Comprehensive Financial Management Consolidation Project Report

VerifiedAdded on 2020/07/23

|7

|1227

|65

Project

AI Summary

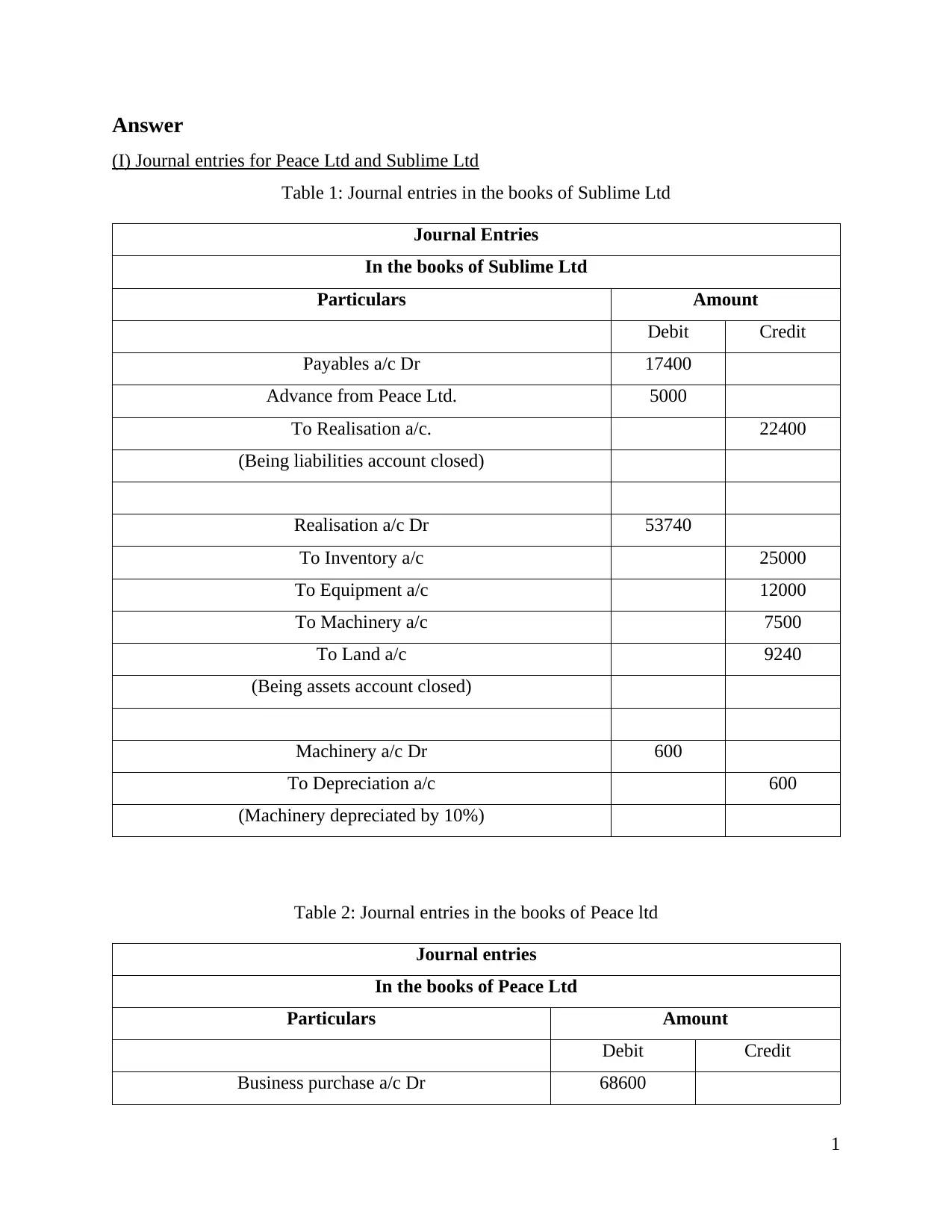

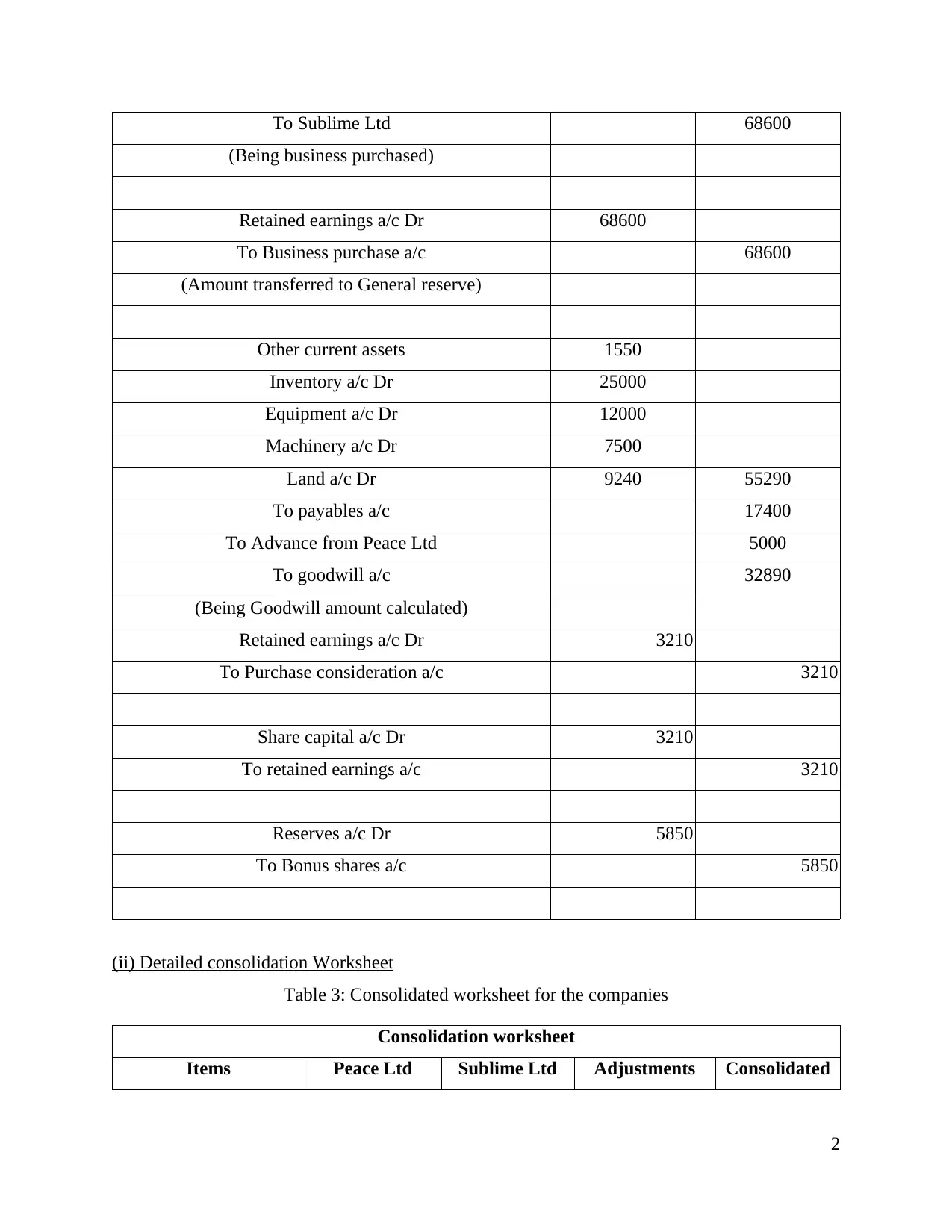

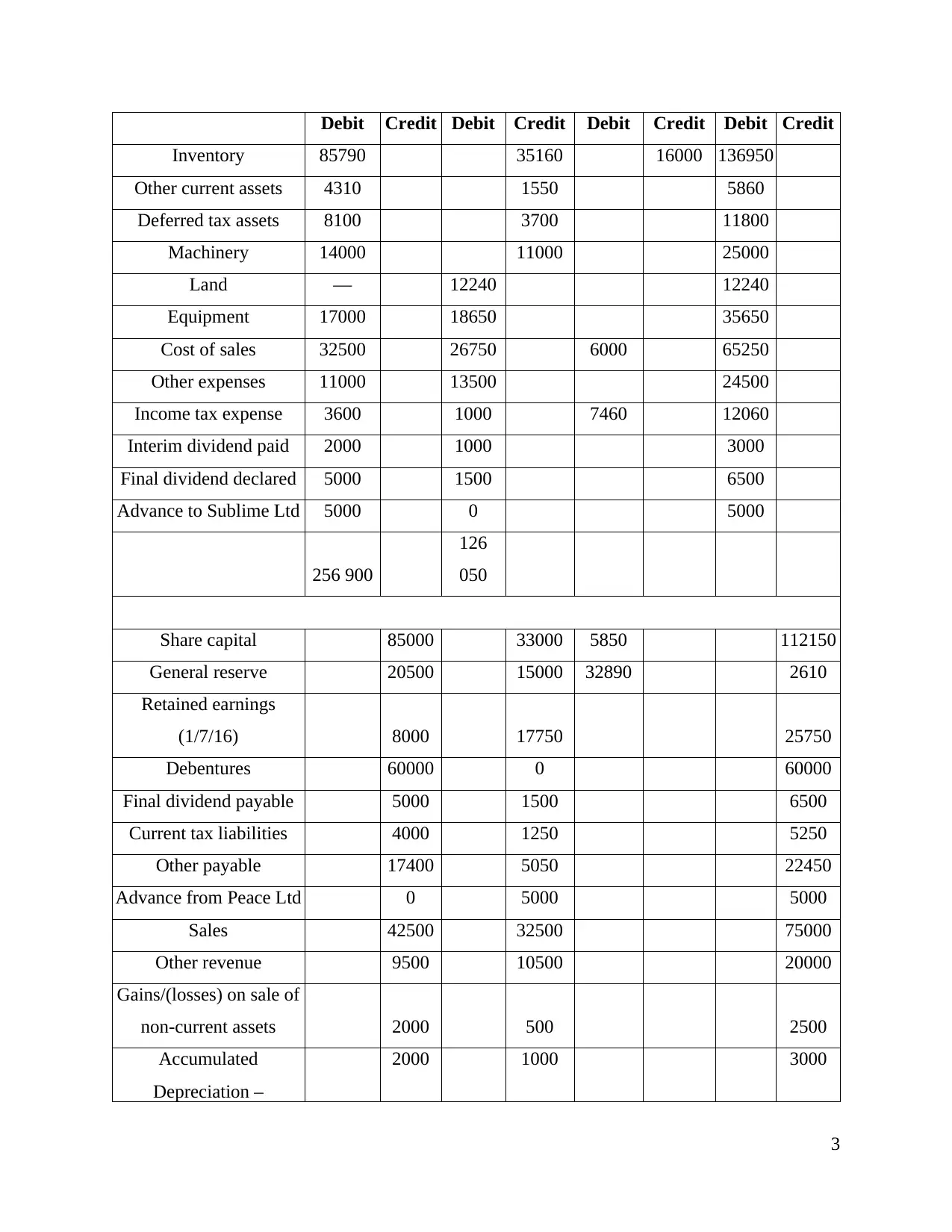

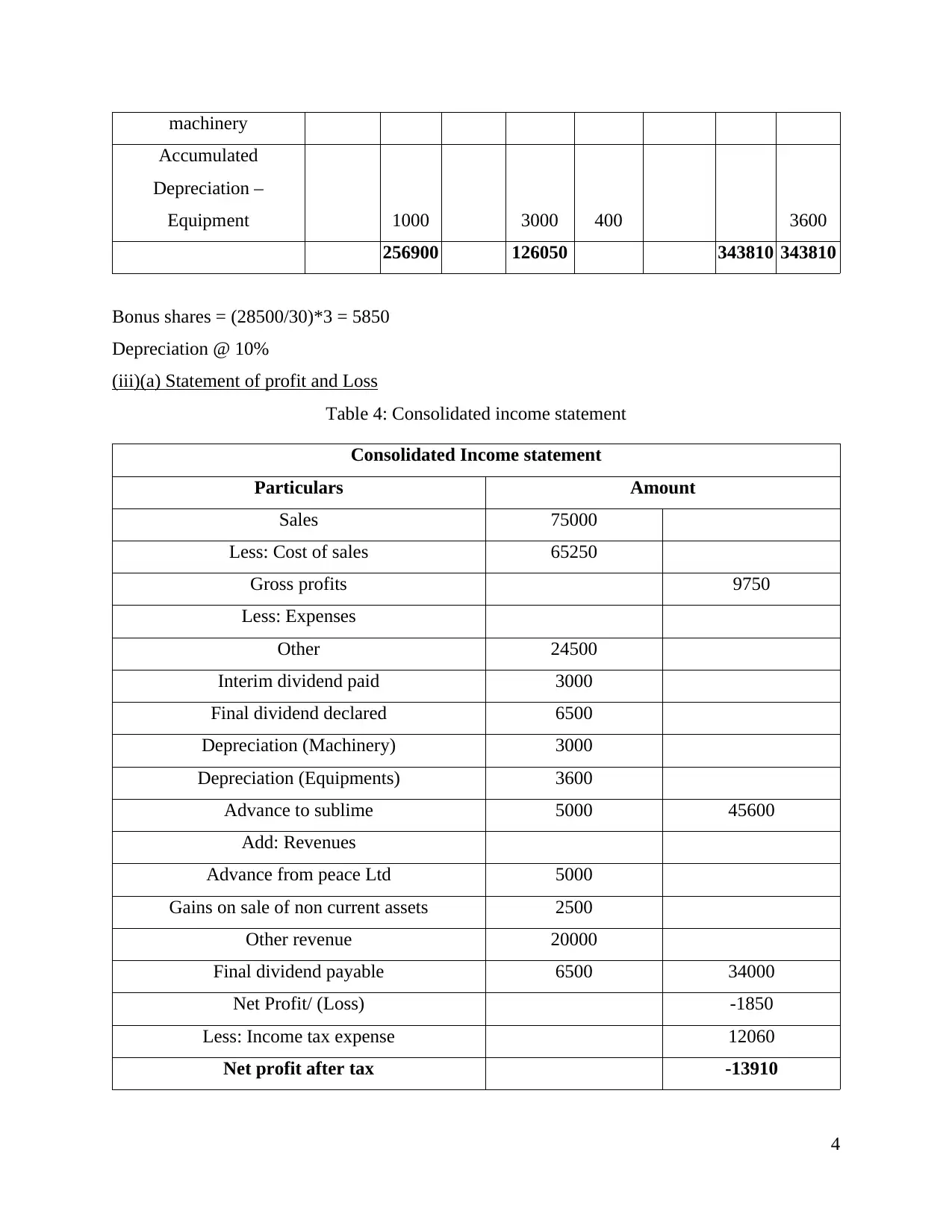

This financial management project presents a detailed consolidation analysis of two companies, Peace Ltd and Sublime Ltd. The project begins with journal entries for both companies, detailing transactions such as the closing of liabilities, asset closures, depreciation, and business purchases. A comprehensive consolidation worksheet is provided, followed by the creation of consolidated financial statements. These include a consolidated income statement, a statement of equity, and a balance sheet. The income statement shows sales, cost of sales, expenses, and revenue to arrive at a net loss after tax. The statement of equity details share capital, general reserve, and retained earnings. Finally, the balance sheet presents the consolidated assets and liabilities. The project demonstrates the process of consolidating financial information to present a unified financial picture of the combined entities.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.