Capital Structure and Payout Policies of Masters Ltd: Case Study

VerifiedAdded on 2020/07/22

|10

|2745

|56

Case Study

AI Summary

This case study examines the financial aspects of Masters Ltd, focusing on capital structure and payout policies. It delves into various capital structure theories like net income approach, net operating income approach, traditional approach, and Modigliani and Miller approach, discussing their implications and practical considerations. The analysis includes a hypothetical financial analysis of a proposed project, evaluating revenue, expenses, and net profits over five years. The study further explores investment appraisal techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), Payback Period, Discounted Payback Period, and Profitability Index to assess the project's viability and make informed financial decisions. The case study provides a comprehensive overview of financial planning and analysis within the context of Masters Ltd.

Finance Case Study 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Capital structure and pay-out policies ..................................................................................1

1.2 Evaluating policy and practical considerations.....................................................................4

TASK 2............................................................................................................................................5

Financial analysis .......................................................................................................................5

Valuable recommendation..........................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Capital structure and pay-out policies ..................................................................................1

1.2 Evaluating policy and practical considerations.....................................................................4

TASK 2............................................................................................................................................5

Financial analysis .......................................................................................................................5

Valuable recommendation..........................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................9

INTRODUCTION

Finance is an utmost important part for every business organization. In order to make a

critical analysis, a decent amount of capital is required. This will assist in the attainment of short

and long term aim and objectives. This project reports summaries two vital tasks which describe

capital structure and pay-out policies analysis of “Masters limited”. Overall financial analysis is

being done to determine the accurate growth and financial stability of an organization (Brealey

and et. al., 2012).

TASK 1

1.1 Capital structure and pay-out policies

In every business organization, it is important to have sufficient amount of capital to

manage and operate their everyday operations in the best suitable manner. Capital structure of

Master Ltd refers to the composition of their total capitalization that consists of every long term

capital sources. This can be measured through using various ratios of permanent loan and equity

capital to total funds available with company. It is used to show relationships among Masters Ltd

total debt obligation, preferences and equity portion in the balance sheet.

Capital structure policy and financial planning often include trade-offs among total risk

and returns. The use of debts outcomes in financial leverage is to find out magnifying impacts

on returns to the Masters owners in order to measure earnings per share (EPS) and return on

equity (ROE) (Embrechts, Klüppelberg and Mikosch, 2013). Some crucial theories of capital

structure are mentioned as below:

Net incomes approach:

This method suggests that total value of firms can be maximized by reducing the overall

cost of capital (WCC) through higher liability proportion. This can be done through having

maximum debt proportion which is an economical source of finance as compared to equity.

Certain assumption to this theory are:

With the increase in debts will not affect the perception of investors.

Cost of debt must be less than the cost of equity.

There is no tax levied.

WACC: RR*cost of equity+ RR*cost of debt

Total cost of capital = Debt + Equity

1

Finance is an utmost important part for every business organization. In order to make a

critical analysis, a decent amount of capital is required. This will assist in the attainment of short

and long term aim and objectives. This project reports summaries two vital tasks which describe

capital structure and pay-out policies analysis of “Masters limited”. Overall financial analysis is

being done to determine the accurate growth and financial stability of an organization (Brealey

and et. al., 2012).

TASK 1

1.1 Capital structure and pay-out policies

In every business organization, it is important to have sufficient amount of capital to

manage and operate their everyday operations in the best suitable manner. Capital structure of

Master Ltd refers to the composition of their total capitalization that consists of every long term

capital sources. This can be measured through using various ratios of permanent loan and equity

capital to total funds available with company. It is used to show relationships among Masters Ltd

total debt obligation, preferences and equity portion in the balance sheet.

Capital structure policy and financial planning often include trade-offs among total risk

and returns. The use of debts outcomes in financial leverage is to find out magnifying impacts

on returns to the Masters owners in order to measure earnings per share (EPS) and return on

equity (ROE) (Embrechts, Klüppelberg and Mikosch, 2013). Some crucial theories of capital

structure are mentioned as below:

Net incomes approach:

This method suggests that total value of firms can be maximized by reducing the overall

cost of capital (WCC) through higher liability proportion. This can be done through having

maximum debt proportion which is an economical source of finance as compared to equity.

Certain assumption to this theory are:

With the increase in debts will not affect the perception of investors.

Cost of debt must be less than the cost of equity.

There is no tax levied.

