Audit Report: Assessment of Rogers Communications Financial Position

VerifiedAdded on 2021/04/24

|21

|5024

|69

Report

AI Summary

This audit report provides a detailed analysis of the audit process for Rogers Communications, a major Canadian telecommunications company. The report outlines the audit planning memorandum, including business information, management integrity assessment, and auditor independence considerations. It addresses risks associated with the audit engagement, such as fraudulent revenue recognition and management override of controls. Preliminary audit planning, risk assessment procedures, and the approach to the audit are discussed, including pre-engagement activities, staffing, and time budgeting. The report also covers materiality levels, internal controls, documentation, and sampling decisions. It details the performance of planned audit programs, audit findings, and concludes with an opinion on the financial statements based on the audit procedures and evidence collected.

Running head: AUDIT

Audit

Name of the Student:

Name of the university:

Authors note:

Audit

Name of the Student:

Name of the university:

Authors note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT

Table of Contents

Introduction:....................................................................................................................................2

Business information:......................................................................................................................2

Integrity and responsibility of the management:.............................................................................3

Auditor’s independence and transparency:......................................................................................3

Risk associated with the audit engagement:....................................................................................4

Preliminary audit planning:.............................................................................................................5

Risk assessment:..........................................................................................................................5

Approach:........................................................................................................................................6

Pre-engagement activities:...............................................................................................................7

Staffing and time budget:.................................................................................................................7

Materiality:......................................................................................................................................8

Internal controls within the company:...........................................................................................10

Documentation...............................................................................................................................12

Sampling decisions:.......................................................................................................................12

Performance of planned audit programs:.......................................................................................13

Audit findings:...............................................................................................................................16

Conclusion:....................................................................................................................................17

Reference.......................................................................................................................................18

Table of Contents

Introduction:....................................................................................................................................2

Business information:......................................................................................................................2

Integrity and responsibility of the management:.............................................................................3

Auditor’s independence and transparency:......................................................................................3

Risk associated with the audit engagement:....................................................................................4

Preliminary audit planning:.............................................................................................................5

Risk assessment:..........................................................................................................................5

Approach:........................................................................................................................................6

Pre-engagement activities:...............................................................................................................7

Staffing and time budget:.................................................................................................................7

Materiality:......................................................................................................................................8

Internal controls within the company:...........................................................................................10

Documentation...............................................................................................................................12

Sampling decisions:.......................................................................................................................12

Performance of planned audit programs:.......................................................................................13

Audit findings:...............................................................................................................................16

Conclusion:....................................................................................................................................17

Reference.......................................................................................................................................18

2AUDIT

Introduction:

The purpose of the Audit Planning Memorandum is to provide a brief to the Audit

committee on the approach that have been adopted for the audit of Rogers Communications.

The main aim of auditing is to provide independent opinion on the financial statements of an

organization. The opinion of the auditors on the financial statements will help the users of the

financial statements to take correct decisions affecting their interests in such organizations. Audit

must be carried out in accordance with the Generally Accepted Auditing Standards in order to

ensure that the audit opinion is in accordance with the standards on auditing (Gildenhuis & Roos,

2015). In this document, an audit shall be conducted on the financial statements of Rogers

Communications, one of the largest companies in terms market valuation in the whole of

Canada. The document shall contain the procedures to be followed in the audit of the financial

statements of Rogers Communications from pre-audit engagement to the conclusion of the audit

of the company.

Business information:

Rogers Communications is one of the largest companies in the whole of Canada and it

operates in the field of communications and technology. To be more specific the company

operates in the field of wireless communications, cable television, telephone, internet and other

forms of communications in the country and other parts of the world. Founded in the year 1960

by Rogers Vacuum Tube Company the company has it’s headquarter situated in Toronto,

Ontario, Canada. Alan Hoe is the current chairman of the company with Joe Natale as the

president and Chief Executive Officer of the company (Krahmer & Phillips, 2016). The

company’s shares are listed on the Toronto stock exchange and New York Stock Exchange with

the ticker RCI. Over the years, the company has invented new ways to enrich the experience of

Introduction:

The purpose of the Audit Planning Memorandum is to provide a brief to the Audit

committee on the approach that have been adopted for the audit of Rogers Communications.

The main aim of auditing is to provide independent opinion on the financial statements of an

organization. The opinion of the auditors on the financial statements will help the users of the

financial statements to take correct decisions affecting their interests in such organizations. Audit

must be carried out in accordance with the Generally Accepted Auditing Standards in order to

ensure that the audit opinion is in accordance with the standards on auditing (Gildenhuis & Roos,

2015). In this document, an audit shall be conducted on the financial statements of Rogers

Communications, one of the largest companies in terms market valuation in the whole of

Canada. The document shall contain the procedures to be followed in the audit of the financial

statements of Rogers Communications from pre-audit engagement to the conclusion of the audit

of the company.

