ANSWER ASIAN LIMITED: Comprehensive Financial Budgeting Project

VerifiedAdded on 2020/05/28

|6

|1151

|314

Project

AI Summary

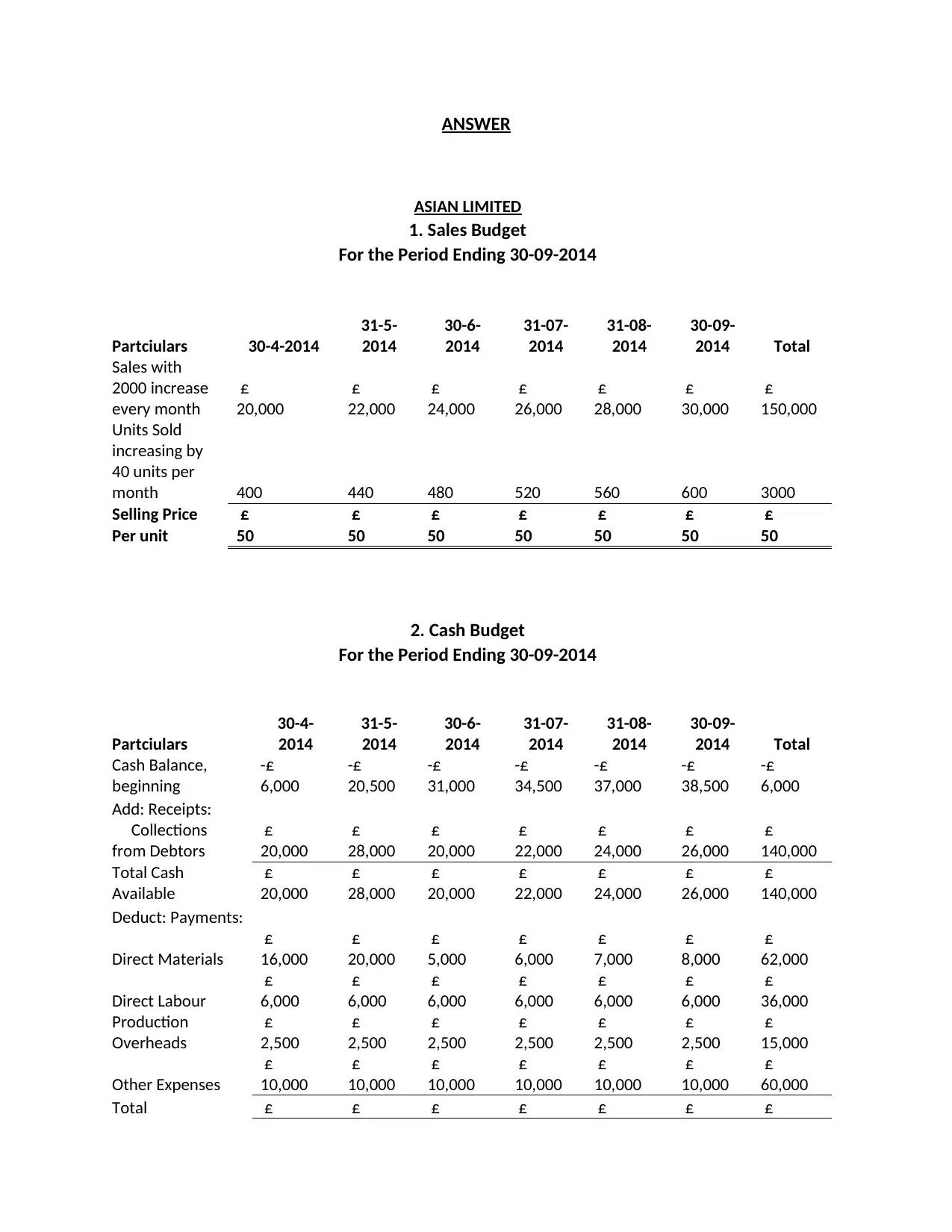

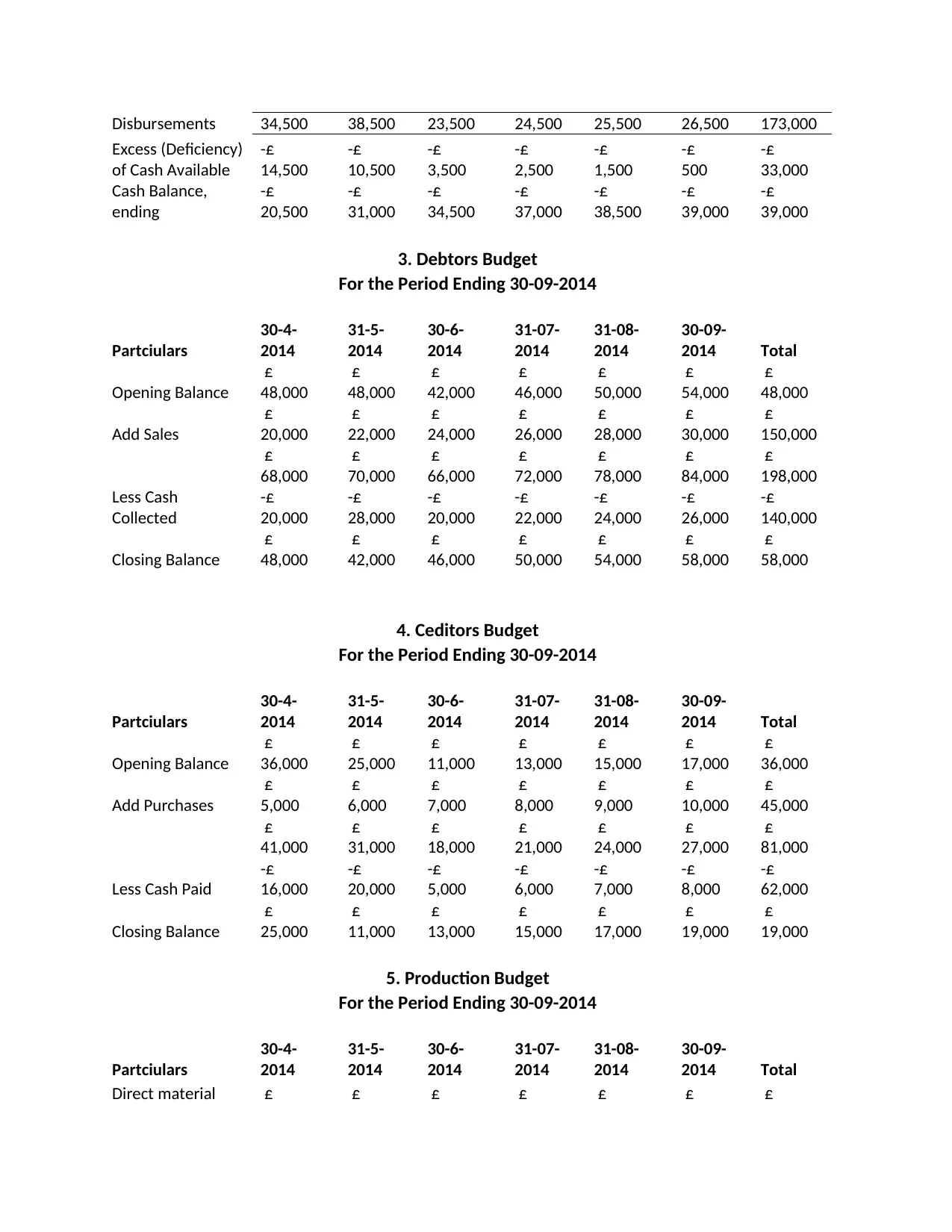

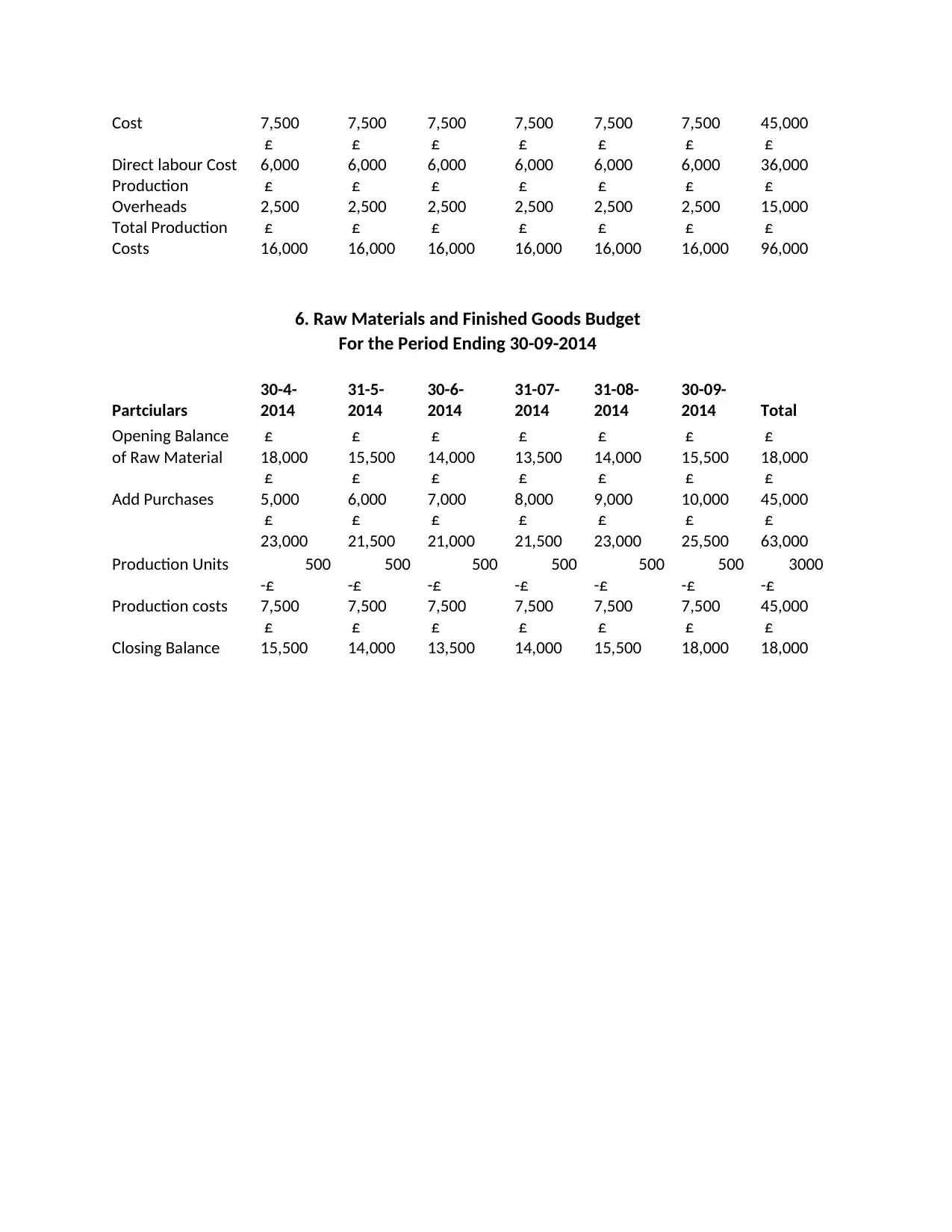

