FPC007B: Financial Behaviour - Client Interview and Critical Analysis

VerifiedAdded on 2022/12/18

|16

|4007

|95

Report

AI Summary

This report presents a comprehensive analysis of client financial behaviour based on interviews with a financial advisor and a client service person. The analysis includes situational comparisons, behavioural assessments, and evaluations of the interviewees' handling of consumer interactions, drawing upon theoretical explanations of consumer choice and decision-making. The interviews reveal insights into client backgrounds, their issues, and the impact of past experiences on their financial decisions. The report identifies strengths and weaknesses in the interviewees' approaches and provides recommendations for improving client communication, counselling, and overall service delivery, emphasizing the importance of a client-centered approach and enhanced staff training to foster better financial outcomes.

Running head: FINANCIAL BEHAVIOUR

Financial Behaviour

Name of the Student

Name of the University

Author note

Financial Behaviour

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2FINANCIAL BEHAVIOUR

Part 1:

Interview of a financial advisor:

Attended by: Name of the financial advisor

Date: 03-Oct,2019 Time: 15:00

Questions Answers and notes

1. Client background/history

Can you provide the background

on the client's situation (back

story) and how it led to this

situation?

The client works in an IT company and is about to get a

retirement in the next month itself. He worked in an IT

company and has under 10 years two daughters and he

is about to retire in 15 years. He appointed me to assess

the current financial situation, the financial aspects

affecting the future of his children 9 their higher

education and weddings) and to understand the

intricacies of his retirement related investments. The

client, in the last few months is really worried about the

future of his daughters, after his retirement. Moreover,

he had previous losses at business investments and since

then he had not taken any investment decisions until

now, when he is planning his retirement life.

Part 1:

Interview of a financial advisor:

Attended by: Name of the financial advisor

Date: 03-Oct,2019 Time: 15:00

Questions Answers and notes

1. Client background/history

Can you provide the background

on the client's situation (back

story) and how it led to this

situation?

The client works in an IT company and is about to get a

retirement in the next month itself. He worked in an IT

company and has under 10 years two daughters and he

is about to retire in 15 years. He appointed me to assess

the current financial situation, the financial aspects

affecting the future of his children 9 their higher

education and weddings) and to understand the

intricacies of his retirement related investments. The

client, in the last few months is really worried about the

future of his daughters, after his retirement. Moreover,

he had previous losses at business investments and since

then he had not taken any investment decisions until

now, when he is planning his retirement life.

3FINANCIAL BEHAVIOUR

2. Outline of the situation

Can you outline the client’s

problem, issue or complaint that

has arisen with yourself or your

firm?

Who was involved?

While I tried to help with the various retirement plans,

in which he can invest from now and then after

investing a certain premium for 15 years – he can have a

stable source of income from the retirement fund, on a

regular basis after 15 years when he retires from his

profession. The client’s main problem with me arose

when he focussed the financial planning just on the

children’s future while I stressed the retirement plan to

be more effective for his older life. The issue was a

communication gap that I faced with my client in this

case and it was difficult to make him understand that

retirement would actually him and his wife to receive

regular income from the retirement fund without any

extra pay. The amount of the premium was a bit high

and he said that I cannot pressurize him ( which I was

not doing) to subscribe for the aforementioned

retirement plan, as he thinks a low investment for an

average retirement plan would be better for him as with

that he can support his daughters predominantly, after

his retirement.

3. Client behaviour

Can you describe the client’s

behaviour throughout the

situation?

The client’s behaviour, initially when we began the

interaction was very polite and adherent to the situation.

As the consultation sessions progressed – instead of

having a trust worthy relationship with me (his financial

advisor), his behaviours started to become very

disruptive. On a couple of situations, instead of listening

patiently for a bit with me – he started to act very

impatient with me and at certain points – he was naïve,

reluctant and verbally very aggressive. He was

countering most of the retirement solutions, I gave him

and started with a challenging behaviour towards me.

2. Outline of the situation

Can you outline the client’s

problem, issue or complaint that

has arisen with yourself or your

firm?

Who was involved?

While I tried to help with the various retirement plans,

in which he can invest from now and then after

investing a certain premium for 15 years – he can have a

stable source of income from the retirement fund, on a

regular basis after 15 years when he retires from his

profession. The client’s main problem with me arose

when he focussed the financial planning just on the

children’s future while I stressed the retirement plan to

be more effective for his older life. The issue was a

communication gap that I faced with my client in this

case and it was difficult to make him understand that

retirement would actually him and his wife to receive

regular income from the retirement fund without any

extra pay. The amount of the premium was a bit high

and he said that I cannot pressurize him ( which I was

not doing) to subscribe for the aforementioned

retirement plan, as he thinks a low investment for an

average retirement plan would be better for him as with

that he can support his daughters predominantly, after

his retirement.

3. Client behaviour

Can you describe the client’s

behaviour throughout the

situation?

The client’s behaviour, initially when we began the

interaction was very polite and adherent to the situation.

