Comprehensive Financial Budgeting, Analysis, and Performance Report

VerifiedAdded on 2020/06/05

|22

|5815

|32

Report

AI Summary

This comprehensive report delves into the core principles of budgeting and financial management. It begins with an introduction to budgeting, emphasizing its importance in forecasting expenditures and revenues. The report then presents various assessments, including sales, purchase, and expense budgets, followed by an analysis of income statements and cash flow projections. It explores flexible budgets, performance reports, and variance analysis to evaluate financial performance. The report also discusses the advantages and disadvantages of budgeting, providing a balanced view of its utility. Furthermore, it includes detailed case studies, such as the 'Pete Sampras' example, demonstrating the practical application of budgeting tools. The conclusion synthesizes the key findings, reinforcing the significance of budgeting in effective financial management, supported by references to relevant literature.

Develop and Manage a

Budget

Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

1...................................................................................................................................................1

2...................................................................................................................................................1

3...................................................................................................................................................1

4...................................................................................................................................................2

5...................................................................................................................................................2

6...................................................................................................................................................3

ASSESSMENT 2.............................................................................................................................4

ASSESSMENT 3.............................................................................................................................4

B) & C)........................................................................................................................................5

D, E & F......................................................................................................................................7

Covered in PPT...........................................................................................................................7

Assessment Activity 4......................................................................................................................7

Question 1...................................................................................................................................7

Question 2...................................................................................................................................8

Question 3.................................................................................................................................14

Question 4.................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION ..........................................................................................................................1

ASSESSMENT 1.............................................................................................................................1

1...................................................................................................................................................1

2...................................................................................................................................................1

3...................................................................................................................................................1

4...................................................................................................................................................2

5...................................................................................................................................................2

6...................................................................................................................................................3

ASSESSMENT 2.............................................................................................................................4

ASSESSMENT 3.............................................................................................................................4

B) & C)........................................................................................................................................5

D, E & F......................................................................................................................................7

Covered in PPT...........................................................................................................................7

Assessment Activity 4......................................................................................................................7

Question 1...................................................................................................................................7

Question 2...................................................................................................................................8

Question 3.................................................................................................................................14

Question 4.................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Budgeting is the important process which is adopted by the management of every

organisation to make the assumptions regarding the amount of expenditures and revenues which

is going to incur in future period of time (Bloch, Blumberg and Laartz, 2012). Such budgets are

prepared on the basis of the estimation of the past data. In this report, various budgets are used in

order to manage the risk in an effective manner. Although, this can be rightly said that the

management needs to adopt diverse kinds of budgets in order to foresee the future course of

actions of the organisation.

ASSESSMENT 1

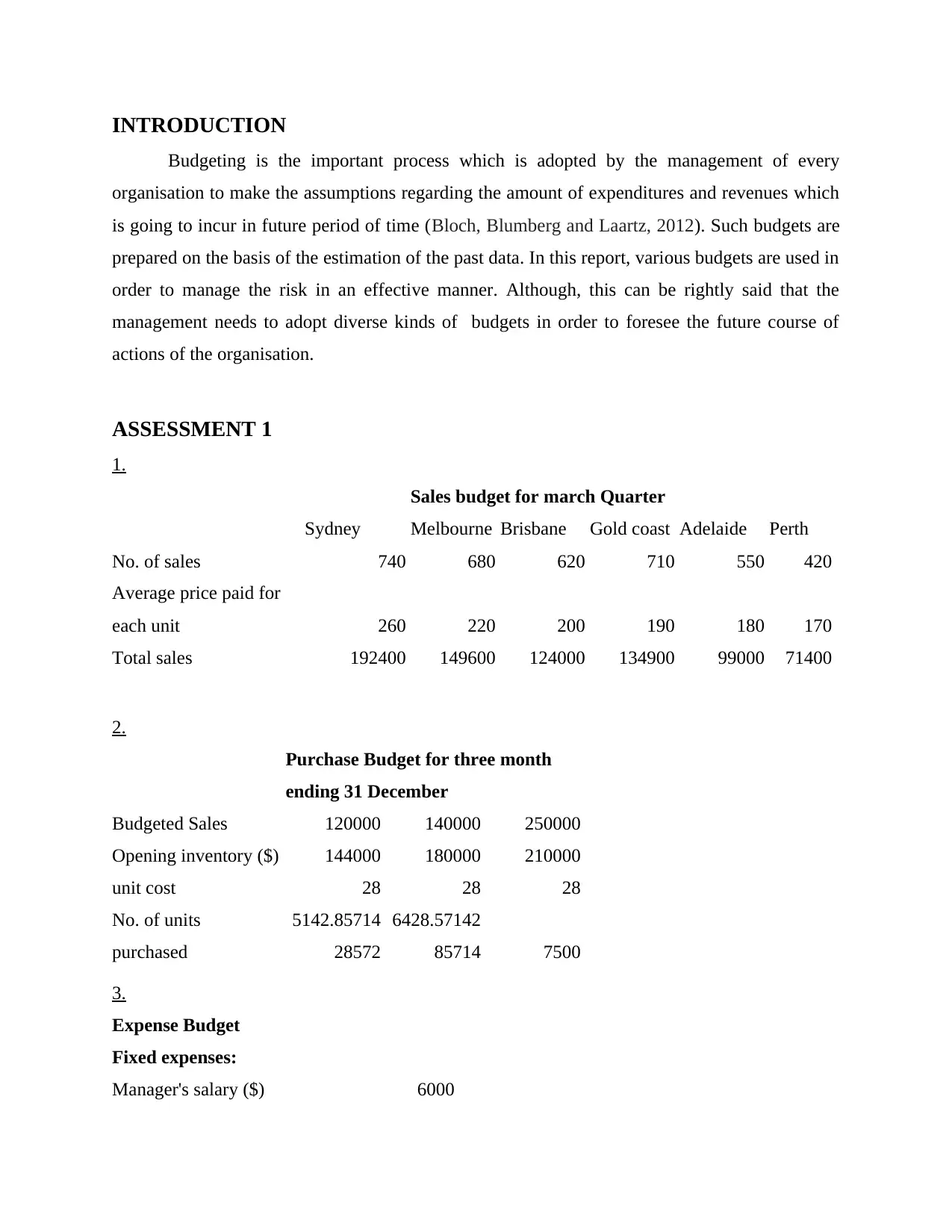

1.

