Financial Budgeting and Analysis: Uxbridge College Solutions

VerifiedAdded on 2023/06/10

|11

|2503

|133

Homework Assignment

AI Summary

This assignment solution delves into the core concepts of financial budgeting and analysis, providing detailed insights into creating a sales budget, analyzing marginal costs, and conducting break-even analysis. The solution includes a breakdown of the problems faced in budget preparation, comparing and contrasting cost changes and their impact, and explaining the role of budgeting in supporting management and organizational activities. It also features a projected budget forecast and variance analysis, along with calculations related to break-even points and marginal costs. Furthermore, the solution analyzes the role of marginal costing as a management technique and discusses the circumstances in which it is used. The assignment uses the case study of Ztatic Trading Ltd. and B&D Clothing Ltd. to illustrate the practical application of these concepts. The document covers various aspects of financial planning, control, and decision-making within a business context, providing a comprehensive overview of financial budgeting and analysis principles.

Financial Budgeting and

Analysis

Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY...................................................................................................................................3

Task 1: Creating a Sales Budget......................................................................................................3

Part C...........................................................................................................................................3

Part D...........................................................................................................................................3

Task 2:..............................................................................................................................................4

Part A...........................................................................................................................................4

Part B...........................................................................................................................................5

Marginal Cost Calculations..........................................................................................................6

TASK 3: The Role of Budgeting.....................................................................................................7

Role of budgeting to support management and organizational activity......................................7

Task 4: Projected Budget Forecast & Variance...............................................................................8

Part C.........................................................................................................................................10

REFERENCES................................................................................................................................1

MAIN BODY...................................................................................................................................3

Task 1: Creating a Sales Budget......................................................................................................3

Part C...........................................................................................................................................3

Part D...........................................................................................................................................3

Task 2:..............................................................................................................................................4

Part A...........................................................................................................................................4

Part B...........................................................................................................................................5

Marginal Cost Calculations..........................................................................................................6

TASK 3: The Role of Budgeting.....................................................................................................7

Role of budgeting to support management and organizational activity......................................7

Task 4: Projected Budget Forecast & Variance...............................................................................8

Part C.........................................................................................................................................10

REFERENCES................................................................................................................................1

MAIN BODY

Task 1: Creating a Sales Budget

Part C

Analysing the problems faced in preparation of budget

Budget preparation requires adequate amount of data to estimate the most accurate in

case of absence of data estimation preparation of budgets become difficult. As in the given

situation of Ztatic Trading Ltd the estimate regarding the ending inventory in each case is not

given this leads to problem in creation of budget. Further, budgets prepared needs to be revised

again and again to evolve them with the changing business environment flowing the prepared

budget without considering the changes in the business environment leads to the rigidity in

decision-making. The preparation of budget is a time-consuming process involving lots of

knowledge (Khan, 2019). Managers have the tendency to prepare budgets based on deliberately

low revenue estimates and high estimated expenses to achieve favourable variances. This gaming

with the system by the managers gives rise to serious problems in the future by encouraging

them to indulge in unethical behaviour increasing the frauds in the company (Lu, Lai and Tse,

2018.). Allocation of expenses to various departments while preparation of budget is difficult and

can cause conflicts within the different departments in the company if the expense allocation

technique is not find appropriate by the departmental managers.

Part D

Comparing and Contrasting the possible changes in costs and the impact on the business’

budget

Budget shows the estimated values that the management expects to see in the future but

the actual figures always varies from the budgeted ones. Change in the budgeted figures happens

due to changes in the fixed and variable costs (Salim and Negara, 2018). The changes in the fixed

and variable overheads results in generation of actual profits different from the estimated profit

reflected by the budget. For example, the budget show fixed factory rent as £200,000 per annum.

But the actual rent increased by the 5% during the year. Thus, the profit in budget will differ by

£10,000 then the actual profit. The actual profit for the year will be less by £10,000. Similarly, if

the budgeted advertising expenses were £120000 for the year. But the firm decides to spend

£20,000 more on social media marketing, the result will reflect in the profit amount being less by

Task 1: Creating a Sales Budget

Part C

Analysing the problems faced in preparation of budget

Budget preparation requires adequate amount of data to estimate the most accurate in

case of absence of data estimation preparation of budgets become difficult. As in the given

situation of Ztatic Trading Ltd the estimate regarding the ending inventory in each case is not

given this leads to problem in creation of budget. Further, budgets prepared needs to be revised

again and again to evolve them with the changing business environment flowing the prepared

budget without considering the changes in the business environment leads to the rigidity in

decision-making. The preparation of budget is a time-consuming process involving lots of

knowledge (Khan, 2019). Managers have the tendency to prepare budgets based on deliberately

low revenue estimates and high estimated expenses to achieve favourable variances. This gaming

with the system by the managers gives rise to serious problems in the future by encouraging

them to indulge in unethical behaviour increasing the frauds in the company (Lu, Lai and Tse,

2018.). Allocation of expenses to various departments while preparation of budget is difficult and

can cause conflicts within the different departments in the company if the expense allocation

technique is not find appropriate by the departmental managers.

Part D

Comparing and Contrasting the possible changes in costs and the impact on the business’

budget

Budget shows the estimated values that the management expects to see in the future but

the actual figures always varies from the budgeted ones. Change in the budgeted figures happens

due to changes in the fixed and variable costs (Salim and Negara, 2018). The changes in the fixed

and variable overheads results in generation of actual profits different from the estimated profit

reflected by the budget. For example, the budget show fixed factory rent as £200,000 per annum.

But the actual rent increased by the 5% during the year. Thus, the profit in budget will differ by

£10,000 then the actual profit. The actual profit for the year will be less by £10,000. Similarly, if

the budgeted advertising expenses were £120000 for the year. But the firm decides to spend

£20,000 more on social media marketing, the result will reflect in the profit amount being less by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

£20,000. Also, the spending will result in high sales turnover increasing the actual profit amount

in comparison to the budgeted.

