Comprehensive Financial Budgeting, Analysis, and Performance Review

VerifiedAdded on 2021/02/20

|18

|4295

|33

Report

AI Summary

This comprehensive report delves into the intricacies of financial budgeting and control, offering a detailed analysis of various budgeting techniques. The report begins with the calculation of budgeted cost of sales and the preparation of a budgeted income statement, followed by the reconstruction of debtors control accounts for evaluating estimated balances. It further explores direct labour and sales budgets, along with an analysis of internal and external factors impacting budgets. The report includes a budgeted cash flow statement and a profit and loss statement, providing insights into the financial performance of a business. Part A focuses on the scope and nature of budgets, data interpretation, and the impact of various factors. Part B presents a cash budget, while Part C examines budget variance reports and cash balance predictions. The report concludes with an evaluation of the appropriateness of quarterly periods for cash budgeting and relevant recommendations.

Prepare And Monitor

Budget

Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

5.1 Calculate the budgeted cost of sales for the year ending 30 June 2016:..........................1

5.2 Prepare a budgeted income statement for the year ending 30 June 2017.........................1

5.3 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June

2016:.......................................................................................................................................2

5.4 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June

2017:.......................................................................................................................................2

6. Direct Labour Budget:........................................................................................................2

7. Sales Budget:......................................................................................................................3

Part A:.....................................................................................................................................3

(a) Scope and Nature of required budgets:.............................................................................3

(b) Identify, access and interpret data and data sources required for budget preparation:.....4

(c) Internal and external factors for potential impact on budget:...........................................4

(d) General control ledgers:....................................................................................................6

(e) Budgeted cash flow statement for Cupcake Heaven for the month ending 31 August 2017:

................................................................................................................................................6

(f) Comment on the likely future cash position of this business:..........................................7

(g) Budgeted profit and loss for the month ending 31 August 2017:.....................................7

(h)Future performance expectations of Cupcake Heaven in related to the expected profit or

loss: ........................................................................................................................................7

Part B......................................................................................................................................8

(a) Prepare a cash budget for Cakes-2-U for the period January - June 2017:.......................8

(b)...........................................................................................................................................9

(c) Budget Explanation and Recommendation:......................................................................9

Part C....................................................................................................................................10

Part 1:....................................................................................................................................10

A. Budget variance report for the quarter ended 30 September 2017:.................................10

B. Predicted cash balance on 30 September:........................................................................10

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

5.1 Calculate the budgeted cost of sales for the year ending 30 June 2016:..........................1

5.2 Prepare a budgeted income statement for the year ending 30 June 2017.........................1

5.3 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June

2016:.......................................................................................................................................2

5.4 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June

2017:.......................................................................................................................................2

6. Direct Labour Budget:........................................................................................................2

7. Sales Budget:......................................................................................................................3

Part A:.....................................................................................................................................3

(a) Scope and Nature of required budgets:.............................................................................3

(b) Identify, access and interpret data and data sources required for budget preparation:.....4

(c) Internal and external factors for potential impact on budget:...........................................4

(d) General control ledgers:....................................................................................................6

(e) Budgeted cash flow statement for Cupcake Heaven for the month ending 31 August 2017:

................................................................................................................................................6

(f) Comment on the likely future cash position of this business:..........................................7

(g) Budgeted profit and loss for the month ending 31 August 2017:.....................................7

(h)Future performance expectations of Cupcake Heaven in related to the expected profit or

loss: ........................................................................................................................................7

Part B......................................................................................................................................8

(a) Prepare a cash budget for Cakes-2-U for the period January - June 2017:.......................8

(b)...........................................................................................................................................9

(c) Budget Explanation and Recommendation:......................................................................9

Part C....................................................................................................................................10

Part 1:....................................................................................................................................10

A. Budget variance report for the quarter ended 30 September 2017:.................................10

B. Predicted cash balance on 30 September:........................................................................10

C. Actual cash balance on 30 September:............................................................................10

PART 2.................................................................................................................................11

D. Major causes of the difference between the budgeted and actual bank balance:............11

C. Appropriateness of Quarterly period for cash budgeting:...............................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

PART 2.................................................................................................................................11

D. Major causes of the difference between the budgeted and actual bank balance:............11

C. Appropriateness of Quarterly period for cash budgeting:...............................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

A budget is a financial plan which is prepared by every type of organisation to evaluate

of future activities. It is producing for particular period of time where consist of planned sales

volumes and revenues, resource quantities, costs and expenses, assets, liabilities and cash flows.

It is important to prepare and monitor budget activities in efficient manner. The report contains

practical knowledge of preparation of various budgets like cash budget, master budget etc. and

general ledger control accounts (Gupta and Yläoutinen, 2014). This report also evaluates to what

extent internal and external factors affects budgets and discussion on identification, access and

interpret data and its sources required for budget preparation.

