Audit Assignment Report: Financial Statement Analysis and Audit

VerifiedAdded on 2020/03/02

|11

|2377

|41

Report

AI Summary

This audit assignment report analyzes the financial statements of Double Ink Printers Limited, focusing on analytical procedures, risk assessment, and fraud risk factors. The report begins with an overview of analytical procedures, including preliminary and substantive analytical procedures, and their impact on audit plans. It examines financial ratios such as gross profit, net profit, return on assets, return on equity, debt-equity ratio, and various turnover ratios, highlighting significant changes and their implications for audit procedures. The report then delves into risk assessment procedures, identifying inherent risks related to inventory valuation methods and the implementation of a new IT system. Finally, the report addresses fraud risk factors, including changes in inventory valuation and a loan condition tied to the current ratio, and their impact on audit procedures. The analysis provides a detailed examination of financial data and potential risks, offering valuable insights for audit planning and execution.

Audit assignment

August 23, 2017

Audit assignment

1

August 23, 2017

Audit assignment

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................7

Question 3........................................................................................................................................9

References......................................................................................................................................11

2

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................7

Question 3........................................................................................................................................9

References......................................................................................................................................11

2

Audit assignment

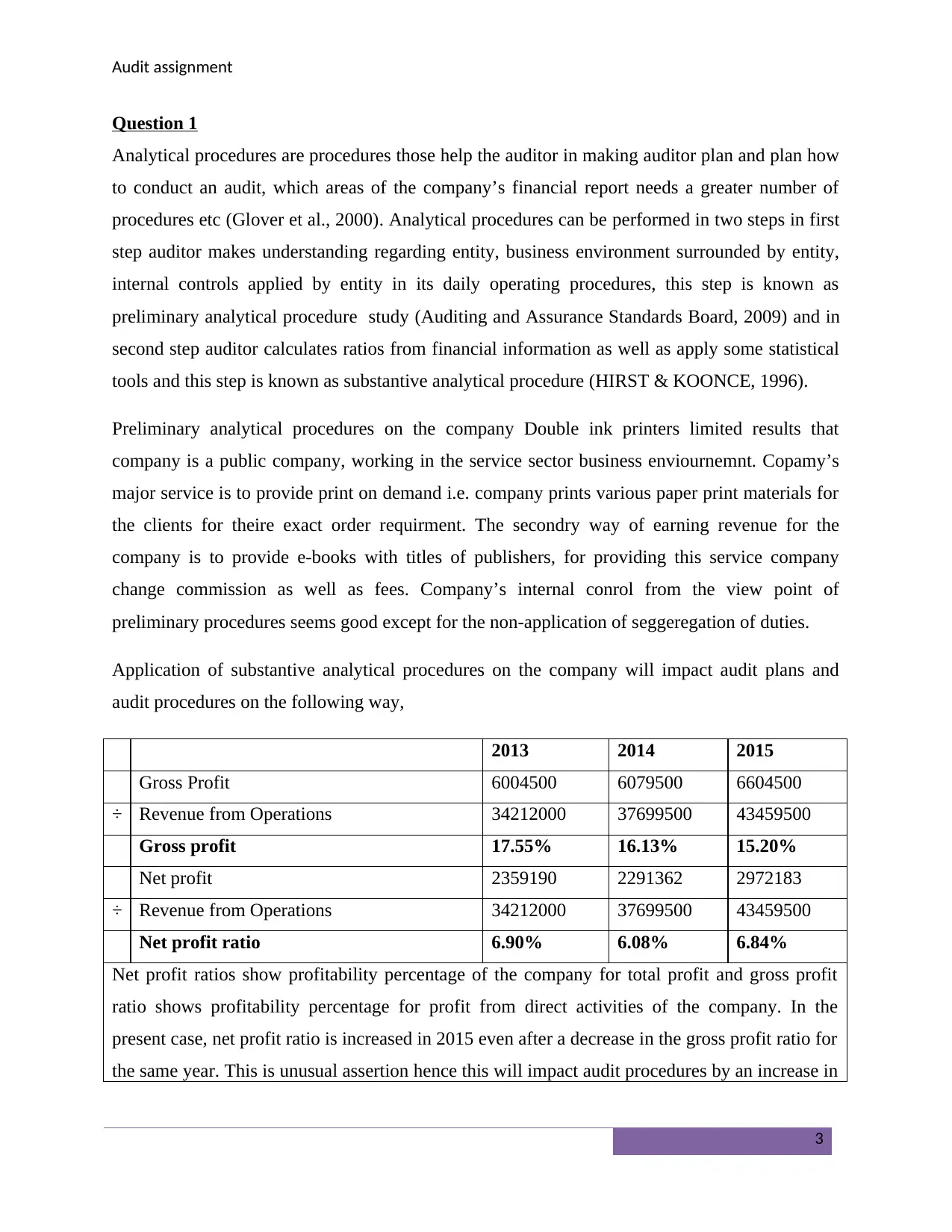

Question 1

Analytical procedures are procedures those help the auditor in making auditor plan and plan how

to conduct an audit, which areas of the company’s financial report needs a greater number of

procedures etc (Glover et al., 2000). Analytical procedures can be performed in two steps in first

step auditor makes understanding regarding entity, business environment surrounded by entity,

internal controls applied by entity in its daily operating procedures, this step is known as

preliminary analytical procedure study (Auditing and Assurance Standards Board, 2009) and in

second step auditor calculates ratios from financial information as well as apply some statistical

tools and this step is known as substantive analytical procedure (HIRST & KOONCE, 1996).

