Detailed Analysis of Auditing, Assurance and Compliance Report

VerifiedAdded on 2020/03/02

|10

|2485

|30

Report

AI Summary

This report presents an analysis of an auditing, assurance, and compliance case study, focusing on the financial performance of DIPL over three fiscal years. It examines the application of analytical procedures, including ratio analysis and benchmarking, to assess DIPL's financial position, highlighting declining profit margins and solvency ratios. The report identifies inherent risks, such as inexperienced staff and potential fraudulent financial reporting, and their impact on the company's operations. It explores specific risks, including those related to fraudulent activities and the use of an average costing method. The report concludes with recommendations for mitigating identified risks and improving financial reporting practices, emphasizing the need for enhanced monitoring systems and accurate cost accounting to ensure financial integrity and compliance.

Running head: AUDITING, ASSURANCE AND COMPLIANCE

Auditing, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING, ASSURANCE AND COMPLIANCE

1

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to Question 3a:..............................................................................................................5

Answer to Question 3b:..............................................................................................................6

Reference and Bibliography:......................................................................................................8

1

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question 2:................................................................................................................4

Answer to Question 3a:..............................................................................................................5

Answer to Question 3b:..............................................................................................................6

Reference and Bibliography:......................................................................................................8

AUDITING, ASSURANCE AND COMPLIANCE

2

Answer to Question 1:

The overall analytical process mainly allows the organisation to gather the required

information for commencing the overall audit plan, which could help in identifying the actual

financial position of an organisation. Furthermore, the overall problems that are faced by the

organisation could be identified with the help of relevant analytical procedures such as

benchmarking and ratios evaluation. Ashcraft et al., (2017) stated that with the help of

adequate audit plan relevant audit procedures could be identified adequately, which could

help in concentrating the overall cost of audit. Moreover, the evaluation of DIPL with the

help of adequate analytical procedures could mainly help in identifying the overall financial

condition of the company. Baylis et al., (2017) argued that the use of analytical approach is

mainly conducted on the overall financial reports provided by the company, which could lose

fiction if the reports are manipulated by the organisation. Moreover, there is an adequate

common size analysis approach, which allows the analyst to evaluate overall financial

declaration provided by the organisation.

There are many ways in which analyst are able to evaluate the performance of an

organisation, which could be used in pinpointing its overall financial condition and position.

The use of benchmarking and ratios could be identified as one of the adequate measures,

which might be used by the analyst to evaluate the performance of the organisation.

Furthermore, the overall problems with the help of benchmarking could be identified, where

the analyst are mainly able to pin point the problematic areas in an organization. The

benchmarking methods directly compare the company with its peers and evaluate the

performance based on relevant industry benchmark. The use of ratio also allows the analyst

to understand the overall financial position of an organisation and the relevant trend in which

it is moving. Caissie et al., (2016) mentioned that overall use of analytical procedures and

2

Answer to Question 1:

The overall analytical process mainly allows the organisation to gather the required

information for commencing the overall audit plan, which could help in identifying the actual

financial position of an organisation. Furthermore, the overall problems that are faced by the

organisation could be identified with the help of relevant analytical procedures such as

benchmarking and ratios evaluation. Ashcraft et al., (2017) stated that with the help of

adequate audit plan relevant audit procedures could be identified adequately, which could

help in concentrating the overall cost of audit. Moreover, the evaluation of DIPL with the

help of adequate analytical procedures could mainly help in identifying the overall financial

condition of the company. Baylis et al., (2017) argued that the use of analytical approach is

mainly conducted on the overall financial reports provided by the company, which could lose

fiction if the reports are manipulated by the organisation. Moreover, there is an adequate

common size analysis approach, which allows the analyst to evaluate overall financial

declaration provided by the organisation.

There are many ways in which analyst are able to evaluate the performance of an

organisation, which could be used in pinpointing its overall financial condition and position.

The use of benchmarking and ratios could be identified as one of the adequate measures,

which might be used by the analyst to evaluate the performance of the organisation.