As the consultation sessions progressed – instead of

having a trust worthy relationship with me (his financial

advisor), his behaviours started to become very

disruptive. On a couple of situations, instead of listening

patiently for a bit with me – he started to act very

impatient with me and at certain points – he was naïve,

reluctant and verbally very aggressive. He was

countering most of the retirement solutions, I gave him

and started with a challenging behaviour towards me.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4FINANCIAL BEHAVIOUR

4. Your own and other employees’

behaviours

How did you feel during this

situation?

Can you describe your own and

other staff’s behaviour/reactions?

After receiving the complaint from my client I was

called for justification and I presented my point with

enough documents. It was very stressful situation in my

career. Numerous office colleges advice me to comply

with my client concerns and to make the financial plan

accordingly to avoid any further consequences.

5. Root cause

What do you believe is the root

cause of the problem?

He might have been involved with a severe loss due to

high volume direct capital investment, that is why he

might be panicking. I believe that, a sense of insecurity

regarding large volume capital investment is the main

reason behind his problem.

6. Impact

What was the impact on the client

from a perception, emotional and

financial perspective?

After facing a huge loss because of unplanned

investment on some other investment operations, a

permanent phobia might have developed in his mind

regarding a high capital direct investment.

7. Action

What would you have done

differently?

If I were in his place, I would rather invest my capital

with proper analytical understanding with rational

problem solving. In this case, while investing in

retirement plan – I would have thought of my own

future with my wife’s and used other funds to support

my children (if required).

8. Changes

What changes to staff training,

back office/business processes,

client service standards and/or

job roles have been undertaken to

reduce the chance of it re-

occurring?

More staff training must pertain to client

communication, skill development sessions in order to

interact and aid the client through a ‘financial’

counselling. In order to meet a high client servicing

standard – the more humanistic financial counselling

approach must be added.

4. Your own and other employees’

behaviours

How did you feel during this

situation?

Can you describe your own and

other staff’s behaviour/reactions?

After receiving the complaint from my client I was

called for justification and I presented my point with

enough documents. It was very stressful situation in my

career. Numerous office colleges advice me to comply

with my client concerns and to make the financial plan

accordingly to avoid any further consequences.

5. Root cause

What do you believe is the root

cause of the problem?

He might have been involved with a severe loss due to

high volume direct capital investment, that is why he

might be panicking. I believe that, a sense of insecurity

regarding large volume capital investment is the main

reason behind his problem.

6. Impact

What was the impact on the client

from a perception, emotional and

financial perspective?

After facing a huge loss because of unplanned

investment on some other investment operations, a

permanent phobia might have developed in his mind

regarding a high capital direct investment.

7. Action

What would you have done

differently?

If I were in his place, I would rather invest my capital

with proper analytical understanding with rational

problem solving. In this case, while investing in

retirement plan – I would have thought of my own

future with my wife’s and used other funds to support

my children (if required).

8. Changes

What changes to staff training,

back office/business processes,

client service standards and/or

job roles have been undertaken to

reduce the chance of it re-

occurring?

More staff training must pertain to client

communication, skill development sessions in order to

interact and aid the client through a ‘financial’

counselling. In order to meet a high client servicing

standard – the more humanistic financial counselling

approach must be added.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5FINANCIAL BEHAVIOUR

9. Current position

Based on the changes put in place,

what is different now?

The client is more secure and feels happy what is

problem is addressed. His dignity is lifted and he is

satisfied that we are addressing his problems in the most

apt way.

10. Client outcomes

How do the changes improve client

outcomes?

After developing the new retirement plans, he withdrew

his campaign. The changes reinforced communication

with the client, better decision making and choosing of

the right plan.

11. Staff outcomes

How do the changes improve the

employees’ work environment?

Reflection and evidence based practise received from

this life insurance case – would increase the morals of

the employee toards a more client cantered practise.

12. The adviser

How do you feel about the way

forward now?

I think in this case, company needs to increase the

mutual communication between employee and client

while having an unbiased standing. Like employee

trainings, client counselling will be also helpful in these

cases.

9. Current position

Based on the changes put in place,

what is different now?

The client is more secure and feels happy what is

problem is addressed. His dignity is lifted and he is

satisfied that we are addressing his problems in the most

apt way.

10. Client outcomes

How do the changes improve client

outcomes?

After developing the new retirement plans, he withdrew

his campaign. The changes reinforced communication

with the client, better decision making and choosing of

the right plan.

11. Staff outcomes

How do the changes improve the

employees’ work environment?

Reflection and evidence based practise received from

this life insurance case – would increase the morals of

the employee toards a more client cantered practise.

12. The adviser

How do you feel about the way

forward now?

I think in this case, company needs to increase the

mutual communication between employee and client

while having an unbiased standing. Like employee

trainings, client counselling will be also helpful in these

cases.