Business information:

Rogers Communications is one of the largest companies in the whole of Canada and it

operates in the field of communications and technology. To be more specific the company

operates in the field of wireless communications, cable television, telephone, internet and other

forms of communications in the country and other parts of the world. Founded in the year 1960

by Rogers Vacuum Tube Company the company has it’s headquarter situated in Toronto,

Ontario, Canada. Alan Hoe is the current chairman of the company with Joe Natale as the

president and Chief Executive Officer of the company (Krahmer & Phillips, 2016). The

company’s shares are listed on the Toronto stock exchange and New York Stock Exchange with

the ticker RCI. Over the years, the company has invented new ways to enrich the experience of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT

its customers by providing wireless network services as well as internet connectivity with

unrivalled quality and transmission power. Bell Canada is the primary competitor of the

company with substantial media assets to provide similar wireless network, cable television,

telephone services and internet connectivity.

Integrity and responsibility of the management:

The management over the years have conducted the business operations with honesty and

integrity to take the company to the top of the telecommunication and network business in the

country. The company is not only the largest telecommunication company in the country but also

one of the largest companies in all across Canada. Over the years, the annual reports of the

company containing the financial statements of the company have been prepared in accordance

with the International Financial Reporting Standards increase the confidence of the auditors on

the integrity and honesty of the management (Council, 2015).

The management is responsible for the preparation and presentation of the financial

statements of the company and the auditors are only reasonable to express an appropriate opinion

on the financial statements of the company. Thus, the use of appropriate accounting standards to

prepare and present the financial statements of the company is the responsibility of the

management and the auditor has nothing to do with the preparation and presentation of these

statements (Rose & Rose, 2014).

Auditor’s independence and transparency:

The Canadian Auditing standard (CAS) 260 “Communicating of Audit matters with

those charged with Governance” requires that the auditor should communicate any relationship

that exists between the company and the auditor. The auditor of the company is required to be

its customers by providing wireless network services as well as internet connectivity with

unrivalled quality and transmission power. Bell Canada is the primary competitor of the

company with substantial media assets to provide similar wireless network, cable television,

telephone services and internet connectivity.

Integrity and responsibility of the management:

The management over the years have conducted the business operations with honesty and

integrity to take the company to the top of the telecommunication and network business in the

country. The company is not only the largest telecommunication company in the country but also

one of the largest companies in all across Canada. Over the years, the annual reports of the

company containing the financial statements of the company have been prepared in accordance

with the International Financial Reporting Standards increase the confidence of the auditors on

the integrity and honesty of the management (Council, 2015).

The management is responsible for the preparation and presentation of the financial

statements of the company and the auditors are only reasonable to express an appropriate opinion

on the financial statements of the company. Thus, the use of appropriate accounting standards to

prepare and present the financial statements of the company is the responsibility of the

management and the auditor has nothing to do with the preparation and presentation of these

statements (Rose & Rose, 2014).

Auditor’s independence and transparency:

The Canadian Auditing standard (CAS) 260 “Communicating of Audit matters with

those charged with Governance” requires that the auditor should communicate any relationship

that exists between the company and the auditor. The auditor of the company is required to be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT

independent of the entity so that the auditor can provide an unbiased opinion on the financial

statement of the company (Miro et al., 2015). It is important to consider the independence while

appointing the auditor of the company and at the. Planning stage. Thus, no employee of the

company or any person who has any interests associated with the company shall be appointed as

the auditors of the company. In this case, the Auditor is independent of the entity and it can be

assured that the audit firms conforms to the highest level of governance standard.

Risk associated with the audit engagement:

The professional standards requires the auditor to consider these two kinds of risks:

Fraudulent revenue recognition;

Management override of control;

There are certain risks that revenues are recognised fraudulently to provide a different picture

of the financial situation of the organisation. The auditor should assess the risk of fraudulent

revenue recognition both at the time of accepting the engagement and at the planning stages of

audit (Okafor, 2015).

The management has the position of power to manipulate the accounting records and prepare

a financial statement with the fraudulent intention. The auditor should assess this risk at the

planning stage. In order to assess this risk test of control is conducted. In addition to this

substantive audit, procedure is conducted over the accounting estimates, journal entries and

significant transactions that occur in the normal course of business (Rahma et al., 2016).

There are two types of risks associated with the expression of audit opinion. Firstly, the

risk of expressing an opinion that the financial statements of the company are free of material

errors and misstatements whereas these are not. Secondly the risk of expressing an opinion that

independent of the entity so that the auditor can provide an unbiased opinion on the financial

statement of the company (Miro et al., 2015). It is important to consider the independence while

appointing the auditor of the company and at the. Planning stage. Thus, no employee of the

company or any person who has any interests associated with the company shall be appointed as

the auditors of the company. In this case, the Auditor is independent of the entity and it can be

assured that the audit firms conforms to the highest level of governance standard.

