FIN5003: Financial Control and Budgeting in Healthcare Services

VerifiedAdded on 2022/12/19

|15

|4731

|83

Report

AI Summary

This report offers a comprehensive analysis of financial control and budgeting within the National Health Service (NHS) in the UK. It begins by exploring the legal, financial, and regulatory environment of health and social care, including the protection of workers and the use of health financing. The report then delves into various funding options like Private Finance Initiatives, agency partnerships, and competitive tendering. Agency theory's role in the NHS is examined, alongside communication strategies with stakeholders. The impact of financial constraints, costs, and budgets on healthcare services is assessed, including budgeting challenges in the public sector and a comparison of incremental and zero-based budgeting. Finally, the report covers the break-even point and margin of safety, providing a valuable overview of financial management in healthcare.

Financial Control and

Budgeting

Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

Question 1 .......................................................................................................................................3

A Legal, financial and regulatory environment of health and social care ..................................3

B Use of funding options ............................................................................................................4

C Agency theory .........................................................................................................................5

Question 2........................................................................................................................................6

A Impact of financial constraints, cost and budget of health and social care services ..............6

B challenges of budgeting in public sector organisations............................................................7

C Advantages and disadvantage of incremental and Zero based budgeting ...............................9

Question 3......................................................................................................................................11

Break even point and margin of safety......................................................................................11

Assumptions for break even point.............................................................................................12

Conclusion ....................................................................................................................................13

REFERENC...................................................................................................................................14

INTRODUCTION ..........................................................................................................................3

Question 1 .......................................................................................................................................3

A Legal, financial and regulatory environment of health and social care ..................................3

B Use of funding options ............................................................................................................4

C Agency theory .........................................................................................................................5

Question 2........................................................................................................................................6

A Impact of financial constraints, cost and budget of health and social care services ..............6

B challenges of budgeting in public sector organisations............................................................7

C Advantages and disadvantage of incremental and Zero based budgeting ...............................9

Question 3......................................................................................................................................11

Break even point and margin of safety......................................................................................11

Assumptions for break even point.............................................................................................12

Conclusion ....................................................................................................................................13

REFERENC...................................................................................................................................14

INTRODUCTION

Budget is the financial plan which is being prepared by any organisation to know future

expenses and by making proper budget organisation may attain the pre- determined goal and

financial control is the procedure of making budget for a specified time duration and the

organisation can compare the actual performance with the standard performance (Drahos, 2017).

This report is based on National health services which is located in UK and It is publicly funded

health care. This report states about the legal, financial environment of the health and social

care. Also it speaks about the various funding options such as private finance initiatives, agency

partnership, competitive tendering. Agency theory is also mentioned in this report. Impact of

cash budgeting is elaborated in this report. Break even point is also mentioned in this report.

Question 1

A Legal, financial and regulatory environment of health and social care

The legal regulatory for health and social care is that they have to protect people at work

and also organisation have to be take care about work activities done by the employees. Legal

rules and regulatory involves the protection of health and safety of the people who are working

in the organisation (Stephan and et.al, 2018). The financial regulatory of health and social care

is concern with making proper plan and policies of the organisation so that they may purchase

the necessary tools and equipments. Health and social care uses heath financing so that they can

give better treatment to the patients by using technology. Apart from this, if the organisation

has properly maintain its machinery and equipments so that the employees also do not get harm

by using such machinery and equipments and also they may offer best services to the patients.

Health financing is useful for the protection of health of workers as per the lows and regulations,

organisation provides proper training and development to the employees so that they know how

to use tools and equipments properly. To manage the finance in heath and social care they need

fund from various sources of funds, through collecting funds from the government and also

from various different schemes and directly payment out of the pocket from the patients.

Budget is the financial plan which is being prepared by any organisation to know future

expenses and by making proper budget organisation may attain the pre- determined goal and

financial control is the procedure of making budget for a specified time duration and the

organisation can compare the actual performance with the standard performance (Drahos, 2017).

This report is based on National health services which is located in UK and It is publicly funded

health care. This report states about the legal, financial environment of the health and social

care. Also it speaks about the various funding options such as private finance initiatives, agency

partnership, competitive tendering. Agency theory is also mentioned in this report. Impact of

cash budgeting is elaborated in this report. Break even point is also mentioned in this report.