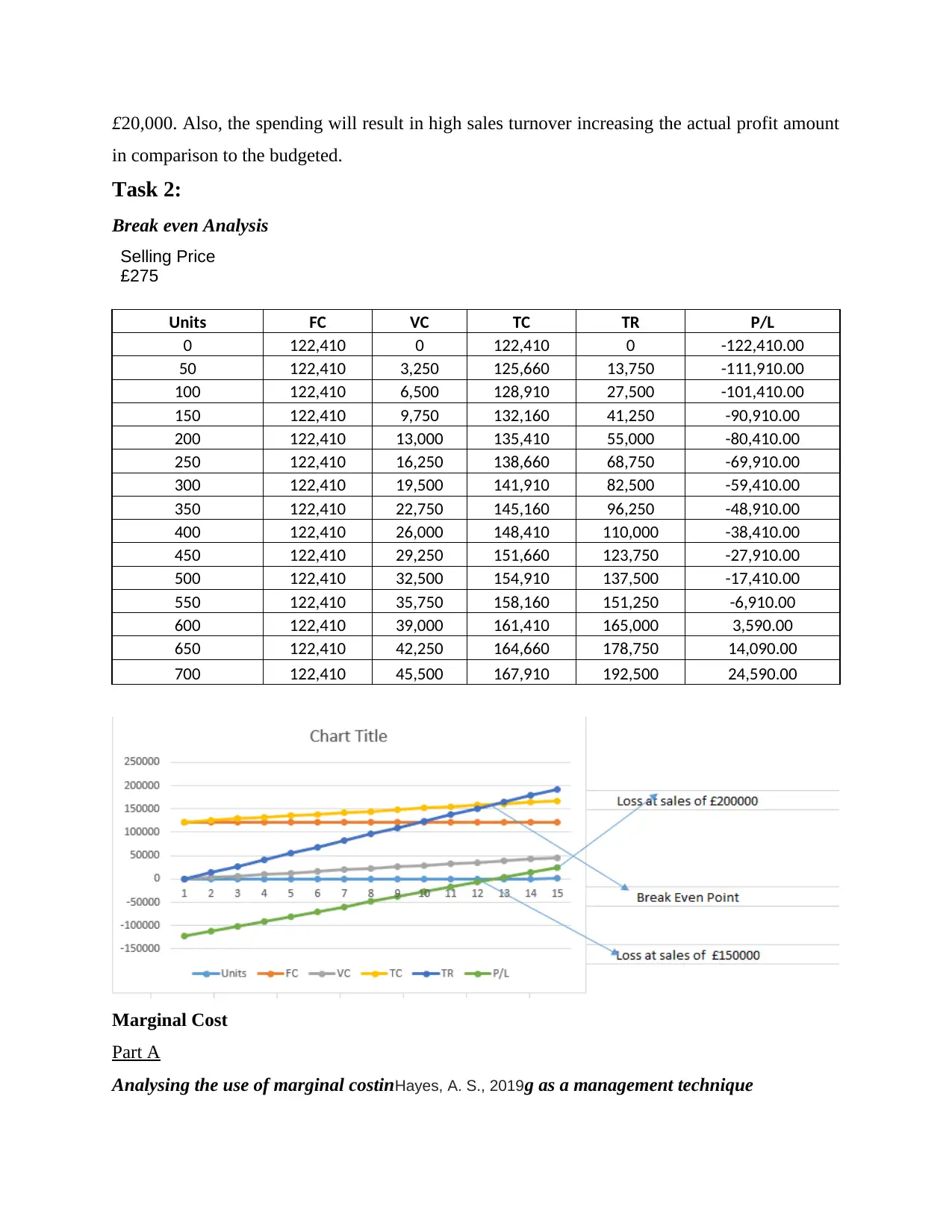

Task 2:

Break even Analysis

Selling Price

£275

Units FC VC TC TR P/L

0 122,410 0 122,410 0 -122,410.00

50 122,410 3,250 125,660 13,750 -111,910.00

100 122,410 6,500 128,910 27,500 -101,410.00

150 122,410 9,750 132,160 41,250 -90,910.00

200 122,410 13,000 135,410 55,000 -80,410.00

250 122,410 16,250 138,660 68,750 -69,910.00

300 122,410 19,500 141,910 82,500 -59,410.00

350 122,410 22,750 145,160 96,250 -48,910.00

400 122,410 26,000 148,410 110,000 -38,410.00

450 122,410 29,250 151,660 123,750 -27,910.00

500 122,410 32,500 154,910 137,500 -17,410.00

550 122,410 35,750 158,160 151,250 -6,910.00

600 122,410 39,000 161,410 165,000 3,590.00

650 122,410 42,250 164,660 178,750 14,090.00

700 122,410 45,500 167,910 192,500 24,590.00

Marginal Cost

Part A

Analysing the use of marginal costinHayes, A. S., 2019g as a management technique

in comparison to the budgeted.

Task 2:

Break even Analysis

Selling Price

£275

Units FC VC TC TR P/L

0 122,410 0 122,410 0 -122,410.00

50 122,410 3,250 125,660 13,750 -111,910.00

100 122,410 6,500 128,910 27,500 -101,410.00

150 122,410 9,750 132,160 41,250 -90,910.00

200 122,410 13,000 135,410 55,000 -80,410.00

250 122,410 16,250 138,660 68,750 -69,910.00

300 122,410 19,500 141,910 82,500 -59,410.00

350 122,410 22,750 145,160 96,250 -48,910.00

400 122,410 26,000 148,410 110,000 -38,410.00

450 122,410 29,250 151,660 123,750 -27,910.00

500 122,410 32,500 154,910 137,500 -17,410.00

550 122,410 35,750 158,160 151,250 -6,910.00

600 122,410 39,000 161,410 165,000 3,590.00

650 122,410 42,250 164,660 178,750 14,090.00

700 122,410 45,500 167,910 192,500 24,590.00

Marginal Cost

Part A

Analysing the use of marginal costinHayes, A. S., 2019g as a management technique

