Auditing and Assurance Report: DIPL Financial Performance Analysis

VerifiedAdded on 2020/03/04

|9

|2305

|41

Report

AI Summary

This report provides an in-depth auditing and assurance analysis of DIPL's financial performance. It begins by explaining how analytical procedures influence audit planning, emphasizing the importance of ratio analysis and benchmarking to assess financial health and identify trends. The report then explores the risks affecting DIPL, including those related to record-keeping omissions, ineffective management, and employee inexperience, and their potential impact on material misstatements in financial reports. Furthermore, it identifies and explains two key fraud risk factors: potential fraudulent activities by employees and the manipulation of the financial reporting process due to loan requirements. The report concludes by depicting how these risk factors would affect the audit process, particularly concerning the valuation of raw materials and the implementation of new systems. The analysis draws upon various academic sources to support its findings and recommendations.

Running head: AUDITING & ASSURANCE

Auditing & Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing & Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING & ASSURANCE

Table of Contents

Question 1: Explaining how results influence planning results of the audit of year ending 30

June 2015...................................................................................................................................2

Question 2: Explaining the risk and how it might affect the material misstatement in the

financial report...........................................................................................................................4

Question 3a: Identifying and explaining the two key fraud risk factors, which might increase

fraudulent financial reporting.....................................................................................................5

Question 3b: Depicting how the risk actors would affect the audit...........................................7

Reference and Bibliography:......................................................................................................8

AUDITING & ASSURANCE

Table of Contents

Question 1: Explaining how results influence planning results of the audit of year ending 30

June 2015...................................................................................................................................2

Question 2: Explaining the risk and how it might affect the material misstatement in the

financial report...........................................................................................................................4

Question 3a: Identifying and explaining the two key fraud risk factors, which might increase

fraudulent financial reporting.....................................................................................................5

Question 3b: Depicting how the risk actors would affect the audit...........................................7

Reference and Bibliography:......................................................................................................8

2

AUDITING & ASSURANCE

Question 1: Explaining how results influence planning results of the audit of year

ending 30 June 2015

Analytical process is considered to be one of the adequate information providing

systems, which allows the company to develop adequate audit plan. The use of the audit plan

mainly allows the auditor’s relevant steps that need to be conducted complete the audit

operation. Arens, Elder and Beasley (2014) mentioned that with the help of audit plan,

auditors are able to control and maintain the overall audit cost, which is needed to complete

the overall audit procedures. However, DIPL need an adequate analytical approach for

reviewing the overall financial information, which has been declared by the organisation. The

analytical approach only allows the financial analyst and auditors to understand overall

performance of the organisation and make relevant accounting and financial decisions.

Furthermore, with the help of common size analytical approach, individuals are able to

evaluate the financial declaration that has been conducted by the organisation. In this context,

Arens et al. (2016) stated that the evaluation and comparison of different financial reports

allows the financial analyst to understand the trend of the organisation.

There are different ways in which financial analyst and Accountants are able to

evaluate the financial report of an organisation. The major analytical process that could be

used by the analyst is the Benchmarking. This method directly allows the analyst to compare

the financial condition of an organisation to its peers. Relevant variance could be identified

with the help of benchmarking process, which could directly pinpointing causes of the

variance and performance between the company and its competitors. Furthermore, the use of

ratios also allows the financial analyst to evaluate the financial information provided by an

organisation. The evaluation conducted by the ratios allows the organisation to compare the

performance of the organisation with not only its competitors but also with the previous fiscal

AUDITING & ASSURANCE

Question 1: Explaining how results influence planning results of the audit of year

ending 30 June 2015

Analytical process is considered to be one of the adequate information providing

systems, which allows the company to develop adequate audit plan. The use of the audit plan

mainly allows the auditor’s relevant steps that need to be conducted complete the audit

operation. Arens, Elder and Beasley (2014) mentioned that with the help of audit plan,

auditors are able to control and maintain the overall audit cost, which is needed to complete

the overall audit procedures. However, DIPL need an adequate analytical approach for

reviewing the overall financial information, which has been declared by the organisation. The

analytical approach only allows the financial analyst and auditors to understand overall

performance of the organisation and make relevant accounting and financial decisions.