Preliminary analytical procedures on the company Double ink printers limited results that

company is a public company, working in the service sector business enviournemnt. Copamy’s

major service is to provide print on demand i.e. company prints various paper print materials for

the clients for theire exact order requirment. The secondry way of earning revenue for the

company is to provide e-books with titles of publishers, for providing this service company

change commission as well as fees. Company’s internal conrol from the view point of

preliminary procedures seems good except for the non-application of seggeregation of duties.

Application of substantive analytical procedures on the company will impact audit plans and

audit procedures on the following way,

2013 2014 2015

Gross Profit 6004500 6079500 6604500

÷ Revenue from Operations 34212000 37699500 43459500

Gross profit 17.55% 16.13% 15.20%

Net profit 2359190 2291362 2972183

÷ Revenue from Operations 34212000 37699500 43459500

Net profit ratio 6.90% 6.08% 6.84%

Net profit ratios show profitability percentage of the company for total profit and gross profit

ratio shows profitability percentage for profit from direct activities of the company. In the

present case, net profit ratio is increased in 2015 even after a decrease in the gross profit ratio for

the same year. This is unusual assertion hence this will impact audit procedures by an increase in

3

Question 1

Analytical procedures are procedures those help the auditor in making auditor plan and plan how

to conduct an audit, which areas of the company’s financial report needs a greater number of

procedures etc (Glover et al., 2000). Analytical procedures can be performed in two steps in first

step auditor makes understanding regarding entity, business environment surrounded by entity,

internal controls applied by entity in its daily operating procedures, this step is known as

preliminary analytical procedure study (Auditing and Assurance Standards Board, 2009) and in

second step auditor calculates ratios from financial information as well as apply some statistical

tools and this step is known as substantive analytical procedure (HIRST & KOONCE, 1996).

Preliminary analytical procedures on the company Double ink printers limited results that

company is a public company, working in the service sector business enviournemnt. Copamy’s

major service is to provide print on demand i.e. company prints various paper print materials for

the clients for theire exact order requirment. The secondry way of earning revenue for the

company is to provide e-books with titles of publishers, for providing this service company

change commission as well as fees. Company’s internal conrol from the view point of

preliminary procedures seems good except for the non-application of seggeregation of duties.

Application of substantive analytical procedures on the company will impact audit plans and

audit procedures on the following way,

2013 2014 2015

Gross Profit 6004500 6079500 6604500

÷ Revenue from Operations 34212000 37699500 43459500

Gross profit 17.55% 16.13% 15.20%

Net profit 2359190 2291362 2972183

÷ Revenue from Operations 34212000 37699500 43459500

Net profit ratio 6.90% 6.08% 6.84%

Net profit ratios show profitability percentage of the company for total profit and gross profit

ratio shows profitability percentage for profit from direct activities of the company. In the

present case, net profit ratio is increased in 2015 even after a decrease in the gross profit ratio for

the same year. This is unusual assertion hence this will impact audit procedures by an increase in