WACC: RR*cost of equity+ RR*cost of debt

Total cost of capital = Debt + Equity

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

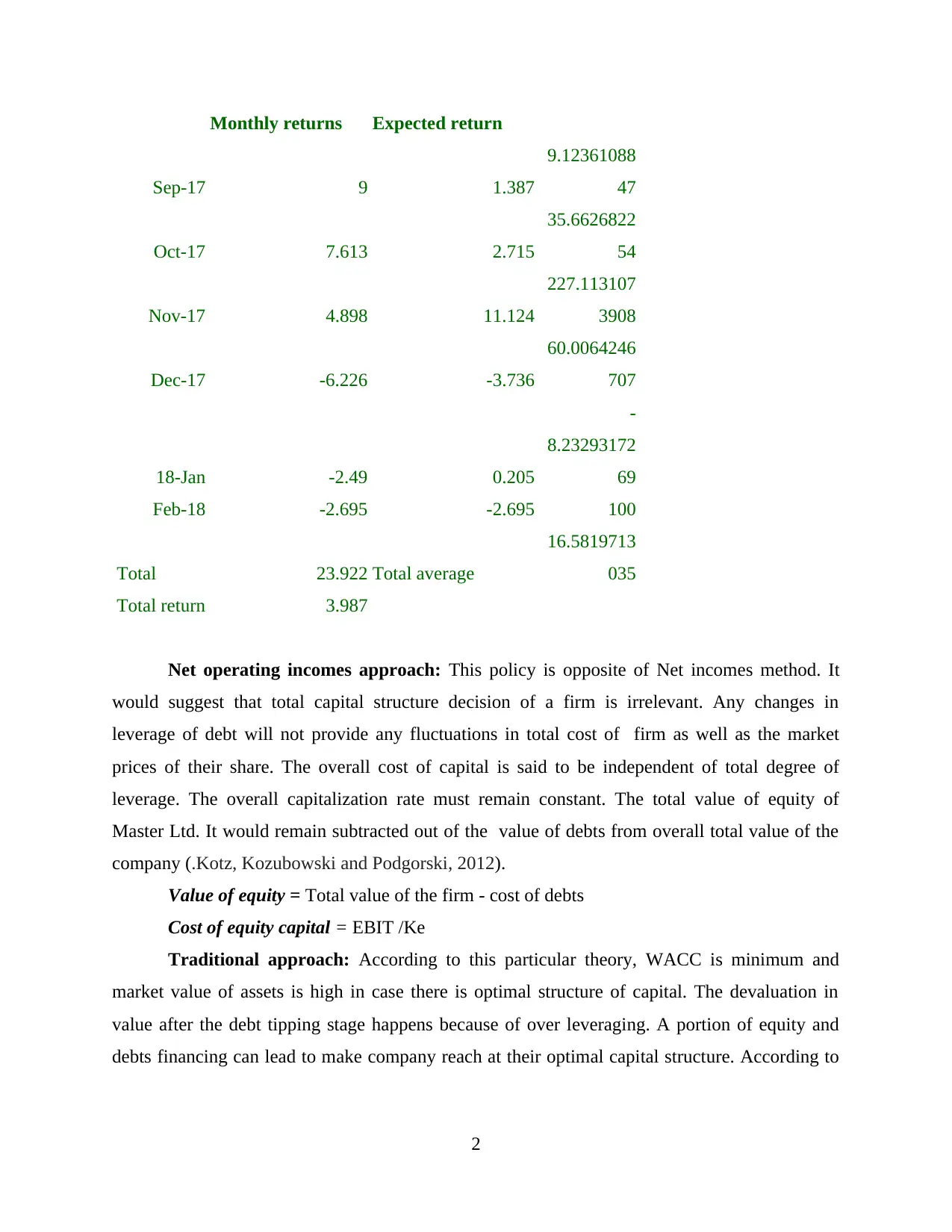

Monthly returns Expected return

Sep-17 9 1.387

9.12361088

47

Oct-17 7.613 2.715

35.6626822

54

Nov-17 4.898 11.124

227.113107

3908

Dec-17 -6.226 -3.736

60.0064246

707

18-Jan -2.49 0.205

-

8.23293172

69

Feb-18 -2.695 -2.695 100

Total 23.922 Total average

16.5819713

035

Total return 3.987

Net operating incomes approach: This policy is opposite of Net incomes method. It

would suggest that total capital structure decision of a firm is irrelevant. Any changes in

leverage of debt will not provide any fluctuations in total cost of firm as well as the market

prices of their share. The overall cost of capital is said to be independent of total degree of

leverage. The overall capitalization rate must remain constant. The total value of equity of

Master Ltd. It would remain subtracted out of the value of debts from overall total value of the

company (.Kotz, Kozubowski and Podgorski, 2012).

Value of equity = Total value of the firm - cost of debts

Cost of equity capital = EBIT /Ke

Traditional approach: According to this particular theory, WACC is minimum and

market value of assets is high in case there is optimal structure of capital. The devaluation in

value after the debt tipping stage happens because of over leveraging. A portion of equity and

debts financing can lead to make company reach at their optimal capital structure. According to

2

Sep-17 9 1.387

9.12361088

47

Oct-17 7.613 2.715

35.6626822

54

Nov-17 4.898 11.124

227.113107

3908

Dec-17 -6.226 -3.736

60.0064246

707

18-Jan -2.49 0.205

-

8.23293172

69

Feb-18 -2.695 -2.695 100

Total 23.922 Total average

16.5819713

035

Total return 3.987

Net operating incomes approach: This policy is opposite of Net incomes method. It

would suggest that total capital structure decision of a firm is irrelevant. Any changes in

leverage of debt will not provide any fluctuations in total cost of firm as well as the market

prices of their share. The overall cost of capital is said to be independent of total degree of

leverage. The overall capitalization rate must remain constant. The total value of equity of

Master Ltd. It would remain subtracted out of the value of debts from overall total value of the

company (.Kotz, Kozubowski and Podgorski, 2012).