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

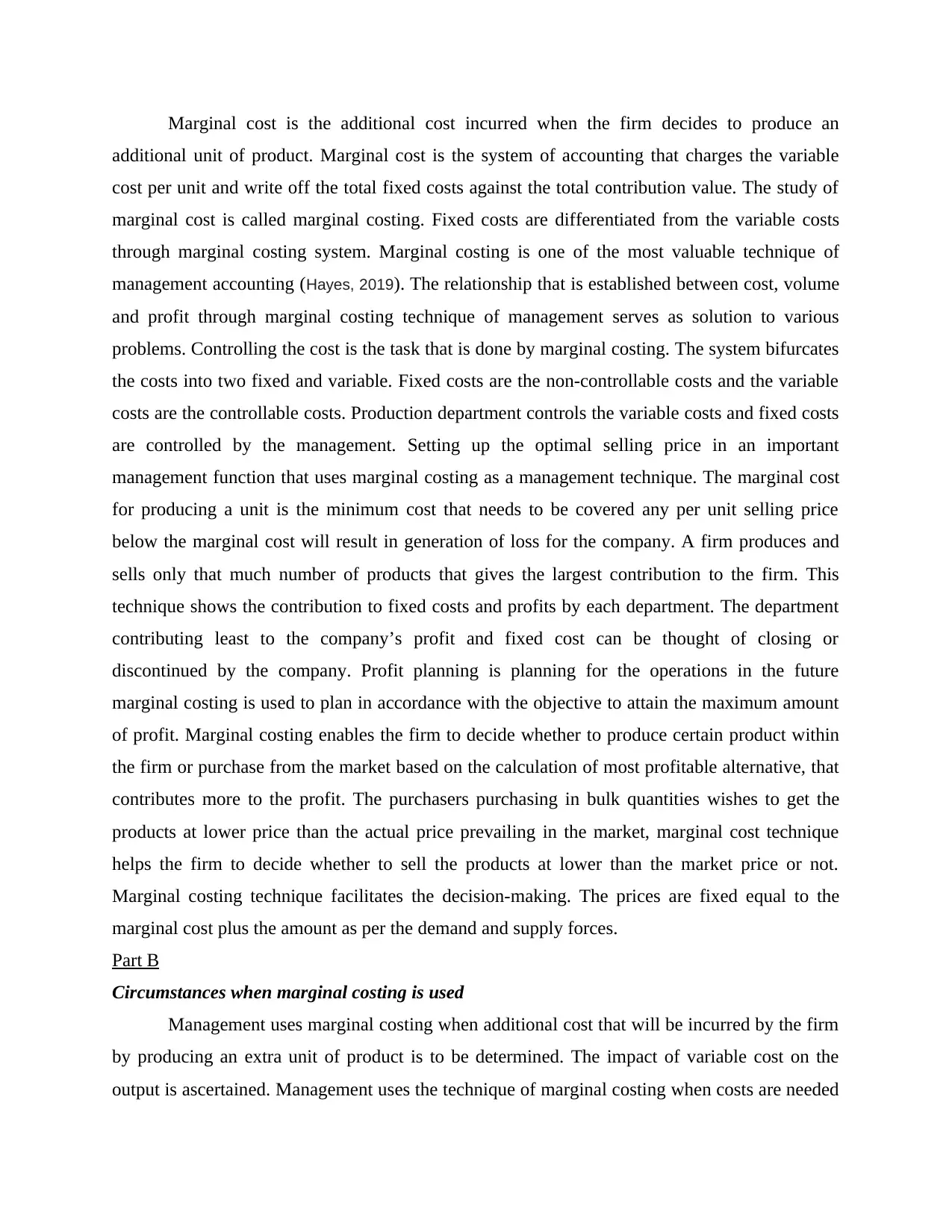

Marginal cost is the additional cost incurred when the firm decides to produce an

additional unit of product. Marginal cost is the system of accounting that charges the variable

cost per unit and write off the total fixed costs against the total contribution value. The study of

marginal cost is called marginal costing. Fixed costs are differentiated from the variable costs

through marginal costing system. Marginal costing is one of the most valuable technique of

management accounting (Hayes, 2019). The relationship that is established between cost, volume

and profit through marginal costing technique of management serves as solution to various

problems. Controlling the cost is the task that is done by marginal costing. The system bifurcates

the costs into two fixed and variable. Fixed costs are the non-controllable costs and the variable

costs are the controllable costs. Production department controls the variable costs and fixed costs

are controlled by the management. Setting up the optimal selling price in an important

management function that uses marginal costing as a management technique. The marginal cost

for producing a unit is the minimum cost that needs to be covered any per unit selling price

below the marginal cost will result in generation of loss for the company. A firm produces and

sells only that much number of products that gives the largest contribution to the firm. This

technique shows the contribution to fixed costs and profits by each department. The department

contributing least to the company’s profit and fixed cost can be thought of closing or

discontinued by the company. Profit planning is planning for the operations in the future

marginal costing is used to plan in accordance with the objective to attain the maximum amount

of profit. Marginal costing enables the firm to decide whether to produce certain product within

the firm or purchase from the market based on the calculation of most profitable alternative, that

contributes more to the profit. The purchasers purchasing in bulk quantities wishes to get the

products at lower price than the actual price prevailing in the market, marginal cost technique

helps the firm to decide whether to sell the products at lower than the market price or not.

Marginal costing technique facilitates the decision-making. The prices are fixed equal to the

marginal cost plus the amount as per the demand and supply forces.