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

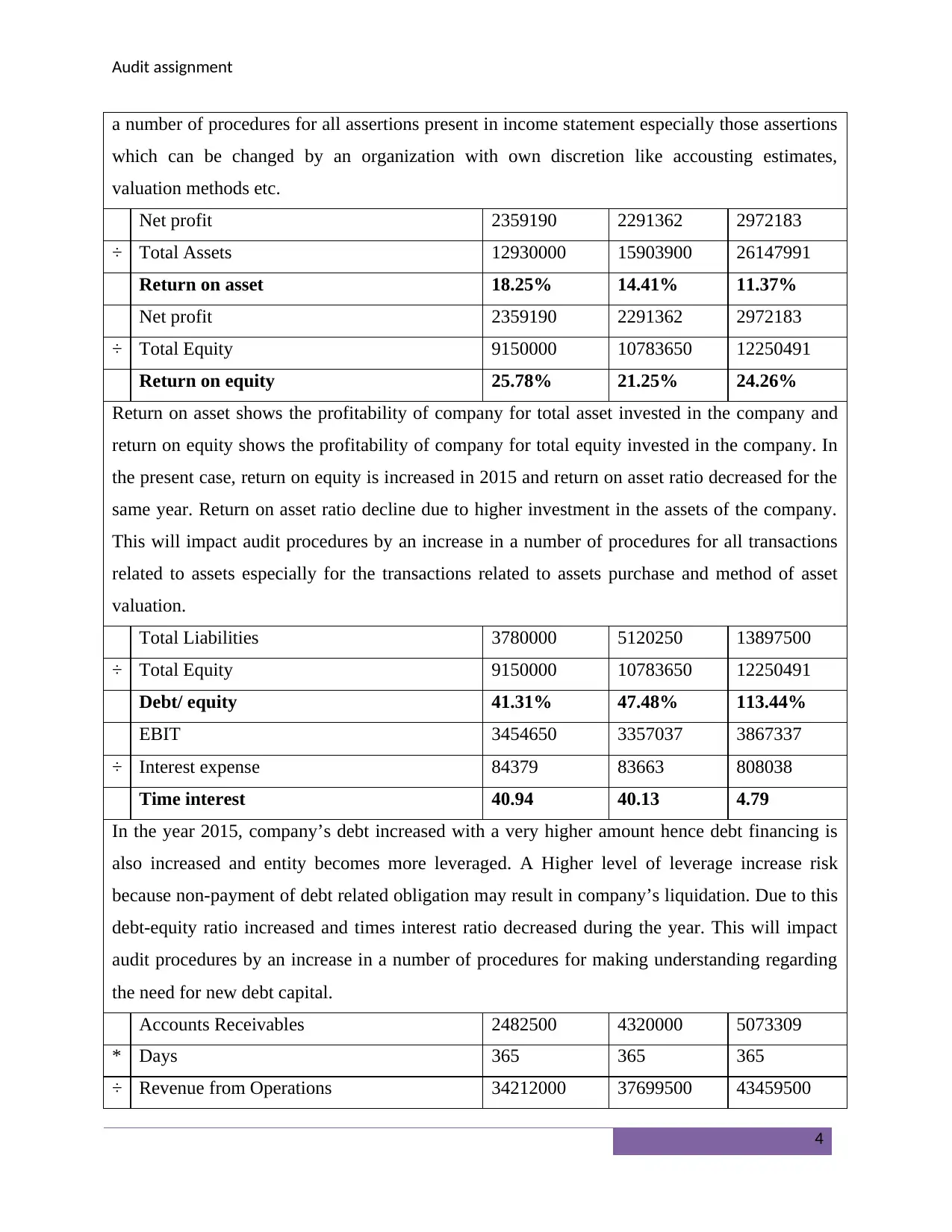

a number of procedures for all assertions present in income statement especially those assertions

which can be changed by an organization with own discretion like accousting estimates,

valuation methods etc.

Net profit 2359190 2291362 2972183

÷ Total Assets 12930000 15903900 26147991

Return on asset 18.25% 14.41% 11.37%

Net profit 2359190 2291362 2972183

÷ Total Equity 9150000 10783650 12250491

Return on equity 25.78% 21.25% 24.26%

Return on asset shows the profitability of company for total asset invested in the company and

return on equity shows the profitability of company for total equity invested in the company. In

the present case, return on equity is increased in 2015 and return on asset ratio decreased for the

same year. Return on asset ratio decline due to higher investment in the assets of the company.

This will impact audit procedures by an increase in a number of procedures for all transactions

related to assets especially for the transactions related to assets purchase and method of asset

valuation.

Total Liabilities 3780000 5120250 13897500

÷ Total Equity 9150000 10783650 12250491

Debt/ equity 41.31% 47.48% 113.44%

EBIT 3454650 3357037 3867337

÷ Interest expense 84379 83663 808038

Time interest 40.94 40.13 4.79

In the year 2015, company’s debt increased with a very higher amount hence debt financing is

also increased and entity becomes more leveraged. A Higher level of leverage increase risk

because non-payment of debt related obligation may result in company’s liquidation. Due to this

debt-equity ratio increased and times interest ratio decreased during the year. This will impact

audit procedures by an increase in a number of procedures for making understanding regarding

the need for new debt capital.

Accounts Receivables 2482500 4320000 5073309

* Days 365 365 365

÷ Revenue from Operations 34212000 37699500 43459500

4

a number of procedures for all assertions present in income statement especially those assertions

which can be changed by an organization with own discretion like accousting estimates,

valuation methods etc.

Net profit 2359190 2291362 2972183

÷ Total Assets 12930000 15903900 26147991

Return on asset 18.25% 14.41% 11.37%

Net profit 2359190 2291362 2972183

÷ Total Equity 9150000 10783650 12250491

Return on equity 25.78% 21.25% 24.26%

Return on asset shows the profitability of company for total asset invested in the company and

return on equity shows the profitability of company for total equity invested in the company. In

the present case, return on equity is increased in 2015 and return on asset ratio decreased for the

same year. Return on asset ratio decline due to higher investment in the assets of the company.

