Financial Accounting Homework: Consolidation and Reporting

VerifiedAdded on 2021/06/17

|7

|1713

|216

Homework Assignment

AI Summary

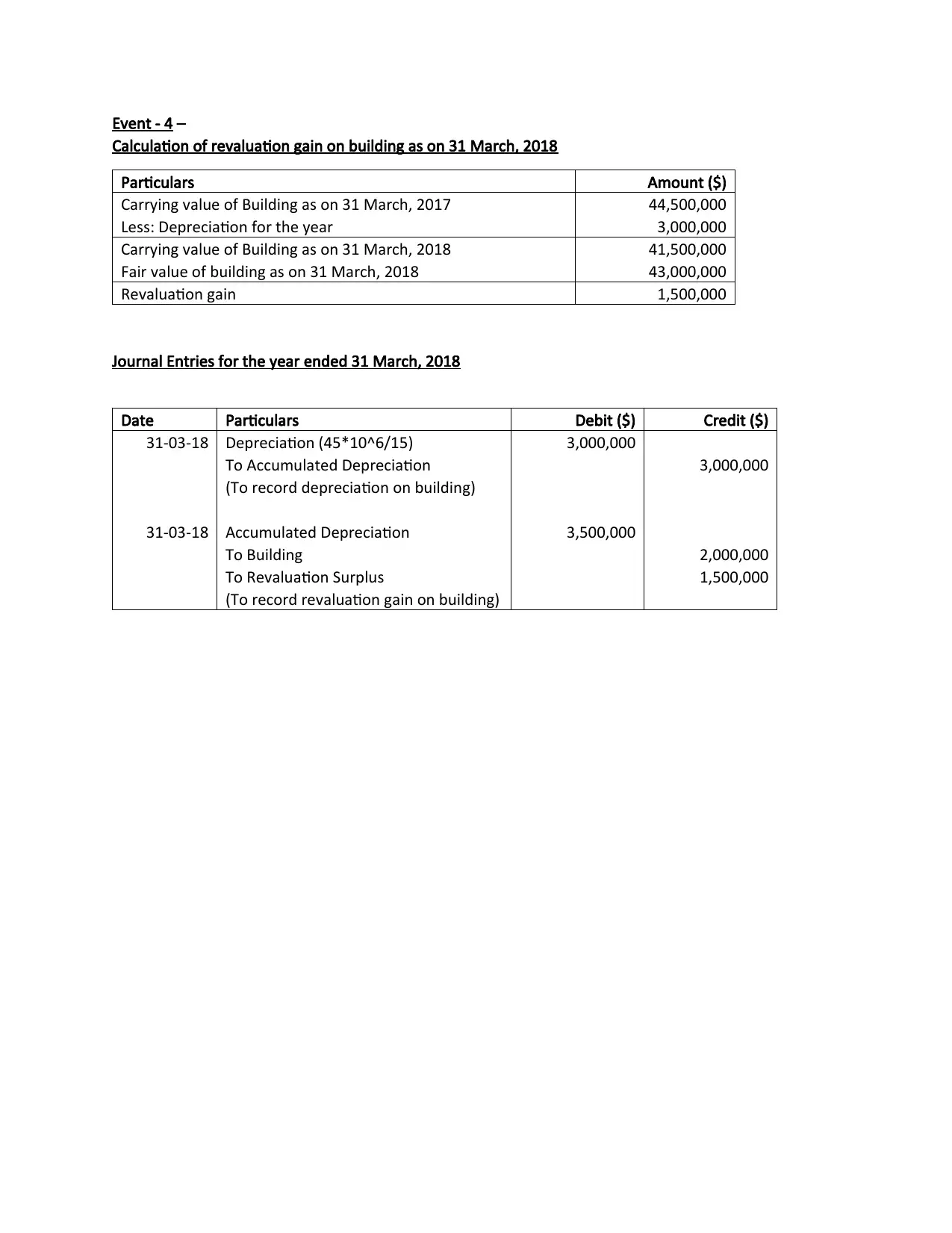

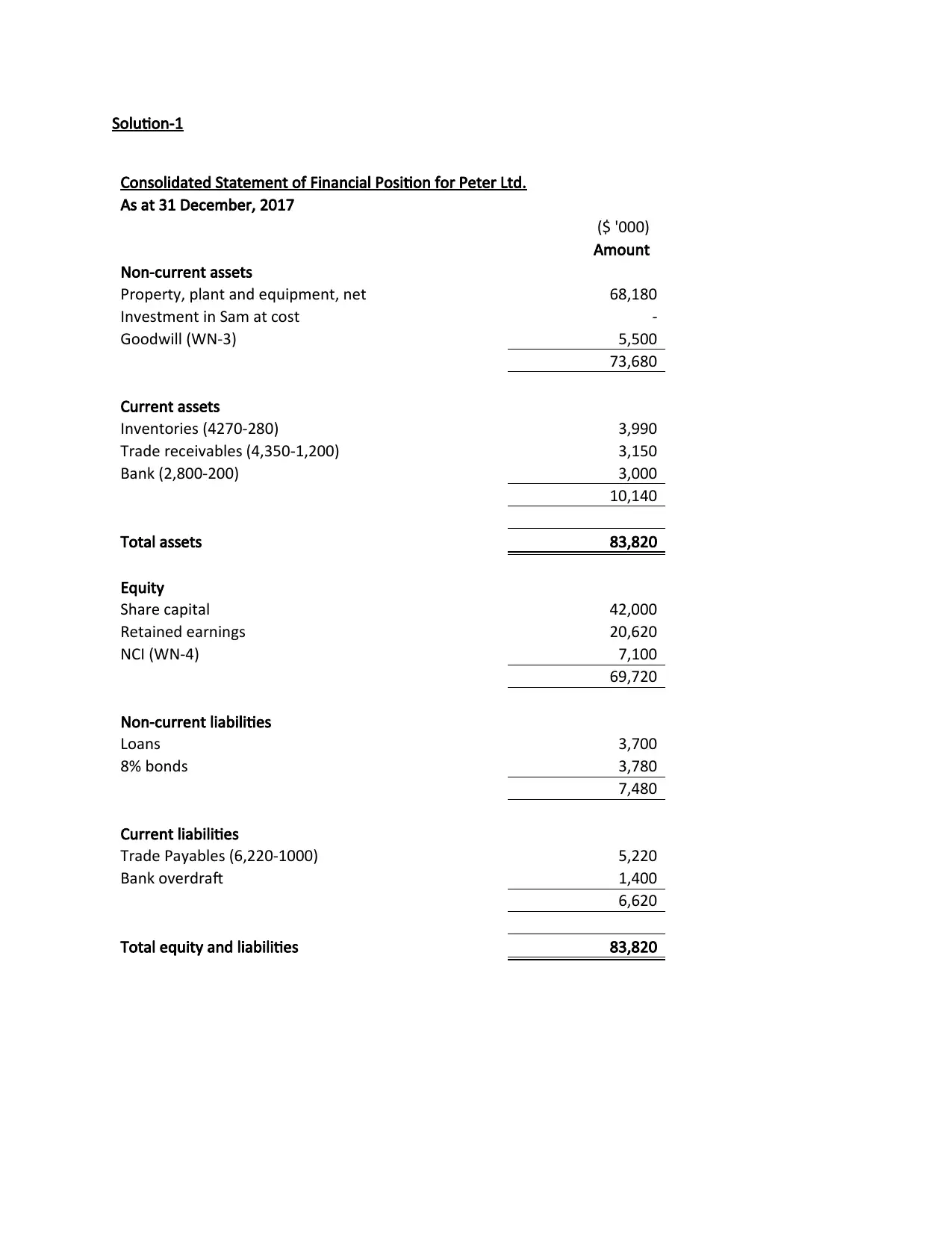

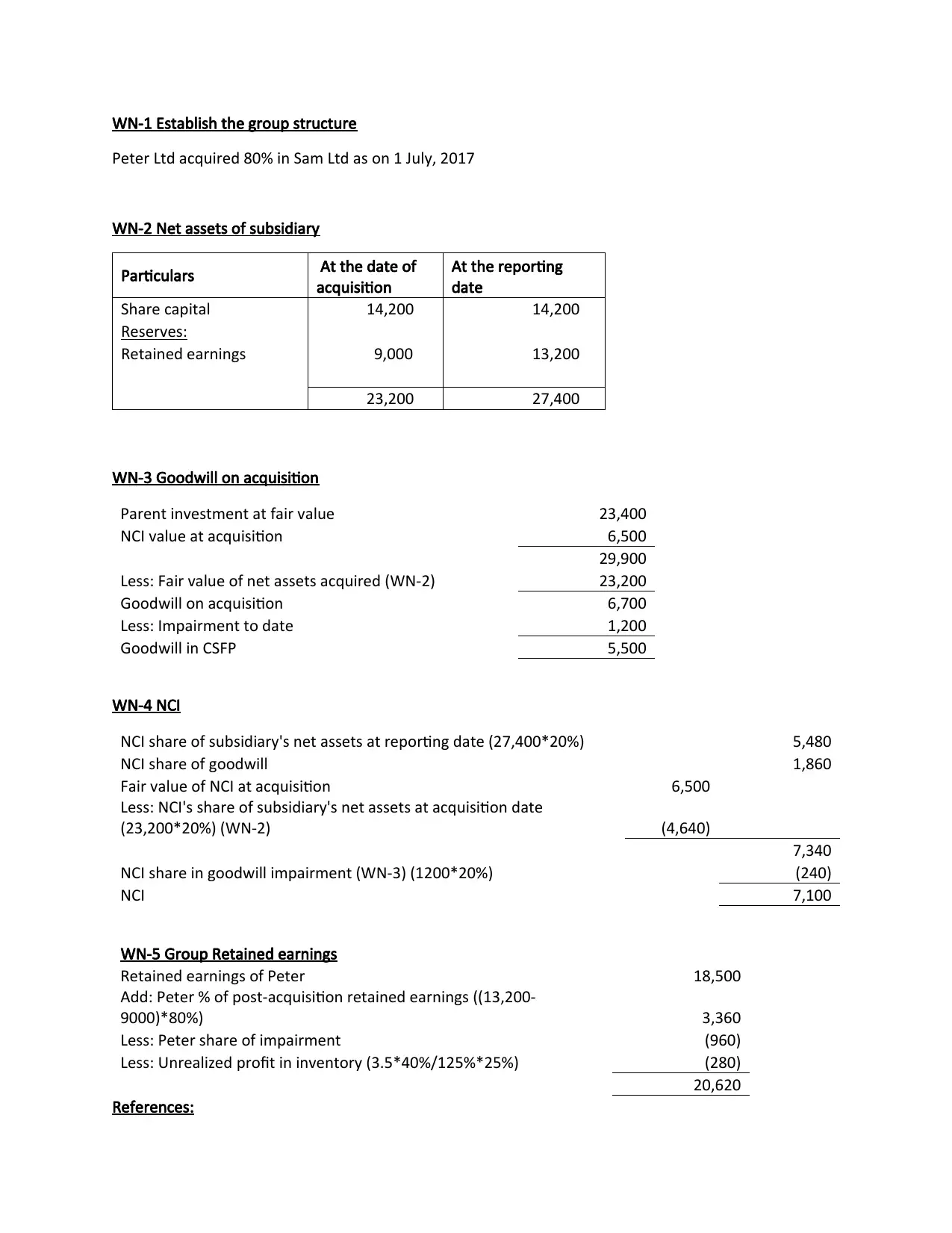

This assignment solution addresses key concepts in financial accounting, including the recognition and measurement of assets under HKAS 16 (Property, Plant and Equipment) and the treatment of provisions and contingent liabilities under HKAS 37. The solution analyzes the accounting for research and development costs, building purchases, and the revaluation of assets. It also includes a consolidated statement of financial position for Peter Ltd., demonstrating the consolidation of a subsidiary (Sam Ltd.), calculation of goodwill, and the treatment of non-controlling interests (NCI). The assignment covers various financial reporting aspects, such as impairment, unrealized profit, and the presentation of consolidated financial statements. The solution provides detailed journal entries and workings to support the accounting treatments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.