Financial Analysis: Coca-Cola Amatil and Treasury Wine Estate Report

VerifiedAdded on 2021/02/19

|12

|3207

|41

Report

AI Summary

This report provides a comparative financial analysis of Coca-Cola Amatil (CCA) and Treasury Wine Estate (TWE), focusing on their accounting policies, governance mechanisms, and CSR practices. It begins with an introduction to accounting and sustainability, followed by a detailed examination of accounting standards (AASB) and policies used by both companies for property, plant, and equipment recognition and measurement. The report highlights differences in accounting theories (normative vs. positive) and policies between CCA and TWE. Furthermore, it delves into CCA's governance mechanisms for addressing sustainability, including the role of the Board Risk & Sustainability Committee and risk management systems. The report also explores the guidance used by CCA for implementing social and environmental performance reporting. Finally, it contrasts the voluntary CSR disclosures of CCA and TWE, noting variations in their focus areas, strategic frameworks, and key performance indicators. The report concludes with a summary of the findings and references used.

COMPANIES'

COMPARISON

COMPARISON

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

SECTION 3: PART A.....................................................................................................................3

Employing widely used accounting theories and comparison for accounting............................7

SECTION 4: PART B......................................................................................................................8

Coca-Cola Amatil 's governance mechanism to address sustainability......................................8

How risk management systems of Coca-Cola Amatil are addressed and incorporated..............8

Guidance used by Coca-Cola Amatil to implement social and environmental performance and

reporting systems........................................................................................................................9

How CSR voluntary disclosure varies across different companies............................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

SECTION 3: PART A.....................................................................................................................3

Employing widely used accounting theories and comparison for accounting............................7

SECTION 4: PART B......................................................................................................................8

Coca-Cola Amatil 's governance mechanism to address sustainability......................................8

How risk management systems of Coca-Cola Amatil are addressed and incorporated..............8

Guidance used by Coca-Cola Amatil to implement social and environmental performance and

reporting systems........................................................................................................................9

How CSR voluntary disclosure varies across different companies............................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Accounting refers to the practice which is adopted by organisations to ensure effective

measurement, processing as well as communication of certain crucial financial information

within a company (Hussain, Rigoni and Orij, 2018). On the other hand, sustainability is another

effective and essential practice which allow an organisation to conduct its operations in ways

which contributes maximum to preserving, protecting and improving the state of environment,

social as well as sustainable aspects of a firm. The report below is based on Coca-Cola Amatil

and Treasury Wine Estate, which are effective companies dealing in consumer staples, especially

beverages. It includes description of recognition and measurement components of policy for

accounting for each class of property, plant and equipment. It also covers comparing accounting

policies and governance mechanisms to address sustainability. The report also includes

addressing and incorporation systems within the firm and guidance used by Coca-Cola Amatil in

implementing environmental and social performance and reporting systems (Bouten and Hoozée,

2015).

SECTION 3: PART A

Accounting policies and standard are set by Australian Accounting standard Board

(AASB), which is independent Australian Government agency (Khan and Gray, 2016). The

standards are the legislative requirements for companies that need to be apply for run a business.

Such as Coca- Cola Amatil and Treasure wine Estate corporation use accounting standard and

policies to run a business. Financial reporting help both companies to prepare the financial report

and compare the profits from past years. Every organisation should follow the rules and

regulation which is governed by government.

CCA uses financial report framework to prepare the financial report as per Accounting

standard that help to identify the policies. By following Australian accounting standard board

CCA get relevant information and statutory which is required to prepare financial reports.

TWE is also uses Australian accounting standard to prepare and maintain the financial

reports. By following accounting standard TWE gets relevancy and reliability of information

which is most important within organisation.

Recognition and measurement

Accounting refers to the practice which is adopted by organisations to ensure effective

measurement, processing as well as communication of certain crucial financial information

within a company (Hussain, Rigoni and Orij, 2018). On the other hand, sustainability is another

effective and essential practice which allow an organisation to conduct its operations in ways

which contributes maximum to preserving, protecting and improving the state of environment,

social as well as sustainable aspects of a firm. The report below is based on Coca-Cola Amatil

and Treasury Wine Estate, which are effective companies dealing in consumer staples, especially

beverages. It includes description of recognition and measurement components of policy for

accounting for each class of property, plant and equipment. It also covers comparing accounting

policies and governance mechanisms to address sustainability. The report also includes

addressing and incorporation systems within the firm and guidance used by Coca-Cola Amatil in

implementing environmental and social performance and reporting systems (Bouten and Hoozée,

2015).

SECTION 3: PART A

Accounting policies and standard are set by Australian Accounting standard Board

(AASB), which is independent Australian Government agency (Khan and Gray, 2016). The

standards are the legislative requirements for companies that need to be apply for run a business.

