Evaluating Financial Control, Budgeting, and Stakeholder Interaction

VerifiedAdded on 2023/06/13

|15

|4715

|484

Portfolio

AI Summary

This portfolio provides a comprehensive analysis of financial control within the health and social care sector, covering legal, regulatory, and fiscal environments. It evaluates funding options, explores the agency theory in the context of the NHS, and discusses stakeholder interactions. The impact of financial limitations, expenses, and budgets on health and social sector managers is critically examined, along with the challenges of budgeting in public sector organizations. The document also determines the pros and cons of incremental and zero-based budgeting, computes breakeven points and safety margins for specified years, and discusses assumptions related to the breakeven model. Desklib offers this assignment as a resource, providing students with valuable study tools and solved assignments.

Assessment Type

Portfolio of Tasks

Portfolio of Tasks

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

a) Analyse critically the legal, regulatory and fiscal environment of health and social care.4

b) Evaluate critically the utilisation of funding options in the health and social care sector.5

c) In the framework of budgeting, elaborate the agency theory in the context of the NHS

and major ways of interacting with stakeholders...................................................................6

TASK 2......................................................................................................................................6

a) Discuss critically the impact of financial limitations, expenses, and budgets have a

significant impact on health and social sector managers.......................................................6

b) Explain the challenges of budgeting in the public sector organisations............................8

c) Determine the pros and cons of incremental and zero based budgeting............................9

TASK 3....................................................................................................................................12

a) Compute the breakeven point and safety margin for the years 2018 and 2019...............12

b) Discuss the assumption that can be taken in the breakeven model by pointing out the

reality of today’s business environment...............................................................................15

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

INTRODUCTION......................................................................................................................4

TASK 1......................................................................................................................................4

a) Analyse critically the legal, regulatory and fiscal environment of health and social care.4

b) Evaluate critically the utilisation of funding options in the health and social care sector.5

c) In the framework of budgeting, elaborate the agency theory in the context of the NHS

and major ways of interacting with stakeholders...................................................................6

TASK 2......................................................................................................................................6

a) Discuss critically the impact of financial limitations, expenses, and budgets have a

significant impact on health and social sector managers.......................................................6

b) Explain the challenges of budgeting in the public sector organisations............................8

c) Determine the pros and cons of incremental and zero based budgeting............................9

TASK 3....................................................................................................................................12

a) Compute the breakeven point and safety margin for the years 2018 and 2019...............12

b) Discuss the assumption that can be taken in the breakeven model by pointing out the

reality of today’s business environment...............................................................................15

CONCLUSION........................................................................................................................15

REFERENCES.........................................................................................................................16

INTRODUCTION

Financial control is a process which involves policies, methods and procedures that

are sued by the organisation to keep a control on financial services. Every organisation is a

have limited resources and every resources have various uses. Budget helps in estimating the

revenue that the organisation will earn and expenses to be incurred during the year (Ayoobi

and et.al., 2021). The following report is divided into three parts. That includes financial,

legal and regulatory framework of social care and health. There are many options for

business funding such as Private Finance Initiatives (PFI), competitive, partnership,

outsourcing and tendering with respect to health care and social factors. A brief summary of

the agency theory is also included, which would be an agreement between one or more

people to execute services on behalf of a person. The public sector is confronted with a

number of budgeting issues. Budgeting can be done in a variety of ways, including zero-

based budgeting and incremental budgeting. The pros and downsides of zero-based and

incremental budgeting are discussed. Task three entails calculating the breakeven point and

margin of safety for the previous two years. At the end, different assumptions connected to

the breakeven model are included.

TASK 1

a) Analyse critically the legal, regulatory and fiscal environment of health and social care.

The services offered by the Ministry of Health in the United Kingdom are referred to

as health and social care. The legal environment is a set of written documents that comprises

the laws, laws and regulations, guidelines, and agreements in every economy. The financial

framework consists of rules and strategies for the fiscal reporting of a specific industry or

sector. The regulatory environment is concerned with the firm's legal framework as a whole.

The numerous frameworks in the area of health and social care can be elaborated as follows:

Legal environment of health and social care:

The Care Act of 2014 is the law that governs social care. There are several additional

legislations that come before this one, such as the National Assistance Act, 1948 and the

NHS Community Act, 1990. The nine acts were consolidated into a single statute known as

the Care Act, 2014. The care act has several functions, which can be summarised as follows:

It ensures that people receive services before their care needs become critical, or it

allows them to postpone their demands (Budding, Faber and Vosselman, 2019).

It aids in the gathering of information necessary to make critical choices about help

and treatment.

It also offers a variety of high-quality and cost-effective services to choose from.

Financial control is a process which involves policies, methods and procedures that

are sued by the organisation to keep a control on financial services. Every organisation is a

have limited resources and every resources have various uses. Budget helps in estimating the

revenue that the organisation will earn and expenses to be incurred during the year (Ayoobi

and et.al., 2021). The following report is divided into three parts. That includes financial,

legal and regulatory framework of social care and health. There are many options for

business funding such as Private Finance Initiatives (PFI), competitive, partnership,

outsourcing and tendering with respect to health care and social factors. A brief summary of

the agency theory is also included, which would be an agreement between one or more

people to execute services on behalf of a person. The public sector is confronted with a

number of budgeting issues. Budgeting can be done in a variety of ways, including zero-

based budgeting and incremental budgeting. The pros and downsides of zero-based and

incremental budgeting are discussed. Task three entails calculating the breakeven point and

margin of safety for the previous two years. At the end, different assumptions connected to

the breakeven model are included.

TASK 1

a) Analyse critically the legal, regulatory and fiscal environment of health and social care.

The services offered by the Ministry of Health in the United Kingdom are referred to

as health and social care. The legal environment is a set of written documents that comprises

the laws, laws and regulations, guidelines, and agreements in every economy. The financial

framework consists of rules and strategies for the fiscal reporting of a specific industry or

sector. The regulatory environment is concerned with the firm's legal framework as a whole.

