Financial Budget Analysis and Methods for Snappy Drinks Plc

VerifiedAdded on 2020/10/22

|11

|3069

|157

Report

AI Summary

This report provides a comprehensive financial analysis focusing on budgeting methods suitable for Snappy Drinks Plc. It begins by explaining the purpose and process of budget formulation, emphasizing effective planning and coordination across various business functions. The report then explores the application of traditional and incremental budgeting, offering a practical example to illustrate its use in forecasting costs and profits. Furthermore, it critically analyzes the usefulness of the traditional budgetary system for Snappy Drinks Plc, highlighting its limitations in efficiency and adaptability. The report then presents and compares alternative budgeting methods, including rolling, zero-based, and activity-based budgeting, detailing their advantages and disadvantages. It concludes by analyzing the best alternative method for Snappy Drinks Plc, providing recommendations based on the company's specific needs and objectives, ensuring optimized financial planning and resource allocation. The report references relevant literature and provides a clear and concise overview of each method, making it a valuable resource for students and professionals alike.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

I. Explaining the purpose of formulating the budget and the process of budgeting...................1

ii. Application of the traditional budgets including incremental budgets for planning the future

cost..............................................................................................................................................2

iii. Analysing the usefulness of the appropriate budgetary system for Snappy Drinks Plc.......3

PART 2............................................................................................................................................4

iv Presenting the alternative methods of budget preparations....................................................4

V Application of the various methods discussed above.............................................................6

vi Analysing the best alternative method, appropriate for Snappy Drinks Plc..........................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

I. Explaining the purpose of formulating the budget and the process of budgeting...................1

ii. Application of the traditional budgets including incremental budgets for planning the future

cost..............................................................................................................................................2

iii. Analysing the usefulness of the appropriate budgetary system for Snappy Drinks Plc.......3

PART 2............................................................................................................................................4

iv Presenting the alternative methods of budget preparations....................................................4

V Application of the various methods discussed above.............................................................6

vi Analysing the best alternative method, appropriate for Snappy Drinks Plc..........................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The business analysis its performance for a particular time period evaluation of its

budgets with the actual performance. The budgets are of vital importance to the businesses as it

sets the target for the business to achieve a certain goal in predetermined funds allocated to each

activity. In the present report the Snappy Drinks Plc is presented with the knowledge over the

preparation of the budgets, use and application of the traditional budget in the business.

Moreover the the different alternative of budgets methods are explained with their advantages

and disadvantages, their application and usefulness of the best methods amongst all.

PART 1

I. Explaining the purpose of formulating the budget and the process of budgeting

Overall purpose for preparing the budget is to make effective planning for different

functions of the operations of business and to coordinate the activities of several divisions of the

Snappy drinks. With the formulation of the budget effective control can be ensured over the

various phases of operations (Grossi, Reichard and Ruggiero, 2016). The major purpose for

framing the budget is to facilitate a model which states the way in which the business activities

must be performed and reflects the strategies, plans, events etc that are to be carried out. The

objective of forecasting the income, expenditure and the profitability are met with the

preparation of the budget.

Process of budgeting-

Setting up of objectives for budgeting- The first and the foremost step of the budgeting is

before evaluating the budget, the budget committee must set the objectives for meeting the future

goals of Snappy drinks. Objectives might include controlling cost, sales target, expansion etc.

Different purposes requires different form of the budgeting so it is necessary to set the objective

first.

Identifying the resource availability- After setting the objectives, availability of the

sufficient resources must be analyzed so that goals can be achieved effectively and efficiently.

Available resources must include cash as well as the other loans and the outside investments

made by the Snappy drinks. Under this the company must also project for its future sales in the

coming years.

1

The business analysis its performance for a particular time period evaluation of its

budgets with the actual performance. The budgets are of vital importance to the businesses as it

sets the target for the business to achieve a certain goal in predetermined funds allocated to each

activity. In the present report the Snappy Drinks Plc is presented with the knowledge over the

preparation of the budgets, use and application of the traditional budget in the business.

Moreover the the different alternative of budgets methods are explained with their advantages

and disadvantages, their application and usefulness of the best methods amongst all.