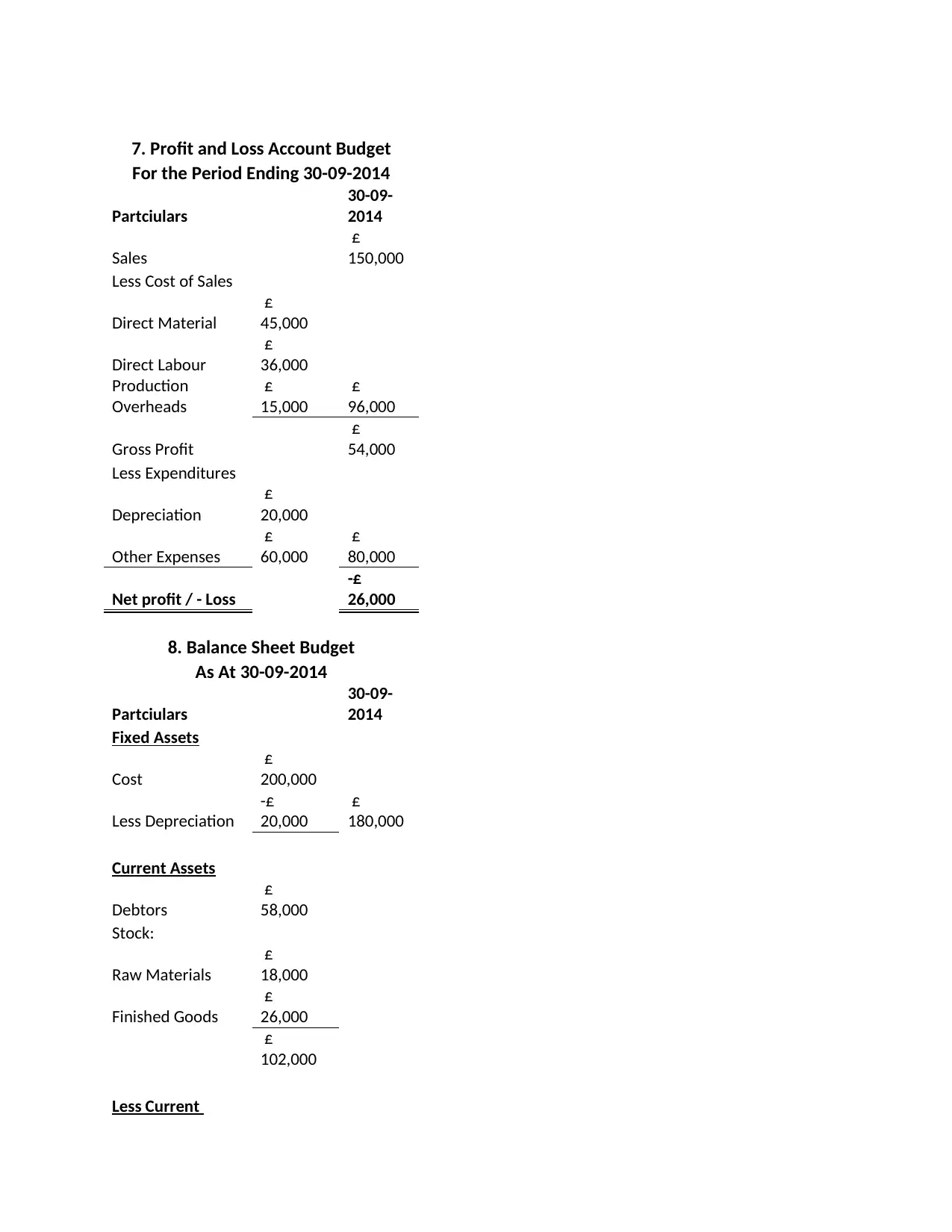

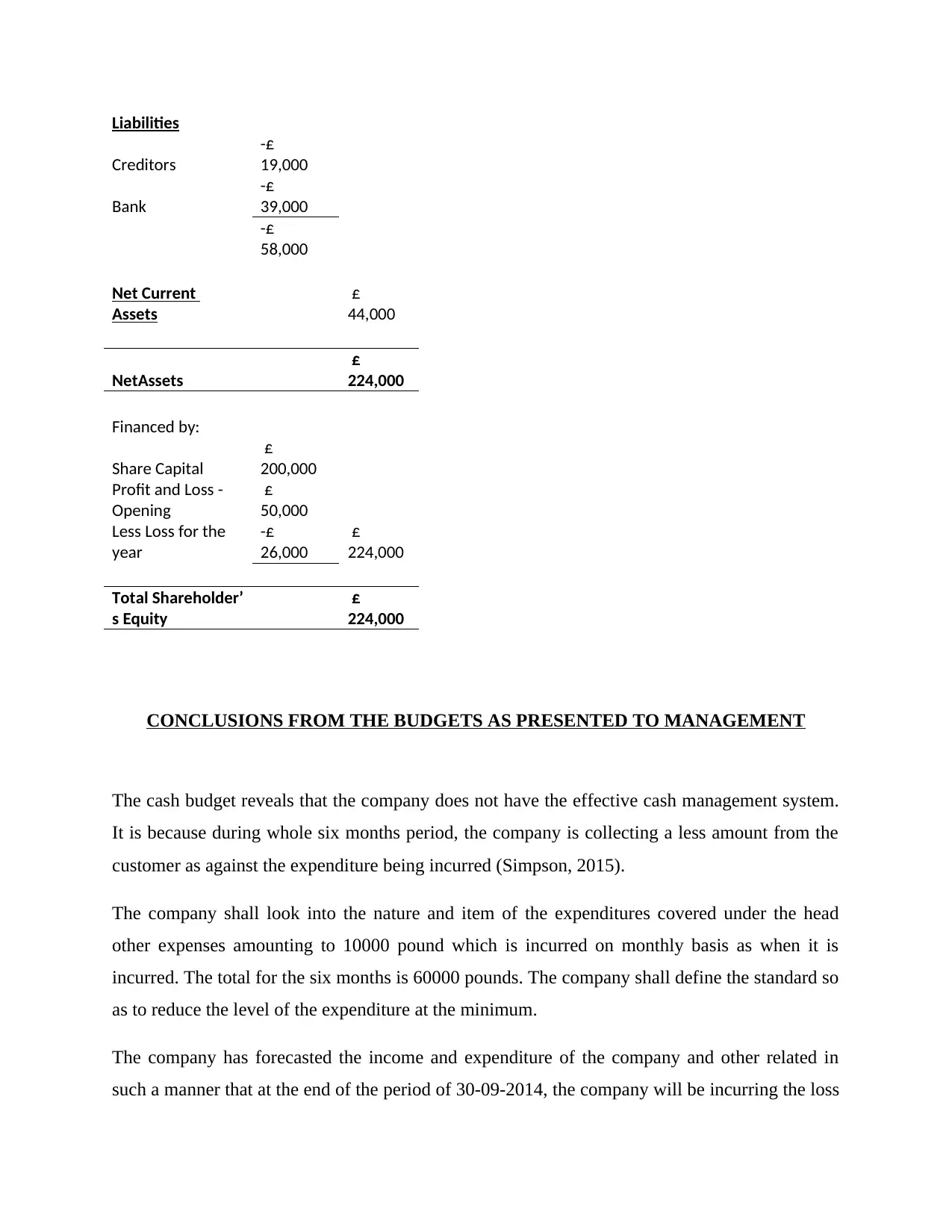

This project analyzes the financial budgets of ANSWER ASIAN LIMITED for the period ending September 30, 2014. It includes a sales budget with increasing sales and units sold, a cash budget detailing cash inflows and outflows, a debtors budget tracking outstanding receivables, and a creditors budget outlining payables. A production budget, raw materials, and finished goods budget are also presented. Furthermore, a profit and loss account budget projects revenues and expenses, leading to a net loss, and a balance sheet budget provides a snapshot of the company's assets, liabilities, and equity at the end of the period. The analysis concludes that the company faces cash management issues, anticipates a loss, and needs to improve its budgetary assumptions to maintain its financial health. References to relevant literature are included to support the analysis.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.