Comprehensive Financial Budgeting and Performance Report

VerifiedAdded on 2020/02/17

|29

|4807

|90

Report

AI Summary

This report delves into the critical aspects of financial budgeting and analysis, focusing on sales budgets, cash flow projections, and their relationship to strategic objectives. It includes a detailed sales budget for March, considering various product types and special orders, alongside calculations for labour hours and contributions. The report further explores the coordination and approval processes involved in budget development, reasons for adjustments, and methods of communication. It also provides insights into cash flow projections, comparing different scenarios and offering feedback on specific policies. The report also includes budget variation reports, contingency plans, and CAPEX budgets, providing a comprehensive overview of financial planning and performance analysis. The report analyzes the role of budgeting in an organization and its connection with strategic objectives, along with the allocation of resources and the importance of customer satisfaction. It also offers insights into the impact of labour costs and overheads on the overall financial performance of a business.

DIPLOMA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

QUESTION 1...................................................................................................................................1

Role of budget and its relation with strategic objectives........................................................1

Prepare sales budget for March..............................................................................................2

QUESTION 2.................................................................................................................................10

Budget development coordination and approval process.....................................................10

Reasons for adjust or methods of communication about budgets to employees..................10

Cash flow projections...........................................................................................................11

Provide feedback on Hugo consent......................................................................................14

APPENDIX 1.................................................................................................................................17

TASK A.........................................................................................................................................17

Budget variation report.........................................................................................................17

TASK B.........................................................................................................................................18

Contingency plan..................................................................................................................18

APPENDIX 2.................................................................................................................................19

Budget preparations..............................................................................................................19

CAPEX budget.....................................................................................................................20

Master budget.......................................................................................................................21

Budget notes.........................................................................................................................22

Apportionment of overheads................................................................................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

QUESTION 1...................................................................................................................................1

Role of budget and its relation with strategic objectives........................................................1

Prepare sales budget for March..............................................................................................2

QUESTION 2.................................................................................................................................10

Budget development coordination and approval process.....................................................10

Reasons for adjust or methods of communication about budgets to employees..................10

Cash flow projections...........................................................................................................11

Provide feedback on Hugo consent......................................................................................14

APPENDIX 1.................................................................................................................................17

TASK A.........................................................................................................................................17

Budget variation report.........................................................................................................17

TASK B.........................................................................................................................................18

Contingency plan..................................................................................................................18

APPENDIX 2.................................................................................................................................19

Budget preparations..............................................................................................................19

CAPEX budget.....................................................................................................................20

Master budget.......................................................................................................................21

Budget notes.........................................................................................................................22

Apportionment of overheads................................................................................................22

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

Index of Tables

Table 1: Sales budget.......................................................................................................................2

Table 2: Special order......................................................................................................................3

Table 3: Revised labour costs..........................................................................................................7

Table 4: Material cost......................................................................................................................9

Table 5: Labour costs.......................................................................................................................9

Table 6: Overhead costs...................................................................................................................9

Table 7: Actual cash flow..............................................................................................................11

Table 8: Projected cash flow under Option 1.................................................................................12

Table 9: Table 8: Projected cash flow under Option 2..................................................................13

Table 10: Discount under policy 1.................................................................................................14

Table 11: Discount under policy 2.................................................................................................15

Table 12: Budget variation report..................................................................................................17

Table 13: Revised Contingency plan.............................................................................................18

Table 14: Revised contingency implementation plan....................................................................18

Table 15: Master budget................................................................................................................21

Table 1: Sales budget.......................................................................................................................2

Table 2: Special order......................................................................................................................3

Table 3: Revised labour costs..........................................................................................................7

Table 4: Material cost......................................................................................................................9

Table 5: Labour costs.......................................................................................................................9

Table 6: Overhead costs...................................................................................................................9

Table 7: Actual cash flow..............................................................................................................11

Table 8: Projected cash flow under Option 1.................................................................................12

Table 9: Table 8: Projected cash flow under Option 2..................................................................13

Table 10: Discount under policy 1.................................................................................................14

Table 11: Discount under policy 2.................................................................................................15

Table 12: Budget variation report..................................................................................................17

Table 13: Revised Contingency plan.............................................................................................18

Table 14: Revised contingency implementation plan....................................................................18

Table 15: Master budget................................................................................................................21

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration Index

Illustration 1: CAPEX budget........................................................................................................20

Illustration 1: CAPEX budget........................................................................................................20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Role of an entity get increases with the passage of time as external market changes are

taken into considerations in improving current business performance. This report is all about

preparing various budgets such as sales, production and material usage in order to analyse the

current business performance. Cash flow projections are don that will be helpful for an entity in

order to get higher competitive advantage on the external business environment.

