Financial Control and Budgeting: Analysis of Health and Social Care

VerifiedAdded on 2023/06/14

|17

|5187

|66

Report

AI Summary

This report provides a comprehensive analysis of financial control and budgeting within the health and social care sector. It critically examines the legal, financial, and regulatory environment, evaluating alternative funding options like private finance institutions and agency partnerships. The report elaborates on agency theory in the context of the NHS and discusses effective communication strategies with stakeholders regarding budgeting. It also addresses the impact of financial constraints, costs, and budgets on health and social service managers, highlighting the challenges of budgeting in public sector organizations. Furthermore, the report explains the advantages and disadvantages of incremental and zero-based budgeting methods. Finally, it includes a calculation of the break-even point and margin of safety for the years 2018 and 2019, along with a critical discussion of the key assumptions related to the break-even model. This detailed analysis offers valuable insights into the financial management of health and social care services.

Financial control and

budgeting.

budgeting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

Critical analysis of legal, financial and regulatory environment of health and social care.........1

Evaluating the use of alternative funding options such as private finance institutions, agency

partnerships and outsourcing in the health and social care sector..............................................3

Elaborating agency theory in context of NHS and significant ways of communicating with

stakeholders in context of budgeting. .........................................................................................4

TASK 2 ...........................................................................................................................................4

Critical discussion on the impact of financial constraints, costs and budgets on health and

social service managers...............................................................................................................4

Describing the challenges of budgeting in public sector organization.......................................6

Explaining the advantages and disadvantages of incremental and zero based budgeting. ........7

TASK 3..........................................................................................................................................10

a.) Calculating break even point and margin of safety for the year 2018 and 2019.................10

b.) Critically discussing the key assumptions related to break even model. ............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

TASK 1............................................................................................................................................1

Critical analysis of legal, financial and regulatory environment of health and social care.........1

Evaluating the use of alternative funding options such as private finance institutions, agency

partnerships and outsourcing in the health and social care sector..............................................3

Elaborating agency theory in context of NHS and significant ways of communicating with

stakeholders in context of budgeting. .........................................................................................4

TASK 2 ...........................................................................................................................................4

Critical discussion on the impact of financial constraints, costs and budgets on health and

social service managers...............................................................................................................4

Describing the challenges of budgeting in public sector organization.......................................6

Explaining the advantages and disadvantages of incremental and zero based budgeting. ........7

TASK 3..........................................................................................................................................10

a.) Calculating break even point and margin of safety for the year 2018 and 2019.................10

b.) Critically discussing the key assumptions related to break even model. ............................12

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Financial control is the process through which procedures, policies and various methods

by which organisation control the uses of financial resources. The resources of the organisation

are limited and it has several uses (ATIENO, 2019).The budgeting is a estimation about the

revenue and expenses for a specific period of time. This report is divided into three tasks. It

includes legal, financial and regulatory framework of health and social care. There are various

funding options such as private finance initiatives ( PFI), agency partnerships, competitive

tendering and outsourcing in relation to the health and social care sector. There is also brief

description about the agency theory which is a contract between one or more persons to perform

service on behalf of another person. NHS stands for national health service which is healthcare

system in England. It is funded by the government of respective company. There are certain

challenges of budgeting which are faced by the public sector organisations. There are different

methods of budgeting such as zero based budgeting and incremental budgeting. It has various

advantages and disadvantages of zero based budgeting and incremental budgeting. In task three,

it includes the computation of break even point and margin of safety for the two consecutive

years. There are various assumptions which are related to break even model are also

encompassed in this report.

MAIN BODY

TASK 1

Critical analysis of legal, financial and regulatory environment of health and social care.

Health and social care refers to the services which are provided by department of health

in the UK. In every economy, there are certain set of written documents which includes

constitution, legislations, regulation and contracts is known as legal environment. The financial

framework includes procedures and strategies regarding the finance of the particular industry or

sector (Beazley and et.al., 2019). The regulatory environment relates to the complying with all

the legal structure of the company. In context of health and social care, the various frameworks

can be elaborated as given below:

Legal environment of health and social care:

1

Financial control is the process through which procedures, policies and various methods

by which organisation control the uses of financial resources. The resources of the organisation

are limited and it has several uses (ATIENO, 2019).The budgeting is a estimation about the

revenue and expenses for a specific period of time. This report is divided into three tasks. It

includes legal, financial and regulatory framework of health and social care. There are various

funding options such as private finance initiatives ( PFI), agency partnerships, competitive

tendering and outsourcing in relation to the health and social care sector. There is also brief

description about the agency theory which is a contract between one or more persons to perform

service on behalf of another person. NHS stands for national health service which is healthcare

system in England. It is funded by the government of respective company. There are certain

challenges of budgeting which are faced by the public sector organisations. There are different

methods of budgeting such as zero based budgeting and incremental budgeting. It has various

advantages and disadvantages of zero based budgeting and incremental budgeting. In task three,

it includes the computation of break even point and margin of safety for the two consecutive

years. There are various assumptions which are related to break even model are also

encompassed in this report.

MAIN BODY

TASK 1

Critical analysis of legal, financial and regulatory environment of health and social care.

