Financial Calculations: Analysis of Time Value of Money and Loans

VerifiedAdded on 2022/11/29

|11

|1637

|231

Homework Assignment

AI Summary

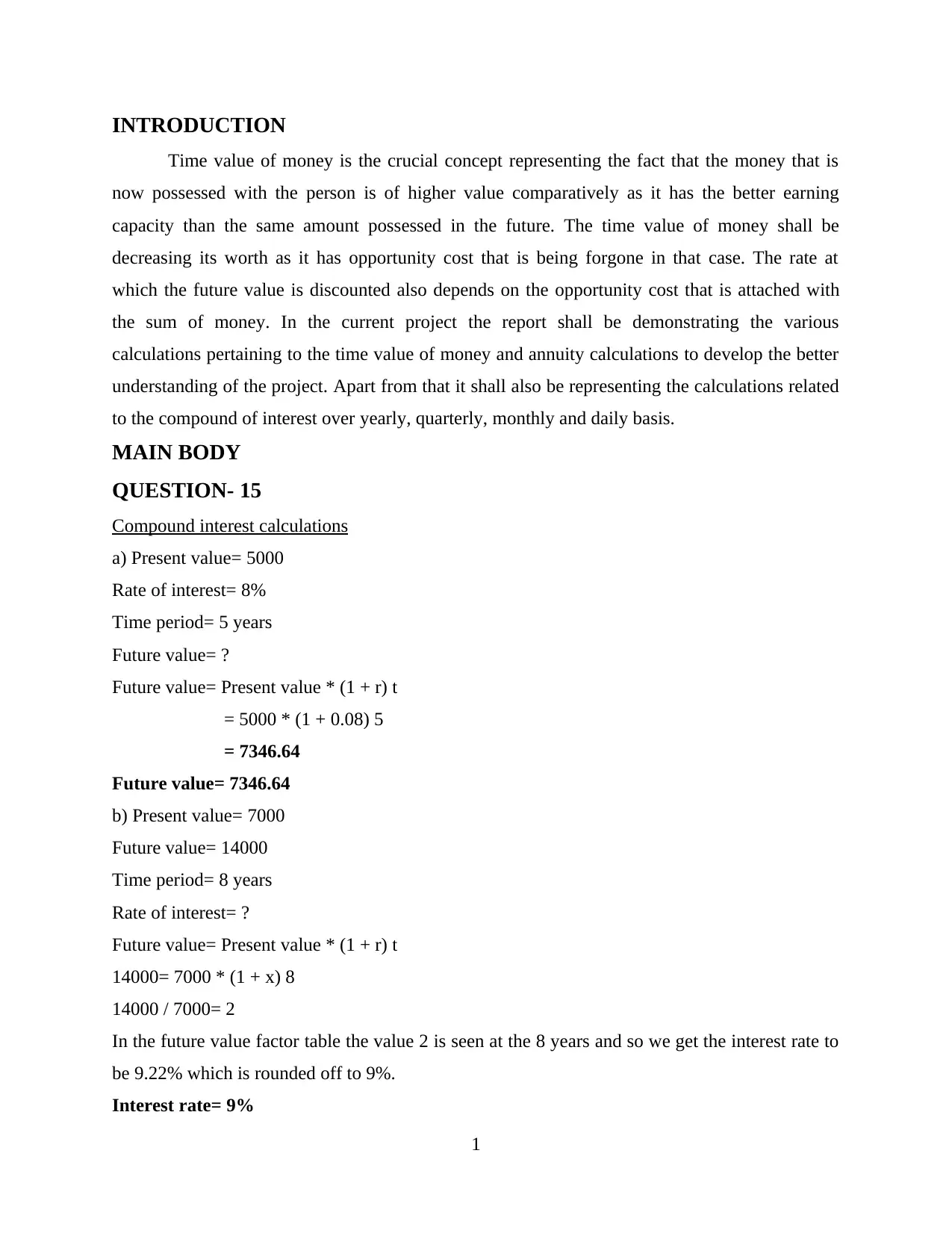

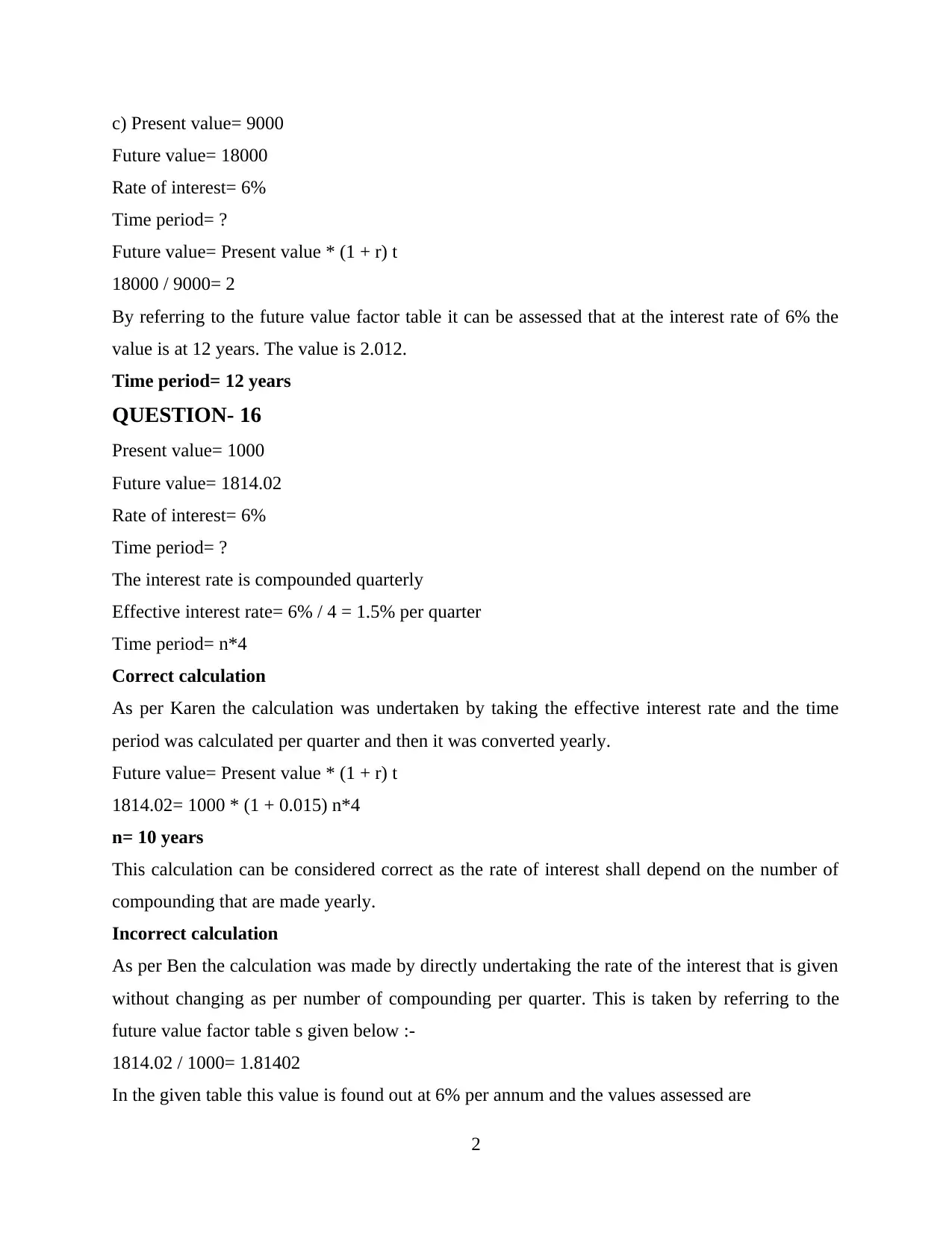

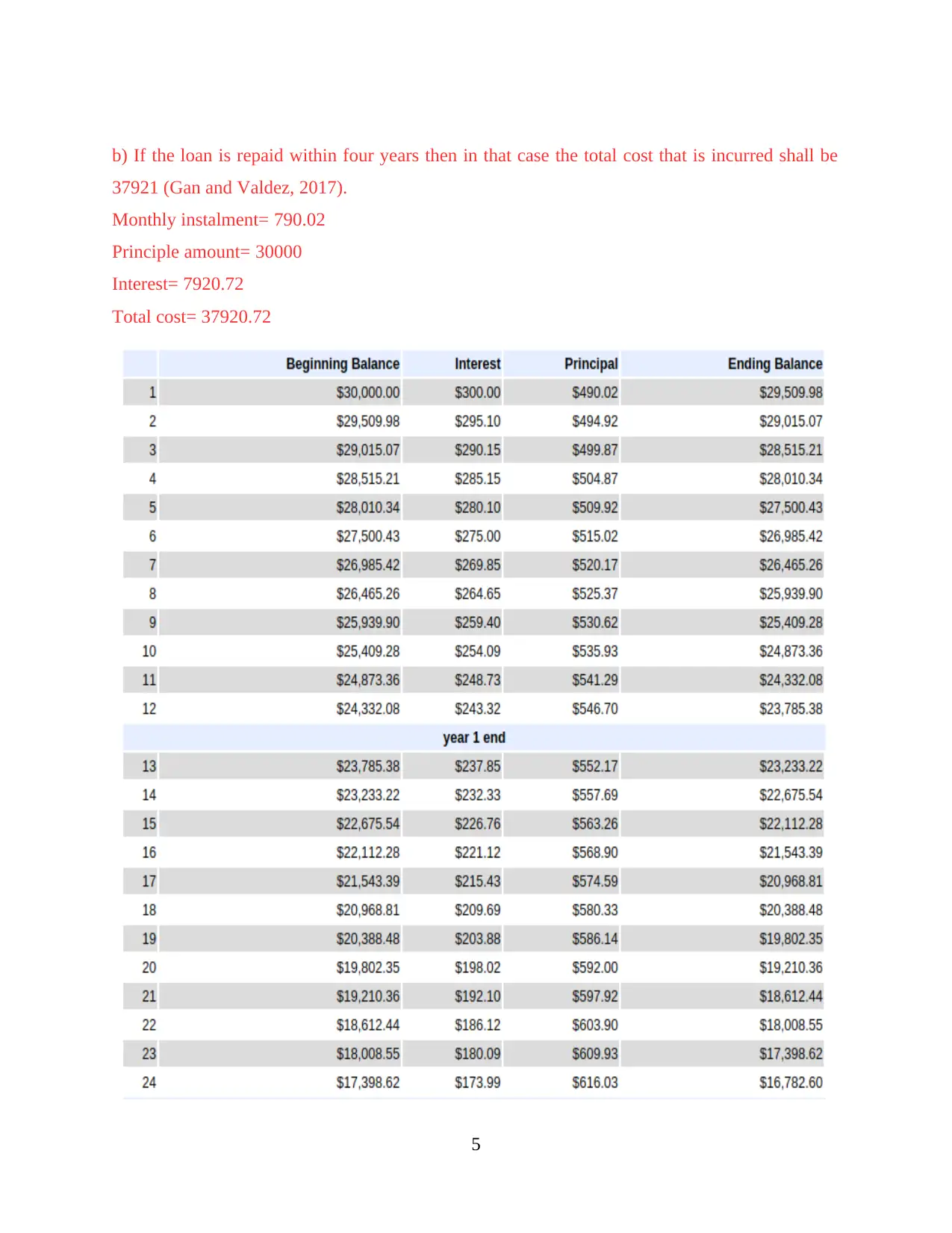

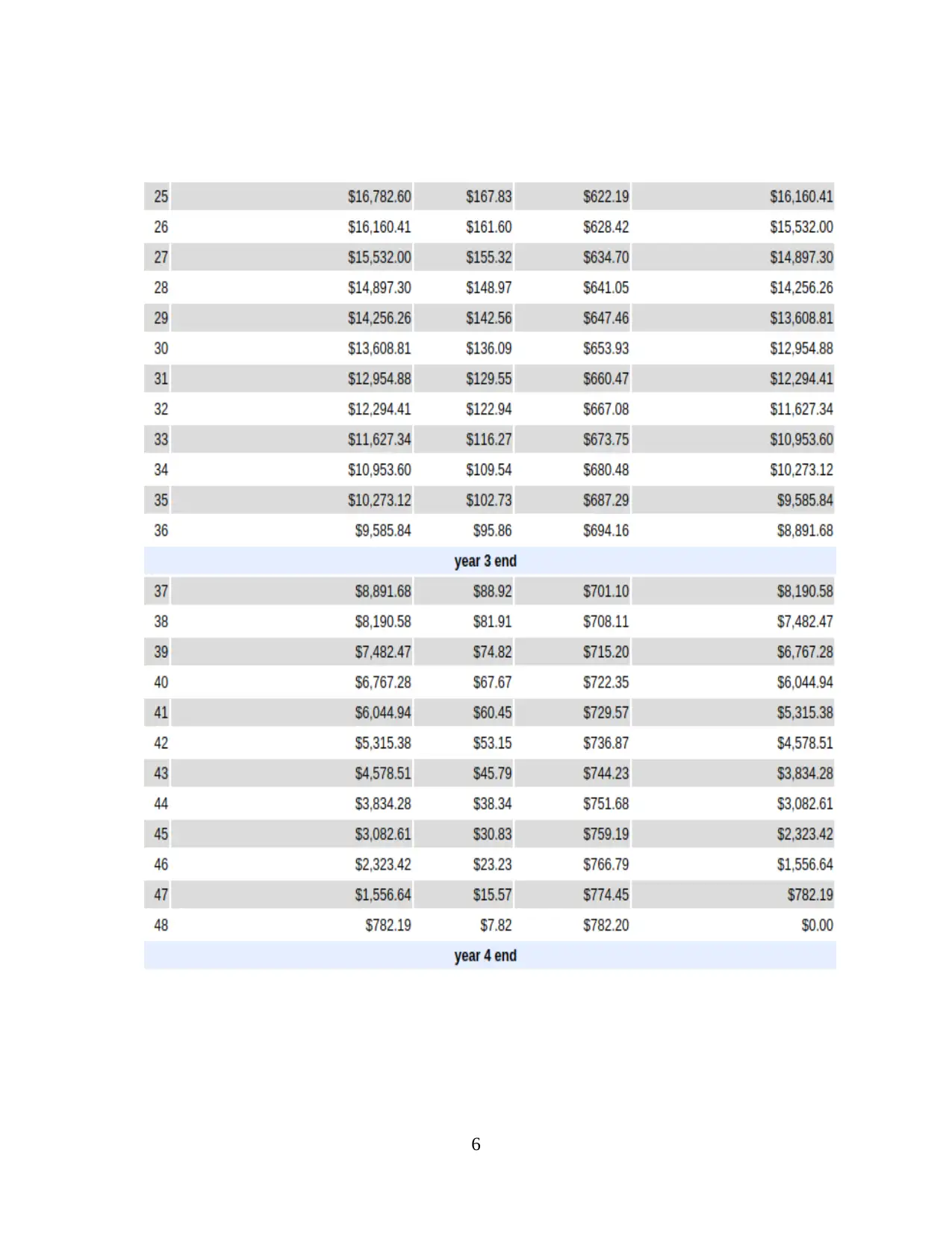