TASK 1

QUESTION 1

Role of budget and its relation with strategic objectives

Budget is regarded as one of the important approach in an organisation to manage all the

expenses incurred in a business. Budgets is a written statements of all the financial resources

incurred in a business for the betterment of the firm. Various kinds of budgets prepared in an

entity as this will help an enterprise in recording all the events appropriately. Budget will act like

a balancing approach in which expenses and income incurred in a business will get stabilise with

the passage of time. It is regarded as important process in an entity that will be helpful for the

business in order to capture higher market share. Expenditure and income incurred in a business

are properly analysed in relation to all the parameters set by an entity. Budget is important tool

used for predicting the future performance of an organisation (Bagliani and Martini, 2012).

Every individual uses budget in analysing its current resources in order to target higher resources

in the external business environment. Forecasting of all the resources is essential for an entity as

in this way they will grab higher opportunities. An entity will prioritize all its aims and targets

which will be helpful for an entity in order to gain higher competitive advantage over variety of

goals and the objectives. Quality of resources is important as the worth of money invested by a

firm in the business will in turn generates higher sales and the revenue for the business.

Frequency of sales need to be increases over a certain period as an entity will enhance its current

revenue by capturing higher market share in the external business environment (Ball, 2013).

It is important for an entity in order to prepare all its aims and the objectives according to

the desired aim of the business. Different kinds of budgets prepared by an entity is to overcome

all the complexities imposed on an entity as their main motive is to capture higher share in the

market. Financial resources currently available in the business need to be tracked by the business

1

Role of an entity get increases with the passage of time as external market changes are

taken into considerations in improving current business performance. This report is all about

preparing various budgets such as sales, production and material usage in order to analyse the

current business performance. Cash flow projections are don that will be helpful for an entity in

order to get higher competitive advantage on the external business environment.

TASK 1

QUESTION 1

Role of budget and its relation with strategic objectives

Budget is regarded as one of the important approach in an organisation to manage all the

expenses incurred in a business. Budgets is a written statements of all the financial resources

incurred in a business for the betterment of the firm. Various kinds of budgets prepared in an

entity as this will help an enterprise in recording all the events appropriately. Budget will act like

a balancing approach in which expenses and income incurred in a business will get stabilise with

the passage of time. It is regarded as important process in an entity that will be helpful for the

business in order to capture higher market share. Expenditure and income incurred in a business

are properly analysed in relation to all the parameters set by an entity. Budget is important tool

used for predicting the future performance of an organisation (Bagliani and Martini, 2012).

Every individual uses budget in analysing its current resources in order to target higher resources

in the external business environment. Forecasting of all the resources is essential for an entity as

in this way they will grab higher opportunities. An entity will prioritize all its aims and targets

which will be helpful for an entity in order to gain higher competitive advantage over variety of

goals and the objectives. Quality of resources is important as the worth of money invested by a

firm in the business will in turn generates higher sales and the revenue for the business.

Frequency of sales need to be increases over a certain period as an entity will enhance its current

revenue by capturing higher market share in the external business environment (Ball, 2013).

It is important for an entity in order to prepare all its aims and the objectives according to

the desired aim of the business. Different kinds of budgets prepared by an entity is to overcome

all the complexities imposed on an entity as their main motive is to capture higher share in the

market. Financial resources currently available in the business need to be tracked by the business

1

as their main motive is to improve the existing business performance of an enterprise with the

passage of time. Variety of budgets are prepared in a business is to improve the current

performance of an enterprise as major motive of the business owner is to achieve all the targets.

Goals and the objectives develop by an entity will be helpful for an organisation in order to

ascertain the overall performance of an enterprise. Role of an entity is to capture higher market

segment by extending the product share in the external market. Products features are added in a

particular product in order to attract large number of customers towards the services offered by

an entity to all its consumers located in the outside business (Ball, 2013). Getting higher level of

customers satisfaction s the primary goals of every enterprise as in this way their current goal

will get achieved. The current business performance of an entity will get increases with the

passage o time as majority of customers relied on the current aims and targets developed by the

business concern. Employees working in a business need to be satisfied by offering high quality

services. Affordable pricing will attract large number of customers located in the external

business environment as the main motive of the business concern is to steal the attention of most

of the clients towards their business. Budgets will cater all the objectives framed by an entity as

they emphasise on both qualitative and quantitative objectives. Financial performance of an

entity is one of the important factors covered in the monetary performance of an entity (Bagliani

and Martini, 2012).

Strategic objectives are linked by an entity with the budget prepared by the business as

the role of an enterprise is to grab the attention of most of the users located in the external

market. Proper segmentation of all the goals and the objectives of an entity will be done based on

the existing performance of an entity. Allocation of all the responsibilities will be based on the

budget prepared by an entity in their organisation. Nature of al the objectives of an entity will

determine the overall business performance of an entity (Ball, 2013). Qualitative aspects and

monetary aspects are linked with each other in order to ensure the overall success of the business

concern by achieving all the desired aims and targets of an entity.