Part B

Circumstances when marginal costing is used

Management uses marginal costing when additional cost that will be incurred by the firm

by producing an extra unit of product is to be determined. The impact of variable cost on the

output is ascertained. Management uses the technique of marginal costing when costs are needed

additional unit of product. Marginal cost is the system of accounting that charges the variable

cost per unit and write off the total fixed costs against the total contribution value. The study of

marginal cost is called marginal costing. Fixed costs are differentiated from the variable costs

through marginal costing system. Marginal costing is one of the most valuable technique of

management accounting (Hayes, 2019). The relationship that is established between cost, volume

and profit through marginal costing technique of management serves as solution to various

problems. Controlling the cost is the task that is done by marginal costing. The system bifurcates

the costs into two fixed and variable. Fixed costs are the non-controllable costs and the variable

costs are the controllable costs. Production department controls the variable costs and fixed costs

are controlled by the management. Setting up the optimal selling price in an important

management function that uses marginal costing as a management technique. The marginal cost

for producing a unit is the minimum cost that needs to be covered any per unit selling price

below the marginal cost will result in generation of loss for the company. A firm produces and

sells only that much number of products that gives the largest contribution to the firm. This

technique shows the contribution to fixed costs and profits by each department. The department

contributing least to the company’s profit and fixed cost can be thought of closing or

discontinued by the company. Profit planning is planning for the operations in the future

marginal costing is used to plan in accordance with the objective to attain the maximum amount

of profit. Marginal costing enables the firm to decide whether to produce certain product within

the firm or purchase from the market based on the calculation of most profitable alternative, that

contributes more to the profit. The purchasers purchasing in bulk quantities wishes to get the

products at lower price than the actual price prevailing in the market, marginal cost technique

helps the firm to decide whether to sell the products at lower than the market price or not.

Marginal costing technique facilitates the decision-making. The prices are fixed equal to the

marginal cost plus the amount as per the demand and supply forces.

Part B

Circumstances when marginal costing is used

Management uses marginal costing when additional cost that will be incurred by the firm

by producing an extra unit of product is to be determined. The impact of variable cost on the

output is ascertained. Management uses the technique of marginal costing when costs are needed

to be classified as fixed or variable costs. The costing method is used to determine the value of

stock of work in progress and the goods finished. For selling price determination contribution is

added to marginal cost. Using the marginal costing the profits are calculated as sales less the sum

of marginal and fixed cost incurred. In the circumstance of calculation of Break Even point

determination marginal costing plays an important role (Wolak, 2021). The contribution of each

department in the overall profits of the company needs to be determined to make the decision of

their continuation or discontinuation. The contribution by each department is based on marginal

costing technique.

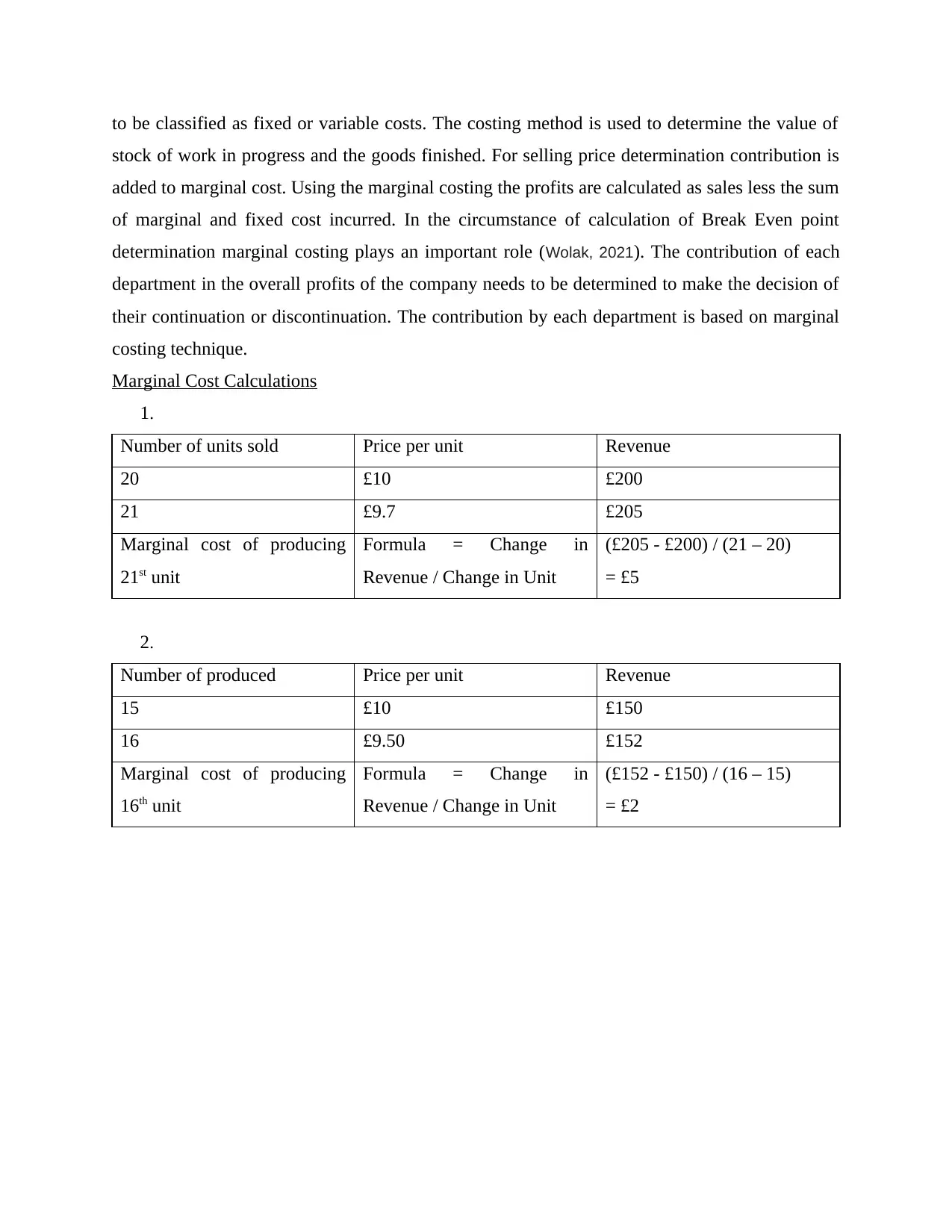

Marginal Cost Calculations

1.

Number of units sold Price per unit Revenue

20 £10 £200

21 £9.7 £205

Marginal cost of producing

21st unit

Formula = Change in

Revenue / Change in Unit

(£205 - £200) / (21 – 20)

= £5

2.