Value of equity = Total value of the firm - cost of debts

Cost of equity capital = EBIT /Ke

Traditional approach: According to this particular theory, WACC is minimum and

market value of assets is high in case there is optimal structure of capital. The devaluation in

value after the debt tipping stage happens because of over leveraging. A portion of equity and

debts financing can lead to make company reach at their optimal capital structure. According to

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

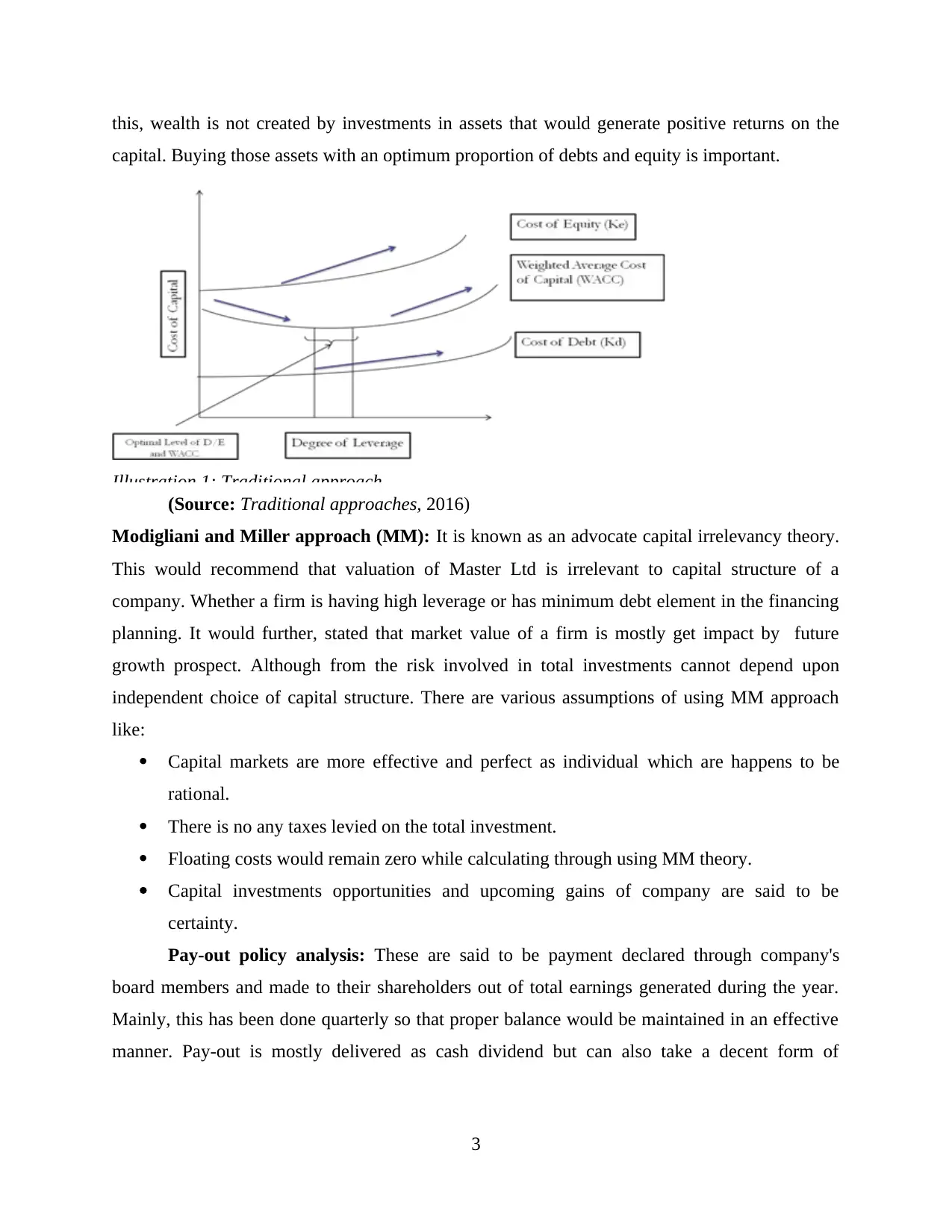

this, wealth is not created by investments in assets that would generate positive returns on the

capital. Buying those assets with an optimum proportion of debts and equity is important.

Illustration 1: Traditional approach

(Source: Traditional approaches, 2016)

Modigliani and Miller approach (MM): It is known as an advocate capital irrelevancy theory.

This would recommend that valuation of Master Ltd is irrelevant to capital structure of a

company. Whether a firm is having high leverage or has minimum debt element in the financing

planning. It would further, stated that market value of a firm is mostly get impact by future

growth prospect. Although from the risk involved in total investments cannot depend upon

independent choice of capital structure. There are various assumptions of using MM approach

like:

Capital markets are more effective and perfect as individual which are happens to be

rational.

There is no any taxes levied on the total investment.

Floating costs would remain zero while calculating through using MM theory.

Capital investments opportunities and upcoming gains of company are said to be

certainty.