Health and social care refers to the services which are provided by department of health

in the UK. In every economy, there are certain set of written documents which includes

constitution, legislations, regulation and contracts is known as legal environment. The financial

framework includes procedures and strategies regarding the finance of the particular industry or

sector (Beazley and et.al., 2019). The regulatory environment relates to the complying with all

the legal structure of the company. In context of health and social care, the various frameworks

can be elaborated as given below:

Legal environment of health and social care:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The law that is responsible for social care is Care Act, 2014. Before this act, there are several

others acts such as national assistance act, 1948 and NHS community act,1990. The nine acts

were merged into the Care act, 2014. There are various functions of the care act, which can be

described as given below:

a.) It ensure that people get services before the care needs get critical or can postponement of

needs (Demirag, Fırtın and Bilbil, 2020).

b.) It helps to gain information which is required to take good decisions about care and support.

c.) It also provide provision for superior quality of services and effective services to select from.

The responsibility for providing healthcare is national and responsibility of social care is based

on local level. In the year 2015, there was introduction of the term known as social care 'percept'.

It provides local authorities, the ability to increase the council tax with an additional amount. The

framework has formed between the four UK health departments and the HRA. It is applied in

England, Northern Ireland, Scotland and Wales. The section 111(6) and (7) of care act, 2014

entails all the legal formalities and it promotes the conduct of the research.

Regulatory framework of health and social care sector:

There are various principles which are to be followed in order to comply the rules of the health

sector. There are various organisations which oversee the health and facility operations. The

regulatory framework with respect to health and social care sector can be described as given

below:

1. US Environmental protection agency – its main focus is on protecting the planet from various

hazardous chemicals(Dhawan, Dheri and Gill, 2021).There are several integrated act which are

RCRA ( resource conservation and recovery act hazardous chemicals) , CWA ( clean water act),

CAA ( clean air act) and FIFRA—Federal Insecticide, Fungicide, and Rodenticide Act.

2.Joint Commission on Accreditation of Healthcare Organizations (Joint Commission)- It has

main focus on the patient health and safety.

Financial framework of health and social care:

The financing of the health and social care deals with allocation, procurement and utilisation of

financial resources in the health system.

The financial needs are fulfilled by WHO and provides necessary funding for all the services

required by the health and social care.

2

others acts such as national assistance act, 1948 and NHS community act,1990. The nine acts

were merged into the Care act, 2014. There are various functions of the care act, which can be

described as given below:

a.) It ensure that people get services before the care needs get critical or can postponement of

needs (Demirag, Fırtın and Bilbil, 2020).

b.) It helps to gain information which is required to take good decisions about care and support.

c.) It also provide provision for superior quality of services and effective services to select from.

The responsibility for providing healthcare is national and responsibility of social care is based

on local level. In the year 2015, there was introduction of the term known as social care 'percept'.

It provides local authorities, the ability to increase the council tax with an additional amount. The

framework has formed between the four UK health departments and the HRA. It is applied in

England, Northern Ireland, Scotland and Wales. The section 111(6) and (7) of care act, 2014

entails all the legal formalities and it promotes the conduct of the research.

Regulatory framework of health and social care sector:

There are various principles which are to be followed in order to comply the rules of the health

sector. There are various organisations which oversee the health and facility operations. The

regulatory framework with respect to health and social care sector can be described as given

below:

1. US Environmental protection agency – its main focus is on protecting the planet from various

hazardous chemicals(Dhawan, Dheri and Gill, 2021).There are several integrated act which are

RCRA ( resource conservation and recovery act hazardous chemicals) , CWA ( clean water act),

CAA ( clean air act) and FIFRA—Federal Insecticide, Fungicide, and Rodenticide Act.

2.Joint Commission on Accreditation of Healthcare Organizations (Joint Commission)- It has

main focus on the patient health and safety.

Financial framework of health and social care:

The financing of the health and social care deals with allocation, procurement and utilisation of

financial resources in the health system.

The financial needs are fulfilled by WHO and provides necessary funding for all the services

required by the health and social care.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Evaluating the use of alternative funding options such as private finance institutions, agency

partnerships and outsourcing in the health and social care sector.

Every organisation require capital to run its operations. In the same way, the health and

social care sector require several sources of funding. The alternative funding options are

additional sources or methods of raising funds except the funds it already possess. There are

numerous funding options which can be described as given below:

Private finance institutions – These are the bodies which are not owned or regulated by

the government. The shareholding is not distributed among various authorities. The main

role of these private institutions is credit availability, risk mitigation and financial

information accuracy (Diab, 2021). The main financial institutions are perishing square

holdings, RSA insurance, London stock exchange group and Admiral group.

Agency partnerships : It is a non governmental form of organisation. It is the most

dynamic, inclusive and effective means which helps to gain the higher return on

investment. In this form of funding, it is an independent, international communication

agency which is set up to raise the funds for health and social care sector.

Outsourcing – It is the practice of recruiting a client outside a organisation to perform

various operational functions. The organisations are using this form of funding to reduce

the labour cost which includes salaries of personnel, overhead, equipment and technology

(Endenich and et.al., 2020). It helps to saves the time and cost of the enterprise. There are

various advantages

Elaborating agency theory in context of NHS and significant ways of communicating with

stakeholders in context of budgeting.

NHS is healthcare system which is funded publicly. NHB stands for national health

service.

There are various ways of communicating with stakeholders which can be described as given

under:

3

partnerships and outsourcing in the health and social care sector.

Every organisation require capital to run its operations. In the same way, the health and

social care sector require several sources of funding. The alternative funding options are

additional sources or methods of raising funds except the funds it already possess. There are

numerous funding options which can be described as given below:

Private finance institutions – These are the bodies which are not owned or regulated by

the government. The shareholding is not distributed among various authorities. The main

role of these private institutions is credit availability, risk mitigation and financial

information accuracy (Diab, 2021). The main financial institutions are perishing square

holdings, RSA insurance, London stock exchange group and Admiral group.