Risk associated with the audit engagement:

The professional standards requires the auditor to consider these two kinds of risks:

Fraudulent revenue recognition;

Management override of control;

There are certain risks that revenues are recognised fraudulently to provide a different picture

of the financial situation of the organisation. The auditor should assess the risk of fraudulent

revenue recognition both at the time of accepting the engagement and at the planning stages of

audit (Okafor, 2015).

The management has the position of power to manipulate the accounting records and prepare

a financial statement with the fraudulent intention. The auditor should assess this risk at the

planning stage. In order to assess this risk test of control is conducted. In addition to this

substantive audit, procedure is conducted over the accounting estimates, journal entries and

significant transactions that occur in the normal course of business (Rahma et al., 2016).

There are two types of risks associated with the expression of audit opinion. Firstly, the

risk of expressing an opinion that the financial statements of the company are free of material

errors and misstatements whereas these are not. Secondly the risk of expressing an opinion that

5AUDIT

the financial statements of the company are not free from misstatements whereas the financial

statements not contain any material errors or misstatements (Chonowitz, 2015). The auditors are

mainly concerned with the risk of expressing an inappropriate opinion on the financial

statements that the statement are free of material errors where in fact the statements contain

material errors.

After appraising the findings from the pre-engagement activities, the auditors shall

determine whether it would be appropriate to accept the engagement as auditor of the company

to express an appropriate audit opinion on the financial statements of the company.

Preliminary audit planning:

Preliminary audit planning is mainly dependent on the identified risks in the audit of the

financial statements of the company. Generally the pre-engagement activities and preliminary

investigation about the affairs and operations of the company will help us to identify the risks

associated with the audit of the financial statements of the company (Onoja & Usman, 2015).

Based on the findings of preliminary audit planning shall be made. The preliminary audit

planning of the company shall have to be made after considering figures and trends identified

from the brief financial statements of the company, i.e. income statement, Balance sheet and cash

flow statement of the company.

Risk assessment:

In order to assess the risk of material misstatement at the overall financial statement level

it is important to have significant knowledge about the financial performance and position of the

company. The auditors will use the financial statements of the company, i.e. Income statement of

the financial statements of the company are not free from misstatements whereas the financial

statements not contain any material errors or misstatements (Chonowitz, 2015). The auditors are

mainly concerned with the risk of expressing an inappropriate opinion on the financial

statements that the statement are free of material errors where in fact the statements contain

material errors.

After appraising the findings from the pre-engagement activities, the auditors shall

determine whether it would be appropriate to accept the engagement as auditor of the company

to express an appropriate audit opinion on the financial statements of the company.

Preliminary audit planning:

Preliminary audit planning is mainly dependent on the identified risks in the audit of the

financial statements of the company. Generally the pre-engagement activities and preliminary

investigation about the affairs and operations of the company will help us to identify the risks

associated with the audit of the financial statements of the company (Onoja & Usman, 2015).

Based on the findings of preliminary audit planning shall be made. The preliminary audit

planning of the company shall have to be made after considering figures and trends identified

from the brief financial statements of the company, i.e. income statement, Balance sheet and cash

flow statement of the company.

Risk assessment:

In order to assess the risk of material misstatement at the overall financial statement level

it is important to have significant knowledge about the financial performance and position of the

company. The auditors will use the financial statements of the company, i.e. Income statement of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT

the company, Balance sheet, cash flow statement of the company, statement of changes in equity

and notes to accounts (Martin et al., 2016).

The auditor will use effective audit procedures to collect necessary audit evidence based

on which the opinion shall be formulated. The necessary documents supporting the revenue as

provided in the financial statements along with the supporting documents against the

expenditures incurred shall be made available by the management of the company to allow the

auditors to conduct an effective audit (Kumar & Sharma, 2015). The overall risks assessment of

the audit will be dependent on the integrity and honesty of the management, employee and other

staffs of the company as the auditors will have to depend on the documents, written and oral

representations along with financial statements prepared by the internal staffs of the company.

As has already mentioned that the company has followed the IFRSs to prepare the financial

statements thus, the auditors can place reliance on the financial statements and conduct the audit

(Toolkit, 2014). Apart from that the auditors will verify the integrity and honesty of the

management to determine the extent to which they can place reliance on the evidences and

representations made by them while conducting the audit of the financial statements of the

company.

Approach:

In order to conduct an effective audit of the financial statements of any organization it is

important to follow the generally accepted auditing standards that have been universally accepted

to be effective auditing standards (Dhand & Diab, 2015). The following procedures shall be

properly followed in the audit of the financial statements of an organization in order to express

an appropriate audit opinion on the financial statements of the organization:

the company, Balance sheet, cash flow statement of the company, statement of changes in equity

and notes to accounts (Martin et al., 2016).