Pay-out policy analysis: These are said to be payment declared through company's

board members and made to their shareholders out of total earnings generated during the year.

Mainly, this has been done quarterly so that proper balance would be maintained in an effective

manner. Pay-out is mostly delivered as cash dividend but can also take a decent form of

3

capital. Buying those assets with an optimum proportion of debts and equity is important.

Illustration 1: Traditional approach

(Source: Traditional approaches, 2016)

Modigliani and Miller approach (MM): It is known as an advocate capital irrelevancy theory.

This would recommend that valuation of Master Ltd is irrelevant to capital structure of a

company. Whether a firm is having high leverage or has minimum debt element in the financing

planning. It would further, stated that market value of a firm is mostly get impact by future

growth prospect. Although from the risk involved in total investments cannot depend upon

independent choice of capital structure. There are various assumptions of using MM approach

like:

Capital markets are more effective and perfect as individual which are happens to be

rational.

There is no any taxes levied on the total investment.

Floating costs would remain zero while calculating through using MM theory.

Capital investments opportunities and upcoming gains of company are said to be

certainty.

Pay-out policy analysis: These are said to be payment declared through company's

board members and made to their shareholders out of total earnings generated during the year.

Mainly, this has been done quarterly so that proper balance would be maintained in an effective

manner. Pay-out is mostly delivered as cash dividend but can also take a decent form of

3

inventory of other property. Investment opportunities are always presented in terms of volatility

which is expected in upcoming earnings (Mandelbrot, 2013).

Dividend irrelevancy theory: It is known as an effective theory which an investors does

not need to consider themselves with master Ltd as dividend policy. Thus, they have an option to

sell a little portion of their investment portfolios of equity in case if there is any requirement of

cash. They proposed that the dividend policy of Master Ltd has no impact on the inventory cost

of a firm’s capital structure.

Tax-preferences theory: It is crucial for a company to make consider tax benefits for

investors. Capital gains are more taxed at minimum rate than dividends. As such, investors or

shareholders can prefers capital gains to dividends of company.

1.2 Evaluating policy and practical considerations

In accordance to get maximum benefits from the various capital structure theories, it has

been seen that every method would deliver the best outcomes to company. In tax environment is

mostly allowing the effective deduction of value, capital structure does affecting the total value

of a Master Ltd and their related stock prices. The importance of capital structure theory value

even if there is any assumption in their theory does not taken into account (Addison, 2017).

In order to determine the impacts of capital structure theories, it is essential to understand

the concept by using proper assumption as an examples. It is discussed underneath:

Firms EBIT level = $ 50,000

Cost of Debt =10%

Total value of debt = $200,000 and WACC= 12.5%

Market value of the firm: EBIT / Ke

: 50000/12.5*100= 400,000

Total value of equity: Total market Cost – Cost of debt

: 400,000-200,000= 200,000

Cost of equity capital: EBIT/ Total market value

Revenue to shareholders: EBIT- rate of interest on total amount

: 50000- 20000*10%= 30000

COE: 30000/200000*100= 15%

In the area of corporate financial management, capital structure is being increasingly

being evaluated by the managers in respective path. Researchers, in their respective field make

4

which is expected in upcoming earnings (Mandelbrot, 2013).

Dividend irrelevancy theory: It is known as an effective theory which an investors does

not need to consider themselves with master Ltd as dividend policy. Thus, they have an option to

sell a little portion of their investment portfolios of equity in case if there is any requirement of

cash. They proposed that the dividend policy of Master Ltd has no impact on the inventory cost

of a firm’s capital structure.

Tax-preferences theory: It is crucial for a company to make consider tax benefits for

investors. Capital gains are more taxed at minimum rate than dividends. As such, investors or

shareholders can prefers capital gains to dividends of company.

1.2 Evaluating policy and practical considerations

In accordance to get maximum benefits from the various capital structure theories, it has

been seen that every method would deliver the best outcomes to company. In tax environment is

mostly allowing the effective deduction of value, capital structure does affecting the total value

of a Master Ltd and their related stock prices. The importance of capital structure theory value

even if there is any assumption in their theory does not taken into account (Addison, 2017).

In order to determine the impacts of capital structure theories, it is essential to understand

the concept by using proper assumption as an examples. It is discussed underneath:

Firms EBIT level = $ 50,000

Cost of Debt =10%

Total value of debt = $200,000 and WACC= 12.5%

Market value of the firm: EBIT / Ke

: 50000/12.5*100= 400,000

Total value of equity: Total market Cost – Cost of debt

: 400,000-200,000= 200,000

Cost of equity capital: EBIT/ Total market value

Revenue to shareholders: EBIT- rate of interest on total amount

: 50000- 20000*10%= 30000

COE: 30000/200000*100= 15%

In the area of corporate financial management, capital structure is being increasingly

being evaluated by the managers in respective path. Researchers, in their respective field make

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

huge works in order to increase their maximum market value and planning to generating as much

return as they can through their overall investments.