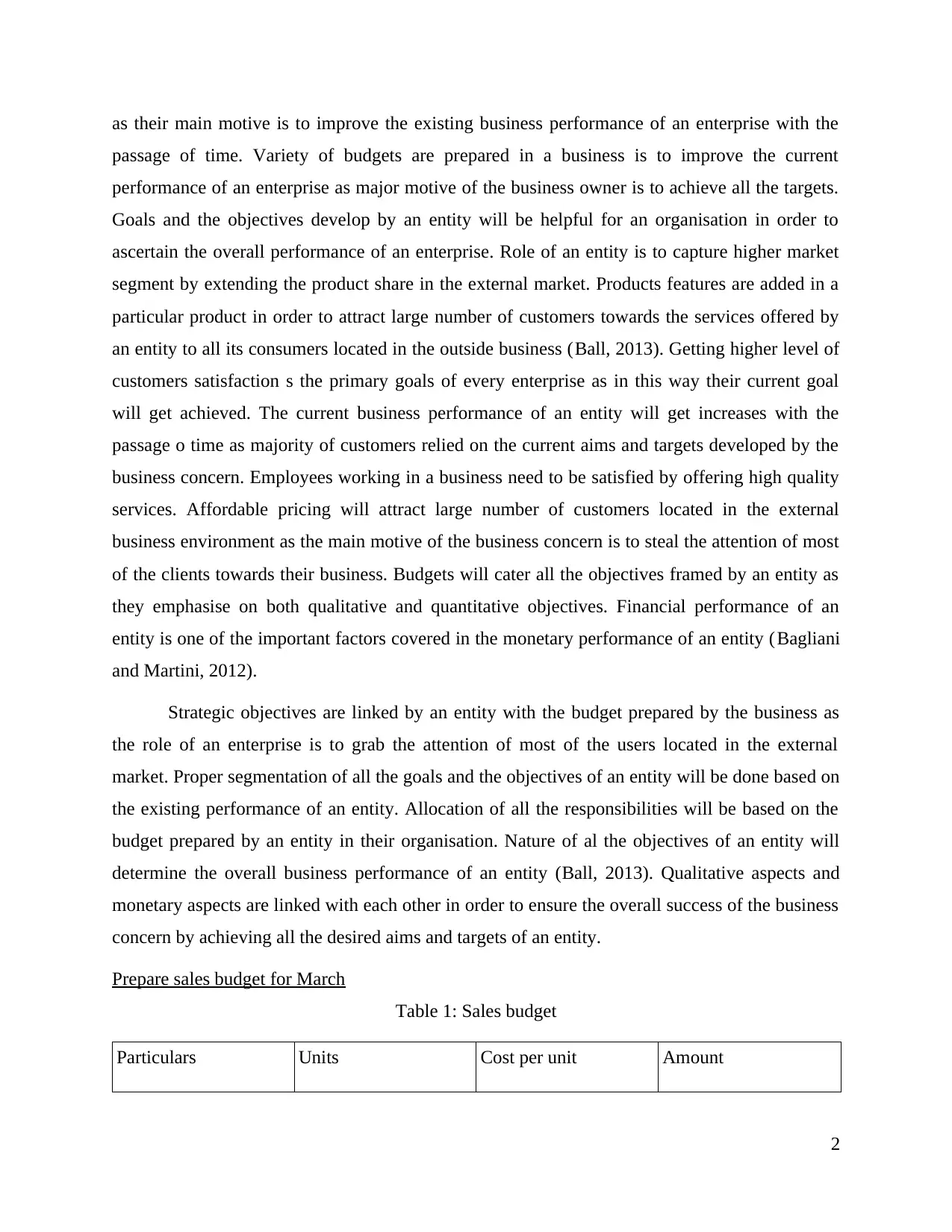

Prepare sales budget for March

Table 1: Sales budget

Particulars Units Cost per unit Amount

2

passage of time. Variety of budgets are prepared in a business is to improve the current

performance of an enterprise as major motive of the business owner is to achieve all the targets.

Goals and the objectives develop by an entity will be helpful for an organisation in order to

ascertain the overall performance of an enterprise. Role of an entity is to capture higher market

segment by extending the product share in the external market. Products features are added in a

particular product in order to attract large number of customers towards the services offered by

an entity to all its consumers located in the outside business (Ball, 2013). Getting higher level of

customers satisfaction s the primary goals of every enterprise as in this way their current goal

will get achieved. The current business performance of an entity will get increases with the

passage o time as majority of customers relied on the current aims and targets developed by the

business concern. Employees working in a business need to be satisfied by offering high quality

services. Affordable pricing will attract large number of customers located in the external

business environment as the main motive of the business concern is to steal the attention of most

of the clients towards their business. Budgets will cater all the objectives framed by an entity as

they emphasise on both qualitative and quantitative objectives. Financial performance of an

entity is one of the important factors covered in the monetary performance of an entity (Bagliani

and Martini, 2012).

