Financial Calculations, Budgeting, and Investment Project Analysis

VerifiedAdded on 2022/12/28

|8

|2017

|96

Homework Assignment

AI Summary

This document presents a comprehensive solution to a finance assignment, addressing various aspects of financial management. The solution begins with the calculation of contribution margin, break-even point, and margin of safety for a given company, along with insightful comments on their relevance. It then delves into project evaluation using payback period and Net Present Value (NPV) methods, comparing two projects and concluding with a justification for the preferred project based on financial metrics. The assignment also explores working capital management, emphasizing its importance and offering strategies for efficient management. Finally, the solution critically analyzes incremental budgeting, discussing its advantages and limitations, and contrasting it with zero-based budgeting to provide a well-rounded understanding of budgeting techniques. The assignment incorporates relevant financial concepts and provides practical applications, making it a valuable resource for students studying finance.

FINANCIAL CALCULATIONS

Student ID:

[Pick the date]

Student ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

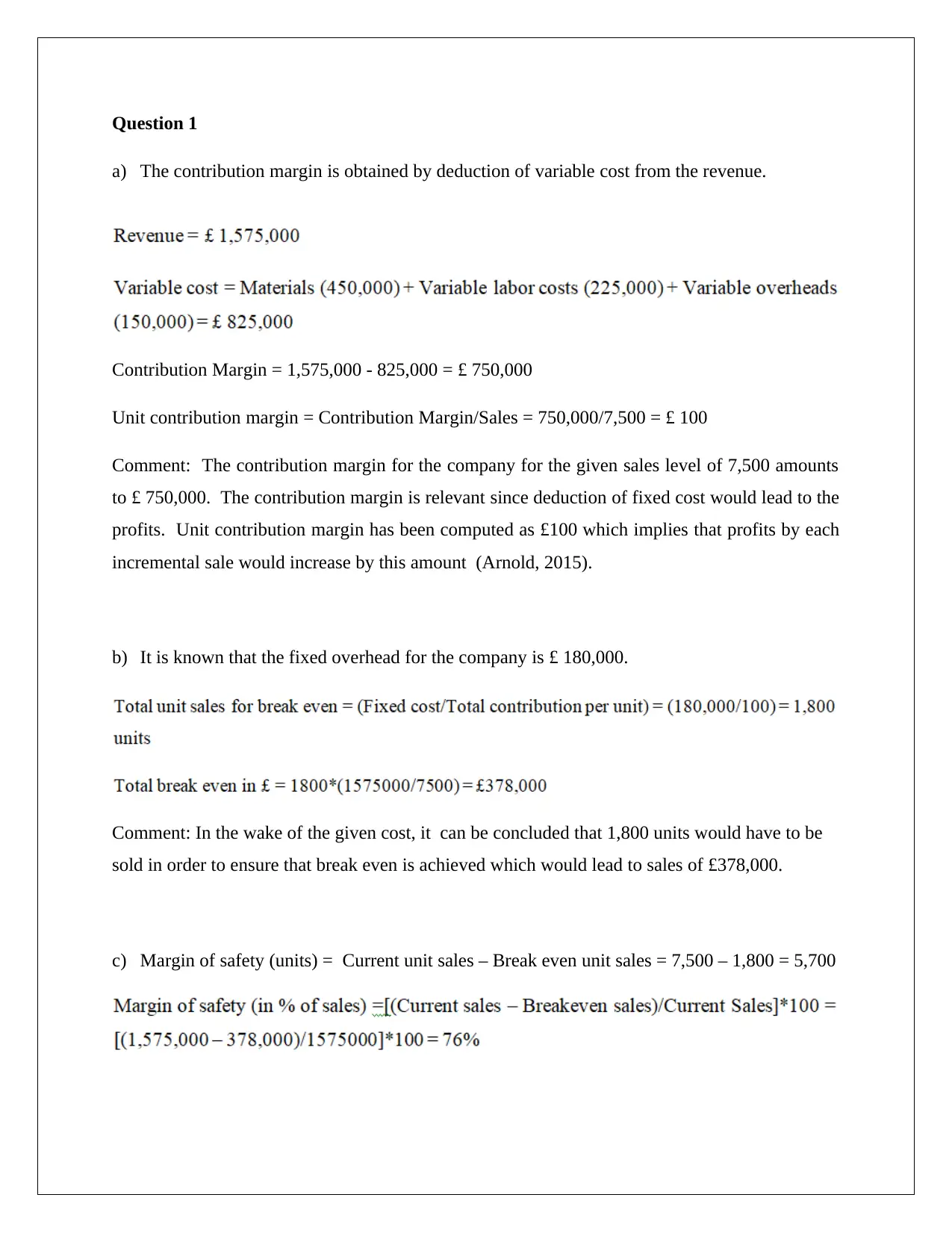

Question 1

a) The contribution margin is obtained by deduction of variable cost from the revenue.

Contribution Margin = 1,575,000 - 825,000 = £ 750,000

Unit contribution margin = Contribution Margin/Sales = 750,000/7,500 = £ 100

