Financial Control and Budgeting: A Healthcare Analysis Report

VerifiedAdded on 2023/01/12

|18

|4904

|95

Report

AI Summary

This report delves into the critical aspects of financial control and budgeting within the National Health Service (NHS) in the UK, examining the challenges faced, particularly in light of recent financial developments. It explores alternative funding options like Private Finance Initiatives and agency partnerships, evaluating their usefulness and benefits. The report identifies key stakeholders in the social care sector and discusses effective communication strategies. Furthermore, it presents a break-even analysis for a care home, calculating break-even capacity and targeted profit levels. The uses of break-even analysis in short-term and long-term decision-making are also discussed. The report then analyzes various budgeting approaches, highlighting their benefits and drawbacks, and addresses specific difficulties encountered when budgeting in public sector organizations. A cash budget formulation for a health and social care firm is provided, and the impact of financial constraints, costs, and budgets on health and social care service managers, clients, and stakeholders is assessed. The report concludes with a comprehensive overview of financial planning and control within the healthcare sector.

Financial Control and

Budgeting

Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

a) Challenges faced by NHS and the recent developments....................................................3

b) The Usefulness of alternative funding options...................................................................4

c) Identification of the key stakeholders within the social care sector and ways of

communication.......................................................................................................................6

TASK 2............................................................................................................................................7

a) Break Even capacity usage rate of ABC care home ltd.....................................................7

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity................7

c) Uses of Break Even analysis in short term and long term decision making......................8

TASK 3............................................................................................................................................9

A. Benefits and drawbacks of various budgeting approaches................................................9

B. Discourse of specific difficulties faced when budgeting in public sector organisation...11

C. Formulation of cash budget within a health and social care firm....................................12

D. Awareness on the impact of financial constraints, costs and budget on health and social

care service managers, their clients and stakeholders..........................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

a) Challenges faced by NHS and the recent developments....................................................3

b) The Usefulness of alternative funding options...................................................................4

c) Identification of the key stakeholders within the social care sector and ways of

communication.......................................................................................................................6

TASK 2............................................................................................................................................7

a) Break Even capacity usage rate of ABC care home ltd.....................................................7

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity................7

c) Uses of Break Even analysis in short term and long term decision making......................8

TASK 3............................................................................................................................................9

A. Benefits and drawbacks of various budgeting approaches................................................9

B. Discourse of specific difficulties faced when budgeting in public sector organisation...11

C. Formulation of cash budget within a health and social care firm....................................12

D. Awareness on the impact of financial constraints, costs and budget on health and social

care service managers, their clients and stakeholders..........................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

In the planning of the financial reports, financial management and budget play a significant role.

It allows the firm to assess its performance and capabilities and to see the firm's inflows and

outflows. Budgeting provides the previous years’ report which allows administrators to decide to

solve the issues they have failed to meet their objective (Huikku, Karjalainen and Seppälä,

2018). Financial monitoring allows managers to handle costs in order to optimize income. Such

reports help to executives to assess about the organization in its entirety. Financial management

provides direct power over the company's earnings and expenditures. Budget reports enables

managers to see the progress and take the decisions required to keep the business growing.

The report is based on a case study of the UK National Health Service on the role of legal control

and budgeting in policy making. As well as to consider the significance of control and financial

planning. This case study outlines certain issues which enable managers to recognize how the

challenges facing the National Health Service on their 70th anniversary have been addressed by

help of monetary and budgetary control.

MAIN BODY

TASK 1

a) Challenges faced by NHS and the recent developments.

NHS is an emergency care service located in Great Britain that helps patients across the

world and receive relatively affordable costs for medical treatment. The national health

services are having a problem in handling adequately the money collected by their leaders

for the improvement of the national health service by 2023 to pay an additional 20 billion

per annum. The real concern is that this vast sum of money is spent adequately in the

provision of health services for the citizens who use the UK National Health Service.

Financial management allows National Health Service administrators to find the best way

to use the assets. In the last 20 years the number of people who die from the attacks has

dropped by 8,390 each year and citizens dying from cancer by 634, as per the case study

10,385 fewer people died from heart attacks. The overall productivity growth reported

throughout the last 5 years was 1.4 percent annually who die of some illnesses.

In the planning of the financial reports, financial management and budget play a significant role.

It allows the firm to assess its performance and capabilities and to see the firm's inflows and

outflows. Budgeting provides the previous years’ report which allows administrators to decide to

solve the issues they have failed to meet their objective (Huikku, Karjalainen and Seppälä,

2018). Financial monitoring allows managers to handle costs in order to optimize income. Such

reports help to executives to assess about the organization in its entirety. Financial management

provides direct power over the company's earnings and expenditures. Budget reports enables

managers to see the progress and take the decisions required to keep the business growing.