TASK 2

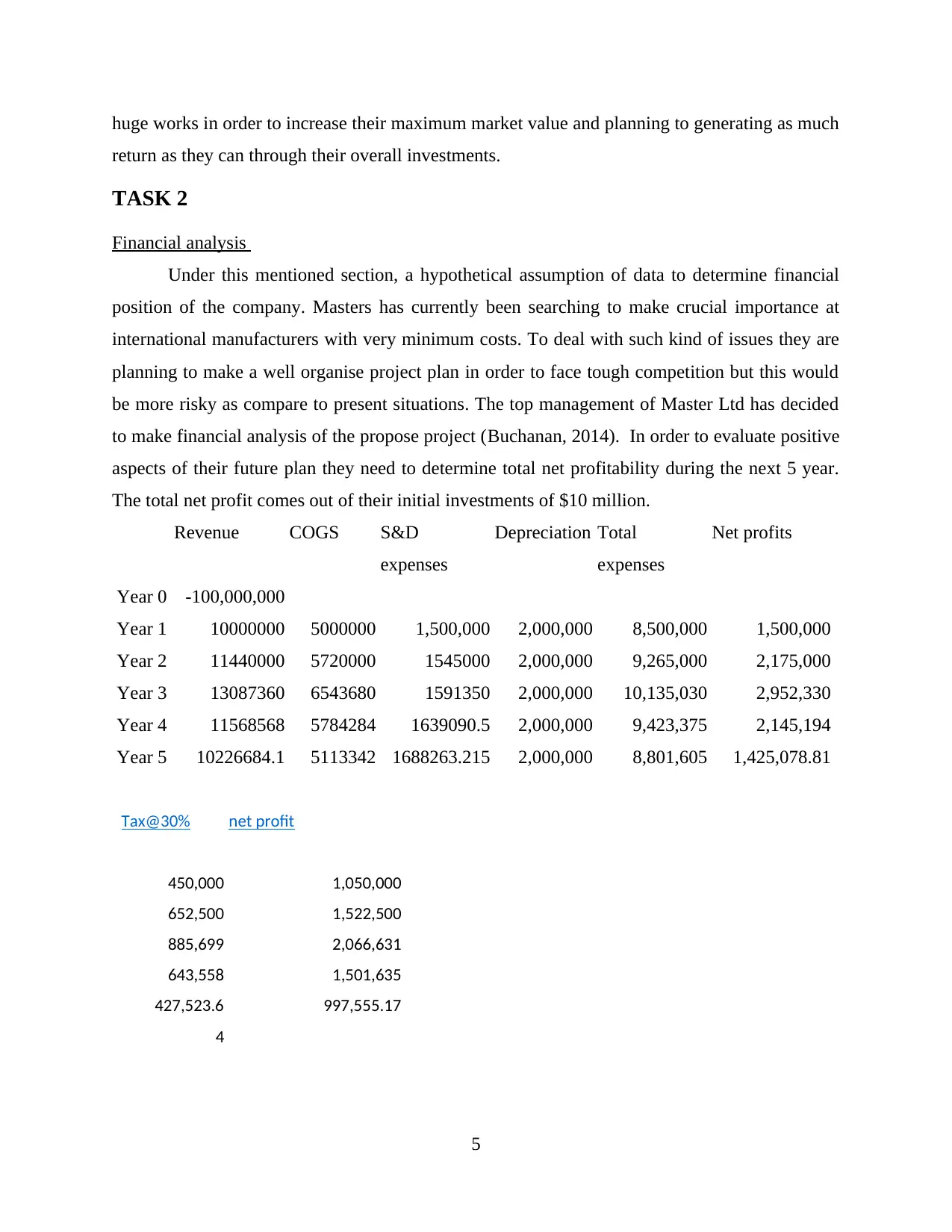

Financial analysis

Under this mentioned section, a hypothetical assumption of data to determine financial

position of the company. Masters has currently been searching to make crucial importance at

international manufacturers with very minimum costs. To deal with such kind of issues they are

planning to make a well organise project plan in order to face tough competition but this would

be more risky as compare to present situations. The top management of Master Ltd has decided

to make financial analysis of the propose project (Buchanan, 2014). In order to evaluate positive

aspects of their future plan they need to determine total net profitability during the next 5 year.

The total net profit comes out of their initial investments of $10 million.

Revenue COGS S&D

expenses

Depreciation Total

expenses

Net profits

Year 0 -100,000,000

Year 1 10000000 5000000 1,500,000 2,000,000 8,500,000 1,500,000

Year 2 11440000 5720000 1545000 2,000,000 9,265,000 2,175,000

Year 3 13087360 6543680 1591350 2,000,000 10,135,030 2,952,330

Year 4 11568568 5784284 1639090.5 2,000,000 9,423,375 2,145,194

Year 5 10226684.1 5113342 1688263.215 2,000,000 8,801,605 1,425,078.81

Tax@30% net profit

450,000 1,050,000

652,500 1,522,500

885,699 2,066,631

643,558 1,501,635

427,523.6

4

997,555.17

5

return as they can through their overall investments.