Agency partnerships : It is a non governmental form of organisation. It is the most

dynamic, inclusive and effective means which helps to gain the higher return on

investment. In this form of funding, it is an independent, international communication

agency which is set up to raise the funds for health and social care sector.

Outsourcing – It is the practice of recruiting a client outside a organisation to perform

various operational functions. The organisations are using this form of funding to reduce

the labour cost which includes salaries of personnel, overhead, equipment and technology

(Endenich and et.al., 2020). It helps to saves the time and cost of the enterprise. There are

various advantages

Elaborating agency theory in context of NHS and significant ways of communicating with

stakeholders in context of budgeting.

NHS is healthcare system which is funded publicly. NHB stands for national health

service.

There are various ways of communicating with stakeholders which can be described as given

under:

3

Project summary report- It is sent at a particular point of time either weekly or monthly.

This report includes the budgets prepared by the top level mangers or higher authorities.

It also consists the overall scope of the selected project such as problem of the project,

recommended solutions and conclusions from the budget prepared(Hadi, Wardayati and

Miqdad, 2020). The stakeholders are benefited by getting the information about the

strategical and financial plans of the enterprise.

Email, e-newsletter and communication automation – It is one of the important tool for

communicating to stakeholders. It helps in reaching to the stakeholders very promptly

and detailed budgets can be communicated to the external as well as internal users.

TASK 2

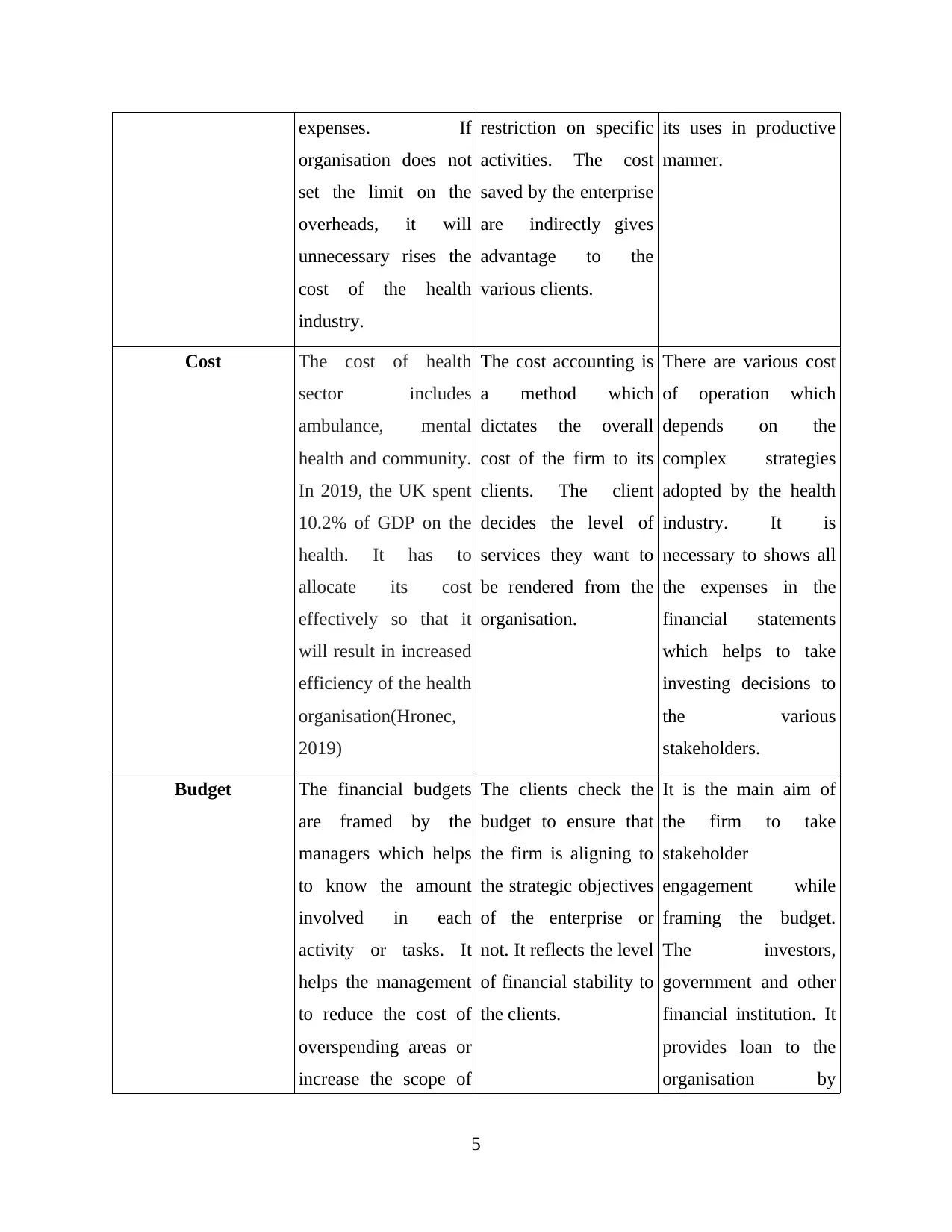

Critical discussion on the impact of financial constraints, costs and budgets on health and social

service managers.

Financial constraints : It is the factor which restrict the quality of numerous investment

options. There are various advantages of financial constraints such as maintaining policy

stability,financial sector reforms.