The report is based on a case study of the UK National Health Service on the role of legal control

and budgeting in policy making. As well as to consider the significance of control and financial

planning. This case study outlines certain issues which enable managers to recognize how the

challenges facing the National Health Service on their 70th anniversary have been addressed by

help of monetary and budgetary control.

MAIN BODY

TASK 1

a) Challenges faced by NHS and the recent developments.

NHS is an emergency care service located in Great Britain that helps patients across the

world and receive relatively affordable costs for medical treatment. The national health

services are having a problem in handling adequately the money collected by their leaders

for the improvement of the national health service by 2023 to pay an additional 20 billion

per annum. The real concern is that this vast sum of money is spent adequately in the

provision of health services for the citizens who use the UK National Health Service.

Financial management allows National Health Service administrators to find the best way

to use the assets. In the last 20 years the number of people who die from the attacks has

dropped by 8,390 each year and citizens dying from cancer by 634, as per the case study

10,385 fewer people died from heart attacks. The overall productivity growth reported

throughout the last 5 years was 1.4 percent annually who die of some illnesses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The health problems of people are growing, the elderly disabled people often rise, and

need for the NHS is rising rapidly. The National Health Service must manage its financial

resources adequately in order to fulfil demand. The financial management provides the NHS

with a mechanism to track their spending to support these people with their various chronic

conditions (Nombo, 2016). The latest pattern shifts and the advancement of treatment modalities.

To order to support patients with these chronic conditions, the National Health Services is trying

to incorporate the new innovations. The technology, genomics and drug development is some of

the new innovations to replace old methods and to start revolutionizing care in the medical field.

Financial planning allows administrators to recognize the obstacles the NHS needs to face in

improving service quality, productivity and costs. The statistics from the past budgets enable the

NHS recognize the issues and conduct the test to fix them. The budget increases efficiency and

security, both of the workforce and of people who seek their care, by helping the National Health

Service plan the new procedure.

b) The Usefulness of alternative funding options.

Private Financing Initiates, Money, Financial Dimensions of Agency Collaboration are the

alternate funding mechanisms for NHS. Herein, underneath description of these

alternatives is mentioned in such manner that is as follows:

Private Finance Initiatives (PFI): The Labour government first introduced PFI in 1992

and was strengthened extensively in the 1997-2010. More than 700 clinics, colleges, jails,

etc. were constructed under the PFI system at the end of 2011. This facilitates the

maintenance of public systems such as new schools, hospitals, council housing, security

contracts, prisoners and road upgrades, through private investors (Guo and Yang, 2018).

The private sector supports public sector initiatives in the private finance program by

offering financial resources and enabling them manage production costs. This assists the

government in raising the burden on donors of the money which they earn immediately.

In nations such as the United Kingdom and Australia these kinds of private financing are

used. Under such schemes, investors, who put their money in public projects, take care of

the capital costs for these initiatives. This began in 1992 when the UK first started

collecting public capital from private banking firms for government projects. It was

need for the NHS is rising rapidly. The National Health Service must manage its financial

resources adequately in order to fulfil demand. The financial management provides the NHS

with a mechanism to track their spending to support these people with their various chronic

conditions (Nombo, 2016). The latest pattern shifts and the advancement of treatment modalities.

To order to support patients with these chronic conditions, the National Health Services is trying

to incorporate the new innovations. The technology, genomics and drug development is some of

the new innovations to replace old methods and to start revolutionizing care in the medical field.

Financial planning allows administrators to recognize the obstacles the NHS needs to face in

improving service quality, productivity and costs. The statistics from the past budgets enable the

NHS recognize the issues and conduct the test to fix them. The budget increases efficiency and

security, both of the workforce and of people who seek their care, by helping the National Health

Service plan the new procedure.

b) The Usefulness of alternative funding options.

Private Financing Initiates, Money, Financial Dimensions of Agency Collaboration are the

alternate funding mechanisms for NHS. Herein, underneath description of these

alternatives is mentioned in such manner that is as follows:

Private Finance Initiatives (PFI): The Labour government first introduced PFI in 1992

and was strengthened extensively in the 1997-2010. More than 700 clinics, colleges, jails,

etc. were constructed under the PFI system at the end of 2011. This facilitates the

maintenance of public systems such as new schools, hospitals, council housing, security

contracts, prisoners and road upgrades, through private investors (Guo and Yang, 2018).

The private sector supports public sector initiatives in the private finance program by

offering financial resources and enabling them manage production costs. This assists the

government in raising the burden on donors of the money which they earn immediately.

In nations such as the United Kingdom and Australia these kinds of private financing are

used. Under such schemes, investors, who put their money in public projects, take care of

the capital costs for these initiatives. This began in 1992 when the UK first started

collecting public capital from private banking firms for government projects. It was

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

becoming more common to collect private investors ' capital for public health projects of

this kind until 1997. It has some benefits such as:

1. Extra investment- Additional funding will launch further initiatives–adding social and

economic gains. The PFI offers private sector funding for initiatives that may prove

problematic to fund by rising lending and taxes.