6FINANCIAL BEHAVIOUR

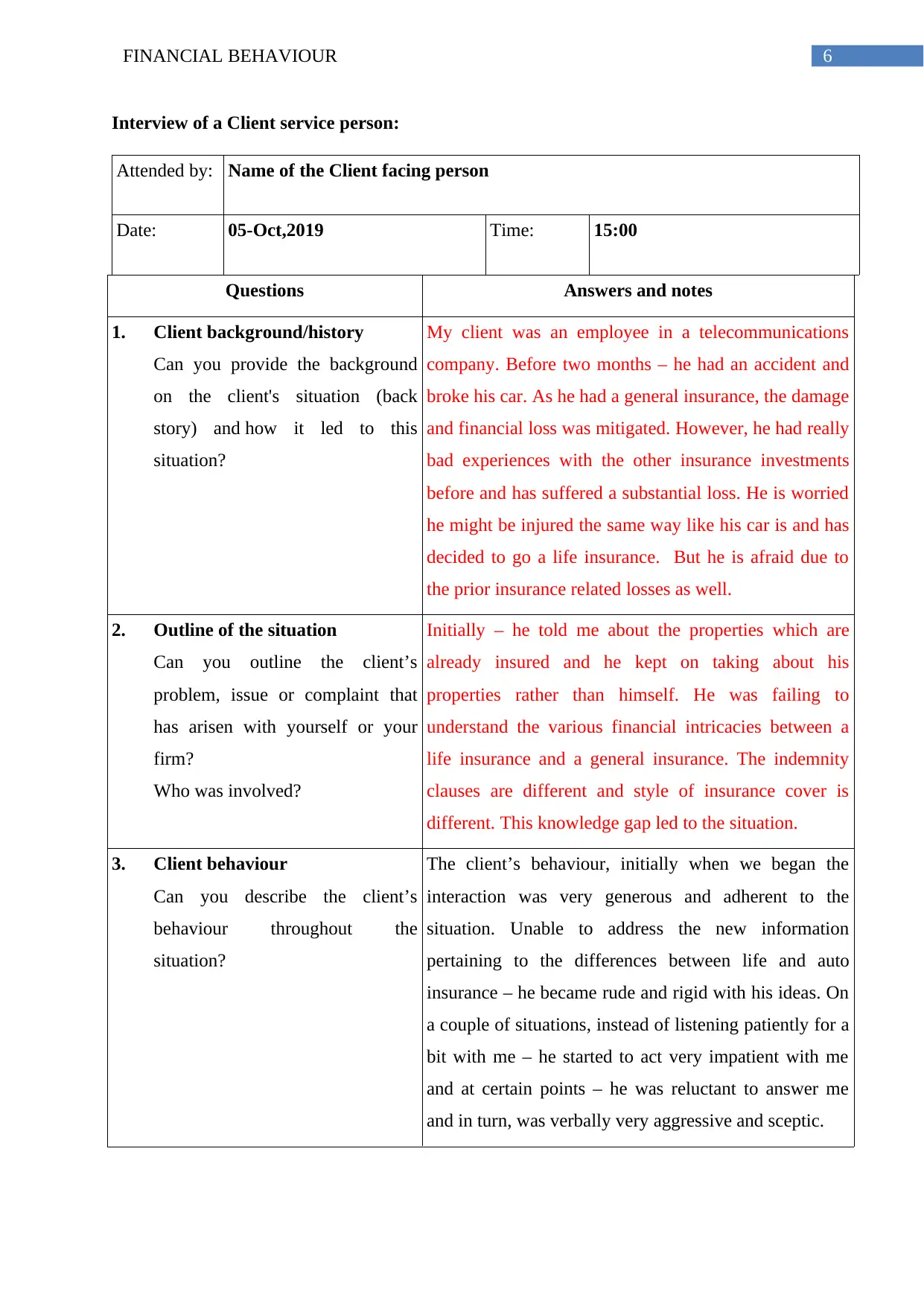

Interview of a Client service person:

Attended by: Name of the Client facing person

Date: 05-Oct,2019 Time: 15:00

Questions Answers and notes

1. Client background/history

Can you provide the background

on the client's situation (back

story) and how it led to this

situation?

My client was an employee in a telecommunications

company. Before two months – he had an accident and

broke his car. As he had a general insurance, the damage

and financial loss was mitigated. However, he had really

bad experiences with the other insurance investments

before and has suffered a substantial loss. He is worried

he might be injured the same way like his car is and has

decided to go a life insurance. But he is afraid due to

the prior insurance related losses as well.

2. Outline of the situation

Can you outline the client’s

problem, issue or complaint that

has arisen with yourself or your

firm?

Who was involved?

Initially – he told me about the properties which are

already insured and he kept on taking about his

properties rather than himself. He was failing to

understand the various financial intricacies between a

life insurance and a general insurance. The indemnity

clauses are different and style of insurance cover is

different. This knowledge gap led to the situation.

3. Client behaviour

Can you describe the client’s

behaviour throughout the

situation?

The client’s behaviour, initially when we began the

interaction was very generous and adherent to the

situation. Unable to address the new information

pertaining to the differences between life and auto

insurance – he became rude and rigid with his ideas. On

a couple of situations, instead of listening patiently for a

bit with me – he started to act very impatient with me

and at certain points – he was reluctant to answer me

and in turn, was verbally very aggressive and sceptic.

