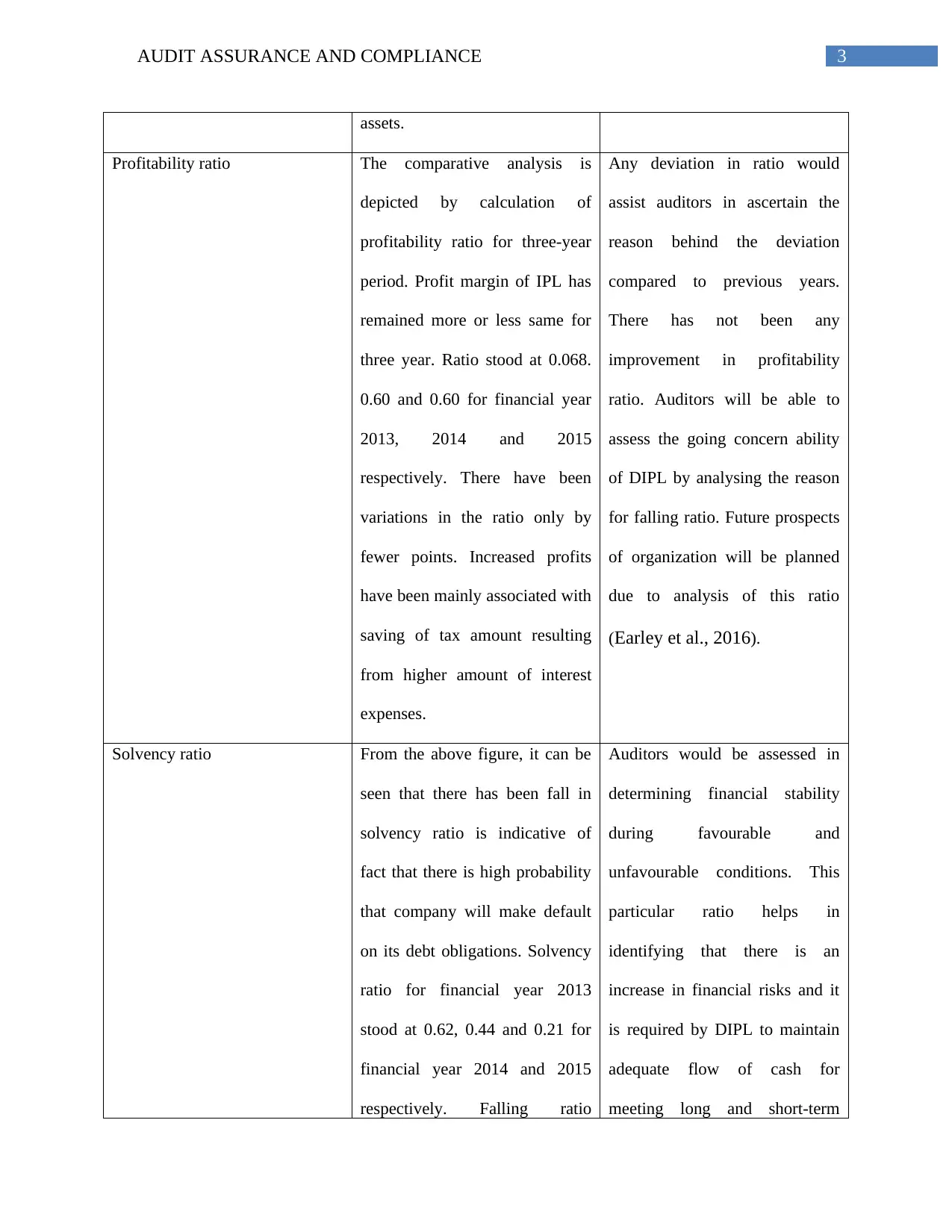

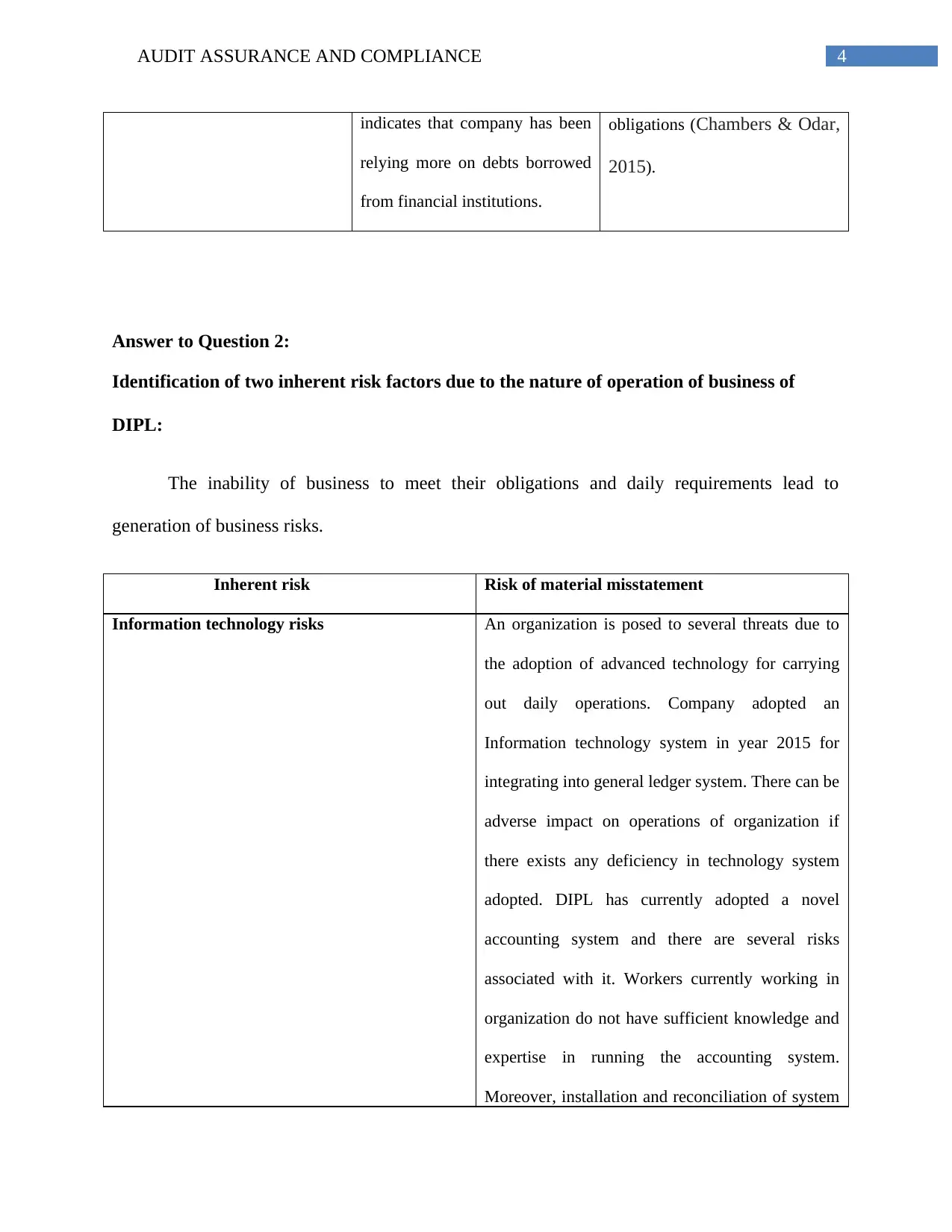

This report presents an analysis of audit assurance and compliance, focusing on a case study of DIPL. It begins by exploring analytical procedures, such as ratio analysis (current, solvency, and profitability ratios), to assess DIPL's financial performance over three years. The report then identifies inherent risk factors stemming from the nature of DIPL's business operations, including information technology and financial risks. Furthermore, it details two types of fraud risk factors related to material misstatements arising from fraudulent reporting, focusing on the nature of the control environment and debt covenants. The report concludes by examining the impact of these identified fraud risks on the conduct of the audit plan, emphasizing the importance of thorough verification and reconciliation processes to mitigate potential risks. This comprehensive analysis provides valuable insights into the complexities of audit assurance and compliance in a real-world business context.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.