The numerous frameworks in the area of health and social care can be elaborated as follows:

Legal environment of health and social care:

The Care Act of 2014 is the law that governs social care. There are several additional

legislations that come before this one, such as the National Assistance Act, 1948 and the

NHS Community Act, 1990. The nine acts were consolidated into a single statute known as

the Care Act, 2014. The care act has several functions, which can be summarised as follows:

It ensures that people receive services before their care needs become critical, or it

allows them to postpone their demands (Budding, Faber and Vosselman, 2019).

It aids in the gathering of information necessary to make critical choices about help

and treatment.

It also offers a variety of high-quality and cost-effective services to choose from.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The provision of healthcare is a national responsibility, but social care is a local

responsibility. During the year 2015, the term social care 'percept' was established. It gives

local governments the capacity to boost the council tax by a certain amount. The HRA as

well as the four UK health authorities have created a framework. It's used in the United

Kingdom, Northern Ireland, Scotland, and Wales. The Care Act of 2014, section 111(6) and

(7), comprises all legal prerequisites and encourages the conduct of research.

The regulatory framework for the health and social care industry is as follows:

In order to comply with the rules of the health sector, a number of principles must be

observed. The health and facilities operations are overseen by a number of organisations

(Cagan, 2018). The following is a summary of the regulatory framework in the health and

social care sector:

The United States Environmental Protection Agency (EPA) is responsible for

protecting the environment from different dangerous chemicals. RCRA, CWA, CAA

(clean air act), and FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act) are

some of the integrated acts.

The Joint Commission on Accreditation of Healthcare Organizations (JCAHO) is a

non-profit organisation that accredits It is primarily concerned with the patient's

health and safety.

Health and social care financial framework:

The allocation, procurement, and use of monetary components of the health system

are all part of the funding of health and social care.

WHO meets the financial needs of the health and social care sectors by providing

essential funds for all services.

b) Evaluate critically the utilisation of funding options in the health and social care sector.

To operate the system, every company needs money. Similarly, the healthcare professional

takes resources from a variety of sources. Other than the finances it already has; other

funding choices are extra sources or means of obtaining funds (Chapman, 2018). There are a

variety of funding alternatives, which can be summarised as follows:

Private finance Institutions: These are organisations that are not government-owned or

regulated. The ownership of the shares is not allocated among the several authorities.

Credit availability, mitigating risk, and financial data accuracy are the primary

functions of these commercial institutions. Pershing Square Holdings, RSA Insurance,

responsibility. During the year 2015, the term social care 'percept' was established. It gives

local governments the capacity to boost the council tax by a certain amount. The HRA as

well as the four UK health authorities have created a framework. It's used in the United

Kingdom, Northern Ireland, Scotland, and Wales. The Care Act of 2014, section 111(6) and

(7), comprises all legal prerequisites and encourages the conduct of research.

The regulatory framework for the health and social care industry is as follows:

In order to comply with the rules of the health sector, a number of principles must be

observed. The health and facilities operations are overseen by a number of organisations

(Cagan, 2018). The following is a summary of the regulatory framework in the health and

social care sector:

The United States Environmental Protection Agency (EPA) is responsible for

protecting the environment from different dangerous chemicals. RCRA, CWA, CAA

(clean air act), and FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act) are

some of the integrated acts.

The Joint Commission on Accreditation of Healthcare Organizations (JCAHO) is a

non-profit organisation that accredits It is primarily concerned with the patient's

health and safety.

Health and social care financial framework:

The allocation, procurement, and use of monetary components of the health system

are all part of the funding of health and social care.

WHO meets the financial needs of the health and social care sectors by providing

essential funds for all services.

b) Evaluate critically the utilisation of funding options in the health and social care sector.

To operate the system, every company needs money. Similarly, the healthcare professional

takes resources from a variety of sources. Other than the finances it already has; other

funding choices are extra sources or means of obtaining funds (Chapman, 2018). There are a

variety of funding alternatives, which can be summarised as follows:

Private finance Institutions: These are organisations that are not government-owned or

regulated. The ownership of the shares is not allocated among the several authorities.

Credit availability, mitigating risk, and financial data accuracy are the primary

functions of these commercial institutions. Pershing Square Holdings, RSA Insurance,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

London Stock Exchange Group, and Admiral Group are the major financial

institutions.

Collaborations between agencies: It is an organisation that is not governed by the

government. This is the most adaptive, inclusive, and successful method for

maximising return on investment. It is an independent, multinational communications

business that was established to raise cash for the health and social care industry

(Cheng and et.al., 2019).

Outsourcing: It is the practise of hiring a customer from outside a company to do

certain operational tasks. This type of funding is being used by organisations to cut

labour costs, which include salary, overhead, equipment, and technology. It

contributes to the enterprise's time and cost savings. There are numerous benefits.

c) In the framework of budgeting, elaborate the agency theory in the context of the NHS and

major ways of interacting with stakeholders.

The National Health Service (NHS) is a publicly funded healthcare system. The

national health service is abbreviated as NHB.

There are a variety of ways to communicate with stakeholders, which can be summarised as

follows:

Project Summary Report: It is issued at a predetermined interval, perhaps weekly and

monthly. The plans established by top-level managers or higher officials are included

in this report. It also includes the general scope of the chosen project, such as the

project's problem, suggested remedies, and budgetary findings. Stakeholders gain

from having access to information about the company's strategic and financial plans.

Email, e-newsletter and communication automation: It is a crucial tool for interacting

with stakeholders. It aids in quickly reaching out to stakeholders, and specific budgets

may be given to both external and internal users.

TASK 2

a) Discuss critically the impact of financial limitations, expenses, and budgets have a

significant impact on health and social sector managers.

Financial constraints: It is this feature that limits the quality of a variety of investment

possibilities (Douglas and Overmans, 2020). Financial limitations have a number of

advantages, including policy stability and financial sector reforms.

institutions.