Managers Client Stakeholders

Financial constraints All the functions of

management such as

planning, organising,

directing and

controlling is done by

the top level mangers.

In context of health

and social services, it

is necessary to set

limits for the

expenditures or

The health and social

service sector is

mainly running for the

purpose of satisfying

public. The budgets

and various financial

statements are helpful

to the clients. The

numerous clients are

benefited when the

enterprise put

Stakeholders are the

persons who take

interest in the

organisation and its

related activities. The

financial constraints

reflects the strategy

adopted by the

organisation to

optimally utilise the

resources and diverse

4

This report includes the budgets prepared by the top level mangers or higher authorities.

It also consists the overall scope of the selected project such as problem of the project,

recommended solutions and conclusions from the budget prepared(Hadi, Wardayati and

Miqdad, 2020). The stakeholders are benefited by getting the information about the

strategical and financial plans of the enterprise.

Email, e-newsletter and communication automation – It is one of the important tool for

communicating to stakeholders. It helps in reaching to the stakeholders very promptly

and detailed budgets can be communicated to the external as well as internal users.

TASK 2

Critical discussion on the impact of financial constraints, costs and budgets on health and social

service managers.

Financial constraints : It is the factor which restrict the quality of numerous investment

options. There are various advantages of financial constraints such as maintaining policy

stability,financial sector reforms.

Managers Client Stakeholders

Financial constraints All the functions of

management such as

planning, organising,

directing and

controlling is done by

the top level mangers.

In context of health

and social services, it

is necessary to set

limits for the

expenditures or

The health and social

service sector is

mainly running for the

purpose of satisfying

public. The budgets

and various financial

statements are helpful

to the clients. The

numerous clients are

benefited when the

enterprise put

Stakeholders are the

persons who take

interest in the

organisation and its

related activities. The

financial constraints

reflects the strategy

adopted by the

organisation to

optimally utilise the

resources and diverse

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses. If

organisation does not

set the limit on the

overheads, it will

unnecessary rises the

cost of the health

industry.

restriction on specific

activities. The cost

saved by the enterprise

are indirectly gives

advantage to the

various clients.

its uses in productive

manner.

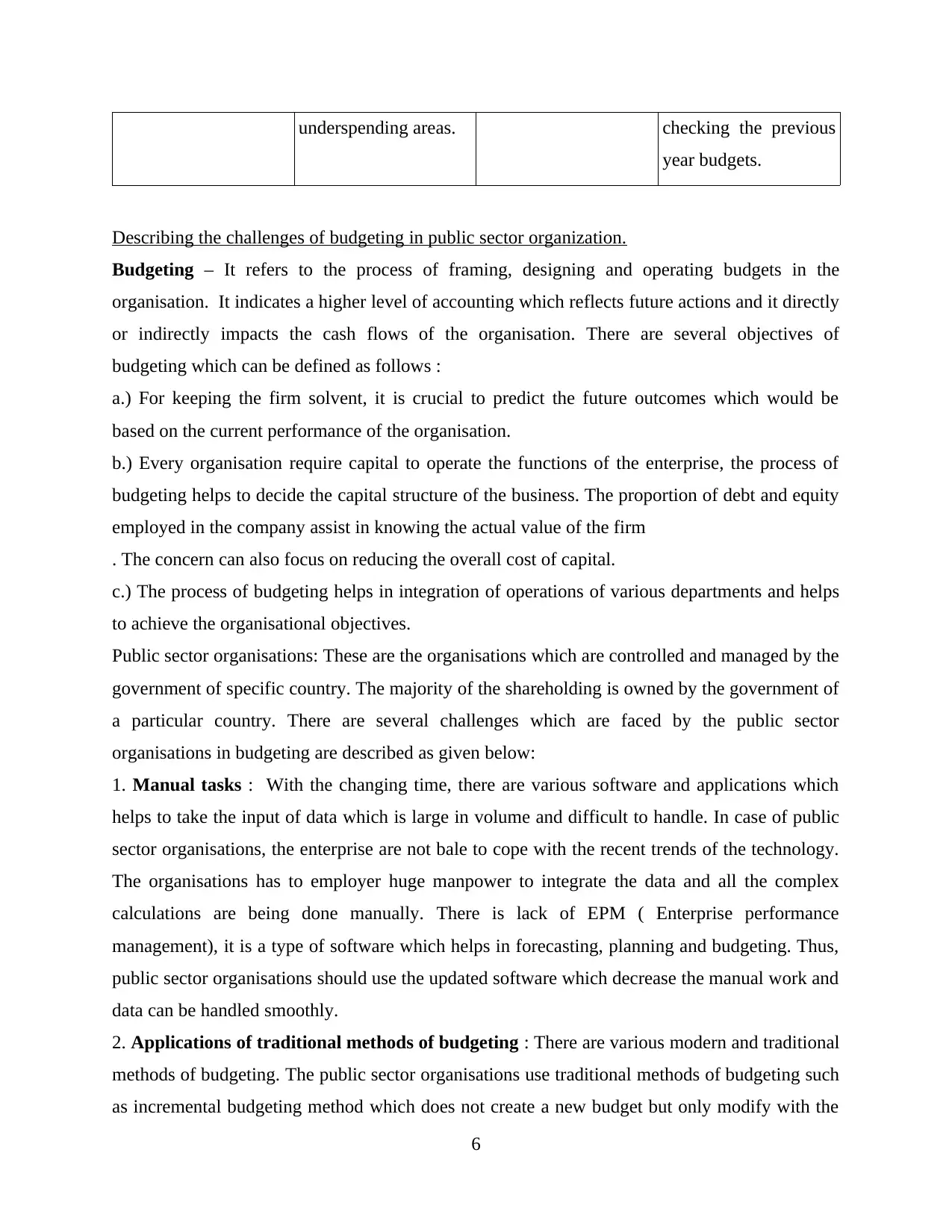

Cost The cost of health

sector includes

ambulance, mental

health and community.