The auditor will use effective audit procedures to collect necessary audit evidence based

on which the opinion shall be formulated. The necessary documents supporting the revenue as

provided in the financial statements along with the supporting documents against the

expenditures incurred shall be made available by the management of the company to allow the

auditors to conduct an effective audit (Kumar & Sharma, 2015). The overall risks assessment of

the audit will be dependent on the integrity and honesty of the management, employee and other

staffs of the company as the auditors will have to depend on the documents, written and oral

representations along with financial statements prepared by the internal staffs of the company.

As has already mentioned that the company has followed the IFRSs to prepare the financial

statements thus, the auditors can place reliance on the financial statements and conduct the audit

(Toolkit, 2014). Apart from that the auditors will verify the integrity and honesty of the

management to determine the extent to which they can place reliance on the evidences and

representations made by them while conducting the audit of the financial statements of the

company.

Approach:

In order to conduct an effective audit of the financial statements of any organization it is

important to follow the generally accepted auditing standards that have been universally accepted

to be effective auditing standards (Dhand & Diab, 2015). The following procedures shall be

properly followed in the audit of the financial statements of an organization in order to express

an appropriate audit opinion on the financial statements of the organization:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT

I. Pre-engagement activities.

II. Preliminary audit panning and risk identification.

III. Risk assessment procedures to plan an audit.

IV. Internal control documentation and testing.

V. Decisions to use sampling techniques and the basis of such decision.

VI. Appropriate use of such sampling techniques to express an appropriate opinion on the

financial statements of the company.

VII. Performance of audit programs as planned taking into consideration the entity and its

activities.

VIII. Review of the audit findings.

IX. Expression of an opinion on the financial statements of the company on the basis of

the audit procedures and appraisal of the evidence collected during the course of the

audit.

Pre-engagement activities:

Obtaining an understanding of the entity and its environment of whose financial

statements are being audited in order to have the basis understanding about the financial

statements of the company. It is essential to obtain necessary knowledge about the nature of the

entity and its business operations to conduct an audit effectively (Johnson, 2017). Apart from

obtaining an understanding about the entity and its environment it is equally important to assess

whether the management of the organization is honest and have necessary integrity to provide

information about the company and to what extent the auditors can place reliance on the

financial as well as non-financial information provided by the management. Accordingly, let us

conduct the pre-engagement activities to start the audit on the right note (Enget, 2015).

I. Pre-engagement activities.

II. Preliminary audit panning and risk identification.

III. Risk assessment procedures to plan an audit.

IV. Internal control documentation and testing.

V. Decisions to use sampling techniques and the basis of such decision.

VI. Appropriate use of such sampling techniques to express an appropriate opinion on the

financial statements of the company.

VII. Performance of audit programs as planned taking into consideration the entity and its

activities.

VIII. Review of the audit findings.

IX. Expression of an opinion on the financial statements of the company on the basis of

the audit procedures and appraisal of the evidence collected during the course of the

audit.

Pre-engagement activities:

Obtaining an understanding of the entity and its environment of whose financial

statements are being audited in order to have the basis understanding about the financial

statements of the company. It is essential to obtain necessary knowledge about the nature of the

entity and its business operations to conduct an audit effectively (Johnson, 2017). Apart from

obtaining an understanding about the entity and its environment it is equally important to assess

whether the management of the organization is honest and have necessary integrity to provide

information about the company and to what extent the auditors can place reliance on the

financial as well as non-financial information provided by the management. Accordingly, let us

conduct the pre-engagement activities to start the audit on the right note (Enget, 2015).