Such as Coca- Cola Amatil and Treasure wine Estate corporation use accounting standard and

policies to run a business. Financial reporting help both companies to prepare the financial report

and compare the profits from past years. Every organisation should follow the rules and

regulation which is governed by government.

CCA uses financial report framework to prepare the financial report as per Accounting

standard that help to identify the policies. By following Australian accounting standard board

CCA get relevant information and statutory which is required to prepare financial reports.

TWE is also uses Australian accounting standard to prepare and maintain the financial

reports. By following accounting standard TWE gets relevancy and reliability of information

which is most important within organisation.

Recognition and measurement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CCA and TWE states the assets, liabilities, equity, revenues and expenses which is

defined in the accounting concepts SAC4. It uses the accounting standard to evaluate the

performance of organisation. It follows AASB 116 which help to maintain the plant and

equipment and selling of assets. Australian accounting standard framework in plant and

machinery is defined as probable useful life of plant and equipment and the warranty number

which help to calculate accurately. Its shows in the financial statement after depreciating value.

Additionally, it shown in foot note of balance sheet which helps to understand the actual value of

plant and equipment. CCA prepares annual report every year that help to define the turn over and

profitability situation of the company (Boiral, 2016). It contains all income and expenditure data

in financial report which is shown end of the year. The plant and equipment information of CCA

is described as-

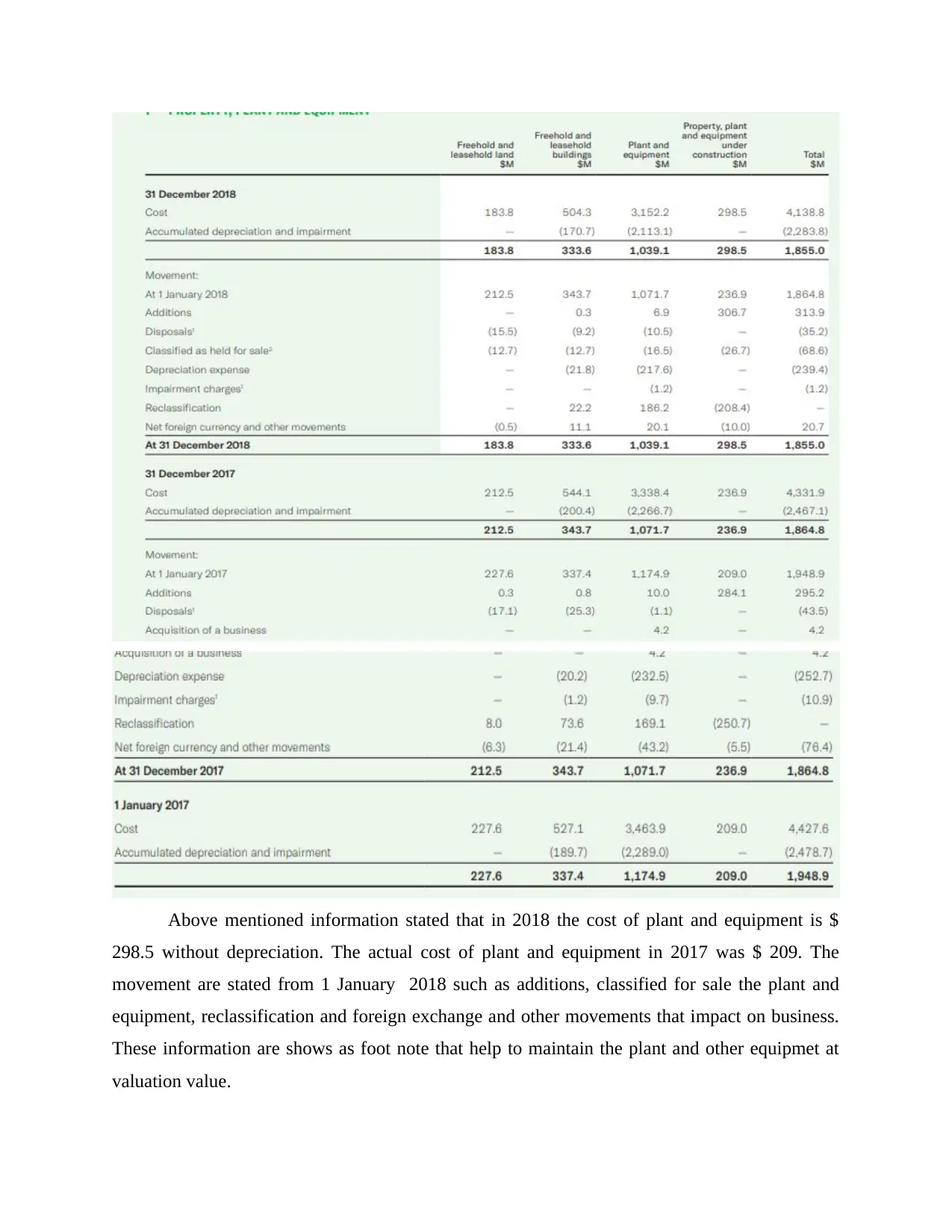

The annual report of Coca Cola Amatil ending of year

defined in the accounting concepts SAC4. It uses the accounting standard to evaluate the

performance of organisation. It follows AASB 116 which help to maintain the plant and

equipment and selling of assets. Australian accounting standard framework in plant and

machinery is defined as probable useful life of plant and equipment and the warranty number

which help to calculate accurately. Its shows in the financial statement after depreciating value.