Strategic objectives are linked by an entity with the budget prepared by the business as

the role of an enterprise is to grab the attention of most of the users located in the external

market. Proper segmentation of all the goals and the objectives of an entity will be done based on

the existing performance of an entity. Allocation of all the responsibilities will be based on the

budget prepared by an entity in their organisation. Nature of al the objectives of an entity will

determine the overall business performance of an entity (Ball, 2013). Qualitative aspects and

monetary aspects are linked with each other in order to ensure the overall success of the business

concern by achieving all the desired aims and targets of an entity.

Prepare sales budget for March

Table 1: Sales budget

Particulars Units Cost per unit Amount

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Basic 150 250 32500

Standard plus 250 500 125000

Deluxe 200 750 150000

Super deluxe 100 100 100000

Total 700 2500 412500

Table 2: Special order

Particulars Units required Cost per unit Amount

Basic 30 275 8250

Standard plus 50 550 27500

Deluxe 10 750 7500

Super deluxe 5 900 4500

Total 95 2475 47750

Total March 795 4925 760250

Types of Screen Units Cost per unit Amount

Basic 180 525 45750

Standard plus 300 1050 152500

Deluxe 210 1500 157500

Super deluxe 105 1900 104500

Total 795 4975 460250

3

Standard plus 250 500 125000

Deluxe 200 750 150000

Super deluxe 100 100 100000

Total 700 2500 412500

Table 2: Special order

Particulars Units required Cost per unit Amount

Basic 30 275 8250

Standard plus 50 550 27500

Deluxe 10 750 7500

Super deluxe 5 900 4500

Total 95 2475 47750

Total March 795 4925 760250

Types of Screen Units Cost per unit Amount

Basic 180 525 45750

Standard plus 300 1050 152500

Deluxe 210 1500 157500

Super deluxe 105 1900 104500

Total 795 4975 460250

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

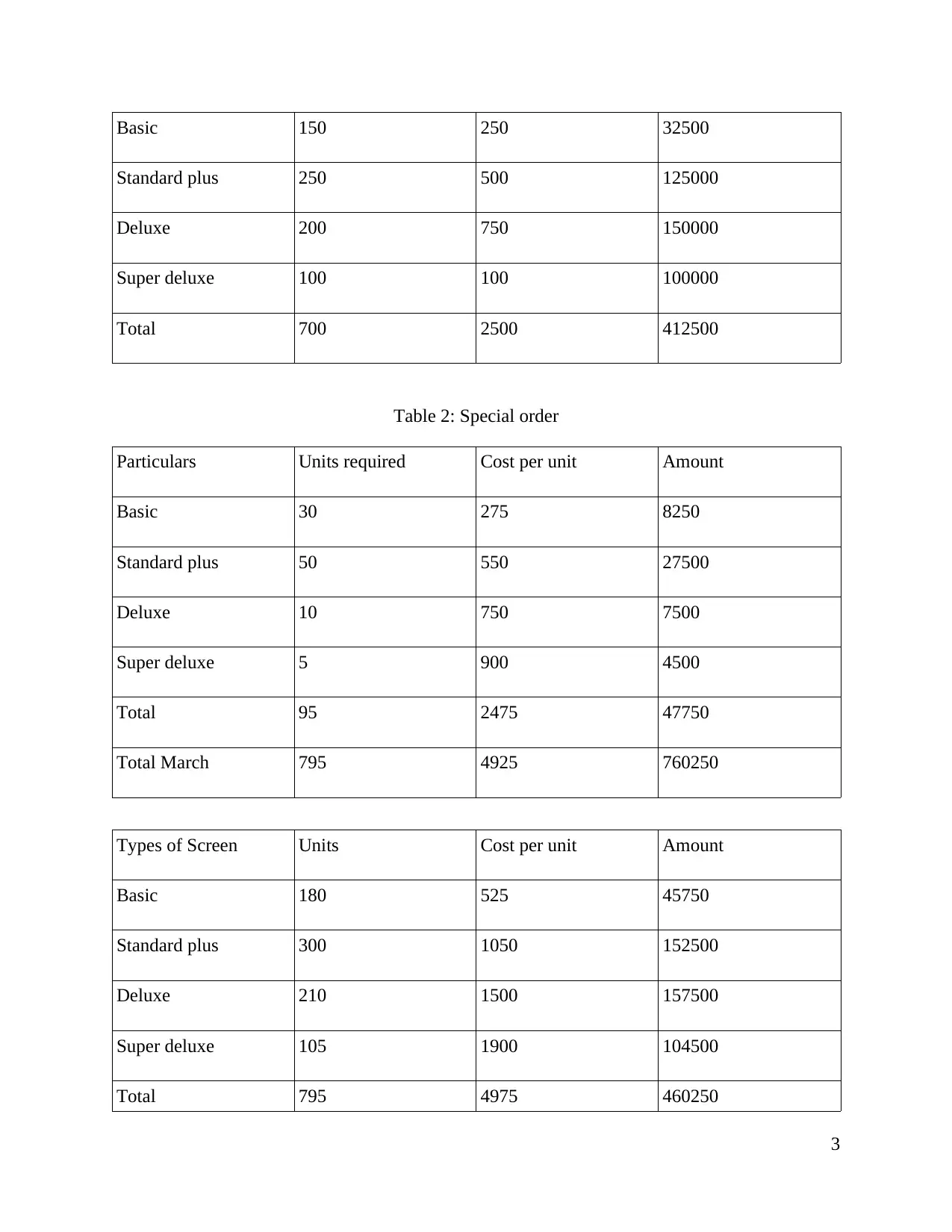

Labour hours required for Special order

Units Labour hr. per unit Total hrs.