8AUDIT

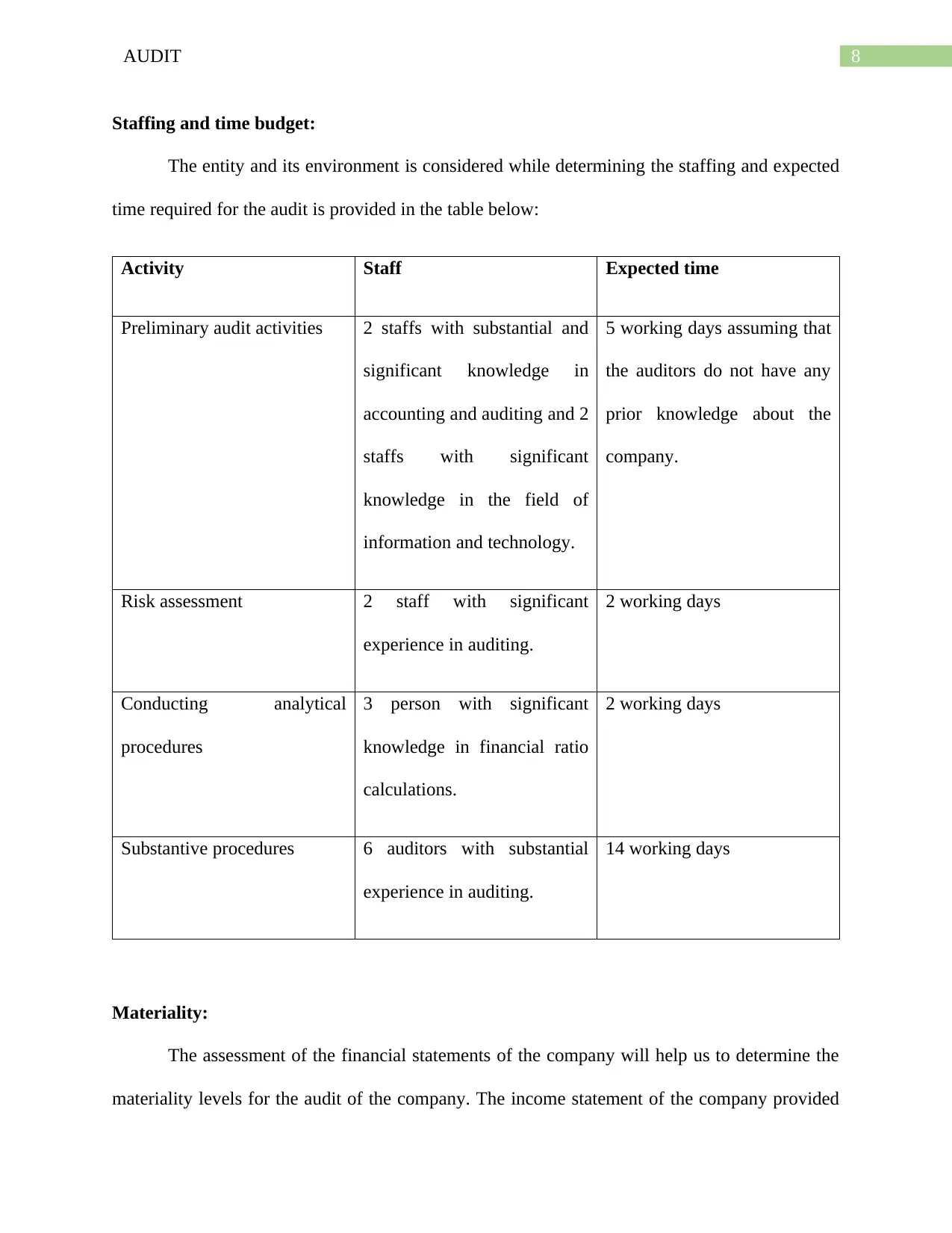

Staffing and time budget:

The entity and its environment is considered while determining the staffing and expected

time required for the audit is provided in the table below:

Activity Staff Expected time

Preliminary audit activities 2 staffs with substantial and

significant knowledge in

accounting and auditing and 2

staffs with significant

knowledge in the field of

information and technology.

5 working days assuming that

the auditors do not have any

prior knowledge about the

company.

Risk assessment 2 staff with significant

experience in auditing.

2 working days

Conducting analytical

procedures

3 person with significant

knowledge in financial ratio

calculations.

2 working days

Substantive procedures 6 auditors with substantial

experience in auditing.

14 working days

Materiality:

The assessment of the financial statements of the company will help us to determine the

materiality levels for the audit of the company. The income statement of the company provided

Staffing and time budget:

The entity and its environment is considered while determining the staffing and expected

time required for the audit is provided in the table below:

Activity Staff Expected time

Preliminary audit activities 2 staffs with substantial and

significant knowledge in

accounting and auditing and 2

staffs with significant

knowledge in the field of

information and technology.

5 working days assuming that

the auditors do not have any

prior knowledge about the

company.

Risk assessment 2 staff with significant

experience in auditing.

2 working days

Conducting analytical

procedures

3 person with significant

knowledge in financial ratio

calculations.

2 working days

Substantive procedures 6 auditors with substantial

experience in auditing.

14 working days

Materiality:

The assessment of the financial statements of the company will help us to determine the

materiality levels for the audit of the company. The income statement of the company provided