Comment: The contribution margin for the company for the given sales level of 7,500 amounts

to £ 750,000. The contribution margin is relevant since deduction of fixed cost would lead to the

profits. Unit contribution margin has been computed as £100 which implies that profits by each

incremental sale would increase by this amount (Arnold, 2015).

b) It is known that the fixed overhead for the company is £ 180,000.

Comment: In the wake of the given cost, it can be concluded that 1,800 units would have to be

sold in order to ensure that break even is achieved which would lead to sales of £378,000.

c) Margin of safety (units) = Current unit sales – Break even unit sales = 7,500 – 1,800 = 5,700

a) The contribution margin is obtained by deduction of variable cost from the revenue.

Contribution Margin = 1,575,000 - 825,000 = £ 750,000

Unit contribution margin = Contribution Margin/Sales = 750,000/7,500 = £ 100

Comment: The contribution margin for the company for the given sales level of 7,500 amounts

to £ 750,000. The contribution margin is relevant since deduction of fixed cost would lead to the

profits. Unit contribution margin has been computed as £100 which implies that profits by each

incremental sale would increase by this amount (Arnold, 2015).

b) It is known that the fixed overhead for the company is £ 180,000.

Comment: In the wake of the given cost, it can be concluded that 1,800 units would have to be

sold in order to ensure that break even is achieved which would lead to sales of £378,000.

c) Margin of safety (units) = Current unit sales – Break even unit sales = 7,500 – 1,800 = 5,700

