Auditing and Assurance Report: ABC Learning Centre Analysis

VerifiedAdded on 2020/03/16

|16

|3544

|58

Report

AI Summary

This report provides an executive summary of auditing and assurance, focusing on how various auditing standards protect against market frauds. It emphasizes the role of auditing in identifying threats and evaluating risks, particularly for ABC Learning Centre. The report targets ASA 701 and ASA 570, highlighting their importance in assessing internal controls and ensuring business performance. It includes an introduction, background analysis of financial statements (income statement, balance sheet, and cash flow statements), and a detailed analysis of the financial data provided for ABC Learning Centre. The report also discusses the application of the going concern principle and the implications of non-compliance. The report concludes with recommendations for improving performance and achieving organizational goals. The financial statements analysis includes a cash flow projection and income statement and balance sheet comparison for the years 2011 and 2012.

AUDITING AND ASSURANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Current assignment is all about different auditing standards that helps an entity in

protecting against all the external market frauds takes places in an entity. Auditing is

regarded as the best suitable procedure that helps an entity in identifying all the threat takes

places in an entity. All kinds of risks are evaluated by the business owner by performing

audit in a particular financial year to know the performance of an entity as compared to all

other competitors in the similar industry. Auditing can be performed by appointing two kinds

of auditors such as internal as well as external auditors. Internal auditors work ii an entity as a

normal employee and external auditor is appointed by the government to conduct the audit of

the business and verifying all the business operations through unbiased ways. Current report

targets various standards of auditing such as ASA 701 and 570 in eliminating all the

deficiency lies in the current business entity. These auditing standards acts as a principle in

testing the capability of the internal controls of the business that reflects all the procedures in

processing various business transactions takes places in an entity. These auditing principles

will guide ABC learning centre to improve its entire performance within a short span of time

to achieve all the goals and the objectives in enhancing the firm’s productivity.

2

Current assignment is all about different auditing standards that helps an entity in

protecting against all the external market frauds takes places in an entity. Auditing is

regarded as the best suitable procedure that helps an entity in identifying all the threat takes

places in an entity. All kinds of risks are evaluated by the business owner by performing

audit in a particular financial year to know the performance of an entity as compared to all

other competitors in the similar industry. Auditing can be performed by appointing two kinds

of auditors such as internal as well as external auditors. Internal auditors work ii an entity as a

normal employee and external auditor is appointed by the government to conduct the audit of

the business and verifying all the business operations through unbiased ways. Current report

targets various standards of auditing such as ASA 701 and 570 in eliminating all the

deficiency lies in the current business entity. These auditing standards acts as a principle in

testing the capability of the internal controls of the business that reflects all the procedures in

processing various business transactions takes places in an entity. These auditing principles

will guide ABC learning centre to improve its entire performance within a short span of time

to achieve all the goals and the objectives in enhancing the firm’s productivity.

2

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................1

Background................................................................................................................................1

Analysis......................................................................................................................................3

Research.....................................................................................................................................8

Recommendation......................................................................................................................10

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

INTRODUCTION......................................................................................................................1

Background................................................................................................................................1

Analysis......................................................................................................................................3

Research.....................................................................................................................................8

Recommendation......................................................................................................................10

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Auditing play an integral role in an entity in considering all the strengths and

weaknesses in an entity by applying various tools and techniques in auditing procedures.

Auditing in an important approach used by all the business concern in overcoming all the

issues currently faced by an entity (Simnett, Carson and Vanstraelen, 2016). ABC learning

centre has selected for the current assignment whose financial and non-monetary

performance has tested in this assignment by taking help of various auditing standards such

as ASA 570. ASA 701 has comes into existence by replacing old standard of ASA 570 for the

going concern concept applied in testing the efficiency of an entity. This assignment explains

all kinds of auditing issues faced by an entity due to the collapse of their business enterprise.

Various reasons for the existence of all auditing issues have explained in the current report.

Auditing issues have explained by focusing on the three major kinds of financial statements

such as income statement, balanced sheet and cash flow statements of the business entity.

BACKGROUND

Auditing is an examination of the financial statements of an entity which includes

income statements, balance sheets, cash flow statements and statement of changes in equity

(Brusca, Caperchione, Cohen and Rossi,eds., 2016). An auditor verifies all such documents

by expressing the true and fair view by evaluating all the financial documents of an entity.

These documents are analyzed by the statutory auditor in expressing unbiased decisions.

Every entity is required to audit its business once in a financial year to identify all the issues

faced by an entity (Brousseau, Bédard and Vanstraelen, 2016). Auditing is an independent

examination of accounting books of accounts of an enterprise that includes all the business

vouchers, financial statements, valuation reports of all the property held by the business,

investment details (Knechel and Salterio, 2016). It is a process which has various steps such

as knowing details about the client’s organization such as nature of the business, size of

business, product details to plan the audit procedure according to the information generated

from the enterprise owner (William Jr, Glover and Prawitt, 2016). After getting enough

information from the client, next phase is to plan audit strategies to collect data from the

business in identifying all the prospective frauds and errors (Boone and et. al., 2017). Field

work covered after crafting strategies in which auditors and its staff will visit the business of

an entity in reviewing the internal controls of the firm by checking the total of all the ledgers,

verifying the accuracy of all the vouchers.

1

Auditing play an integral role in an entity in considering all the strengths and

weaknesses in an entity by applying various tools and techniques in auditing procedures.

Auditing in an important approach used by all the business concern in overcoming all the

issues currently faced by an entity (Simnett, Carson and Vanstraelen, 2016). ABC learning

centre has selected for the current assignment whose financial and non-monetary

performance has tested in this assignment by taking help of various auditing standards such

as ASA 570. ASA 701 has comes into existence by replacing old standard of ASA 570 for the

going concern concept applied in testing the efficiency of an entity. This assignment explains

all kinds of auditing issues faced by an entity due to the collapse of their business enterprise.

Various reasons for the existence of all auditing issues have explained in the current report.