This will impact audit procedures by an increase in a number of procedures for all transactions

related to assets especially for the transactions related to assets purchase and method of asset

valuation.

Total Liabilities 3780000 5120250 13897500

÷ Total Equity 9150000 10783650 12250491

Debt/ equity 41.31% 47.48% 113.44%

EBIT 3454650 3357037 3867337

÷ Interest expense 84379 83663 808038

Time interest 40.94 40.13 4.79

In the year 2015, company’s debt increased with a very higher amount hence debt financing is

also increased and entity becomes more leveraged. A Higher level of leverage increase risk

because non-payment of debt related obligation may result in company’s liquidation. Due to this

debt-equity ratio increased and times interest ratio decreased during the year. This will impact

audit procedures by an increase in a number of procedures for making understanding regarding

the need for new debt capital.

Accounts Receivables 2482500 4320000 5073309

* Days 365 365 365

÷ Revenue from Operations 34212000 37699500 43459500

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

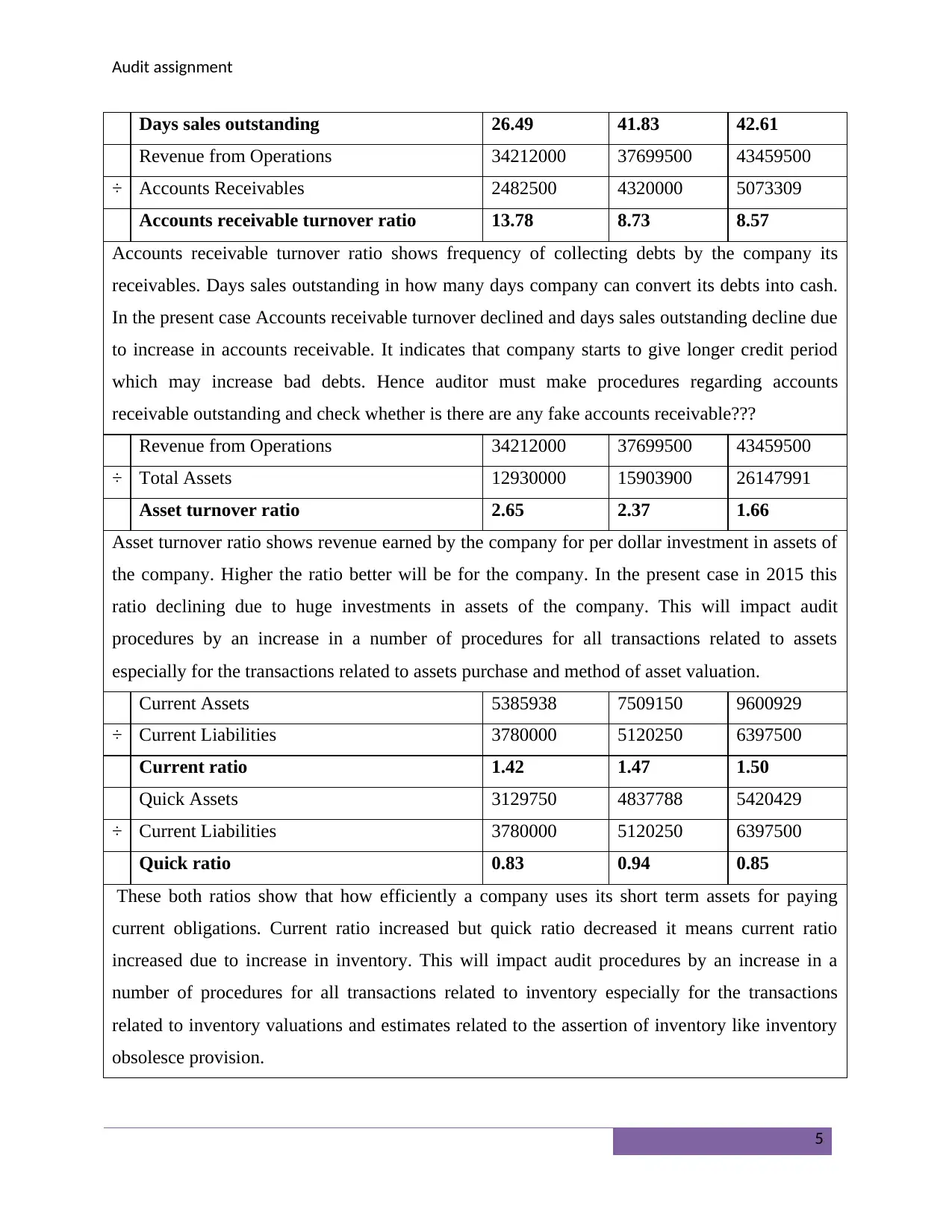

Days sales outstanding 26.49 41.83 42.61

Revenue from Operations 34212000 37699500 43459500

÷ Accounts Receivables 2482500 4320000 5073309

Accounts receivable turnover ratio 13.78 8.73 8.57

Accounts receivable turnover ratio shows frequency of collecting debts by the company its

receivables. Days sales outstanding in how many days company can convert its debts into cash.