2. Dynamic efficiency- Development and a great design for programs, better standard of

production and reduced maintenance costs are best paid for by the private industry.

The PFI bid process induces rivalry at the bidding stage.

Agency Partnership- Agency Partnership is the relationship where one party normally

has the judgment-making power, while the other side can only assist with fund-raising in

order to make the other side more efficient and more successful. The government also

makes the financial support, choice available to develop the agency in partnership with

the private sector in order to look after the resources. As well as manage the money and

help government projects to accomplish their primary objective of providing medical care

for the individuals. In the above case study, the National Health Service of Great Britain

was listed as having the choice to collect funds from the private industry input into the

department. It has some benefits such as:

1. Effective- This funding option is more effective and can be used at lower cost. In the

aspect of above organisation, this can be used.

2. Cost effective- In addition, this source of finance takes lower cost and time in process

of acquiring funds.

Resources: It is a method of raising the fund directly for government programs from the

various resources accessible to the private sectors as well as the federal funds and

surpluses. In order to fulfil their needs to treat full patients, the National Health Service

requires the form of private funds to help them stabilize from the multiple chronic

illnesses. Such kinds of private funds give the government the benefit of focusing solely

on the welfare of those needing medical facilities (Ouassini, 2018).

There are some private finance strategies which are adopted by the national health

services ' for raising capital to minimize the number of people who die from medical

problems like the assault on Hearth, heart attack and much more. The case study above

this kind until 1997. It has some benefits such as:

1. Extra investment- Additional funding will launch further initiatives–adding social and

economic gains. The PFI offers private sector funding for initiatives that may prove

problematic to fund by rising lending and taxes.

2. Dynamic efficiency- Development and a great design for programs, better standard of

production and reduced maintenance costs are best paid for by the private industry.

The PFI bid process induces rivalry at the bidding stage.

Agency Partnership- Agency Partnership is the relationship where one party normally

has the judgment-making power, while the other side can only assist with fund-raising in

order to make the other side more efficient and more successful. The government also

makes the financial support, choice available to develop the agency in partnership with

the private sector in order to look after the resources. As well as manage the money and

help government projects to accomplish their primary objective of providing medical care

for the individuals. In the above case study, the National Health Service of Great Britain

was listed as having the choice to collect funds from the private industry input into the

department. It has some benefits such as:

1. Effective- This funding option is more effective and can be used at lower cost. In the

aspect of above organisation, this can be used.

2. Cost effective- In addition, this source of finance takes lower cost and time in process

of acquiring funds.

Resources: It is a method of raising the fund directly for government programs from the

various resources accessible to the private sectors as well as the federal funds and

surpluses. In order to fulfil their needs to treat full patients, the National Health Service

requires the form of private funds to help them stabilize from the multiple chronic

illnesses. Such kinds of private funds give the government the benefit of focusing solely

on the welfare of those needing medical facilities (Ouassini, 2018).

There are some private finance strategies which are adopted by the national health

services ' for raising capital to minimize the number of people who die from medical

problems like the assault on Hearth, heart attack and much more. The case study above

indicates that the National Health Services are funded over the last 30 years through

central tax, but the NHS needs to take steps in widening their initiatives and seeking to

implement emerging technology in the field of medical research.

c) Identification of the key stakeholders within the social care sector and ways of

communication.

Stakeholders: Stakeholders are persons or groups of people directly involved in the

success and benefit of the company and often decide the appropriate steps. In certain

cases, the government may be shareholders, the creditors who made their investments in

the companies and the interested parties in the business who take advantage of the

company's revenue.

The social care stakeholders may be private industry donors, donors, workers, personnel

and the National Health Services personnel, and people who are in the public's programs for

therapy. It can be conveyed and even reported in the office articles to the main shareholders in

their financial statements and general sessions. The data which main shareholders need is the

quarterly report that shows the progress of the business, in whose creation the national health

services have spent a considerable amount of money. The budget reports provide shareholders

with a map for expenditures, whether the money they spend is used correctly or not (Henttu-Aho,

2016). These data are often needed in the sense of the previous year for workers to assess their

performance. Such budgets assist the managers in giving the organization the appropriate role.

The theory of the agency says that the government collects its fund by establishing an agency

with private industries, whereby power over the entity is not given by the private firm to collect

funds. In decision making, corporate management plays a significant role. It helps managers to

coordinate their workers better for the firm's development. This also allows companies to decide

fully how to help the business to expand. Corporate governance allows the corporation to better

control its resources and use its resources wisely and consistently.

TASK 2

a) Break Even capacity usage rate of ABC care home ltd.

Break Even Capacity: It can be defined as capacity of an organization's willingness to operate

at the point that makes little benefit from the profits obtained from its services to both clients and

central tax, but the NHS needs to take steps in widening their initiatives and seeking to

implement emerging technology in the field of medical research.

c) Identification of the key stakeholders within the social care sector and ways of

communication.