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT

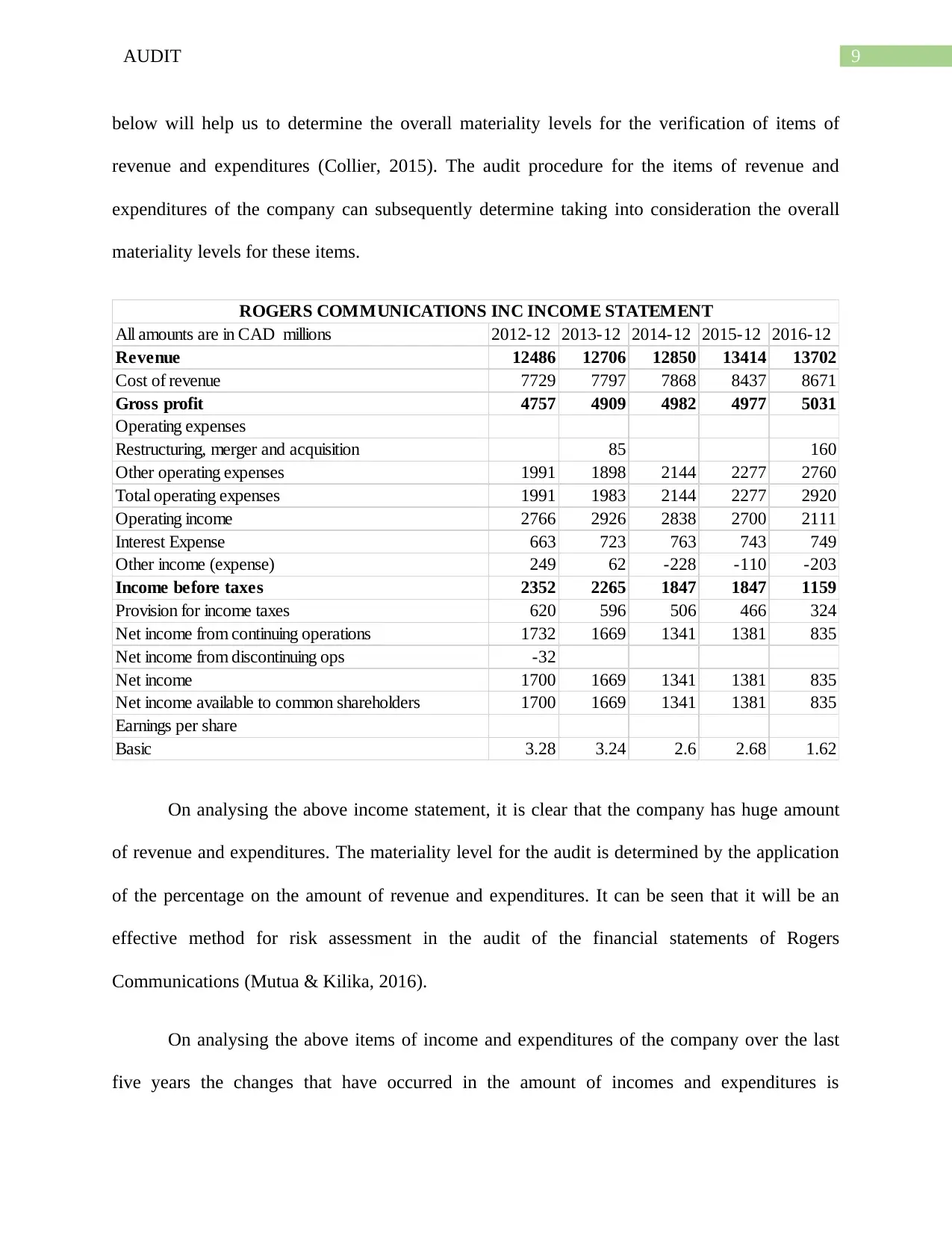

below will help us to determine the overall materiality levels for the verification of items of

revenue and expenditures (Collier, 2015). The audit procedure for the items of revenue and

expenditures of the company can subsequently determine taking into consideration the overall

materiality levels for these items.

All amounts are in CAD millions 2012-12 2013-12 2014-12 2015-12 2016-12

Revenue 12486 12706 12850 13414 13702

Cost of revenue 7729 7797 7868 8437 8671

Gross profit 4757 4909 4982 4977 5031

Operating expenses

Restructuring, merger and acquisition 85 160

Other operating expenses 1991 1898 2144 2277 2760

Total operating expenses 1991 1983 2144 2277 2920

Operating income 2766 2926 2838 2700 2111

Interest Expense 663 723 763 743 749

Other income (expense) 249 62 -228 -110 -203

Income before taxes 2352 2265 1847 1847 1159

Provision for income taxes 620 596 506 466 324

Net income from continuing operations 1732 1669 1341 1381 835

Net income from discontinuing ops -32

Net income 1700 1669 1341 1381 835

Net income available to common shareholders 1700 1669 1341 1381 835

Earnings per share

Basic 3.28 3.24 2.6 2.68 1.62

ROGERS COMMUNICATIONS INC INCOME STATEMENT

On analysing the above income statement, it is clear that the company has huge amount

of revenue and expenditures. The materiality level for the audit is determined by the application

of the percentage on the amount of revenue and expenditures. It can be seen that it will be an

effective method for risk assessment in the audit of the financial statements of Rogers

Communications (Mutua & Kilika, 2016).

On analysing the above items of income and expenditures of the company over the last

five years the changes that have occurred in the amount of incomes and expenditures is

below will help us to determine the overall materiality levels for the verification of items of

revenue and expenditures (Collier, 2015). The audit procedure for the items of revenue and

expenditures of the company can subsequently determine taking into consideration the overall

materiality levels for these items.