180 2 360

300 3 900

210 4 840

105 5 525

Total hours required 2625 hours

Labour hours required in order to complete the special order of the clients for different

types of screen such as basic, standard plus, deluxe and super deluxe. These screens are provided

by an entity in order to facilitate all the external market clients as their desired am is to

accomplish all their orders by applying their skills and efforts (Bagliani and Martini, 2012).

Order will be completed by an entity in limited time as they emphasise on getting higher

customer satisfaction by meeting all their needs in less span of time. Labour hours required to

complete the special order is 2625 hours but the existing labour hours available is 2400 hours as

the extra hours will be compensated by treating the special order appropriately. Additional

requirement of the external market user by accomplishing the special order with the available

labour hours of 2400 hours instead of 2625 hours. The current process will get completed by

ranking method approach in which key factor method will be used in order to allocate the

existing labour hours among all kinds of screen type available in an entity. Contribution will be

generated that will be helpful for an entity in order to determine the actual allocation of all the

labour hours according to the current labour hours requirement of an entity whose major aim is

to achieve all the desired goals and the objectives of the business owner (Ball, 2013).

Calculation of Contribution

4

Units Labour hr. per unit Total hrs.

180 2 360

300 3 900

210 4 840

105 5 525

Total hours required 2625 hours

Labour hours required in order to complete the special order of the clients for different

types of screen such as basic, standard plus, deluxe and super deluxe. These screens are provided

by an entity in order to facilitate all the external market clients as their desired am is to

accomplish all their orders by applying their skills and efforts (Bagliani and Martini, 2012).

Order will be completed by an entity in limited time as they emphasise on getting higher

customer satisfaction by meeting all their needs in less span of time. Labour hours required to

complete the special order is 2625 hours but the existing labour hours available is 2400 hours as

the extra hours will be compensated by treating the special order appropriately. Additional

requirement of the external market user by accomplishing the special order with the available

labour hours of 2400 hours instead of 2625 hours. The current process will get completed by

ranking method approach in which key factor method will be used in order to allocate the

existing labour hours among all kinds of screen type available in an entity. Contribution will be

generated that will be helpful for an entity in order to determine the actual allocation of all the

labour hours according to the current labour hours requirement of an entity whose major aim is

to achieve all the desired goals and the objectives of the business owner (Ball, 2013).