TASK

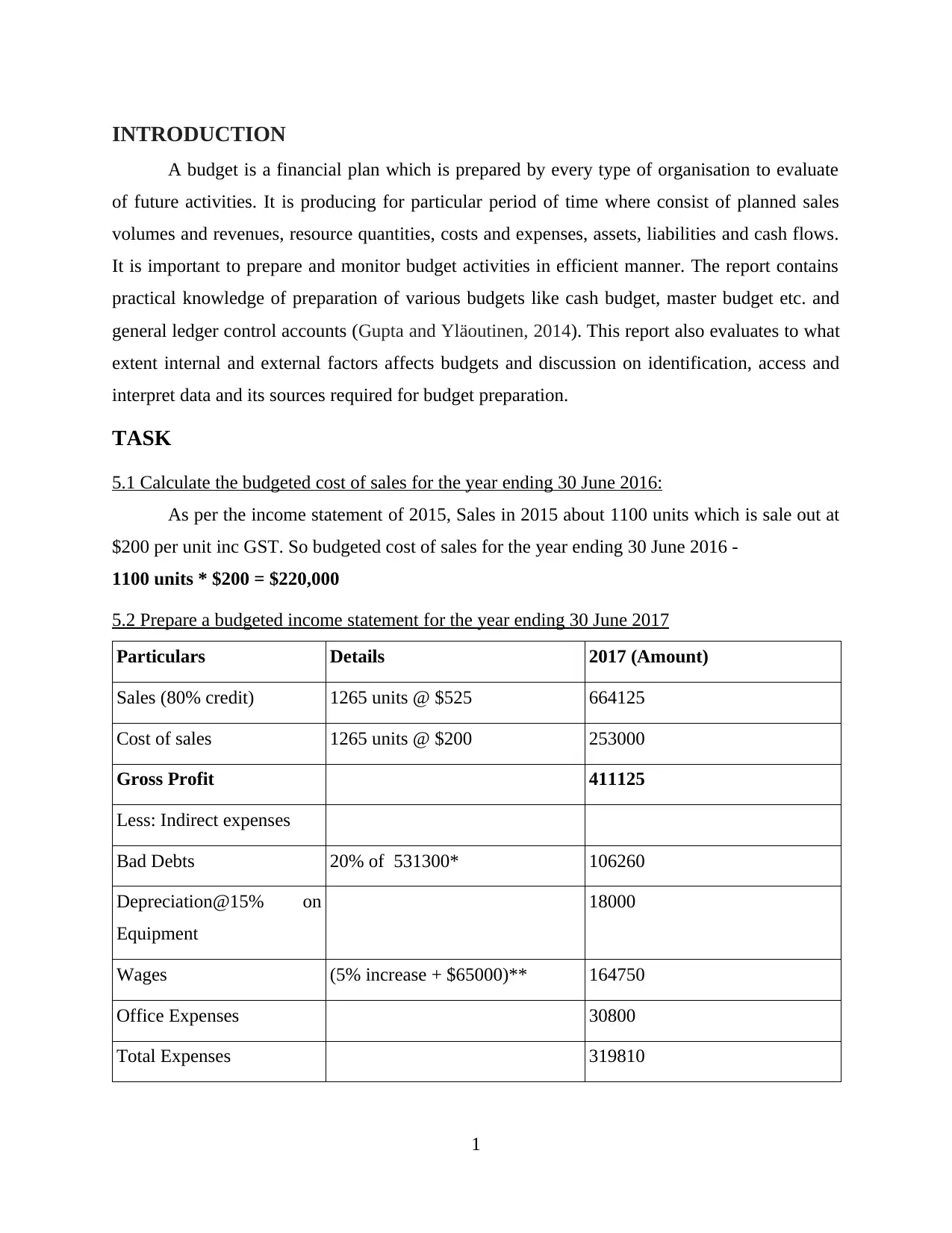

5.1 Calculate the budgeted cost of sales for the year ending 30 June 2016:

As per the income statement of 2015, Sales in 2015 about 1100 units which is sale out at

$200 per unit inc GST. So budgeted cost of sales for the year ending 30 June 2016 -

1100 units * $200 = $220,000

5.2 Prepare a budgeted income statement for the year ending 30 June 2017

Particulars Details 2017 (Amount)

Sales (80% credit) 1265 units @ $525 664125

Cost of sales 1265 units @ $200 253000

Gross Profit 411125

Less: Indirect expenses

Bad Debts 20% of 531300* 106260

Depreciation@15% on

Equipment

18000

Wages (5% increase + $65000)** 164750

Office Expenses 30800

Total Expenses 319810

1

A budget is a financial plan which is prepared by every type of organisation to evaluate

of future activities. It is producing for particular period of time where consist of planned sales

volumes and revenues, resource quantities, costs and expenses, assets, liabilities and cash flows.

It is important to prepare and monitor budget activities in efficient manner. The report contains

practical knowledge of preparation of various budgets like cash budget, master budget etc. and

general ledger control accounts (Gupta and Yläoutinen, 2014). This report also evaluates to what

extent internal and external factors affects budgets and discussion on identification, access and

interpret data and its sources required for budget preparation.

TASK

5.1 Calculate the budgeted cost of sales for the year ending 30 June 2016:

As per the income statement of 2015, Sales in 2015 about 1100 units which is sale out at

$200 per unit inc GST. So budgeted cost of sales for the year ending 30 June 2016 -

1100 units * $200 = $220,000

5.2 Prepare a budgeted income statement for the year ending 30 June 2017

Particulars Details 2017 (Amount)

Sales (80% credit) 1265 units @ $525 664125

Cost of sales 1265 units @ $200 253000

Gross Profit 411125

Less: Indirect expenses

Bad Debts 20% of 531300* 106260

Depreciation@15% on

Equipment

18000

Wages (5% increase + $65000)** 164750

Office Expenses 30800

Total Expenses 319810

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit 91315

* Credit sales is 80% of total sales i.e. 664125*80% = 531300

**Wages = ($95000*5% + $95000) + $65000 = 106260

Note:

All sales are on credit.

Bad debts 20% of credit sales.

5.3 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June 2016:

Particulars Amount Particulars Amount

To Balance b/d 52000 By Bad debts 4000

To Credit sales 440000

By Closing c/d 488000

492000 492000

5.4 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June 2017:

Debtor Control Account – It indicate the total amount which is owned by the all the

individuals debtors. It is a nominal account which is reconciled easily as accountant enter new

transaction. At the time of reconciliation of debtor control account accountant check that this

account's balance is matches with total due amount of accounts receivables.