TASK 2

Financial analysis

Under this mentioned section, a hypothetical assumption of data to determine financial

position of the company. Masters has currently been searching to make crucial importance at

international manufacturers with very minimum costs. To deal with such kind of issues they are

planning to make a well organise project plan in order to face tough competition but this would

be more risky as compare to present situations. The top management of Master Ltd has decided

to make financial analysis of the propose project (Buchanan, 2014). In order to evaluate positive

aspects of their future plan they need to determine total net profitability during the next 5 year.

The total net profit comes out of their initial investments of $10 million.

Revenue COGS S&D

expenses

Depreciation Total

expenses

Net profits

Year 0 -100,000,000

Year 1 10000000 5000000 1,500,000 2,000,000 8,500,000 1,500,000

Year 2 11440000 5720000 1545000 2,000,000 9,265,000 2,175,000

Year 3 13087360 6543680 1591350 2,000,000 10,135,030 2,952,330

Year 4 11568568 5784284 1639090.5 2,000,000 9,423,375 2,145,194

Year 5 10226684.1 5113342 1688263.215 2,000,000 8,801,605 1,425,078.81

Tax@30% net profit

450,000 1,050,000

652,500 1,522,500

885,699 2,066,631

643,558 1,501,635

427,523.6

4

997,555.17

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above calculation, it has been seen that with the initial investments of $10

million they are getting sufficient amount of net profit as 1425078 in the end of 5 year. As the

cash flows are not similar with the initial investment because of which they are getting return on

by charging valuable amount of depreciation on straight line basis. After deducting 30% of total

tax rate the are getting net profit of 997555 in end of 5th year. For making more effective analyse

of these total investments, managers need to calculate various investment appraisal techniques

such as:

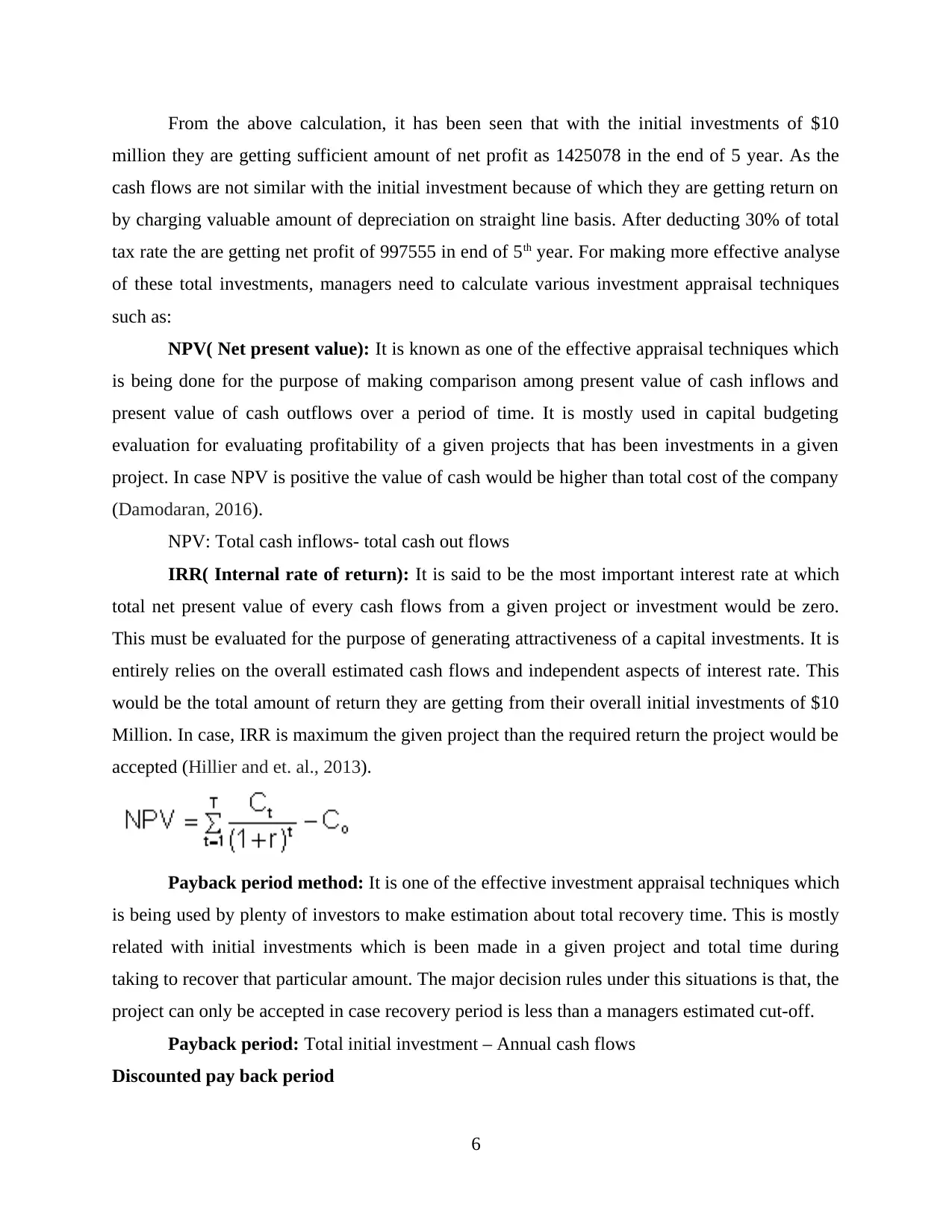

NPV( Net present value): It is known as one of the effective appraisal techniques which

is being done for the purpose of making comparison among present value of cash inflows and

present value of cash outflows over a period of time. It is mostly used in capital budgeting

evaluation for evaluating profitability of a given projects that has been investments in a given

project. In case NPV is positive the value of cash would be higher than total cost of the company

(Damodaran, 2016).