Stakeholders: Stakeholders are persons or groups of people directly involved in the

success and benefit of the company and often decide the appropriate steps. In certain

cases, the government may be shareholders, the creditors who made their investments in

the companies and the interested parties in the business who take advantage of the

company's revenue.

The social care stakeholders may be private industry donors, donors, workers, personnel

and the National Health Services personnel, and people who are in the public's programs for

therapy. It can be conveyed and even reported in the office articles to the main shareholders in

their financial statements and general sessions. The data which main shareholders need is the

quarterly report that shows the progress of the business, in whose creation the national health

services have spent a considerable amount of money. The budget reports provide shareholders

with a map for expenditures, whether the money they spend is used correctly or not (Henttu-Aho,

2016). These data are often needed in the sense of the previous year for workers to assess their

performance. Such budgets assist the managers in giving the organization the appropriate role.

The theory of the agency says that the government collects its fund by establishing an agency

with private industries, whereby power over the entity is not given by the private firm to collect

funds. In decision making, corporate management plays a significant role. It helps managers to

coordinate their workers better for the firm's development. This also allows companies to decide

fully how to help the business to expand. Corporate governance allows the corporation to better

control its resources and use its resources wisely and consistently.

TASK 2

a) Break Even capacity usage rate of ABC care home ltd.

Break Even Capacity: It can be defined as capacity of an organization's willingness to operate

at the point that makes little benefit from the profits obtained from its services to both clients and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

patients. Also break points illustrate the ability of the companies to cover their costs. Breakeven

is reached when only fixed expense and income can be retained by the company. On the basis of

given data set, this can be find out that the ABC caring homes Ltd.’s brake even capacity is 50.6

percent. This indicates that caring houses work to the fullest advantage.

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

61560x 90% 11400

Break Even Point 540000/11400 47.36

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity.

Targeted profit: Targeted income is the amount that the company wants to gain with forecasts

of costs associated with the manufacture of the commodity in a financial year. It allows

executives to budget as per the business's specifications (Zielniewicz, 2016).

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

615600x 95%/90%

Profit 109800

c) Uses of Break Even analysis in short term and long term decision making.

Breakeven point is a business method used by executives in order to determine whether to begin

manufacturing and sell goods by a corporation or not. It allows to assess the sales level with

balanced costs and revenues. The point of equilibrium is also known as the point of breach. This

is useful for developing flexible budgets that display costs and benefits of different activity rates.

This analysis also helps to establish pricing policies by explaining the effects on costs and

income of various market systems. The principle of benefit planning is helped to carry out. The

is reached when only fixed expense and income can be retained by the company. On the basis of

given data set, this can be find out that the ABC caring homes Ltd.’s brake even capacity is 50.6

percent. This indicates that caring houses work to the fullest advantage.

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

61560x 90% 11400

Break Even Point 540000/11400 47.36

b) Calculation of the Targeted profit at 90% and 95% of the total usage capacity.

Targeted profit: Targeted income is the amount that the company wants to gain with forecasts

of costs associated with the manufacture of the commodity in a financial year. It allows

executives to budget as per the business's specifications (Zielniewicz, 2016).

Total Fixed Cost 45000x12 540000

Contribution

Revenue

Total Cost

[(150+180+120)x12x60x90%]

372000

356400

615600x 95%/90%

Profit 109800

c) Uses of Break Even analysis in short term and long term decision making.

Breakeven point is a business method used by executives in order to determine whether to begin

manufacturing and sell goods by a corporation or not. It allows to assess the sales level with

balanced costs and revenues. The point of equilibrium is also known as the point of breach. This

is useful for developing flexible budgets that display costs and benefits of different activity rates.

This analysis also helps to establish pricing policies by explaining the effects on costs and

income of various market systems. The principle of benefit planning is helped to carry out. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understanding of the connection between cost volume and profit contributes to the desired

benefit. Evaluation of a correlation between cost and amount of income often allows

management to determine whether to shutting down or lose the business (Htun, 2019).

TASK 3

A. Benefits and drawbacks of various budgeting approaches.

The effective process related with planning about future expenses and making an

assumption that specific amount can be earned by making these expenditure is known as

budgeting. The concept of making budgets can be beneficial for companies in order to identify

the most productive activities and also eliminating the ones which can reduce the overall

profitability (Heydari, 2018). In general term, this can be described as an accounting device used

to manage organisation's profits and expenses. Drawing out strategies using various methods and

creating possible predictions dependent on historical evidence is important for corporate

organisations. There are several forms of financial planning strategies that businesses use to

devise an expenditure plan in an acceptable way. In large and small company’s effective budgets

have a greater role as it supports to manage and engage the available monetary as well as other

resources to give higher productivity. Thus manager is needed to implement the most suitable

strategies while designing budget for the year that are most suitable to the company’s operation.