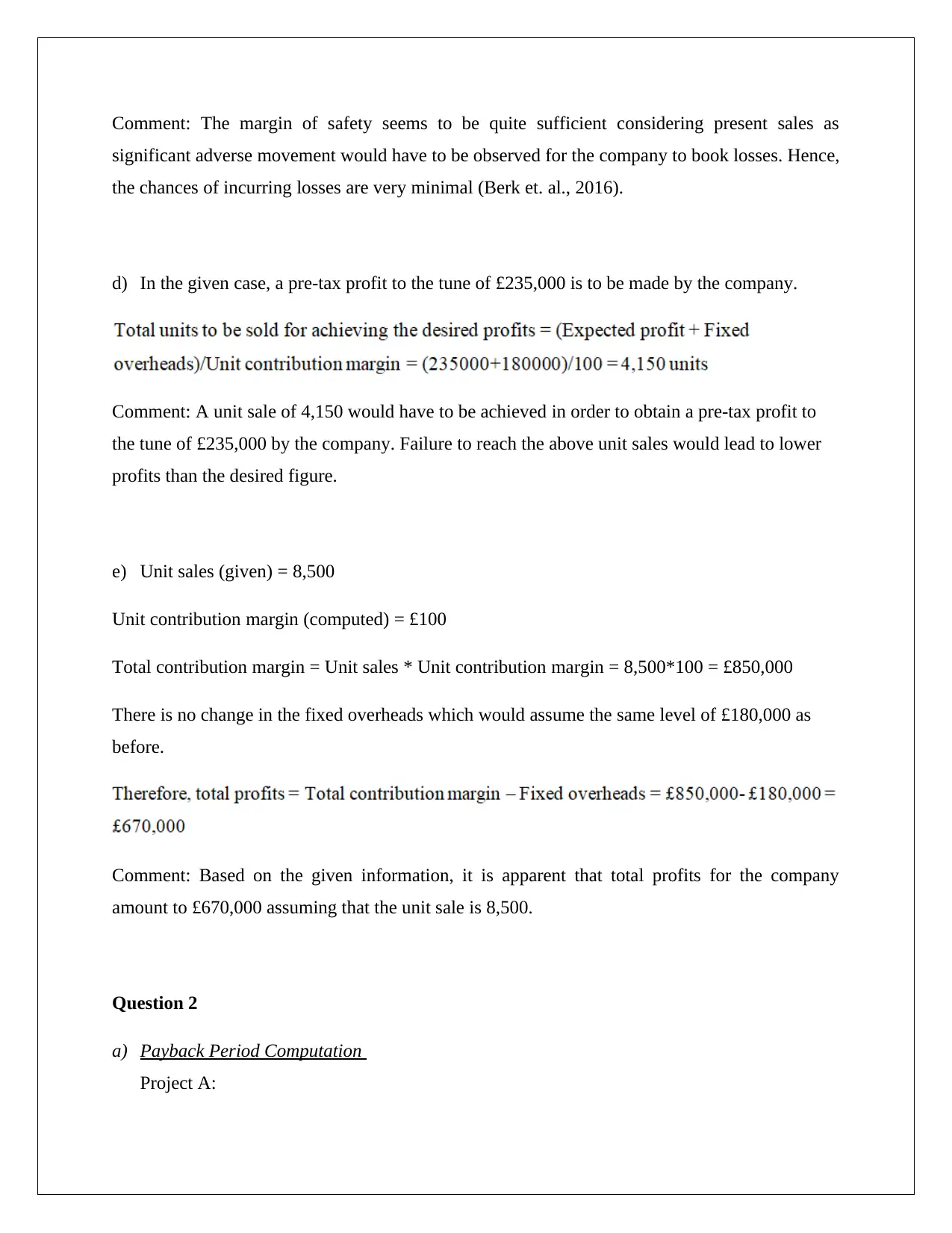

Comment: The margin of safety seems to be quite sufficient considering present sales as

significant adverse movement would have to be observed for the company to book losses. Hence,

the chances of incurring losses are very minimal (Berk et. al., 2016).

d) In the given case, a pre-tax profit to the tune of £235,000 is to be made by the company.

Comment: A unit sale of 4,150 would have to be achieved in order to obtain a pre-tax profit to

the tune of £235,000 by the company. Failure to reach the above unit sales would lead to lower

profits than the desired figure.

e) Unit sales (given) = 8,500

Unit contribution margin (computed) = £100

Total contribution margin = Unit sales * Unit contribution margin = 8,500*100 = £850,000

There is no change in the fixed overheads which would assume the same level of £180,000 as

before.

Comment: Based on the given information, it is apparent that total profits for the company

amount to £670,000 assuming that the unit sale is 8,500.

Question 2

a) Payback Period Computation

Project A:

significant adverse movement would have to be observed for the company to book losses. Hence,

the chances of incurring losses are very minimal (Berk et. al., 2016).

d) In the given case, a pre-tax profit to the tune of £235,000 is to be made by the company.

Comment: A unit sale of 4,150 would have to be achieved in order to obtain a pre-tax profit to

the tune of £235,000 by the company. Failure to reach the above unit sales would lead to lower

profits than the desired figure.

e) Unit sales (given) = 8,500

Unit contribution margin (computed) = £100

Total contribution margin = Unit sales * Unit contribution margin = 8,500*100 = £850,000

There is no change in the fixed overheads which would assume the same level of £180,000 as

before.

Comment: Based on the given information, it is apparent that total profits for the company

amount to £670,000 assuming that the unit sale is 8,500.