Calculation of Contribution

4

Particulars Amount

Sale

Basic 37500

Standard plus 125000

Deluxe 150000

Super deluxe 100000

Total sales 412500

Less: Variable costs

Material cost 233500

Labour costs 600

Overhead costs 17600

Total variable costs 251700

Contribution 160800

Allocation of labour hours

Contribution 160800 160800 160800 160800

Key factor 2 3 4 5

Contribution/Key

factor

80400 53600 40200 32160

Ranking 1 2 3 4

5

Sale

Basic 37500

Standard plus 125000

Deluxe 150000

Super deluxe 100000

Total sales 412500

Less: Variable costs

Material cost 233500

Labour costs 600

Overhead costs 17600

Total variable costs 251700

Contribution 160800

Allocation of labour hours

Contribution 160800 160800 160800 160800

Key factor 2 3 4 5

Contribution/Key

factor

80400 53600 40200 32160

Ranking 1 2 3 4

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

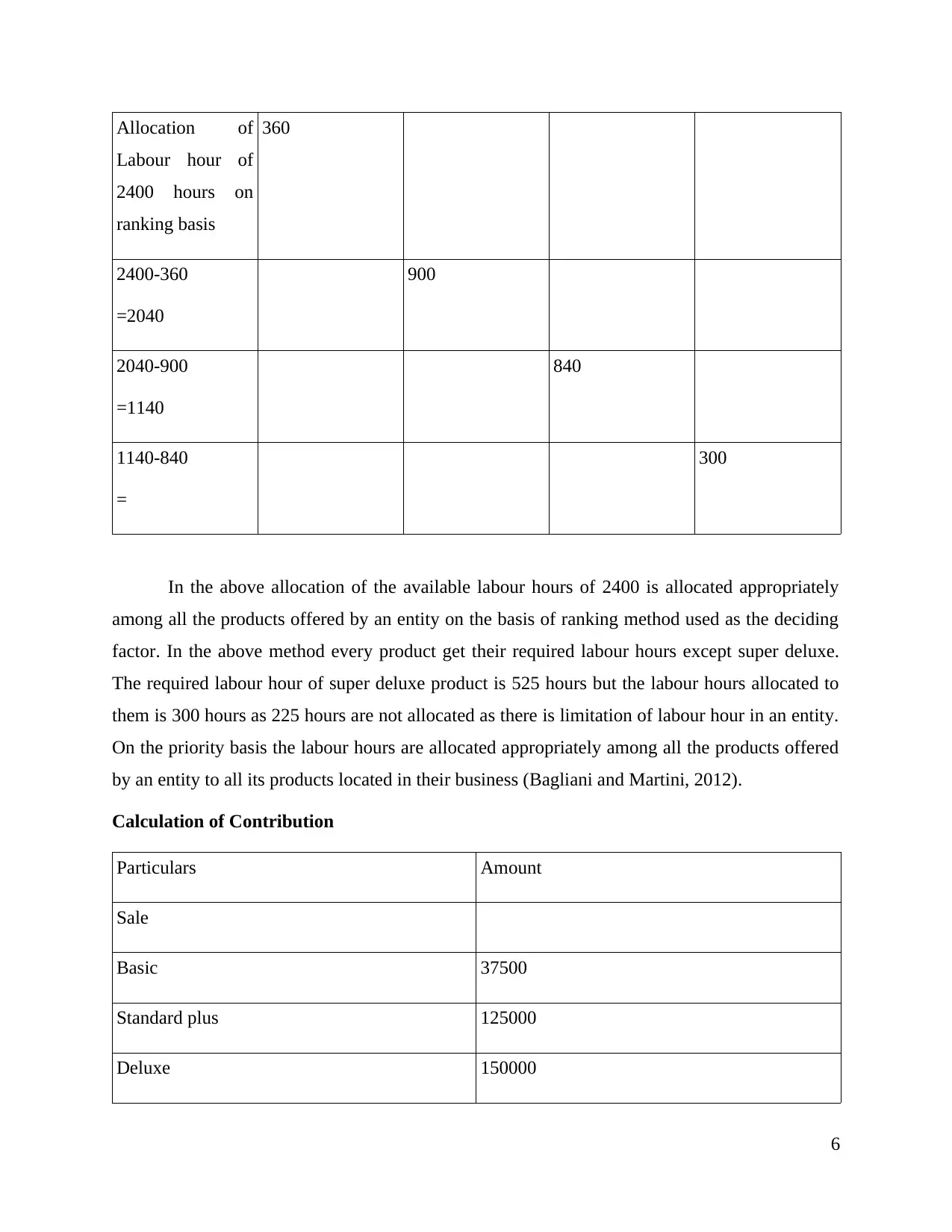

Allocation of

Labour hour of

2400 hours on

ranking basis

360

2400-360

=2040

900

2040-900

=1140

840

1140-840

=

300

In the above allocation of the available labour hours of 2400 is allocated appropriately

among all the products offered by an entity on the basis of ranking method used as the deciding

factor. In the above method every product get their required labour hours except super deluxe.

The required labour hour of super deluxe product is 525 hours but the labour hours allocated to

them is 300 hours as 225 hours are not allocated as there is limitation of labour hour in an entity.

On the priority basis the labour hours are allocated appropriately among all the products offered

by an entity to all its products located in their business (Bagliani and Martini, 2012).

Calculation of Contribution

Particulars Amount

Sale

Basic 37500

Standard plus 125000

Deluxe 150000

6

Labour hour of

2400 hours on

ranking basis

360

2400-360

=2040

900

2040-900

=1140

840

1140-840

=

300

In the above allocation of the available labour hours of 2400 is allocated appropriately

among all the products offered by an entity on the basis of ranking method used as the deciding

factor. In the above method every product get their required labour hours except super deluxe.

The required labour hour of super deluxe product is 525 hours but the labour hours allocated to

them is 300 hours as 225 hours are not allocated as there is limitation of labour hour in an entity.

On the priority basis the labour hours are allocated appropriately among all the products offered

by an entity to all its products located in their business (Bagliani and Martini, 2012).