Particulars Amount Particulars Amount

To Balance b/d 52000 By Bad debts 106260

To credit sales 531300 By collection 500,0000

To closing c/d 4522960

5106260 5106260

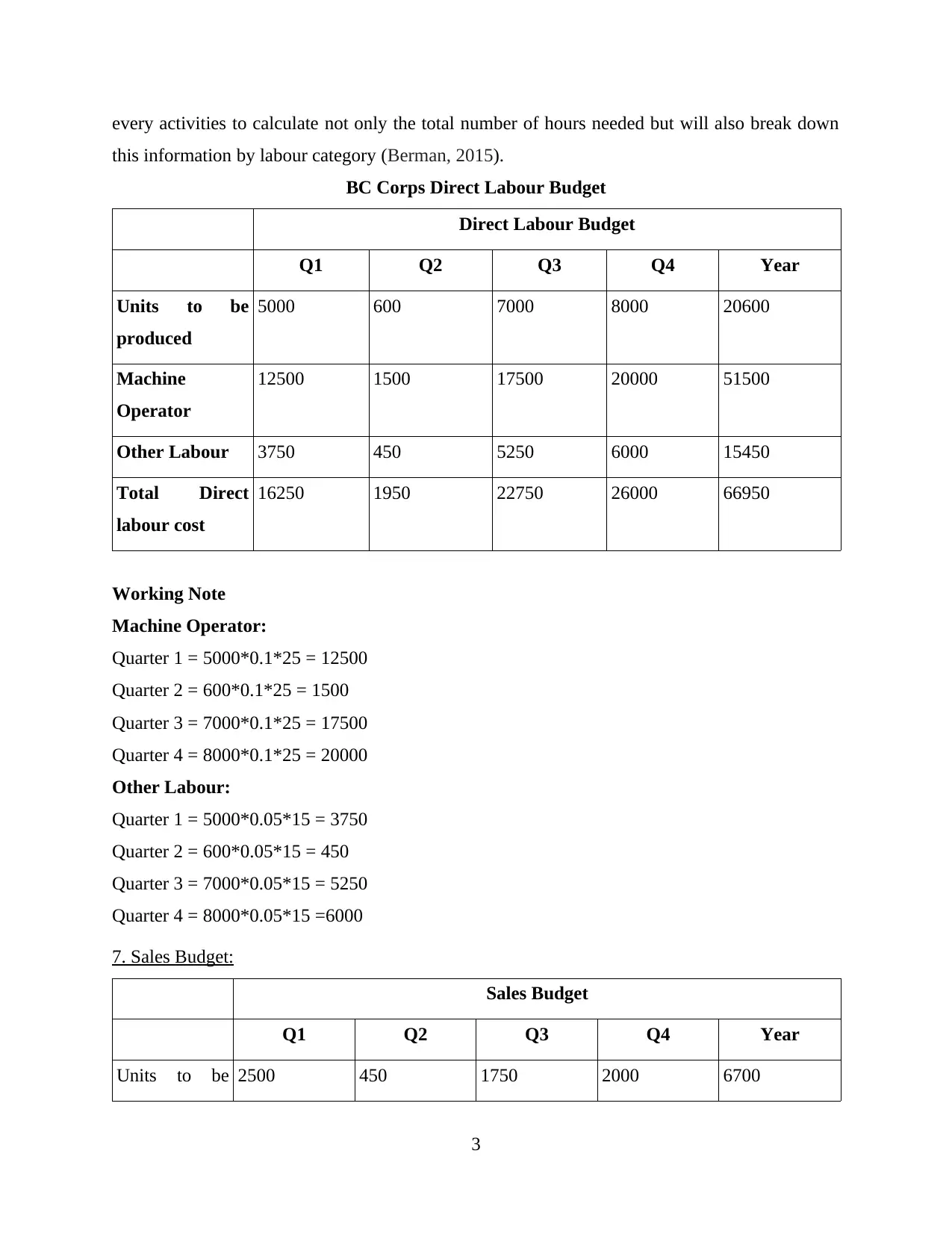

6. Direct Labour Budget:

A direct labour budget has been used to compute the labour of hours that will be required

to develop the units itemized in the manufacturing budget. It is complex to prepare and analysing

2

* Credit sales is 80% of total sales i.e. 664125*80% = 531300

**Wages = ($95000*5% + $95000) + $65000 = 106260

Note:

All sales are on credit.

Bad debts 20% of credit sales.

5.3 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June 2016:

Particulars Amount Particulars Amount

To Balance b/d 52000 By Bad debts 4000

To Credit sales 440000

By Closing c/d 488000

492000 492000

5.4 Reconstruct the Debtors control account to evaluate the estimated balance at 30 June 2017:

Debtor Control Account – It indicate the total amount which is owned by the all the

individuals debtors. It is a nominal account which is reconciled easily as accountant enter new

transaction. At the time of reconciliation of debtor control account accountant check that this

account's balance is matches with total due amount of accounts receivables.

Particulars Amount Particulars Amount

To Balance b/d 52000 By Bad debts 106260

To credit sales 531300 By collection 500,0000

To closing c/d 4522960

5106260 5106260

6. Direct Labour Budget:

A direct labour budget has been used to compute the labour of hours that will be required

to develop the units itemized in the manufacturing budget. It is complex to prepare and analysing

2

every activities to calculate not only the total number of hours needed but will also break down

this information by labour category (Berman, 2015).

BC Corps Direct Labour Budget

Direct Labour Budget

Q1 Q2 Q3 Q4 Year

Units to be

produced

5000 600 7000 8000 20600

Machine

Operator

12500 1500 17500 20000 51500

Other Labour 3750 450 5250 6000 15450

Total Direct

labour cost

16250 1950 22750 26000 66950

Working Note

Machine Operator:

Quarter 1 = 5000*0.1*25 = 12500

Quarter 2 = 600*0.1*25 = 1500

Quarter 3 = 7000*0.1*25 = 17500

Quarter 4 = 8000*0.1*25 = 20000

Other Labour:

Quarter 1 = 5000*0.05*15 = 3750

Quarter 2 = 600*0.05*15 = 450

Quarter 3 = 7000*0.05*15 = 5250

Quarter 4 = 8000*0.05*15 =6000

7. Sales Budget:

Sales Budget

Q1 Q2 Q3 Q4 Year

Units to be 2500 450 1750 2000 6700

3

this information by labour category (Berman, 2015).

