Financial and Cost Accounting: Analysis and Assessment Assignment

VerifiedAdded on 2020/03/16

|14

|2291

|37

Homework Assignment

AI Summary

This document presents solutions to an accounting assessment, encompassing various aspects of financial and cost accounting. The answers cover topics such as the users of accounting information, the importance of an accounting system, steps for data accuracy, and the differences between financial and cost accounting. Further solutions include manufacturing statements, inventory valuation methods (FIFO, LIFO, weighted average), variance analysis (materials and labor), and break-even analysis. The assessment also includes case studies and true/false questions related to cost accounting principles and job costing.

Assessment 1

Answer to Question 1

At the time of making business decisions, accounting data and information play an

integral part. It can be seen that there are many users of accounting information in the

business world. Three of the major users of accounting data are discussed below:

Management of the Companies: One of the major tasks of the management is to measure

the performance of the business organizations. For this reason, the management of the

companies needs accounting data and information to measure the financial performance of

the companies (Hall 2012).

Investors of the Companies: Before making investment decisions, the investors need to

make sure that they can get good return from the company. In this process, accounting data

provide them great assistance as they help the investors in making right investment decisions

(Simkin, Norman and Rose 2014).

Regulatory Authorities: In order to make sure that the disclosure of accounting information

of the companies is done according to the rules and regulations, the regulatory authorities

need the help of organizational accounting data (Hall 2012).

Answer to Question 2

It is important for every business organization to establish an appropriate accounting

system due to the following reasons:

Answer to Question 1

At the time of making business decisions, accounting data and information play an

integral part. It can be seen that there are many users of accounting information in the

business world. Three of the major users of accounting data are discussed below:

Management of the Companies: One of the major tasks of the management is to measure

the performance of the business organizations. For this reason, the management of the

companies needs accounting data and information to measure the financial performance of

the companies (Hall 2012).

Investors of the Companies: Before making investment decisions, the investors need to

make sure that they can get good return from the company. In this process, accounting data

provide them great assistance as they help the investors in making right investment decisions

(Simkin, Norman and Rose 2014).

Regulatory Authorities: In order to make sure that the disclosure of accounting information

of the companies is done according to the rules and regulations, the regulatory authorities

need the help of organizational accounting data (Hall 2012).

Answer to Question 2

It is important for every business organization to establish an appropriate accounting

system due to the following reasons:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appropriate accounting system helps the business organizations in capturing the

relevant accounting and financial information so that they can provide assistance in

the business decision-making process (Knežević, Stanković and Tepavac 2012).

Appropriate accounting system helps the business organizations to bring innovation in

the accounting practices so that it can become more efficient.

Appropriate accounting system helps in the effective communication of accounting

and financial information in the business organizations. These are the major reason

for the establishment of appropriate accounting system in the companies (Emeka-

Nwokeji 2012).

Name of some of the common accounting system are Accounting Suite, Accounting by

Wave, Dynamics, QuickBooks, AvaTax, DeltekCostpoint, Accounting Xpert and others

(Emeka-Nwokeji 2012).

Answer to Question 3

There are certain steps to code, classify and check for accuracy and reliability of the

organizational data in the organizational accounting system. They are discussed below:

In the first step, the accountants of the companies need to ensure that all the

accounting values are put in the correct way under each accounting heads.

After that, in case there is any doubt, the accountants need to check the put amounts

with the actual amount or balance.

In case, there is any indication of fraudulent in the accounting information, it is the

responsibility of the accountants to take actions against those errors (Romney and

Steinbart 2012).

relevant accounting and financial information so that they can provide assistance in

the business decision-making process (Knežević, Stanković and Tepavac 2012).

Appropriate accounting system helps the business organizations to bring innovation in

the accounting practices so that it can become more efficient.

Appropriate accounting system helps in the effective communication of accounting

and financial information in the business organizations. These are the major reason

for the establishment of appropriate accounting system in the companies (Emeka-

Nwokeji 2012).

Name of some of the common accounting system are Accounting Suite, Accounting by

Wave, Dynamics, QuickBooks, AvaTax, DeltekCostpoint, Accounting Xpert and others

(Emeka-Nwokeji 2012).