Auditing issues have explained by focusing on the three major kinds of financial statements

such as income statement, balanced sheet and cash flow statements of the business entity.

BACKGROUND

Auditing is an examination of the financial statements of an entity which includes

income statements, balance sheets, cash flow statements and statement of changes in equity

(Brusca, Caperchione, Cohen and Rossi,eds., 2016). An auditor verifies all such documents

by expressing the true and fair view by evaluating all the financial documents of an entity.

These documents are analyzed by the statutory auditor in expressing unbiased decisions.

Every entity is required to audit its business once in a financial year to identify all the issues

faced by an entity (Brousseau, Bédard and Vanstraelen, 2016). Auditing is an independent

examination of accounting books of accounts of an enterprise that includes all the business

vouchers, financial statements, valuation reports of all the property held by the business,

investment details (Knechel and Salterio, 2016). It is a process which has various steps such

as knowing details about the client’s organization such as nature of the business, size of

business, product details to plan the audit procedure according to the information generated

from the enterprise owner (William Jr, Glover and Prawitt, 2016). After getting enough

information from the client, next phase is to plan audit strategies to collect data from the

business in identifying all the prospective frauds and errors (Boone and et. al., 2017). Field

work covered after crafting strategies in which auditors and its staff will visit the business of

an entity in reviewing the internal controls of the firm by checking the total of all the ledgers,

verifying the accuracy of all the vouchers.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

New standard of auditing has come into existence due to the severity of the global

financial crisis takes places in the external business environment (Piscopo, 2016). The new

auditing standard has come into bigger picture by making changes in the ASA 570 for going

concern principle. ABC learning centre has not followed the principles of the going concern

auditing principle. According to this principle, the survival of an entity is assumed as

indefinite life of years. But due to violation of the principle, the consequences need to face by

the business entity.

According to auditing standards of Australia 50, related to the concept of going

concern, under which total survival of the firm is measured as this principles assumes the

longer survival of the firm till its wound up (ASA 570, 2017). Violating this principle is not

beneficial for the firm as collapsing ABC learning style before the stipulated time period

creates complexities for all the internal as well external stakeholders of an enterprise. The

current standard ASA 570 is apples to different entities which will be checked by an auditor

during its auditing procedures (Thomé, Shar, Bianculli and Briand, 2017). It is applicable on

the firm who is registered under corporation’s act 2001 whose financial audit is conducted by

the business concern by generating financial reports of the firm and another requirement of

this act is to audit the financial report of the business entity or analyzing all the financial

statements. Under this standard, assumption used by an auditor that business operations will

be conducted for the foreseeable future by taking all the accounting treatment of all the

transactions takes places in an entity.

Standards acts a benchmarking concept in which the performance of the business is

measured by an auditor that is related to the communicating key audit matters in the

independent auditor’s Report (Zarr, Cottrell and Merrill, 2017). Australian auditing standards

has applicable in reviewing the current matter. This committee is an independent committee

that takes all the decisions separately by taking views and opinions of all the members takes

places in an external entity. This approach cum standards comes into existence in 2015 (Risk

based evaluation, 2014). The legislative provisions used by the authority according to this

principle are reviewed as per legislative instruments act 2003 (Internal control, 2007). The

auditing standards worked in accordance with the financial reporting council which arouses

interests among all the users in complying with all the rules and the regulations of the current

standard.

2

financial crisis takes places in the external business environment (Piscopo, 2016). The new

auditing standard has come into bigger picture by making changes in the ASA 570 for going

concern principle. ABC learning centre has not followed the principles of the going concern

auditing principle. According to this principle, the survival of an entity is assumed as

indefinite life of years. But due to violation of the principle, the consequences need to face by

the business entity.

According to auditing standards of Australia 50, related to the concept of going

concern, under which total survival of the firm is measured as this principles assumes the

longer survival of the firm till its wound up (ASA 570, 2017). Violating this principle is not

beneficial for the firm as collapsing ABC learning style before the stipulated time period

creates complexities for all the internal as well external stakeholders of an enterprise. The

current standard ASA 570 is apples to different entities which will be checked by an auditor

during its auditing procedures (Thomé, Shar, Bianculli and Briand, 2017). It is applicable on

the firm who is registered under corporation’s act 2001 whose financial audit is conducted by

the business concern by generating financial reports of the firm and another requirement of

this act is to audit the financial report of the business entity or analyzing all the financial

statements. Under this standard, assumption used by an auditor that business operations will

be conducted for the foreseeable future by taking all the accounting treatment of all the

transactions takes places in an entity.

Standards acts a benchmarking concept in which the performance of the business is

measured by an auditor that is related to the communicating key audit matters in the

independent auditor’s Report (Zarr, Cottrell and Merrill, 2017). Australian auditing standards

has applicable in reviewing the current matter. This committee is an independent committee

that takes all the decisions separately by taking views and opinions of all the members takes

places in an external entity. This approach cum standards comes into existence in 2015 (Risk

based evaluation, 2014). The legislative provisions used by the authority according to this

principle are reviewed as per legislative instruments act 2003 (Internal control, 2007). The

auditing standards worked in accordance with the financial reporting council which arouses

interests among all the users in complying with all the rules and the regulations of the current

standard.