Interview of a Client service person:

Attended by: Name of the Client facing person

Date: 05-Oct,2019 Time: 15:00

Questions Answers and notes

1. Client background/history

Can you provide the background

on the client's situation (back

story) and how it led to this

situation?

My client was an employee in a telecommunications

company. Before two months – he had an accident and

broke his car. As he had a general insurance, the damage

and financial loss was mitigated. However, he had really

bad experiences with the other insurance investments

before and has suffered a substantial loss. He is worried

he might be injured the same way like his car is and has

decided to go a life insurance. But he is afraid due to

the prior insurance related losses as well.

2. Outline of the situation

Can you outline the client’s

problem, issue or complaint that

has arisen with yourself or your

firm?

Who was involved?

Initially – he told me about the properties which are

already insured and he kept on taking about his

properties rather than himself. He was failing to

understand the various financial intricacies between a

life insurance and a general insurance. The indemnity

clauses are different and style of insurance cover is

different. This knowledge gap led to the situation.

3. Client behaviour

Can you describe the client’s

behaviour throughout the

situation?

The client’s behaviour, initially when we began the

interaction was very generous and adherent to the

situation. Unable to address the new information

pertaining to the differences between life and auto

insurance – he became rude and rigid with his ideas. On

a couple of situations, instead of listening patiently for a

bit with me – he started to act very impatient with me

and at certain points – he was reluctant to answer me

and in turn, was verbally very aggressive and sceptic.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7FINANCIAL BEHAVIOUR

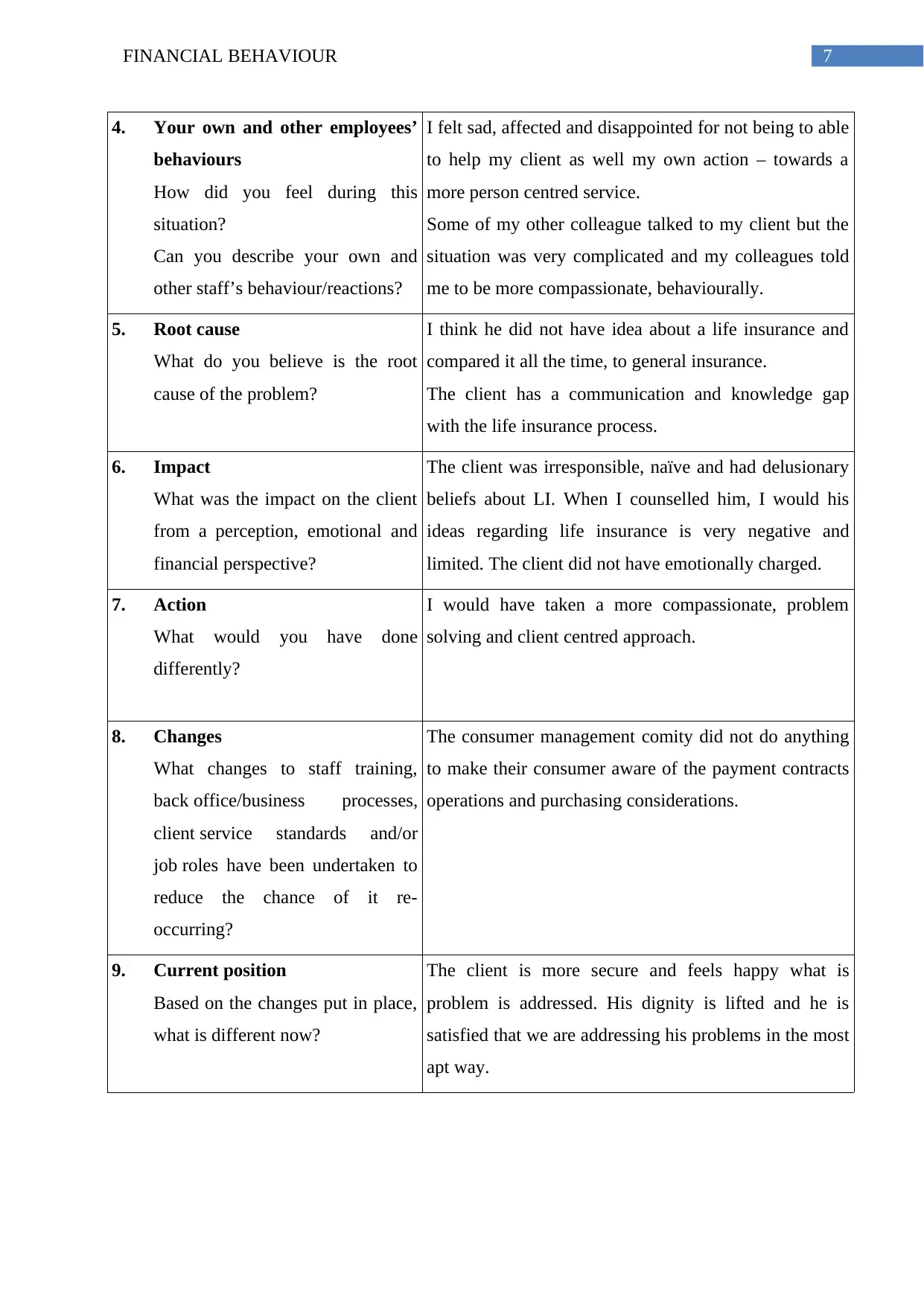

4. Your own and other employees’

behaviours

How did you feel during this

situation?