PART 1

I. Explaining the purpose of formulating the budget and the process of budgeting

Overall purpose for preparing the budget is to make effective planning for different

functions of the operations of business and to coordinate the activities of several divisions of the

Snappy drinks. With the formulation of the budget effective control can be ensured over the

various phases of operations (Grossi, Reichard and Ruggiero, 2016). The major purpose for

framing the budget is to facilitate a model which states the way in which the business activities

must be performed and reflects the strategies, plans, events etc that are to be carried out. The

objective of forecasting the income, expenditure and the profitability are met with the

preparation of the budget.

Process of budgeting-

Setting up of objectives for budgeting- The first and the foremost step of the budgeting is

before evaluating the budget, the budget committee must set the objectives for meeting the future

goals of Snappy drinks. Objectives might include controlling cost, sales target, expansion etc.

Different purposes requires different form of the budgeting so it is necessary to set the objective

first.

Identifying the resource availability- After setting the objectives, availability of the

sufficient resources must be analyzed so that goals can be achieved effectively and efficiently.

Available resources must include cash as well as the other loans and the outside investments

made by the Snappy drinks. Under this the company must also project for its future sales in the

coming years.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Anticipating future needs- The next step after determining the resource availability

includes the requirement of funds for meeting the future needs of the company (Srithongrung,

Yusuf and Kriz, 2019). The future needs can be estimated on the basis of the past data, data

available on the competitors, by assessing the current and the developing economic trends that

may occur in the upcoming years.

Matching the future needs with the available resources- In this phase of the process of

budgeting, Snappy drinks need to make some negotiations within their departments for

determining the allocation of the scarce resources in the best possible manner. While performing

this step, the priorities of the business and the strategic needs must be kept in mind.

Obtaining the final approval- After the completion of the budget, next step is getting the

approval from budget committee. Acquiring the approval for the budget becomes smoother for

Snappy drinks if the budget is prepared by keeping in mind the needs of the key stakeholders.

Distribution of the approved funds- After the approval received from the committee, the

final step in the process of budgeting is for distributing the funds allocated to several

departments and the segments of the business of Snappy drinks. For processing this step it is

duty of the controller and the chief financial officer.

Evaluating and monitoring- Once the finalization of they budget and the distribution of

the funds, the success of the execution of the budget has to be tracked or traced (Vargas-

Hernández, Cárdenaz and Vargas, 2019). The areas that are lacking with the resources has to be

identified so that any uncertainty can be met in the future.

ii. Application of the traditional budgets including incremental budgets for planning the future

cost

The application of the traditional budget in the Snappy Drinks Plc is like using the

previous years budgets to forecast the current year budgets regarding the spending into the

different activity involved in manufacturing of the products such as productions, sales,

marketing, overheads and other.