Question 1

A Legal, financial and regulatory environment of health and social care

The legal regulatory for health and social care is that they have to protect people at work

and also organisation have to be take care about work activities done by the employees. Legal

rules and regulatory involves the protection of health and safety of the people who are working

in the organisation (Stephan and et.al, 2018). The financial regulatory of health and social care

is concern with making proper plan and policies of the organisation so that they may purchase

the necessary tools and equipments. Health and social care uses heath financing so that they can

give better treatment to the patients by using technology. Apart from this, if the organisation

has properly maintain its machinery and equipments so that the employees also do not get harm

by using such machinery and equipments and also they may offer best services to the patients.

Health financing is useful for the protection of health of workers as per the lows and regulations,

organisation provides proper training and development to the employees so that they know how

to use tools and equipments properly. To manage the finance in heath and social care they need

fund from various sources of funds, through collecting funds from the government and also

from various different schemes and directly payment out of the pocket from the patients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Another thing which is being used by the health care is that they collect fund from high net worth

individual and those people who are from lower middle income group. This can be the direct

income of the organisation which they get from such patients in the form of fees and charges

which they charge from their patients by giving them proper health care services. But the funds

and finance of the organisation depends on the country as well if the organisation is situated at

the developed country it may easy for them to gather funds from various sources and on the flip

side if the organisation is located in such country which is financially weak it may become

difficult for the organisation to collect fund thus they provide poor services to the patients as they

do not have money to buy machinery and necessary tools.

B Use of funding options

Private Finance Initiative

Private finance initiative as the name suggest, it is one of the way to finance public

sector organisation and projects through private sector (Kuluski and et.al, 2017). It is one of the

important and controversial method of collecting fund from the public in the form of tax so it is

an unnecessary burden on the general pubic. Because the PFI alleviate on the government and

public, to gain the fund, this public sector projects gather money from only those people who are

the regular payer of tax. In this method, any private company handles the cost instead of

government and private companies manage all the collected fund in the appropriate manner.

Agency partnership

Agency partnership is one of the most dynamic and effective way of collecting and

gathering the fund so that the government can allocate funds to the government so that they may

provide better services to the customer and patient (Regenstein and et.al, 2018). As the name

suggest, in the agency partnership, this government projects do partnership with big name and

famed agencies who collect the fund on the behalf of the government and manages the entire

business and aft6er collecting the fund these agencies distributes the funds in different

departments of the organisation. But the agency have to make sure that they do not distribute the

funds in a wrong manner so that no body can misuse such funds.

Competitive tendering

This is one of the popular method of collecting fund for the government project and

organisation. It is known to be the bidding system in which the investor and big organisation

bid for the higher they will purchase the government debt (Huggett, , 2020.). It is similar to the

individual and those people who are from lower middle income group. This can be the direct

income of the organisation which they get from such patients in the form of fees and charges

which they charge from their patients by giving them proper health care services. But the funds

and finance of the organisation depends on the country as well if the organisation is situated at

the developed country it may easy for them to gather funds from various sources and on the flip

side if the organisation is located in such country which is financially weak it may become

difficult for the organisation to collect fund thus they provide poor services to the patients as they

do not have money to buy machinery and necessary tools.

B Use of funding options

Private Finance Initiative

Private finance initiative as the name suggest, it is one of the way to finance public

sector organisation and projects through private sector (Kuluski and et.al, 2017). It is one of the

important and controversial method of collecting fund from the public in the form of tax so it is

an unnecessary burden on the general pubic. Because the PFI alleviate on the government and

public, to gain the fund, this public sector projects gather money from only those people who are

the regular payer of tax. In this method, any private company handles the cost instead of

government and private companies manage all the collected fund in the appropriate manner.

Agency partnership

Agency partnership is one of the most dynamic and effective way of collecting and

gathering the fund so that the government can allocate funds to the government so that they may

provide better services to the customer and patient (Regenstein and et.al, 2018). As the name

suggest, in the agency partnership, this government projects do partnership with big name and

famed agencies who collect the fund on the behalf of the government and manages the entire

business and aft6er collecting the fund these agencies distributes the funds in different

departments of the organisation. But the agency have to make sure that they do not distribute the

funds in a wrong manner so that no body can misuse such funds.

Competitive tendering

This is one of the popular method of collecting fund for the government project and

organisation. It is known to be the bidding system in which the investor and big organisation

bid for the higher they will purchase the government debt (Huggett, , 2020.). It is similar to the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

auction process. The main motive of this tendering system is to fulfil the cost of the government

and the main motive of governments is to collect more and more fund so that they can buy all

the machineries and equipments which is necessary for the success of the organisation and

project.