Answer to Question 3

There are certain steps to code, classify and check for accuracy and reliability of the

organizational data in the organizational accounting system. They are discussed below:

In the first step, the accountants of the companies need to ensure that all the

accounting values are put in the correct way under each accounting heads.

After that, in case there is any doubt, the accountants need to check the put amounts

with the actual amount or balance.

In case, there is any indication of fraudulent in the accounting information, it is the

responsibility of the accountants to take actions against those errors (Romney and

Steinbart 2012).

Answer to Question 4

Financial Accounting vs. Cost Accounting: Financial Accounting (FA) keeps track of the

financial information of the companies where Cost Accounting (CA) keeps track of various

costs of the companies. Thus, the information of FA includes information related to monetary

terms while the information of CA includes the information related with material, labor and

overhead of the companies. The users of FA are creditors, investors and customers of the

companies. The users of CA are employees, directors, supervisors, managers and others

(Horngrenet al. 2012).

Management Accounting vs. Cost Accounting: The main objective of CA is to assist the

managers in cost control process and decision-making process while the main objective of

Management Accounting (MA) is to assist the organizational managers in the process of

planning, controlling, performance evaluation and decision-making. CA includes the

principles of only cost accounting while MA includes the principles of both cost accounting

and financial accounting (Horngrenet al. 2012).

Answer to Question 5

Cost Accounting helps the organizational managers in the process of organizational

planning and controlling by providing them with appropriate cost and accounting

information. In order to establish effective internal control in the organizations, the

organizational managers need information regarding cost of the company and cost accounting

does the work for them. In addition, in the presence of effective cost information, the

organizational managers become able to plan the future business activities of the companies.

Thus, cost accounting is very much important for organizational planning and controlling

(Drury 2013).

Financial Accounting vs. Cost Accounting: Financial Accounting (FA) keeps track of the

financial information of the companies where Cost Accounting (CA) keeps track of various

costs of the companies. Thus, the information of FA includes information related to monetary

terms while the information of CA includes the information related with material, labor and

overhead of the companies. The users of FA are creditors, investors and customers of the

companies. The users of CA are employees, directors, supervisors, managers and others

(Horngrenet al. 2012).

Management Accounting vs. Cost Accounting: The main objective of CA is to assist the

managers in cost control process and decision-making process while the main objective of

Management Accounting (MA) is to assist the organizational managers in the process of

planning, controlling, performance evaluation and decision-making. CA includes the

principles of only cost accounting while MA includes the principles of both cost accounting

and financial accounting (Horngrenet al. 2012).

Answer to Question 5

Cost Accounting helps the organizational managers in the process of organizational

planning and controlling by providing them with appropriate cost and accounting

information. In order to establish effective internal control in the organizations, the

organizational managers need information regarding cost of the company and cost accounting

does the work for them. In addition, in the presence of effective cost information, the

organizational managers become able to plan the future business activities of the companies.

Thus, cost accounting is very much important for organizational planning and controlling

(Drury 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Answer to Question No 6

In the Books of

Casco Manufacturing Company

Manufacturing Statement

For the year ended 30 June, 2014

Particulars Amount (in $) Amount (in $)

Direct materials:

Beginning raw materials

49,00

0

Add: Net purchases of raw

materials

198,00

0

Raw materials available

247,00

0

Less: Closing raw materials

42,00

0

Raw materials transferred

to production

205,00

0

Direct labour

205,00

0

Manufacturing overhead

173,00

0

Total manufacturing costs

583,00

0

Add: Beginning work-in-

process inventory

28,00

0

In the Books of

Casco Manufacturing Company

Manufacturing Statement

For the year ended 30 June, 2014

Particulars Amount (in $) Amount (in $)

Direct materials:

Beginning raw materials

49,00

0

Add: Net purchases of raw

materials

198,00

0

Raw materials available

247,00

0

Less: Closing raw materials

42,00

0

Raw materials transferred

to production

205,00

0

Direct labour

205,00

0

Manufacturing overhead

173,00

0

Total manufacturing costs

583,00

0

Add: Beginning work-in-

process inventory

28,00

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

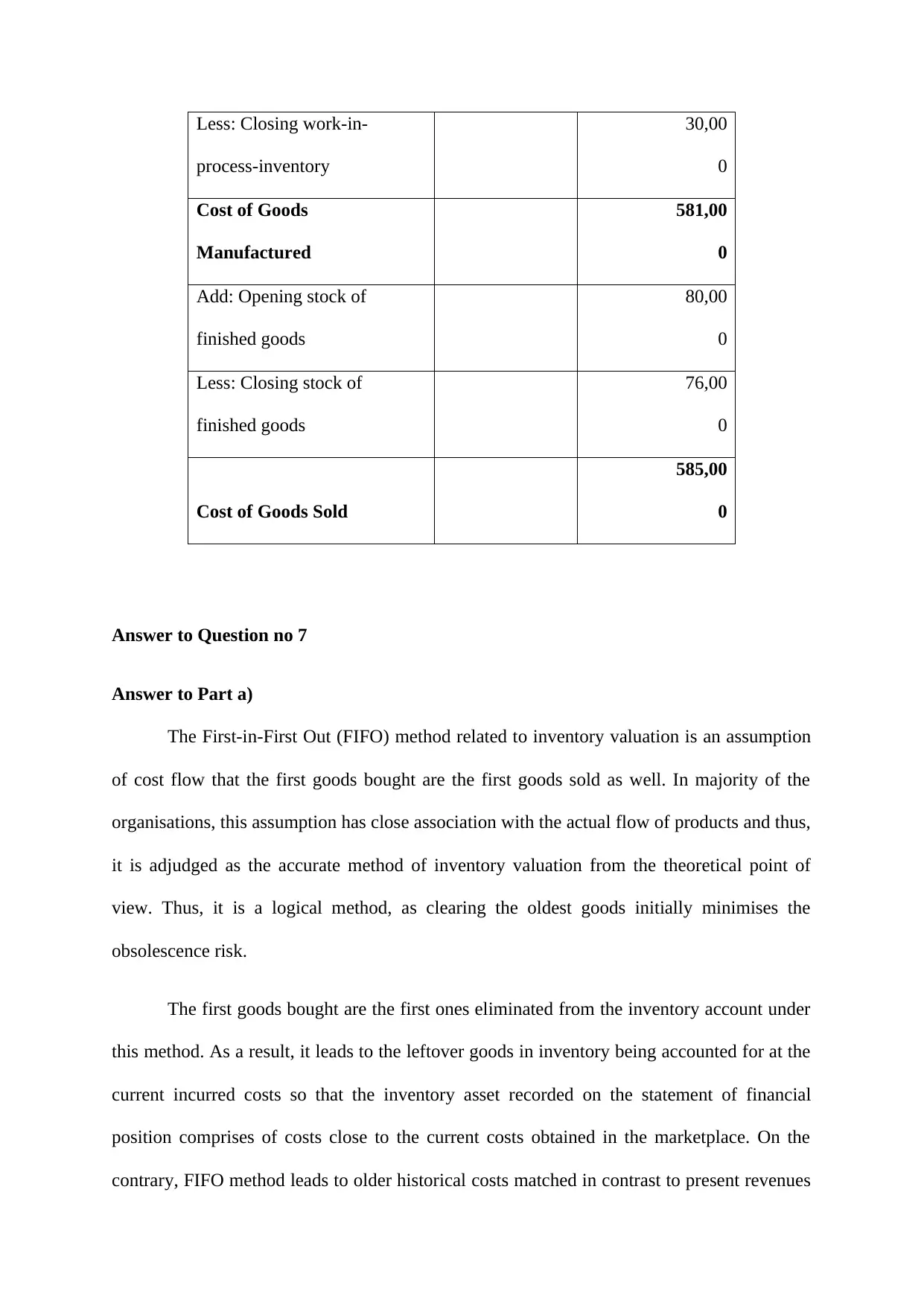

Less: Closing work-in-

process-inventory

30,00

0

Cost of Goods

Manufactured

581,00

0

Add: Opening stock of

finished goods

80,00

0

Less: Closing stock of

finished goods

76,00

0

Cost of Goods Sold

585,00

0

Answer to Question no 7

Answer to Part a)

The First-in-First Out (FIFO) method related to inventory valuation is an assumption

of cost flow that the first goods bought are the first goods sold as well. In majority of the

organisations, this assumption has close association with the actual flow of products and thus,

it is adjudged as the accurate method of inventory valuation from the theoretical point of

view. Thus, it is a logical method, as clearing the oldest goods initially minimises the

obsolescence risk.