Can you describe your own and

other staff’s behaviour/reactions?

I felt sad, affected and disappointed for not being to able

to help my client as well my own action – towards a

more person centred service.

Some of my other colleague talked to my client but the

situation was very complicated and my colleagues told

me to be more compassionate, behaviourally.

5. Root cause

What do you believe is the root

cause of the problem?

I think he did not have idea about a life insurance and

compared it all the time, to general insurance.

The client has a communication and knowledge gap

with the life insurance process.

6. Impact

What was the impact on the client

from a perception, emotional and

financial perspective?

The client was irresponsible, naïve and had delusionary

beliefs about LI. When I counselled him, I would his

ideas regarding life insurance is very negative and

limited. The client did not have emotionally charged.

7. Action

What would you have done

differently?

I would have taken a more compassionate, problem

solving and client centred approach.

8. Changes

What changes to staff training,

back office/business processes,

client service standards and/or

job roles have been undertaken to

reduce the chance of it re-

occurring?

The consumer management comity did not do anything

to make their consumer aware of the payment contracts

operations and purchasing considerations.

9. Current position

Based on the changes put in place,

what is different now?

The client is more secure and feels happy what is

problem is addressed. His dignity is lifted and he is

satisfied that we are addressing his problems in the most

apt way.

4. Your own and other employees’

behaviours

How did you feel during this

situation?

Can you describe your own and

other staff’s behaviour/reactions?

I felt sad, affected and disappointed for not being to able

to help my client as well my own action – towards a

more person centred service.

Some of my other colleague talked to my client but the

situation was very complicated and my colleagues told

me to be more compassionate, behaviourally.

5. Root cause

What do you believe is the root

cause of the problem?

I think he did not have idea about a life insurance and

compared it all the time, to general insurance.

The client has a communication and knowledge gap

with the life insurance process.

6. Impact

What was the impact on the client

from a perception, emotional and

financial perspective?

The client was irresponsible, naïve and had delusionary

beliefs about LI. When I counselled him, I would his

ideas regarding life insurance is very negative and

limited. The client did not have emotionally charged.

7. Action

What would you have done

differently?

I would have taken a more compassionate, problem

solving and client centred approach.

8. Changes

What changes to staff training,

back office/business processes,

client service standards and/or

job roles have been undertaken to

reduce the chance of it re-

occurring?

The consumer management comity did not do anything

to make their consumer aware of the payment contracts

operations and purchasing considerations.

9. Current position

Based on the changes put in place,

what is different now?

The client is more secure and feels happy what is

problem is addressed. His dignity is lifted and he is

satisfied that we are addressing his problems in the most

apt way.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8FINANCIAL BEHAVIOUR