Furthermore, the overall problems with the help of benchmarking could be identified, where

the analyst are mainly able to pin point the problematic areas in an organization. The

benchmarking methods directly compare the company with its peers and evaluate the

performance based on relevant industry benchmark. The use of ratio also allows the analyst

to understand the overall financial position of an organisation and the relevant trend in which

it is moving. Caissie et al., (2016) mentioned that overall use of analytical procedures and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING, ASSURANCE AND COMPLIANCE

3

evaluation allows the analyst to understand the financial condition of an organisation and

identified any manipulation or unethical behaviour in drafting the financial report.

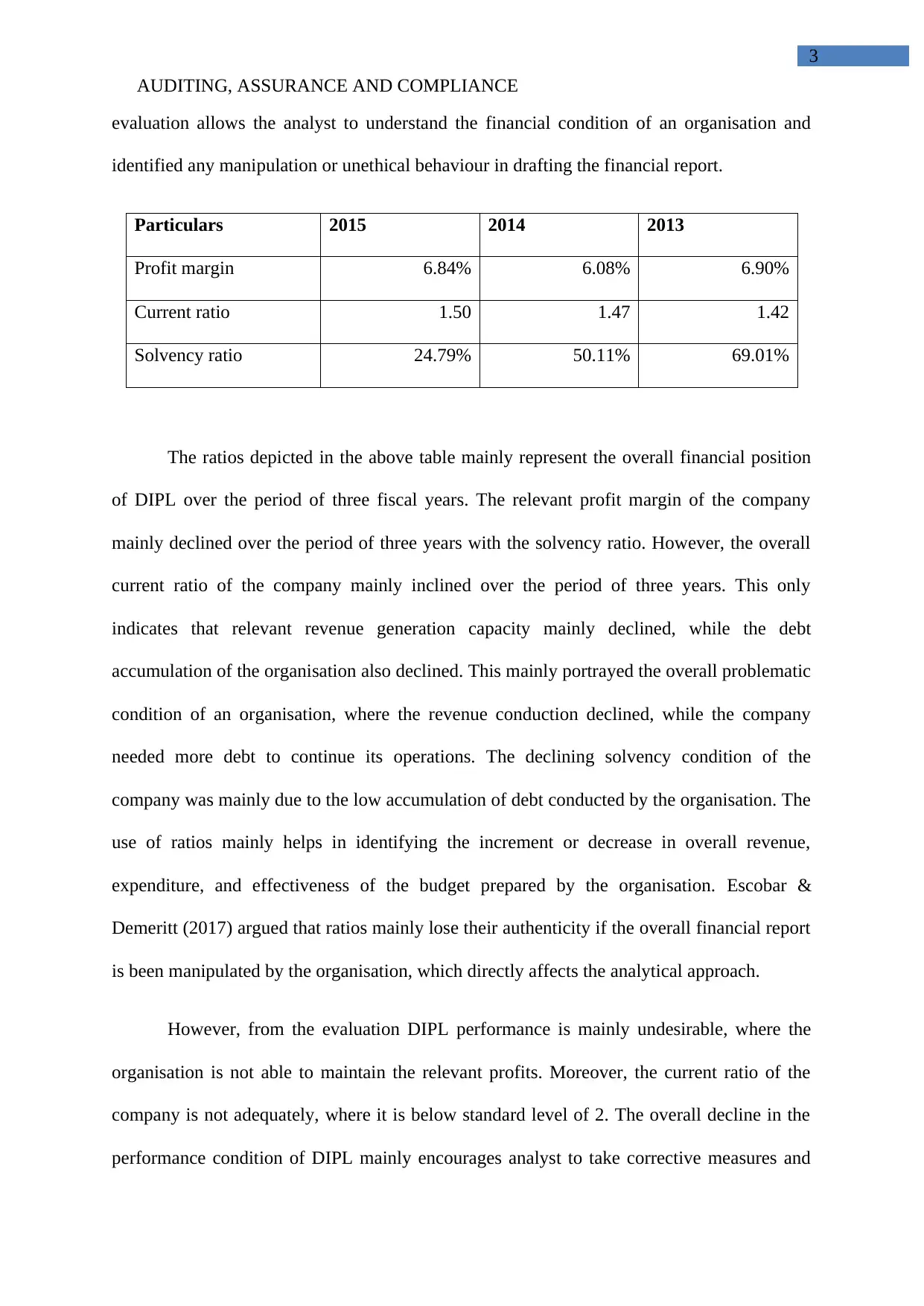

Particulars 2015 2014 2013

Profit margin 6.84% 6.08% 6.90%

Current ratio 1.50 1.47 1.42

Solvency ratio 24.79% 50.11% 69.01%

The ratios depicted in the above table mainly represent the overall financial position

of DIPL over the period of three fiscal years. The relevant profit margin of the company

mainly declined over the period of three years with the solvency ratio. However, the overall

current ratio of the company mainly inclined over the period of three years. This only

indicates that relevant revenue generation capacity mainly declined, while the debt

accumulation of the organisation also declined. This mainly portrayed the overall problematic

condition of an organisation, where the revenue conduction declined, while the company

needed more debt to continue its operations. The declining solvency condition of the

company was mainly due to the low accumulation of debt conducted by the organisation. The

use of ratios mainly helps in identifying the increment or decrease in overall revenue,

expenditure, and effectiveness of the budget prepared by the organisation. Escobar &

Demeritt (2017) argued that ratios mainly lose their authenticity if the overall financial report

is been manipulated by the organisation, which directly affects the analytical approach.

However, from the evaluation DIPL performance is mainly undesirable, where the

organisation is not able to maintain the relevant profits. Moreover, the current ratio of the

company is not adequately, where it is below standard level of 2. The overall decline in the

performance condition of DIPL mainly encourages analyst to take corrective measures and

3

evaluation allows the analyst to understand the financial condition of an organisation and

identified any manipulation or unethical behaviour in drafting the financial report.