Question 2

a) Payback Period Computation

Project A:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

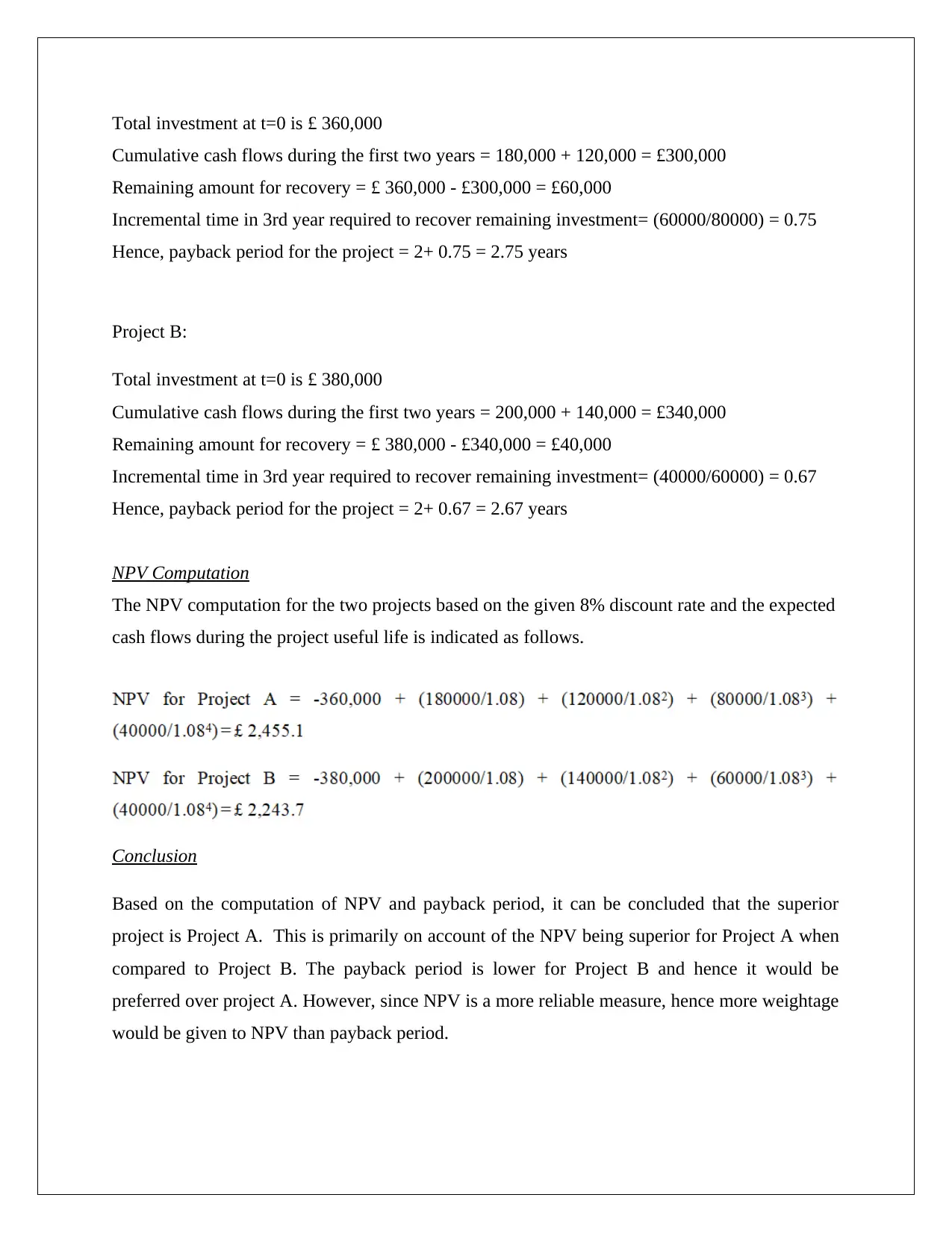

Total investment at t=0 is £ 360,000

Cumulative cash flows during the first two years = 180,000 + 120,000 = £300,000

Remaining amount for recovery = £ 360,000 - £300,000 = £60,000

Incremental time in 3rd year required to recover remaining investment= (60000/80000) = 0.75

Hence, payback period for the project = 2+ 0.75 = 2.75 years

Project B:

Total investment at t=0 is £ 380,000

Cumulative cash flows during the first two years = 200,000 + 140,000 = £340,000

Remaining amount for recovery = £ 380,000 - £340,000 = £40,000

Incremental time in 3rd year required to recover remaining investment= (40000/60000) = 0.67

Hence, payback period for the project = 2+ 0.67 = 2.67 years

NPV Computation

The NPV computation for the two projects based on the given 8% discount rate and the expected

cash flows during the project useful life is indicated as follows.