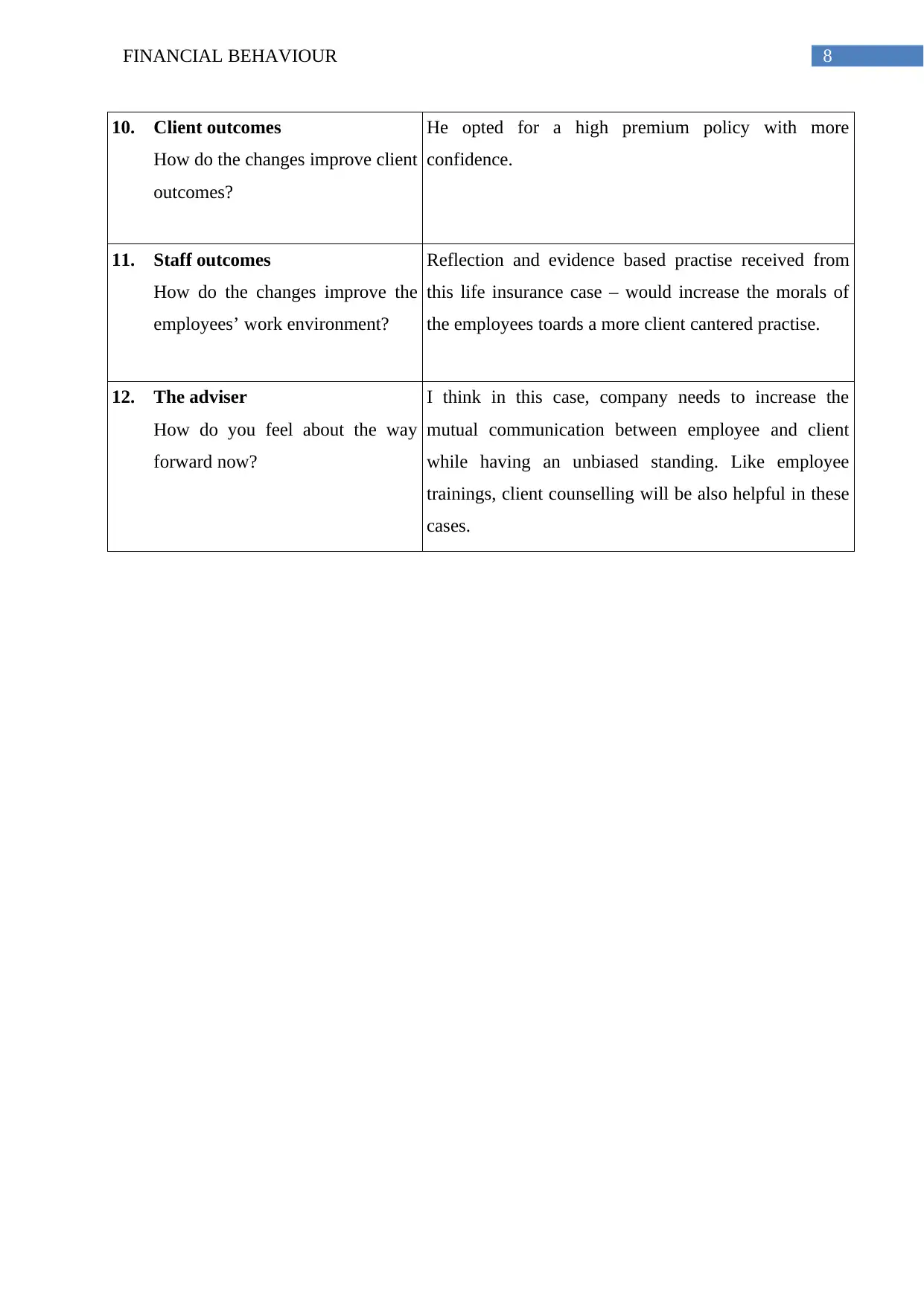

10. Client outcomes

How do the changes improve client

outcomes?

He opted for a high premium policy with more

confidence.

11. Staff outcomes

How do the changes improve the

employees’ work environment?

Reflection and evidence based practise received from

this life insurance case – would increase the morals of

the employees toards a more client cantered practise.

12. The adviser

How do you feel about the way

forward now?

I think in this case, company needs to increase the

mutual communication between employee and client

while having an unbiased standing. Like employee

trainings, client counselling will be also helpful in these

cases.

10. Client outcomes

How do the changes improve client

outcomes?

He opted for a high premium policy with more

confidence.

11. Staff outcomes

How do the changes improve the

employees’ work environment?

Reflection and evidence based practise received from

this life insurance case – would increase the morals of

the employees toards a more client cantered practise.

12. The adviser

How do you feel about the way

forward now?

I think in this case, company needs to increase the

mutual communication between employee and client

while having an unbiased standing. Like employee

trainings, client counselling will be also helpful in these

cases.

9FINANCIAL BEHAVIOUR

Part 2

Critical Analysis of Clients’ Financial Behaviour

Introduction:

Financial behaviour has even more impact on the business procedure marketing campaign of

banks and developing the Government policies. Consumer financial behaviour is one of the

most major concerns in any organisation and their marketing and promotion related activities.

The protective actions of these organisational operations depend on assumptions about

consumer needs, their emotional needs, psychological stimulus and other factors that works

under the decision making process (Kaminski et al. 2017)..

The purpose of this paper is to discuss the financial behaviour of the clients with critical

analysis considering the theoretical explanation of consumer choice and decision making

before and after making an investment. In this particular study two interviews are included

for critical analysis. One interview was taken from a financial advisor and another interview

was taken from a client service person. To understand the Consumer Financial Behaviour an

organisation needs a systemic economic and behavioural approach (Topa, Lunceford and

Boyatzis 2018). It can also help to compare different types of financial behaviours of the

consumers along with the psychological explanations for their behaviour and decision

making. Hence analysis of the financial behaviour of client and the partial influence of their

environment is necessary to understand the consumer expectation and business opportunity.

Through the interviews, two cases of client financial investment behaviour have been

acquired. In the following section Situational comparison between financial advisor’s and

client service person’s clients have been discussed followed by the behavioural analysis and

comparison between two clients. After that the strength and weakness in interviewees’

behaviour regarding consumer handling have been discussed with theoretical explanation.

Part 2

Critical Analysis of Clients’ Financial Behaviour

Introduction:

Financial behaviour has even more impact on the business procedure marketing campaign of

banks and developing the Government policies. Consumer financial behaviour is one of the

most major concerns in any organisation and their marketing and promotion related activities.

The protective actions of these organisational operations depend on assumptions about

consumer needs, their emotional needs, psychological stimulus and other factors that works

under the decision making process (Kaminski et al. 2017)..