Particulars 2015 2014 2013

Profit margin 6.84% 6.08% 6.90%

Current ratio 1.50 1.47 1.42

Solvency ratio 24.79% 50.11% 69.01%

The ratios depicted in the above table mainly represent the overall financial position

of DIPL over the period of three fiscal years. The relevant profit margin of the company

mainly declined over the period of three years with the solvency ratio. However, the overall

current ratio of the company mainly inclined over the period of three years. This only

indicates that relevant revenue generation capacity mainly declined, while the debt

accumulation of the organisation also declined. This mainly portrayed the overall problematic

condition of an organisation, where the revenue conduction declined, while the company

needed more debt to continue its operations. The declining solvency condition of the

company was mainly due to the low accumulation of debt conducted by the organisation. The

use of ratios mainly helps in identifying the increment or decrease in overall revenue,

expenditure, and effectiveness of the budget prepared by the organisation. Escobar &

Demeritt (2017) argued that ratios mainly lose their authenticity if the overall financial report

is been manipulated by the organisation, which directly affects the analytical approach.

However, from the evaluation DIPL performance is mainly undesirable, where the

organisation is not able to maintain the relevant profits. Moreover, the current ratio of the

company is not adequately, where it is below standard level of 2. The overall decline in the

performance condition of DIPL mainly encourages analyst to take corrective measures and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING, ASSURANCE AND COMPLIANCE

4

identify actual performance of the organisation. Therefore, the evaluation of the above

method could mainly help in identifying the problems faced by the organisation, where

adequate analytical measures need to be conducted (Hut-Mossel, Welker, Ahaus & Gans,

2017).

Answer to Question 2:

Relevant problems could be identified from the evaluation of the case study of DIPL,

which mainly consist of the inheritance risk affecting operations of the company. The overall

case study also states that the management did not adequately record the various business

transactions in its financial report. Furthermore, the overall inefficiency and ineffectiveness

of the overall management mainly declined ability of the DIPL to perform adequately in the

fiscal year. The declining revenue and net profit of the organisation mainly depicts the

inheriting risk affecting operations of the business (Ismanto & Hassan, 2017).