Some of these techniques are elaborated underneath:

Incremental budgeting: It is mechanism used to build incremental expenditure plans.

This sort of budget is designed by using the details from the previous cycle or by using the

existing situation and results as a basis for making current budget numbers. This is considering to

be main component of financial accounting and is often used to allow minor adjustments in the

organizations budgets. The addition of any substance in previous year budget does not requires

to follow any sort of mathematical equation because changes are made as per convenient to reach

a specific target. The main benefits and drawbacks are listed below:

Advantages:

This is really a convenient and efficient method for companies to use, either small or big.

Method of calculation throughout this financial planning is very easy and will enable

administrators report correct amount in the accounting reports.

benefit. Evaluation of a correlation between cost and amount of income often allows

management to determine whether to shutting down or lose the business (Htun, 2019).

TASK 3

A. Benefits and drawbacks of various budgeting approaches.

The effective process related with planning about future expenses and making an

assumption that specific amount can be earned by making these expenditure is known as

budgeting. The concept of making budgets can be beneficial for companies in order to identify

the most productive activities and also eliminating the ones which can reduce the overall

profitability (Heydari, 2018). In general term, this can be described as an accounting device used

to manage organisation's profits and expenses. Drawing out strategies using various methods and

creating possible predictions dependent on historical evidence is important for corporate

organisations. There are several forms of financial planning strategies that businesses use to

devise an expenditure plan in an acceptable way. In large and small company’s effective budgets

have a greater role as it supports to manage and engage the available monetary as well as other

resources to give higher productivity. Thus manager is needed to implement the most suitable

strategies while designing budget for the year that are most suitable to the company’s operation.

Some of these techniques are elaborated underneath:

Incremental budgeting: It is mechanism used to build incremental expenditure plans.

This sort of budget is designed by using the details from the previous cycle or by using the

existing situation and results as a basis for making current budget numbers. This is considering to

be main component of financial accounting and is often used to allow minor adjustments in the

organizations budgets. The addition of any substance in previous year budget does not requires

to follow any sort of mathematical equation because changes are made as per convenient to reach

a specific target. The main benefits and drawbacks are listed below:

Advantages:

This is really a convenient and efficient method for companies to use, either small or big.

Method of calculation throughout this financial planning is very easy and will enable

administrators report correct amount in the accounting reports.

It's used in most organizations for growing rivalry and creating the importance of equity

amongst operational divisions

Disadvantages:

In this approach the top-level managers ignore creativity and little cost savings.

This promotes massive investment to obtain favourable or beneficial variances.

Zero based budgeting: It is primarily used as a forecasting method in financial

accounting, in which expenditure with a zero value is constructed from start. In this system

managers insure that costs for the relevant duration are justified (Scott, 2017). The requirement

for this kind of budgeting strategy is the foundation for the future and proper classification about

each operation support to reduce the chances contingency. Some of its major advantages and

disadvantages are discussed underneath:

Advantages:

Zero-based budgeting allows administrators to assign expenses according to specific

needs to the company's divisions.

As growing cost in this strategy is explained because it can enable management to resolve

the limitations of incremental expenditure plan.

Disadvantages:

In this process, vast quantities of workers are needed to devise budgets which is not easy

for every organisation to engage more and more worker in budgeting process.

This required some time to shape the budgets because it would be a time-consuming

operation.

Activity based budgeting: According to this budgeting strategy, activity based cost is

being used to shape financial plan for every specific activity. Under the framework of this

technique expenditure or money were assigned as per their criteria of growing operation

undertaken by the organization. It main merits and demerits are listed underneath:

Advantages:

It approaches measures each and every expense driver because it takes into account all

the measures involved in the respective activity of company.

In this financial planning strategy all unwanted tasks are removed.

Disadvantages:

amongst operational divisions

Disadvantages:

In this approach the top-level managers ignore creativity and little cost savings.

This promotes massive investment to obtain favourable or beneficial variances.

Zero based budgeting: It is primarily used as a forecasting method in financial

accounting, in which expenditure with a zero value is constructed from start. In this system

managers insure that costs for the relevant duration are justified (Scott, 2017). The requirement

for this kind of budgeting strategy is the foundation for the future and proper classification about

each operation support to reduce the chances contingency. Some of its major advantages and

disadvantages are discussed underneath:

Advantages:

Zero-based budgeting allows administrators to assign expenses according to specific

needs to the company's divisions.

As growing cost in this strategy is explained because it can enable management to resolve

the limitations of incremental expenditure plan.

Disadvantages:

In this process, vast quantities of workers are needed to devise budgets which is not easy

for every organisation to engage more and more worker in budgeting process.

This required some time to shape the budgets because it would be a time-consuming

operation.

Activity based budgeting: According to this budgeting strategy, activity based cost is

being used to shape financial plan for every specific activity. Under the framework of this

technique expenditure or money were assigned as per their criteria of growing operation

undertaken by the organization. It main merits and demerits are listed underneath:

Advantages:

It approaches measures each and every expense driver because it takes into account all

the measures involved in the respective activity of company.