Collaborations between agencies: It is an organisation that is not governed by the

government. This is the most adaptive, inclusive, and successful method for

maximising return on investment. It is an independent, multinational communications

business that was established to raise cash for the health and social care industry

(Cheng and et.al., 2019).

Outsourcing: It is the practise of hiring a customer from outside a company to do

certain operational tasks. This type of funding is being used by organisations to cut

labour costs, which include salary, overhead, equipment, and technology. It

contributes to the enterprise's time and cost savings. There are numerous benefits.

c) In the framework of budgeting, elaborate the agency theory in the context of the NHS and

major ways of interacting with stakeholders.

The National Health Service (NHS) is a publicly funded healthcare system. The

national health service is abbreviated as NHB.

There are a variety of ways to communicate with stakeholders, which can be summarised as

follows:

Project Summary Report: It is issued at a predetermined interval, perhaps weekly and

monthly. The plans established by top-level managers or higher officials are included

in this report. It also includes the general scope of the chosen project, such as the

project's problem, suggested remedies, and budgetary findings. Stakeholders gain

from having access to information about the company's strategic and financial plans.

Email, e-newsletter and communication automation: It is a crucial tool for interacting

with stakeholders. It aids in quickly reaching out to stakeholders, and specific budgets

may be given to both external and internal users.

TASK 2

a) Discuss critically the impact of financial limitations, expenses, and budgets have a

significant impact on health and social sector managers.

Financial constraints: It is this feature that limits the quality of a variety of investment

possibilities (Douglas and Overmans, 2020). Financial limitations have a number of

advantages, including policy stability and financial sector reforms.

Managers Client Stakeholders

Financial constraints The highest level

managers are in charge

of all management

functions such as

planning, organising,

leading, and

controlling. The

highest level managers

are in charge of all

management functions

such as planning,

coordinating, leading,

and controlling. It is

vital to set boundaries

for expenditures or

expenses in the area of

health and social

services. If an

organisation does not

place a ceiling on

overheads, the expense

of health care will rise

unnecessarily.

The primary goal of

the health and social

care industry is to

please the public.

Clients benefit from

budgeting and various

financial statements.

When a company

restricts certain

actions, it benefits a

large number of

customers. The

savings made by the

company benefit a

variety of clients

indirectly (Galarraga

and et.al., 2020).

Stakeholders are those

who are interested in

the corporation and the

tasks it conducts. The

budgetary constraints

reflect the

organization's strategy

of maximising

resource utilisation

and diversifying its

applications in a

profitable manner.

Cost Medical,

psychological health,

and community health

are all included in the

cost of health. In 2019,

the United Kingdom

spent 10.2% of its

GDP on health. It must

properly allocate its

Cost accounting is a

way for determining a

company's overall cost

to its customers. The

client selects the

degree of assistance

they require from the

organisation.

The cost of operation

varies depending on

the complicated

techniques used by the

healthcare industry.

All cost must be

shown in the fiscal

accounts in order for

diverse providers to

Financial constraints The highest level

managers are in charge

of all management

functions such as

planning, organising,

leading, and

controlling. The

highest level managers

are in charge of all

management functions

such as planning,

coordinating, leading,

and controlling. It is

vital to set boundaries

for expenditures or

expenses in the area of

health and social

services. If an

organisation does not

place a ceiling on

overheads, the expense

of health care will rise

unnecessarily.

The primary goal of

the health and social

care industry is to

please the public.

Clients benefit from

budgeting and various

financial statements.

When a company

restricts certain

actions, it benefits a

large number of

customers. The

savings made by the

company benefit a

variety of clients

indirectly (Galarraga

and et.al., 2020).

Stakeholders are those

who are interested in

the corporation and the

tasks it conducts. The

budgetary constraints

reflect the

organization's strategy

of maximising

resource utilisation

and diversifying its

applications in a

profitable manner.

Cost Medical,

psychological health,

and community health

are all included in the

cost of health. In 2019,

the United Kingdom

spent 10.2% of its

GDP on health. It must

properly allocate its

Cost accounting is a

way for determining a

company's overall cost

to its customers. The

client selects the

degree of assistance

they require from the

organisation.

The cost of operation

varies depending on

the complicated

techniques used by the

healthcare industry.

All cost must be

shown in the fiscal

accounts in order for

diverse providers to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

resources so that the

health organization's

efficiency improves.

make investment

decisions.

Budget Managers create

financial budgets that

assist them understand

how much money is

spent on each activity

or assignment. It

assists management in

lowering the expense

of overspending

regions while

widening the range of

underspending areas.

Clients examine the

budget to see if the

firm is on track to

meet the strategic

goals of the company.

It represents the

customers degree of

financial stability.

The firm's major goal

is to involve

stakeholders in the

budgeting process.

Companies, the state,

and other financial

firms are all involved.

It gives the

organisation a loan

after analysing the past

year's budgeting (Goda

and Sawada, 2020).

b) Explain the challenges of budgeting in the public sector organisations.

The process of conceptualising, designing, and budgetary control in an organisation is

referred to as budgeting. It denotes a greater level of accountancy that represents future

actions and has a significant impact on an organization's cash flows. Budgeting has numerous

goals, which can be summarised as follows:

It is critical to forecast future outcomes based on the organization's current

performance in order to keep the company solvent.

Each business needs capital to run its operations, and the budgeting process aids in

determining the financial structure of the company. The percentage of equity and debt

used in the company can help determine the firm's true value. The focus of the

concern might alternatively be on lowering the cost of capital.

The budgeting process aids in the integration of activities across departments and the

achievement of organisational goals (Ho, 2018).

Public organizations are those that are governed and overseen by the governments of a

particular country. The administration of a certain country owns the vast bulk of the stock.

The following are some of the issues that public sector organisations encounter when it

comes to budgeting:

health organization's

efficiency improves.

make investment

decisions.

Budget Managers create

financial budgets that

assist them understand

how much money is

spent on each activity

or assignment. It

assists management in

lowering the expense

of overspending

regions while

widening the range of

underspending areas.

Clients examine the

budget to see if the

firm is on track to

meet the strategic

goals of the company.