Additionally, it shown in foot note of balance sheet which helps to understand the actual value of

plant and equipment. CCA prepares annual report every year that help to define the turn over and

profitability situation of the company (Boiral, 2016). It contains all income and expenditure data

in financial report which is shown end of the year. The plant and equipment information of CCA

is described as-

The annual report of Coca Cola Amatil ending of year

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Above mentioned information stated that in 2018 the cost of plant and equipment is $

298.5 without depreciation. The actual cost of plant and equipment in 2017 was $ 209. The

movement are stated from 1 January 2018 such as additions, classified for sale the plant and

equipment, reclassification and foreign exchange and other movements that impact on business.

These information are shows as foot note that help to maintain the plant and other equipmet at

valuation value.

298.5 without depreciation. The actual cost of plant and equipment in 2017 was $ 209. The

movement are stated from 1 January 2018 such as additions, classified for sale the plant and

equipment, reclassification and foreign exchange and other movements that impact on business.

These information are shows as foot note that help to maintain the plant and other equipmet at

valuation value.

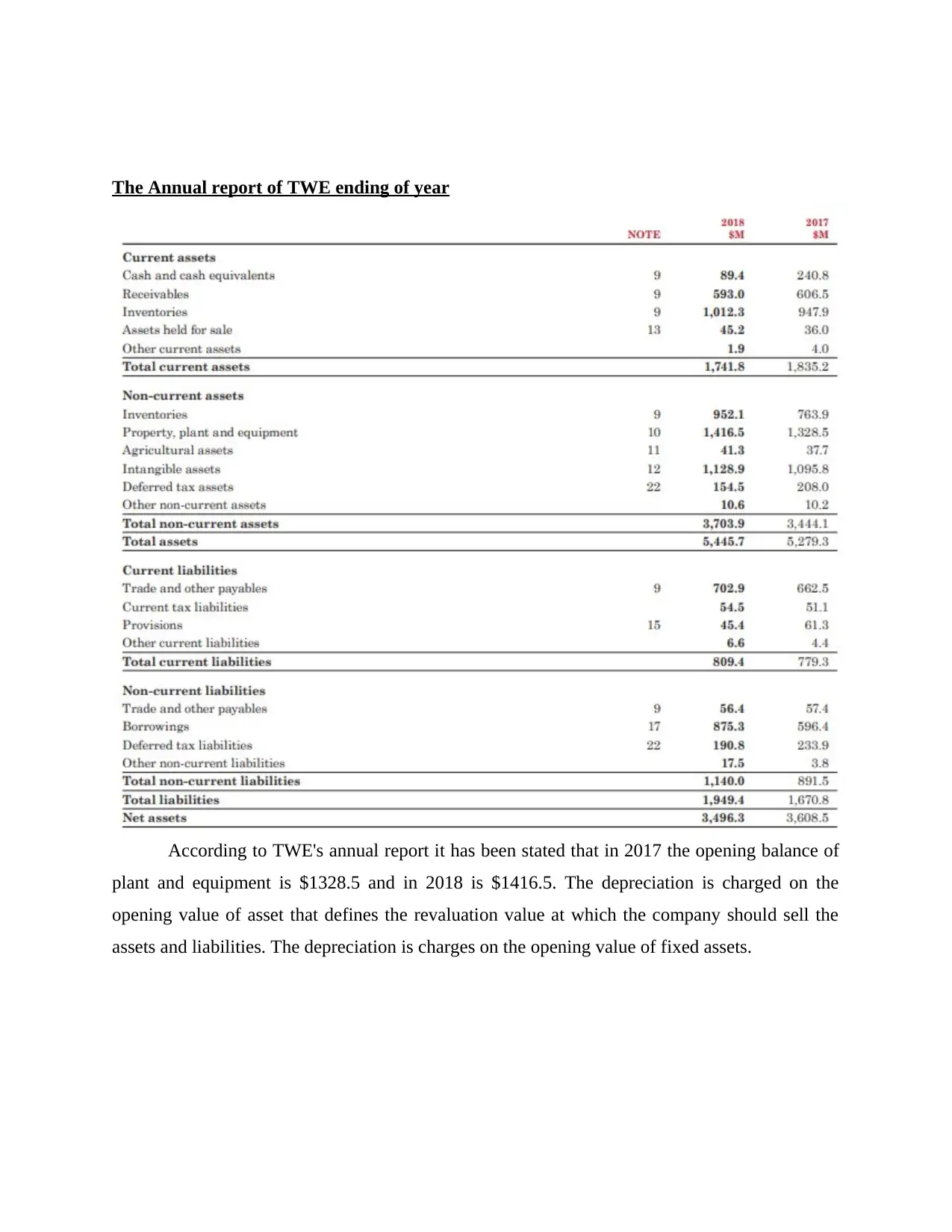

The Annual report of TWE ending of year

According to TWE's annual report it has been stated that in 2017 the opening balance of

plant and equipment is $1328.5 and in 2018 is $1416.5. The depreciation is charged on the

opening value of asset that defines the revaluation value at which the company should sell the

assets and liabilities. The depreciation is charges on the opening value of fixed assets.

According to TWE's annual report it has been stated that in 2017 the opening balance of

plant and equipment is $1328.5 and in 2018 is $1416.5. The depreciation is charged on the

opening value of asset that defines the revaluation value at which the company should sell the

assets and liabilities. The depreciation is charges on the opening value of fixed assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employing widely used accounting theories and comparison for accounting

As per AASB 116, CCA states that it records the plant and equipment at cost less

accumulated depreciation. The cost of these assets are transfer from equity of gains or losses that

defines the actual cost of assets. Further expenses are concluded in capital expenditure which is

associated with the expenditure (Retolaza, San-Jose and Ruíz-Roqueñi, 2016). The useful life of

CCA's equipment is 3 to 15 years and depreciation is calculated on straight line basis.

According to AASB 116 , TWE records the plant and equipment at cost then reduced by

accumulated depreciation. These assets are depreciated so assets can be written down at residual

value over its useful life by using straight line method. As per AASB 116 the depreciation rate at

plant and machinery is 3.3% to 40.0% which reveals depreciated value.