Conclusion

Based on the computation of NPV and payback period, it can be concluded that the superior

project is Project A. This is primarily on account of the NPV being superior for Project A when

compared to Project B. The payback period is lower for Project B and hence it would be

preferred over project A. However, since NPV is a more reliable measure, hence more weightage

would be given to NPV than payback period.

Cumulative cash flows during the first two years = 180,000 + 120,000 = £300,000

Remaining amount for recovery = £ 360,000 - £300,000 = £60,000

Incremental time in 3rd year required to recover remaining investment= (60000/80000) = 0.75

Hence, payback period for the project = 2+ 0.75 = 2.75 years

Project B:

Total investment at t=0 is £ 380,000

Cumulative cash flows during the first two years = 200,000 + 140,000 = £340,000

Remaining amount for recovery = £ 380,000 - £340,000 = £40,000

Incremental time in 3rd year required to recover remaining investment= (40000/60000) = 0.67

Hence, payback period for the project = 2+ 0.67 = 2.67 years

NPV Computation

The NPV computation for the two projects based on the given 8% discount rate and the expected

cash flows during the project useful life is indicated as follows.

Conclusion

Based on the computation of NPV and payback period, it can be concluded that the superior

project is Project A. This is primarily on account of the NPV being superior for Project A when

compared to Project B. The payback period is lower for Project B and hence it would be

preferred over project A. However, since NPV is a more reliable measure, hence more weightage

would be given to NPV than payback period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) In relation to payback period, a noteworthy benefit is the underlying simplicity which makes

it easy to compute and understand. Additionally, there is no involvement of any discount rate

for payback period computation which makes it reliable. But, a key limitation of payback

period as a measure of capital budgeting is the failure to take into account the time value of

money as this method used cash flows which have not been adjusted for time. Also, payback

period takes into consideration the cash flows that tend to occur till the payback period and

ignores those cashflows which may occur after this period. As a result, this method is not

reliable when mutually exclusive projects ought to be compared (Ross et. al., 2015).

In relation to NPV, one of the biggest advantages is the reliability owing to which it is often used

for determining the superior project when mutually exclusive projects ought to be compared.

Also, unlike payback period, this considers all the cashflows occurring over the useful project

life in entirety and thereby provides accurate assessment. However, a key limitation of this

method is that it is complex to understand and implement. Additionally, the NPV tends to be

highly dependent on discount rate and thereby vulnerable to the accuracy of this input

(Damodaran, 2015).

Question 3

The difference in current assets and current liabilities is referred to as working capital. Prudent

management of this is imperative so as to ensure that external financing requirement is

minimised. Considering that there may be mismatch in the cash payments and cash receipts,

hence external finance may be required for normal business operations. The company first

procures inventory from the supplier which then would be sold. In the meanwhile, cost is

incurred with regards to storage and selling of this inventory. Further, some sale would be credit

based where the cash realization would take some time. However, the company would need to

meet the various obligations in regards to payments related to supplier, staff and labour. For

meeting these obligations, working capital financing may be required (Berk et. al., 2016).

There is a need on company’s part to manage the working capital. This would require efforts to

reduce the period for inventory turnover which would lower the costs related to inventory.

Besides, the company needs to make effort to lower the cash collection period from credit sales

it easy to compute and understand. Additionally, there is no involvement of any discount rate

for payback period computation which makes it reliable. But, a key limitation of payback

period as a measure of capital budgeting is the failure to take into account the time value of

money as this method used cash flows which have not been adjusted for time. Also, payback

period takes into consideration the cash flows that tend to occur till the payback period and

ignores those cashflows which may occur after this period. As a result, this method is not

reliable when mutually exclusive projects ought to be compared (Ross et. al., 2015).

In relation to NPV, one of the biggest advantages is the reliability owing to which it is often used

for determining the superior project when mutually exclusive projects ought to be compared.

Also, unlike payback period, this considers all the cashflows occurring over the useful project

life in entirety and thereby provides accurate assessment. However, a key limitation of this

method is that it is complex to understand and implement. Additionally, the NPV tends to be

highly dependent on discount rate and thereby vulnerable to the accuracy of this input

(Damodaran, 2015).