2

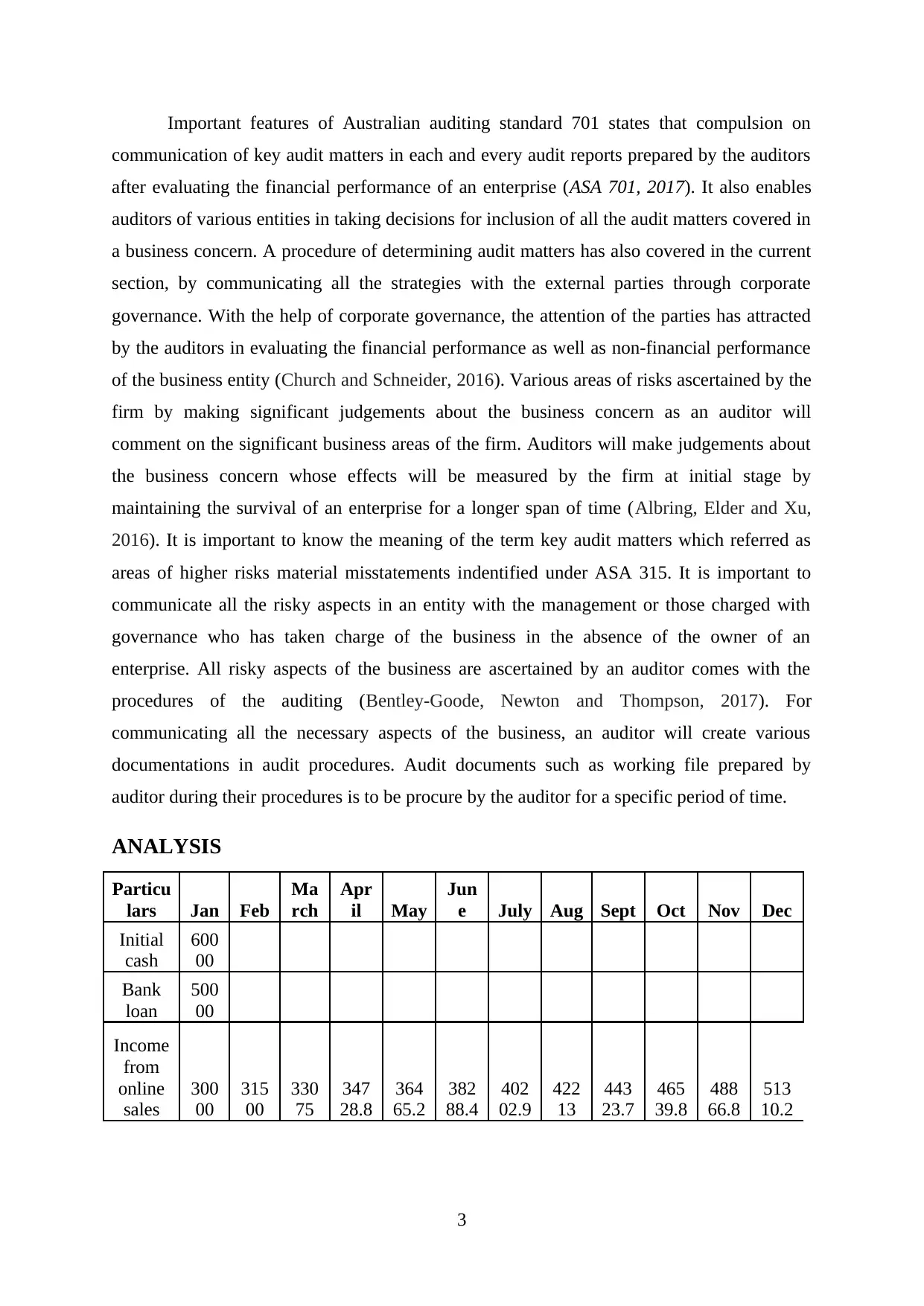

Important features of Australian auditing standard 701 states that compulsion on

communication of key audit matters in each and every audit reports prepared by the auditors

after evaluating the financial performance of an enterprise (ASA 701, 2017). It also enables

auditors of various entities in taking decisions for inclusion of all the audit matters covered in

a business concern. A procedure of determining audit matters has also covered in the current

section, by communicating all the strategies with the external parties through corporate

governance. With the help of corporate governance, the attention of the parties has attracted

by the auditors in evaluating the financial performance as well as non-financial performance

of the business entity (Church and Schneider, 2016). Various areas of risks ascertained by the

firm by making significant judgements about the business concern as an auditor will

comment on the significant business areas of the firm. Auditors will make judgements about

the business concern whose effects will be measured by the firm at initial stage by

maintaining the survival of an enterprise for a longer span of time (Albring, Elder and Xu,

2016). It is important to know the meaning of the term key audit matters which referred as

areas of higher risks material misstatements indentified under ASA 315. It is important to

communicate all the risky aspects in an entity with the management or those charged with

governance who has taken charge of the business in the absence of the owner of an

enterprise. All risky aspects of the business are ascertained by an auditor comes with the

procedures of the auditing (Bentley-Goode, Newton and Thompson, 2017). For

communicating all the necessary aspects of the business, an auditor will create various

documentations in audit procedures. Audit documents such as working file prepared by

auditor during their procedures is to be procure by the auditor for a specific period of time.

ANALYSIS

Particu

lars Jan Feb

Ma

rch

Apr

il May

Jun

e July Aug Sept Oct Nov Dec

Initial

cash

600

00

Bank

loan

500

00

Income

from

online

sales

300

00

315

00

330

75

347

28.8

364

65.2

382

88.4

402

02.9

422

13

443

23.7

465

39.8

488

66.8

513

10.2

3

communication of key audit matters in each and every audit reports prepared by the auditors

after evaluating the financial performance of an enterprise (ASA 701, 2017). It also enables

auditors of various entities in taking decisions for inclusion of all the audit matters covered in

a business concern. A procedure of determining audit matters has also covered in the current

section, by communicating all the strategies with the external parties through corporate

governance. With the help of corporate governance, the attention of the parties has attracted

by the auditors in evaluating the financial performance as well as non-financial performance

of the business entity (Church and Schneider, 2016). Various areas of risks ascertained by the

firm by making significant judgements about the business concern as an auditor will

comment on the significant business areas of the firm. Auditors will make judgements about

the business concern whose effects will be measured by the firm at initial stage by

maintaining the survival of an enterprise for a longer span of time (Albring, Elder and Xu,

2016). It is important to know the meaning of the term key audit matters which referred as

areas of higher risks material misstatements indentified under ASA 315. It is important to

communicate all the risky aspects in an entity with the management or those charged with

governance who has taken charge of the business in the absence of the owner of an

enterprise. All risky aspects of the business are ascertained by an auditor comes with the

procedures of the auditing (Bentley-Goode, Newton and Thompson, 2017). For

communicating all the necessary aspects of the business, an auditor will create various

documentations in audit procedures. Audit documents such as working file prepared by

auditor during their procedures is to be procure by the auditor for a specific period of time.