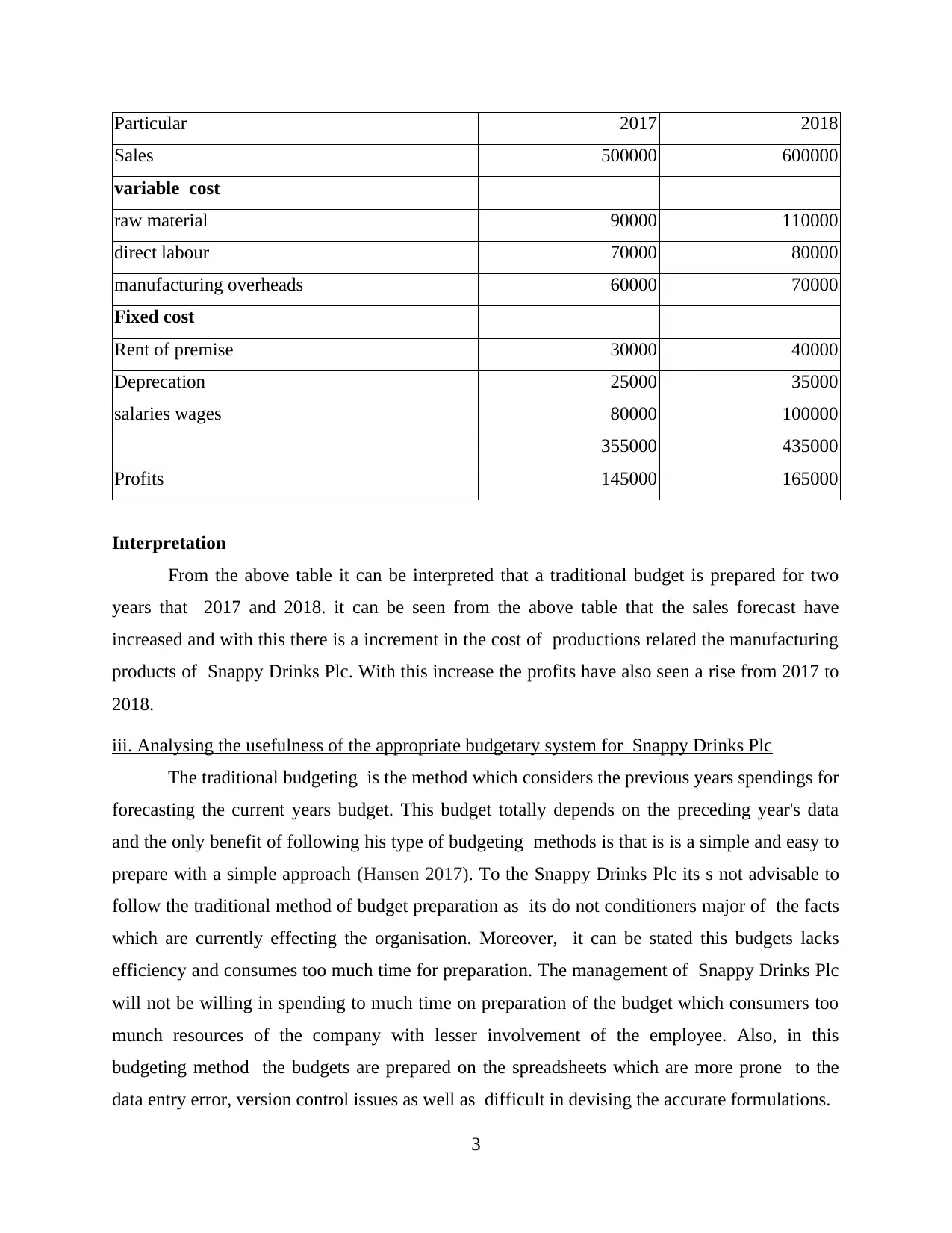

For example:

Traditional budget forecast for Snappy Drinks

Plc for 2 years

2

includes the requirement of funds for meeting the future needs of the company (Srithongrung,

Yusuf and Kriz, 2019). The future needs can be estimated on the basis of the past data, data

available on the competitors, by assessing the current and the developing economic trends that

may occur in the upcoming years.

Matching the future needs with the available resources- In this phase of the process of

budgeting, Snappy drinks need to make some negotiations within their departments for

determining the allocation of the scarce resources in the best possible manner. While performing

this step, the priorities of the business and the strategic needs must be kept in mind.

Obtaining the final approval- After the completion of the budget, next step is getting the

approval from budget committee. Acquiring the approval for the budget becomes smoother for

Snappy drinks if the budget is prepared by keeping in mind the needs of the key stakeholders.

Distribution of the approved funds- After the approval received from the committee, the

final step in the process of budgeting is for distributing the funds allocated to several

departments and the segments of the business of Snappy drinks. For processing this step it is

duty of the controller and the chief financial officer.

Evaluating and monitoring- Once the finalization of they budget and the distribution of

the funds, the success of the execution of the budget has to be tracked or traced (Vargas-

Hernández, Cárdenaz and Vargas, 2019). The areas that are lacking with the resources has to be

identified so that any uncertainty can be met in the future.

ii. Application of the traditional budgets including incremental budgets for planning the future

cost

The application of the traditional budget in the Snappy Drinks Plc is like using the

previous years budgets to forecast the current year budgets regarding the spending into the

different activity involved in manufacturing of the products such as productions, sales,

marketing, overheads and other.