All amounts are in CAD millions 2012-12 2013-12 2014-12 2015-12 2016-12

Revenue 12486 12706 12850 13414 13702

Cost of revenue 7729 7797 7868 8437 8671

Gross profit 4757 4909 4982 4977 5031

Operating expenses

Restructuring, merger and acquisition 85 160

Other operating expenses 1991 1898 2144 2277 2760

Total operating expenses 1991 1983 2144 2277 2920

Operating income 2766 2926 2838 2700 2111

Interest Expense 663 723 763 743 749

Other income (expense) 249 62 -228 -110 -203

Income before taxes 2352 2265 1847 1847 1159

Provision for income taxes 620 596 506 466 324

Net income from continuing operations 1732 1669 1341 1381 835

Net income from discontinuing ops -32

Net income 1700 1669 1341 1381 835

Net income available to common shareholders 1700 1669 1341 1381 835

Earnings per share

Basic 3.28 3.24 2.6 2.68 1.62

ROGERS COMMUNICATIONS INC INCOME STATEMENT

On analysing the above income statement, it is clear that the company has huge amount

of revenue and expenditures. The materiality level for the audit is determined by the application

of the percentage on the amount of revenue and expenditures. It can be seen that it will be an

effective method for risk assessment in the audit of the financial statements of Rogers

Communications (Mutua & Kilika, 2016).

On analysing the above items of income and expenditures of the company over the last

five years the changes that have occurred in the amount of incomes and expenditures is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT

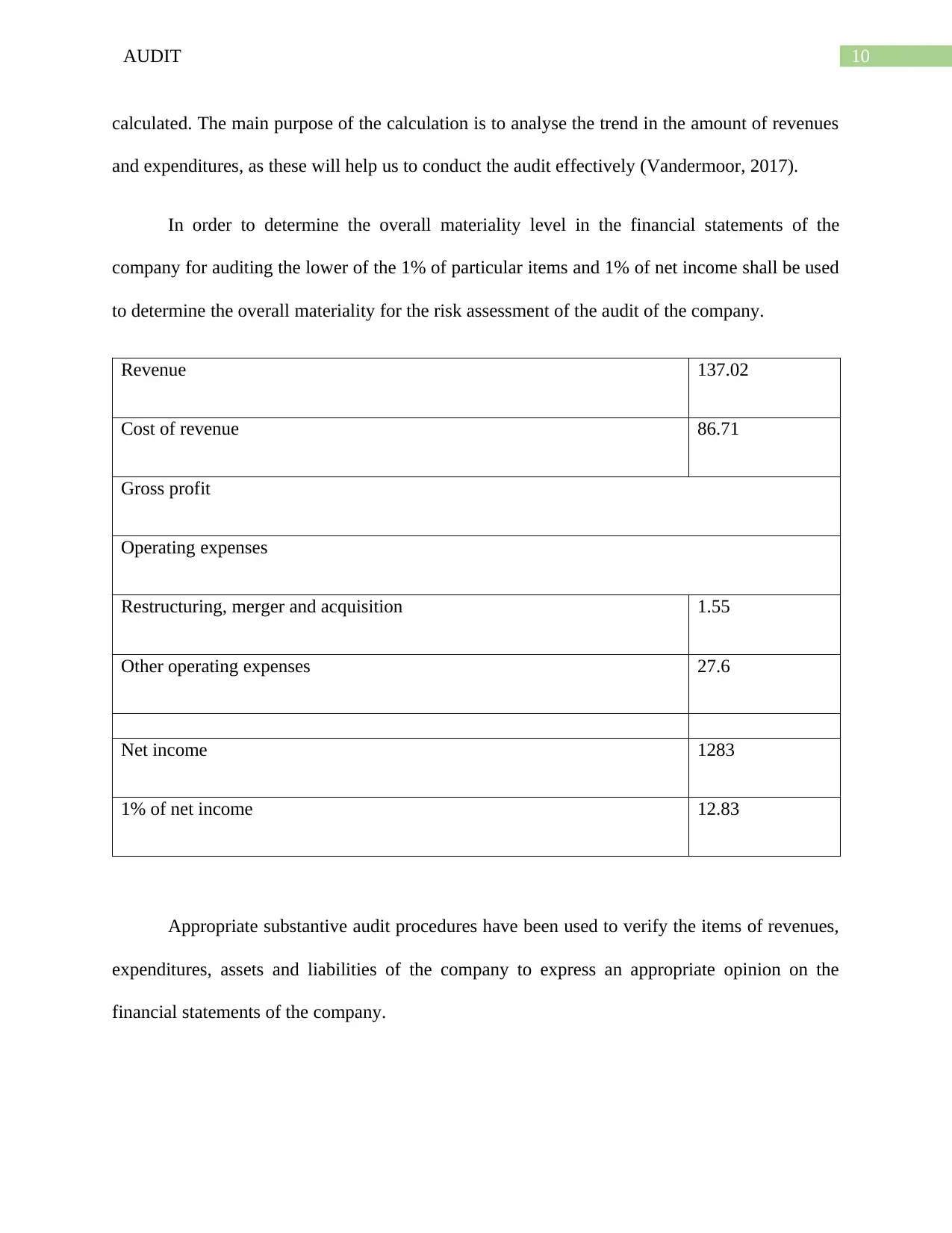

calculated. The main purpose of the calculation is to analyse the trend in the amount of revenues

and expenditures, as these will help us to conduct the audit effectively (Vandermoor, 2017).