In this financial planning strategy all unwanted tasks are removed.

Disadvantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Within this method the process of evaluating budget is quite complicated and not easily

understandable.

To carry out this method of budgeting, effective and sufficient expertise is necessary and

businesses are expected to employ trained staff representatives for this reason.

Rolling budgets: This kind of budget usually include certain addition on previous budget

as per the requirement of company (Downes, Moretti and Nicol, 2017). This mainly include

making suitable changes within the activities which can give higher results for company and

additional alteration into these activities does not make any burden. Some of its advantages and

disadvantages are discussed underneath:

Advantages:

This is a balanced schedule, where adjustments are made due to results from the

preceding year.

With the aid of this financial planning strategy, evidence of each and every cost may be

calculated.

Disadvantages:

The method of implementing rolling budget is indeed a time intensive procedure that

takes a significant period of time to effectively execute all of the operations.

The main disadvantages of this techniques are that many time companies make

assumption over negative activities and implement changes by thinking that it will

provide good result in future.

B. Discourse of specific difficulties faced when budgeting in public sector organisation.

As public service executives carry out budgeting exercises they need to address

increasing forms of problems and challenges (Naseri and Hosseini, 2017). This is really

necessary for all forms of companies to prioritize accordingly so that fiscal capital can be utilized

wisely and consistently. The major difficulties faced by the management of public company at

the time of preparing budgets are:

1. Public sector organisations have as their primary aim the protection of community. They

should not rely on making income, but administrators are expected to ensure sure they

allow good use of the overall public monetary capital.

2. Expenditures plan of public sector firms are presented to the general population because

they want so, so that the administrators face a problem that is linked to the quality of the

understandable.

To carry out this method of budgeting, effective and sufficient expertise is necessary and

businesses are expected to employ trained staff representatives for this reason.

Rolling budgets: This kind of budget usually include certain addition on previous budget

as per the requirement of company (Downes, Moretti and Nicol, 2017). This mainly include

making suitable changes within the activities which can give higher results for company and

additional alteration into these activities does not make any burden. Some of its advantages and

disadvantages are discussed underneath:

Advantages:

This is a balanced schedule, where adjustments are made due to results from the

preceding year.

With the aid of this financial planning strategy, evidence of each and every cost may be

calculated.

Disadvantages:

The method of implementing rolling budget is indeed a time intensive procedure that

takes a significant period of time to effectively execute all of the operations.

The main disadvantages of this techniques are that many time companies make

assumption over negative activities and implement changes by thinking that it will

provide good result in future.

B. Discourse of specific difficulties faced when budgeting in public sector organisation.

As public service executives carry out budgeting exercises they need to address

increasing forms of problems and challenges (Naseri and Hosseini, 2017). This is really

necessary for all forms of companies to prioritize accordingly so that fiscal capital can be utilized

wisely and consistently. The major difficulties faced by the management of public company at

the time of preparing budgets are:

1. Public sector organisations have as their primary aim the protection of community. They

should not rely on making income, but administrators are expected to ensure sure they

allow good use of the overall public monetary capital.

2. Expenditures plan of public sector firms are presented to the general population because

they want so, so that the administrators face a problem that is linked to the quality of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sum reported in the report. When it's not correct then that will cause challenges with the

managers and the whole organization.

3. Public sector administrators tend to consider whether the expenditures plan have a greater

level of flexibility in order to make any adjustment as per the government opinions.

However, in the private industry budgets are not needed to be flexible because once one

budget is created then no modifications can be produced.

Thus, it has been determined that manager dealing in public industry are intend to meet

with large number of regulation and laws imposed by governance of a country. Whereas, the

manager in private company are not liable to make each and every standard of governance at the

time of preparing budget for specific period related to specific activity (Derfuss, 2016).