For example:

Traditional budget forecast for Snappy Drinks

Plc for 2 years

2

Particular 2017 2018

Sales 500000 600000

variable cost

raw material 90000 110000

direct labour 70000 80000

manufacturing overheads 60000 70000

Fixed cost

Rent of premise 30000 40000

Deprecation 25000 35000

salaries wages 80000 100000

355000 435000

Profits 145000 165000

Interpretation

From the above table it can be interpreted that a traditional budget is prepared for two

years that 2017 and 2018. it can be seen from the above table that the sales forecast have

increased and with this there is a increment in the cost of productions related the manufacturing

products of Snappy Drinks Plc. With this increase the profits have also seen a rise from 2017 to

2018.

iii. Analysing the usefulness of the appropriate budgetary system for Snappy Drinks Plc

The traditional budgeting is the method which considers the previous years spendings for

forecasting the current years budget. This budget totally depends on the preceding year's data

and the only benefit of following his type of budgeting methods is that is is a simple and easy to

prepare with a simple approach (Hansen 2017). To the Snappy Drinks Plc its s not advisable to

follow the traditional method of budget preparation as its do not conditioners major of the facts

which are currently effecting the organisation. Moreover, it can be stated this budgets lacks

efficiency and consumes too much time for preparation. The management of Snappy Drinks Plc

will not be willing in spending to much time on preparation of the budget which consumers too

munch resources of the company with lesser involvement of the employee. Also, in this

budgeting method the budgets are prepared on the spreadsheets which are more prone to the

data entry error, version control issues as well as difficult in devising the accurate formulations.

3

Sales 500000 600000

variable cost

raw material 90000 110000

direct labour 70000 80000

manufacturing overheads 60000 70000

Fixed cost

Rent of premise 30000 40000

Deprecation 25000 35000

salaries wages 80000 100000

355000 435000

Profits 145000 165000

Interpretation

From the above table it can be interpreted that a traditional budget is prepared for two

years that 2017 and 2018. it can be seen from the above table that the sales forecast have

increased and with this there is a increment in the cost of productions related the manufacturing

products of Snappy Drinks Plc. With this increase the profits have also seen a rise from 2017 to

2018.

iii. Analysing the usefulness of the appropriate budgetary system for Snappy Drinks Plc

The traditional budgeting is the method which considers the previous years spendings for

forecasting the current years budget. This budget totally depends on the preceding year's data

and the only benefit of following his type of budgeting methods is that is is a simple and easy to

prepare with a simple approach (Hansen 2017). To the Snappy Drinks Plc its s not advisable to

follow the traditional method of budget preparation as its do not conditioners major of the facts

which are currently effecting the organisation. Moreover, it can be stated this budgets lacks

efficiency and consumes too much time for preparation. The management of Snappy Drinks Plc

will not be willing in spending to much time on preparation of the budget which consumers too

munch resources of the company with lesser involvement of the employee. Also, in this

budgeting method the budgets are prepared on the spreadsheets which are more prone to the

data entry error, version control issues as well as difficult in devising the accurate formulations.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Moreover, in the traditional budget the annual budget cycle do not have a focus on the

reviews on a regular basis or are even not in taken in account at all. As the budgets are prepared

by taking into consideration the past figures, so there is no motivation among the employees od

Snappy Drinks Plc to act in the interest of the company or use their skills and abilities in

forecasting and preparation of the budgets. Also, in the traditional approach of the budget

preparation the mangers sometimes tend to obsessed with hitting the right numbers where they

often miss the strategic purpose of the budgeting as this budgets focus on the cost reduction

rather than value creation and strategic initiatives. This is advised to the Snappy Drinks Plc that

there is no benefit in following traditional budgeting method as this do not show the efficiency in

preparation of the budgets for the organisation and do not take into consideration the present

facts prevailing within the organisation which can directly affect the budget prepration.

PART 2

iv Presenting the alternative methods of budget preparations

Rolling budgets:

The rolling budgets s the one which is updated on a continuous basis and it considers a

incremental approach for every new budget period. The rolling budget for Snappy Drinks Plc

involves extension of the exiting budget in a new financial year. This way the business can

extent one years budgets into the future (Fitzpartick and Hawke 2015). The another name for

this budgets is the horizon budget as it take in to consideration the past figures and assumption to

prepare and ascertain the future budgets as well as performance of Snappy Drinks Plc.