Comparison between CCA and TWE

Basis CCA TWE

Accounting theory CCA is using normative

accounting theory that help to

explain actual accounting

policies. In other words, it help to

explain that what should incurs or

not and what is the actual cost of

assets.

TWE is using positive accounting

theory that states what should

occur instead of predication.

Accounting policies CCA is multinational company

which is using revenue

recognition accounting policies

that help to define the relevancy

of information. According to

AASB1001, the company records

all expenses at cost and

depreciation is charged at 3.30 -

40%.

TWE is using the cost accounting

policies that help to maintain the

cost at actual cost and depreciation

is charged at straight line method.

By following this, it get reliable

and relevant information which

help to gain long term profit within

industry.

As per AASB 116, CCA states that it records the plant and equipment at cost less

accumulated depreciation. The cost of these assets are transfer from equity of gains or losses that

defines the actual cost of assets. Further expenses are concluded in capital expenditure which is

associated with the expenditure (Retolaza, San-Jose and Ruíz-Roqueñi, 2016). The useful life of

CCA's equipment is 3 to 15 years and depreciation is calculated on straight line basis.

According to AASB 116 , TWE records the plant and equipment at cost then reduced by

accumulated depreciation. These assets are depreciated so assets can be written down at residual

value over its useful life by using straight line method. As per AASB 116 the depreciation rate at

plant and machinery is 3.3% to 40.0% which reveals depreciated value.

Comparison between CCA and TWE

Basis CCA TWE

Accounting theory CCA is using normative

accounting theory that help to

explain actual accounting

policies. In other words, it help to

explain that what should incurs or

not and what is the actual cost of

assets.

TWE is using positive accounting

theory that states what should

occur instead of predication.

Accounting policies CCA is multinational company

which is using revenue

recognition accounting policies

that help to define the relevancy

of information. According to

AASB1001, the company records

all expenses at cost and

depreciation is charged at 3.30 -

40%.

TWE is using the cost accounting

policies that help to maintain the

cost at actual cost and depreciation

is charged at straight line method.

By following this, it get reliable

and relevant information which

help to gain long term profit within

industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to Australian accounting standard board 116 it has been recommended that

organisation CCA and TWE follows different accounting policies whi8ch help to maintain the

assets at cost. The AASB states that if organisation is using old pant and equipment then further

expenses which is incurred by organisation should be included in revenue expenditure instead of

capital expenditure. Additionally, if plant and equipment is new then installation cost will be

included in the purchasing cost of plant and equipment.