NPV: Total cash inflows- total cash out flows

IRR( Internal rate of return): It is said to be the most important interest rate at which

total net present value of every cash flows from a given project or investment would be zero.

This must be evaluated for the purpose of generating attractiveness of a capital investments. It is

entirely relies on the overall estimated cash flows and independent aspects of interest rate. This

would be the total amount of return they are getting from their overall initial investments of $10

Million. In case, IRR is maximum the given project than the required return the project would be

accepted (Hillier and et. al., 2013).

Payback period method: It is one of the effective investment appraisal techniques which

is being used by plenty of investors to make estimation about total recovery time. This is mostly

related with initial investments which is been made in a given project and total time during

taking to recover that particular amount. The major decision rules under this situations is that, the

project can only be accepted in case recovery period is less than a managers estimated cut-off.

Payback period: Total initial investment – Annual cash flows

Discounted pay back period

6

million they are getting sufficient amount of net profit as 1425078 in the end of 5 year. As the

cash flows are not similar with the initial investment because of which they are getting return on

by charging valuable amount of depreciation on straight line basis. After deducting 30% of total

tax rate the are getting net profit of 997555 in end of 5th year. For making more effective analyse

of these total investments, managers need to calculate various investment appraisal techniques

such as:

NPV( Net present value): It is known as one of the effective appraisal techniques which

is being done for the purpose of making comparison among present value of cash inflows and

present value of cash outflows over a period of time. It is mostly used in capital budgeting

evaluation for evaluating profitability of a given projects that has been investments in a given

project. In case NPV is positive the value of cash would be higher than total cost of the company

(Damodaran, 2016).

NPV: Total cash inflows- total cash out flows

IRR( Internal rate of return): It is said to be the most important interest rate at which

total net present value of every cash flows from a given project or investment would be zero.

This must be evaluated for the purpose of generating attractiveness of a capital investments. It is

entirely relies on the overall estimated cash flows and independent aspects of interest rate. This

would be the total amount of return they are getting from their overall initial investments of $10

Million. In case, IRR is maximum the given project than the required return the project would be

accepted (Hillier and et. al., 2013).

Payback period method: It is one of the effective investment appraisal techniques which

is being used by plenty of investors to make estimation about total recovery time. This is mostly

related with initial investments which is been made in a given project and total time during

taking to recover that particular amount. The major decision rules under this situations is that, the

project can only be accepted in case recovery period is less than a managers estimated cut-off.

Payback period: Total initial investment – Annual cash flows

Discounted pay back period

6

It is effective method which is used by the management of Master company regarding

determination of the profitability which is associated with the project. It is the method of capital

budgeting. This method provides the information regarding the number of years taken by the

organization to attain break even from undertaking of their initial expenditure, by discounting

future cash flows and recognition of time value of money (Yescombe, 2011).

It gives the understanding about the time period which is required to attain the break even

point after starting of new project. In this period, cumulative net present value of project is zero.