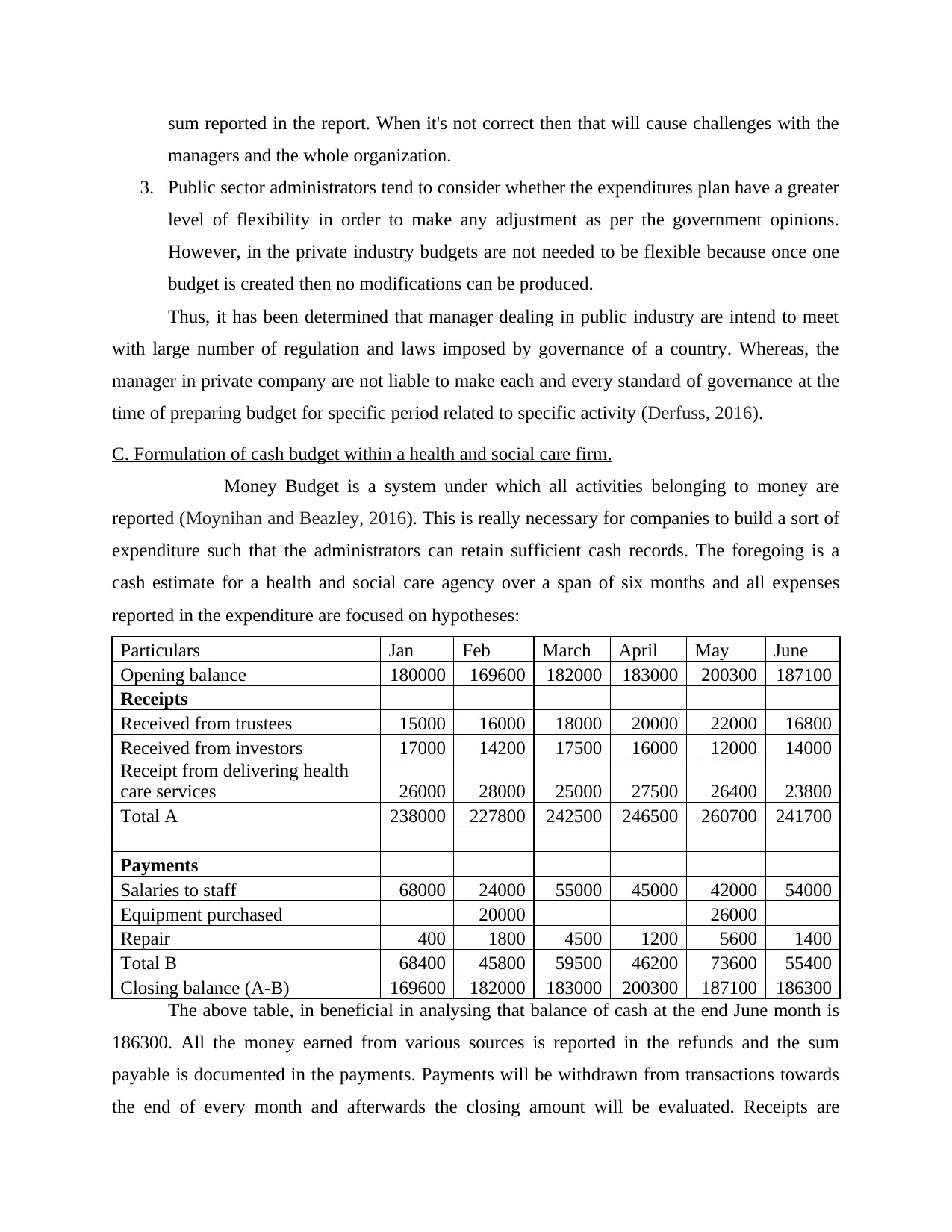

C. Formulation of cash budget within a health and social care firm.

Money Budget is a system under which all activities belonging to money are

reported (Moynihan and Beazley, 2016). This is really necessary for companies to build a sort of

expenditure such that the administrators can retain sufficient cash records. The foregoing is a

cash estimate for a health and social care agency over a span of six months and all expenses

reported in the expenditure are focused on hypotheses:

Particulars Jan Feb March April May June

Opening balance 180000 169600 182000 183000 200300 187100

Receipts

Received from trustees 15000 16000 18000 20000 22000 16800

Received from investors 17000 14200 17500 16000 12000 14000

Receipt from delivering health

care services 26000 28000 25000 27500 26400 23800

Total A 238000 227800 242500 246500 260700 241700

Payments

Salaries to staff 68000 24000 55000 45000 42000 54000

Equipment purchased 20000 26000

Repair 400 1800 4500 1200 5600 1400

Total B 68400 45800 59500 46200 73600 55400

Closing balance (A-B) 169600 182000 183000 200300 187100 186300

The above table, in beneficial in analysing that balance of cash at the end June month is

186300. All the money earned from various sources is reported in the refunds and the sum

payable is documented in the payments. Payments will be withdrawn from transactions towards

the end of every month and afterwards the closing amount will be evaluated. Receipts are

managers and the whole organization.

3. Public sector administrators tend to consider whether the expenditures plan have a greater

level of flexibility in order to make any adjustment as per the government opinions.

However, in the private industry budgets are not needed to be flexible because once one

budget is created then no modifications can be produced.

Thus, it has been determined that manager dealing in public industry are intend to meet

with large number of regulation and laws imposed by governance of a country. Whereas, the

manager in private company are not liable to make each and every standard of governance at the

time of preparing budget for specific period related to specific activity (Derfuss, 2016).

