Audit Risk Report - Analysis of DON & RUMPT Ltd. Financial Statements

VerifiedAdded on 2023/01/19

|5

|538

|55

Report

AI Summary

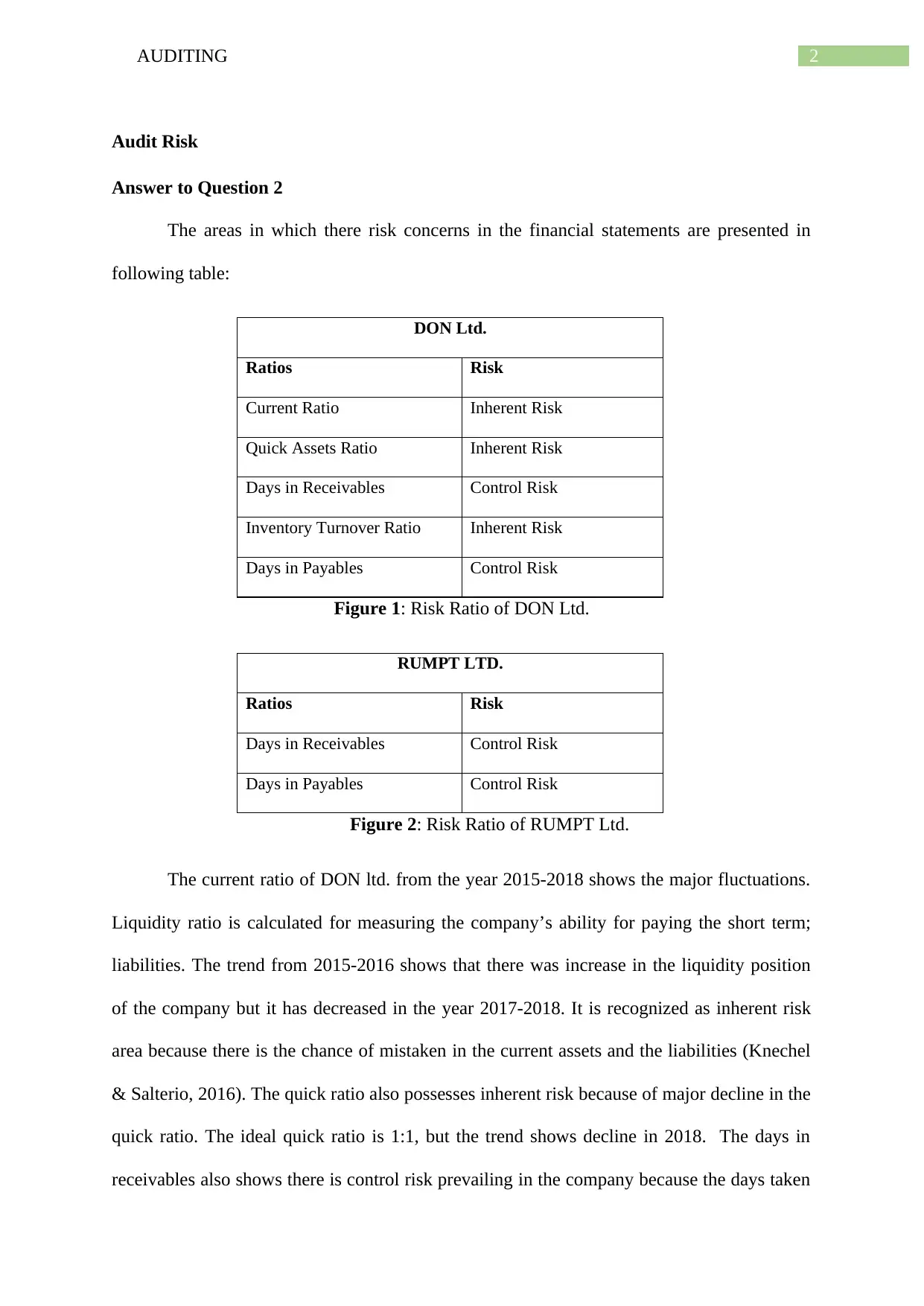

This report assesses the audit risks associated with DON Ltd. and RUMPT Ltd., two retail sportswear companies, for the financial year ending June 30, 2018. As part of the audit process conducted by Pran & Partners, the report analyzes key financial ratios, including current ratio, quick assets ratio, operating cash flow ratio, days in receivables, inventory turnover ratio, days in payables, and debt-to-equity ratio, over a four-year period. The analysis identifies areas of inherent and control risks, such as fluctuations in liquidity ratios and increasing days in receivables and payables, which could impact the accuracy of the financial statements. The report highlights specific risk areas for each company and provides insights into the potential for misstatements, emphasizing the importance of careful examination of these trends during the audit process. The report concludes by summarizing the key risks and recommending further investigation to ensure the financial statements are accurate and reliable.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.