BC Corps Direct Labour Budget

Direct Labour Budget

Q1 Q2 Q3 Q4 Year

Units to be

produced

5000 600 7000 8000 20600

Machine

Operator

12500 1500 17500 20000 51500

Other Labour 3750 450 5250 6000 15450

Total Direct

labour cost

16250 1950 22750 26000 66950

Working Note

Machine Operator:

Quarter 1 = 5000*0.1*25 = 12500

Quarter 2 = 600*0.1*25 = 1500

Quarter 3 = 7000*0.1*25 = 17500

Quarter 4 = 8000*0.1*25 = 20000

Other Labour:

Quarter 1 = 5000*0.05*15 = 3750

Quarter 2 = 600*0.05*15 = 450

Quarter 3 = 7000*0.05*15 = 5250

Quarter 4 = 8000*0.05*15 =6000

7. Sales Budget:

Sales Budget

Q1 Q2 Q3 Q4 Year

Units to be 2500 450 1750 2000 6700

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

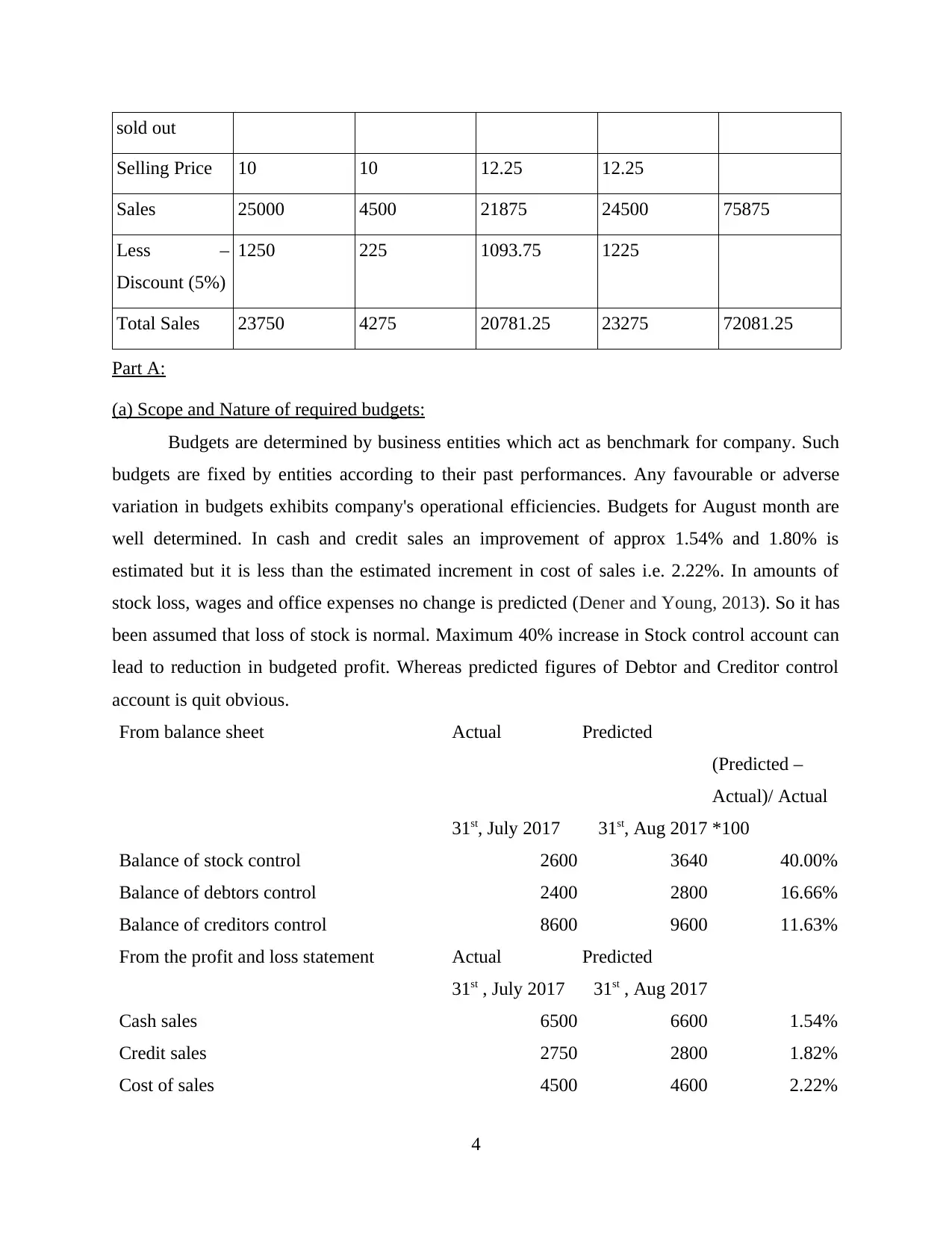

sold out

Selling Price 10 10 12.25 12.25

Sales 25000 4500 21875 24500 75875

Less –

Discount (5%)

1250 225 1093.75 1225

Total Sales 23750 4275 20781.25 23275 72081.25

Part A:

(a) Scope and Nature of required budgets:

Budgets are determined by business entities which act as benchmark for company. Such

budgets are fixed by entities according to their past performances. Any favourable or adverse

variation in budgets exhibits company's operational efficiencies. Budgets for August month are

well determined. In cash and credit sales an improvement of approx 1.54% and 1.80% is

estimated but it is less than the estimated increment in cost of sales i.e. 2.22%. In amounts of

stock loss, wages and office expenses no change is predicted (Dener and Young, 2013). So it has

been assumed that loss of stock is normal. Maximum 40% increase in Stock control account can

lead to reduction in budgeted profit. Whereas predicted figures of Debtor and Creditor control

account is quit obvious.