Number of produced Price per unit Revenue

15 £10 £150

16 £9.50 £152

Marginal cost of producing

16th unit

Formula = Change in

Revenue / Change in Unit

(£152 - £150) / (16 – 15)

= £2

stock of work in progress and the goods finished. For selling price determination contribution is

added to marginal cost. Using the marginal costing the profits are calculated as sales less the sum

of marginal and fixed cost incurred. In the circumstance of calculation of Break Even point

determination marginal costing plays an important role (Wolak, 2021). The contribution of each

department in the overall profits of the company needs to be determined to make the decision of

their continuation or discontinuation. The contribution by each department is based on marginal

costing technique.

Marginal Cost Calculations

1.

Number of units sold Price per unit Revenue

20 £10 £200

21 £9.7 £205

Marginal cost of producing

21st unit

Formula = Change in

Revenue / Change in Unit

(£205 - £200) / (21 – 20)

= £5

2.

Number of produced Price per unit Revenue

15 £10 £150

16 £9.50 £152

Marginal cost of producing

16th unit

Formula = Change in

Revenue / Change in Unit

(£152 - £150) / (16 – 15)

= £2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3: The Role of Budgeting

Role of budgeting to support management and organizational activity

Budgeting refers to the process of creating a proper plan in order to spend money in the

organization. By creating the budget it helps the organization to determine in advance that they

are available with the enough amount in order to do expenses in present and future. This is

basically done by balancing the expenses with the income of the organization. It is important for

the company to have the strategic planning that helps them to create the budget and have proper

organizational activity (Scott and Enu-Kwesi, 2018). By having the good budgeting system it

helps the Ztatic Trading Ltd. To reach its strategic goals by having the proper management of

planning and control its activities such as revenue, financing options and expenses. Budget used

to play and important role in the financial implications of the plans and helps the company to

measure, view and control its results with the made plan. By having the good plan it ensures the

owner of the business to focus on the cash flows, reducing costs, improving the profits and have

good return on investments. This used to help the company by having he proper planning and

controlling of the finances of the organization.

Budgeting helps the managers to have communication with the employees regarding the

plan made which used to have proper coordination in the entire company. The budget made is

basically compared with the actual results which helps the company to know about the areas they

are lacking. The main aim of making the budget is to have the proper management plan and have

good organizational activities. This used to provide the process of controlling the income and

have optimum utilization of resources which makes them to have less expenditure. By having the

proper planning of the expenditure it provides the company to evaluate its policies and attain the

organizational goals (Ostaev and et.al., 2019). The cited organization must have the proper

budgeting of the expenses which makes them to have good productivity and profitability in the

market. The budgets are basically made in advance in order to help the organization to have

proper flow of money and makes the employees to have proper coordination in the organization.

These budgets made by the cited organization are compared with the actual results in order to

check the employee and organizational performance. This used to have proper management in

the cited organization and makes the organization to achieve the profitability in the market by

having more sales. By tis it helps the organization to have the cost reduction of its goods by

having the optimum utilization of the resources. This is the main base for the company to get

Role of budgeting to support management and organizational activity

Budgeting refers to the process of creating a proper plan in order to spend money in the

organization. By creating the budget it helps the organization to determine in advance that they

are available with the enough amount in order to do expenses in present and future. This is

basically done by balancing the expenses with the income of the organization. It is important for

the company to have the strategic planning that helps them to create the budget and have proper

organizational activity (Scott and Enu-Kwesi, 2018). By having the good budgeting system it

helps the Ztatic Trading Ltd. To reach its strategic goals by having the proper management of

planning and control its activities such as revenue, financing options and expenses. Budget used

to play and important role in the financial implications of the plans and helps the company to

measure, view and control its results with the made plan. By having the good plan it ensures the

owner of the business to focus on the cash flows, reducing costs, improving the profits and have

good return on investments. This used to help the company by having he proper planning and

controlling of the finances of the organization.

Budgeting helps the managers to have communication with the employees regarding the

plan made which used to have proper coordination in the entire company. The budget made is

basically compared with the actual results which helps the company to know about the areas they

are lacking. The main aim of making the budget is to have the proper management plan and have

good organizational activities. This used to provide the process of controlling the income and

have optimum utilization of resources which makes them to have less expenditure. By having the

proper planning of the expenditure it provides the company to evaluate its policies and attain the

organizational goals (Ostaev and et.al., 2019). The cited organization must have the proper

budgeting of the expenses which makes them to have good productivity and profitability in the

market. The budgets are basically made in advance in order to help the organization to have

proper flow of money and makes the employees to have proper coordination in the organization.

These budgets made by the cited organization are compared with the actual results in order to

check the employee and organizational performance. This used to have proper management in

the cited organization and makes the organization to achieve the profitability in the market by

having more sales. By tis it helps the organization to have the cost reduction of its goods by

having the optimum utilization of the resources. This is the main base for the company to get

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

success and attain the good profits in the market. By having the proper planning of the budget it

helps the organization to know about amount they are needed in order to achieve the profits. The

cited organization must have the proper budgeting which helps them to focus on the cash flows,

reducing costs, improving the profits, etc.