The purpose of this paper is to discuss the financial behaviour of the clients with critical

analysis considering the theoretical explanation of consumer choice and decision making

before and after making an investment. In this particular study two interviews are included

for critical analysis. One interview was taken from a financial advisor and another interview

was taken from a client service person. To understand the Consumer Financial Behaviour an

organisation needs a systemic economic and behavioural approach (Topa, Lunceford and

Boyatzis 2018). It can also help to compare different types of financial behaviours of the

consumers along with the psychological explanations for their behaviour and decision

making. Hence analysis of the financial behaviour of client and the partial influence of their

environment is necessary to understand the consumer expectation and business opportunity.

Through the interviews, two cases of client financial investment behaviour have been

acquired. In the following section Situational comparison between financial advisor’s and

client service person’s clients have been discussed followed by the behavioural analysis and

comparison between two clients. After that the strength and weakness in interviewees’

behaviour regarding consumer handling have been discussed with theoretical explanation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10FINANCIAL BEHAVIOUR

Finally the aim of this paper to present set of recommendations for the financial advisor and

the client service person regarding their consumer handling.

Situational comparison between financial advisor’s and client service person’s clients

In first case. The client works in an IT company and is about to get a retirement in the next

month itself. He worked in an IT company and has under 10 years two daughters and he is

about to retire in 15 years. He appointed me to assess the current financial situation, the

financial aspects affecting the future of his children 9 their higher education and weddings)

and to understand the intricacies of his retirement related investments. The client, in the last

few months is really worried about the future of his daughters, after his retirement. Moreover,

he had previous losses at business investments and since then he had not taken any

investment decisions until now. On the other hand, in second case - client was an employee

in a telecommunications company. Before two months – he had an accident and broke his

car. As he had a general insurance, the damage and financial loss was mitigated. However, he

had really bad experiences with the other insurance investments before and has suffered a

substantial loss. He is worried he might be injured the same way like his car is and has

decided to go a life insurance. But he is afraid of the prior insurance related losses as well.

In first case the client had suffered losses to direct investment and could not decide between

the execution or intention for taking up the retirement plans. Precisely, he had a goal setting

problem. In the second case, he was a genuine fear in repetition of a similar mistake while

choosing for the insurance policy.

Behavioural analysis and comparison between two clients

For both clients they avoided choosing the guided decision because it was their way to avoid

any potential regret of having made a high investment for a wrong product or service. It also

allows them to avoid embarrassment of reporting a loss. The client hated to be faulty

Finally the aim of this paper to present set of recommendations for the financial advisor and

the client service person regarding their consumer handling.

Situational comparison between financial advisor’s and client service person’s clients

In first case. The client works in an IT company and is about to get a retirement in the next

month itself. He worked in an IT company and has under 10 years two daughters and he is

about to retire in 15 years. He appointed me to assess the current financial situation, the

financial aspects affecting the future of his children 9 their higher education and weddings)

and to understand the intricacies of his retirement related investments. The client, in the last

few months is really worried about the future of his daughters, after his retirement. Moreover,

he had previous losses at business investments and since then he had not taken any

investment decisions until now. On the other hand, in second case - client was an employee

in a telecommunications company. Before two months – he had an accident and broke his

car. As he had a general insurance, the damage and financial loss was mitigated. However, he

had really bad experiences with the other insurance investments before and has suffered a

substantial loss. He is worried he might be injured the same way like his car is and has

decided to go a life insurance. But he is afraid of the prior insurance related losses as well.

In first case the client had suffered losses to direct investment and could not decide between

the execution or intention for taking up the retirement plans. Precisely, he had a goal setting

problem. In the second case, he was a genuine fear in repetition of a similar mistake while

choosing for the insurance policy.

Behavioural analysis and comparison between two clients

For both clients they avoided choosing the guided decision because it was their way to avoid

any potential regret of having made a high investment for a wrong product or service. It also

allows them to avoid embarrassment of reporting a loss. The client hated to be faulty

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11FINANCIAL BEHAVIOUR

investor. Human mind has a tendency to store the experience of particular events in the

memory where different memories generate from different experiences have great impact on

resultant behaviour, which is even stronger than the event itself. In behavioural science this

phenomenon is called Mental Accounting Behaviours (Anderson, Baker and Robinson 2017).

At the same time, all consumers who are going to invest prefer a sure investment return to an

uncertain one. In both of these cases clients has their rigid and bias through process regarding

investment. The first client ( who came for retirement plans) had a rigid sense of insecurity

regarding direct capital investment in terms of retirement plans. As the client himself

mentioned, that he faced a huge loss due to direct investment. However, he was failed to

distinguish the past and present situation. In past, he was not guided by a financial advisor

and therefore perhaps the loss he had experienced was caused by wrong planning and

execution rather than wrong direct investment plan.

