IFRS, Financial Capital, AASB 9: Financial Instrument Analysis Report

VerifiedAdded on 2019/10/30

|9

|1596

|165

Report

AI Summary

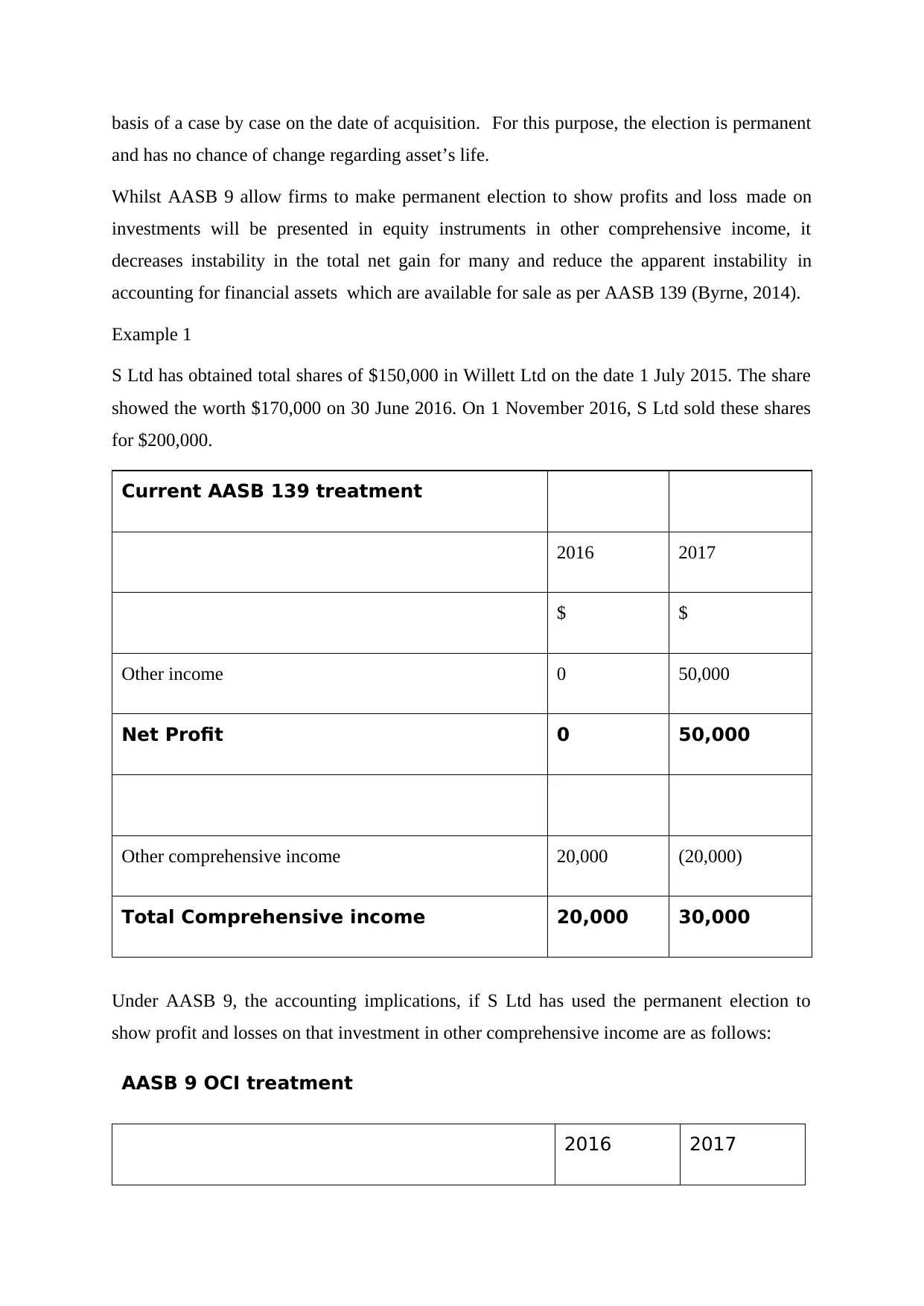

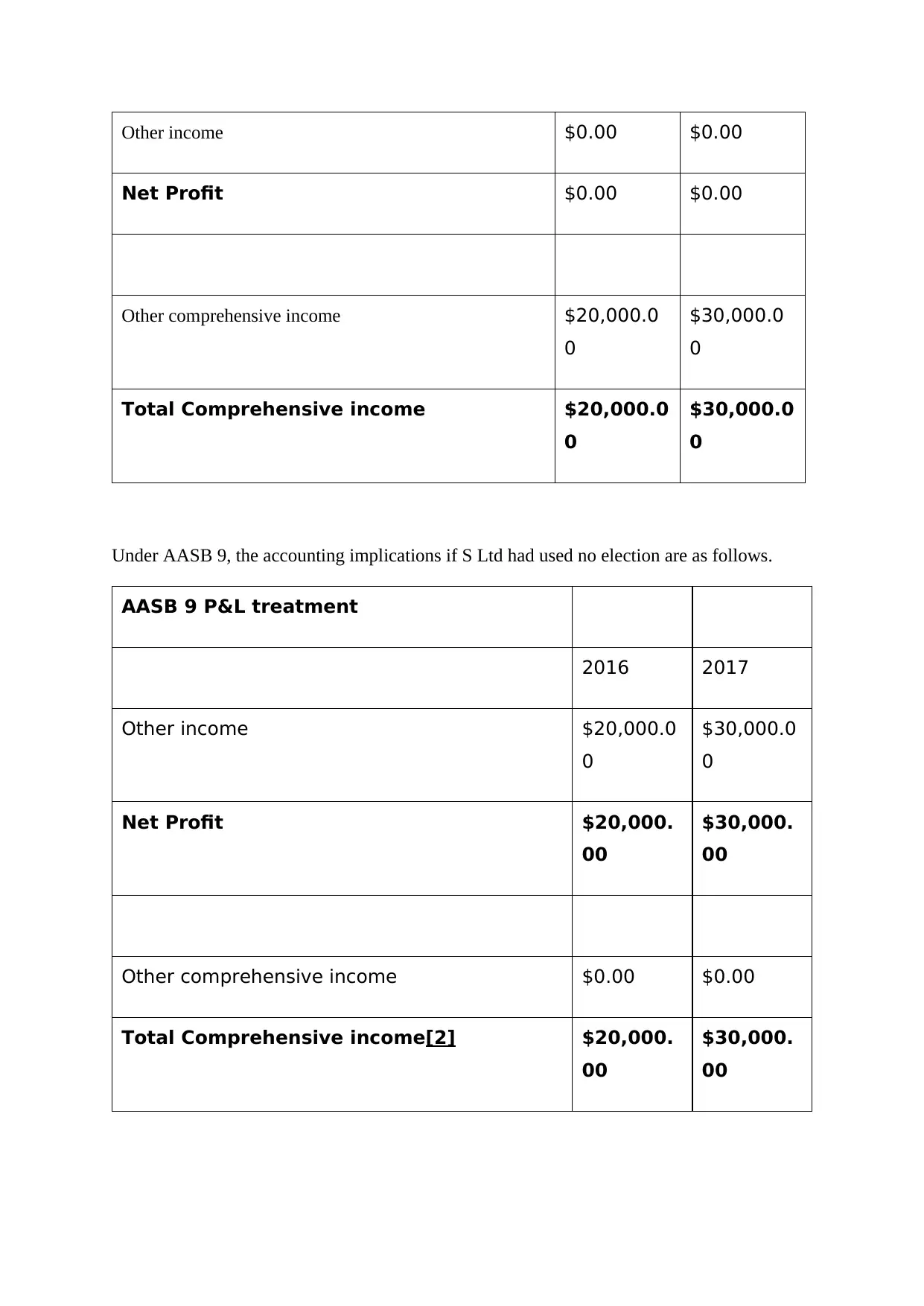

This report provides a detailed overview of financial capital maintenance and physical capital maintenance under the IFRS framework. It differentiates between the financial concept of capital, related to net assets and equity, and the physical concept, based on an entity's production capacity. The report then focuses on AASB 9, the new and revised standard for financial instruments, exploring its implications on classification, measurement, and recognition of financial assets and liabilities. It highlights the changes from AASB 139, including the categorization of financial assets into amortized cost and fair value, along with the flexibility in applying hedge accounting. The report includes an example illustrating the accounting implications of AASB 9, comparing the treatment under both current and the new standards. References from various academic sources are provided to support the analysis.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.