In 2019, the UK spent

10.2% of GDP on the

health. It has to

allocate its cost

effectively so that it

will result in increased

efficiency of the health

organisation(Hronec,

2019)

The cost accounting is

a method which

dictates the overall

cost of the firm to its

clients. The client

decides the level of

services they want to

be rendered from the

organisation.

There are various cost

of operation which

depends on the

complex strategies

adopted by the health

industry. It is

necessary to shows all

the expenses in the

financial statements

which helps to take

investing decisions to

the various

stakeholders.

Budget The financial budgets

are framed by the

managers which helps

to know the amount

involved in each

activity or tasks. It

helps the management

to reduce the cost of

overspending areas or

increase the scope of

The clients check the

budget to ensure that

the firm is aligning to

the strategic objectives

of the enterprise or

not. It reflects the level

of financial stability to

the clients.

It is the main aim of

the firm to take

stakeholder

engagement while

framing the budget.

The investors,

government and other

financial institution. It

provides loan to the

organisation by

5

organisation does not

set the limit on the

overheads, it will

unnecessary rises the

cost of the health

industry.

restriction on specific

activities. The cost

saved by the enterprise

are indirectly gives

advantage to the

various clients.

its uses in productive

manner.

Cost The cost of health

sector includes

ambulance, mental

health and community.

In 2019, the UK spent

10.2% of GDP on the

health. It has to

allocate its cost

effectively so that it

will result in increased

efficiency of the health

organisation(Hronec,

2019)

The cost accounting is

a method which

dictates the overall

cost of the firm to its

clients. The client

decides the level of

services they want to

be rendered from the

organisation.

There are various cost

of operation which

depends on the

complex strategies

adopted by the health

industry. It is

necessary to shows all

the expenses in the

financial statements

which helps to take

investing decisions to

the various

stakeholders.

Budget The financial budgets

are framed by the

managers which helps

to know the amount

involved in each

activity or tasks. It

helps the management

to reduce the cost of

overspending areas or

increase the scope of

The clients check the

budget to ensure that

the firm is aligning to

the strategic objectives

of the enterprise or

not. It reflects the level

of financial stability to

the clients.

It is the main aim of

the firm to take

stakeholder

engagement while

framing the budget.

The investors,

government and other

financial institution. It

provides loan to the

organisation by

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

underspending areas. checking the previous

year budgets.

Describing the challenges of budgeting in public sector organization.

Budgeting – It refers to the process of framing, designing and operating budgets in the

organisation. It indicates a higher level of accounting which reflects future actions and it directly

or indirectly impacts the cash flows of the organisation. There are several objectives of

budgeting which can be defined as follows :

a.) For keeping the firm solvent, it is crucial to predict the future outcomes which would be

based on the current performance of the organisation.

b.) Every organisation require capital to operate the functions of the enterprise, the process of

budgeting helps to decide the capital structure of the business. The proportion of debt and equity

employed in the company assist in knowing the actual value of the firm

. The concern can also focus on reducing the overall cost of capital.

c.) The process of budgeting helps in integration of operations of various departments and helps

to achieve the organisational objectives.

Public sector organisations: These are the organisations which are controlled and managed by the

government of specific country. The majority of the shareholding is owned by the government of

a particular country. There are several challenges which are faced by the public sector

organisations in budgeting are described as given below:

1. Manual tasks : With the changing time, there are various software and applications which

helps to take the input of data which is large in volume and difficult to handle. In case of public

sector organisations, the enterprise are not bale to cope with the recent trends of the technology.

The organisations has to employer huge manpower to integrate the data and all the complex

calculations are being done manually. There is lack of EPM ( Enterprise performance

management), it is a type of software which helps in forecasting, planning and budgeting. Thus,

public sector organisations should use the updated software which decrease the manual work and

data can be handled smoothly.

2. Applications of traditional methods of budgeting : There are various modern and traditional

methods of budgeting. The public sector organisations use traditional methods of budgeting such

as incremental budgeting method which does not create a new budget but only modify with the

6

year budgets.

Describing the challenges of budgeting in public sector organization.

Budgeting – It refers to the process of framing, designing and operating budgets in the

organisation. It indicates a higher level of accounting which reflects future actions and it directly

or indirectly impacts the cash flows of the organisation. There are several objectives of

budgeting which can be defined as follows :

a.) For keeping the firm solvent, it is crucial to predict the future outcomes which would be

based on the current performance of the organisation.

b.) Every organisation require capital to operate the functions of the enterprise, the process of

budgeting helps to decide the capital structure of the business. The proportion of debt and equity

employed in the company assist in knowing the actual value of the firm

. The concern can also focus on reducing the overall cost of capital.

c.) The process of budgeting helps in integration of operations of various departments and helps

to achieve the organisational objectives.