In the present case Accounts receivable turnover declined and days sales outstanding decline due

to increase in accounts receivable. It indicates that company starts to give longer credit period

which may increase bad debts. Hence auditor must make procedures regarding accounts

receivable outstanding and check whether is there are any fake accounts receivable???

Revenue from Operations 34212000 37699500 43459500

÷ Total Assets 12930000 15903900 26147991

Asset turnover ratio 2.65 2.37 1.66

Asset turnover ratio shows revenue earned by the company for per dollar investment in assets of

the company. Higher the ratio better will be for the company. In the present case in 2015 this

ratio declining due to huge investments in assets of the company. This will impact audit

procedures by an increase in a number of procedures for all transactions related to assets

especially for the transactions related to assets purchase and method of asset valuation.

Current Assets 5385938 7509150 9600929

÷ Current Liabilities 3780000 5120250 6397500

Current ratio 1.42 1.47 1.50

Quick Assets 3129750 4837788 5420429

÷ Current Liabilities 3780000 5120250 6397500

Quick ratio 0.83 0.94 0.85

These both ratios show that how efficiently a company uses its short term assets for paying

current obligations. Current ratio increased but quick ratio decreased it means current ratio

increased due to increase in inventory. This will impact audit procedures by an increase in a

number of procedures for all transactions related to inventory especially for the transactions

related to inventory valuations and estimates related to the assertion of inventory like inventory

obsolesce provision.

5

Days sales outstanding 26.49 41.83 42.61

Revenue from Operations 34212000 37699500 43459500

÷ Accounts Receivables 2482500 4320000 5073309

Accounts receivable turnover ratio 13.78 8.73 8.57

Accounts receivable turnover ratio shows frequency of collecting debts by the company its

receivables. Days sales outstanding in how many days company can convert its debts into cash.

In the present case Accounts receivable turnover declined and days sales outstanding decline due

to increase in accounts receivable. It indicates that company starts to give longer credit period

which may increase bad debts. Hence auditor must make procedures regarding accounts

receivable outstanding and check whether is there are any fake accounts receivable???

Revenue from Operations 34212000 37699500 43459500

÷ Total Assets 12930000 15903900 26147991

Asset turnover ratio 2.65 2.37 1.66

Asset turnover ratio shows revenue earned by the company for per dollar investment in assets of

the company. Higher the ratio better will be for the company. In the present case in 2015 this

ratio declining due to huge investments in assets of the company. This will impact audit

procedures by an increase in a number of procedures for all transactions related to assets

especially for the transactions related to assets purchase and method of asset valuation.

Current Assets 5385938 7509150 9600929

÷ Current Liabilities 3780000 5120250 6397500

Current ratio 1.42 1.47 1.50

Quick Assets 3129750 4837788 5420429

÷ Current Liabilities 3780000 5120250 6397500

Quick ratio 0.83 0.94 0.85

These both ratios show that how efficiently a company uses its short term assets for paying

current obligations. Current ratio increased but quick ratio decreased it means current ratio

increased due to increase in inventory. This will impact audit procedures by an increase in a

number of procedures for all transactions related to inventory especially for the transactions

related to inventory valuations and estimates related to the assertion of inventory like inventory

obsolesce provision.

5

Audit assignment

Analytical procedures are procedures those help the auditor in making auditor plan and plan how

to conduct an audit, which areas of the company’s financial report needs a greater number of

procedures etc. Results from these procedures will increase the procedures for the above

mentioned assertions and transactions.

6

Analytical procedures are procedures those help the auditor in making auditor plan and plan how

to conduct an audit, which areas of the company’s financial report needs a greater number of

procedures etc. Results from these procedures will increase the procedures for the above

mentioned assertions and transactions.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

Question 2

Risk assessment procedures are performed by organizations for examining the risk present in the

financial reports which may misstate financial reports of the company significantly (Auditing

and Assurance Standards Board, 2011), due to which decisions of users of financial statements

will effect considerably. This process is a relevant process for conduct of the audit. Under this

process auditor of the organization obtain assurance that risk falsehood in the financial report is

at the level which can be accepted by the auditor. Risk of significant falsehood in the financial

statements can arise due to three reason i.e. due to nature of transactions, due to the absence of

appropriate controls or due to non-detection significant falsehood by auditor because of the

lower number of audit procedures. Risk arises because of first, second and third reasons termed

as inherent risk, control risk, and detection risk respectively (Houston et al., 1999).