From the overall evaluation, it is also understood that the staff working in DIPL has

relevant inexperience and are inefficient in completing the relevant tasks. Furthermore, there

is relevant unprofessionalism present in the current operations of DIPL, which directly

increases the overall inheritance risk of the organisation. Moreover, the inheritance risk could

be portrayed in the overall selection of the CEO, which was conducted by the organisation.

James (2016) argued that inheritance risk involved in workforce of the organisation could

increase the overall material misstatement conducted in an organisation. Moreover, DIPL

does not have adequate workforce to support its operational capability, which is directly

increasing the overall inherent risk of DIPL.

Therefore, it could be understood the there is huge pressure on the employees of

DIPL, which is directly increasing the overall work pressure on its workforce. This pressure

on the workforce mainly increases the manipulation in financial statements, which is

4

identify actual performance of the organisation. Therefore, the evaluation of the above

method could mainly help in identifying the problems faced by the organisation, where

adequate analytical measures need to be conducted (Hut-Mossel, Welker, Ahaus & Gans,

2017).

Answer to Question 2:

Relevant problems could be identified from the evaluation of the case study of DIPL,

which mainly consist of the inheritance risk affecting operations of the company. The overall

case study also states that the management did not adequately record the various business

transactions in its financial report. Furthermore, the overall inefficiency and ineffectiveness

of the overall management mainly declined ability of the DIPL to perform adequately in the

fiscal year. The declining revenue and net profit of the organisation mainly depicts the

inheriting risk affecting operations of the business (Ismanto & Hassan, 2017).

From the overall evaluation, it is also understood that the staff working in DIPL has

relevant inexperience and are inefficient in completing the relevant tasks. Furthermore, there

is relevant unprofessionalism present in the current operations of DIPL, which directly

increases the overall inheritance risk of the organisation. Moreover, the inheritance risk could

be portrayed in the overall selection of the CEO, which was conducted by the organisation.

James (2016) argued that inheritance risk involved in workforce of the organisation could

increase the overall material misstatement conducted in an organisation. Moreover, DIPL

does not have adequate workforce to support its operational capability, which is directly

increasing the overall inherent risk of DIPL.

Therefore, it could be understood the there is huge pressure on the employees of

DIPL, which is directly increasing the overall work pressure on its workforce. This pressure

on the workforce mainly increases the manipulation in financial statements, which is

AUDITING, ASSURANCE AND COMPLIANCE

5

conducted by the employees. The management of DIPL is mainly not responsible for the lack

of effective interpretation, which is not been conducted. The management is also lacking

accountability and integrity, which is directly affecting the reputation of the organisation in

the business world. Moreover, the material misstatement present in the current activities of

the management and employee is directly affecting the overall financial reporting of DIPL.

Therefore, it could be stated that the company mainly needs adequate audit evaluation for

identifying the relevant impact of the inheritance risk on financial report of DIPL (Nalewaik

& Mills, 2016).

Answer to Question 3a:

Identified risk Impact of the risk on operations of the organisation

Risk from

fraudulent

financial

reporting

process

The evaluation of case study of DIPL mainly depicted relevant fraudulent

activities, which was been conducted by employees of the organisation.

Employee mainly conducted these fraudulent activities, as the management

forced them to use the new accounting system. This adoption of the new

accounting system mainly put immense pressure on the overall activities of

the employees, which led to the augmentation of the fraudulent activities.

Therefore, the staff could use the manipulations and fraudulent activities in

coping with then reconciliation process. Thus, the increment in overall

manipulation conducted by employees could directly increase the material

misstatement in the annual report of the organisation. The evaluation also

stated that adequate loss of financial information was mainly presented in

the annual report, which directly increases the overall material

misstatement of DIPL (Oliveri et al., 2016).