ANALYSIS

Particu

lars Jan Feb

Ma

rch

Apr

il May

Jun

e July Aug Sept Oct Nov Dec

Initial

cash

600

00

Bank

loan

500

00

Income

from

online

sales

300

00

315

00

330

75

347

28.8

364

65.2

382

88.4

402

02.9

422

13

443

23.7

465

39.8

488

66.8

513

10.2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

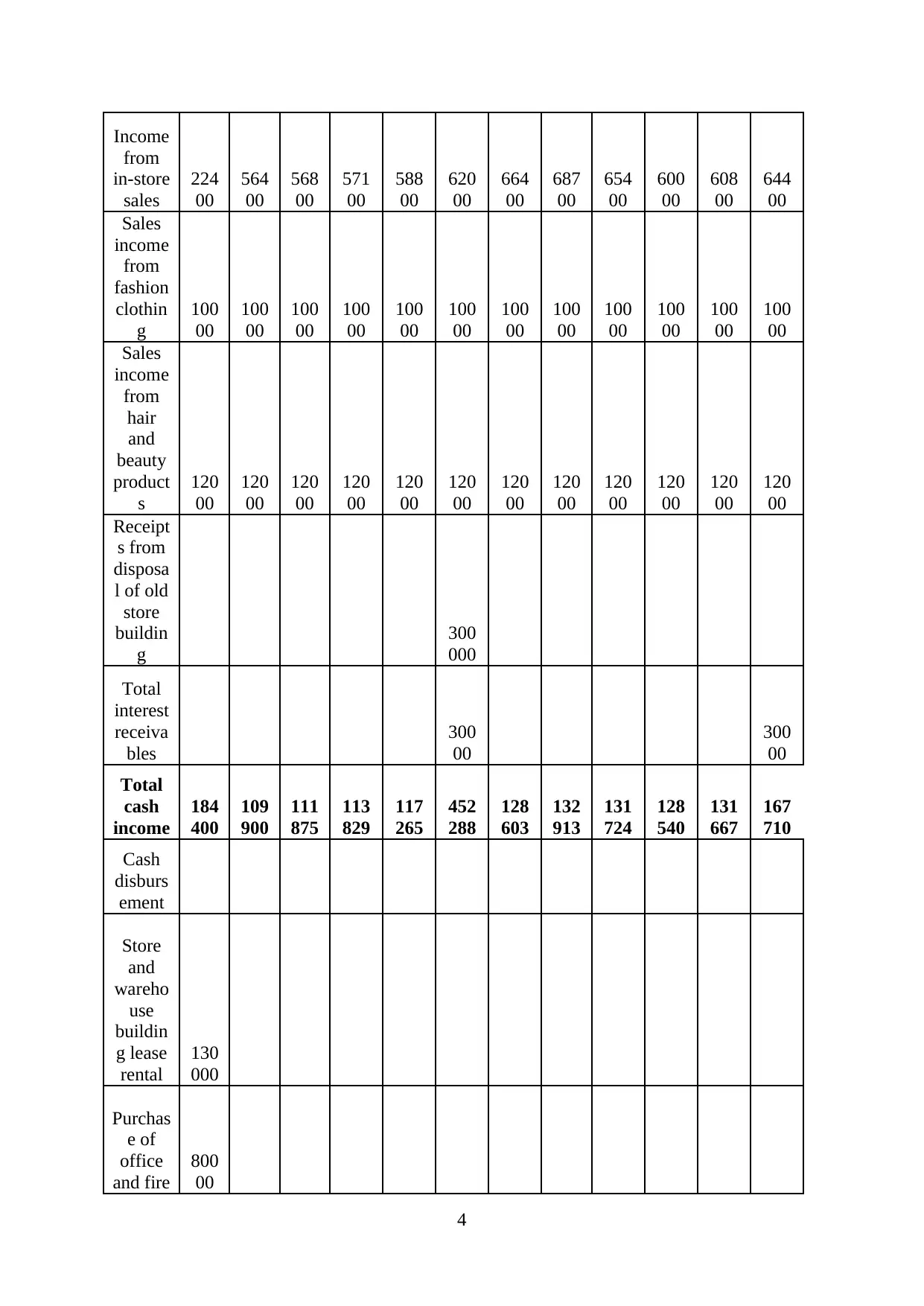

Income

from

in-store

sales

224

00

564

00

568

00

571

00

588

00

620

00

664

00

687

00

654

00

600

00

608

00

644

00

Sales

income

from

fashion

clothin

g

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from

hair

and

beauty

product

s

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipt

s from

disposa

l of old

store

buildin

g

300

000

Total

interest

receiva

bles

300

00

300

00

Total

cash

income

184

400

109

900

111

875

113

829

117

265

452

288

128

603

132

913

131

724

128

540

131

667

167

710

Cash

disburs

ement

Store

and

wareho

use

buildin

g lease

rental

130

000

Purchas

e of

office

and fire

800

00

4

from

in-store

sales

224

00

564

00

568

00

571

00

588

00

620

00

664

00

687

00

654

00

600

00

608

00

644

00

Sales

income

from

fashion

clothin

g

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

100

00

Sales

income

from

hair

and

beauty

product

s

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

120

00

Receipt

s from

disposa

l of old

store

buildin

g

300

000

Total

interest