The first goods bought are the first ones eliminated from the inventory account under

this method. As a result, it leads to the leftover goods in inventory being accounted for at the

current incurred costs so that the inventory asset recorded on the statement of financial

position comprises of costs close to the current costs obtained in the marketplace. On the

contrary, FIFO method leads to older historical costs matched in contrast to present revenues

process-inventory

30,00

0

Cost of Goods

Manufactured

581,00

0

Add: Opening stock of

finished goods

80,00

0

Less: Closing stock of

finished goods

76,00

0

Cost of Goods Sold

585,00

0

Answer to Question no 7

Answer to Part a)

The First-in-First Out (FIFO) method related to inventory valuation is an assumption

of cost flow that the first goods bought are the first goods sold as well. In majority of the

organisations, this assumption has close association with the actual flow of products and thus,

it is adjudged as the accurate method of inventory valuation from the theoretical point of

view. Thus, it is a logical method, as clearing the oldest goods initially minimises the

obsolescence risk.

The first goods bought are the first ones eliminated from the inventory account under

this method. As a result, it leads to the leftover goods in inventory being accounted for at the

current incurred costs so that the inventory asset recorded on the statement of financial

position comprises of costs close to the current costs obtained in the marketplace. On the

contrary, FIFO method leads to older historical costs matched in contrast to present revenues

along with the cost of sales. This implies that gross margin does not depict effective matching

of costs and revenues.

Answer to Part b)

Last-in-First-Out (LIFO) method is utilised for placing an accounting value on

inventory. This method is based on the assumption that the final item of inventory bought is

the first item sold. However, this method is used rarely in practice. If an organisation has to

utilise the process flow that LIFO has embodied, a major portion of its inventory would be

extremely old and this is likely to become obsolete. On the other hand, with the help of this

method, the organisation could cope up with the inflating prices, since the inventory cost rises

with the passage of time.

Answer to Part c)

The weighted average cost or moving average method is utilised in assigning the

average production cost to a product. This method is used in situations, in which the

inventory items are intermingled in such a manner that it is not possible to apportion a

particular cost to an individual unit. In addition, this method is useful when the accounting

system of an organisation is not sophisticated adequately in identifying FIFO or LIFO layers

of inventory. Finally, weighted average cost method is beneficial when there is greater

commoditisation of inventory items, in which there is no option for apportioning cost to an

individual unit.