C Agency theory

The efficiency of health and social care has been a political issue in many countries and

now the government of UK has categorised the health care in to agency network, which means

that government has given the contract of one or group of persons who is known ton agent to

perform all the activities and services in the NHS on the behalf of the government (Buchanan,

2020). But government plays the role of principal and other person plays a role of agent. The

main reason behind using agency theory in the NHS is that government is not able to keep an eye

on he activities so they hire agent who will work for the welfare and development of the health

care and give preference to the needs of the patient and patients and they get the best treatment

which they are looking for.

Importance of agency theory

This theory has become a need for NHS, as in the absence of proper communication with

the stakeholders and also government is not able to check the status of NHS so this theory has

been come into action. As the agent is always there in the organisation to sort out the problem

faced by the employees and also it may give solution to the problems and queries of patients if

they do not get the treatment as per their preference.

Ways of communication with stakeholders

Stakeholders are the one who have keen interest in the organisation , they can be –

employees, investors, and customers (Sussex and et.al, 2019). It is very necessary for the

organisation that they communicate with the stakeholders.

Sent out a news letter

NHS should send a news letter to the stakeholders so that they know what extra this

organisation is doing and what new NHS is going to launch, so this new have to be sent to

stakeholders on quarterly and annually basis.

Schedule a meeting

It is the another way to communicate with the stakeholders by conducting a meeting with

them so that the stakeholder may know that what are the future goals of the NHS and what extra

and the main motive of governments is to collect more and more fund so that they can buy all

the machineries and equipments which is necessary for the success of the organisation and

project.

C Agency theory

The efficiency of health and social care has been a political issue in many countries and

now the government of UK has categorised the health care in to agency network, which means

that government has given the contract of one or group of persons who is known ton agent to

perform all the activities and services in the NHS on the behalf of the government (Buchanan,

2020). But government plays the role of principal and other person plays a role of agent. The

main reason behind using agency theory in the NHS is that government is not able to keep an eye

on he activities so they hire agent who will work for the welfare and development of the health

care and give preference to the needs of the patient and patients and they get the best treatment

which they are looking for.

Importance of agency theory

This theory has become a need for NHS, as in the absence of proper communication with

the stakeholders and also government is not able to check the status of NHS so this theory has

been come into action. As the agent is always there in the organisation to sort out the problem

faced by the employees and also it may give solution to the problems and queries of patients if

they do not get the treatment as per their preference.

Ways of communication with stakeholders

Stakeholders are the one who have keen interest in the organisation , they can be –

employees, investors, and customers (Sussex and et.al, 2019). It is very necessary for the

organisation that they communicate with the stakeholders.

Sent out a news letter

NHS should send a news letter to the stakeholders so that they know what extra this

organisation is doing and what new NHS is going to launch, so this new have to be sent to

stakeholders on quarterly and annually basis.

Schedule a meeting

It is the another way to communicate with the stakeholders by conducting a meeting with

them so that the stakeholder may know that what are the future goals of the NHS and what extra

they have to give to the stakeholder so that they do not have to face any kind of issues within in

the company (Jordev, 2020).

Question 2

A Impact of financial constraints, cost and budget of health and social care services

Financial constraints refers to the factors which put restriction on the quality of investment

options which is available for the investor (Watkins and et.al, 2017). These factors could be

internal and external which is being consider of internal constraints like lack of knowledge and

poor cash flows. In the area of health care, if they face financial constraints it directly impacts

the services given by the health care to its patient. The key role of finance in the health care

system is to plan, acquire and use the resources to increase the efficiency of the organisation.

The major role of financial constraints is to specify activities like planning and budgeting when

the organisation make proper planning and budgeting about the cost and expenses then only they

can provide proper health care services to its patients. Cost and budget are fully different term,

as budget refers the money available with the organisation which they are going to spend over

a time period, specially on a specific time period. Cost is majorly concern with the expenses

which is going to occur and bear by the organisation. So budget is a tool which is being used

by the organisation for planning and controlling the financial resources of the organisation.

Budget is being made only by knowing the priorities of the organisation, they may make budgets

and although as per the budget they think to provide services to their patients apart from this,

NHS is a publicly funded organisation and they have to make sure that they must provide good

and better services to its customer so they may get best services which is not possible for them to

get it from other health care. But this can only possible when they prepare financial budget as

per the needs. The major financial constraints which put the NHS in limelight and controversies

is that they were not having proper budget and cost planning thus it is not possible for them to

pay salary on time to their employees in result this organisation is facing employee turnover and

organisation cant provide proper treatment in the situations of emergency specially in the

pandemic (Blecher and et.al, 2017). This organisation was running short of employees and staff.

In result all patience were not getting proper treatment at time although organisation was not

the company (Jordev, 2020).