Moreover, there is chance of inherent risk, as the overall organisation

5

conducted by the employees. The management of DIPL is mainly not responsible for the lack

of effective interpretation, which is not been conducted. The management is also lacking

accountability and integrity, which is directly affecting the reputation of the organisation in

the business world. Moreover, the material misstatement present in the current activities of

the management and employee is directly affecting the overall financial reporting of DIPL.

Therefore, it could be stated that the company mainly needs adequate audit evaluation for

identifying the relevant impact of the inheritance risk on financial report of DIPL (Nalewaik

& Mills, 2016).

Answer to Question 3a:

Identified risk Impact of the risk on operations of the organisation

Risk from

fraudulent

financial

reporting

process

The evaluation of case study of DIPL mainly depicted relevant fraudulent

activities, which was been conducted by employees of the organisation.

Employee mainly conducted these fraudulent activities, as the management

forced them to use the new accounting system. This adoption of the new

accounting system mainly put immense pressure on the overall activities of

the employees, which led to the augmentation of the fraudulent activities.

Therefore, the staff could use the manipulations and fraudulent activities in

coping with then reconciliation process. Thus, the increment in overall

manipulation conducted by employees could directly increase the material

misstatement in the annual report of the organisation. The evaluation also

stated that adequate loss of financial information was mainly presented in

the annual report, which directly increases the overall material

misstatement of DIPL (Oliveri et al., 2016).

Moreover, there is chance of inherent risk, as the overall organisation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING, ASSURANCE AND COMPLIANCE

6

mainly deals with a workforce, which is inexperience and inefficient.

Therefore, the overall activities that is conducted by the employees could

directly increase the misstatement conducted in financial report of DIPL.

Furthermore, the succession process of the CEO is also in question, where

the accountability and integrity of the overall management is questioned

(Robbins & Meyer, 2016).

Risk from the

fraudulent

activities

conducted by

employees

The second risk is mainly portrayed from the fraudulent activities

conducted in preparing the annual report of DIPL. The company mainly

needs to have a specified current and debt ratio in its financial books to

acquire the loan of 7.5 million from BDO finance. Therefore, the company

could conduct fraudulent activities in its financial, report to acquire the

relevant loans to support its activities. Moreover, the company mainly

needs to keep the overall current ratio at the levels of 1.5, while the debt-to-

equity ratio needs to be below 1, which is conveniently been maintained in

the financial report of 2015. This mainly portrays the overall fraudulent

activities, which could be conducted by the management to comply with

the loan requirements. This could increase the material misstatement

conducted in the financial report of DIPL (Sandberg et al, 2016).

Answer to Question 3b:

From the evaluation, relevant fraudulent activities that are present in operations of

DIPL could be identified. The company can implement new system for monitoring the

activities of the organisation, which could directly help in reducing the fraudulent activities,

which is been conducted by the employees. Moreover, there are also relevant problems with

6

mainly deals with a workforce, which is inexperience and inefficient.

Therefore, the overall activities that is conducted by the employees could

directly increase the misstatement conducted in financial report of DIPL.

Furthermore, the succession process of the CEO is also in question, where

the accountability and integrity of the overall management is questioned

(Robbins & Meyer, 2016).

Risk from the

fraudulent

activities

conducted by

employees

The second risk is mainly portrayed from the fraudulent activities

conducted in preparing the annual report of DIPL. The company mainly

needs to have a specified current and debt ratio in its financial books to

acquire the loan of 7.5 million from BDO finance. Therefore, the company

could conduct fraudulent activities in its financial, report to acquire the

relevant loans to support its activities. Moreover, the company mainly

needs to keep the overall current ratio at the levels of 1.5, while the debt-to-

equity ratio needs to be below 1, which is conveniently been maintained in

the financial report of 2015. This mainly portrays the overall fraudulent

activities, which could be conducted by the management to comply with

the loan requirements. This could increase the material misstatement

conducted in the financial report of DIPL (Sandberg et al, 2016).

