Comprehensive Financial Analysis and Budgeting for Motel Operations

VerifiedAdded on 2020/01/28

|9

|2102

|33

Report

AI Summary

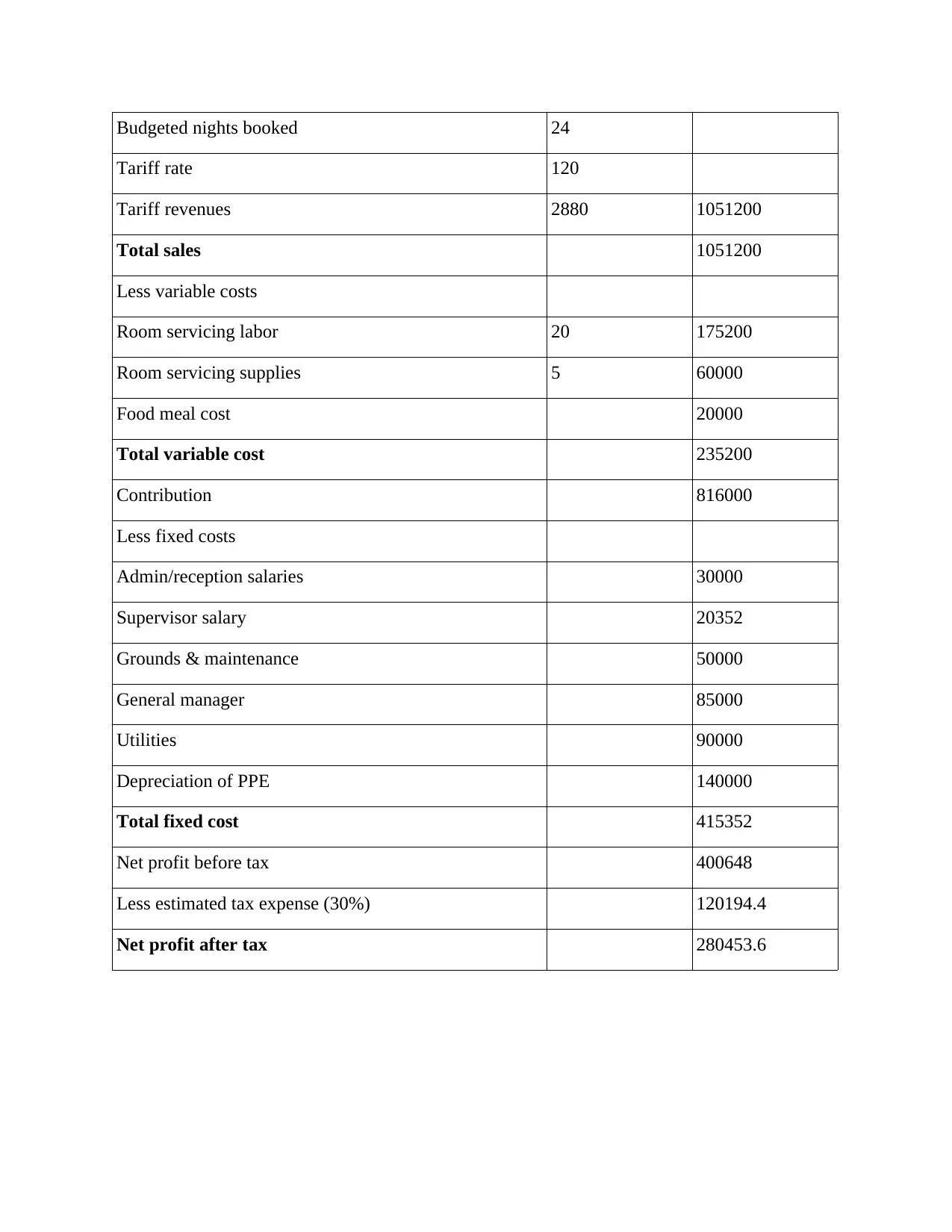

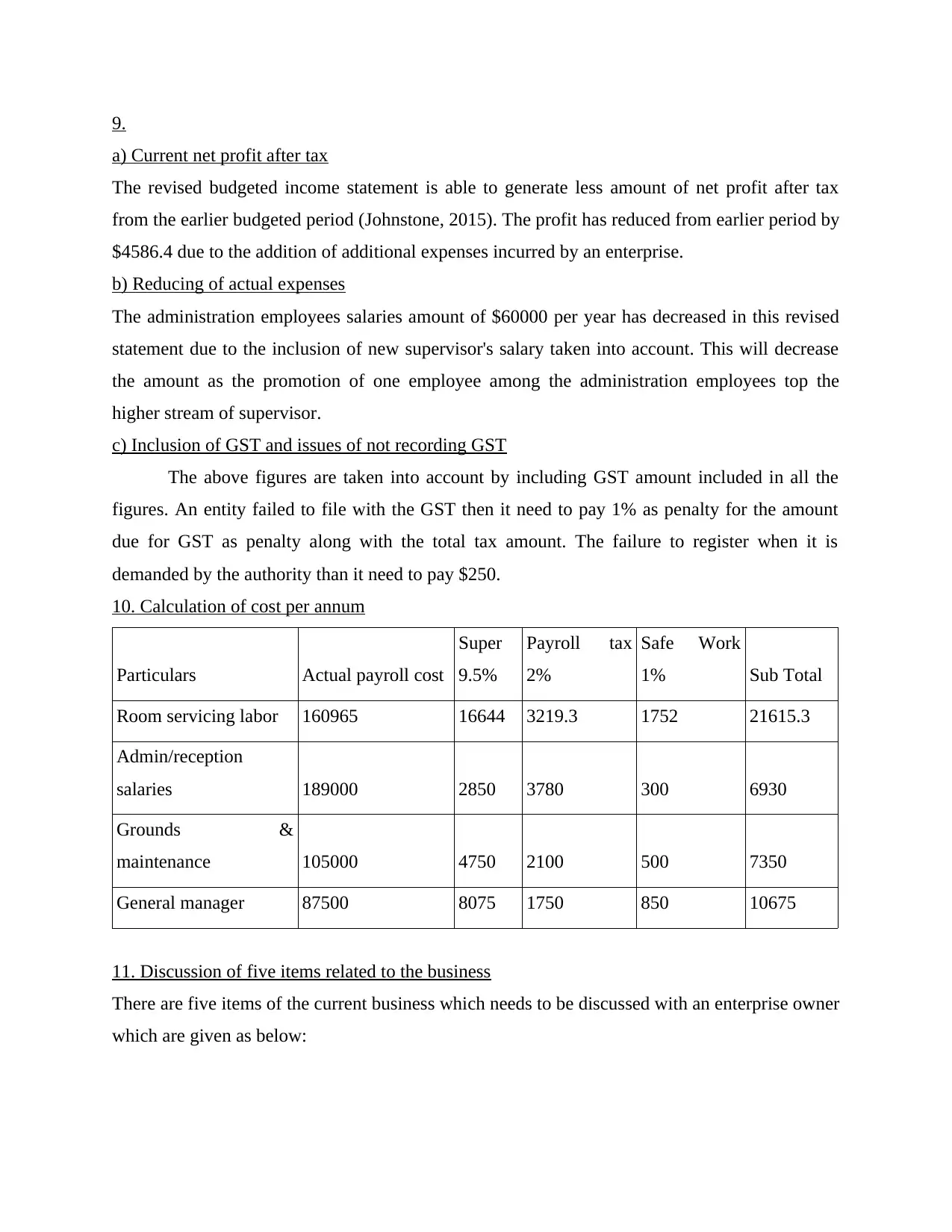

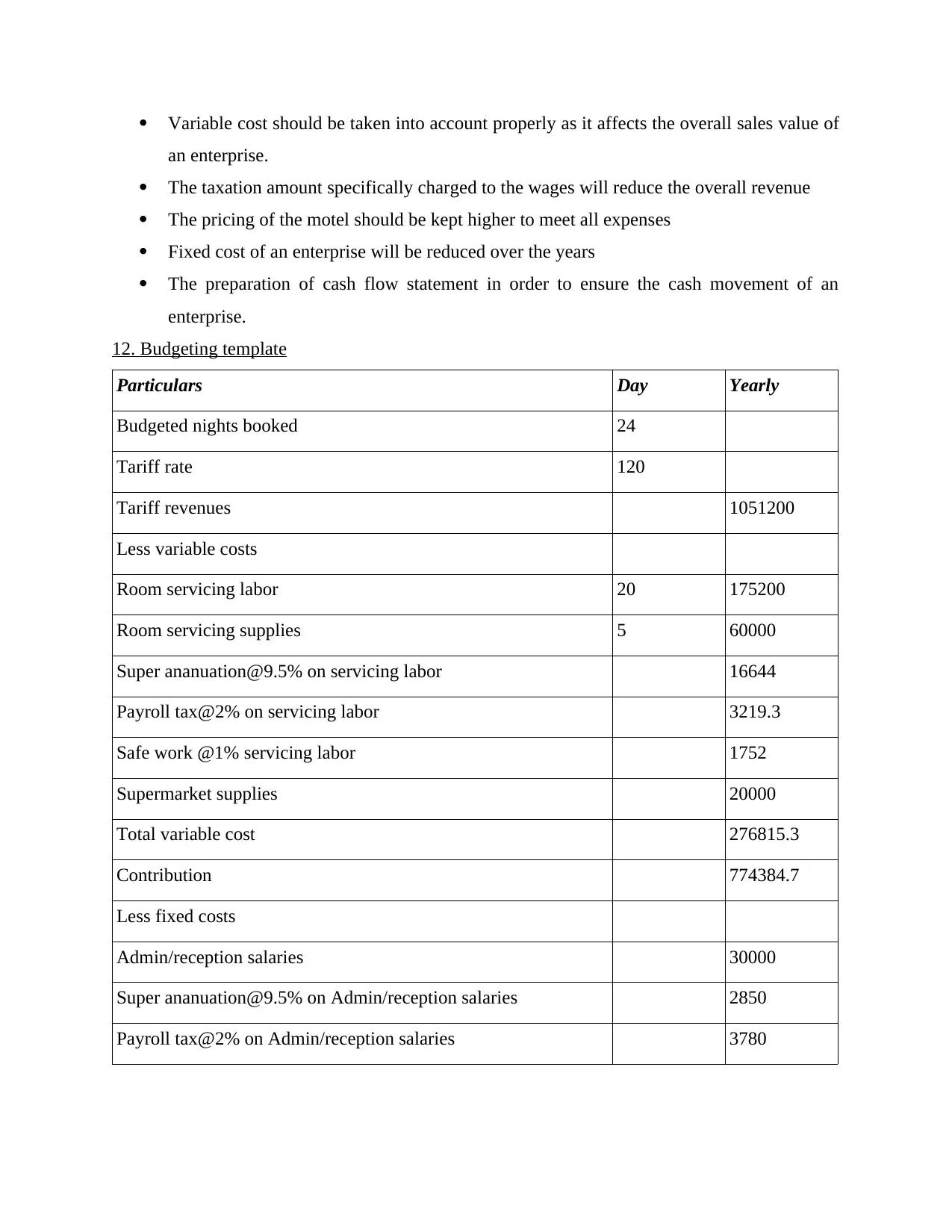

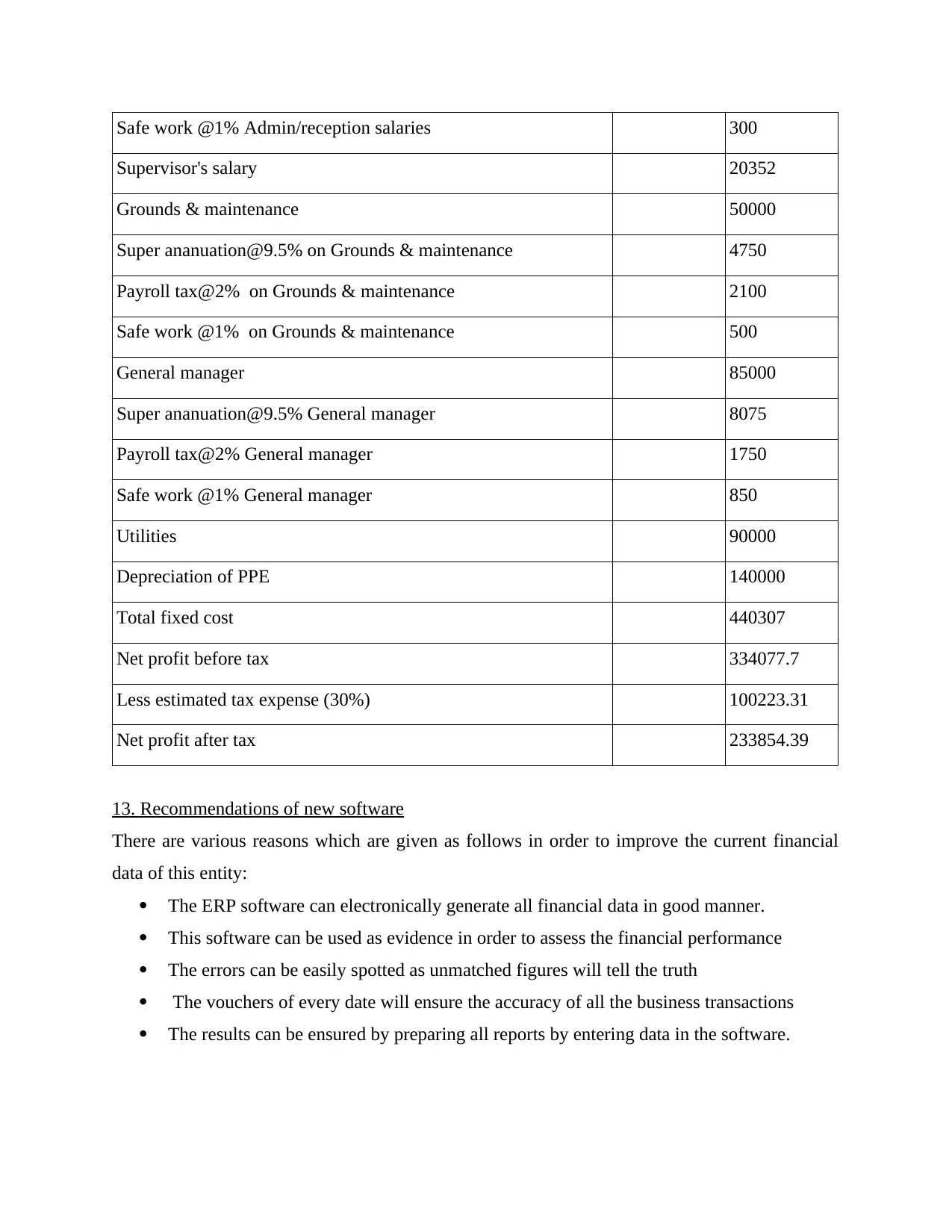

This report provides a comprehensive financial analysis of a motel's operations, starting with a budgeted income statement. It offers recommendations for non-financial users, addresses financial management issues like delegation of authority and inventory systems, and explores communication strategies with management. The report calculates wages, investigates variances in the budget, and suggests the inclusion of new expenses like meal costs. It also frames new company policies for stock ordering and discusses the impact of these policies. A revised budgeted income statement is presented, along with an analysis of the net profit after tax, expense reduction strategies, and the implications of GST. The report includes cost calculations, a discussion of key business items, a detailed budgeting template, and recommendations for new software to improve financial data management. The report references several financial and accounting sources to support its analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.