Furthermore, with the help of common size analytical approach, individuals are able to

evaluate the financial declaration that has been conducted by the organisation. In this context,

Arens et al. (2016) stated that the evaluation and comparison of different financial reports

allows the financial analyst to understand the trend of the organisation.

There are different ways in which financial analyst and Accountants are able to

evaluate the financial report of an organisation. The major analytical process that could be

used by the analyst is the Benchmarking. This method directly allows the analyst to compare

the financial condition of an organisation to its peers. Relevant variance could be identified

with the help of benchmarking process, which could directly pinpointing causes of the

variance and performance between the company and its competitors. Furthermore, the use of

ratios also allows the financial analyst to evaluate the financial information provided by an

organisation. The evaluation conducted by the ratios allows the organisation to compare the

performance of the organisation with not only its competitors but also with the previous fiscal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING & ASSURANCE

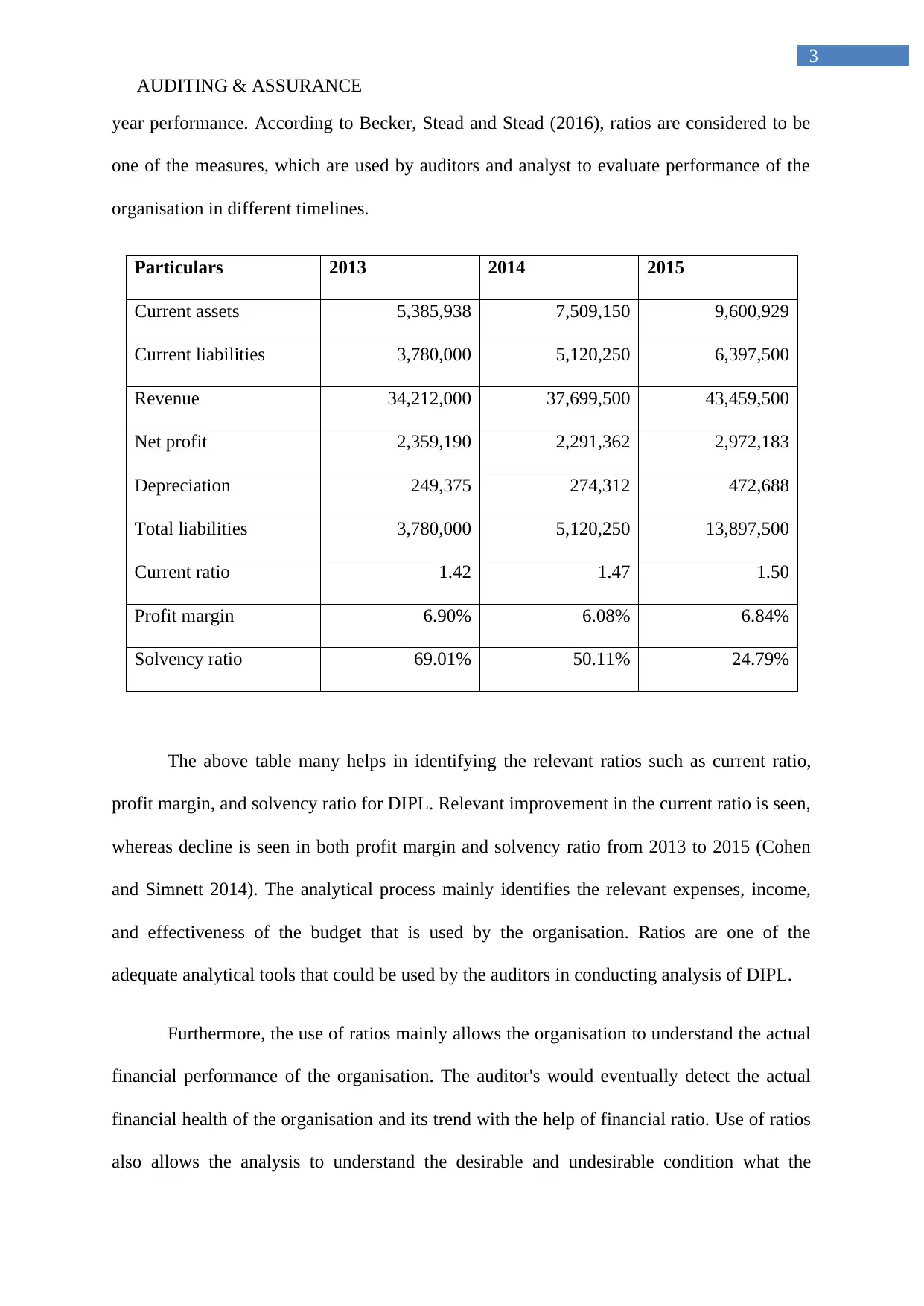

year performance. According to Becker, Stead and Stead (2016), ratios are considered to be

one of the measures, which are used by auditors and analyst to evaluate performance of the

organisation in different timelines.

Particulars 2013 2014 2015

Current assets 5,385,938 7,509,150 9,600,929

Current liabilities 3,780,000 5,120,250 6,397,500

Revenue 34,212,000 37,699,500 43,459,500

Net profit 2,359,190 2,291,362 2,972,183

Depreciation 249,375 274,312 472,688

Total liabilities 3,780,000 5,120,250 13,897,500

Current ratio 1.42 1.47 1.50

Profit margin 6.90% 6.08% 6.84%

Solvency ratio 69.01% 50.11% 24.79%

The above table many helps in identifying the relevant ratios such as current ratio,

profit margin, and solvency ratio for DIPL. Relevant improvement in the current ratio is seen,

whereas decline is seen in both profit margin and solvency ratio from 2013 to 2015 (Cohen

and Simnett 2014). The analytical process mainly identifies the relevant expenses, income,

and effectiveness of the budget that is used by the organisation. Ratios are one of the

adequate analytical tools that could be used by the auditors in conducting analysis of DIPL.

Furthermore, the use of ratios mainly allows the organisation to understand the actual