receiva

bles

300

00

300

00

Total

cash

income

184

400

109

900

111

875

113

829

117

265

452

288

128

603

132

913

131

724

128

540

131

667

167

710

Cash

disburs

ement

Store

and

wareho

use

buildin

g lease

rental

130

000

Purchas

e of

office

and fire

800

00

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

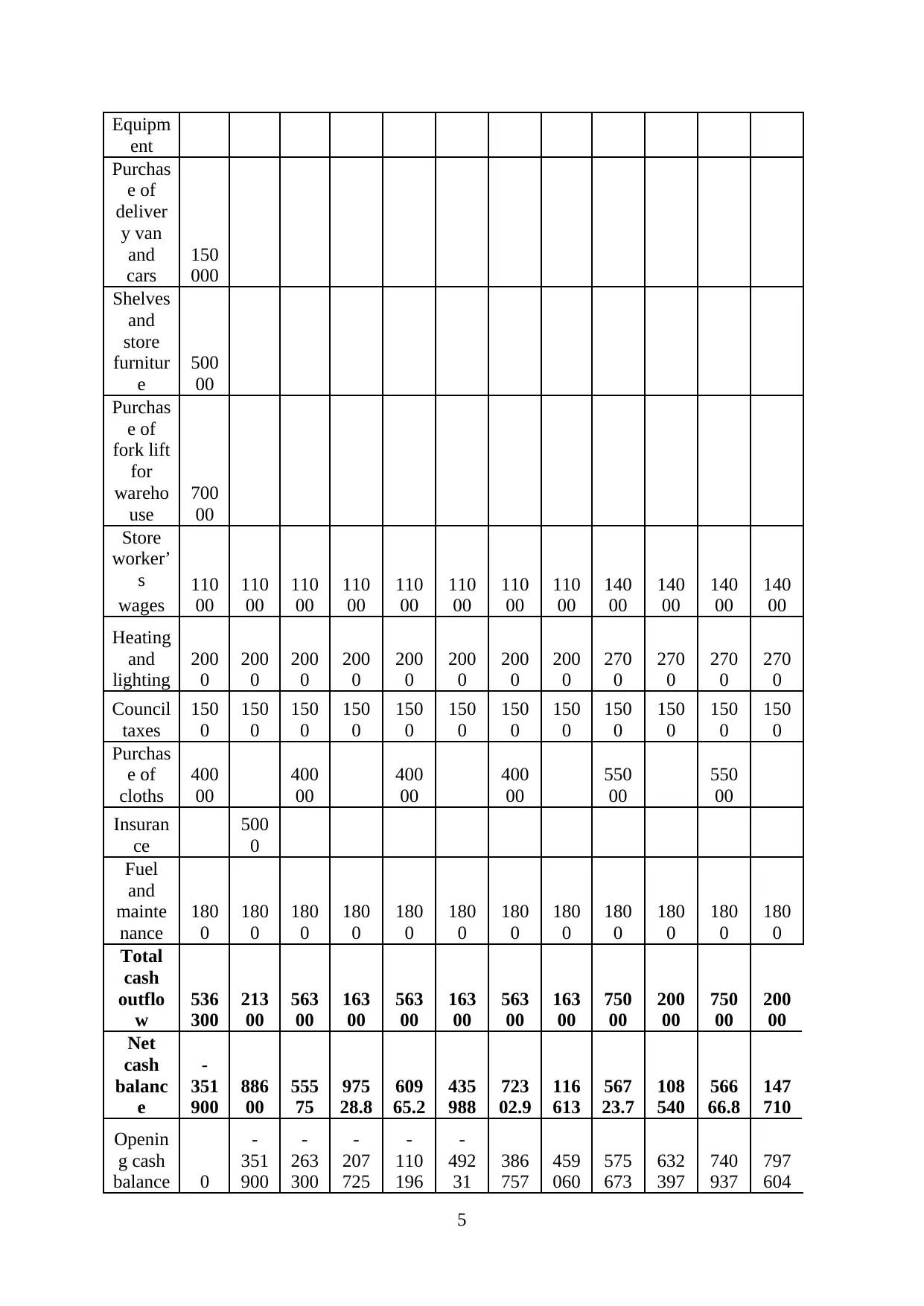

Equipm

ent

Purchas

e of

deliver

y van

and

cars

150

000

Shelves

and

store

furnitur

e

500

00

Purchas

e of

fork lift

for

wareho

use

700

00

Store

worker’

s 110

00

110

00

110

00

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00wages

Heating

and

lighting

200

0

200

0

200

0

200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchas

e of

cloths

400

00

400

00

400

00

400

00

550

00

550

00

Insuran

ce

500

0

Fuel

and

mainte

nance

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total

cash

outflo

w

536

300

213

00

563

00

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net

cash

balanc

e

-

351

900

886

00

555

75

975

28.8

609

65.2

435

988

723

02.9

116

613

567

23.7

108

540

566

66.8

147

710

Openin

g cash

balance 0

-

351

900

-

263

300

-

207

725

-

110

196

-

492

31

386

757

459

060

575

673

632

397

740

937

797

604

5

ent

Purchas

e of

deliver

y van

and

cars

150

000

Shelves

and

store

furnitur

e

500

00

Purchas

e of

fork lift

for

wareho

use

700

00

Store

worker’