It represents the

customers degree of

financial stability.

The firm's major goal

is to involve

stakeholders in the

budgeting process.

Companies, the state,

and other financial

firms are all involved.

It gives the

organisation a loan

after analysing the past

year's budgeting (Goda

and Sawada, 2020).

b) Explain the challenges of budgeting in the public sector organisations.

The process of conceptualising, designing, and budgetary control in an organisation is

referred to as budgeting. It denotes a greater level of accountancy that represents future

actions and has a significant impact on an organization's cash flows. Budgeting has numerous

goals, which can be summarised as follows:

It is critical to forecast future outcomes based on the organization's current

performance in order to keep the company solvent.

Each business needs capital to run its operations, and the budgeting process aids in

determining the financial structure of the company. The percentage of equity and debt

used in the company can help determine the firm's true value. The focus of the

concern might alternatively be on lowering the cost of capital.

The budgeting process aids in the integration of activities across departments and the

achievement of organisational goals (Ho, 2018).

Public organizations are those that are governed and overseen by the governments of a

particular country. The administration of a certain country owns the vast bulk of the stock.

The following are some of the issues that public sector organisations encounter when it

comes to budgeting:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Manual Tasks: With the passage of time, numerous software applications have

emerged to assist with the input of massive volumes of data that are difficult to

manage. In the situation of public entities, the firm is unable to keep up with current

technological advances. To incorporate the data, businesses must hire a large number

of people, and all advanced computations must be performed manually. EPM, which

is a form of software that aids in forecasting, planning, and budgeting, is lacking. As a

result, public sector companies should adopt current software to reduce manual labour

and ensure that data is handled efficiently (Huang, Samali and Li, 2021).

Conventional accounting approaches: Budgeting can be done in a variety of ways,

both modern and old. Traditional budgeting approaches are used by public sector

organisations, such as incremental budgeting, which does not produce a new budget

but only modifies existing adjustments. This problem ignores the precise amount of

rate of return, net cash flows, and profitability of the company.

Budget process challenge: Static budgeting and multi-year financial plans in the

public sector result in a high level of financial and regulatory targets. The emergence

of structural deviations in organisations causes the enterprise's operations to be

misaligned. Budgets become out of balance due to the industry's unpredictable and

highly variable in nature, as well as fluctuations in resource consumption levels. To

address this problem, businesses should regularly revise their budgets by analysing

both internal and external elements.

Inaccurate data and assumptions: Every accounting process necessitates data,

which is comprised of basic facts and figures. The accuracy of data is necessary for

budget implementation. Public organisations struggle to obtain correct data from

many departments, and compiling information from various departmental functions is

a major challenge (Kawatu and Kewo, 2019). Occasionally, the organisation would be

unable to fulfil the budgetary standards. Identifying the expense trend of each

organizational unit is a common activity that causes issues when combining the data

for budgeting purposes.

c) Determine the pros and cons of incremental and zero based budgeting.

Incremental Budgeting: It is a method of budgeting in which updated modifications

are factored into the current budgeted or actual outcomes. There are a number of benefits to

incremental budgeting, which are listed below:

Pros Cons

emerged to assist with the input of massive volumes of data that are difficult to

manage. In the situation of public entities, the firm is unable to keep up with current

technological advances. To incorporate the data, businesses must hire a large number

of people, and all advanced computations must be performed manually. EPM, which

is a form of software that aids in forecasting, planning, and budgeting, is lacking. As a

result, public sector companies should adopt current software to reduce manual labour

and ensure that data is handled efficiently (Huang, Samali and Li, 2021).

Conventional accounting approaches: Budgeting can be done in a variety of ways,

both modern and old. Traditional budgeting approaches are used by public sector

organisations, such as incremental budgeting, which does not produce a new budget

but only modifies existing adjustments. This problem ignores the precise amount of

rate of return, net cash flows, and profitability of the company.

Budget process challenge: Static budgeting and multi-year financial plans in the

public sector result in a high level of financial and regulatory targets. The emergence

of structural deviations in organisations causes the enterprise's operations to be

misaligned. Budgets become out of balance due to the industry's unpredictable and

highly variable in nature, as well as fluctuations in resource consumption levels. To

address this problem, businesses should regularly revise their budgets by analysing

both internal and external elements.

Inaccurate data and assumptions: Every accounting process necessitates data,

which is comprised of basic facts and figures. The accuracy of data is necessary for

budget implementation. Public organisations struggle to obtain correct data from

many departments, and compiling information from various departmental functions is

a major challenge (Kawatu and Kewo, 2019). Occasionally, the organisation would be

unable to fulfil the budgetary standards. Identifying the expense trend of each

organizational unit is a common activity that causes issues when combining the data

for budgeting purposes.

c) Determine the pros and cons of incremental and zero based budgeting.

Incremental Budgeting: It is a method of budgeting in which updated modifications

are factored into the current budgeted or actual outcomes. There are a number of benefits to

incremental budgeting, which are listed below:

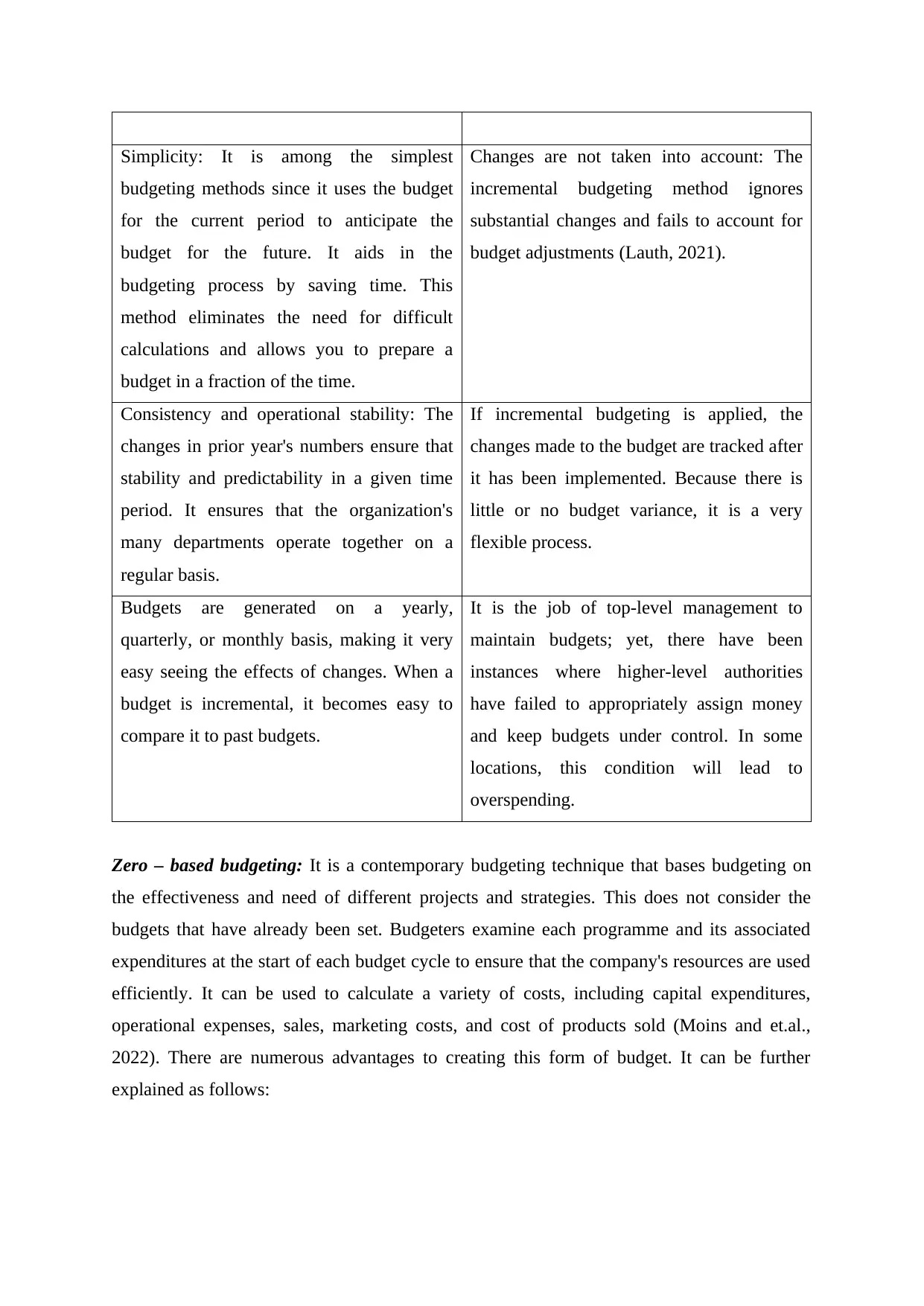

Pros Cons

Simplicity: It is among the simplest

budgeting methods since it uses the budget

for the current period to anticipate the

budget for the future. It aids in the

budgeting process by saving time. This

method eliminates the need for difficult

calculations and allows you to prepare a

budget in a fraction of the time.

Changes are not taken into account: The

incremental budgeting method ignores

substantial changes and fails to account for

budget adjustments (Lauth, 2021).

Consistency and operational stability: The

changes in prior year's numbers ensure that

stability and predictability in a given time

period. It ensures that the organization's

many departments operate together on a

regular basis.

If incremental budgeting is applied, the

changes made to the budget are tracked after

it has been implemented. Because there is

little or no budget variance, it is a very

flexible process.

Budgets are generated on a yearly,

quarterly, or monthly basis, making it very

easy seeing the effects of changes. When a

budget is incremental, it becomes easy to

compare it to past budgets.

It is the job of top-level management to

maintain budgets; yet, there have been

instances where higher-level authorities

have failed to appropriately assign money

and keep budgets under control. In some

locations, this condition will lead to

overspending.

Zero – based budgeting: It is a contemporary budgeting technique that bases budgeting on

the effectiveness and need of different projects and strategies. This does not consider the

budgets that have already been set. Budgeters examine each programme and its associated

expenditures at the start of each budget cycle to ensure that the company's resources are used

efficiently. It can be used to calculate a variety of costs, including capital expenditures,

operational expenses, sales, marketing costs, and cost of products sold (Moins and et.al.,

2022). There are numerous advantages to creating this form of budget. It can be further

explained as follows:

budgeting methods since it uses the budget

for the current period to anticipate the

budget for the future. It aids in the

budgeting process by saving time. This

method eliminates the need for difficult

calculations and allows you to prepare a

budget in a fraction of the time.

Changes are not taken into account: The

incremental budgeting method ignores

substantial changes and fails to account for

budget adjustments (Lauth, 2021).

Consistency and operational stability: The

changes in prior year's numbers ensure that

stability and predictability in a given time

period. It ensures that the organization's

many departments operate together on a

regular basis.

If incremental budgeting is applied, the

changes made to the budget are tracked after

it has been implemented. Because there is

little or no budget variance, it is a very

flexible process.

Budgets are generated on a yearly,

quarterly, or monthly basis, making it very

easy seeing the effects of changes. When a

budget is incremental, it becomes easy to

compare it to past budgets.

It is the job of top-level management to

maintain budgets; yet, there have been

instances where higher-level authorities

have failed to appropriately assign money

and keep budgets under control. In some

locations, this condition will lead to

overspending.