Calculation of Contribution

Particulars Amount

Sale

Basic 37500

Standard plus 125000

Deluxe 150000

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Super deluxe 100000

Total sales 412500

Less: Variable costs

Material cost 233500

Labour costs 1050

Overhead costs 17600

Total variable costs 252150

Contribution 160350

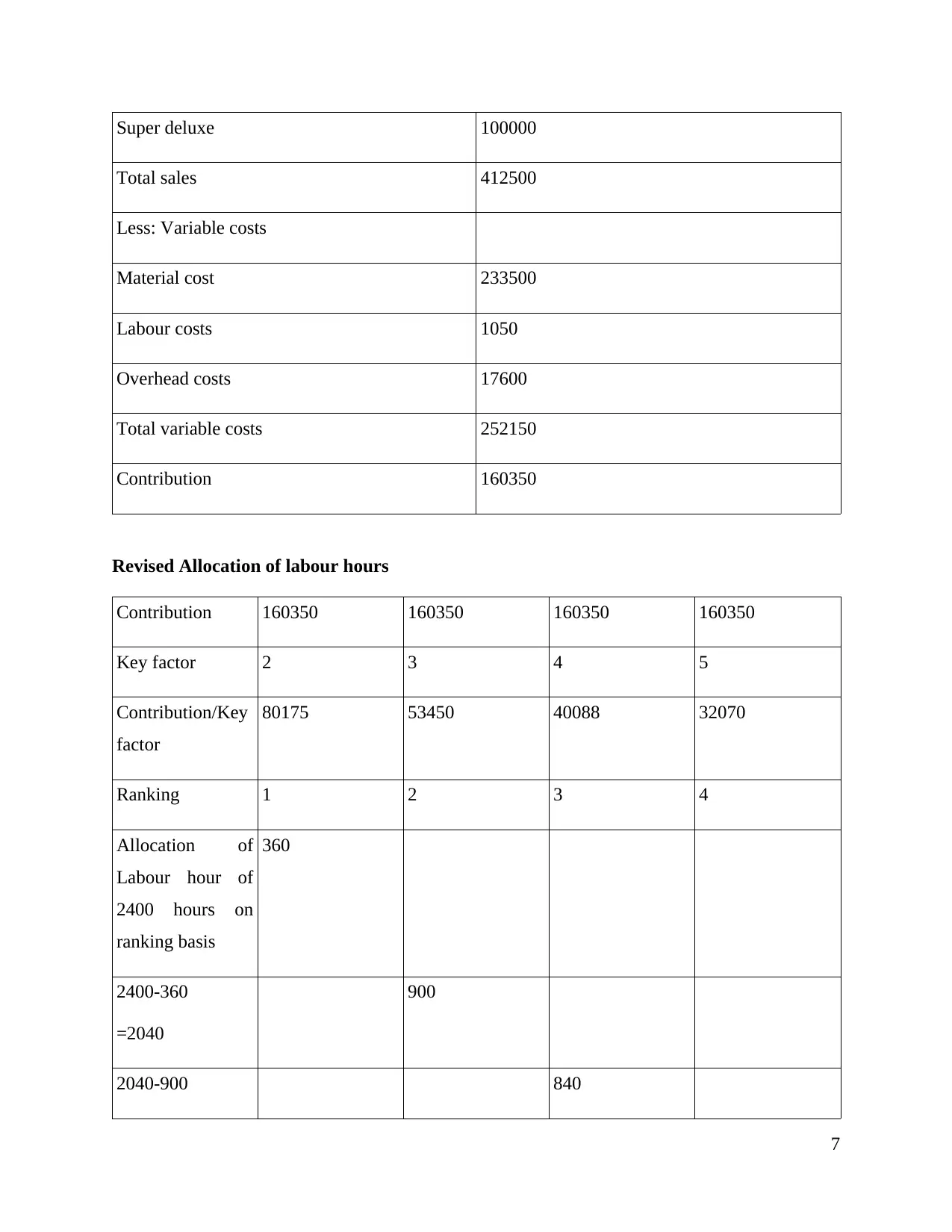

Revised Allocation of labour hours

Contribution 160350 160350 160350 160350

Key factor 2 3 4 5

Contribution/Key

factor

80175 53450 40088 32070

Ranking 1 2 3 4

Allocation of

Labour hour of

2400 hours on

ranking basis

360

2400-360

=2040

900

2040-900 840

7

Total sales 412500

Less: Variable costs

Material cost 233500

Labour costs 1050

Overhead costs 17600

Total variable costs 252150

Contribution 160350

Revised Allocation of labour hours

Contribution 160350 160350 160350 160350

Key factor 2 3 4 5

Contribution/Key

factor

80175 53450 40088 32070

Ranking 1 2 3 4

Allocation of

Labour hour of

2400 hours on

ranking basis

360

2400-360

=2040

900

2040-900 840

7

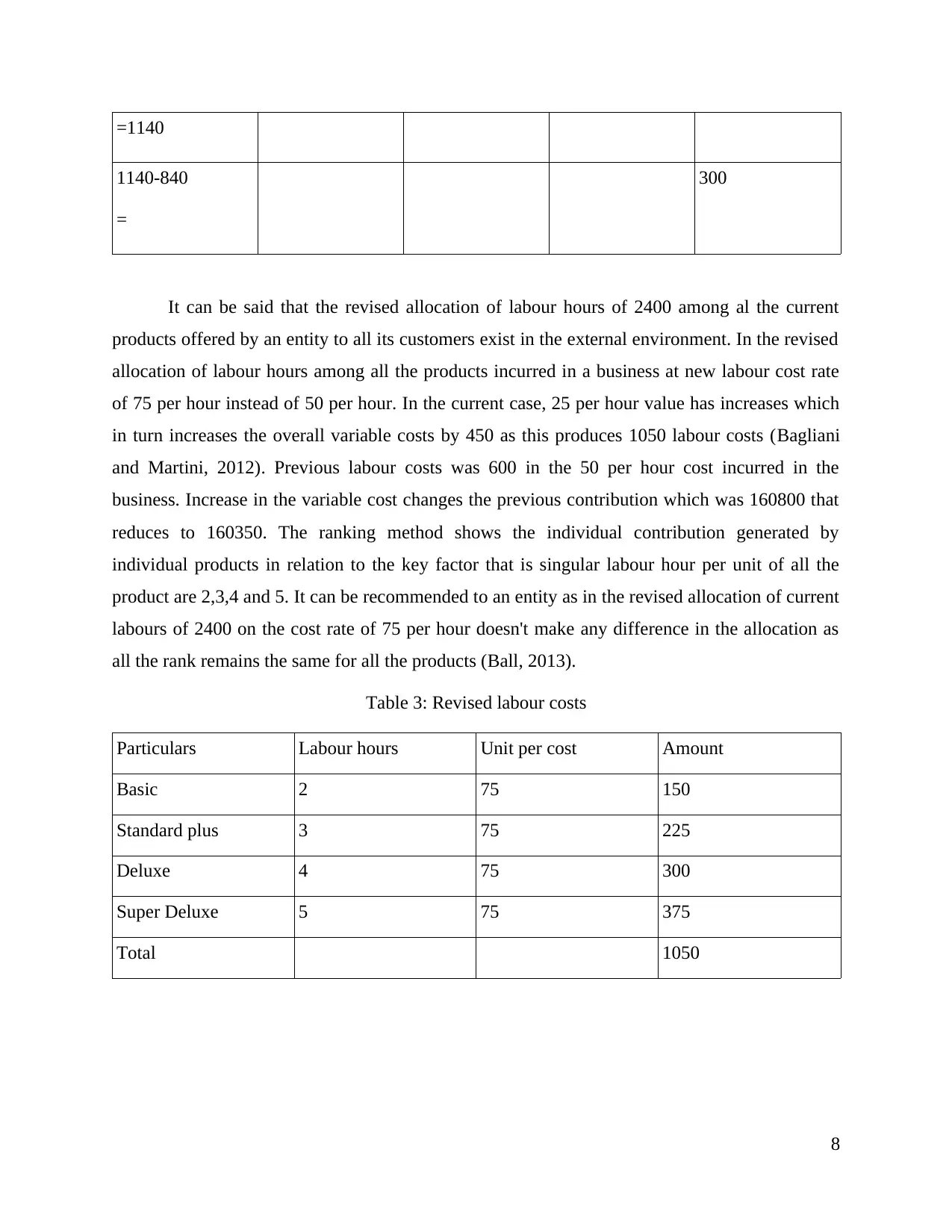

=1140

1140-840

=

300

It can be said that the revised allocation of labour hours of 2400 among al the current

products offered by an entity to all its customers exist in the external environment. In the revised

allocation of labour hours among all the products incurred in a business at new labour cost rate

of 75 per hour instead of 50 per hour. In the current case, 25 per hour value has increases which

in turn increases the overall variable costs by 450 as this produces 1050 labour costs (Bagliani

and Martini, 2012). Previous labour costs was 600 in the 50 per hour cost incurred in the

business. Increase in the variable cost changes the previous contribution which was 160800 that

reduces to 160350. The ranking method shows the individual contribution generated by