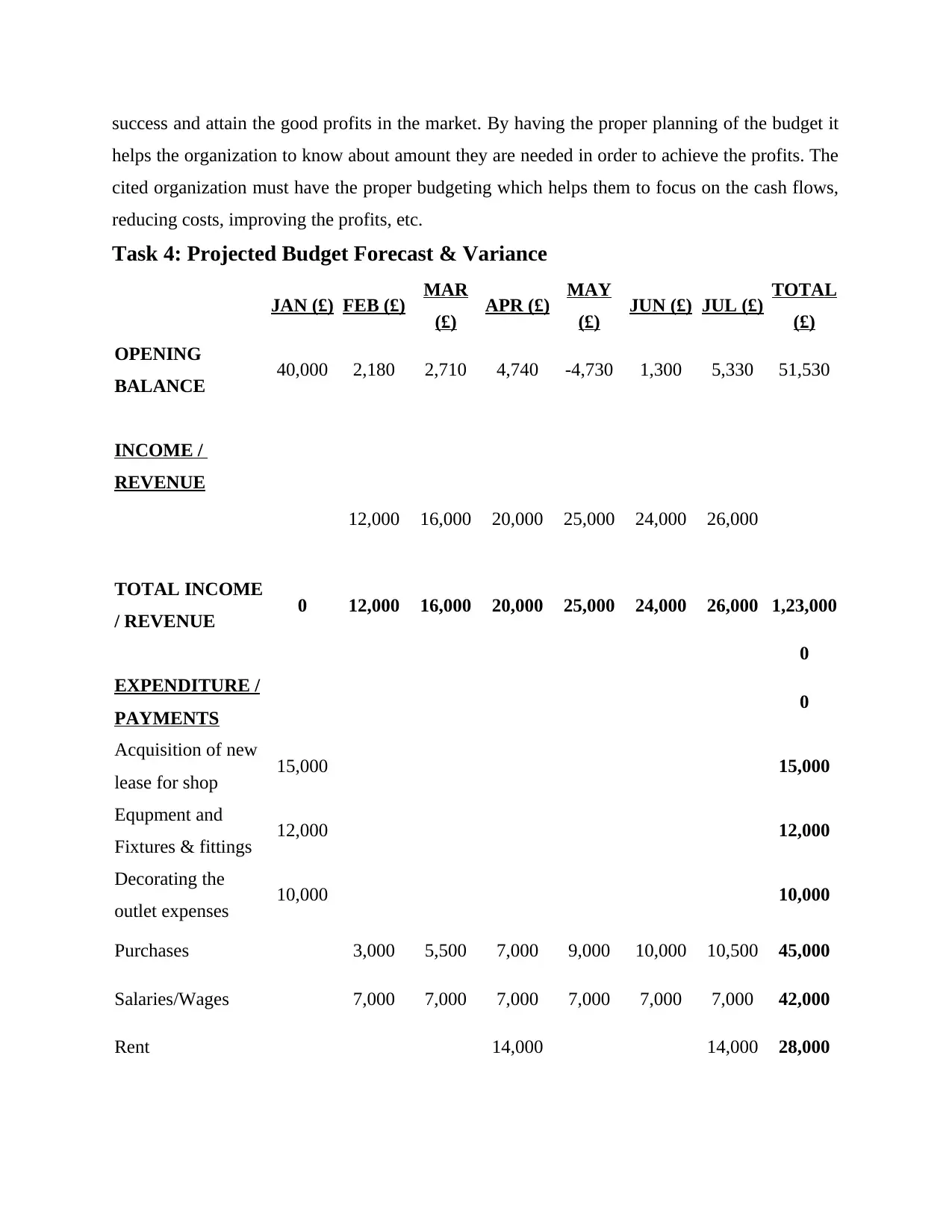

Task 4: Projected Budget Forecast & Variance

JAN (£) FEB (£) MAR

(£) APR (£) MAY

(£) JUN (£) JUL (£) TOTAL

(£)

OPENING

BALANCE 40,000 2,180 2,710 4,740 -4,730 1,300 5,330 51,530

INCOME /

REVENUE

12,000 16,000 20,000 25,000 24,000 26,000

TOTAL INCOME

/ REVENUE 0 12,000 16,000 20,000 25,000 24,000 26,000 1,23,000

0

EXPENDITURE /

PAYMENTS 0

Acquisition of new

lease for shop 15,000 15,000

Equpment and

Fixtures & fittings 12,000 12,000

Decorating the

outlet expenses 10,000 10,000

Purchases 3,000 5,500 7,000 9,000 10,000 10,500 45,000

Salaries/Wages 7,000 7,000 7,000 7,000 7,000 7,000 42,000

Rent 14,000 14,000 28,000

helps the organization to know about amount they are needed in order to achieve the profits. The

cited organization must have the proper budgeting which helps them to focus on the cash flows,

reducing costs, improving the profits, etc.

Task 4: Projected Budget Forecast & Variance

JAN (£) FEB (£) MAR

(£) APR (£) MAY

(£) JUN (£) JUL (£) TOTAL

(£)