In the present case in Double ink printers limited, following are inherent risk factors,

Change in inventory valuation method

In the present case Double ink printers limited change its method for estimating the carring

amount of inventory. Previously company used average cost method where the average cost of

all puchases applied to closing inventory, but in 2015 company stoped using average cost

method and starts using first in fist out method, where inventory valuation made on the basis of

the purchase price of units purchased just before the end of the period. Due to inflation first in

first out method always provide higher inventory value. Incerease in carring amount of closing

inventory incerease the amount of profit earned by copany during the year in the income

statement. Incerease in the amount of profit earned by copany during the year in the income

statement surely impacts the decisions of person useine financial repors for making decisions.

Application of new IT system

During the year company set new system for accounting processes. This system will be fully

automated and will also integrate general ledger system of the company. This system imposed by

the board of a company with pressure without having appropriate staff and after receiving

complaints form IT department of the company after application of the system. Application of

this system results in many problems like interfacing between the previous and new system, non-

allocation of year end entries to the appropriate accounting year. Due to this transaction in the

7

Question 2

Risk assessment procedures are performed by organizations for examining the risk present in the

financial reports which may misstate financial reports of the company significantly (Auditing

and Assurance Standards Board, 2011), due to which decisions of users of financial statements

will effect considerably. This process is a relevant process for conduct of the audit. Under this

process auditor of the organization obtain assurance that risk falsehood in the financial report is

at the level which can be accepted by the auditor. Risk of significant falsehood in the financial

statements can arise due to three reason i.e. due to nature of transactions, due to the absence of

appropriate controls or due to non-detection significant falsehood by auditor because of the

lower number of audit procedures. Risk arises because of first, second and third reasons termed

as inherent risk, control risk, and detection risk respectively (Houston et al., 1999).

In the present case in Double ink printers limited, following are inherent risk factors,

Change in inventory valuation method

In the present case Double ink printers limited change its method for estimating the carring

amount of inventory. Previously company used average cost method where the average cost of

all puchases applied to closing inventory, but in 2015 company stoped using average cost

method and starts using first in fist out method, where inventory valuation made on the basis of

the purchase price of units purchased just before the end of the period. Due to inflation first in

first out method always provide higher inventory value. Incerease in carring amount of closing

inventory incerease the amount of profit earned by copany during the year in the income

statement. Incerease in the amount of profit earned by copany during the year in the income

statement surely impacts the decisions of person useine financial repors for making decisions.

Application of new IT system

During the year company set new system for accounting processes. This system will be fully

automated and will also integrate general ledger system of the company. This system imposed by

the board of a company with pressure without having appropriate staff and after receiving

complaints form IT department of the company after application of the system. Application of

this system results in many problems like interfacing between the previous and new system, non-

allocation of year end entries to the appropriate accounting year. Due to this transaction in the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

year, there may be a higher number of inappropriate allocations of significant transaction year

end entries that can influence decisions of person useine financial repors for making decisions.

8

year, there may be a higher number of inappropriate allocations of significant transaction year

end entries that can influence decisions of person useine financial repors for making decisions.

8

Audit assignment

Question 3

Fraud is an illegal activity which performed for enjoying unjust benefits. Fraud is an intentional

act and cannot be interchanged with the error because the error is an unintentional act. Fraud is

performed with the intention hence person making fraud use ways to cover that fraud. Fraud is

covered by fraudster hence there is a higher chance of non-detection of fraud in comparison of a

chance of non-detection of error (Auditing and Assurance Standards Board, 2013). Fraud risk

arises when any person comes under the pressure of showing the better position of the financial

report in comparison of the actual position of financial report or it can arise when any person

having a higher level of privileges (Knapp & Knapp, 2001). Fraud can be initiated at any level of

the organization’s management, staff or employee.

In the present case following are the fraud risk factors arise,

Fraud risk

factor

Company changes its method for estimating the

carring amount of inventory. Previously

company used average cost method but in 2015

company stoped using average cost method and

starts using first in fist out method, Due to

inflation first in first out method always provide

higher inventory value. In addition to this

company stopped making inventory absolance

reserve. The company took a loan during the

year 2015 for BDO finance company which

includes a condition that loan can be recalled by

financing company due to the non maintenance

of current ratio at least one.

In previous year company

made an investment in the net

assets of Nuclear Publishing

limited company. A company

by stating the reason that this

company’s book data is

worthy and useful for

increasing revenue from e-

books.

Identification

of fraud risk

factor

Connecting both transactions with each other

emerge the doubt of the presence of fraud risk

factor because the company needs to increase

current ratio for meeting financial company’s

condition. Current ratio can be increased by an

increase in inventory value. Incerease in carring

In current year a journal

article reveals that book data

of Nuclear Publishing limited

can be loose its value due to

the implication of new theory.

This article emerges as fraud

9

Question 3

Fraud is an illegal activity which performed for enjoying unjust benefits. Fraud is an intentional

act and cannot be interchanged with the error because the error is an unintentional act. Fraud is

performed with the intention hence person making fraud use ways to cover that fraud. Fraud is

covered by fraudster hence there is a higher chance of non-detection of fraud in comparison of a

chance of non-detection of error (Auditing and Assurance Standards Board, 2013). Fraud risk

arises when any person comes under the pressure of showing the better position of the financial

report in comparison of the actual position of financial report or it can arise when any person

having a higher level of privileges (Knapp & Knapp, 2001). Fraud can be initiated at any level of

the organization’s management, staff or employee.