SECTION 4: PART B

Coca-Cola Amatil 's governance mechanism to address sustainability

Sustainability is a procedure adopted by companies in relation to maintaining appropriate

as well as essential change within an environment in which focus of the company is upon

appropriate and effective exploitation of resources (Maas, Schaltegger and Crutzen, 2016). In

context with Coca-Cola Amatil, board of directors of the organisation have taken sustainability

quite seriously in recent times and promotes highest standards of corporate governance. The

board has also formed Board Risk & Sustainability Committee which is responsible for handling

out sustainable practices within the organisation (Coca Cola Amatil: Annual Report 2018, 2018).

There are several governance mechanisms adopted by Coca-Cola Amatil in relation to

attain sustainability. These mechanisms are discussed below:

The committee is set up to assess as well as oversee effectiveness of the firm's

sustainability framework, which includes several practices such as sustainable packaging.

Furthermore, all the practices performed by the firm in relation to their employees,

customers, environment as well as community are appropriately monitored by the board

as a part of sustainability culture (Thoradeniya and et. al., 2015).

In addition to this, they appropriately manage and approve several initiatives and policies

which help in ensuring that best practices in terms of sustainability and better and

enhanced methods to achieve the same.

How risk management systems of Coca-Cola Amatil are addressed and incorporated

As ethical and social responsibility of an organisation, it is very important that a proper

and long term risk management systems be incorporated within the company, contributing to the

organisation in terms of sustainability (Komori, 2015). Board Risk & Sustainability Committee

within Coca-Cola Amatil is also responsible for addressing several risks and incorporate

organisation CCA and TWE follows different accounting policies whi8ch help to maintain the

assets at cost. The AASB states that if organisation is using old pant and equipment then further

expenses which is incurred by organisation should be included in revenue expenditure instead of

capital expenditure. Additionally, if plant and equipment is new then installation cost will be

included in the purchasing cost of plant and equipment.

SECTION 4: PART B

Coca-Cola Amatil 's governance mechanism to address sustainability

Sustainability is a procedure adopted by companies in relation to maintaining appropriate

as well as essential change within an environment in which focus of the company is upon

appropriate and effective exploitation of resources (Maas, Schaltegger and Crutzen, 2016). In

context with Coca-Cola Amatil, board of directors of the organisation have taken sustainability

quite seriously in recent times and promotes highest standards of corporate governance. The

board has also formed Board Risk & Sustainability Committee which is responsible for handling

out sustainable practices within the organisation (Coca Cola Amatil: Annual Report 2018, 2018).

There are several governance mechanisms adopted by Coca-Cola Amatil in relation to

attain sustainability. These mechanisms are discussed below:

The committee is set up to assess as well as oversee effectiveness of the firm's

sustainability framework, which includes several practices such as sustainable packaging.

Furthermore, all the practices performed by the firm in relation to their employees,

customers, environment as well as community are appropriately monitored by the board

as a part of sustainability culture (Thoradeniya and et. al., 2015).

In addition to this, they appropriately manage and approve several initiatives and policies

which help in ensuring that best practices in terms of sustainability and better and

enhanced methods to achieve the same.

How risk management systems of Coca-Cola Amatil are addressed and incorporated

As ethical and social responsibility of an organisation, it is very important that a proper

and long term risk management systems be incorporated within the company, contributing to the

organisation in terms of sustainability (Komori, 2015). Board Risk & Sustainability Committee

within Coca-Cola Amatil is also responsible for addressing several risks and incorporate

appropriate management systems for the same. Some of the examples for its working is

mentioned below:

Risk culture of the company is monitored as well as reviewed periodically .

Along with implementation of sustainability strategy, the company also analyse various

factors which could possibly be risk for the firm and its strategies. Further, several

implementation plans are formulated taking in account these factors for incorporation of

suitable and relevant risk management strategies. Moreover, all these plans are

formulated in light to combat the existing and potential risks which might affect

sustainability within the company's operations.

Guidance used by Coca-Cola Amatil to implement social and environmental performance and

reporting systems.

It is crucial for an organisation to implement social and environmental performance as an

effective part of their sustainability strategy (Coca Cola Amatil: Sustainability Report 2018,

2018). Furthermore, it is also required that they acquire proper guidance on implementation of

such performance as well as on reporting systems. There are several guidance based on both of

these factors which are discussed below:

As for reporting systems, Coca-Cola Amatil is guided by Global Reporting Initiative

Standards along with feedbacks by stakeholders on their previous reports. Follow ups of

both these entities allow the firm to improve its quality of reporting and how gaps could

be fulfilled in future reporting.

As for environmental and social performance, the company receives active and essential

guidance related to several practices to ensure consistent and improved performance. For

instance well being of stakeholders along with methods applied for packaging and other

processes allow Coca-Cola Amatil to be socially active and environmentally sound in

whatever effective practice they perform within their company (Schneider, 2015).