Advantages:

The approach used in the preparation of the rolling budget by Snappy Drinks Plc pay

attention to content focus on the budget model and receiving the budget assumptions for the last

incremental budget for the previous period. Another benefits attached to this type of budget for

Snappy Drinks Plc is that it follows a continues approach and is a perpetual budget.

Disadvantages

There are certain disadvantages attached to rolling budgets which can effect Snappy

Drinks Plc, this includes this budgets might no be able to yield a more achievable budgets than

the traditional static budget. Also the previous and past figures on whose basis rolling budget is

prepared are not revised which can lad t to a wring ascertainment of the budgeted figures.

4

reviews on a regular basis or are even not in taken in account at all. As the budgets are prepared

by taking into consideration the past figures, so there is no motivation among the employees od

Snappy Drinks Plc to act in the interest of the company or use their skills and abilities in

forecasting and preparation of the budgets. Also, in the traditional approach of the budget

preparation the mangers sometimes tend to obsessed with hitting the right numbers where they

often miss the strategic purpose of the budgeting as this budgets focus on the cost reduction

rather than value creation and strategic initiatives. This is advised to the Snappy Drinks Plc that

there is no benefit in following traditional budgeting method as this do not show the efficiency in

preparation of the budgets for the organisation and do not take into consideration the present

facts prevailing within the organisation which can directly affect the budget prepration.

PART 2

iv Presenting the alternative methods of budget preparations

Rolling budgets:

The rolling budgets s the one which is updated on a continuous basis and it considers a

incremental approach for every new budget period. The rolling budget for Snappy Drinks Plc

involves extension of the exiting budget in a new financial year. This way the business can

extent one years budgets into the future (Fitzpartick and Hawke 2015). The another name for

this budgets is the horizon budget as it take in to consideration the past figures and assumption to

prepare and ascertain the future budgets as well as performance of Snappy Drinks Plc.

Advantages:

The approach used in the preparation of the rolling budget by Snappy Drinks Plc pay

attention to content focus on the budget model and receiving the budget assumptions for the last

incremental budget for the previous period. Another benefits attached to this type of budget for

Snappy Drinks Plc is that it follows a continues approach and is a perpetual budget.

Disadvantages

There are certain disadvantages attached to rolling budgets which can effect Snappy

Drinks Plc, this includes this budgets might no be able to yield a more achievable budgets than

the traditional static budget. Also the previous and past figures on whose basis rolling budget is

prepared are not revised which can lad t to a wring ascertainment of the budgeted figures.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zero based budgeting:

The anther methods to prepare a budgets for Snappy Drinks Plc is zero based approach.

In this methods of budgeting all the expenses are justified for each new period. The process of

preparation of this budgets starts from a zero base , which means the budgets is set with new

figures and assumption without taking any reference from the past budgets and does not follows

a incremental approach.

Advantages:

The befits of this budget for Snappy Drinks Plc can be outlined as this effectively

allocate of the resource as per need and requirement of the task and activities of the organisation.

This is an cost effective approach which drive the managers of Snappy Drinks Plc for

improvisation of the activities (Pyhrr, 2012). This is also identifies and eliminated the wastage

and out of date operations.

Disadvantages

The drawback attached to this type of budget is that it is a time consuming approach as

all the some of the expenses are hard to determine and its consumes to much time of the mangers

of Snappy Drinks Plc. It requires involvement of man power as R&D is needed and all the

details in the budgets are required to justified.

Activity based budgeting:

This type of budgets focus n recording, researching and analysing of the activities of

the Snappy Drinks Plc and then determines the cost and funds requirement for each activity. For

each of the activity of the Snappy Drinks Plc cost is scrutinized for potential ways to create

efficiency. This is more rigorous than the traditional budgeting as it adjust the previous budgets

as well as identifies the costs and funds required for each activity of the Snappy Drinks Plc.