Sales budget for march Quarter

Sydney Melbourne Brisbane Gold coast Adelaide Perth

No. of sales 740 680 620 710 550 420

Average price paid for

each unit 260 220 200 190 180 170

Total sales 192400 149600 124000 134900 99000 71400

2.

Purchase Budget for three month

ending 31 December

Budgeted Sales 120000 140000 250000

Opening inventory ($) 144000 180000 210000

unit cost 28 28 28

No. of units

purchased

5142.85714

28572

6428.57142

85714 7500

3.

Expense Budget

Fixed expenses:

Manager's salary ($) 6000

Budgeting is the important process which is adopted by the management of every

organisation to make the assumptions regarding the amount of expenditures and revenues which

is going to incur in future period of time (Bloch, Blumberg and Laartz, 2012). Such budgets are

prepared on the basis of the estimation of the past data. In this report, various budgets are used in

order to manage the risk in an effective manner. Although, this can be rightly said that the

management needs to adopt diverse kinds of budgets in order to foresee the future course of

actions of the organisation.

ASSESSMENT 1

1.

Sales budget for march Quarter

Sydney Melbourne Brisbane Gold coast Adelaide Perth

No. of sales 740 680 620 710 550 420

Average price paid for

each unit 260 220 200 190 180 170

Total sales 192400 149600 124000 134900 99000 71400

2.

Purchase Budget for three month

ending 31 December

Budgeted Sales 120000 140000 250000

Opening inventory ($) 144000 180000 210000

unit cost 28 28 28

No. of units

purchased

5142.85714

28572

6428.57142

85714 7500

3.

Expense Budget

Fixed expenses:

Manager's salary ($) 6000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

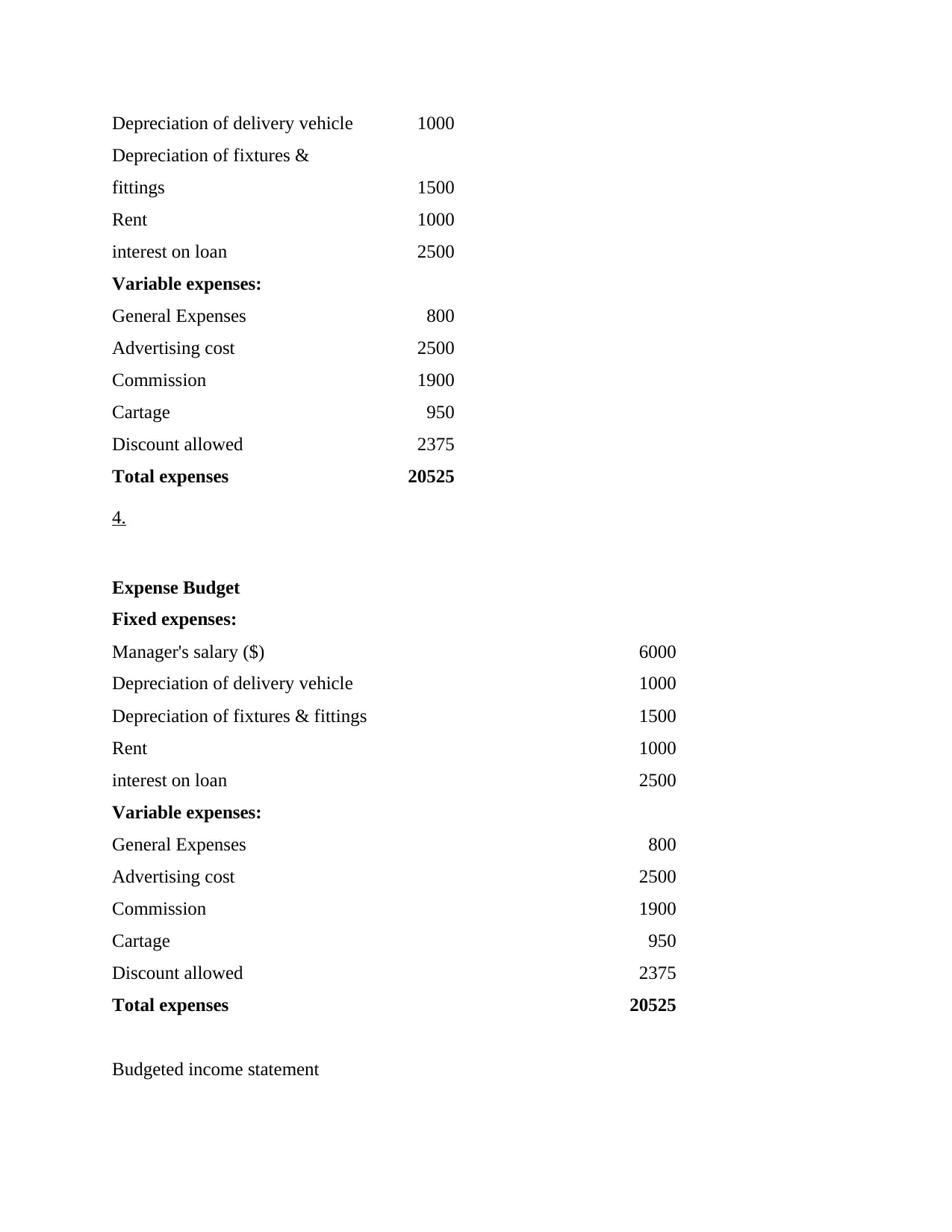

Depreciation of delivery vehicle 1000

Depreciation of fixtures &

fittings 1500

Rent 1000

interest on loan 2500

Variable expenses:

General Expenses 800

Advertising cost 2500

Commission 1900

Cartage 950

Discount allowed 2375

Total expenses 20525

4.

Expense Budget

Fixed expenses:

Manager's salary ($) 6000

Depreciation of delivery vehicle 1000

Depreciation of fixtures & fittings 1500

Rent 1000

interest on loan 2500

Variable expenses:

General Expenses 800

Advertising cost 2500

Commission 1900

Cartage 950

Discount allowed 2375

Total expenses 20525

Budgeted income statement

Depreciation of fixtures &

fittings 1500

Rent 1000

interest on loan 2500

Variable expenses:

General Expenses 800

Advertising cost 2500

Commission 1900

Cartage 950

Discount allowed 2375

Total expenses 20525

4.