Prospect theory also explains why investors hold onto losing stocks. The prospect theory is

also applicable for the second client. For second client, he had lack of knowledge regarding

general and life insurances. Influences from his peers, close relatives, family members and

the opinion of his trusted person might be the cause of his rigid stand on his perception of

payment contracts. Prospect theory clearly states that in practical investment situation lack of

knowledge in clients is very common. This case is not an exception. Most of the investors

make a common mistake of investing in a product or service or chasing for a stock which

already has a great attention in market. On the other hand, most of the individuals tend to

organize their market ideas, suppositions and investment opinions whereas making a choice

(Fulda and Lersch 2018). Before investing – the client take into consideration – the more

verifiable, long-term midpoints and probabilities. In this case, the client was unable to

difference between the general insurance and life insurance policies and he had previous

losses when it came to choosing insurances. He was irrational, rigid and had delusionary

investor. Human mind has a tendency to store the experience of particular events in the

memory where different memories generate from different experiences have great impact on

resultant behaviour, which is even stronger than the event itself. In behavioural science this

phenomenon is called Mental Accounting Behaviours (Anderson, Baker and Robinson 2017).

At the same time, all consumers who are going to invest prefer a sure investment return to an

uncertain one. In both of these cases clients has their rigid and bias through process regarding

investment. The first client ( who came for retirement plans) had a rigid sense of insecurity

regarding direct capital investment in terms of retirement plans. As the client himself

mentioned, that he faced a huge loss due to direct investment. However, he was failed to

distinguish the past and present situation. In past, he was not guided by a financial advisor

and therefore perhaps the loss he had experienced was caused by wrong planning and

execution rather than wrong direct investment plan.

Prospect theory also explains why investors hold onto losing stocks. The prospect theory is

also applicable for the second client. For second client, he had lack of knowledge regarding

general and life insurances. Influences from his peers, close relatives, family members and

the opinion of his trusted person might be the cause of his rigid stand on his perception of

payment contracts. Prospect theory clearly states that in practical investment situation lack of

knowledge in clients is very common. This case is not an exception. Most of the investors

make a common mistake of investing in a product or service or chasing for a stock which

already has a great attention in market. On the other hand, most of the individuals tend to

organize their market ideas, suppositions and investment opinions whereas making a choice

(Fulda and Lersch 2018). Before investing – the client take into consideration – the more

verifiable, long-term midpoints and probabilities. In this case, the client was unable to

difference between the general insurance and life insurance policies and he had previous

losses when it came to choosing insurances. He was irrational, rigid and had delusionary

12FINANCIAL BEHAVIOUR

ideas about the product. He lacked attention and focus in his behaviour and he lacked the skill

of active listening as well.

Strength and weakness in interviewees’ behaviour regarding consumer handling

There was professionalism and enough competency regarding the whole client handling and

consumer guiding process, although in some areas – the communication was missing between

the specialist and the consumer. Both of the interviewers tried to communicate with their

client to guide them in a proper investment direction. The first interviewer showed lack of

client counselling and the second interviewer should lack of instant problem solving

(Jiménez, Chiesa and Topa 2019).

Similarly in the case of retirement plan, the client (because of his direct losses at business

investments previously) is focussing to take up a retirement plan that as minimum as possible

but that way – she is losing the utility of taking an retirement plan. The client of second case

had lack of knowledge between the policies pertaining to General insurance and life

insurance. He perceives taking life insurance as a financial risk because of bad experience

with LI before.

Recommendations

It has been also found from the above case study that previous experience and

knowledge are two major factors of consumer decision making. In this case both interviewees

have to make their consumer preference modulating skill very strong. Improving their

emotional intelligence will be very helpful in this case (Agarwal et al. 2015). The financial

advisor and the client person have to undergo through specific training that can improve their

interpersonal communication skill and emotional intelligence.

It has been often found that the decision of the investor is highly influence by a Group

such as the primary influential group includes family members, relatives and the secondary

influential group including neighbours. Hence, both advisors need to take care of the origin of

ideas about the product. He lacked attention and focus in his behaviour and he lacked the skill

of active listening as well.

Strength and weakness in interviewees’ behaviour regarding consumer handling

There was professionalism and enough competency regarding the whole client handling and

consumer guiding process, although in some areas – the communication was missing between

the specialist and the consumer. Both of the interviewers tried to communicate with their

client to guide them in a proper investment direction. The first interviewer showed lack of

client counselling and the second interviewer should lack of instant problem solving

(Jiménez, Chiesa and Topa 2019).

Similarly in the case of retirement plan, the client (because of his direct losses at business

investments previously) is focussing to take up a retirement plan that as minimum as possible

but that way – she is losing the utility of taking an retirement plan. The client of second case

had lack of knowledge between the policies pertaining to General insurance and life

insurance. He perceives taking life insurance as a financial risk because of bad experience

with LI before.

Recommendations

It has been also found from the above case study that previous experience and

knowledge are two major factors of consumer decision making. In this case both interviewees

have to make their consumer preference modulating skill very strong. Improving their

emotional intelligence will be very helpful in this case (Agarwal et al. 2015). The financial

advisor and the client person have to undergo through specific training that can improve their

interpersonal communication skill and emotional intelligence.

It has been often found that the decision of the investor is highly influence by a Group

such as the primary influential group includes family members, relatives and the secondary

influential group including neighbours. Hence, both advisors need to take care of the origin of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.