Advantages:

The cons of preparation of this type of budget for Snappy Drinks Plc includes more

accuracy in the costing of products , services, consumers and distribution channel. Its gives

better understanding of the overheads and is easy to understand as well. This budgets utilizes the

unit cost rather than the total cost and enables costing processes, supply chain and the value

system.

Disadvantages:

5

The anther methods to prepare a budgets for Snappy Drinks Plc is zero based approach.

In this methods of budgeting all the expenses are justified for each new period. The process of

preparation of this budgets starts from a zero base , which means the budgets is set with new

figures and assumption without taking any reference from the past budgets and does not follows

a incremental approach.

Advantages:

The befits of this budget for Snappy Drinks Plc can be outlined as this effectively

allocate of the resource as per need and requirement of the task and activities of the organisation.

This is an cost effective approach which drive the managers of Snappy Drinks Plc for

improvisation of the activities (Pyhrr, 2012). This is also identifies and eliminated the wastage

and out of date operations.

Disadvantages

The drawback attached to this type of budget is that it is a time consuming approach as

all the some of the expenses are hard to determine and its consumes to much time of the mangers

of Snappy Drinks Plc. It requires involvement of man power as R&D is needed and all the

details in the budgets are required to justified.

Activity based budgeting:

This type of budgets focus n recording, researching and analysing of the activities of

the Snappy Drinks Plc and then determines the cost and funds requirement for each activity. For

each of the activity of the Snappy Drinks Plc cost is scrutinized for potential ways to create

efficiency. This is more rigorous than the traditional budgeting as it adjust the previous budgets

as well as identifies the costs and funds required for each activity of the Snappy Drinks Plc.

Advantages:

The cons of preparation of this type of budget for Snappy Drinks Plc includes more

accuracy in the costing of products , services, consumers and distribution channel. Its gives

better understanding of the overheads and is easy to understand as well. This budgets utilizes the

unit cost rather than the total cost and enables costing processes, supply chain and the value

system.

Disadvantages:

5

The con of this budgets for Snappy Drinks Plc can be started as its implementation

requires substantial resources and also it is costly to maintain this budget. The data of this

budgets is more prone to be misinterpreted and requires a utter care while using it in the decision

making process.

V Application of the various methods discussed above

Rolling budget:

Snappy Drinks Plc can apply this type of budget in its organisation practise as

forecasting the overall spending on the manufacturing in different products of the organisation.

For the next period previous data is use to continue to the budgets. For example: the rolling

budget for Snappy Drinks Plc is prepared for a time of 12 months staring from January to

December, after this the budgeting for all the manufacturing activities of the business a continues

budget form next January will be prepared till next December.

Zero based budget:

Snappy Drinks Plc can apply this budget as preparing a budgets regarding each

production activity of the organisation from a base Zero, for all the activities a new budgets will

be prepares without taking a reference form the previous budget. Fox example for the year 2017-

2018 a budget is prepared by Snappy Drinks Plc to forecast the spending and expected revenues

for over all manufacturing activities of the business. But for the the year 2018-2019 a new

budgets will be prepared for and no reference form the budget of 2017-2018 will be taken.

Activity based budget:

Snappy Drinks Plc can apply the preparation of the activity based budgeting as for all the

activities pertaining each of the products a separate is prepared such as productions, sales,

marketing , promotions, procurements ect. For example, with launching the a new range of

health led drinks there are 15 new products which will be be manufactures. In this context for

activities of sales, productions, marketing and others a separate budgets will be prepared for each

of the 15 products.

vi Analysing the best alternative method, appropriate for Snappy Drinks Plc

For the Snappy Drinks Plc the best of all the three alternative methods above regarding

the method of preparation of the budgets is the Zero based budgeting. This option is suggested

to the management of Snappy Drinks Plc because in this budgets there is efficient allocation of

the resources which are required for completion and carrying out e operations of the business

6

requires substantial resources and also it is costly to maintain this budget. The data of this

budgets is more prone to be misinterpreted and requires a utter care while using it in the decision

making process.

V Application of the various methods discussed above

Rolling budget:

Snappy Drinks Plc can apply this type of budget in its organisation practise as

forecasting the overall spending on the manufacturing in different products of the organisation.