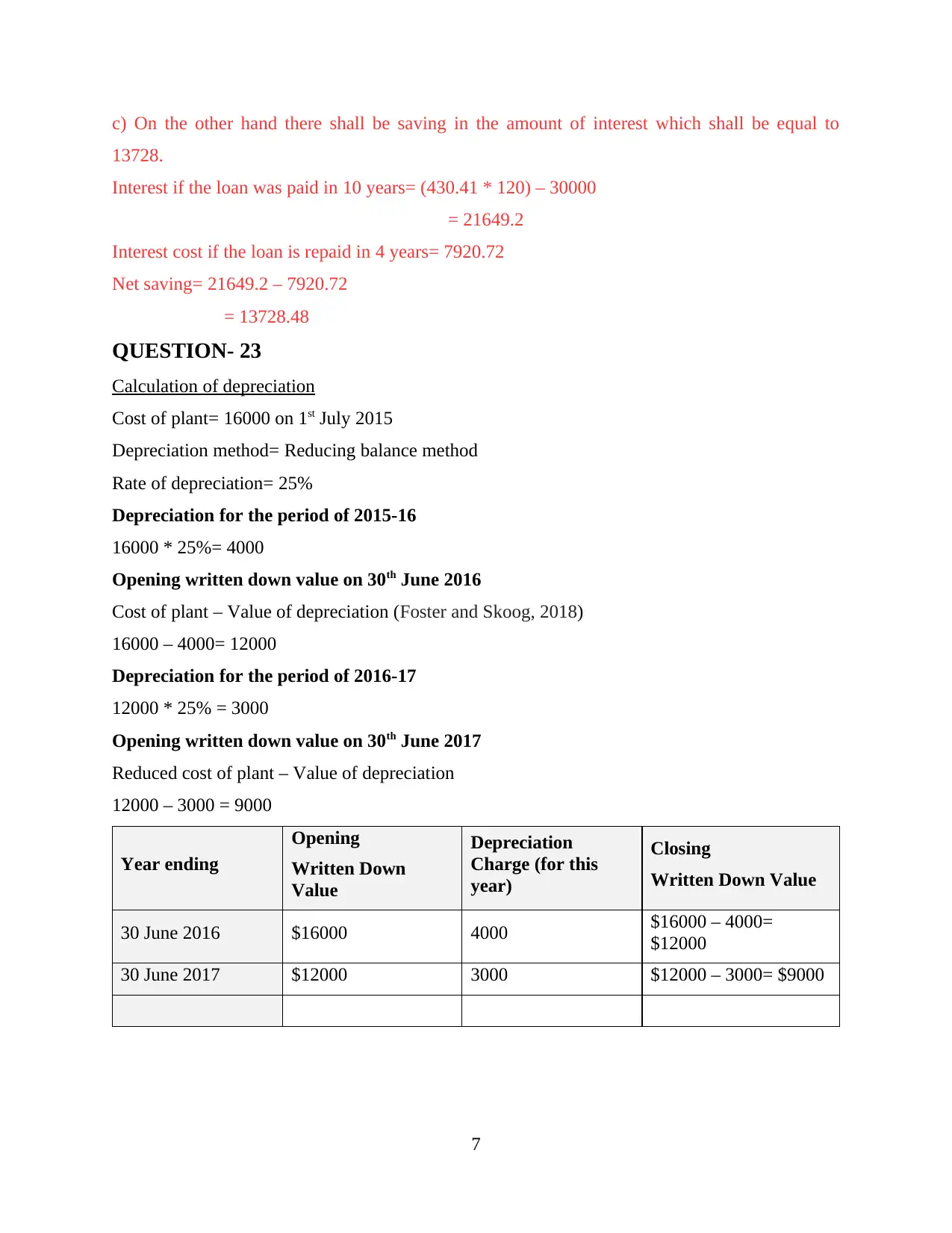

This assignment delves into various financial calculations, including the time value of money, compound interest, and depreciation. The introduction explains the core concept of time value of money and its impact on investment decisions. The main body of the assignment provides detailed solutions to several questions. Question 15 involves compound interest calculations, determining future values, interest rates, and time periods. Question 16 analyzes a disagreement between two individuals on the time required for an investment to grow, highlighting the importance of correct compounding frequency. Question 17 covers interest rate calculations, EMI calculations, and annuity calculations. Question 21 focuses on loan calculations, including EMI and total cost analysis under different repayment scenarios. Finally, question 23 demonstrates depreciation calculations using the reducing balance method. The conclusion summarizes the significance of the time value of money in evaluating investment opportunities and the impact of interest rates and compounding periods. The document references various books and journals to support its analysis.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.