How CSR voluntary disclosure varies across different companies

Corporate Social Responsibility refers to a self regulation, which provides an ethical

framework to organisations to effectively conduct their operations with providing immense

social and environmental benefits to the firm itself as well as to community. In addition to this,

with rising awareness about CSR, there has been a substantial rise within the voluntary CSR

disclosure as well as sustainability reports (Jain, Keneley and Thomson, 2015). Organisations

mentioned below:

Risk culture of the company is monitored as well as reviewed periodically .

Along with implementation of sustainability strategy, the company also analyse various

factors which could possibly be risk for the firm and its strategies. Further, several

implementation plans are formulated taking in account these factors for incorporation of

suitable and relevant risk management strategies. Moreover, all these plans are

formulated in light to combat the existing and potential risks which might affect

sustainability within the company's operations.

Guidance used by Coca-Cola Amatil to implement social and environmental performance and

reporting systems.

It is crucial for an organisation to implement social and environmental performance as an

effective part of their sustainability strategy (Coca Cola Amatil: Sustainability Report 2018,

2018). Furthermore, it is also required that they acquire proper guidance on implementation of

such performance as well as on reporting systems. There are several guidance based on both of

these factors which are discussed below:

As for reporting systems, Coca-Cola Amatil is guided by Global Reporting Initiative

Standards along with feedbacks by stakeholders on their previous reports. Follow ups of

both these entities allow the firm to improve its quality of reporting and how gaps could

be fulfilled in future reporting.

As for environmental and social performance, the company receives active and essential

guidance related to several practices to ensure consistent and improved performance. For

instance well being of stakeholders along with methods applied for packaging and other

processes allow Coca-Cola Amatil to be socially active and environmentally sound in

whatever effective practice they perform within their company (Schneider, 2015).

How CSR voluntary disclosure varies across different companies

Corporate Social Responsibility refers to a self regulation, which provides an ethical

framework to organisations to effectively conduct their operations with providing immense

social and environmental benefits to the firm itself as well as to community. In addition to this,

with rising awareness about CSR, there has been a substantial rise within the voluntary CSR

disclosure as well as sustainability reports (Jain, Keneley and Thomson, 2015). Organisations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

voluntarily disclose their Corporate Social Responsibilities adopted by them to gain appropriate

support from political end as well as from communities.

However, there is a significant difference between this disclosure across different

companies. For instance, in context of Coca-Cola Amatil, the disclosure of this firm's Corporate

Social Responsibility focuses on four main aspects, which are people of the company, well

being, community as well as environment. Furthermore, the overall emphasis of the firm's CSR

disclosure is situated upon how the firm is delivering and satisfying these four pillars. Moreover,

its reporting also has a strategic framework, which the company would be adopting in relation to

deliver its corporate social responsibility.

As far as Treasury Wine Estates is considered, the firm's voluntary disclosure related to

CSR has differed in terms of including certain other aspects along with the ones discussed above.

There are certain aspects related to the product responsibility and product quality which has been

given appropriate importance within the disclosure and how well the future policies have been

laid down (Treasury Wine Estate: 2018 Sustainability Report, 2018), In addition to this, unlike

the disclosure of Coca-Cola Amatil, the organisation has also laid down several Key

Performance indicators in response to the future CSR practice adopted by the firm. Another

difference between the voluntary disclosure of these companies is the limitations within practices

which has been showcased.

In context with industries, there is a huge difference in CSR voluntary disclosure,

especially between companies belonging to resources, technology as well as industrial products.

Reason for the same is that large organisations operating within these industries often opt

sustainability reports rather than CSR voluntary disclosure. However, while there are several

similar contents within their disclosures such as policies for equality and human rights, there are

several information which differs depending upon industries. For instance, technological

industries focuses on disclosing aspects such as using techniques for low carbon footprint,

whereas emphasis of industries focusing on development of products is upon sustainable

packaging and delivery. More or less, the prime focus of each industry is related to the best

practices followed by businesses in their sectors. Still, there is a lot of difference between their

CSR voluntary disclosures (Wuttichindanon, 2017). Furthermore, there is also a significant

difference between reporting of these voluntary disclosures, the major one being timeline of their

respective reporting (Hąbek and Wolniak, 2016). As an example, each industry has different time

support from political end as well as from communities.

However, there is a significant difference between this disclosure across different

companies. For instance, in context of Coca-Cola Amatil, the disclosure of this firm's Corporate

Social Responsibility focuses on four main aspects, which are people of the company, well

being, community as well as environment. Furthermore, the overall emphasis of the firm's CSR

disclosure is situated upon how the firm is delivering and satisfying these four pillars. Moreover,

its reporting also has a strategic framework, which the company would be adopting in relation to

deliver its corporate social responsibility.

As far as Treasury Wine Estates is considered, the firm's voluntary disclosure related to

CSR has differed in terms of including certain other aspects along with the ones discussed above.