OPENING

BALANCE 40,000 2,180 2,710 4,740 -4,730 1,300 5,330 51,530

INCOME /

REVENUE

12,000 16,000 20,000 25,000 24,000 26,000

TOTAL INCOME

/ REVENUE 0 12,000 16,000 20,000 25,000 24,000 26,000 1,23,000

0

EXPENDITURE /

PAYMENTS 0

Acquisition of new

lease for shop 15,000 15,000

Equpment and

Fixtures & fittings 12,000 12,000

Decorating the

outlet expenses 10,000 10,000

Purchases 3,000 5,500 7,000 9,000 10,000 10,500 45,000

Salaries/Wages 7,000 7,000 7,000 7,000 7,000 7,000 42,000

Rent 14,000 14,000 28,000

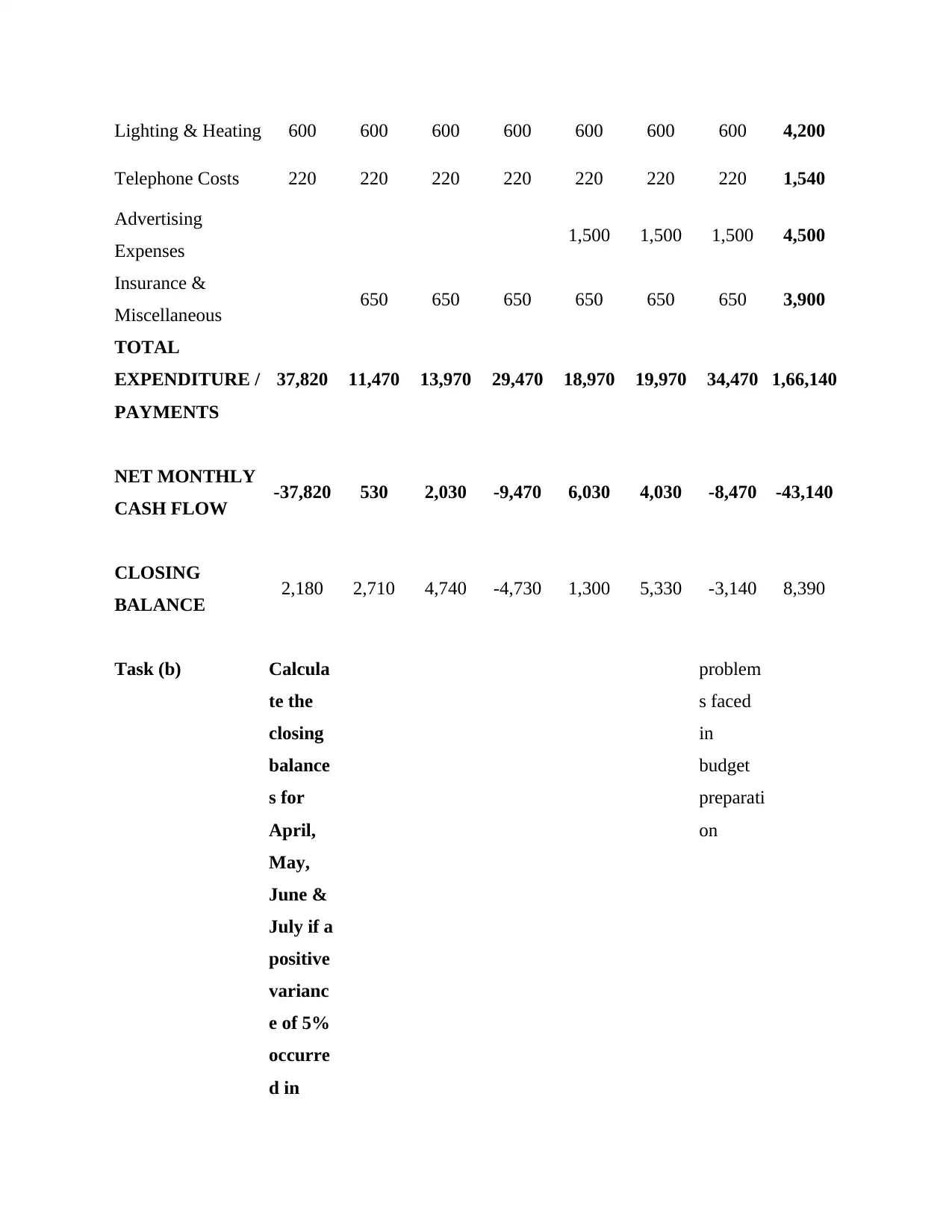

Lighting & Heating 600 600 600 600 600 600 600 4,200

Telephone Costs 220 220 220 220 220 220 220 1,540

Advertising

Expenses 1,500 1,500 1,500 4,500

Insurance &

Miscellaneous 650 650 650 650 650 650 3,900

TOTAL

EXPENDITURE /

PAYMENTS

37,820 11,470 13,970 29,470 18,970 19,970 34,470 1,66,140

NET MONTHLY

CASH FLOW -37,820 530 2,030 -9,470 6,030 4,030 -8,470 -43,140

CLOSING

BALANCE 2,180 2,710 4,740 -4,730 1,300 5,330 -3,140 8,390

Task (b) Calcula

te the

closing

balance

s for

April,

May,

June &

July if a

positive

varianc

e of 5%

occurre

d in

problem

s faced

in

budget

preparati

on

Telephone Costs 220 220 220 220 220 220 220 1,540

Advertising

Expenses 1,500 1,500 1,500 4,500

Insurance &

Miscellaneous 650 650 650 650 650 650 3,900

TOTAL

EXPENDITURE /

PAYMENTS

37,820 11,470 13,970 29,470 18,970 19,970 34,470 1,66,140

NET MONTHLY

CASH FLOW -37,820 530 2,030 -9,470 6,030 4,030 -8,470 -43,140

CLOSING

BALANCE 2,180 2,710 4,740 -4,730 1,300 5,330 -3,140 8,390

Task (b) Calcula

te the

closing

balance

s for

April,

May,

June &

July if a

positive

varianc

e of 5%

occurre

d in

problem

s faced

in

budget

preparati

on

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

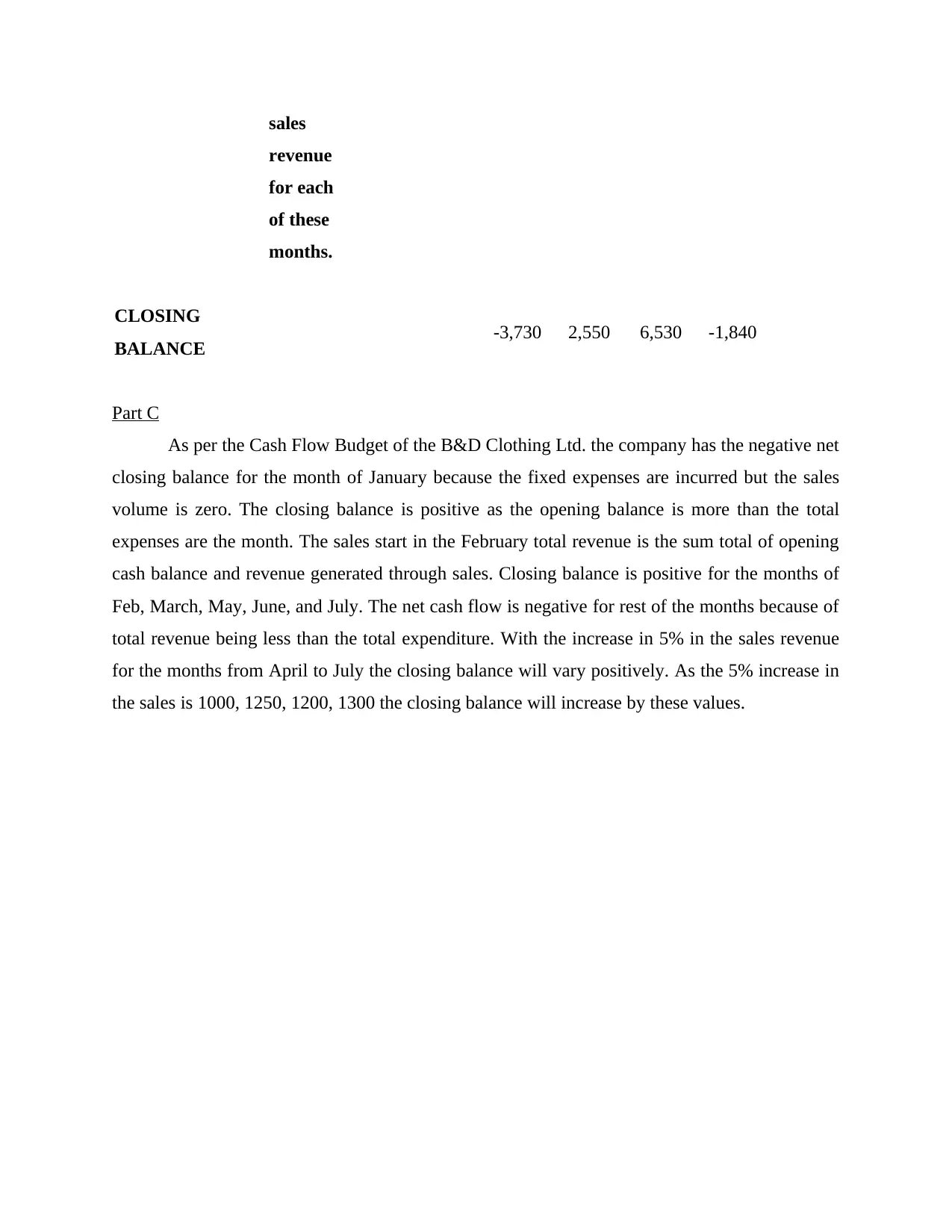

sales

revenue

for each

of these

months.

CLOSING

BALANCE -3,730 2,550 6,530 -1,840

Part C

As per the Cash Flow Budget of the B&D Clothing Ltd. the company has the negative net

closing balance for the month of January because the fixed expenses are incurred but the sales

volume is zero. The closing balance is positive as the opening balance is more than the total

expenses are the month. The sales start in the February total revenue is the sum total of opening

cash balance and revenue generated through sales. Closing balance is positive for the months of

Feb, March, May, June, and July. The net cash flow is negative for rest of the months because of

total revenue being less than the total expenditure. With the increase in 5% in the sales revenue

for the months from April to July the closing balance will vary positively. As the 5% increase in

the sales is 1000, 1250, 1200, 1300 the closing balance will increase by these values.

revenue

for each

of these

months.

CLOSING

BALANCE -3,730 2,550 6,530 -1,840

Part C

As per the Cash Flow Budget of the B&D Clothing Ltd. the company has the negative net