From balance sheet Actual Predicted

31st, July 2017 31st, Aug 2017

(Predicted –

Actual)/ Actual

*100

Balance of stock control 2600 3640 40.00%

Balance of debtors control 2400 2800 16.66%

Balance of creditors control 8600 9600 11.63%

From the profit and loss statement Actual Predicted

31st , July 2017 31st , Aug 2017

Cash sales 6500 6600 1.54%

Credit sales 2750 2800 1.82%

Cost of sales 4500 4600 2.22%

4

Selling Price 10 10 12.25 12.25

Sales 25000 4500 21875 24500 75875

Less –

Discount (5%)

1250 225 1093.75 1225

Total Sales 23750 4275 20781.25 23275 72081.25

Part A:

(a) Scope and Nature of required budgets:

Budgets are determined by business entities which act as benchmark for company. Such

budgets are fixed by entities according to their past performances. Any favourable or adverse

variation in budgets exhibits company's operational efficiencies. Budgets for August month are

well determined. In cash and credit sales an improvement of approx 1.54% and 1.80% is

estimated but it is less than the estimated increment in cost of sales i.e. 2.22%. In amounts of

stock loss, wages and office expenses no change is predicted (Dener and Young, 2013). So it has

been assumed that loss of stock is normal. Maximum 40% increase in Stock control account can

lead to reduction in budgeted profit. Whereas predicted figures of Debtor and Creditor control

account is quit obvious.

From balance sheet Actual Predicted

31st, July 2017 31st, Aug 2017

(Predicted –

Actual)/ Actual

*100

Balance of stock control 2600 3640 40.00%

Balance of debtors control 2400 2800 16.66%

Balance of creditors control 8600 9600 11.63%

From the profit and loss statement Actual Predicted

31st , July 2017 31st , Aug 2017

Cash sales 6500 6600 1.54%

Credit sales 2750 2800 1.82%

Cost of sales 4500 4600 2.22%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stock loss 800 800 -

Wages 1600 1600 -

Office expenses 200 200 -

Discount expense 110 120 9.09%

Discount revenue 150 160 6.67%

Bad debts 100 100 -

(b) Identify, access and interpret data and data sources required for budget preparation:

Generally budgets are prepared on the basis of company's objectives, historical data and

managerial personnel's experiences. In budget preparation process, at first step relevant data are

identified and classified to assess the performance result. Thereafter managers and other officials

set budgeted figures by collecting such data, historical data and applying experiences (Chen,

Weikart and Williams, 2014). Normally discussed process of identify, access and interpreting

data is part of finalisation of accounts. Only budgeted figures are determined on the basis of

analysis of past results and data sources like financial statement, income statement etc.

(c) Internal and external factors for potential impact on budget:

Budgets and other documents are are highly affected by several internal and external

factors. Such factors also determines company's efficiencies to attain targeted figures. Following

is discussion on analysis of internal and external factors for possible effect on budget and

document in a report, as follows:

Internal Factors: These factors are integral part of an organisation and have direct impact on

company's budgets. Analysis of these variables are important, as this can lead to increase in

reliability and accuracy of budgeted figures. Following are the major internal factors which can

influence company's budget, as follows:

Revenues: Budget forecasts will be affected if the real income obtained is not as

much as initially expected. External variables that adversely affect presumed income

can include an downturn in the economy, unanticipated competitiveness that causes

lower revenues or an failure to maintain the necessary growth rate (Lynch and

Tollestrup, 2012). Internal factors like insufficient collections and weak receivable

accounts can also affect revenue. Hostile forecasts that believe a high level of

5

Wages 1600 1600 -

Office expenses 200 200 -

Discount expense 110 120 9.09%

Discount revenue 150 160 6.67%

Bad debts 100 100 -

(b) Identify, access and interpret data and data sources required for budget preparation:

Generally budgets are prepared on the basis of company's objectives, historical data and

managerial personnel's experiences. In budget preparation process, at first step relevant data are

identified and classified to assess the performance result. Thereafter managers and other officials

set budgeted figures by collecting such data, historical data and applying experiences (Chen,

Weikart and Williams, 2014). Normally discussed process of identify, access and interpreting

data is part of finalisation of accounts. Only budgeted figures are determined on the basis of

analysis of past results and data sources like financial statement, income statement etc.

(c) Internal and external factors for potential impact on budget:

Budgets and other documents are are highly affected by several internal and external

factors. Such factors also determines company's efficiencies to attain targeted figures. Following

is discussion on analysis of internal and external factors for possible effect on budget and

document in a report, as follows:

Internal Factors: These factors are integral part of an organisation and have direct impact on

company's budgets. Analysis of these variables are important, as this can lead to increase in

reliability and accuracy of budgeted figures. Following are the major internal factors which can

influence company's budget, as follows:

Revenues: Budget forecasts will be affected if the real income obtained is not as

much as initially expected. External variables that adversely affect presumed income

can include an downturn in the economy, unanticipated competitiveness that causes

lower revenues or an failure to maintain the necessary growth rate (Lynch and

Tollestrup, 2012). Internal factors like insufficient collections and weak receivable

accounts can also affect revenue. Hostile forecasts that believe a high level of

5

development or enhanced income have a much higher inaccuracy capability than

optimistic estimates on the basis of previous years ' information.

Expenditure: Expenditure is most challenging variable in predicting budget.

Expenses are not reliably predictable because these may be increased or decreased by

change in circumstances. Any unanticipated fiscal event can change the variances in

actual and budgeted figures. For instance salary expenses can be predicted easily on

the basis of current pays but if any change in employee turnover will arise in future

than such prediction is not so much relevant for company.

External Factors: These are most considerable variables in budget preparation. Analysing

external factors is time consuming task and also require professional expertise. Managers always

tries to predetermine the effect of external factors as it is necessary for increasing the

creditability of budgets. Following are major external factors, as discusses below:

Market Conditions: There are several ways wherein the industry, market and present

business circumstances can affect monetary and fiscal forecasts. A shifts in rate of

inflation and events of stock market directly influence current worth of company and its

capacity to develop new resources. In case company is dependent on investments then in

case of adverse stock market condition this would lead to negative impacts on estimation

made in budgets (Kelly and Rivenbark, 2014).

Legislative Changes: Several legislature changes or happenings directly influence

budget's projections. Mostly business entities tracks pending legislation and

predetermines the effect accordingly. Introduction of any new or future legislation can

lead to change in current projections. Although a legislation doest not affect immediately

and future impact of legislation can be easily assessed by business entity.