Zero – based budgeting: It is a contemporary budgeting technique that bases budgeting on

the effectiveness and need of different projects and strategies. This does not consider the

budgets that have already been set. Budgeters examine each programme and its associated

expenditures at the start of each budget cycle to ensure that the company's resources are used

efficiently. It can be used to calculate a variety of costs, including capital expenditures,

operational expenses, sales, marketing costs, and cost of products sold (Moins and et.al.,

2022). There are numerous advantages to creating this form of budget. It can be further

explained as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

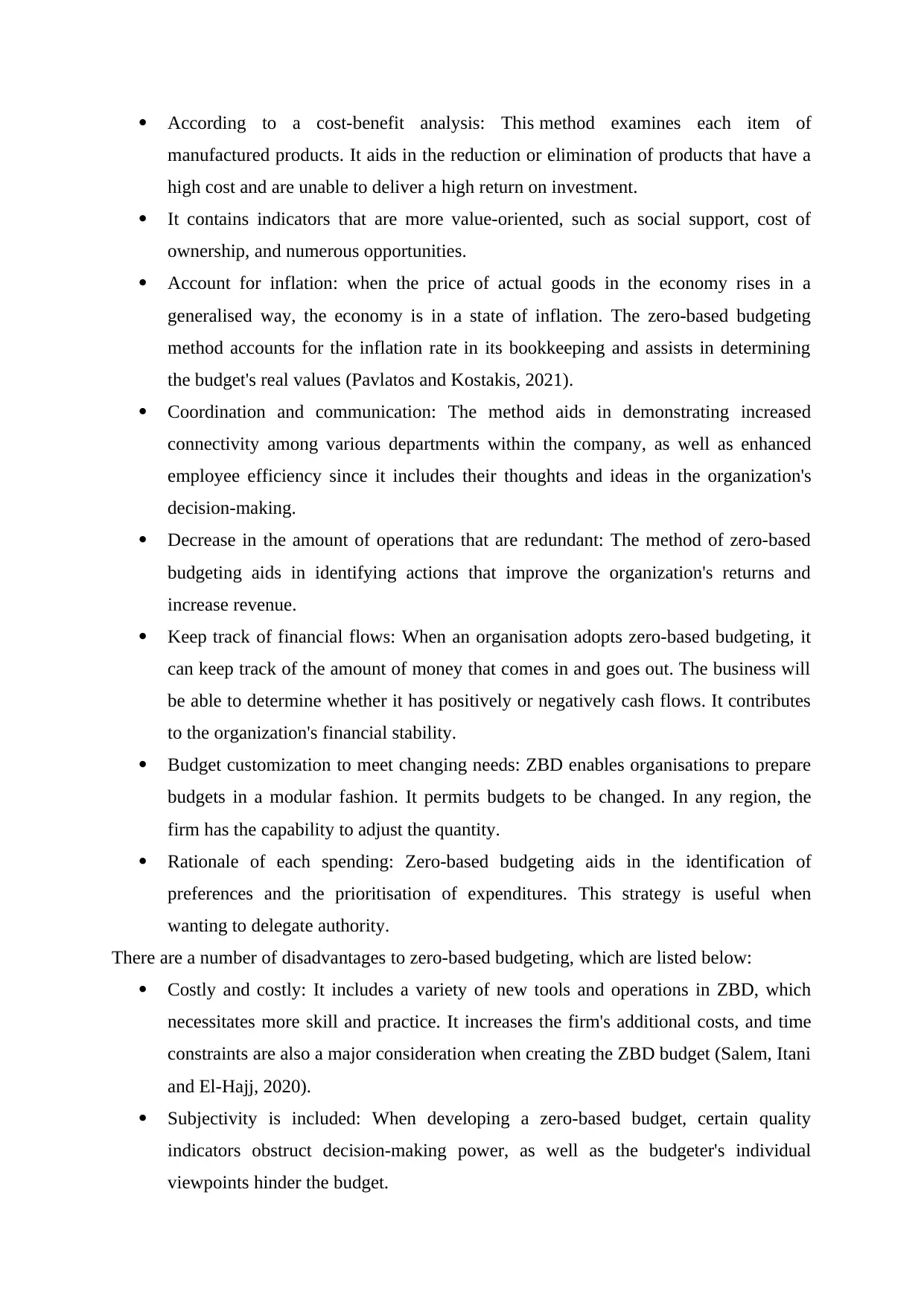

According to a cost-benefit analysis: This method examines each item of

manufactured products. It aids in the reduction or elimination of products that have a

high cost and are unable to deliver a high return on investment.

It contains indicators that are more value-oriented, such as social support, cost of

ownership, and numerous opportunities.

Account for inflation: when the price of actual goods in the economy rises in a

generalised way, the economy is in a state of inflation. The zero-based budgeting

method accounts for the inflation rate in its bookkeeping and assists in determining

the budget's real values (Pavlatos and Kostakis, 2021).

Coordination and communication: The method aids in demonstrating increased

connectivity among various departments within the company, as well as enhanced

employee efficiency since it includes their thoughts and ideas in the organization's

decision-making.

Decrease in the amount of operations that are redundant: The method of zero-based

budgeting aids in identifying actions that improve the organization's returns and

increase revenue.

Keep track of financial flows: When an organisation adopts zero-based budgeting, it

can keep track of the amount of money that comes in and goes out. The business will

be able to determine whether it has positively or negatively cash flows. It contributes

to the organization's financial stability.

Budget customization to meet changing needs: ZBD enables organisations to prepare

budgets in a modular fashion. It permits budgets to be changed. In any region, the

firm has the capability to adjust the quantity.

Rationale of each spending: Zero-based budgeting aids in the identification of

preferences and the prioritisation of expenditures. This strategy is useful when

wanting to delegate authority.

There are a number of disadvantages to zero-based budgeting, which are listed below:

Costly and costly: It includes a variety of new tools and operations in ZBD, which

necessitates more skill and practice. It increases the firm's additional costs, and time

constraints are also a major consideration when creating the ZBD budget (Salem, Itani

and El-Hajj, 2020).

Subjectivity is included: When developing a zero-based budget, certain quality

indicators obstruct decision-making power, as well as the budgeter's individual

viewpoints hinder the budget.

manufactured products. It aids in the reduction or elimination of products that have a

high cost and are unable to deliver a high return on investment.

It contains indicators that are more value-oriented, such as social support, cost of

ownership, and numerous opportunities.