closing balance for the month of January because the fixed expenses are incurred but the sales

volume is zero. The closing balance is positive as the opening balance is more than the total

expenses are the month. The sales start in the February total revenue is the sum total of opening

cash balance and revenue generated through sales. Closing balance is positive for the months of

Feb, March, May, June, and July. The net cash flow is negative for rest of the months because of

total revenue being less than the total expenditure. With the increase in 5% in the sales revenue

for the months from April to July the closing balance will vary positively. As the 5% increase in

the sales is 1000, 1250, 1200, 1300 the closing balance will increase by these values.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Hayes, A. S., 2019. Bitcoin price and its marginal cost of production: support for a fundamental

value. Applied Economics Letters. 26(7). pp.554-560.

Khan, A., 2019. Fundamentals of Public Budgeting and Finance. Springer Nature.

Lu, W., Lai, C. C. and Tse, T., 2018. BIM and Big Data for Construction Cost Management.

Routledge.

Ostaev, G. Y. and et.al., 2019. Integrated budgeting at agricultural enterprises: functionality and

management decision making. Amazonia Investiga. 8(22). pp.593-601.

Salim, W. and Negara, S.D., 2018. Infrastructure development under the Jokowi administration:

Progress, challenges and policies. Journal of Southeast Asian Economies. 35(3). pp.386-

401.

Scott, G. K. and Enu-Kwesi, F., 2018. Role of budgeting practices in service delivery in the

public sector: A study of district assemblies in Ghana. Hum Resour Manag Res. 8.

pp.23-33.

Wolak, F. A., 2021. Market design in an intermittent renewable future: cost recovery with zero-

marginal-cost resources. IEEE Power and Energy Magazine. 19(1). pp.29-40.

1

Books and Journals

Hayes, A. S., 2019. Bitcoin price and its marginal cost of production: support for a fundamental

value. Applied Economics Letters. 26(7). pp.554-560.

Khan, A., 2019. Fundamentals of Public Budgeting and Finance. Springer Nature.

Lu, W., Lai, C. C. and Tse, T., 2018. BIM and Big Data for Construction Cost Management.

Routledge.

Ostaev, G. Y. and et.al., 2019. Integrated budgeting at agricultural enterprises: functionality and

management decision making. Amazonia Investiga. 8(22). pp.593-601.

Salim, W. and Negara, S.D., 2018. Infrastructure development under the Jokowi administration:

Progress, challenges and policies. Journal of Southeast Asian Economies. 35(3). pp.386-

401.

Scott, G. K. and Enu-Kwesi, F., 2018. Role of budgeting practices in service delivery in the

public sector: A study of district assemblies in Ghana. Hum Resour Manag Res. 8.

pp.23-33.

Wolak, F. A., 2021. Market design in an intermittent renewable future: cost recovery with zero-

marginal-cost resources. IEEE Power and Energy Magazine. 19(1). pp.29-40.

1

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.