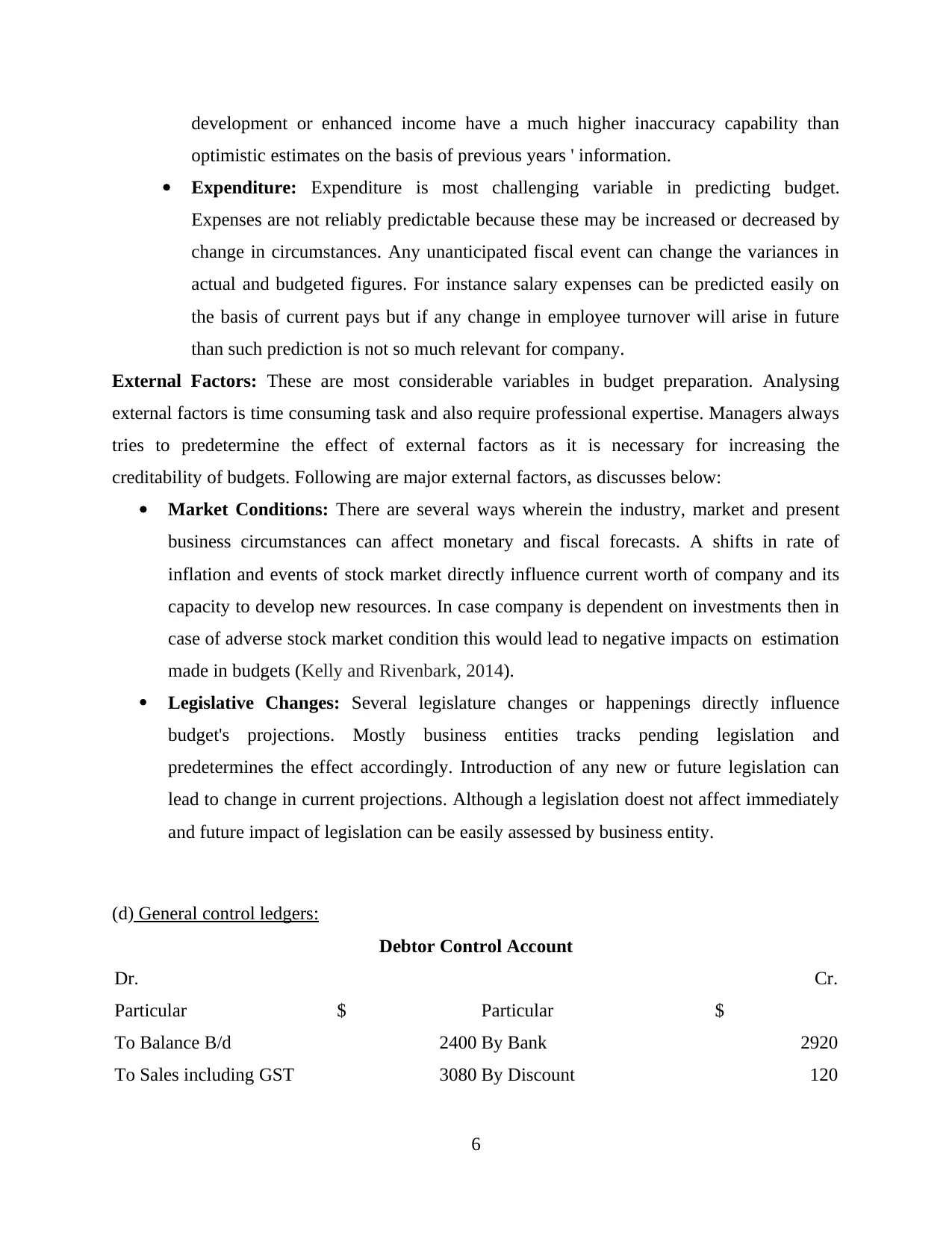

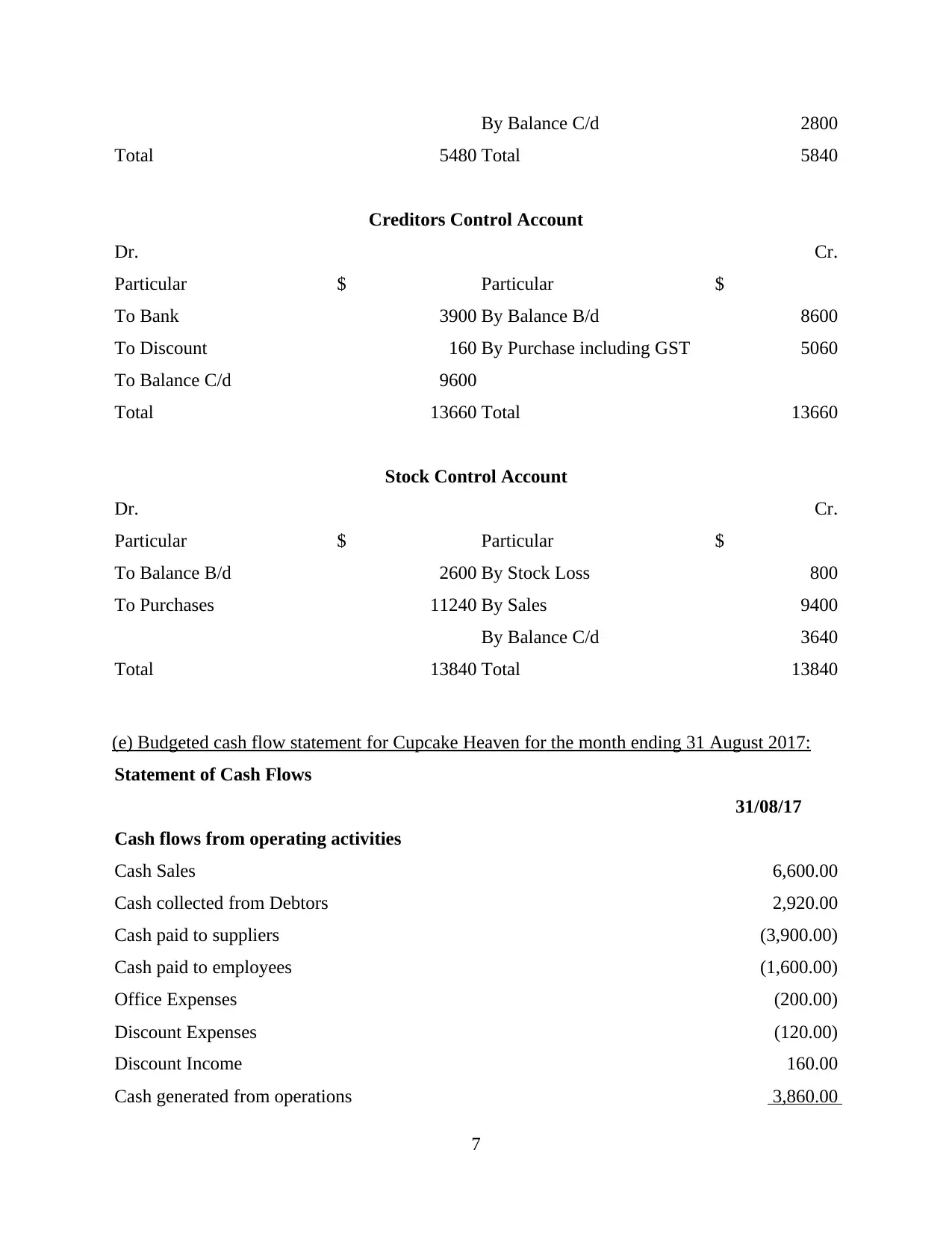

(d) General control ledgers:

Debtor Control Account

Dr. Cr.

Particular $ Particular $

To Balance B/d 2400 By Bank 2920

To Sales including GST 3080 By Discount 120

6

optimistic estimates on the basis of previous years ' information.

Expenditure: Expenditure is most challenging variable in predicting budget.

Expenses are not reliably predictable because these may be increased or decreased by

change in circumstances. Any unanticipated fiscal event can change the variances in

actual and budgeted figures. For instance salary expenses can be predicted easily on

the basis of current pays but if any change in employee turnover will arise in future

than such prediction is not so much relevant for company.

External Factors: These are most considerable variables in budget preparation. Analysing

external factors is time consuming task and also require professional expertise. Managers always

tries to predetermine the effect of external factors as it is necessary for increasing the

creditability of budgets. Following are major external factors, as discusses below:

Market Conditions: There are several ways wherein the industry, market and present

business circumstances can affect monetary and fiscal forecasts. A shifts in rate of

inflation and events of stock market directly influence current worth of company and its

capacity to develop new resources. In case company is dependent on investments then in

case of adverse stock market condition this would lead to negative impacts on estimation

made in budgets (Kelly and Rivenbark, 2014).

Legislative Changes: Several legislature changes or happenings directly influence

budget's projections. Mostly business entities tracks pending legislation and

predetermines the effect accordingly. Introduction of any new or future legislation can

lead to change in current projections. Although a legislation doest not affect immediately

and future impact of legislation can be easily assessed by business entity.

(d) General control ledgers:

Debtor Control Account

Dr. Cr.

Particular $ Particular $

To Balance B/d 2400 By Bank 2920

To Sales including GST 3080 By Discount 120