individual products in relation to the key factor that is singular labour hour per unit of all the

product are 2,3,4 and 5. It can be recommended to an entity as in the revised allocation of current

labours of 2400 on the cost rate of 75 per hour doesn't make any difference in the allocation as

all the rank remains the same for all the products (Ball, 2013).

Table 3: Revised labour costs

Particulars Labour hours Unit per cost Amount

Basic 2 75 150

Standard plus 3 75 225

Deluxe 4 75 300

Super Deluxe 5 75 375

Total 1050

8

1140-840

=

300

It can be said that the revised allocation of labour hours of 2400 among al the current

products offered by an entity to all its customers exist in the external environment. In the revised

allocation of labour hours among all the products incurred in a business at new labour cost rate

of 75 per hour instead of 50 per hour. In the current case, 25 per hour value has increases which

in turn increases the overall variable costs by 450 as this produces 1050 labour costs (Bagliani

and Martini, 2012). Previous labour costs was 600 in the 50 per hour cost incurred in the

business. Increase in the variable cost changes the previous contribution which was 160800 that

reduces to 160350. The ranking method shows the individual contribution generated by

individual products in relation to the key factor that is singular labour hour per unit of all the

product are 2,3,4 and 5. It can be recommended to an entity as in the revised allocation of current

labours of 2400 on the cost rate of 75 per hour doesn't make any difference in the allocation as

all the rank remains the same for all the products (Ball, 2013).

Table 3: Revised labour costs

Particulars Labour hours Unit per cost Amount

Basic 2 75 150

Standard plus 3 75 225

Deluxe 4 75 300

Super Deluxe 5 75 375

Total 1050

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.