In the present case following are the fraud risk factors arise,

Fraud risk

factor

Company changes its method for estimating the

carring amount of inventory. Previously

company used average cost method but in 2015

company stoped using average cost method and

starts using first in fist out method, Due to

inflation first in first out method always provide

higher inventory value. In addition to this

company stopped making inventory absolance

reserve. The company took a loan during the

year 2015 for BDO finance company which

includes a condition that loan can be recalled by

financing company due to the non maintenance

of current ratio at least one.

In previous year company

made an investment in the net

assets of Nuclear Publishing

limited company. A company

by stating the reason that this

company’s book data is

worthy and useful for

increasing revenue from e-

books.

Identification

of fraud risk

factor

Connecting both transactions with each other

emerge the doubt of the presence of fraud risk

factor because the company needs to increase

current ratio for meeting financial company’s

condition. Current ratio can be increased by an

increase in inventory value. Incerease in carring

In current year a journal

article reveals that book data

of Nuclear Publishing limited

can be loose its value due to

the implication of new theory.

This article emerges as fraud

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

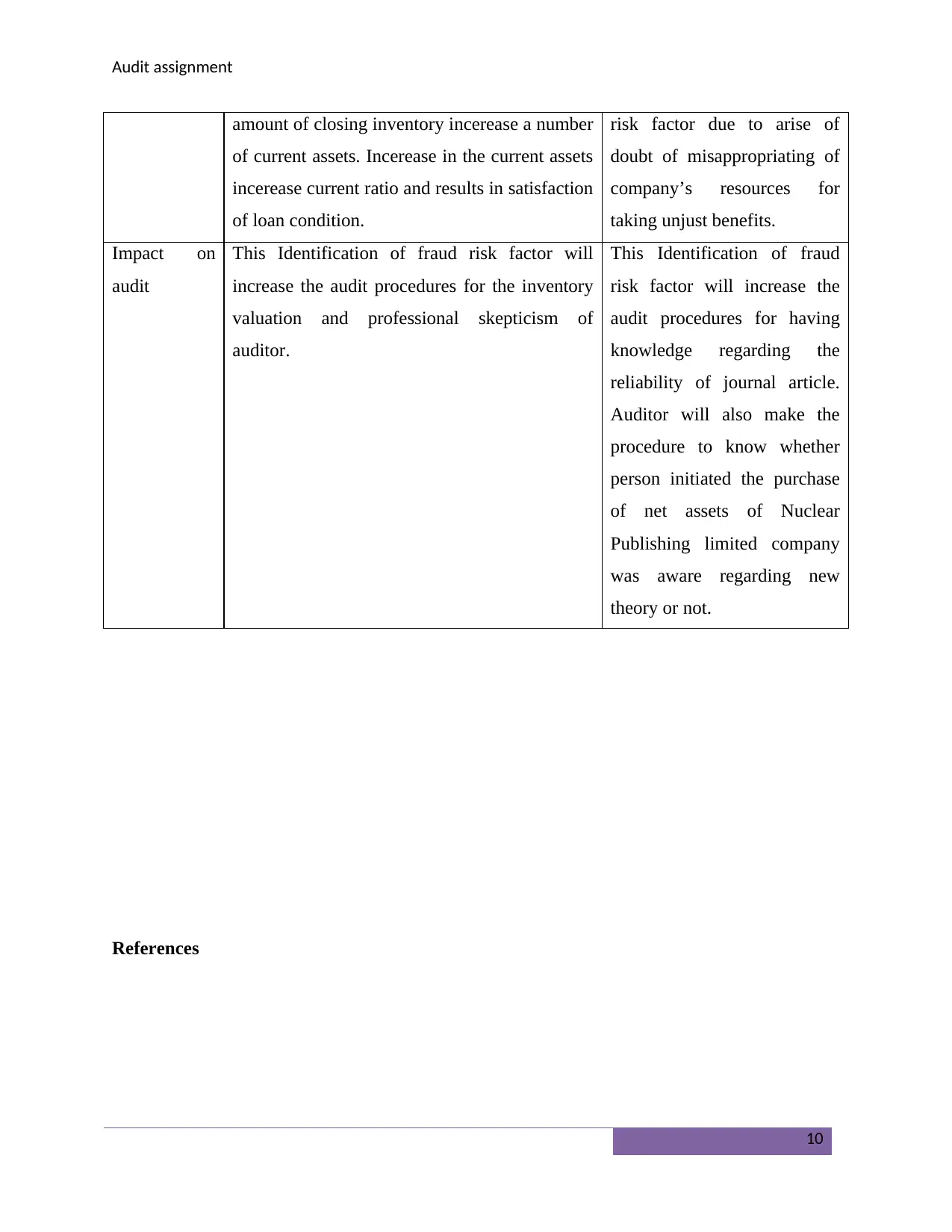

amount of closing inventory incerease a number

of current assets. Incerease in the current assets

incerease current ratio and results in satisfaction

of loan condition.

risk factor due to arise of

doubt of misappropriating of

company’s resources for

taking unjust benefits.