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By Balance C/d 2800

Total 5480 Total 5840

Creditors Control Account

Dr. Cr.

Particular $ Particular $

To Bank 3900 By Balance B/d 8600

To Discount 160 By Purchase including GST 5060

To Balance C/d 9600

Total 13660 Total 13660

Stock Control Account

Dr. Cr.

Particular $ Particular $

To Balance B/d 2600 By Stock Loss 800

To Purchases 11240 By Sales 9400

By Balance C/d 3640

Total 13840 Total 13840

(e) Budgeted cash flow statement for Cupcake Heaven for the month ending 31 August 2017:

Statement of Cash Flows

31/08/17

Cash flows from operating activities

Cash Sales 6,600.00

Cash collected from Debtors 2,920.00

Cash paid to suppliers (3,900.00)

Cash paid to employees (1,600.00)

Office Expenses (200.00)

Discount Expenses (120.00)

Discount Income 160.00

Cash generated from operations 3,860.00

7

Total 5480 Total 5840

Creditors Control Account

Dr. Cr.

Particular $ Particular $

To Bank 3900 By Balance B/d 8600

To Discount 160 By Purchase including GST 5060

To Balance C/d 9600

Total 13660 Total 13660

Stock Control Account

Dr. Cr.

Particular $ Particular $

To Balance B/d 2600 By Stock Loss 800

To Purchases 11240 By Sales 9400

By Balance C/d 3640

Total 13840 Total 13840

(e) Budgeted cash flow statement for Cupcake Heaven for the month ending 31 August 2017:

Statement of Cash Flows

31/08/17

Cash flows from operating activities

Cash Sales 6,600.00

Cash collected from Debtors 2,920.00

Cash paid to suppliers (3,900.00)

Cash paid to employees (1,600.00)

Office Expenses (200.00)

Discount Expenses (120.00)

Discount Income 160.00

Cash generated from operations 3,860.00

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Opening Cash Balance 3,210.00

Closing Cash Balance 7,070.00

(f) Comment on the likely future cash position of this business:

As per budgeted cash flow prepared in Point (e) it has been analysed that company has

expected a positive cash flow. Opening cash flow for August month is $3210.00 and closing

budgeted cash flow after considering all budgeted incomes and expenses, at the end of month is

$7070.00. Figures of cash collected from Debtors and Cash paid to suppliers are obtained from

budgeted ledgers.