Expense Budget

Fixed expenses:

Manager's salary ($) 6000

Depreciation of delivery vehicle 1000

Depreciation of fixtures & fittings 1500

Rent 1000

interest on loan 2500

Variable expenses:

General Expenses 800

Advertising cost 2500

Commission 1900

Cartage 950

Discount allowed 2375

Total expenses 20525

Budgeted income statement

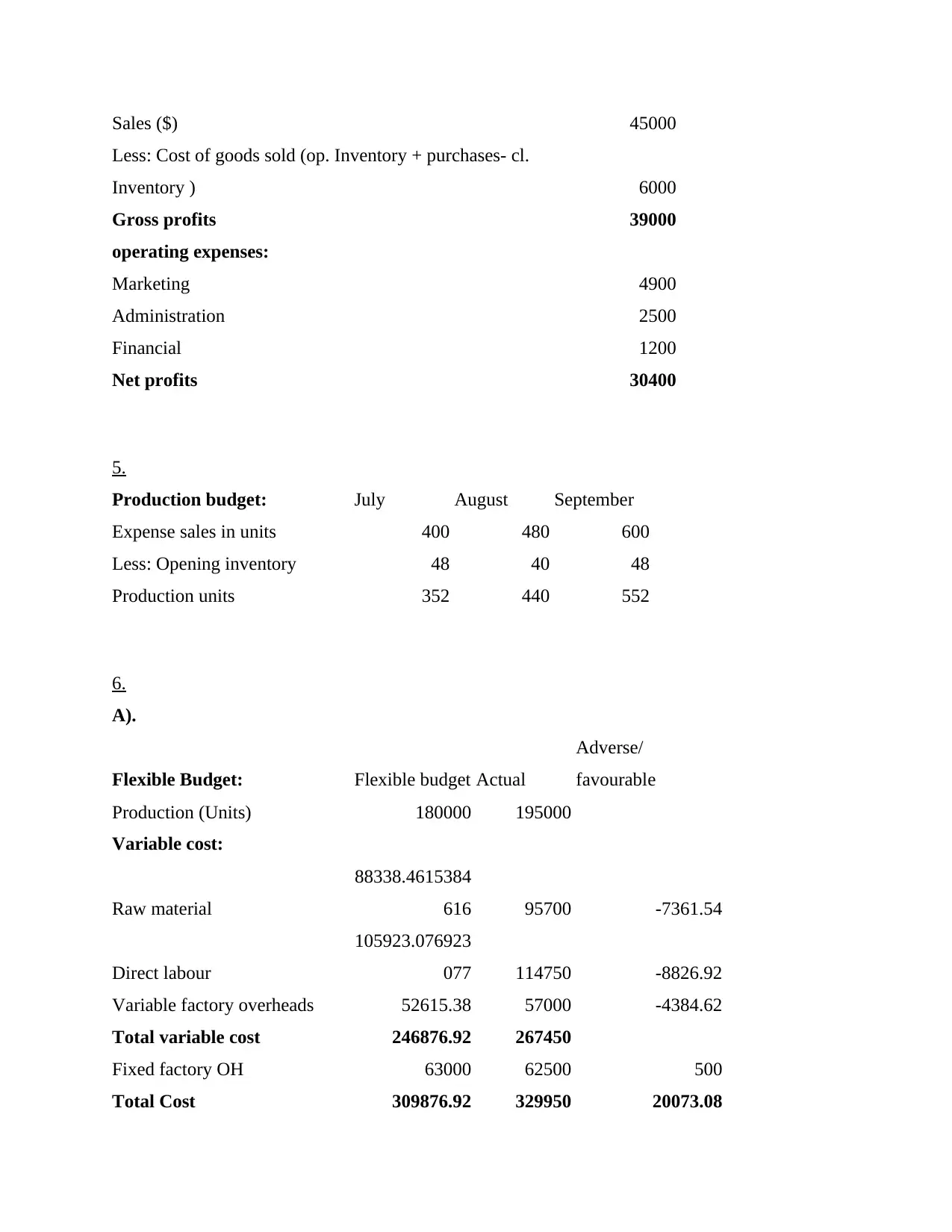

Sales ($) 45000

Less: Cost of goods sold (op. Inventory + purchases- cl.

Inventory ) 6000

Gross profits 39000

operating expenses:

Marketing 4900

Administration 2500

Financial 1200

Net profits 30400

5.

Production budget: July August September

Expense sales in units 400 480 600

Less: Opening inventory 48 40 48

Production units 352 440 552

6.

A).

Flexible Budget: Flexible budget Actual

Adverse/

favourable

Production (Units) 180000 195000

Variable cost:

Raw material

88338.4615384

616 95700 -7361.54

Direct labour

105923.076923

077 114750 -8826.92

Variable factory overheads 52615.38 57000 -4384.62

Total variable cost 246876.92 267450

Fixed factory OH 63000 62500 500

Total Cost 309876.92 329950 20073.08

Less: Cost of goods sold (op. Inventory + purchases- cl.

Inventory ) 6000

Gross profits 39000

operating expenses:

Marketing 4900

Administration 2500

Financial 1200

Net profits 30400

5.

Production budget: July August September

Expense sales in units 400 480 600

Less: Opening inventory 48 40 48

Production units 352 440 552

6.

A).