Question 3

The difference in current assets and current liabilities is referred to as working capital. Prudent

management of this is imperative so as to ensure that external financing requirement is

minimised. Considering that there may be mismatch in the cash payments and cash receipts,

hence external finance may be required for normal business operations. The company first

procures inventory from the supplier which then would be sold. In the meanwhile, cost is

incurred with regards to storage and selling of this inventory. Further, some sale would be credit

based where the cash realization would take some time. However, the company would need to

meet the various obligations in regards to payments related to supplier, staff and labour. For

meeting these obligations, working capital financing may be required (Berk et. al., 2016).

There is a need on company’s part to manage the working capital. This would require efforts to

reduce the period for inventory turnover which would lower the costs related to inventory.

Besides, the company needs to make effort to lower the cash collection period from credit sales

without adversely impacting sales. Also, bad debts need to be prudently managed. Appropriate

incentives in the form of discounts may be offered to the debtors so as to make cash payment for

the sale at an early done. Besides, there is a need to secure bank funding based on the expected

shortfall in working capital requirements of the company. The importance of working capital

funding is comparatively higher in seasonal businesses where a significant amount of sales tend

to be concentrated in a limited time. In such a business, the profitability and revenue of the

business may be significantly impacted if working capital shortage is observed. As a result, it is

imperative that suitable arrangements ought to be made by the company so that enough cash is

available for servicing of current liabilities related to business (Arnold, 2015).

The discussion carried out above clearly highlights that there are two pivotal elements for

working capital management. The first element focuses on reducing the requirement of working

capital by ensuring better management of receivables, payable and inventory related days so that

cash conversion cycle is low. The second element relates to ensure that adequate funding is

available at the minimum cost so that there is no shortfall and business does not get adversely

impacted. Working capital management can potentially lead to higher profitability for the

business and also plays an enabling role in management of short term liquidity (Petty at. al.,

2016).

Question 4

There are a host of choices available to companies in relation to budgeting. One of the choices

available is incremental budgeting which tends to make incremental changes in the budget

allocation based on the previous year allocation. For ascertaining the validity of the statement

claiming that this technique is the best, it is essential to carry a critical analysis of this technique.

A big advantage associated with incremental budgeting is that there is stability as no radical

changes would be observed in budget since incremental changes are observed. This would result

in continuity as money allocation would continue with small differences for the projects that are

already under progress from previous year. This leads to lowering of risk related to major

changes in departmental allocation. The key assumption that drives the incremental budgeting is

that the allocations made in earlier year were accurate and hence tweaking the allocations would

incentives in the form of discounts may be offered to the debtors so as to make cash payment for

the sale at an early done. Besides, there is a need to secure bank funding based on the expected

shortfall in working capital requirements of the company. The importance of working capital

funding is comparatively higher in seasonal businesses where a significant amount of sales tend

to be concentrated in a limited time. In such a business, the profitability and revenue of the

business may be significantly impacted if working capital shortage is observed. As a result, it is

imperative that suitable arrangements ought to be made by the company so that enough cash is

available for servicing of current liabilities related to business (Arnold, 2015).

The discussion carried out above clearly highlights that there are two pivotal elements for

working capital management. The first element focuses on reducing the requirement of working

capital by ensuring better management of receivables, payable and inventory related days so that

cash conversion cycle is low. The second element relates to ensure that adequate funding is

available at the minimum cost so that there is no shortfall and business does not get adversely

impacted. Working capital management can potentially lead to higher profitability for the

business and also plays an enabling role in management of short term liquidity (Petty at. al.,

2016).

Question 4

There are a host of choices available to companies in relation to budgeting. One of the choices

available is incremental budgeting which tends to make incremental changes in the budget

allocation based on the previous year allocation. For ascertaining the validity of the statement

claiming that this technique is the best, it is essential to carry a critical analysis of this technique.

A big advantage associated with incremental budgeting is that there is stability as no radical

changes would be observed in budget since incremental changes are observed. This would result

in continuity as money allocation would continue with small differences for the projects that are

already under progress from previous year. This leads to lowering of risk related to major

changes in departmental allocation. The key assumption that drives the incremental budgeting is

that the allocations made in earlier year were accurate and hence tweaking the allocations would

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

be fine. Since, there is an existing base where changes ought to be made, hence this budgeting

system is quite simple to implement and understand. Additionally, the changes made in

budgetary allocation can be obtained by comparison with the previous year allocation

(Damodaran, 2015).