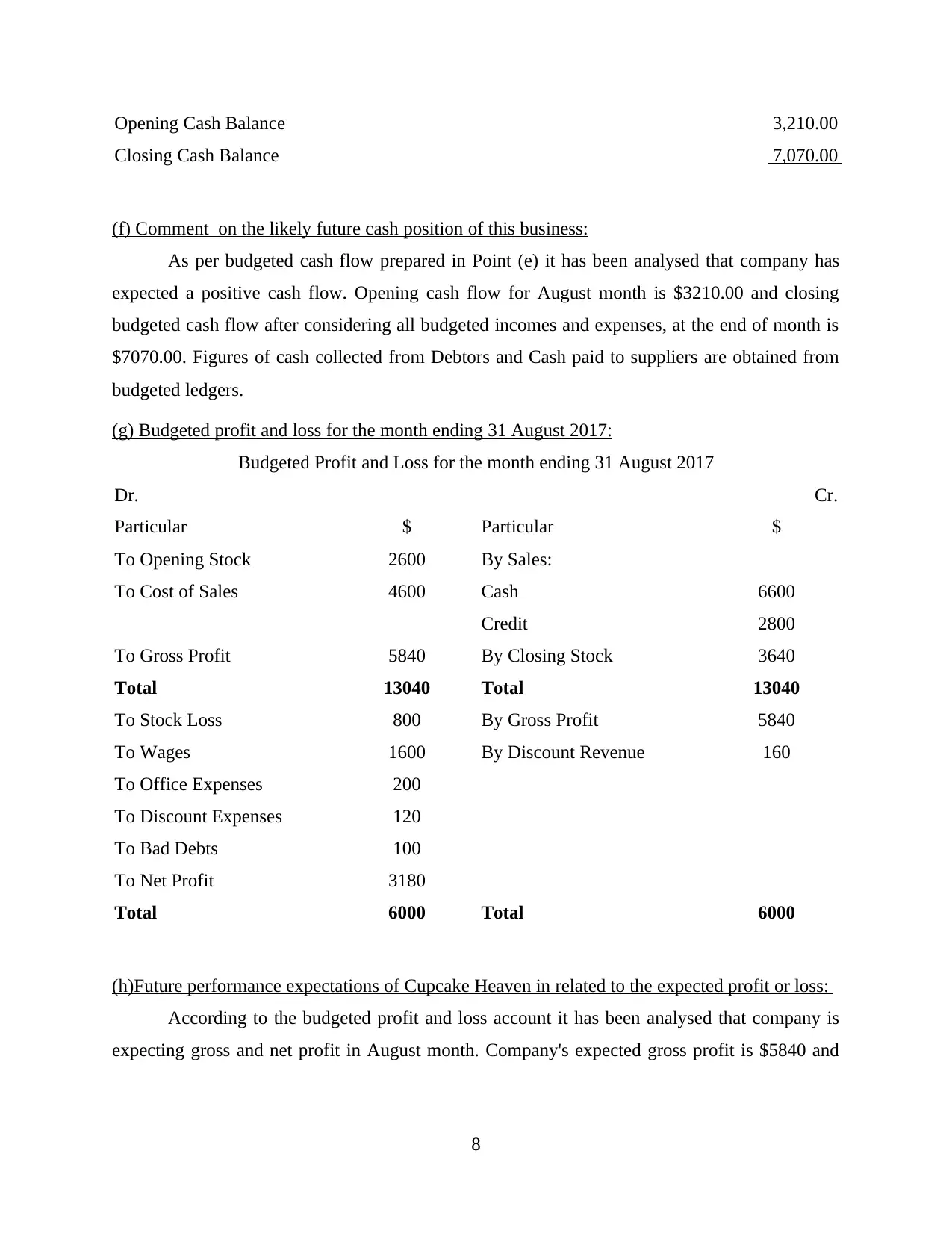

(g) Budgeted profit and loss for the month ending 31 August 2017:

Budgeted Profit and Loss for the month ending 31 August 2017

Dr. Cr.

Particular $ Particular $

To Opening Stock 2600 By Sales:

To Cost of Sales 4600 Cash 6600

Credit 2800

To Gross Profit 5840 By Closing Stock 3640

Total 13040 Total 13040

To Stock Loss 800 By Gross Profit 5840

To Wages 1600 By Discount Revenue 160

To Office Expenses 200

To Discount Expenses 120

To Bad Debts 100

To Net Profit 3180

Total 6000 Total 6000

(h)Future performance expectations of Cupcake Heaven in related to the expected profit or loss:

According to the budgeted profit and loss account it has been analysed that company is

expecting gross and net profit in August month. Company's expected gross profit is $5840 and

8

Closing Cash Balance 7,070.00

(f) Comment on the likely future cash position of this business:

As per budgeted cash flow prepared in Point (e) it has been analysed that company has

expected a positive cash flow. Opening cash flow for August month is $3210.00 and closing

budgeted cash flow after considering all budgeted incomes and expenses, at the end of month is

$7070.00. Figures of cash collected from Debtors and Cash paid to suppliers are obtained from

budgeted ledgers.

(g) Budgeted profit and loss for the month ending 31 August 2017:

Budgeted Profit and Loss for the month ending 31 August 2017

Dr. Cr.

Particular $ Particular $

To Opening Stock 2600 By Sales:

To Cost of Sales 4600 Cash 6600

Credit 2800

To Gross Profit 5840 By Closing Stock 3640

Total 13040 Total 13040

To Stock Loss 800 By Gross Profit 5840

To Wages 1600 By Discount Revenue 160

To Office Expenses 200

To Discount Expenses 120

To Bad Debts 100

To Net Profit 3180

Total 6000 Total 6000

(h)Future performance expectations of Cupcake Heaven in related to the expected profit or loss:

According to the budgeted profit and loss account it has been analysed that company is

expecting gross and net profit in August month. Company's expected gross profit is $5840 and

8

expected net profit is $3180. It indicates that company is expecting overall growth in profitability

position of company. Company has reported no change in bad-debt's amount.

9

position of company. Company has reported no change in bad-debt's amount.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.