Flexible Budget: Flexible budget Actual

Adverse/

favourable

Production (Units) 180000 195000

Variable cost:

Raw material

88338.4615384

616 95700 -7361.54

Direct labour

105923.076923

077 114750 -8826.92

Variable factory overheads 52615.38 57000 -4384.62

Total variable cost 246876.92 267450

Fixed factory OH 63000 62500 500

Total Cost 309876.92 329950 20073.08

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

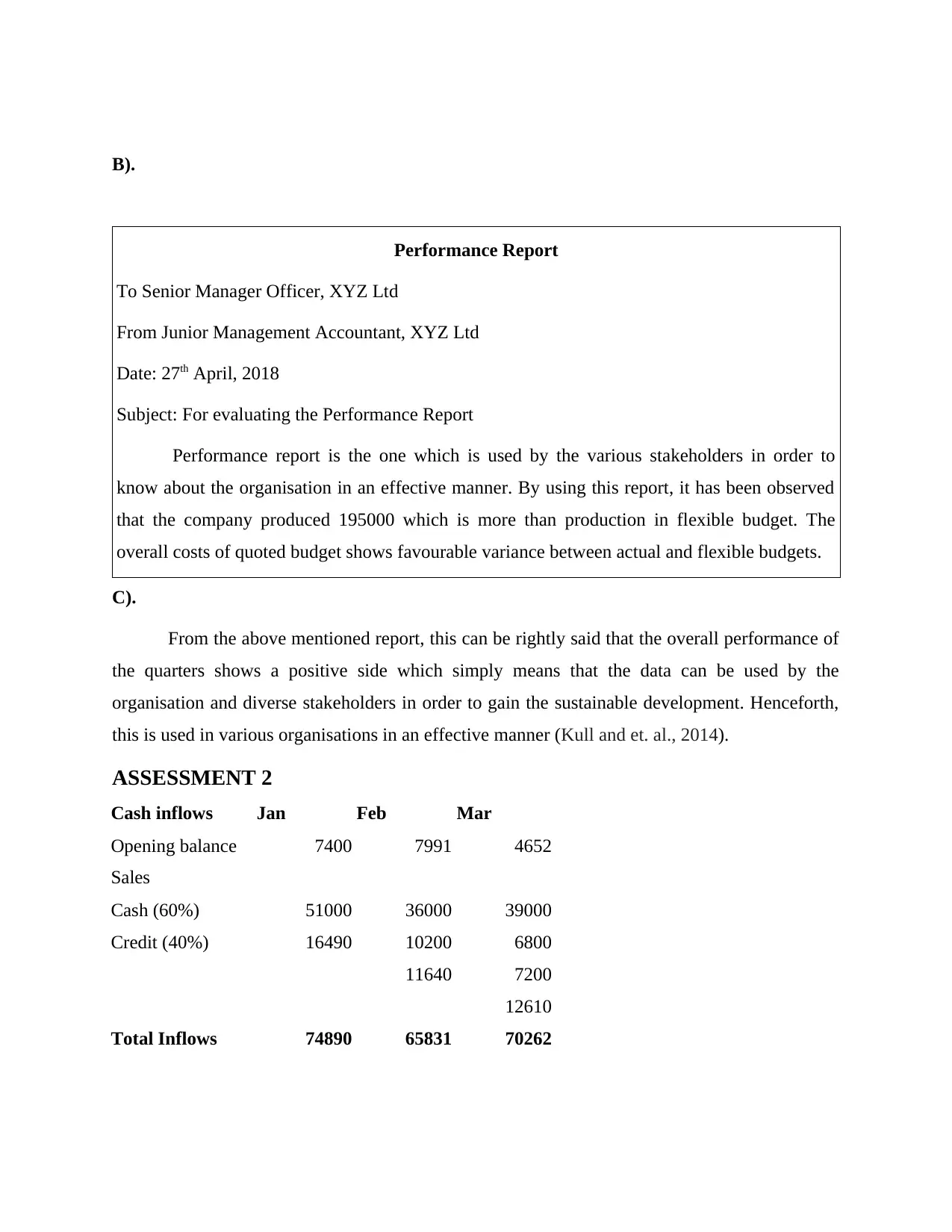

B).

Performance Report

To Senior Manager Officer, XYZ Ltd

From Junior Management Accountant, XYZ Ltd

Date: 27th April, 2018

Subject: For evaluating the Performance Report

Performance report is the one which is used by the various stakeholders in order to

know about the organisation in an effective manner. By using this report, it has been observed

that the company produced 195000 which is more than production in flexible budget. The

overall costs of quoted budget shows favourable variance between actual and flexible budgets.

C).

From the above mentioned report, this can be rightly said that the overall performance of

the quarters shows a positive side which simply means that the data can be used by the

organisation and diverse stakeholders in order to gain the sustainable development. Henceforth,

this is used in various organisations in an effective manner (Kull and et. al., 2014).

ASSESSMENT 2

Cash inflows Jan Feb Mar

Opening balance 7400 7991 4652

Sales

Cash (60%) 51000 36000 39000

Credit (40%) 16490 10200 6800

11640 7200

12610

Total Inflows 74890 65831 70262

Performance Report

To Senior Manager Officer, XYZ Ltd

From Junior Management Accountant, XYZ Ltd

Date: 27th April, 2018

Subject: For evaluating the Performance Report

Performance report is the one which is used by the various stakeholders in order to

know about the organisation in an effective manner. By using this report, it has been observed

that the company produced 195000 which is more than production in flexible budget. The

overall costs of quoted budget shows favourable variance between actual and flexible budgets.

C).

From the above mentioned report, this can be rightly said that the overall performance of

the quarters shows a positive side which simply means that the data can be used by the

organisation and diverse stakeholders in order to gain the sustainable development. Henceforth,

this is used in various organisations in an effective manner (Kull and et. al., 2014).

ASSESSMENT 2

Cash inflows Jan Feb Mar

Opening balance 7400 7991 4652

Sales

Cash (60%) 51000 36000 39000

Credit (40%) 16490 10200 6800

11640 7200

12610

Total Inflows 74890 65831 70262

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cash Outflows

Purchase 39984 10200 0

28224 7200

30576

Other Expenses 7115 7115 7115

Salary 8000 8640 8640

Drawings 7000 7000 7000

GST 4800

Total Outflows 66899 61179 60531

Cash Balance 7991 4652 9731

ASSESSMENT 3

A).

Budgeted income statements helps organisation to forecast the revenues of the

organisation apart from that expenses (Schick, 2015). As per this, actual expenses are

then compared to the budgeted expenses and if any kind of favourable variances occurred

then in that situation, company would get to know about the business objectives in an

effective manner. On the other hand, this could be rightly said that the budgeted incomes

statement helps to know about the business performance are adequately used in this or

not. While this would finally help out to gain the business objectives attainable. If the

variances happen in an adverse way. Then, in this there is a requirement to overcome

such types of values by using various management accounting tools in an effective

manner. However, this can be rightly said that the organisation is required to address this

in an efficient manner. Budgeted income statement assist an organisation to forecast the

revenues of the organisation along with expenses. This is the tool which can be used by

the organisation in a most effective manner.

