Financial Accounting Analysis of Business Investment Decisions

VerifiedAdded on 2020/04/01

|9

|1895

|80

Homework Assignment

AI Summary

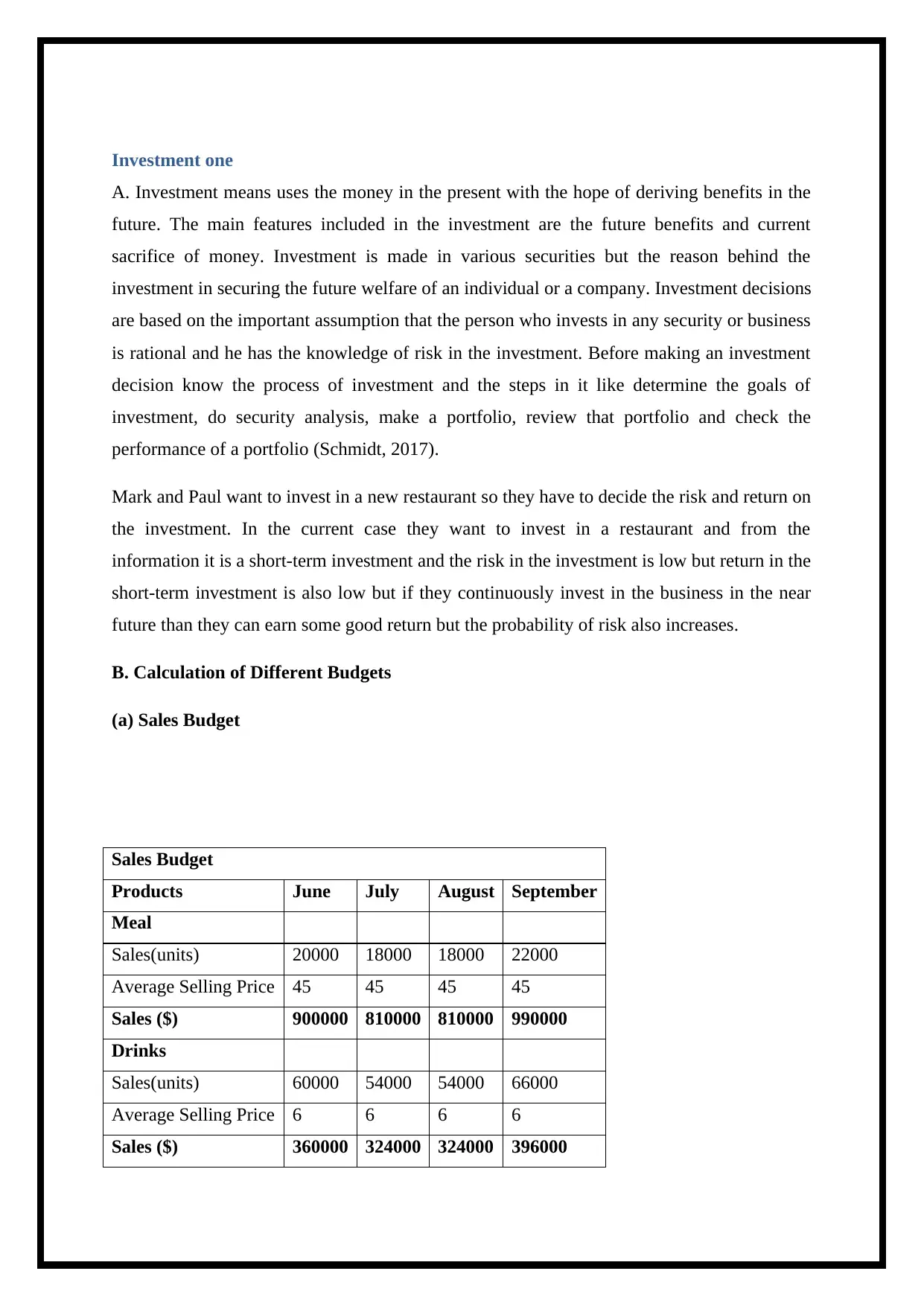

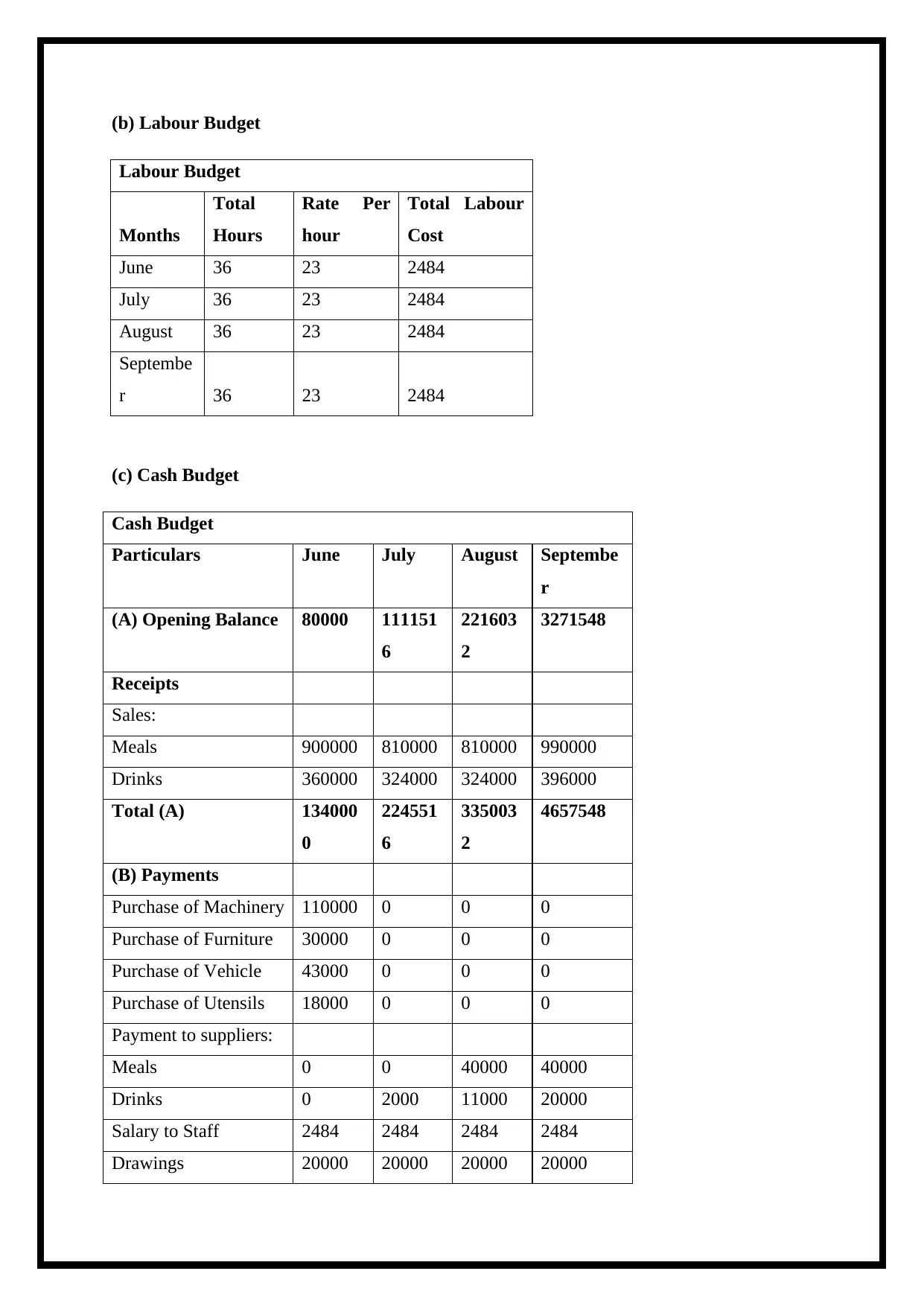

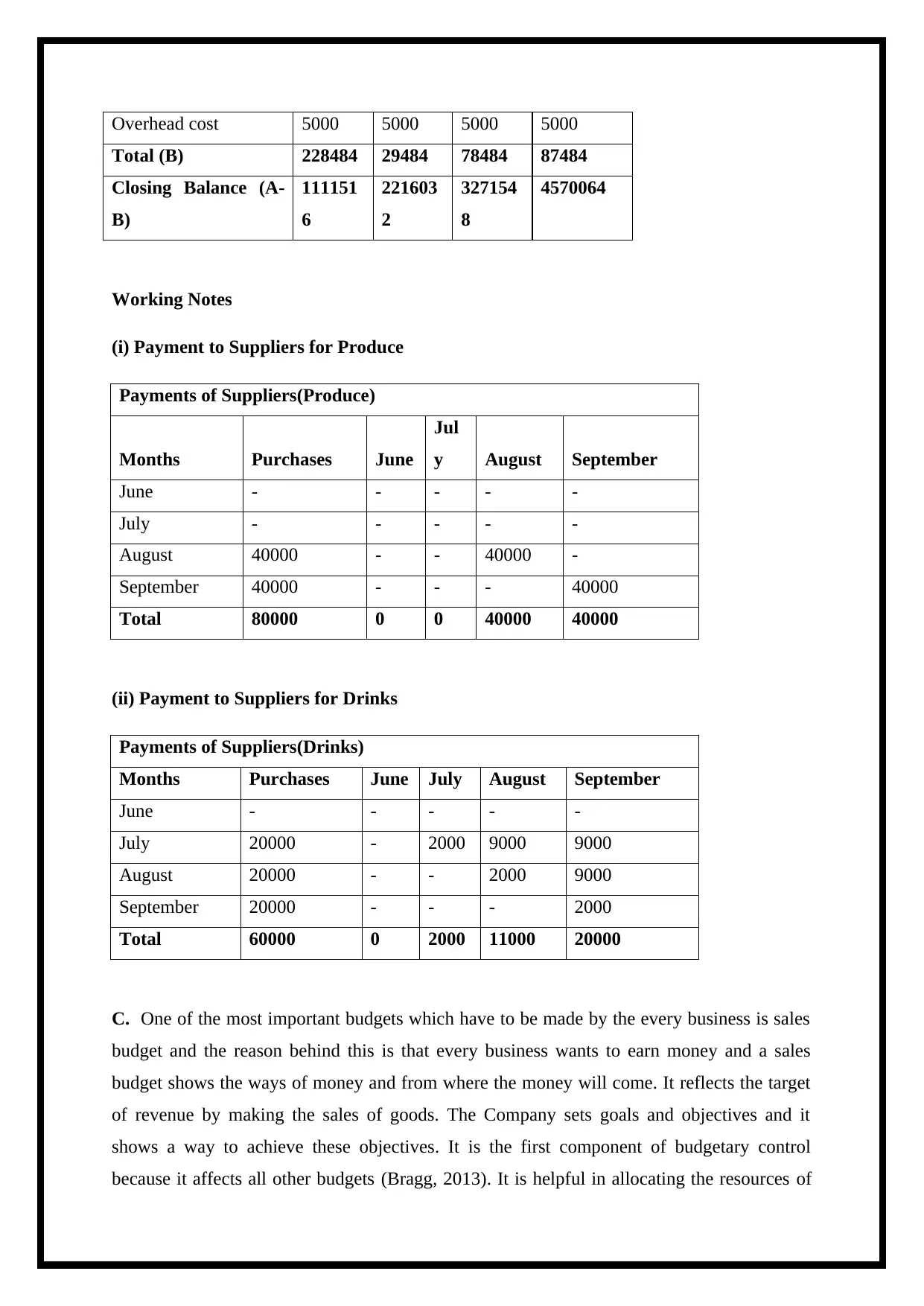

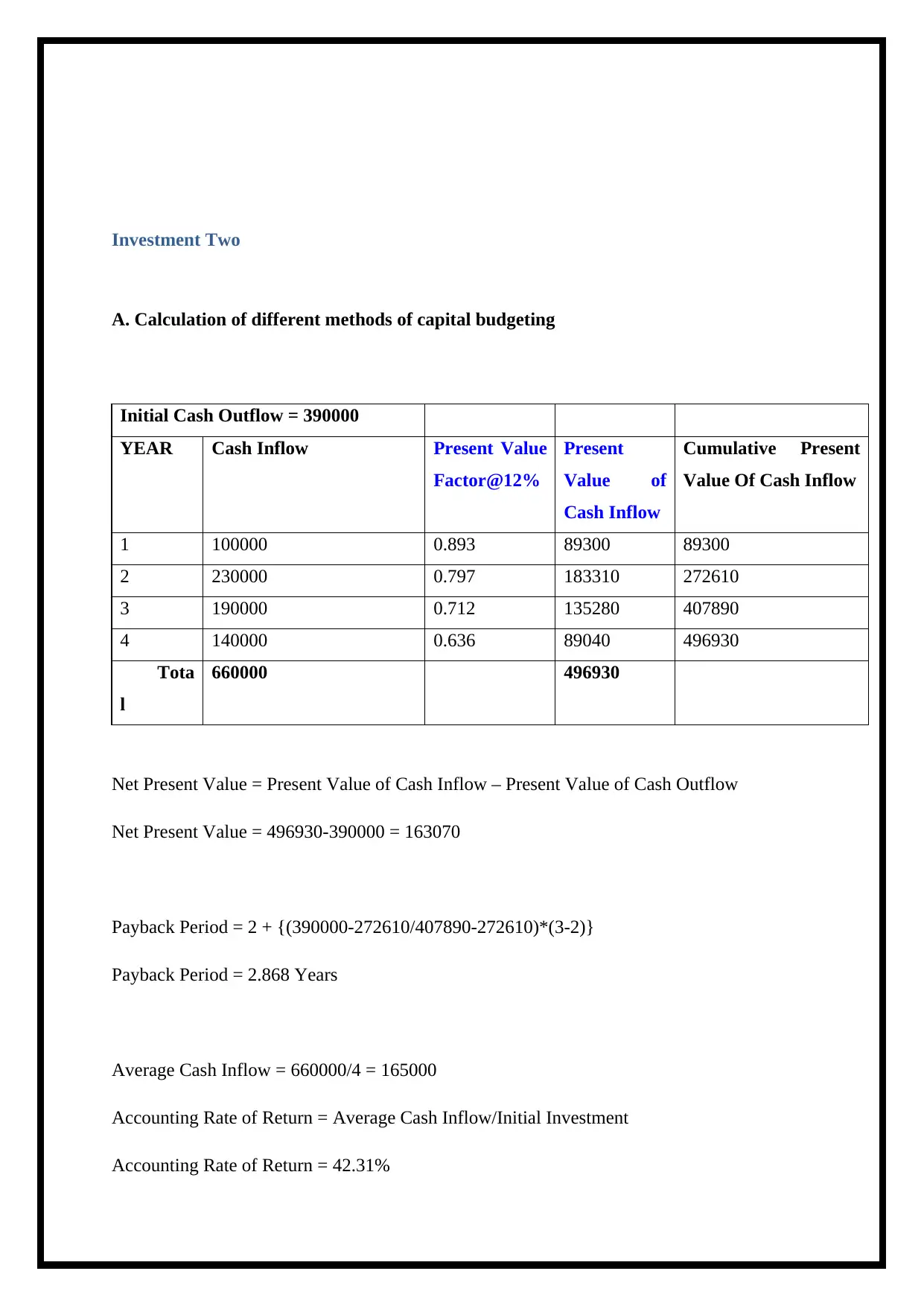

This assignment provides a detailed accounting analysis of business investments, focusing on the decision-making process for Mark and Paul who are considering investing in a restaurant. The solution includes the calculation and analysis of various budgets, such as sales, labour, and cash budgets, to assess the financial viability of the investment. The assignment also covers key financial metrics like Net Present Value (NPV), payback period, and accounting rate of return (ARR) to evaluate different investment opportunities. Furthermore, the document explores the significance of sales budgets in revenue forecasting, the role of labour budgets in determining labour costs, and the importance of cash budgets in managing cash flow. It also discusses the limitations of these budgeting methods and the importance of considering risk and return. Finally, it provides a comparative analysis of two investment opportunities and discusses factors influencing investment decisions, such as risk assessment and the time value of money, which are crucial for making informed financial choices.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.