financial performance of the organisation. The auditor's would eventually detect the actual

financial health of the organisation and its trend with the help of financial ratio. Use of ratios

also allows the analysis to understand the desirable and undesirable condition what the

AUDITING & ASSURANCE

year performance. According to Becker, Stead and Stead (2016), ratios are considered to be

one of the measures, which are used by auditors and analyst to evaluate performance of the

organisation in different timelines.

Particulars 2013 2014 2015

Current assets 5,385,938 7,509,150 9,600,929

Current liabilities 3,780,000 5,120,250 6,397,500

Revenue 34,212,000 37,699,500 43,459,500

Net profit 2,359,190 2,291,362 2,972,183

Depreciation 249,375 274,312 472,688

Total liabilities 3,780,000 5,120,250 13,897,500

Current ratio 1.42 1.47 1.50

Profit margin 6.90% 6.08% 6.84%

Solvency ratio 69.01% 50.11% 24.79%

The above table many helps in identifying the relevant ratios such as current ratio,

profit margin, and solvency ratio for DIPL. Relevant improvement in the current ratio is seen,

whereas decline is seen in both profit margin and solvency ratio from 2013 to 2015 (Cohen

and Simnett 2014). The analytical process mainly identifies the relevant expenses, income,

and effectiveness of the budget that is used by the organisation. Ratios are one of the

adequate analytical tools that could be used by the auditors in conducting analysis of DIPL.

Furthermore, the use of ratios mainly allows the organisation to understand the actual

financial performance of the organisation. The auditor's would eventually detect the actual

financial health of the organisation and its trend with the help of financial ratio. Use of ratios

also allows the analysis to understand the desirable and undesirable condition what the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING & ASSURANCE

company's current financial position. However, the current case of DIPL is relatively

undesirable, as the organisations performance has rapidly declined over the period of three

years. The performance of the organisations have deteriorated over the period of three fiscal

years, which directly imposes the overall corrective measures that needs to be conducted by

the organisation for increasing its future performance (Cohen and Simnett 2015). Thus, it

could be evaluated that the above mentioned reasons have relevant significance, which forces

the organisation to use analytical process on its financial information.