Question 2

A Impact of financial constraints, cost and budget of health and social care services

Financial constraints refers to the factors which put restriction on the quality of investment

options which is available for the investor (Watkins and et.al, 2017). These factors could be

internal and external which is being consider of internal constraints like lack of knowledge and

poor cash flows. In the area of health care, if they face financial constraints it directly impacts

the services given by the health care to its patient. The key role of finance in the health care

system is to plan, acquire and use the resources to increase the efficiency of the organisation.

The major role of financial constraints is to specify activities like planning and budgeting when

the organisation make proper planning and budgeting about the cost and expenses then only they

can provide proper health care services to its patients. Cost and budget are fully different term,

as budget refers the money available with the organisation which they are going to spend over

a time period, specially on a specific time period. Cost is majorly concern with the expenses

which is going to occur and bear by the organisation. So budget is a tool which is being used

by the organisation for planning and controlling the financial resources of the organisation.

Budget is being made only by knowing the priorities of the organisation, they may make budgets

and although as per the budget they think to provide services to their patients apart from this,

NHS is a publicly funded organisation and they have to make sure that they must provide good

and better services to its customer so they may get best services which is not possible for them to

get it from other health care. But this can only possible when they prepare financial budget as

per the needs. The major financial constraints which put the NHS in limelight and controversies

is that they were not having proper budget and cost planning thus it is not possible for them to

pay salary on time to their employees in result this organisation is facing employee turnover and

organisation cant provide proper treatment in the situations of emergency specially in the

pandemic (Blecher and et.al, 2017). This organisation was running short of employees and staff.

In result all patience were not getting proper treatment at time although organisation was not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

having proper machinery and tools so that they can provide proper treatment to the patient.

Situation like this arise just because the health care were not properly make budget for the

expenses and how they will buy necessary equipments and tools. Budget make sure about the

current performance of the business and is consistency with the goal and plans of the

organisation. So the impact of budget and cost in health care organisation is must as w with the

help of budget, health care organisation may know how much funds they have to spent on

projects and different tools and section and how much fund have to be allocated on different

equipments so that they may provide best treatment to the patients (Cookson and et.al, 2017). To

make budget, this organisation is dependent on the fund which is being given by the government

and in the form of the donation from public and other high net worth individual. But NHS have

to ensure that budget must be prepare as per time. It can be long term , short term and medium

term in nature. Another thing which is necessary to ensure that budget can be classified in two

sections first is fixed budget and flexible budget. The another thing which can be ensure while

creating a budget is that they have to be analysed first , and make proper planning about the

budget then the organisation should implement such budget then only the health care will get

benefit from the budget and cost. On the other hand, the financial constraints must be implied in

the health care and it has to be properly managed then only it can provide benefits the

organisation.

B challenges of budgeting in public sector organisations

Budget refers to be the estimation of revenue and expenditure for a specified future

period of time and usually it is concern on the periodic budget (Malbon and et.al, 2019). But

now this budgeting has become a challenge specially for the public sector organisation as they

do not have proper availability of the fund because they relied on the government and public for

funds and money. There are some big health care organisations which are facing budget issues

and challenges such as NHS and department of health and social care.

Inaccuracy

The common challenge and issues faced by the organisation is inaccuracy as the

budgeting take place on the assumptions only, which can give some disadvantage to the

organisation if the environment of the organisation changes frequently, the budgeting can get

failed in such situation and organisation may face loss. Apart from this it can be possible that the

revenue structure of the company may change very often this can impact the entire budget of the

Situation like this arise just because the health care were not properly make budget for the

expenses and how they will buy necessary equipments and tools. Budget make sure about the

current performance of the business and is consistency with the goal and plans of the

organisation. So the impact of budget and cost in health care organisation is must as w with the

help of budget, health care organisation may know how much funds they have to spent on

projects and different tools and section and how much fund have to be allocated on different

equipments so that they may provide best treatment to the patients (Cookson and et.al, 2017). To

make budget, this organisation is dependent on the fund which is being given by the government

and in the form of the donation from public and other high net worth individual. But NHS have

to ensure that budget must be prepare as per time. It can be long term , short term and medium

term in nature. Another thing which is necessary to ensure that budget can be classified in two

sections first is fixed budget and flexible budget. The another thing which can be ensure while

creating a budget is that they have to be analysed first , and make proper planning about the

budget then the organisation should implement such budget then only the health care will get

benefit from the budget and cost. On the other hand, the financial constraints must be implied in

the health care and it has to be properly managed then only it can provide benefits the

organisation.