Impact on

audit

This Identification of fraud risk factor will

increase the audit procedures for the inventory

valuation and professional skepticism of

auditor.

This Identification of fraud

risk factor will increase the

audit procedures for having

knowledge regarding the

reliability of journal article.

Auditor will also make the

procedure to know whether

person initiated the purchase

of net assets of Nuclear

Publishing limited company

was aware regarding new

theory or not.

References

10

amount of closing inventory incerease a number

of current assets. Incerease in the current assets

incerease current ratio and results in satisfaction

of loan condition.

risk factor due to arise of

doubt of misappropriating of

company’s resources for

taking unjust benefits.

Impact on

audit

This Identification of fraud risk factor will

increase the audit procedures for the inventory

valuation and professional skepticism of

auditor.

This Identification of fraud

risk factor will increase the

audit procedures for having

knowledge regarding the

reliability of journal article.

Auditor will also make the

procedure to know whether

person initiated the purchase

of net assets of Nuclear

Publishing limited company

was aware regarding new

theory or not.

References

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

Auditing and Assurance Standards Board, 2009. ASA 520 Analytical Procedures. [Online]

Available at: www.auasb.gov.au/admin/file/content102/c3/ASA_520_27-10-09.pdf [Accessed

August 23 2017].

Auditing and Assurance Standards Board, 2009. Auditing Standard ASA 200 Overall Objectives

of the Independent Auditor and the Conduct of an Audit in Accordance with Australian Auditing

Standards. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_200_27-10-09.pdf [Accessed 23 august

2017].

Auditing and Assurance Standards Board, 2011. Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment. [Online] Available at: file:///F:/GS%20Solution%20(60%20paise)/Aug/16/risk

%20assement%20procedure.pdf [Accessed 23 august 2017].

Auditing and Assurance Standards Board, 2013. Auditing Standard ASA 240 The Auditor's

Responsibilities Relating to Fraud in an Audit of a Financial Report. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA_

240.pdf [Accessed 2017 August 23].

Glover, S.M., Jiambalvo, J. & Kennedy, J., 2000. Analytical Procedures and Audit‐Planning

Decisions. AUDITING: A Journal of Practice & Theory, pp.27-45.

HIRST, D.E. & KOONCE, L., 1996. Audit Analytical Procedures: A Field Investigation.

Contemporary Accounting Research, 13(2), pp.457-86.

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The Audit Risk Model, Business Risk, and

Audit‐Planning Decisions. The Accounting Review, 74(3), pp.281-98.

Knapp, C.A. & Knapp, M.C., 2001. The effects of experience and explicit fraud risk assessment

in detecting fraud with analytical procedures. Accounting, Organizations and Society, 26(1),

pp.25-37.

11

Auditing and Assurance Standards Board, 2009. ASA 520 Analytical Procedures. [Online]

Available at: www.auasb.gov.au/admin/file/content102/c3/ASA_520_27-10-09.pdf [Accessed

August 23 2017].

Auditing and Assurance Standards Board, 2009. Auditing Standard ASA 200 Overall Objectives

of the Independent Auditor and the Conduct of an Audit in Accordance with Australian Auditing

Standards. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_200_27-10-09.pdf [Accessed 23 august

2017].

Auditing and Assurance Standards Board, 2011. Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment. [Online] Available at: file:///F:/GS%20Solution%20(60%20paise)/Aug/16/risk

%20assement%20procedure.pdf [Accessed 23 august 2017].

Auditing and Assurance Standards Board, 2013. Auditing Standard ASA 240 The Auditor's

Responsibilities Relating to Fraud in an Audit of a Financial Report. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA_

240.pdf [Accessed 2017 August 23].

Glover, S.M., Jiambalvo, J. & Kennedy, J., 2000. Analytical Procedures and Audit‐Planning

Decisions. AUDITING: A Journal of Practice & Theory, pp.27-45.

HIRST, D.E. & KOONCE, L., 1996. Audit Analytical Procedures: A Field Investigation.

Contemporary Accounting Research, 13(2), pp.457-86.

Houston, R.W., Peters, M.F. & Pratt, J.H., 1999. The Audit Risk Model, Business Risk, and

Audit‐Planning Decisions. The Accounting Review, 74(3), pp.281-98.

Knapp, C.A. & Knapp, M.C., 2001. The effects of experience and explicit fraud risk assessment

in detecting fraud with analytical procedures. Accounting, Organizations and Society, 26(1),

pp.25-37.

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.