Question 2: Explaining the risk and how it might affect the material misstatement in the

financial report

There are two types of inheritance that could be identified from the operations of

DIPL, which is hindering the operational capability of the organisation. However there are

certain risk that could be evaluated first to understand the risk factors that is hampering the

operations of the DIPL. Evaluation of a case study mainly helps in understanding that the

accounts department of the organisation have conducted different types of omission in

Record Keeping. The omissions of the transaction mainly increase the inconsistency in the

planning and marketing phase for the organisation. Moreover, it is seen that the organisation

failed to achieve the targeted revenue and profit level, which was set by the analyst. The other

risk comprises of the inconsistency and ineffectiveness of the company's management, which

is hampering the overall operations of the organisation (Earley et al. 2016). Moreover,

management was not able to comprehend the risk identified from micro and macroeconomic

factors such as economic, political, and social. Therefore, declining profit margin and

revenue mainly increased the inheritance risk of the organisation.

The second inheritance risk mainly comprises of the employees currently working in

DIPL, who are not having the adequate experience and proficiency level to increase

AUDITING & ASSURANCE

company's current financial position. However, the current case of DIPL is relatively

undesirable, as the organisations performance has rapidly declined over the period of three

years. The performance of the organisations have deteriorated over the period of three fiscal

years, which directly imposes the overall corrective measures that needs to be conducted by

the organisation for increasing its future performance (Cohen and Simnett 2015). Thus, it

could be evaluated that the above mentioned reasons have relevant significance, which forces

the organisation to use analytical process on its financial information.

Question 2: Explaining the risk and how it might affect the material misstatement in the

financial report

There are two types of inheritance that could be identified from the operations of

DIPL, which is hindering the operational capability of the organisation. However there are

certain risk that could be evaluated first to understand the risk factors that is hampering the

operations of the DIPL. Evaluation of a case study mainly helps in understanding that the

accounts department of the organisation have conducted different types of omission in

Record Keeping. The omissions of the transaction mainly increase the inconsistency in the

planning and marketing phase for the organisation. Moreover, it is seen that the organisation

failed to achieve the targeted revenue and profit level, which was set by the analyst. The other

risk comprises of the inconsistency and ineffectiveness of the company's management, which

is hampering the overall operations of the organisation (Earley et al. 2016). Moreover,

management was not able to comprehend the risk identified from micro and macroeconomic

factors such as economic, political, and social. Therefore, declining profit margin and

revenue mainly increased the inheritance risk of the organisation.

The second inheritance risk mainly comprises of the employees currently working in

DIPL, who are not having the adequate experience and proficiency level to increase

5

AUDITING & ASSURANCE

productivity of the organisation. The evaluation of the study mainly states the inexperienced

employees working in DIPL, which could increase mistakes that might directly raise the

inheritance risk. Another way of finding the inheritance risk is by evaluating succession of

the so, which was conducted by an ineffective process (Eilifsen et al. 2013). This has directly

influenced inheritance risk of the organisation, which is affecting its operation and

productivity. Furthermore, the organisation does not have adequate workforce to handle the

business operations, which is also the reason why accountant are not able to record all the

transactions and are making relevant omission. The second inheritance risk that could be

identified from the case study is mainly the business operations of the organisation.

From the evaluation of the case study it is seen that poor bookkeeping is been

conducted due to excessive workloads imposed by the organisation. Furthermore, there is a

lack of adequate interpretation by the management, which increases the inheritance risk of the

organisation. Both the identified inheritance could directly increase the material misstatement

in the annual report, which in turn could reduce viability of the financial statement (Junior,

Best and Cotter 2014).