B challenges of budgeting in public sector organisations

Budget refers to be the estimation of revenue and expenditure for a specified future

period of time and usually it is concern on the periodic budget (Malbon and et.al, 2019). But

now this budgeting has become a challenge specially for the public sector organisation as they

do not have proper availability of the fund because they relied on the government and public for

funds and money. There are some big health care organisations which are facing budget issues

and challenges such as NHS and department of health and social care.

Inaccuracy

The common challenge and issues faced by the organisation is inaccuracy as the

budgeting take place on the assumptions only, which can give some disadvantage to the

organisation if the environment of the organisation changes frequently, the budgeting can get

failed in such situation and organisation may face loss. Apart from this it can be possible that the

revenue structure of the company may change very often this can impact the entire budget of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. So inaccuracy has become a big challenge in front of the organisation. Another

thing which can impact the budget is economic downturn, the biggest example of economic

downturn which every organisation faces during the proliferation of Covid 19, in this pandemic

the entire budget of the the public healthcare organisation get failed, as they were not having

proper equipments and tools through which they may provide bets treatment to the patients, as

the budget of these organisations got failed in result they were not having proper funds , these

organisations were not able to pay salary to its staff which was a biggest example of budget

failure.

Requirement of time

Time is a very important constraints for making a budget and on the same time it is one

of the challenge which is being faced by the organisations (Ibrahim and et.al, 2017). It

becomes one of the lengthy process when the environment of the organisation is poorly

organised, it takes lot of time when the organisation is weak in making budget. But some good

organisations uses budgeting software which provides them better result in less time. But this

organisations are public health care and do not uses any kind of software in result the budget

making process becomes time consuming for them. So this are one of the big challenge which is

being faced by the organisations.

Allocation of expenses

The main objective behind making budget is that organisation wants to allocate and

distribute the fund to different resources and department so the organisation may face the

challenges of the organisation. As NHS and Department of health and social care are one of the

big organisations and they have to allocate funds to each and every department and which is only

possible when the organisation properly manage the budget for every department.

Right budgeting tool

Many of the challenges which takes place due to inappropriate tools have been selected

by the organisations (Ouassini, 2018). To make good budget organisation must be sure about the

tools which can give them proper and correct result which helps the organisation and also the

organisation have to be make sure that the budgeting tool must be useful for other departments

and tools as well. To avoid this challenge, organisations must use technology which will help

the organisation to get faster result and also the organisation will save extra money and time,

and the chances of miscommunication will decrease and also the organisation can provide better

thing which can impact the budget is economic downturn, the biggest example of economic

downturn which every organisation faces during the proliferation of Covid 19, in this pandemic

the entire budget of the the public healthcare organisation get failed, as they were not having

proper equipments and tools through which they may provide bets treatment to the patients, as

the budget of these organisations got failed in result they were not having proper funds , these

organisations were not able to pay salary to its staff which was a biggest example of budget

failure.

Requirement of time

Time is a very important constraints for making a budget and on the same time it is one

of the challenge which is being faced by the organisations (Ibrahim and et.al, 2017). It

becomes one of the lengthy process when the environment of the organisation is poorly

organised, it takes lot of time when the organisation is weak in making budget. But some good

organisations uses budgeting software which provides them better result in less time. But this

organisations are public health care and do not uses any kind of software in result the budget

making process becomes time consuming for them. So this are one of the big challenge which is

being faced by the organisations.

Allocation of expenses

The main objective behind making budget is that organisation wants to allocate and

distribute the fund to different resources and department so the organisation may face the

challenges of the organisation. As NHS and Department of health and social care are one of the

big organisations and they have to allocate funds to each and every department and which is only

possible when the organisation properly manage the budget for every department.

Right budgeting tool

Many of the challenges which takes place due to inappropriate tools have been selected

by the organisations (Ouassini, 2018). To make good budget organisation must be sure about the

tools which can give them proper and correct result which helps the organisation and also the

organisation have to be make sure that the budgeting tool must be useful for other departments

and tools as well. To avoid this challenge, organisations must use technology which will help

the organisation to get faster result and also the organisation will save extra money and time,

and the chances of miscommunication will decrease and also the organisation can provide better

treatment to the patients. So by selecting the right budgeting tool, employees can also help the

employees so that they may know the invoicing and payroll opportunity, this will assist the

organisation to sort out any kind of issue.

Goal setting

The another challenge which is being faced by the organisation while making budgetary

is that they do not involve entire team in it. As it is a public organisations so they do not give

much importance to the their team, thus they do not involve the entire team in result organisation

make wrong budget hence the organisation do not get proper result which they expecting.