Public sector organisations: These are the organisations which are controlled and managed by the

government of specific country. The majority of the shareholding is owned by the government of

a particular country. There are several challenges which are faced by the public sector

organisations in budgeting are described as given below:

1. Manual tasks : With the changing time, there are various software and applications which

helps to take the input of data which is large in volume and difficult to handle. In case of public

sector organisations, the enterprise are not bale to cope with the recent trends of the technology.

The organisations has to employer huge manpower to integrate the data and all the complex

calculations are being done manually. There is lack of EPM ( Enterprise performance

management), it is a type of software which helps in forecasting, planning and budgeting. Thus,

public sector organisations should use the updated software which decrease the manual work and

data can be handled smoothly.

2. Applications of traditional methods of budgeting : There are various modern and traditional

methods of budgeting. The public sector organisations use traditional methods of budgeting such

as incremental budgeting method which does not create a new budget but only modify with the

6

existing adjustments. This issue fails to address the exact amount of return on investment, net

cash flows and level of profitability in the organisation.

3. Budget process challenge : In public sector organisation, static budgets and multi year

financial plans results into high level of targets in terms of finance and constraints. The

occurrence of material deviations in the organisations, misalign the functions of the enterprise.

The volatile and dynamic nature of the market and changes in the consumption of resource levels

results into the disequilibrium of budgets. For overcoming this issue, the organisation should

frequently update the budgets by analysing the internal as well as external variables.

4. Inaccurate data and assumptions : Every process of accounting requires data which is raw

facts and figures. For implementing the budgets, the accuracy of data is required. Public

organisations fail to collect the accurate data from various departments and it is a big problem to

compile the information of various departmental functions. Sometimes, the organisation are

unable to follow the assumptions related to budgeting. Identifying the cost pattern of each

functional department can be typical task and creates problems while synthesis the information

for framing the budgets.

Explaining the advantages and disadvantages of incremental and zero based budgeting.

Incremental budgeting : It is a type of budgeting process in which the revised changes are

considered in the existing budgeted or actual results. There are several advantages of incremental

budgeting which can be described as given below:

a.) Simplicity : It is one of the easiest approach of budgeting because it takes the budget of

existing period for forecasting the future budget. It helps to save the time in the process of

budgeting. This method does not include the complex calculations and assists in preparing

budget in very less time.

b.) Consistency and operational stability – The modifications in the figures of previous year

assures that stability and consistency in a particular time period. It ensures that different

department of the organizations work on the consistent basis(Im and Kwon, 2019)

c.) Easy to see the impact of change – budget is prepared on annual, quarter or monthly

basis. In case of incremental budget, it becomes easier to compare the budget with

previous budgets.

7

cash flows and level of profitability in the organisation.

3. Budget process challenge : In public sector organisation, static budgets and multi year

financial plans results into high level of targets in terms of finance and constraints. The

occurrence of material deviations in the organisations, misalign the functions of the enterprise.

The volatile and dynamic nature of the market and changes in the consumption of resource levels

results into the disequilibrium of budgets. For overcoming this issue, the organisation should

frequently update the budgets by analysing the internal as well as external variables.

4. Inaccurate data and assumptions : Every process of accounting requires data which is raw

facts and figures. For implementing the budgets, the accuracy of data is required. Public

organisations fail to collect the accurate data from various departments and it is a big problem to

compile the information of various departmental functions. Sometimes, the organisation are

unable to follow the assumptions related to budgeting. Identifying the cost pattern of each

functional department can be typical task and creates problems while synthesis the information

for framing the budgets.

Explaining the advantages and disadvantages of incremental and zero based budgeting.

Incremental budgeting : It is a type of budgeting process in which the revised changes are

considered in the existing budgeted or actual results. There are several advantages of incremental

budgeting which can be described as given below:

a.) Simplicity : It is one of the easiest approach of budgeting because it takes the budget of

existing period for forecasting the future budget. It helps to save the time in the process of

budgeting. This method does not include the complex calculations and assists in preparing

budget in very less time.

b.) Consistency and operational stability – The modifications in the figures of previous year

assures that stability and consistency in a particular time period. It ensures that different

department of the organizations work on the consistent basis(Im and Kwon, 2019)

c.) Easy to see the impact of change – budget is prepared on annual, quarter or monthly

basis. In case of incremental budget, it becomes easier to compare the budget with

previous budgets.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There are several limitations of incremental budgeting which can be described as given below:

a.) Does not consider changes : The incremental budgeting does not consider major changes

and it fails to consider the changes in the budget.

b.) When incremental budgeting is used, the alternations done in the budget are observed after its

implementation. It is a very flexible process because it has little or fixed deviation in the budget.

c.) Overspending – It is the responsibility of the top level managers to maintain the budgets,

there are some cases when higher level authorities does not effectively allocate the budget and

fails to keep check on the budgets. This situation will lead to overspending in some areas

(Laguir, Laguir and Tchemeni, 2019) .

d.) Budgetary slack – It is a condition when there is probability that actual performance is better

than the standard budget. There are various ways to accomplish budgetary slack. It maintains low

revenue growth in comparison to the high expense growth(Munzhedzi, 2021)

Zero based budgeting : It is modern approach of budgeting which creates budget on the

efficiency and necessity of various programmes and projects. It does not takes into account the

previously framed budgets. At the beginning of each cycle of budget, the budgeters monitor

each program and its related expenditure to effectively utilise the resources of the organization. It

can be applied to various costs such as capital expenditure, operating expenses, sales, marketing

cost and the cost of goods sold. There are various pros of preparing this type of budget. It can be

elaborated as given below:

1.) Based on cost benefit analysis : The zero based budgeting analyse each item of the

produced goods. It helps to reduce or eliminate those product which involves huge cost

and not able to generate the higher return on investment(Parson and Steele, 2019)

2.) . . It includes more value centric metrics, for instance social capital, total cost of

ownership and various opportunities.