It can be rightly observed that the management is required to the assess about the cash

transactions henceforth, they needs to form appropriate cash statements (Rummler and

Brache, 2012).

Budgeted balance sheet assist organisation to make the operational manner. Henceforth,

this would help out to assess about the predicted balance sheet. A budgeted sheet is a

report which management implements to forecasted levels of assets, liabilities, and

Purchase 39984 10200 0

28224 7200

30576

Other Expenses 7115 7115 7115

Salary 8000 8640 8640

Drawings 7000 7000 7000

GST 4800

Total Outflows 66899 61179 60531

Cash Balance 7991 4652 9731

ASSESSMENT 3

A).

Budgeted income statements helps organisation to forecast the revenues of the

organisation apart from that expenses (Schick, 2015). As per this, actual expenses are

then compared to the budgeted expenses and if any kind of favourable variances occurred

then in that situation, company would get to know about the business objectives in an

effective manner. On the other hand, this could be rightly said that the budgeted incomes

statement helps to know about the business performance are adequately used in this or

not. While this would finally help out to gain the business objectives attainable. If the

variances happen in an adverse way. Then, in this there is a requirement to overcome

such types of values by using various management accounting tools in an effective

manner. However, this can be rightly said that the organisation is required to address this

in an efficient manner. Budgeted income statement assist an organisation to forecast the

revenues of the organisation along with expenses. This is the tool which can be used by

the organisation in a most effective manner.

It can be rightly observed that the management is required to the assess about the cash

transactions henceforth, they needs to form appropriate cash statements (Rummler and

Brache, 2012).

Budgeted balance sheet assist organisation to make the operational manner. Henceforth,

this would help out to assess about the predicted balance sheet. A budgeted sheet is a

report which management implements to forecasted levels of assets, liabilities, and

equity which are relied upon the budget for existing accounting period. On the other

hand, budgeted balance sheet demonstrates where whole account will be at the end of

period. At the end of each period, management normally introduces planning a master

budget for the next period (Davila, Epstein and Shelton, 2012). Master budget is formed

up of a ton of little budgets for sales, cash, selling expenses and basic expenses. Whole of

these are integrated to form one comprehensive financial plans. If the master budget is

completed, manager requires to oversee about what kinds of organisation financial

statements would oversee if an organisation could attain their targets for period. These

kinds of two reports summary affects the budget would needs on the financial position of

the organisation if budgeted numbers are meet out. Management wants to investigate

their plans in order to assure that they are required to be done in the best interest in the

long run.

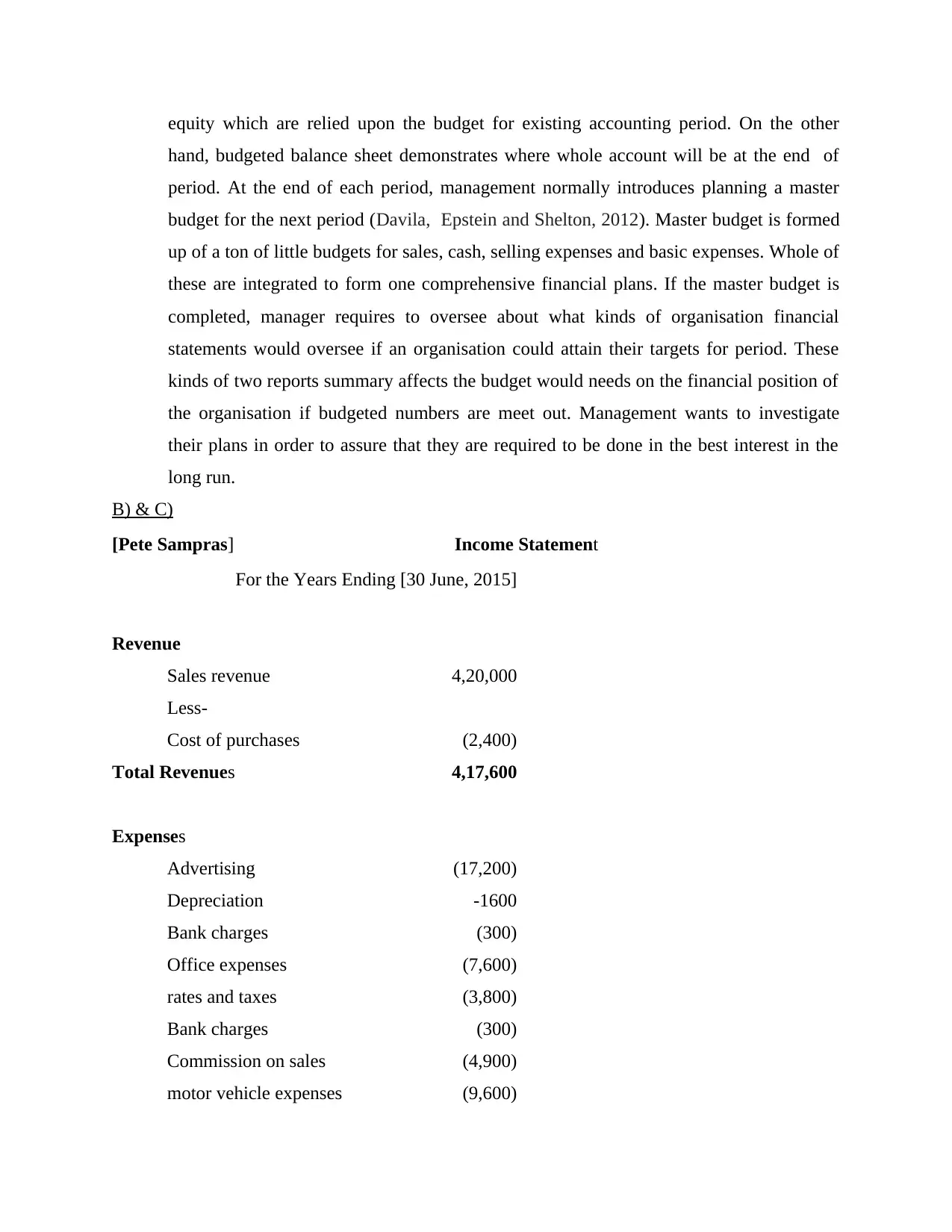

B) & C)