C Advantages and disadvantage of incremental and Zero based budgeting

Incremental budgeting

Incremental budgeting is refers to traditional budgeting method in which the budget is

made on the basis of current period budget and actual performance which is being taken as the

base which is needed in making new budget (Kang and et.al, 2020). Basically incremental

budget uses the budget of previous years or on the basis of actual performance and the

incremental amount added to the new budget.

Advantage of Incremental budgeting

Simplicity

Increment budgeting is one of the simplest and easiest approach that's why it is used for

the forecasting of future expenses and future projects. This approach do not require any kind of

complex calculations and only needs few assumptions in which the entire budget get prepared.

Funding

Incremental budgeting ensure that funding must remain n stable over the passage of time

this is most suitable for those organisations who haven projects for long run and they require

funding for long term.

Disadvantages of Incremental budgeting

Promote extra spendings

Incremental budgeting promotes unnecessary spending for the company the main reason

which has been found is that whenever any organisation allocate fund to other departments they

try to use all the funds which has been allocated to them.

Lack of innovation

employees so that they may know the invoicing and payroll opportunity, this will assist the

organisation to sort out any kind of issue.

Goal setting

The another challenge which is being faced by the organisation while making budgetary

is that they do not involve entire team in it. As it is a public organisations so they do not give

much importance to the their team, thus they do not involve the entire team in result organisation

make wrong budget hence the organisation do not get proper result which they expecting.

C Advantages and disadvantage of incremental and Zero based budgeting

Incremental budgeting

Incremental budgeting is refers to traditional budgeting method in which the budget is

made on the basis of current period budget and actual performance which is being taken as the

base which is needed in making new budget (Kang and et.al, 2020). Basically incremental

budget uses the budget of previous years or on the basis of actual performance and the

incremental amount added to the new budget.

Advantage of Incremental budgeting

Simplicity

Increment budgeting is one of the simplest and easiest approach that's why it is used for

the forecasting of future expenses and future projects. This approach do not require any kind of

complex calculations and only needs few assumptions in which the entire budget get prepared.

Funding

Incremental budgeting ensure that funding must remain n stable over the passage of time

this is most suitable for those organisations who haven projects for long run and they require

funding for long term.

Disadvantages of Incremental budgeting

Promote extra spendings

Incremental budgeting promotes unnecessary spending for the company the main reason

which has been found is that whenever any organisation allocate fund to other departments they

try to use all the funds which has been allocated to them.

Lack of innovation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This type of budgeting process do not promote innovation and also do not consider new

ideas and growth in the company. As the new budget is also based on the old budget thus this

process discourages the usage and implementation of new ideas in the organisational

environment.

Lack of incentives

When the company uses incremental budget it does not give and provide any kind of

incentive to the company and its management, there for the management of the organisation also

review this budget (Prabowo and et.al, 2017). The lack of review system makes the budget

waste and inadequate assumptions and lead to mistakes as well.

Zero based budget

This is a tool and approach which makes a budget from scratches. This budget do not

uses previous and past budgets. As the name suggest this budget begin from zero. When any

organisation go for zero based budgeting, they need to make justification for every expenses

before they mention this in to the official budget. The major goal behind preparing this budget

is to cut out the extra cost wherever company can cut. In the preparation of this budget

organisation sometimes includes employees as well so that they will make accurate budget for

the organisation.

Advantages of Zero based budgeting

Cost – benefit analysis

This is one of the biggest advantage of zero based budgeting as the every item and

equipments get justified when the organisation prepares budget. So with the help of analysis

zeros based budgeting provides cost saving benefits to the organisation. It leads the organisation

on the way of cost saving.

Promote optimisation

This budgeting focuses only on those items which directly benefits the business

and provide more value, greater efficiency and cost reduction as well. With the help of this

budgeting tool organisation get the continuous improvement in the orgabnsiation.

Disadvantage of Zero based budgeting

Complex procedure

It is not same like traditional budgeting, zero based budgeting is quite expensive and

costly and along with this, it is time consuming as well (Ab and et.al, 2018). It needs extra

ideas and growth in the company. As the new budget is also based on the old budget thus this

process discourages the usage and implementation of new ideas in the organisational

environment.

Lack of incentives

When the company uses incremental budget it does not give and provide any kind of

incentive to the company and its management, there for the management of the organisation also

review this budget (Prabowo and et.al, 2017). The lack of review system makes the budget

waste and inadequate assumptions and lead to mistakes as well.