There are certain aspects related to the product responsibility and product quality which has been

given appropriate importance within the disclosure and how well the future policies have been

laid down (Treasury Wine Estate: 2018 Sustainability Report, 2018), In addition to this, unlike

the disclosure of Coca-Cola Amatil, the organisation has also laid down several Key

Performance indicators in response to the future CSR practice adopted by the firm. Another

difference between the voluntary disclosure of these companies is the limitations within practices

which has been showcased.

In context with industries, there is a huge difference in CSR voluntary disclosure,

especially between companies belonging to resources, technology as well as industrial products.

Reason for the same is that large organisations operating within these industries often opt

sustainability reports rather than CSR voluntary disclosure. However, while there are several

similar contents within their disclosures such as policies for equality and human rights, there are

several information which differs depending upon industries. For instance, technological

industries focuses on disclosing aspects such as using techniques for low carbon footprint,

whereas emphasis of industries focusing on development of products is upon sustainable

packaging and delivery. More or less, the prime focus of each industry is related to the best

practices followed by businesses in their sectors. Still, there is a lot of difference between their

CSR voluntary disclosures (Wuttichindanon, 2017). Furthermore, there is also a significant

difference between reporting of these voluntary disclosures, the major one being timeline of their

respective reporting (Hąbek and Wolniak, 2016). As an example, each industry has different time

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

schedules lined up for CSR disclosure, moreover, some even consider then irregularly. In

addition to this, distinct industries have different indicators. For instance, companies like Coca-

Cola Amatil as well as Treasury Wine Estates could use different indicators for measuring their

CSR activities. Furthermore, there is no set format of reporting of these voluntary disclosures.

Furthermore, there are different sets of metrics used by businesses within different industries.

The major determinant factor of the same is related to the understandability of the country in

which the industry is situated in. there are several countries which do not stress about adoption of

CSR practices and does not welcome the idea of CSR voluntary disclosures. Whereas, within

some countries like Australia and UK, there have been emphasis given on such reporting. Thus,

there is a significant difference between CSR voluntary disclosures, however, it is an imperative

practice and must be adopted by businesses of each sector to ensure effective and necessary

sustainability (O'Dwyer and Unerman, 2016).

CONCLUSION

Thus, it is concluded from the above report, that accounting and sustainability are crucial

practices for business organisations. It is essential to describe measurement and recognition

components of accounting policies for the firm. Furthermore, accounting theories also hold a

necessary position in comparing the policies for accounting. In addition to this, governance

mechanisms, risk management systems and several guidances are necessary for firms to follow

with respect to achieving effective sustainability. Lastly, it is important that difference between

CSR voluntary disclosure is highlighted to ensure better understandability of this concept.

addition to this, distinct industries have different indicators. For instance, companies like Coca-

Cola Amatil as well as Treasury Wine Estates could use different indicators for measuring their

CSR activities. Furthermore, there is no set format of reporting of these voluntary disclosures.

Furthermore, there are different sets of metrics used by businesses within different industries.

The major determinant factor of the same is related to the understandability of the country in

which the industry is situated in. there are several countries which do not stress about adoption of

CSR practices and does not welcome the idea of CSR voluntary disclosures. Whereas, within

some countries like Australia and UK, there have been emphasis given on such reporting. Thus,

there is a significant difference between CSR voluntary disclosures, however, it is an imperative

practice and must be adopted by businesses of each sector to ensure effective and necessary

sustainability (O'Dwyer and Unerman, 2016).

CONCLUSION

Thus, it is concluded from the above report, that accounting and sustainability are crucial

practices for business organisations. It is essential to describe measurement and recognition

components of accounting policies for the firm. Furthermore, accounting theories also hold a

necessary position in comparing the policies for accounting. In addition to this, governance

mechanisms, risk management systems and several guidances are necessary for firms to follow

with respect to achieving effective sustainability. Lastly, it is important that difference between

CSR voluntary disclosure is highlighted to ensure better understandability of this concept.

REFERENCES

Books and Journals

Boiral, O. (2016). Accounting for the unaccountable: Biodiversity reporting and impression

management. Journal of Business Ethics. 135(4). 751-768.

Bouten, L., & Hoozée, S. (2015). Challenges in sustainability and integrated reporting. Issues in

Accounting Education Teaching Notes. 30(4). 83-93.

Hąbek, P., & Wolniak, R. (2016). Assessing the quality of corporate social responsibility reports:

the case of reporting practices in selected European Union member states. Quality &

quantity. 50(1). 399-420.

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability

performance: Analysis of triple bottom line performance. Journal of Business Ethics.

149(2). 411-432.

Jain, A., Keneley, M., & Thomson, D. (2015). Voluntary CSR disclosure works! Evidence from

Asia-Pacific banks. Social Responsibility Journal. 11(1). 2-18.