C. Formulation of cash budget within a health and social care firm.

Money Budget is a system under which all activities belonging to money are

reported (Moynihan and Beazley, 2016). This is really necessary for companies to build a sort of

expenditure such that the administrators can retain sufficient cash records. The foregoing is a

cash estimate for a health and social care agency over a span of six months and all expenses

reported in the expenditure are focused on hypotheses:

Particulars Jan Feb March April May June

Opening balance 180000 169600 182000 183000 200300 187100

Receipts

Received from trustees 15000 16000 18000 20000 22000 16800

Received from investors 17000 14200 17500 16000 12000 14000

Receipt from delivering health

care services 26000 28000 25000 27500 26400 23800

Total A 238000 227800 242500 246500 260700 241700

Payments

Salaries to staff 68000 24000 55000 45000 42000 54000

Equipment purchased 20000 26000

Repair 400 1800 4500 1200 5600 1400

Total B 68400 45800 59500 46200 73600 55400

Closing balance (A-B) 169600 182000 183000 200300 187100 186300

The above table, in beneficial in analysing that balance of cash at the end June month is

186300. All the money earned from various sources is reported in the refunds and the sum

payable is documented in the payments. Payments will be withdrawn from transactions towards

the end of every month and afterwards the closing amount will be evaluated. Receipts are

reported in the financial expenditure only as monetary payments. Any trade contributing to credit

is not applied to the cash bill. It will direct management in evaluating whether the business is

financially healthy or not for that period.

D. Awareness on the impact of financial constraints, costs and budget on health and social care

service managers, their clients and stakeholders

Costs: Total resources incurred by hospitals and social care agencies to provide programs

to consumers are defined as charges. Controlling expenses is extremely essential for corporate

companies, so that higher income may be gained from pleasing customers (Johnson and Pfeiffer,

2016). Price greater or smaller all leave influences on consumers. If a business increases its

costs, therefore consumers ' interest in the organization that decrease because they do not favour

those businesses that offer services at higher prices because opposed to others. Setting low rates

will also have a detrimental effect on the company as top-level consumers may believe the

businesses cannot suit their position and this is why they move to another firm. To cope with this

effect, it is really necessary to establish the correct prices for the services that it provides to the

consumers, or the company. Justification of consumers can help to calculate reasonable costs for

the services provided by a health and social agency.

Budget: The strategy that is developed in the phase of budgeting is regarded as the

budget in which potential and past expenditure data is documented. It is basing mostly on data

from the previous year. This is extremely necessary for corporate companies to evaluate the

expenditures in order to provide the owners with fair and accurate client details. This leaves

effect directly on creditors since, if it is not correctly developed, it is not feasible to forecast

potential requirements and assign funds to corporate activities. In order to maximize their

involvement in the business, agency administrators are expected to take responsible decisions

and efficiently build budgets such that shareholder confidence can be obtained.

Financial constraints: This can be described as the shortage of financial capital and

considering the lack of funds people and organizations could not afford anything in this case.

This is really necessary for all companies to evaluate most of them so that the company

operations can be conducted in an acceptable way at the moment of the result. It will influence

the service operators as they need to be more conscious of the problems at the moment and make

appropriate choices to solve them. Less funds for operating operations are one of the key

financial restrictions and in this scenario the administrators have to behave smartly and consider

is not applied to the cash bill. It will direct management in evaluating whether the business is

financially healthy or not for that period.

D. Awareness on the impact of financial constraints, costs and budget on health and social care

service managers, their clients and stakeholders

Costs: Total resources incurred by hospitals and social care agencies to provide programs

to consumers are defined as charges. Controlling expenses is extremely essential for corporate

companies, so that higher income may be gained from pleasing customers (Johnson and Pfeiffer,

2016). Price greater or smaller all leave influences on consumers. If a business increases its

costs, therefore consumers ' interest in the organization that decrease because they do not favour

those businesses that offer services at higher prices because opposed to others. Setting low rates

will also have a detrimental effect on the company as top-level consumers may believe the

businesses cannot suit their position and this is why they move to another firm. To cope with this

effect, it is really necessary to establish the correct prices for the services that it provides to the

consumers, or the company. Justification of consumers can help to calculate reasonable costs for

the services provided by a health and social agency.

Budget: The strategy that is developed in the phase of budgeting is regarded as the

budget in which potential and past expenditure data is documented. It is basing mostly on data

from the previous year. This is extremely necessary for corporate companies to evaluate the

expenditures in order to provide the owners with fair and accurate client details. This leaves

effect directly on creditors since, if it is not correctly developed, it is not feasible to forecast

potential requirements and assign funds to corporate activities. In order to maximize their

involvement in the business, agency administrators are expected to take responsible decisions

and efficiently build budgets such that shareholder confidence can be obtained.

Financial constraints: This can be described as the shortage of financial capital and

considering the lack of funds people and organizations could not afford anything in this case.

This is really necessary for all companies to evaluate most of them so that the company

operations can be conducted in an acceptable way at the moment of the result. It will influence

the service operators as they need to be more conscious of the problems at the moment and make

appropriate choices to solve them. Less funds for operating operations are one of the key

financial restrictions and in this scenario the administrators have to behave smartly and consider

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.