Answer to Question 3b:

From the evaluation, relevant fraudulent activities that are present in operations of

DIPL could be identified. The company can implement new system for monitoring the

activities of the organisation, which could directly help in reducing the fraudulent activities,

which is been conducted by the employees. Moreover, there are also relevant problems with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDITING, ASSURANCE AND COMPLIANCE

7

the calculation of raw materials, where the organisation mainly uses the average costing

method in its books. This average costing method is relevantly lower that the actual costs

incurred by the organisation in purchasing the product. This method mainly reduces the

capability of the organisation to determine the actual cost incurred from its operations.

Moreover, the financial reporting process of the organisation also portrays different types of

risk, which could be evaluated by the auditors during the audit procedure. Thus, the identified

risk of the organisation could directly affect its overall financial capability and reduce its

required profitability (Schmidt, Wood & Grabski, 2016).

7

the calculation of raw materials, where the organisation mainly uses the average costing

method in its books. This average costing method is relevantly lower that the actual costs

incurred by the organisation in purchasing the product. This method mainly reduces the

capability of the organisation to determine the actual cost incurred from its operations.

Moreover, the financial reporting process of the organisation also portrays different types of

risk, which could be evaluated by the auditors during the audit procedure. Thus, the identified

risk of the organisation could directly affect its overall financial capability and reduce its

required profitability (Schmidt, Wood & Grabski, 2016).

AUDITING, ASSURANCE AND COMPLIANCE

8

Reference and Bibliography:

Ashcraft, M., Arous, E. J., Judelson, D. R., Simons, J. P., Kush, D., Arous, E. J., ... &

Schanzer, A. (2017). IP245 Implementation of a Standardized Audit-Feedback-

Education Quality Assurance Cycle Improves Venous Duplex Ultrasound Protocol

Compliance in a Vascular Laboratory. Journal of Vascular Surgery, 65(6), 120S-

121S.

Baylis, R. M., Burnap, P., Clatworthy, M. A., Gad, M. A., & Pong, C. K. (2017). Private

lenders’ demand for audit. Journal of Accounting and Economics.

Caissie, A., Brown, E., Bissonnette, J. P., Tyldesley, S., Brundage, M., & Milosevic, M.

(2016). 176: Measuring Uptake of the Canadian Partnership for Quality Radiotherapy

(CPQR) Programmatic Key Quality Indicators (KQI): A Pan-Canadian Audit of

Compliance. Radiotherapy and Oncology, 120, S65.

Escobar, M. P., & Demeritt, D. (2017). Paperwork and the decoupling of audit and animal

welfare: The challenges of materiality for better regulation. Environment and

Planning C: Politics and Space, 35(1), 169-190.

Hut-Mossel, L., Welker, G., Ahaus, K., & Gans, R. (2017). Understanding how and why

audits work: protocol for a realist review of audit programmes to improve hospital

care. BMJ open, 7(6), e015121.

Ismanto, S., & Hassan, C. H. (2017). A Clinical Audit for Compliance on the Innovated

Radiographic Technique at a Radiologic Unit. ASEAN Journal on Science and

Technolgy for Development, 33(1), 1-9.

8

Reference and Bibliography:

Ashcraft, M., Arous, E. J., Judelson, D. R., Simons, J. P., Kush, D., Arous, E. J., ... &

Schanzer, A. (2017). IP245 Implementation of a Standardized Audit-Feedback-

Education Quality Assurance Cycle Improves Venous Duplex Ultrasound Protocol

Compliance in a Vascular Laboratory. Journal of Vascular Surgery, 65(6), 120S-

121S.

Baylis, R. M., Burnap, P., Clatworthy, M. A., Gad, M. A., & Pong, C. K. (2017). Private

lenders’ demand for audit. Journal of Accounting and Economics.

Caissie, A., Brown, E., Bissonnette, J. P., Tyldesley, S., Brundage, M., & Milosevic, M.

(2016). 176: Measuring Uptake of the Canadian Partnership for Quality Radiotherapy

(CPQR) Programmatic Key Quality Indicators (KQI): A Pan-Canadian Audit of

Compliance. Radiotherapy and Oncology, 120, S65.