For the next period previous data is use to continue to the budgets. For example: the rolling

budget for Snappy Drinks Plc is prepared for a time of 12 months staring from January to

December, after this the budgeting for all the manufacturing activities of the business a continues

budget form next January will be prepared till next December.

Zero based budget:

Snappy Drinks Plc can apply this budget as preparing a budgets regarding each

production activity of the organisation from a base Zero, for all the activities a new budgets will

be prepares without taking a reference form the previous budget. Fox example for the year 2017-

2018 a budget is prepared by Snappy Drinks Plc to forecast the spending and expected revenues

for over all manufacturing activities of the business. But for the the year 2018-2019 a new

budgets will be prepared for and no reference form the budget of 2017-2018 will be taken.

Activity based budget:

Snappy Drinks Plc can apply the preparation of the activity based budgeting as for all the

activities pertaining each of the products a separate is prepared such as productions, sales,

marketing , promotions, procurements ect. For example, with launching the a new range of

health led drinks there are 15 new products which will be be manufactures. In this context for

activities of sales, productions, marketing and others a separate budgets will be prepared for each

of the 15 products.

vi Analysing the best alternative method, appropriate for Snappy Drinks Plc

For the Snappy Drinks Plc the best of all the three alternative methods above regarding

the method of preparation of the budgets is the Zero based budgeting. This option is suggested

to the management of Snappy Drinks Plc because in this budgets there is efficient allocation of

the resources which are required for completion and carrying out e operations of the business

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Rubin, 2019). This approach drives the mangers in the finding the cost effective ways to

improvise the activities of the organisation. Moreover it can be stated that with this type of

budgets are useful for the departments of the Snappy Drinks Plc as as increase the staff

motivation as it gives them more initiatives and responsibilities which assist their decision

making process.

With the zero based budgeting approach the management of the Snappy Drinks Plc can

also identify the opportunities of outsourcing and to force the cost centres to link them with the

mission of the organisation and directly assist in attainment of the organisational objectives.

This types f budgets will assist the Snappy Drinks Plc in saving the money and improving the

services as this budgets retains the increase in the developing budgets and it reduces the

entitlement mentality regarding the cost increments. The making of the budgets includes

discussion which is meaningful during the review sessions. This directly enhances the

effectiveness of the mangers and the personnels involved in the budgets preparations and its

review. As the preparation of this budgets requires to start from the zero which is to be done by

taking the costs and expenses from new base and this includes critical discussions and directly

improvises the communication and coordination among the employees and within Snappy

Drinks Plc for making certain decisions. This can be stated for the organisation Snappy Drinks

Plc Zeros based budgeting is the best from of budget as this takes into consideration actual facts

and figures pertaining at the time of its making and increases overall communication process of

the business.

CONCLUSION

From the above report it can be be stated that the budgets hold a crucial position in the

business operation and management. Budget preparation is important task for the organisation to

forecast its future performance and then to achieve the performance in predetermined allocated

funds and resource. It assist the the Snappy Drinks Plc in preparation of the business model.

Furthermore it can be articulated that the various type of budgets prepared by the Snappy Drinks

Plc includes rolling, zero based and activity based budget. All have different forms of application

in the business. Moreover it has been analysed that zero based budgeting is the best method of

budgeting for Snappy Drinks Plc.

7

improvise the activities of the organisation. Moreover it can be stated that with this type of

budgets are useful for the departments of the Snappy Drinks Plc as as increase the staff

motivation as it gives them more initiatives and responsibilities which assist their decision

making process.

With the zero based budgeting approach the management of the Snappy Drinks Plc can

also identify the opportunities of outsourcing and to force the cost centres to link them with the

mission of the organisation and directly assist in attainment of the organisational objectives.