Question 3a: Identifying and explaining the two key fraud risk factors, which might

increase fraudulent financial reporting

Risk identified from the case Evaluating the risk

Fraud risk The first risk that could be identified from the Case study of

DIPL is mainly the fraudulent Paris which might be

conducted by employees of the organisation. the employees

of the organisation is relatively that satisfied with the

current operational capability, which might increase the

fraudulent activities. The case study mainly states the

AUDITING & ASSURANCE

productivity of the organisation. The evaluation of the study mainly states the inexperienced

employees working in DIPL, which could increase mistakes that might directly raise the

inheritance risk. Another way of finding the inheritance risk is by evaluating succession of

the so, which was conducted by an ineffective process (Eilifsen et al. 2013). This has directly

influenced inheritance risk of the organisation, which is affecting its operation and

productivity. Furthermore, the organisation does not have adequate workforce to handle the

business operations, which is also the reason why accountant are not able to record all the

transactions and are making relevant omission. The second inheritance risk that could be

identified from the case study is mainly the business operations of the organisation.

From the evaluation of the case study it is seen that poor bookkeeping is been

conducted due to excessive workloads imposed by the organisation. Furthermore, there is a

lack of adequate interpretation by the management, which increases the inheritance risk of the

organisation. Both the identified inheritance could directly increase the material misstatement

in the annual report, which in turn could reduce viability of the financial statement (Junior,

Best and Cotter 2014).

Question 3a: Identifying and explaining the two key fraud risk factors, which might

increase fraudulent financial reporting

Risk identified from the case Evaluating the risk

Fraud risk The first risk that could be identified from the Case study of

DIPL is mainly the fraudulent Paris which might be

conducted by employees of the organisation. the employees

of the organisation is relatively that satisfied with the

current operational capability, which might increase the

fraudulent activities. The case study mainly states the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING & ASSURANCE

pressure that was given to the Accountants of the

organisation to use the new accounting system, which

would increase the pressure on the employees. Thus,

increasing pressure could eventually result in fraudulent

activities conducted by the accountant, which in turn might

increase material misstatement in the financial report.

Moreover, inherent risk of the organisation could directly

increase due to the mistakes conducted by accountant in

drafting the financial report. Evaluation of the succession

process of CEO could also help in identifying the

inheritance risk that is affecting operations of the

organisation. The management of DIPL is relatively lacking

integrity and accountability in conducting relevant

operations in your organisation, which is why the company

is losing reputation in the business community (Kinney

2015).

The financial reporting process The second major risk that could affect operation of the

organisation can be identified from its financial reporting

process. The overall financial statement process of the

organisation could be manipulated and portray adequate

risk. The analysis of the case study also states that DIPL

mainly needs to maintain adequate current ratio of 1.5 and

debt ratio below 1, as stated in its loan requirements. This

restriction in the current ratio and debt ratio could

eventually force the management to manipulate the overall

AUDITING & ASSURANCE

pressure that was given to the Accountants of the

organisation to use the new accounting system, which

would increase the pressure on the employees. Thus,

increasing pressure could eventually result in fraudulent

activities conducted by the accountant, which in turn might

increase material misstatement in the financial report.

Moreover, inherent risk of the organisation could directly

increase due to the mistakes conducted by accountant in

drafting the financial report. Evaluation of the succession

process of CEO could also help in identifying the

inheritance risk that is affecting operations of the

organisation. The management of DIPL is relatively lacking

integrity and accountability in conducting relevant

operations in your organisation, which is why the company

is losing reputation in the business community (Kinney

2015).

The financial reporting process The second major risk that could affect operation of the

organisation can be identified from its financial reporting

process. The overall financial statement process of the

organisation could be manipulated and portray adequate

risk. The analysis of the case study also states that DIPL

mainly needs to maintain adequate current ratio of 1.5 and

debt ratio below 1, as stated in its loan requirements. This

restriction in the current ratio and debt ratio could

eventually force the management to manipulate the overall

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING & ASSURANCE

financial report to support its loan obligation. If adequate

measures of current ratio and debt ratio are not maintained

by the organisation then it would not be able to obtain the

loans provided from BDO Finance, which could directly

affect its operational capability. This need of the fixed

current ratio could eventually increase fraudulent actions

and activities in DIPL, which might force them to

manipulate the financial report. Therefore, it could be

understood that relevant fraudulent activities might be

conducted in the organisation and portray material

misstatements in the financial report (Knechel and Salterio

2016).