Zero based budget

This is a tool and approach which makes a budget from scratches. This budget do not

uses previous and past budgets. As the name suggest this budget begin from zero. When any

organisation go for zero based budgeting, they need to make justification for every expenses

before they mention this in to the official budget. The major goal behind preparing this budget

is to cut out the extra cost wherever company can cut. In the preparation of this budget

organisation sometimes includes employees as well so that they will make accurate budget for

the organisation.

Advantages of Zero based budgeting

Cost – benefit analysis

This is one of the biggest advantage of zero based budgeting as the every item and

equipments get justified when the organisation prepares budget. So with the help of analysis

zeros based budgeting provides cost saving benefits to the organisation. It leads the organisation

on the way of cost saving.

Promote optimisation

This budgeting focuses only on those items which directly benefits the business

and provide more value, greater efficiency and cost reduction as well. With the help of this

budgeting tool organisation get the continuous improvement in the orgabnsiation.

Disadvantage of Zero based budgeting

Complex procedure

It is not same like traditional budgeting, zero based budgeting is quite expensive and

costly and along with this, it is time consuming as well (Ab and et.al, 2018). It needs extra

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

training which include new software and workflows then only this budget can be prepared. So

expenses and time consumption are the drawback of this method.

Disruptive process

It is a disruptive process, because whenever orgabnsiation wants to make changes in this

budget it takes a lot of time and entire management have to face extra cost. In the area of

disruption can impact then brand value and reputation of the organisation, and also it put

negative impact on the customer experience as well.

Question 3

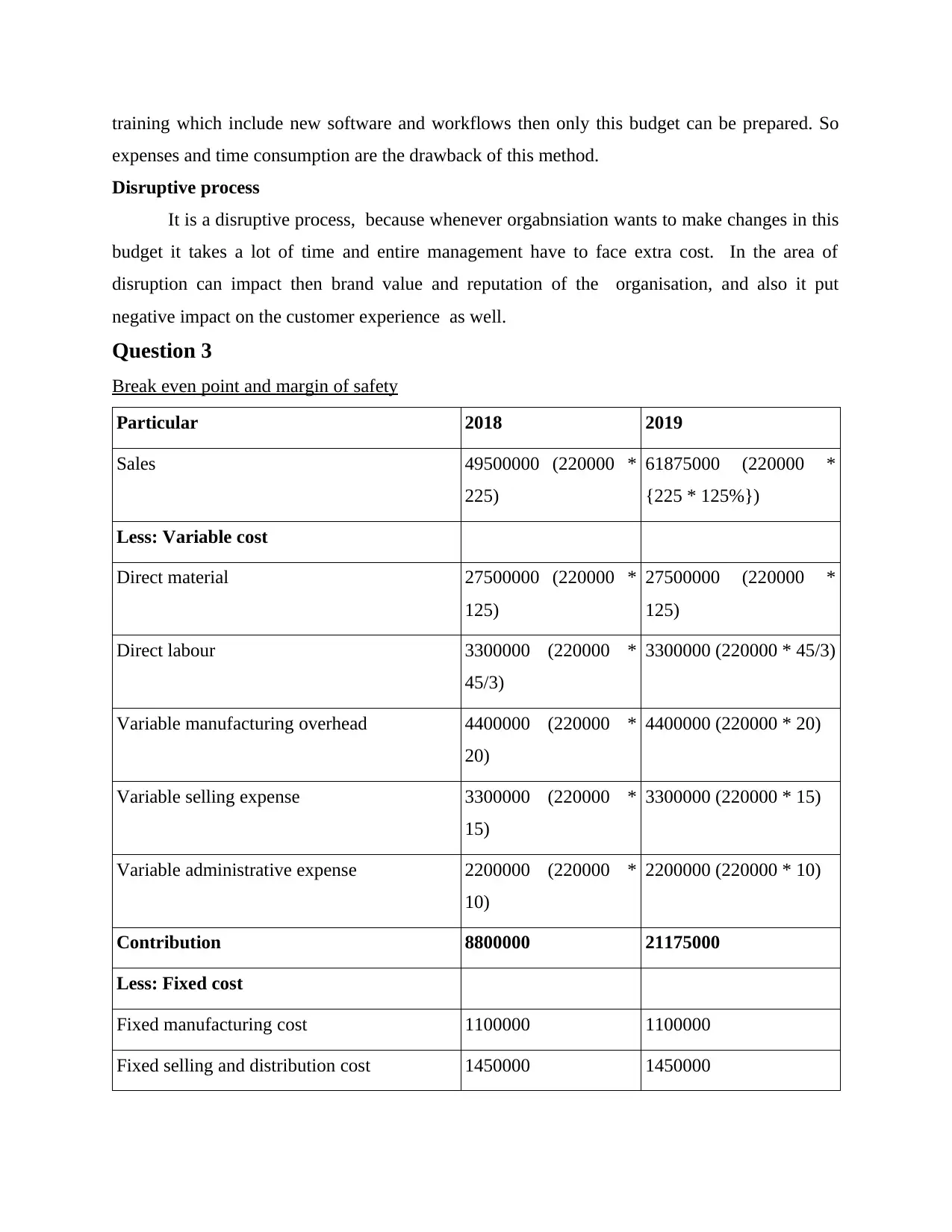

Break even point and margin of safety

Particular 2018 2019

Sales 49500000 (220000 *

225)