s 110

00

110

00

110

00

110

00

110

00

110

00

110

00

110

00

140

00

140

00

140

00

140

00wages

Heating

and

lighting

200

0

200

0

200

0

200

0

200

0

200

0

200

0

200

0

270

0

270

0

270

0

270

0

Council

taxes

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

150

0

Purchas

e of

cloths

400

00

400

00

400

00

400

00

550

00

550

00

Insuran

ce

500

0

Fuel

and

mainte

nance

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

180

0

Total

cash

outflo

w

536

300

213

00

563

00

163

00

563

00

163

00

563

00

163

00

750

00

200

00

750

00

200

00

Net

cash

balanc

e

-

351

900

886

00

555

75

975

28.8

609

65.2

435

988

723

02.9

116

613

567

23.7

108

540

566

66.8

147

710

Openin

g cash

balance 0

-

351

900

-

263

300

-

207

725

-

110

196

-

492

31

386

757

459

060

575

673

632

397

740

937

797

604

5

Closin

g cash

balanc

e

-

351

900

-

263

300

-

207

725

-

110

196

-

492

31

386

757

459

060

575

673

632

397

740

937

797

604

945

314

ABC Learning centre

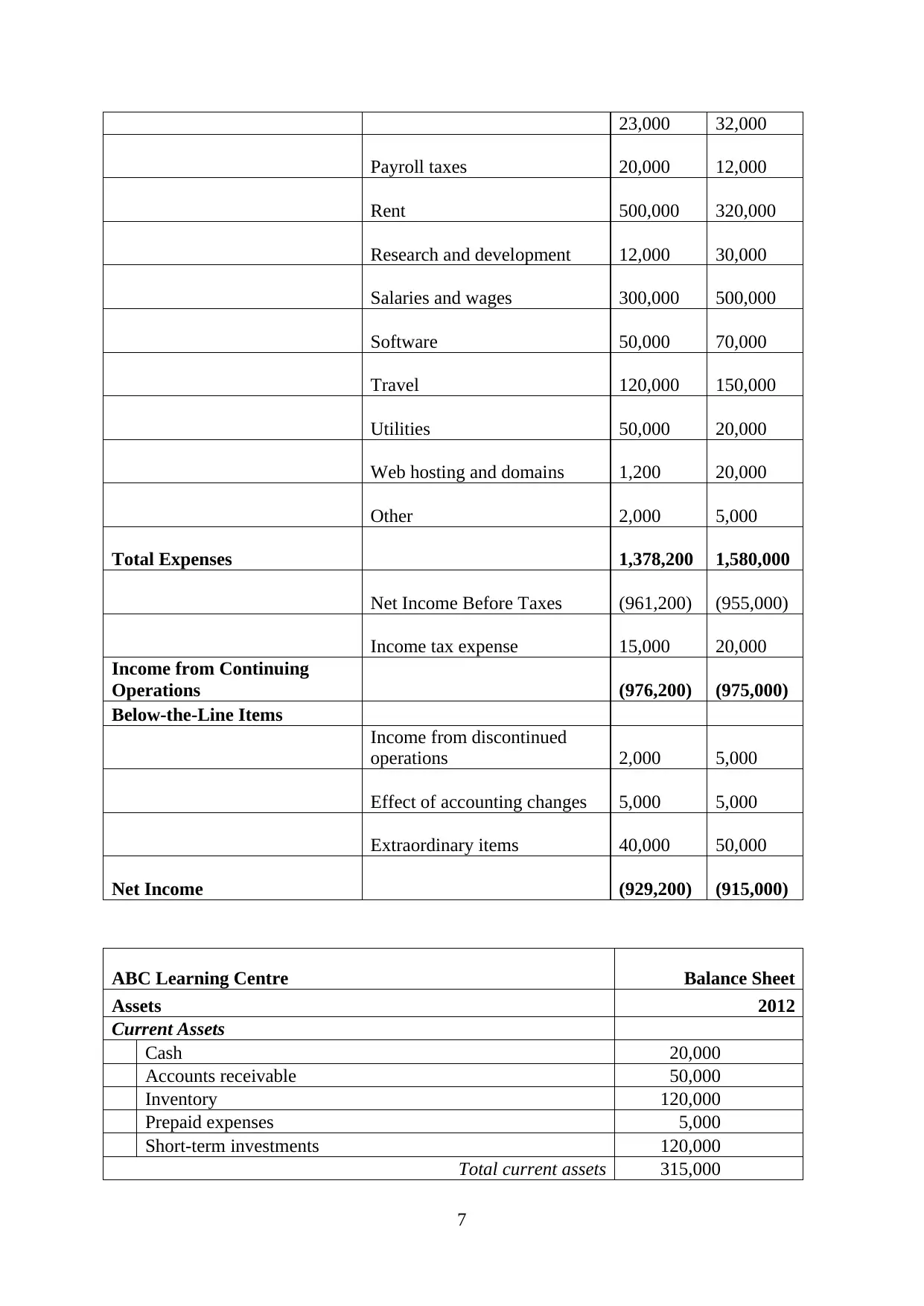

Income Statement

For the Years Ending [Dec 31, 2012 and Dec 31, 2011]

Revenue 2012 2011

Sales revenue 200,000 300,000

(Less sales returns and

allowances) 50,000 10,000

Service revenue 150,000 290,000

Interest revenue 5,000 10,000

Other revenue 12,000 15,000

Total Revenues 417,000 625,000

Expenses

Advertising 5,000 10,000

Bad debt 3,000 4,000

Commissions 12,000 20,000

Cost of goods sold 150,000 200,000

Depreciation 50,000 60,000

Employee benefits 12,000 15,000

Furniture and equipment 50,000 80,000

Insurance 12,000 25,000

Interest expense 4,000 2,000

Maintenance and repairs 2,000 5,000

Office supplies

6

g cash

balanc

e

-

351

900

-

263

300

-

207

725

-

110

196

-

492

31

386

757

459

060

575

673

632

397

740

937

797

604

945

314

ABC Learning centre

Income Statement

For the Years Ending [Dec 31, 2012 and Dec 31, 2011]

Revenue 2012 2011

Sales revenue 200,000 300,000

(Less sales returns and

allowances) 50,000 10,000

Service revenue 150,000 290,000

Interest revenue 5,000 10,000

Other revenue 12,000 15,000

Total Revenues 417,000 625,000

Expenses

Advertising 5,000 10,000

Bad debt 3,000 4,000

Commissions 12,000 20,000

Cost of goods sold 150,000 200,000

Depreciation 50,000 60,000

Employee benefits 12,000 15,000

Furniture and equipment 50,000 80,000

Insurance 12,000 25,000

Interest expense 4,000 2,000

Maintenance and repairs 2,000 5,000

Office supplies

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

23,000 32,000

Payroll taxes 20,000 12,000

Rent 500,000 320,000

Research and development 12,000 30,000

Salaries and wages 300,000 500,000

Software 50,000 70,000

Travel 120,000 150,000

Utilities 50,000 20,000

Web hosting and domains 1,200 20,000

Other 2,000 5,000

Total Expenses 1,378,200 1,580,000

Net Income Before Taxes (961,200) (955,000)