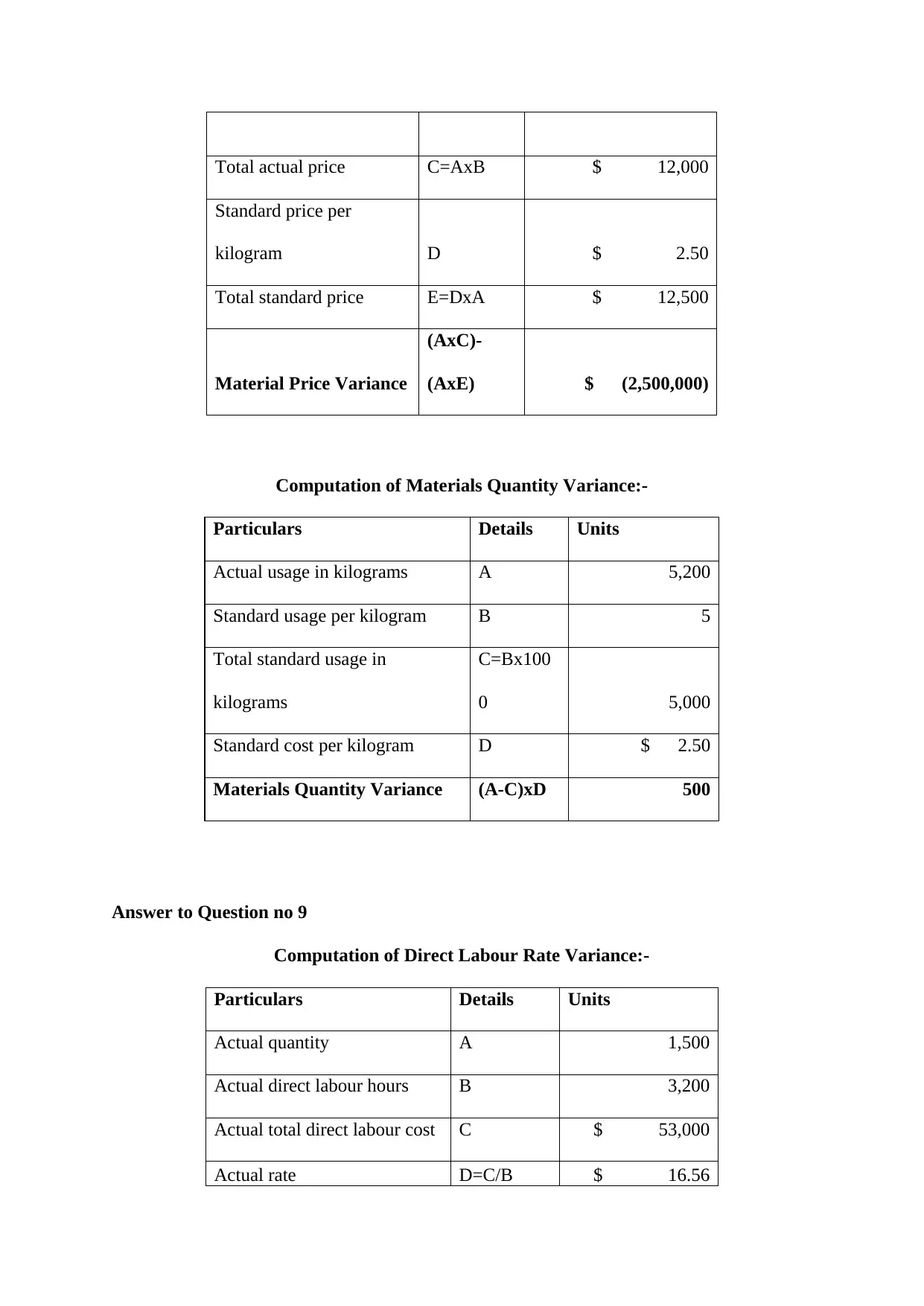

Answer to Question no 8

Computation of Materials Price Variance:-

Particulars Details Units

Actual quantity A 5,000

Actual price per kilogram B $ 2.40

of costs and revenues.

Answer to Part b)

Last-in-First-Out (LIFO) method is utilised for placing an accounting value on

inventory. This method is based on the assumption that the final item of inventory bought is

the first item sold. However, this method is used rarely in practice. If an organisation has to

utilise the process flow that LIFO has embodied, a major portion of its inventory would be

extremely old and this is likely to become obsolete. On the other hand, with the help of this

method, the organisation could cope up with the inflating prices, since the inventory cost rises

with the passage of time.

Answer to Part c)

The weighted average cost or moving average method is utilised in assigning the

average production cost to a product. This method is used in situations, in which the

inventory items are intermingled in such a manner that it is not possible to apportion a

particular cost to an individual unit. In addition, this method is useful when the accounting

system of an organisation is not sophisticated adequately in identifying FIFO or LIFO layers

of inventory. Finally, weighted average cost method is beneficial when there is greater

commoditisation of inventory items, in which there is no option for apportioning cost to an

individual unit.

Answer to Question no 8

Computation of Materials Price Variance:-

Particulars Details Units

Actual quantity A 5,000

Actual price per kilogram B $ 2.40

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total actual price C=AxB $ 12,000

Standard price per

kilogram D $ 2.50

Total standard price E=DxA $ 12,500

Material Price Variance

(AxC)-

(AxE) $ (2,500,000)