Escobar, M. P., & Demeritt, D. (2017). Paperwork and the decoupling of audit and animal

welfare: The challenges of materiality for better regulation. Environment and

Planning C: Politics and Space, 35(1), 169-190.

Hut-Mossel, L., Welker, G., Ahaus, K., & Gans, R. (2017). Understanding how and why

audits work: protocol for a realist review of audit programmes to improve hospital

care. BMJ open, 7(6), e015121.

Ismanto, S., & Hassan, C. H. (2017). A Clinical Audit for Compliance on the Innovated

Radiographic Technique at a Radiologic Unit. ASEAN Journal on Science and

Technolgy for Development, 33(1), 1-9.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDITING, ASSURANCE AND COMPLIANCE

9

JAMES, K. (2016). POLK STATE OFFICE BUILDING NASHVILLE, TENNESSEE

37243-1402 PHONE (615) 401-7841 Independent Auditor's Report for Federal

Awards (Uniform Guidance). Those standards and the Uniform Guidance require that

we plan and perform the audit to obtain reasonable assurance about whether

noncompliance with the types of compliance requirements referred to above that

could have a direct and material effect on a major federal program occurred. An audit

includes examining, on a test basis, evidence about Cheatham .... Opinion on Each

Major Federal Program.

Nalewaik, A., & Mills, A. (2016). Project Performance Review: Capturing the Value of

Audit, Oversight, and Compliance for Project Success. CRC Press.

Oliveri, A., Howarth, N., Gevenois, P. A., & Tack, D. (2016). Short-and long-term effects of

clinical audits on compliance with procedures in CT scanning. European

radiology, 26(8), 2663-2668.

Robbins, M., & Meyer, M. (2016). Auditing the National HR Standards: governance: HR

standards. HR Future, 2(Feb 2016), 25-27.

Sandberg, M., Dahl, J., Lindegaard, L. L., & Pedersen, J. R. (2016). Compliance/non-

compliance with biosecurity rules specified in the Danish Quality Assurance system

(KIK) and Campylobacter-positive broiler flocks 2012 and 2013. Poultry

science, 96(1), 184-191.

Schmidt, P. J., Wood, J. T., & Grabski, S. V. (2016). Business in the Cloud: Research

Questions on Governance, Audit, and Assurance. Journal of Information

Systems, 30(3), 173-189.

9

JAMES, K. (2016). POLK STATE OFFICE BUILDING NASHVILLE, TENNESSEE

37243-1402 PHONE (615) 401-7841 Independent Auditor's Report for Federal

Awards (Uniform Guidance). Those standards and the Uniform Guidance require that

we plan and perform the audit to obtain reasonable assurance about whether

noncompliance with the types of compliance requirements referred to above that

could have a direct and material effect on a major federal program occurred. An audit

includes examining, on a test basis, evidence about Cheatham .... Opinion on Each

Major Federal Program.

Nalewaik, A., & Mills, A. (2016). Project Performance Review: Capturing the Value of

Audit, Oversight, and Compliance for Project Success. CRC Press.

Oliveri, A., Howarth, N., Gevenois, P. A., & Tack, D. (2016). Short-and long-term effects of

clinical audits on compliance with procedures in CT scanning. European

radiology, 26(8), 2663-2668.

Robbins, M., & Meyer, M. (2016). Auditing the National HR Standards: governance: HR

standards. HR Future, 2(Feb 2016), 25-27.

Sandberg, M., Dahl, J., Lindegaard, L. L., & Pedersen, J. R. (2016). Compliance/non-

compliance with biosecurity rules specified in the Danish Quality Assurance system

(KIK) and Campylobacter-positive broiler flocks 2012 and 2013. Poultry

science, 96(1), 184-191.

Schmidt, P. J., Wood, J. T., & Grabski, S. V. (2016). Business in the Cloud: Research

Questions on Governance, Audit, and Assurance. Journal of Information

Systems, 30(3), 173-189.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.