Income tax expense 15,000 20,000

Income from Continuing

Operations (976,200) (975,000)

Below-the-Line Items

Income from discontinued

operations 2,000 5,000

Effect of accounting changes 5,000 5,000

Extraordinary items 40,000 50,000

Net Income (929,200) (915,000)

ABC Learning Centre Balance Sheet

Assets 2012

Current Assets

Cash 20,000

Accounts receivable 50,000

Inventory 120,000

Prepaid expenses 5,000

Short-term investments 120,000

Total current assets 315,000

7

Payroll taxes 20,000 12,000

Rent 500,000 320,000

Research and development 12,000 30,000

Salaries and wages 300,000 500,000

Software 50,000 70,000

Travel 120,000 150,000

Utilities 50,000 20,000

Web hosting and domains 1,200 20,000

Other 2,000 5,000

Total Expenses 1,378,200 1,580,000

Net Income Before Taxes (961,200) (955,000)

Income tax expense 15,000 20,000

Income from Continuing

Operations (976,200) (975,000)

Below-the-Line Items

Income from discontinued

operations 2,000 5,000

Effect of accounting changes 5,000 5,000

Extraordinary items 40,000 50,000

Net Income (929,200) (915,000)

ABC Learning Centre Balance Sheet

Assets 2012

Current Assets

Cash 20,000

Accounts receivable 50,000

Inventory 120,000

Prepaid expenses 5,000

Short-term investments 120,000

Total current assets 315,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

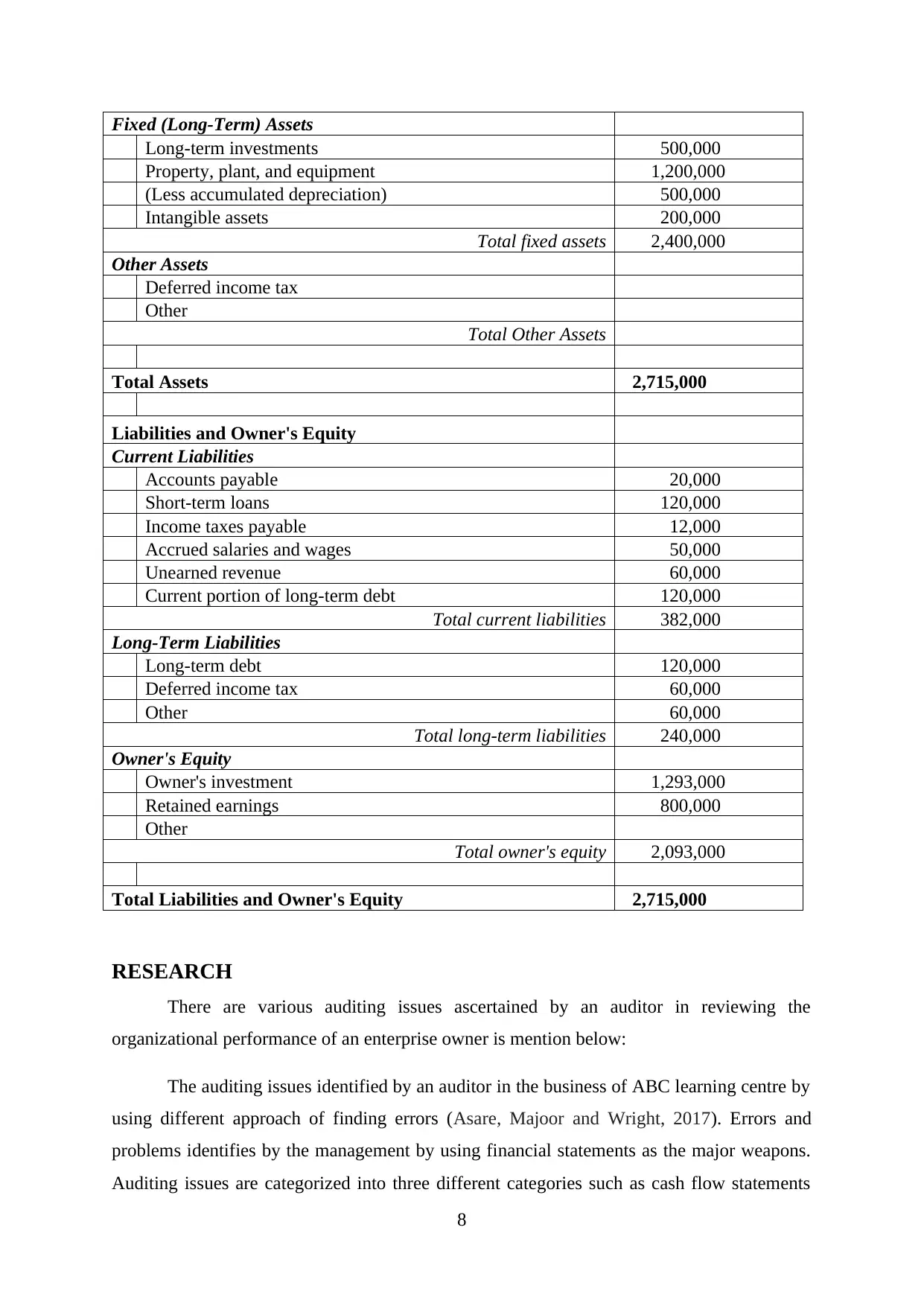

Fixed (Long-Term) Assets

Long-term investments 500,000

Property, plant, and equipment 1,200,000

(Less accumulated depreciation) 500,000

Intangible assets 200,000

Total fixed assets 2,400,000

Other Assets

Deferred income tax

Other

Total Other Assets

Total Assets 2,715,000

Liabilities and Owner's Equity

Current Liabilities

Accounts payable 20,000

Short-term loans 120,000

Income taxes payable 12,000

Accrued salaries and wages 50,000

Unearned revenue 60,000

Current portion of long-term debt 120,000

Total current liabilities 382,000

Long-Term Liabilities

Long-term debt 120,000

Deferred income tax 60,000

Other 60,000

Total long-term liabilities 240,000

Owner's Equity

Owner's investment 1,293,000

Retained earnings 800,000

Other

Total owner's equity 2,093,000

Total Liabilities and Owner's Equity 2,715,000

RESEARCH

There are various auditing issues ascertained by an auditor in reviewing the

organizational performance of an enterprise owner is mention below:

The auditing issues identified by an auditor in the business of ABC learning centre by

using different approach of finding errors (Asare, Majoor and Wright, 2017). Errors and

problems identifies by the management by using financial statements as the major weapons.

Auditing issues are categorized into three different categories such as cash flow statements

8

Long-term investments 500,000

Property, plant, and equipment 1,200,000

(Less accumulated depreciation) 500,000

Intangible assets 200,000

Total fixed assets 2,400,000

Other Assets

Deferred income tax

Other

Total Other Assets

Total Assets 2,715,000

Liabilities and Owner's Equity

Current Liabilities

Accounts payable 20,000

Short-term loans 120,000

Income taxes payable 12,000

Accrued salaries and wages 50,000

Unearned revenue 60,000

Current portion of long-term debt 120,000

Total current liabilities 382,000

Long-Term Liabilities

Long-term debt 120,000

Deferred income tax 60,000

Other 60,000

Total long-term liabilities 240,000

Owner's Equity

Owner's investment 1,293,000

Retained earnings 800,000

Other

Total owner's equity 2,093,000

Total Liabilities and Owner's Equity 2,715,000

RESEARCH

There are various auditing issues ascertained by an auditor in reviewing the

organizational performance of an enterprise owner is mention below:

The auditing issues identified by an auditor in the business of ABC learning centre by

using different approach of finding errors (Asare, Majoor and Wright, 2017). Errors and

problems identifies by the management by using financial statements as the major weapons.

Auditing issues are categorized into three different categories such as cash flow statements

8

issues, income statement issues ads last but not the least issues found in the positional

statements of the business entity. All accounting treatment deficiency has reflected in these

issues which lead to future consequences faced by an enterprise in the future.

Cash flow statement issues

Segregating all the cash expenditures and the revenues from the total revenues and

expenditures incurred in an entity (Chen, Knechel, Marisetty, Truong and Veeraraghavan,

2016). All the vouchers are to be evaluated by an entity as frauds in the vouchers is checked

by the auditors by verifying the same with all the entries posted in the cash budget. Entries in

the books of account does not matches with the cash budget is reviewed by taking consent of

the top management. In absence of any information from the management disclaimer of

opinion is filed by an auditor. Cash received by an entity is checked by authorized department

as fake vouchers can be created to create fraud with an entity. A petty cash book has also

checked with the normal cash book prepared in an entity as fraud can be done by using

various ways.

Income statement issues

Violation of accounting principles by recording revenues in the expense account to

show lower profit in front of the external authority in minimizing the tax obligations incurred

in an enterprise (Barranger and et. al., 2016). Tax is evaded by the firm by false recording of

the transactions as this will matches the trial balance of an entity but this can be ascertained

by an auditor in deep checking conducted by them. Audit staff will verify all the vouchers

against its entries in the books of account will ascertain the actual amount of revenues and

expenditures to present the accurate financial performance of an entity in front of the external

as well as internal parties.

Positional statement issues

Assets and liabilities are two important components for preparing the balance sheet

that means both assets and liabilities needs to be balanced. Valuation of the property is

checked properly as enterprise shows lower amount of property to eliminate its future tax

obligations (Lennox and DeFond, 2017). Inventory is valued according to IAS according to

which inventory is valued n lower value of costs or net realisable value but business owner

defrauds the authority by showing less amount of inventory by deflating all the users of the

external business environment.

9

statements of the business entity. All accounting treatment deficiency has reflected in these

issues which lead to future consequences faced by an enterprise in the future.

Cash flow statement issues

Segregating all the cash expenditures and the revenues from the total revenues and

expenditures incurred in an entity (Chen, Knechel, Marisetty, Truong and Veeraraghavan,

2016). All the vouchers are to be evaluated by an entity as frauds in the vouchers is checked

by the auditors by verifying the same with all the entries posted in the cash budget. Entries in

the books of account does not matches with the cash budget is reviewed by taking consent of

the top management. In absence of any information from the management disclaimer of

opinion is filed by an auditor. Cash received by an entity is checked by authorized department

as fake vouchers can be created to create fraud with an entity. A petty cash book has also

checked with the normal cash book prepared in an entity as fraud can be done by using

various ways.

Income statement issues

Violation of accounting principles by recording revenues in the expense account to

show lower profit in front of the external authority in minimizing the tax obligations incurred

in an enterprise (Barranger and et. al., 2016). Tax is evaded by the firm by false recording of

the transactions as this will matches the trial balance of an entity but this can be ascertained

by an auditor in deep checking conducted by them. Audit staff will verify all the vouchers

against its entries in the books of account will ascertain the actual amount of revenues and

expenditures to present the accurate financial performance of an entity in front of the external

as well as internal parties.

Positional statement issues

Assets and liabilities are two important components for preparing the balance sheet

that means both assets and liabilities needs to be balanced. Valuation of the property is

checked properly as enterprise shows lower amount of property to eliminate its future tax

obligations (Lennox and DeFond, 2017). Inventory is valued according to IAS according to

which inventory is valued n lower value of costs or net realisable value but business owner

defrauds the authority by showing less amount of inventory by deflating all the users of the

external business environment.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.