Question 3b: Depicting how the risk actors would affect the audit

The risk from fraudulent activities conducted by staff can be identified from the case

study, where implementation of new system could eventually help in monitoring activities of

the employees. For the more there is a problem with the valuation of raw materials, which is

conducted on average cost method. The average cost method is relevantly not adequate, as

the actual cost is higher than the average cost, which does not allow the organisation to

determine the actual expenses conducted in purchasing the raw materials (Louwers et al.

2015). There is a relevant risk that can be seen in the financial reporting process, which needs

to be evaluated by the auditor during the audit procedure.

AUDITING & ASSURANCE

financial report to support its loan obligation. If adequate

measures of current ratio and debt ratio are not maintained

by the organisation then it would not be able to obtain the

loans provided from BDO Finance, which could directly

affect its operational capability. This need of the fixed

current ratio could eventually increase fraudulent actions

and activities in DIPL, which might force them to

manipulate the financial report. Therefore, it could be

understood that relevant fraudulent activities might be

conducted in the organisation and portray material

misstatements in the financial report (Knechel and Salterio

2016).

Question 3b: Depicting how the risk actors would affect the audit

The risk from fraudulent activities conducted by staff can be identified from the case

study, where implementation of new system could eventually help in monitoring activities of

the employees. For the more there is a problem with the valuation of raw materials, which is

conducted on average cost method. The average cost method is relevantly not adequate, as

the actual cost is higher than the average cost, which does not allow the organisation to

determine the actual expenses conducted in purchasing the raw materials (Louwers et al.

2015). There is a relevant risk that can be seen in the financial reporting process, which needs

to be evaluated by the auditor during the audit procedure.

8

AUDITING & ASSURANCE

Reference and Bibliography:

Arens, A., Elder, R. and Beasley, M., 2014. Auditing and assurance services-An integrated

approach; includes coverage of international standards and global auditing issues, in addition

to coverage of. Boston: Aufl.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Becker, L.L., Stead, J.G. and Stead, W.E., 2016. Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), p.29.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Cohen, J.R. and Simnett, R., 2015. A forum on CSR and assurance services introduction.

Earley, C.E., Hooks, K.L., Joe, J.R., Polinski, P.W., Rezaee, Z., Roush, P.B., Sanderson,

K.A. and Wu, Y.J., 2016. The Auditing Standards Committee of the Auditing Section of the

American Accounting Association's Response to the International Auditing and Assurance

Standard's Board's Invitation to Comment: Enhancing Audit Quality in the Public

Interest. Current Issues in Auditing, 11(1), pp.C1-C25.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A

historical analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kinney Jr, W.R., 2015. GAAS 1963-2012: The Global Foundation of Independent Audits and

Research in Auditing.

AUDITING & ASSURANCE

Reference and Bibliography:

Arens, A., Elder, R. and Beasley, M., 2014. Auditing and assurance services-An integrated

approach; includes coverage of international standards and global auditing issues, in addition

to coverage of. Boston: Aufl.

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance

services. Pearson.

Becker, L.L., Stead, J.G. and Stead, W.E., 2016. Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), p.29.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing:

A Journal of Practice & Theory, 34(1), pp.59-74.

Cohen, J.R. and Simnett, R., 2015. A forum on CSR and assurance services introduction.

Earley, C.E., Hooks, K.L., Joe, J.R., Polinski, P.W., Rezaee, Z., Roush, P.B., Sanderson,

K.A. and Wu, Y.J., 2016. The Auditing Standards Committee of the Auditing Section of the

American Accounting Association's Response to the International Auditing and Assurance

Standard's Board's Invitation to Comment: Enhancing Audit Quality in the Public

Interest. Current Issues in Auditing, 11(1), pp.C1-C25.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A

historical analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kinney Jr, W.R., 2015. GAAS 1963-2012: The Global Foundation of Independent Audits and

Research in Auditing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.