[Pete Sampras] Income Statement

For the Years Ending [30 June, 2015]

Revenue

Sales revenue 4,20,000

Less-

Cost of purchases (2,400)

Total Revenues 4,17,600

Expenses

Advertising (17,200)

Depreciation -1600

Bank charges (300)

Office expenses (7,600)

rates and taxes (3,800)

Bank charges (300)

Commission on sales (4,900)

motor vehicle expenses (9,600)

hand, budgeted balance sheet demonstrates where whole account will be at the end of

period. At the end of each period, management normally introduces planning a master

budget for the next period (Davila, Epstein and Shelton, 2012). Master budget is formed

up of a ton of little budgets for sales, cash, selling expenses and basic expenses. Whole of

these are integrated to form one comprehensive financial plans. If the master budget is

completed, manager requires to oversee about what kinds of organisation financial

statements would oversee if an organisation could attain their targets for period. These

kinds of two reports summary affects the budget would needs on the financial position of

the organisation if budgeted numbers are meet out. Management wants to investigate

their plans in order to assure that they are required to be done in the best interest in the

long run.

B) & C)

[Pete Sampras] Income Statement

For the Years Ending [30 June, 2015]

Revenue

Sales revenue 4,20,000

Less-

Cost of purchases (2,400)

Total Revenues 4,17,600

Expenses

Advertising (17,200)

Depreciation -1600

Bank charges (300)

Office expenses (7,600)

rates and taxes (3,800)

Bank charges (300)

Commission on sales (4,900)

motor vehicle expenses (9,600)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

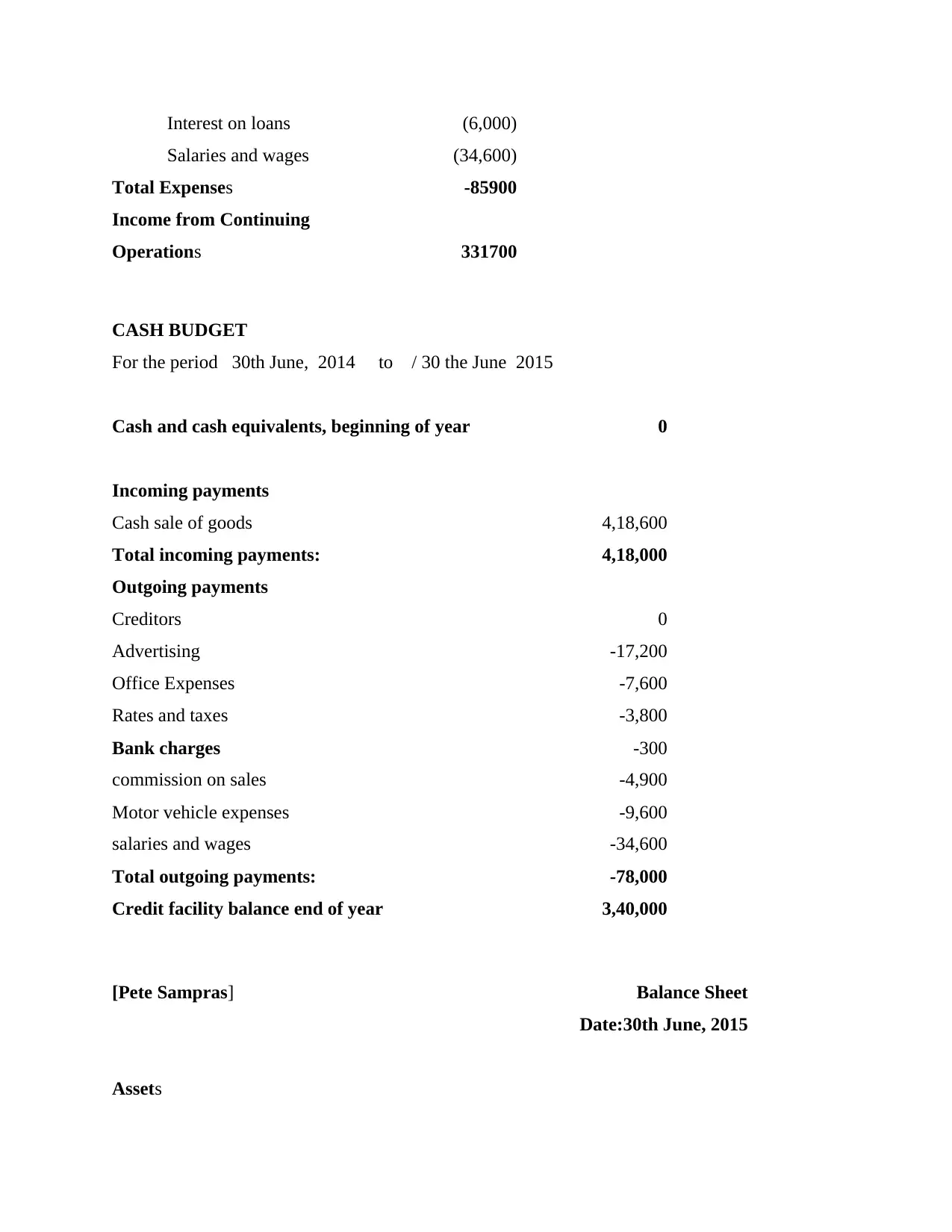

Interest on loans (6,000)

Salaries and wages (34,600)

Total Expenses -85900

Income from Continuing

Operations 331700

CASH BUDGET

For the period 30th June, 2014 to / 30 the June 2015

Cash and cash equivalents, beginning of year 0

Incoming payments

Cash sale of goods 4,18,600

Total incoming payments: 4,18,000

Outgoing payments

Creditors 0

Advertising -17,200

Office Expenses -7,600

Rates and taxes -3,800

Bank charges -300

commission on sales -4,900

Motor vehicle expenses -9,600

salaries and wages -34,600

Total outgoing payments: -78,000

Credit facility balance end of year 3,40,000

[Pete Sampras] Balance Sheet

Date:30th June, 2015

Assets

Salaries and wages (34,600)