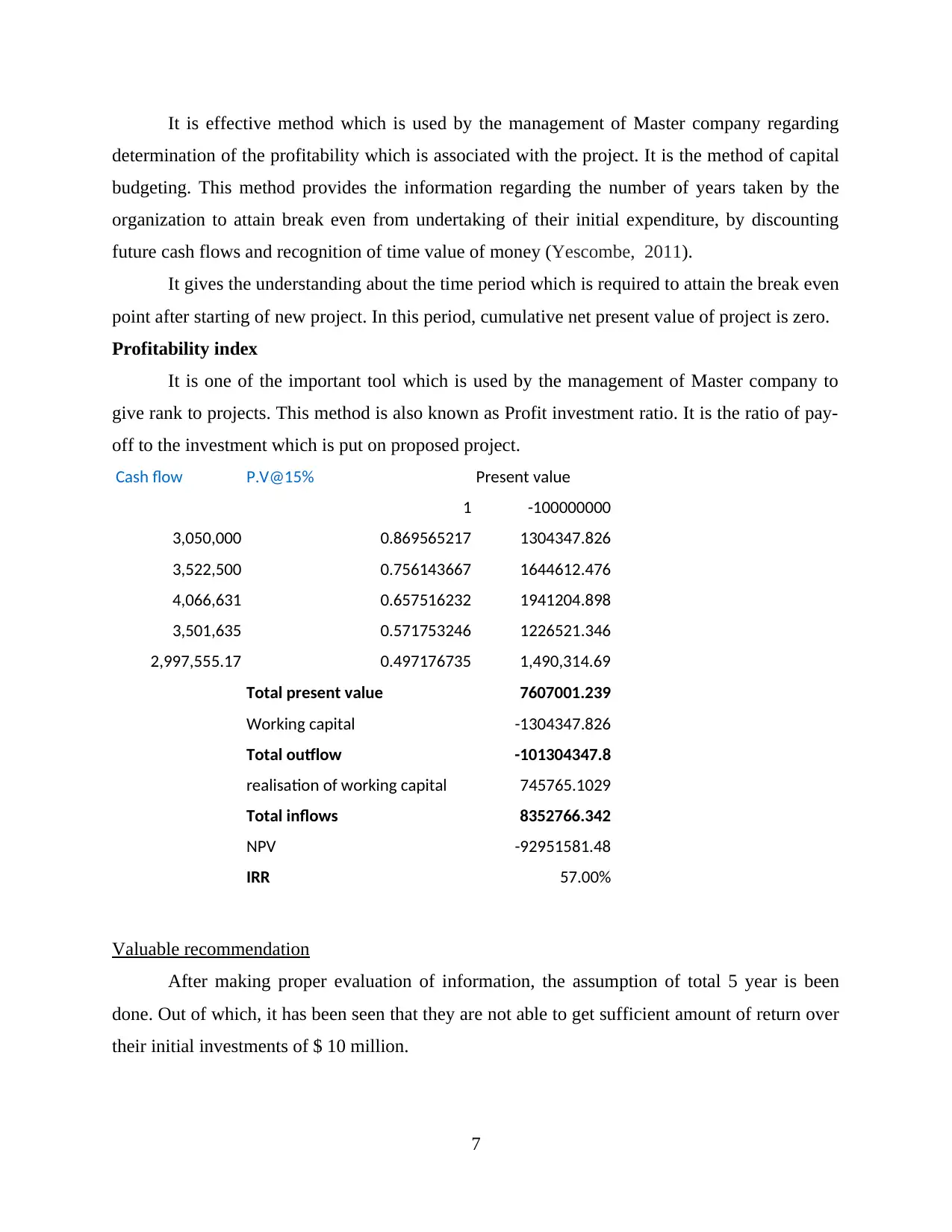

Profitability index

It is one of the important tool which is used by the management of Master company to

give rank to projects. This method is also known as Profit investment ratio. It is the ratio of pay-

off to the investment which is put on proposed project.

Cash flow P.V@15% Present value

1 -100000000

3,050,000 0.869565217 1304347.826

3,522,500 0.756143667 1644612.476

4,066,631 0.657516232 1941204.898

3,501,635 0.571753246 1226521.346

2,997,555.17 0.497176735 1,490,314.69

Total present value 7607001.239

Working capital -1304347.826

Total outflow -101304347.8

realisation of working capital 745765.1029

Total inflows 8352766.342

NPV -92951581.48

IRR 57.00%

Valuable recommendation

After making proper evaluation of information, the assumption of total 5 year is been

done. Out of which, it has been seen that they are not able to get sufficient amount of return over

their initial investments of $ 10 million.

7

determination of the profitability which is associated with the project. It is the method of capital

budgeting. This method provides the information regarding the number of years taken by the

organization to attain break even from undertaking of their initial expenditure, by discounting

future cash flows and recognition of time value of money (Yescombe, 2011).

It gives the understanding about the time period which is required to attain the break even

point after starting of new project. In this period, cumulative net present value of project is zero.

Profitability index

It is one of the important tool which is used by the management of Master company to

give rank to projects. This method is also known as Profit investment ratio. It is the ratio of pay-

off to the investment which is put on proposed project.

Cash flow P.V@15% Present value

1 -100000000

3,050,000 0.869565217 1304347.826

3,522,500 0.756143667 1644612.476

4,066,631 0.657516232 1941204.898

3,501,635 0.571753246 1226521.346

2,997,555.17 0.497176735 1,490,314.69

Total present value 7607001.239

Working capital -1304347.826

Total outflow -101304347.8

realisation of working capital 745765.1029

Total inflows 8352766.342

NPV -92951581.48

IRR 57.00%

Valuable recommendation

After making proper evaluation of information, the assumption of total 5 year is been

done. Out of which, it has been seen that they are not able to get sufficient amount of return over

their initial investments of $ 10 million.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It has been suggested that to make use of data for 10 year so that accurate return and

recovery time duration can be generated. After the end of 5 year they are getting total present

value of 7607001. They need to make use of their capital investments so they valuable amount of

return they would get in near future.

CONCLUSION

It has been concluded from the above report that, large number of benefits are attained by

organization with the help of determination of capital structure and identification of pay out

ratios. It provides the opportunity regarding make effective decisions to improvement of their

profitability. Investment appraisal techniques also plays an important role to choose appropriate

project which is most profitable.

8

recovery time duration can be generated. After the end of 5 year they are getting total present

value of 7607001. They need to make use of their capital investments so they valuable amount of

return they would get in near future.

CONCLUSION

It has been concluded from the above report that, large number of benefits are attained by

organization with the help of determination of capital structure and identification of pay out

ratios. It provides the opportunity regarding make effective decisions to improvement of their

profitability. Investment appraisal techniques also plays an important role to choose appropriate

project which is most profitable.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.