Account for inflation: when the price of actual goods in the economy rises in a

generalised way, the economy is in a state of inflation. The zero-based budgeting

method accounts for the inflation rate in its bookkeeping and assists in determining

the budget's real values (Pavlatos and Kostakis, 2021).

Coordination and communication: The method aids in demonstrating increased

connectivity among various departments within the company, as well as enhanced

employee efficiency since it includes their thoughts and ideas in the organization's

decision-making.

Decrease in the amount of operations that are redundant: The method of zero-based

budgeting aids in identifying actions that improve the organization's returns and

increase revenue.

Keep track of financial flows: When an organisation adopts zero-based budgeting, it

can keep track of the amount of money that comes in and goes out. The business will

be able to determine whether it has positively or negatively cash flows. It contributes

to the organization's financial stability.

Budget customization to meet changing needs: ZBD enables organisations to prepare

budgets in a modular fashion. It permits budgets to be changed. In any region, the

firm has the capability to adjust the quantity.

Rationale of each spending: Zero-based budgeting aids in the identification of

preferences and the prioritisation of expenditures. This strategy is useful when

wanting to delegate authority.

There are a number of disadvantages to zero-based budgeting, which are listed below:

Costly and costly: It includes a variety of new tools and operations in ZBD, which

necessitates more skill and practice. It increases the firm's additional costs, and time

constraints are also a major consideration when creating the ZBD budget (Salem, Itani

and El-Hajj, 2020).

Subjectivity is included: When developing a zero-based budget, certain quality

indicators obstruct decision-making power, as well as the budgeter's individual

viewpoints hinder the budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Savvy budgeters influence the process – There are a variety of budgeters who

manipulate the approach employed in the zero-based budgeting process, resulting in

incorrect justification of the budgets maintained.

Unpredictable income: There are a few sources of revenue in any organisation that are

unpredictable and have a large impact on monthly income levels. Unexpected income

sources wreak havoc on the budget and reduce the firm's managerial efficiency.

TASK 3

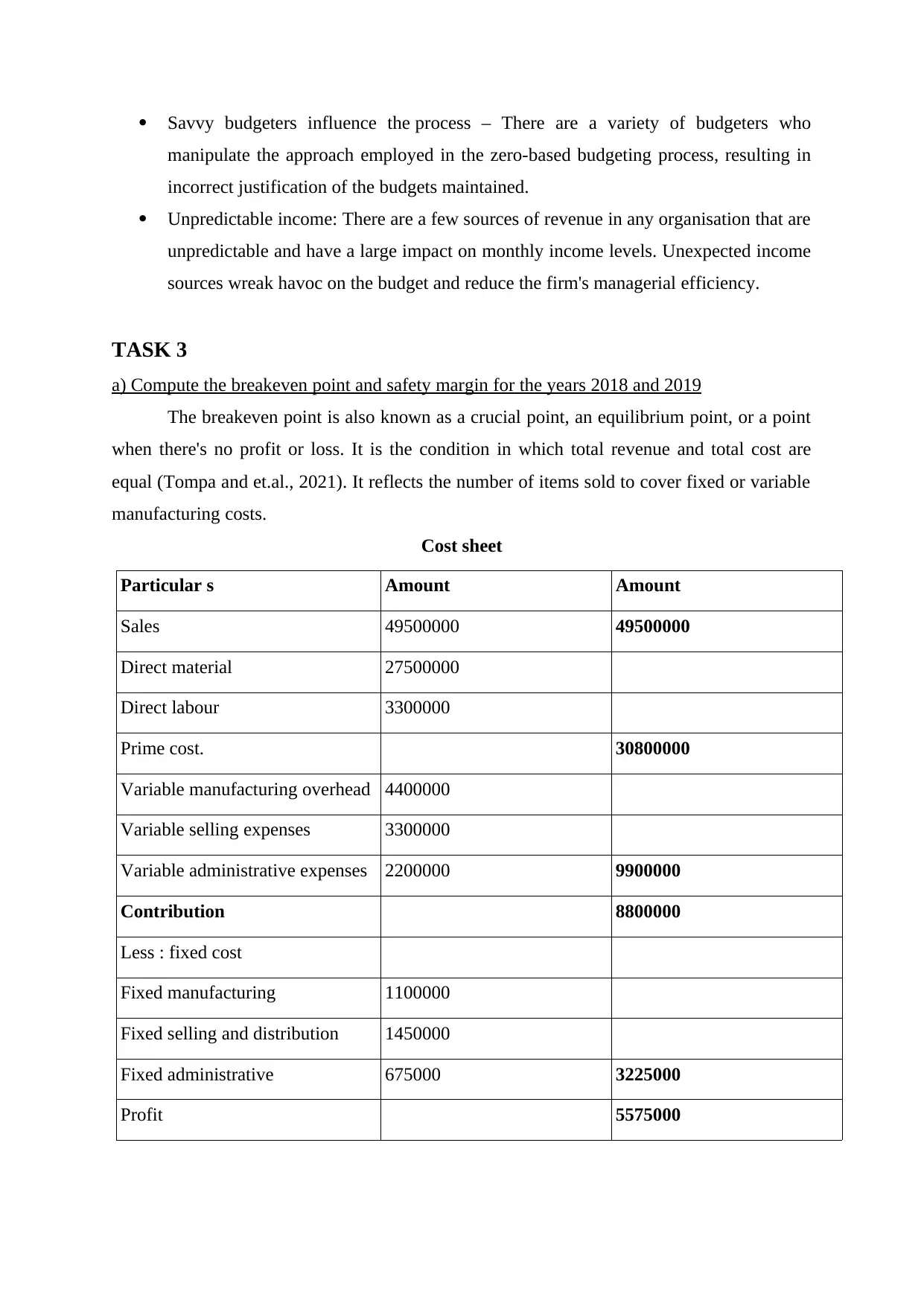

a) Compute the breakeven point and safety margin for the years 2018 and 2019

The breakeven point is also known as a crucial point, an equilibrium point, or a point

when there's no profit or loss. It is the condition in which total revenue and total cost are

equal (Tompa and et.al., 2021). It reflects the number of items sold to cover fixed or variable

manufacturing costs.