Total Expenses -85900

Income from Continuing

Operations 331700

CASH BUDGET

For the period 30th June, 2014 to / 30 the June 2015

Cash and cash equivalents, beginning of year 0

Incoming payments

Cash sale of goods 4,18,600

Total incoming payments: 4,18,000

Outgoing payments

Creditors 0

Advertising -17,200

Office Expenses -7,600

Rates and taxes -3,800

Bank charges -300

commission on sales -4,900

Motor vehicle expenses -9,600

salaries and wages -34,600

Total outgoing payments: -78,000

Credit facility balance end of year 3,40,000

[Pete Sampras] Balance Sheet

Date:30th June, 2015

Assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

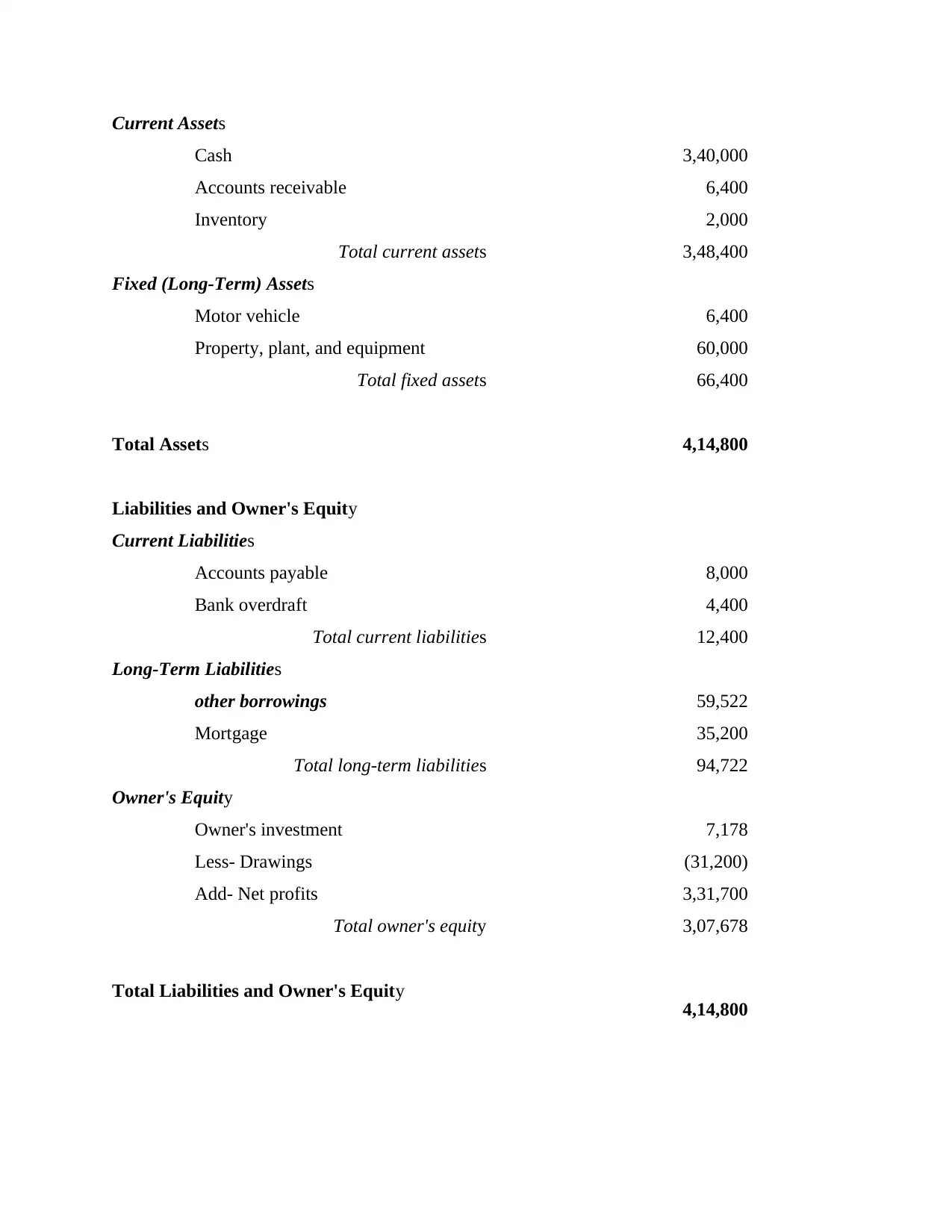

Current Assets

Cash 3,40,000

Accounts receivable 6,400

Inventory 2,000

Total current assets 3,48,400

Fixed (Long-Term) Assets

Motor vehicle 6,400

Property, plant, and equipment 60,000

Total fixed assets 66,400

Total Assets 4,14,800

Liabilities and Owner's Equity

Current Liabilities

Accounts payable 8,000

Bank overdraft 4,400

Total current liabilities 12,400

Long-Term Liabilities

other borrowings 59,522

Mortgage 35,200

Total long-term liabilities 94,722

Owner's Equity

Owner's investment 7,178

Less- Drawings (31,200)

Add- Net profits 3,31,700

Total owner's equity 3,07,678

Total Liabilities and Owner's Equity 4,14,800

Cash 3,40,000

Accounts receivable 6,400

Inventory 2,000

Total current assets 3,48,400

Fixed (Long-Term) Assets

Motor vehicle 6,400

Property, plant, and equipment 60,000

Total fixed assets 66,400

Total Assets 4,14,800

Liabilities and Owner's Equity

Current Liabilities

Accounts payable 8,000

Bank overdraft 4,400

Total current liabilities 12,400

Long-Term Liabilities

other borrowings 59,522

Mortgage 35,200

Total long-term liabilities 94,722

Owner's Equity

Owner's investment 7,178

Less- Drawings (31,200)