Khan, T., & Gray, R. (2016). Accounting, identity, autopoiesis+ sustainability: A comment,

development and expansion on Lawrence, Botes, Collins and Roper (2013). Meditari

Accountancy Research. 24(1). 36-55.

Komori, N. (2015). Beneath the globalization paradox: Towards the sustainability of cultural

diversity in accounting research. Critical Perspectives on Accounting. 26. 141-156.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Advancing the integration of corporate

sustainability measurement, management and reporting. Journal of cleaner production.

133. 859-862.

O'Dwyer, B., & Unerman, J. (2016). Fostering rigour in accounting for social sustainability.

Accounting, Organizations and Society. 49. 32-40.

Retolaza, J. L., San-Jose, L., & Ruíz-Roqueñi, M. (2016). Social accounting for sustainability:

Monetizing the social value. Cham: Springer.

Schneider, A. (2015). Reflexivity in sustainability accounting and management: Transcending

the economic focus of corporate sustainability. Journal of Business Ethics. 127(3). 525-

536.

Thoradeniya, P., & et. al. (2015). Sustainability reporting and the theory of planned behaviour.

Accounting, Auditing & Accountability Journal. 28(7). 1099-1137.

Wuttichindanon, S. (2017). Corporate social responsibility disclosure—choices of report and its

determinants: Empirical evidence from firms listed on the Stock Exchange of Thailand.

Kasetsart Journal of Social Sciences. 38(2). 156-162.

Online

Coca Cola Amatil: Annual Report 2018. [Online] Available Through:

<https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2019/2018-

Annual-Report.ashx>

Coca Cola Amatil: Sustainability Report 2018. 2018. [Online] Available Through:

<https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2019/2018-

Sustainability-Report.ashx>

Treasury Wine Estate: 2018 Sustainability Report. 2018. [Online] Available Through:

<https://www.tweglobal.com/-/media/Files/Global/Responsibility/2018-Sustainability-

Report.ashx>

Books and Journals

Boiral, O. (2016). Accounting for the unaccountable: Biodiversity reporting and impression

management. Journal of Business Ethics. 135(4). 751-768.

Bouten, L., & Hoozée, S. (2015). Challenges in sustainability and integrated reporting. Issues in

Accounting Education Teaching Notes. 30(4). 83-93.

Hąbek, P., & Wolniak, R. (2016). Assessing the quality of corporate social responsibility reports:

the case of reporting practices in selected European Union member states. Quality &

quantity. 50(1). 399-420.

Hussain, N., Rigoni, U., & Orij, R. P. (2018). Corporate governance and sustainability

performance: Analysis of triple bottom line performance. Journal of Business Ethics.

149(2). 411-432.

Jain, A., Keneley, M., & Thomson, D. (2015). Voluntary CSR disclosure works! Evidence from

Asia-Pacific banks. Social Responsibility Journal. 11(1). 2-18.

Khan, T., & Gray, R. (2016). Accounting, identity, autopoiesis+ sustainability: A comment,

development and expansion on Lawrence, Botes, Collins and Roper (2013). Meditari

Accountancy Research. 24(1). 36-55.

Komori, N. (2015). Beneath the globalization paradox: Towards the sustainability of cultural

diversity in accounting research. Critical Perspectives on Accounting. 26. 141-156.

Maas, K., Schaltegger, S., & Crutzen, N. (2016). Advancing the integration of corporate

sustainability measurement, management and reporting. Journal of cleaner production.

133. 859-862.

O'Dwyer, B., & Unerman, J. (2016). Fostering rigour in accounting for social sustainability.

Accounting, Organizations and Society. 49. 32-40.

Retolaza, J. L., San-Jose, L., & Ruíz-Roqueñi, M. (2016). Social accounting for sustainability:

Monetizing the social value. Cham: Springer.

Schneider, A. (2015). Reflexivity in sustainability accounting and management: Transcending

the economic focus of corporate sustainability. Journal of Business Ethics. 127(3). 525-

536.

Thoradeniya, P., & et. al. (2015). Sustainability reporting and the theory of planned behaviour.

Accounting, Auditing & Accountability Journal. 28(7). 1099-1137.

Wuttichindanon, S. (2017). Corporate social responsibility disclosure—choices of report and its

determinants: Empirical evidence from firms listed on the Stock Exchange of Thailand.

Kasetsart Journal of Social Sciences. 38(2). 156-162.

Online

Coca Cola Amatil: Annual Report 2018. [Online] Available Through:

<https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2019/2018-

Annual-Report.ashx>

Coca Cola Amatil: Sustainability Report 2018. 2018. [Online] Available Through:

<https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2019/2018-

Sustainability-Report.ashx>

Treasury Wine Estate: 2018 Sustainability Report. 2018. [Online] Available Through:

<https://www.tweglobal.com/-/media/Files/Global/Responsibility/2018-Sustainability-

Report.ashx>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.