3.) Consider inflation: when there is general increase in the price of real commodities in the

economy, the situation of inflation exists. The zero based budgeting considers the rate of

inflation in its accounting and helps to know the real values in the budget(Vries and

Nemec, 2019) ..

4.) Coordination and communication – The process of ZBD helps in proving enhanced

coordination and communication among various departments exist in the organization

8

a.) Does not consider changes : The incremental budgeting does not consider major changes

and it fails to consider the changes in the budget.

b.) When incremental budgeting is used, the alternations done in the budget are observed after its

implementation. It is a very flexible process because it has little or fixed deviation in the budget.

c.) Overspending – It is the responsibility of the top level managers to maintain the budgets,

there are some cases when higher level authorities does not effectively allocate the budget and

fails to keep check on the budgets. This situation will lead to overspending in some areas

(Laguir, Laguir and Tchemeni, 2019) .

d.) Budgetary slack – It is a condition when there is probability that actual performance is better

than the standard budget. There are various ways to accomplish budgetary slack. It maintains low

revenue growth in comparison to the high expense growth(Munzhedzi, 2021)

Zero based budgeting : It is modern approach of budgeting which creates budget on the

efficiency and necessity of various programmes and projects. It does not takes into account the

previously framed budgets. At the beginning of each cycle of budget, the budgeters monitor

each program and its related expenditure to effectively utilise the resources of the organization. It

can be applied to various costs such as capital expenditure, operating expenses, sales, marketing

cost and the cost of goods sold. There are various pros of preparing this type of budget. It can be

elaborated as given below:

1.) Based on cost benefit analysis : The zero based budgeting analyse each item of the

produced goods. It helps to reduce or eliminate those product which involves huge cost

and not able to generate the higher return on investment(Parson and Steele, 2019)

2.) . . It includes more value centric metrics, for instance social capital, total cost of

ownership and various opportunities.

3.) Consider inflation: when there is general increase in the price of real commodities in the

economy, the situation of inflation exists. The zero based budgeting considers the rate of

inflation in its accounting and helps to know the real values in the budget(Vries and

Nemec, 2019) ..

4.) Coordination and communication – The process of ZBD helps in proving enhanced

coordination and communication among various departments exist in the organization

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and it also results in improved performance of employees because it considers their ideas

and thoughts in the decision making of the organization.

5.) Reduction in the redundant activities : the process of zero based budgeting helps in

knowing the activities which improve the returns of the organization and helps to

increase the revenue of the enterprise.

6.) Keep aware about cash flows : when an organization uses zero based budgeting, the

organization is able to keep check on the amount of inflows and outflows of the cash. The

enterprise will able to know whether the organization is having positive or negative cash

flows. It helps to improves the financial security of the organization(Lepori and

Montauti, 2020)

7.) Customisation the budget to meet the dynamic needs : ZBD enables the organization to

prepare the budget in a flexible manner. It allows to modify the budgets. The firm can

increase or decrease the amount in any area.

8.) Justification of each expenditure – The zero based budgeting helps in knowing the

preferences and selecting the expenditures which are required on priority basis. This

method helps in attempting delegation of authority.

There are various cons of the zero based budgeting which can be described as given below:

1. Costly and expensive : In ZBD, it involves various new software and workflows which

require training and extra time. It raises the additional cost of the firm and constraint of

time is also a big issue while framing the ZBD budget.

2. Includes subjectivity : While preparing the zero based budget, there are some qualitative

factors which interrupt the decision making power and the personal perspectives of the

budgeter disrupt the budget.

3. Savvy budgeters manipulate the zero based process – There are various budgeters who

manipulates the approach used in the zero based budgeting process and leads to wrong

justification of the budgets maintained(Tellier, 2019)

4. Unpredictable income – In every organisation, there are some sources of income which

are unpredictable and occurs suddenly in the monthly income levels. The unpredictable

sources of income, disturb the budget maintained and declines the management efficiency

of the firm.

9

and thoughts in the decision making of the organization.

5.) Reduction in the redundant activities : the process of zero based budgeting helps in

knowing the activities which improve the returns of the organization and helps to

increase the revenue of the enterprise.

6.) Keep aware about cash flows : when an organization uses zero based budgeting, the

organization is able to keep check on the amount of inflows and outflows of the cash. The

enterprise will able to know whether the organization is having positive or negative cash

flows. It helps to improves the financial security of the organization(Lepori and

Montauti, 2020)

7.) Customisation the budget to meet the dynamic needs : ZBD enables the organization to

prepare the budget in a flexible manner. It allows to modify the budgets. The firm can

increase or decrease the amount in any area.

8.) Justification of each expenditure – The zero based budgeting helps in knowing the

preferences and selecting the expenditures which are required on priority basis. This

method helps in attempting delegation of authority.

There are various cons of the zero based budgeting which can be described as given below:

1. Costly and expensive : In ZBD, it involves various new software and workflows which

require training and extra time. It raises the additional cost of the firm and constraint of

time is also a big issue while framing the ZBD budget.

2. Includes subjectivity : While preparing the zero based budget, there are some qualitative

factors which interrupt the decision making power and the personal perspectives of the

budgeter disrupt the budget.