61875000 (220000 *

{225 * 125%})

Less: Variable cost

Direct material 27500000 (220000 *

125)

27500000 (220000 *

125)

Direct labour 3300000 (220000 *

45/3)

3300000 (220000 * 45/3)

Variable manufacturing overhead 4400000 (220000 *

20)

4400000 (220000 * 20)

Variable selling expense 3300000 (220000 *

15)

3300000 (220000 * 15)

Variable administrative expense 2200000 (220000 *

10)

2200000 (220000 * 10)

Contribution 8800000 21175000

Less: Fixed cost

Fixed manufacturing cost 1100000 1100000

Fixed selling and distribution cost 1450000 1450000

expenses and time consumption are the drawback of this method.

Disruptive process

It is a disruptive process, because whenever orgabnsiation wants to make changes in this

budget it takes a lot of time and entire management have to face extra cost. In the area of

disruption can impact then brand value and reputation of the organisation, and also it put

negative impact on the customer experience as well.

Question 3

Break even point and margin of safety

Particular 2018 2019

Sales 49500000 (220000 *

225)

61875000 (220000 *

{225 * 125%})

Less: Variable cost

Direct material 27500000 (220000 *

125)

27500000 (220000 *

125)

Direct labour 3300000 (220000 *

45/3)

3300000 (220000 * 45/3)

Variable manufacturing overhead 4400000 (220000 *

20)

4400000 (220000 * 20)

Variable selling expense 3300000 (220000 *

15)

3300000 (220000 * 15)

Variable administrative expense 2200000 (220000 *

10)

2200000 (220000 * 10)

Contribution 8800000 21175000

Less: Fixed cost

Fixed manufacturing cost 1100000 1100000

Fixed selling and distribution cost 1450000 1450000

Fixed administrative 675000 675000

Additional fixed cost 1450000

Profit 5575000 16500000

Break even point (BEP In Units):

Fixed cost / contribution per unit

2018

= 3225000 (1100000 + 1450000 + 675000) / 40 (8800000 / 220000)

= 80625 Units

BEP (in amount): 80625 * 225

= 18140625

2019

= 4675000 (1100000 + 1450000 + 675000 + 1450000) / 96.25 (21175000 / 220000)

= 48571 Units

BEP (In amount):

48571 * 281.25 (225 * 125%)

= 13660594

Margin of safety sale: Current sale - Break even point sale

2018 = 49500000 – 18140625

= 31359375

2019 = 61875000 – 13660594

= 48214406

It can demonstrate that the result stated above denote that company could address better

break even point as compare to the previous financial year. The modification also denote the

increase in sales price that also favoured the business entity in its sales that further increased the

break even point for the respective entity (Verhougstraete and et.al., 2019). Margin safety of sale

in the year 2019 is also increased due to the increased sale price of company in the respective

financial year. This all denotes that company could entertain better performance under the

respective financial year.

Additional fixed cost 1450000

Profit 5575000 16500000

Break even point (BEP In Units):

Fixed cost / contribution per unit

2018

= 3225000 (1100000 + 1450000 + 675000) / 40 (8800000 / 220000)

= 80625 Units

BEP (in amount): 80625 * 225

= 18140625

2019

= 4675000 (1100000 + 1450000 + 675000 + 1450000) / 96.25 (21175000 / 220000)

= 48571 Units

BEP (In amount):

48571 * 281.25 (225 * 125%)

= 13660594

Margin of safety sale: Current sale - Break even point sale

2018 = 49500000 – 18140625

= 31359375

2019 = 61875000 – 13660594

= 48214406

It can demonstrate that the result stated above denote that company could address better

break even point as compare to the previous financial year. The modification also denote the

increase in sales price that also favoured the business entity in its sales that further increased the

break even point for the respective entity (Verhougstraete and et.al., 2019). Margin safety of sale

in the year 2019 is also increased due to the increased sale price of company in the respective

financial year. This all denotes that company could entertain better performance under the

respective financial year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.