Cost sheet

Particular s Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

Less : fixed cost

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

manipulate the approach employed in the zero-based budgeting process, resulting in

incorrect justification of the budgets maintained.

Unpredictable income: There are a few sources of revenue in any organisation that are

unpredictable and have a large impact on monthly income levels. Unexpected income

sources wreak havoc on the budget and reduce the firm's managerial efficiency.

TASK 3

a) Compute the breakeven point and safety margin for the years 2018 and 2019

The breakeven point is also known as a crucial point, an equilibrium point, or a point

when there's no profit or loss. It is the condition in which total revenue and total cost are

equal (Tompa and et.al., 2021). It reflects the number of items sold to cover fixed or variable

manufacturing costs.

Cost sheet

Particular s Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

Less : fixed cost

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

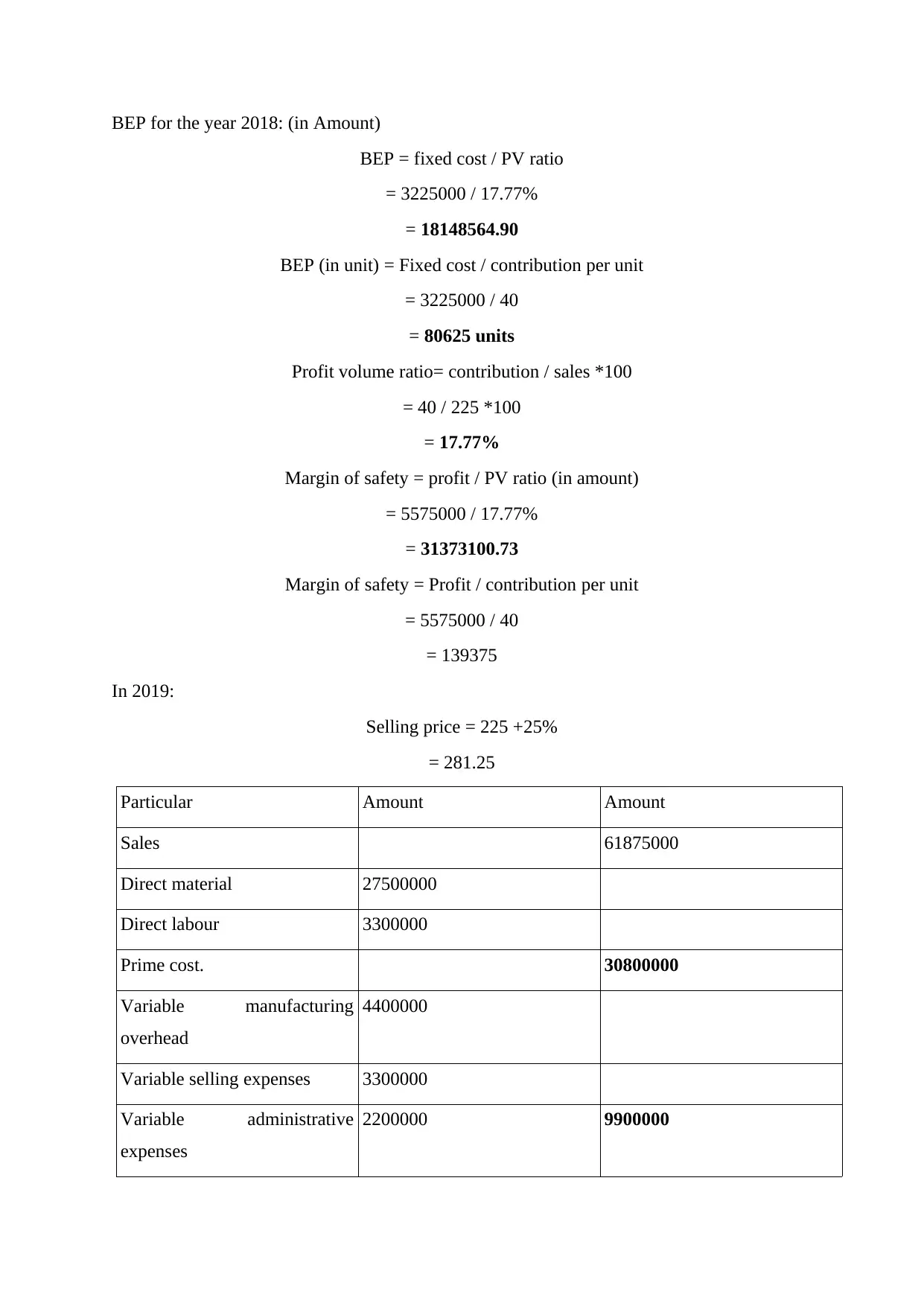

BEP for the year 2018: (in Amount)

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.90

BEP (in unit) = Fixed cost / contribution per unit

= 3225000 / 40

= 80625 units

Profit volume ratio= contribution / sales *100

= 40 / 225 *100

= 17.77%

Margin of safety = profit / PV ratio (in amount)

= 5575000 / 17.77%

= 31373100.73

Margin of safety = Profit / contribution per unit

= 5575000 / 40

= 139375

In 2019:

Selling price = 225 +25%

= 281.25

Particular Amount Amount

Sales 61875000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing

overhead

4400000

Variable selling expenses 3300000

Variable administrative

expenses

2200000 9900000

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.90

BEP (in unit) = Fixed cost / contribution per unit

= 3225000 / 40

= 80625 units

Profit volume ratio= contribution / sales *100

= 40 / 225 *100

= 17.77%

Margin of safety = profit / PV ratio (in amount)

= 5575000 / 17.77%

= 31373100.73

Margin of safety = Profit / contribution per unit

= 5575000 / 40

= 139375

In 2019:

Selling price = 225 +25%

= 281.25

Particular Amount Amount

Sales 61875000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing

overhead

4400000

Variable selling expenses 3300000

Variable administrative

expenses

2200000 9900000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.