3. Savvy budgeters manipulate the zero based process – There are various budgeters who

manipulates the approach used in the zero based budgeting process and leads to wrong

justification of the budgets maintained(Tellier, 2019)

4. Unpredictable income – In every organisation, there are some sources of income which

are unpredictable and occurs suddenly in the monthly income levels. The unpredictable

sources of income, disturb the budget maintained and declines the management efficiency

of the firm.

9

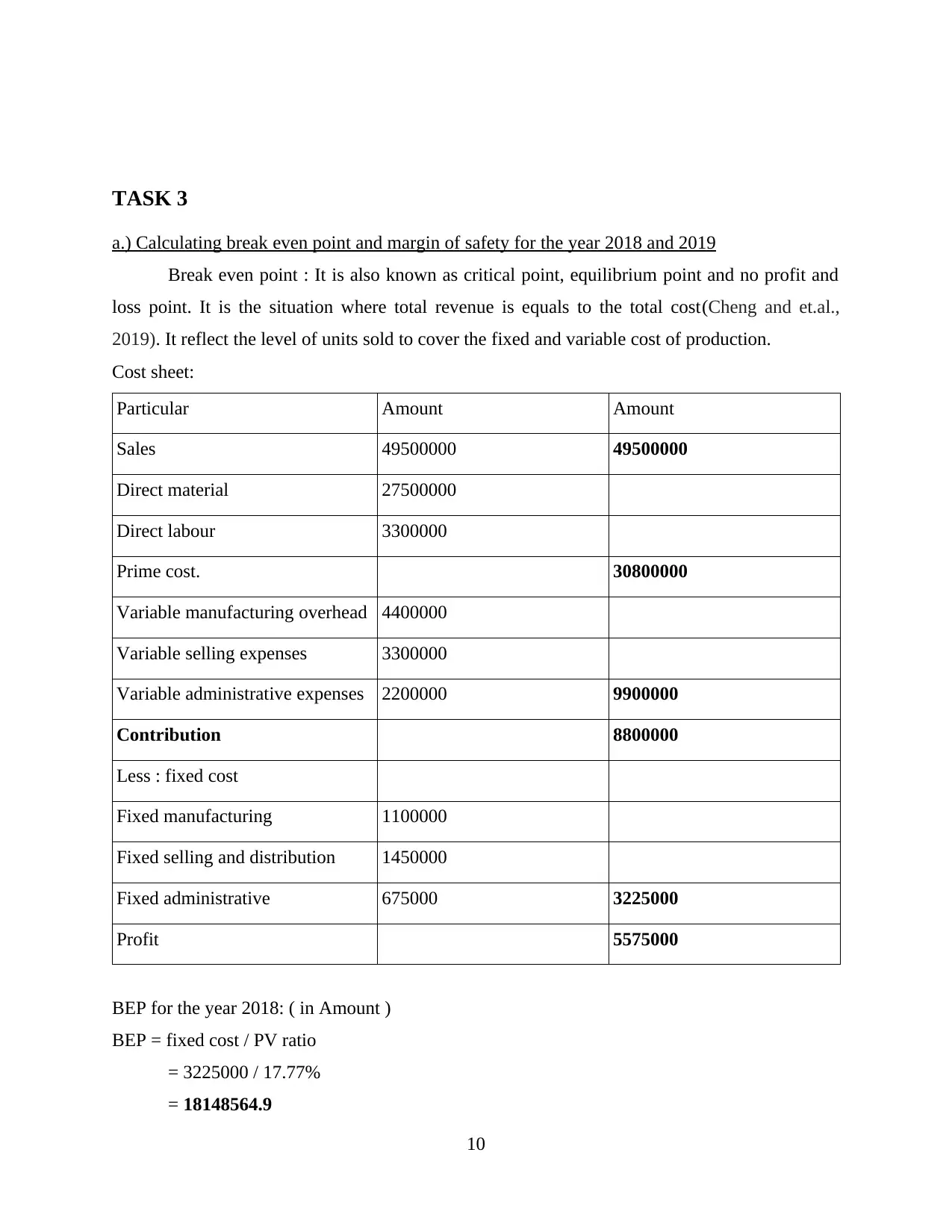

TASK 3

a.) Calculating break even point and margin of safety for the year 2018 and 2019

Break even point : It is also known as critical point, equilibrium point and no profit and

loss point. It is the situation where total revenue is equals to the total cost(Cheng and et.al.,

2019). It reflect the level of units sold to cover the fixed and variable cost of production.

Cost sheet:

Particular Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

Less : fixed cost

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

BEP for the year 2018: ( in Amount )

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.9

10

a.) Calculating break even point and margin of safety for the year 2018 and 2019

Break even point : It is also known as critical point, equilibrium point and no profit and

loss point. It is the situation where total revenue is equals to the total cost(Cheng and et.al.,

2019). It reflect the level of units sold to cover the fixed and variable cost of production.

Cost sheet:

Particular Amount Amount

Sales 49500000 49500000

Direct material 27500000

Direct labour 3300000

Prime cost. 30800000

Variable manufacturing overhead 4400000

Variable selling expenses 3300000

Variable administrative expenses 2200000 9900000

Contribution 8800000

Less : fixed cost

Fixed manufacturing 1100000

Fixed selling and distribution 1450000

Fixed administrative 675000 3225000

Profit 5575000

BEP for the year 2018: ( in Amount )

BEP = fixed cost / PV ratio

= 3225000 / 17.77%

= 18148564.9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.