In order to determine the overall materiality level in the financial statements of the

company for auditing the lower of the 1% of particular items and 1% of net income shall be used

to determine the overall materiality for the risk assessment of the audit of the company.

Revenue 137.02

Cost of revenue 86.71

Gross profit

Operating expenses

Restructuring, merger and acquisition 1.55

Other operating expenses 27.6

Net income 1283

1% of net income 12.83

Appropriate substantive audit procedures have been used to verify the items of revenues,

expenditures, assets and liabilities of the company to express an appropriate opinion on the

financial statements of the company.

calculated. The main purpose of the calculation is to analyse the trend in the amount of revenues

and expenditures, as these will help us to conduct the audit effectively (Vandermoor, 2017).

In order to determine the overall materiality level in the financial statements of the

company for auditing the lower of the 1% of particular items and 1% of net income shall be used

to determine the overall materiality for the risk assessment of the audit of the company.

Revenue 137.02

Cost of revenue 86.71

Gross profit

Operating expenses

Restructuring, merger and acquisition 1.55

Other operating expenses 27.6

Net income 1283

1% of net income 12.83

Appropriate substantive audit procedures have been used to verify the items of revenues,

expenditures, assets and liabilities of the company to express an appropriate opinion on the

financial statements of the company.

11AUDIT

Internal controls within the company:

The auditors to assess their appropriateness and correctness shall verify the internal

controls, which have been installed within the organizations, properly. In case of Rogers

Communications, the company has installed number of internal controls that have been up-dated

at periodic intervals to ensure their effectiveness and efficiency (Young & Waterhouse, 2015).

The digital employee cards will help us to track the actual attendance of the employees and

accordingly, the payment of salaries and wages to the employees can be verified to assess the

correctness of the accounting treatment and financial disclosure in the financial statements of the

company for the item of salaries and wages of the company. The company has maintain clear

line of separation in duty and have segregated the responsibilities of different employees and

workers including the management thus, the auditors will not find it difficult to determine the

employees responsible for different works and jobs within the organization and accordingly, will

be able to conduct the audit properly (Sorunke, 2016). The employees have also been rotated by

the management at periodical intervals to reduce the possibility of frauds by ensuring that an

employee do not get the chance to collide with other employees to take carry out any unethical

acts at the expense of the company. The use of close circuit cameras within the office and factory

premises is also one of the methods to control and manage the functions within the organization

effectively. The management has a standard procedure to conduct through testing of these

internal controls to see whether these need any changes in order to be more effective that these

are at any point of time (Egbon et al., 2017). Apart from that, the company has separate

accounting departments that are responsible to maintain the books of accounts of the company.

The accrual basis of accounting and double entry system to record the accounting transactions

have been followed to maintain the books of accounts of the company. Apart from that, the

Internal controls within the company:

The auditors to assess their appropriateness and correctness shall verify the internal

controls, which have been installed within the organizations, properly. In case of Rogers

Communications, the company has installed number of internal controls that have been up-dated

at periodic intervals to ensure their effectiveness and efficiency (Young & Waterhouse, 2015).

The digital employee cards will help us to track the actual attendance of the employees and

accordingly, the payment of salaries and wages to the employees can be verified to assess the

correctness of the accounting treatment and financial disclosure in the financial statements of the

company for the item of salaries and wages of the company. The company has maintain clear

line of separation in duty and have segregated the responsibilities of different employees and

workers including the management thus, the auditors will not find it difficult to determine the

employees responsible for different works and jobs within the organization and accordingly, will

be able to conduct the audit properly (Sorunke, 2016). The employees have also been rotated by

the management at periodical intervals to reduce the possibility of frauds by ensuring that an

employee do not get the chance to collide with other employees to take carry out any unethical

acts at the expense of the company. The use of close circuit cameras within the office and factory

premises is also one of the methods to control and manage the functions within the organization

effectively. The management has a standard procedure to conduct through testing of these

internal controls to see whether these need any changes in order to be more effective that these

are at any point of time (Egbon et al., 2017). Apart from that, the company has separate

accounting departments that are responsible to maintain the books of accounts of the company.

The accrual basis of accounting and double entry system to record the accounting transactions

have been followed to maintain the books of accounts of the company. Apart from that, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.