It is noteworthy that there are key limitations witnessed in the incremental budgeting

methodology. There is implicit incentive present for the departments to incur higher expenditure

than required so that the funding for the next year remains at same level or is improved. Failure

to incur the allocated resource spending would potentially lead to lower allocation in the next

year budget. As a result, there is no incentive for the rationalization of spending by the various

departments. However, arguably the most pivotal issue with this budgetary technique is that it

does not encourage change as the previous methodology and activity prioritization is maintained.

This makes this technique unsuitable for a company or industry which is in the midst of

sweeping changes or is at the cusp of same. In such a scenario, zero budgeting is recommended

as it does not make any assumption about the previous allocation and starts the budgetary

allocation from scratch considering the given business priorities and climate (Lasher, 2017).

The above discussion clearly highlights that incremental budgeting as a appropriate technique for

firms which have a stable internal and external environment and stability is desirable in budget.

But for businesses where may be witnessing significant change either internally or externally

would require to view budgeting from a fresh perspective and hence zero budgeting would be

found more useful as it can potentially be disruptive which is not possible with incremental

budgeting. Thus, the critical analysis of incremental budgeting clearly reflects that it is not the

most apt budgetary technique for firms which are witnessing change (Ross et. al., 2015).

system is quite simple to implement and understand. Additionally, the changes made in

budgetary allocation can be obtained by comparison with the previous year allocation

(Damodaran, 2015).

It is noteworthy that there are key limitations witnessed in the incremental budgeting

methodology. There is implicit incentive present for the departments to incur higher expenditure

than required so that the funding for the next year remains at same level or is improved. Failure

to incur the allocated resource spending would potentially lead to lower allocation in the next

year budget. As a result, there is no incentive for the rationalization of spending by the various

departments. However, arguably the most pivotal issue with this budgetary technique is that it

does not encourage change as the previous methodology and activity prioritization is maintained.

This makes this technique unsuitable for a company or industry which is in the midst of

sweeping changes or is at the cusp of same. In such a scenario, zero budgeting is recommended

as it does not make any assumption about the previous allocation and starts the budgetary

allocation from scratch considering the given business priorities and climate (Lasher, 2017).

The above discussion clearly highlights that incremental budgeting as a appropriate technique for

firms which have a stable internal and external environment and stability is desirable in budget.

But for businesses where may be witnessing significant change either internally or externally

would require to view budgeting from a fresh perspective and hence zero budgeting would be

found more useful as it can potentially be disruptive which is not possible with incremental

budgeting. Thus, the critical analysis of incremental budgeting clearly reflects that it is not the

most apt budgetary technique for firms which are witnessing change (Ross et. al., 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2016) Fundamentals of

corporate finance. London: Pearson Higher Education AU.

Damodaran, A. (2015) Applied corporate finance: A user’s manual. 3rd ed. New York: Wiley,

John & Sons.

Lasher, W. R., (2017) Practical Financial Management. 5th ed. London: South- Western

College Publisher

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2016)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

Ross,S.A., Tryaler,R., Bird, R.,Westerfield, R.W. and Jorden,B.D. (2015) Essentials of Corporate

Finance. 2nd ed. New York City: McGraw-Hill.

Arnold, G. (2015) Corporate Financial Management. 3rd ed. Sydney: Financial Times

Management.

Berk, J., DeMarzo, P., Harford, J., Ford, G., Mollica, V. and Finch, N. (2016) Fundamentals of

corporate finance. London: Pearson Higher Education AU.

Damodaran, A. (2015) Applied corporate finance: A user’s manual. 3rd ed. New York: Wiley,

John & Sons.

Lasher, W. R., (2017) Practical Financial Management. 5th ed. London: South- Western

College Publisher

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2016)

Financial Management, Principles and Applications. 6th ed. NSW: Pearson Education, French

Forest Australia.

Ross,S.A., Tryaler,R., Bird, R.,Westerfield, R.W. and Jorden,B.D. (2015) Essentials of Corporate

Finance. 2nd ed. New York City: McGraw-Hill.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.