This types f budgets will assist the Snappy Drinks Plc in saving the money and improving the

services as this budgets retains the increase in the developing budgets and it reduces the

entitlement mentality regarding the cost increments. The making of the budgets includes

discussion which is meaningful during the review sessions. This directly enhances the

effectiveness of the mangers and the personnels involved in the budgets preparations and its

review. As the preparation of this budgets requires to start from the zero which is to be done by

taking the costs and expenses from new base and this includes critical discussions and directly

improvises the communication and coordination among the employees and within Snappy

Drinks Plc for making certain decisions. This can be stated for the organisation Snappy Drinks

Plc Zeros based budgeting is the best from of budget as this takes into consideration actual facts

and figures pertaining at the time of its making and increases overall communication process of

the business.

CONCLUSION

From the above report it can be be stated that the budgets hold a crucial position in the

business operation and management. Budget preparation is important task for the organisation to

forecast its future performance and then to achieve the performance in predetermined allocated

funds and resource. It assist the the Snappy Drinks Plc in preparation of the business model.

Furthermore it can be articulated that the various type of budgets prepared by the Snappy Drinks

Plc includes rolling, zero based and activity based budget. All have different forms of application

in the business. Moreover it has been analysed that zero based budgeting is the best method of

budgeting for Snappy Drinks Plc.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals

Fitzpartick, M. and Hawke, K., 2015. The Return of zero-base budgeting. McKinsey &

Company. Pobrano z: http://www. mckinsey. com/business-functions/strategy-and-

corporate-finance/our-insights/the-return-of-zero--base-budgeting (7.03. 2017).

Grossi, G., Reichard, C. and Ruggiero, P., 2016. Appropriateness and use of performance

information in the budgeting process: Some experiences from German and Italian

municipalities. Public Performance & Management Review. 39(3). pp.581-606.

Hansen, S. C., 2017. A theoretical analysis of the impact of adopting rolling budgets, activity-

based budgeting and beyond budgeting. European Accounting Review, 20(2), pp.289-319.

Pyhrr, P. A., 2012. Zero‐Based Budgeting. Handbook of Budgeting, pp.677-696.

Rubin, I. S., 2019. The politics of public budgeting: Getting and spending, borrowing and

balancing. CQ Press.

Srithongrung, A., Yusuf, J. E. W. and Kriz, K. A., 2019. A systematic public capital

management and budgeting process. In Capital management and budgeting in the public

sector (pp. 1-22). IGI Global.

Vargas-Hernández, J. G., Cárdenaz, R. C. and Vargas, O. B., 2019. THE BUDGET IN THE

FINANCIAL MANAGEMENT OF THE SMES ASSISTED BY THE

ADMINISTRATIVE PROCESS AS A COMPETITIVE TOOL. REVISTA

INTERCONTINENTAL DE GESTÃO DESPORTIVA-RIGD. 8(3). pp.15-35.

8

Books and journals

Fitzpartick, M. and Hawke, K., 2015. The Return of zero-base budgeting. McKinsey &

Company. Pobrano z: http://www. mckinsey. com/business-functions/strategy-and-

corporate-finance/our-insights/the-return-of-zero--base-budgeting (7.03. 2017).

Grossi, G., Reichard, C. and Ruggiero, P., 2016. Appropriateness and use of performance

information in the budgeting process: Some experiences from German and Italian

municipalities. Public Performance & Management Review. 39(3). pp.581-606.

Hansen, S. C., 2017. A theoretical analysis of the impact of adopting rolling budgets, activity-

based budgeting and beyond budgeting. European Accounting Review, 20(2), pp.289-319.

Pyhrr, P. A., 2012. Zero‐Based Budgeting. Handbook of Budgeting, pp.677-696.

Rubin, I. S., 2019. The politics of public budgeting: Getting and spending, borrowing and

balancing. CQ Press.

Srithongrung, A., Yusuf, J. E. W. and Kriz, K. A., 2019. A systematic public capital

management and budgeting process. In Capital management and budgeting in the public

sector (pp. 1-22). IGI Global.

Vargas-Hernández, J. G., Cárdenaz, R. C. and Vargas, O. B., 2019. THE BUDGET IN THE

FINANCIAL MANAGEMENT OF THE SMES ASSISTED BY THE

ADMINISTRATIVE PROCESS AS A COMPETITIVE TOOL. REVISTA

INTERCONTINENTAL DE GESTÃO DESPORTIVA-RIGD. 8(3). pp.15-35.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.