Add- Net profits 3,31,700

Total owner's equity 3,07,678

Total Liabilities and Owner's Equity 4,14,800

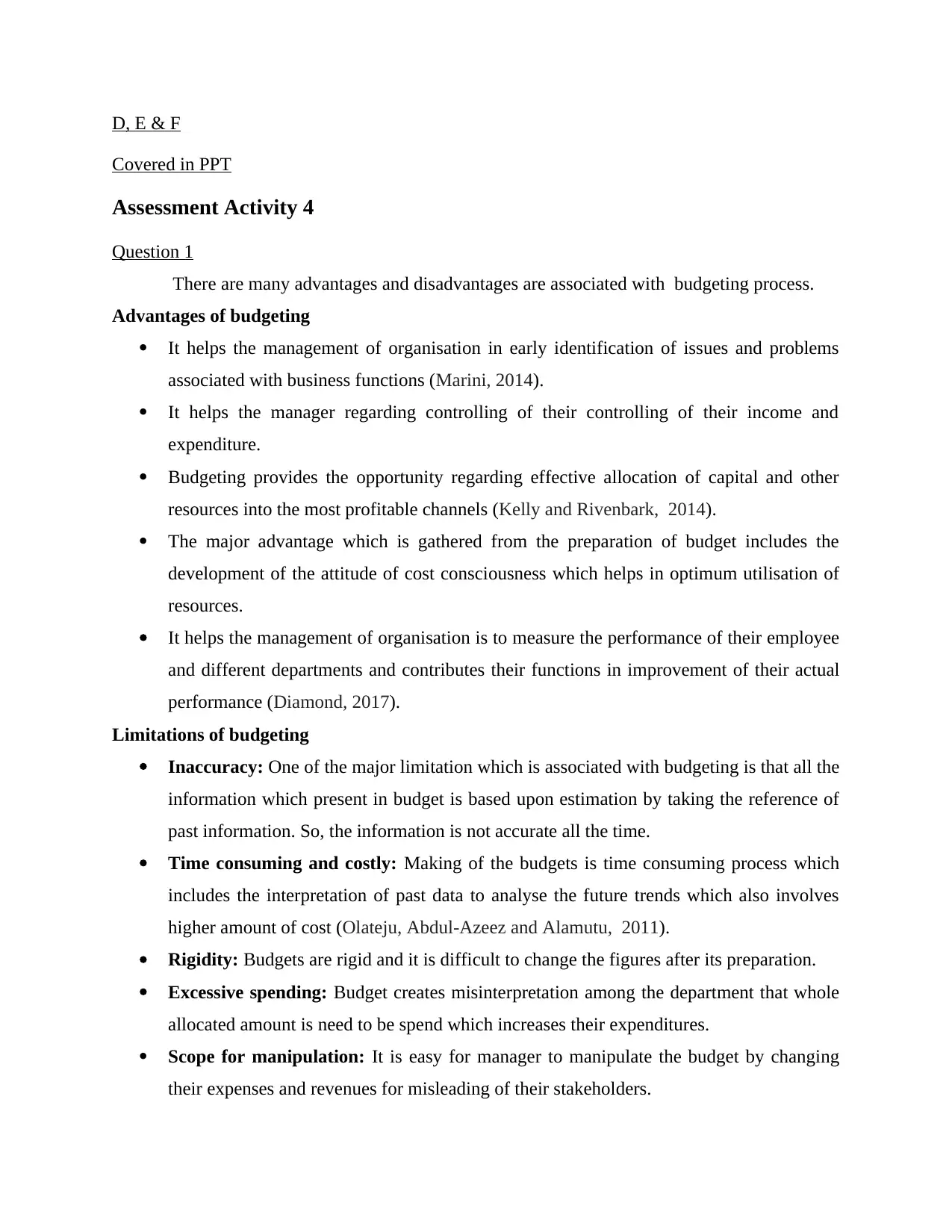

D, E & F

Covered in PPT

Assessment Activity 4

Question 1

There are many advantages and disadvantages are associated with budgeting process.

Advantages of budgeting

It helps the management of organisation in early identification of issues and problems

associated with business functions (Marini, 2014).

It helps the manager regarding controlling of their controlling of their income and

expenditure.

Budgeting provides the opportunity regarding effective allocation of capital and other

resources into the most profitable channels (Kelly and Rivenbark, 2014).

The major advantage which is gathered from the preparation of budget includes the

development of the attitude of cost consciousness which helps in optimum utilisation of

resources.

It helps the management of organisation is to measure the performance of their employee

and different departments and contributes their functions in improvement of their actual

performance (Diamond, 2017).

Limitations of budgeting

Inaccuracy: One of the major limitation which is associated with budgeting is that all the

information which present in budget is based upon estimation by taking the reference of

past information. So, the information is not accurate all the time.

Time consuming and costly: Making of the budgets is time consuming process which

includes the interpretation of past data to analyse the future trends which also involves

higher amount of cost (Olateju, Abdul-Azeez and Alamutu, 2011).

Rigidity: Budgets are rigid and it is difficult to change the figures after its preparation.

Excessive spending: Budget creates misinterpretation among the department that whole

allocated amount is need to be spend which increases their expenditures.

Scope for manipulation: It is easy for manager to manipulate the budget by changing

their expenses and revenues for misleading of their stakeholders.

Covered in PPT

Assessment Activity 4

Question 1

There are many advantages and disadvantages are associated with budgeting process.

Advantages of budgeting

It helps the management of organisation in early identification of issues and problems

associated with business functions (Marini, 2014).

It helps the manager regarding controlling of their controlling of their income and

expenditure.

Budgeting provides the opportunity regarding effective allocation of capital and other

resources into the most profitable channels (Kelly and Rivenbark, 2014).

The major advantage which is gathered from the preparation of budget includes the

development of the attitude of cost consciousness which helps in optimum utilisation of

resources.

It helps the management of organisation is to measure the performance of their employee

and different departments and contributes their functions in improvement of their actual

performance (Diamond, 2017).

Limitations of budgeting

Inaccuracy: One of the major limitation which is associated with budgeting is that all the

information which present in budget is based upon estimation by taking the reference of

past information. So, the information is not accurate all the time.

Time consuming and costly: Making of the budgets is time consuming process which

includes the interpretation of past data to analyse the future trends which also involves

higher amount of cost (Olateju, Abdul-Azeez and Alamutu, 2011).

Rigidity: Budgets are rigid and it is difficult to change the figures after its preparation.

Excessive spending: Budget creates misinterpretation among the department that whole

allocated amount is need to be spend which increases their expenditures.

Scope for manipulation: It is easy for manager to manipulate the budget by changing

their expenses and revenues for misleading of their stakeholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.