Computation of Materials Quantity Variance:-

Particulars Details Units

Actual usage in kilograms A 5,200

Standard usage per kilogram B 5

Total standard usage in

kilograms

C=Bx100

0 5,000

Standard cost per kilogram D $ 2.50

Materials Quantity Variance (A-C)xD 500

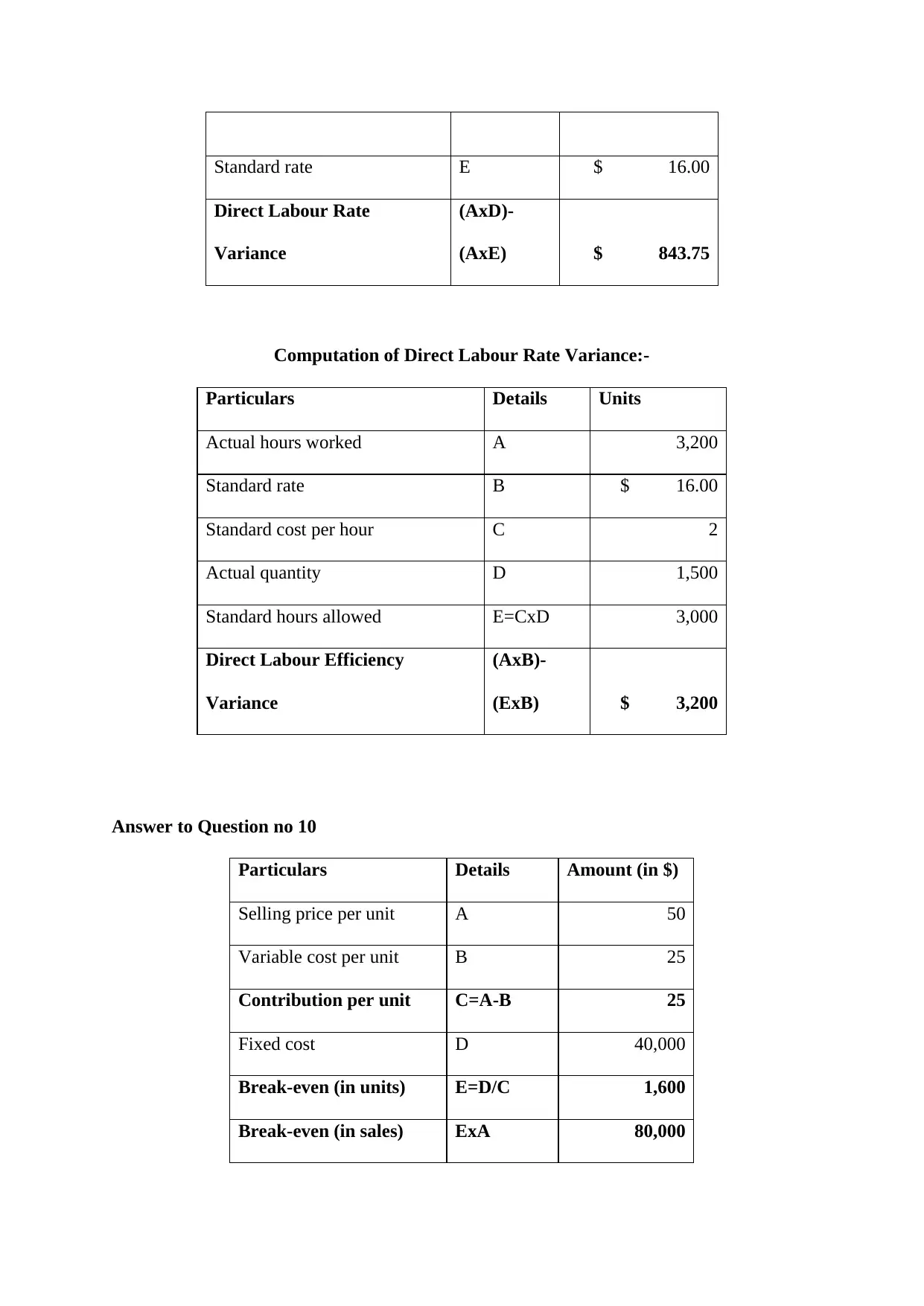

Answer to Question no 9

Computation of Direct Labour Rate Variance:-

Particulars Details Units

Actual quantity A 1,500

Actual direct labour hours B 3,200

Actual total direct labour cost C $ 53,000

Actual rate D=C/B $ 16.56

Standard price per

kilogram D $ 2.50

Total standard price E=DxA $ 12,500

Material Price Variance

(AxC)-

(AxE) $ (2,500,000)

Computation of Materials Quantity Variance:-

Particulars Details Units

Actual usage in kilograms A 5,200

Standard usage per kilogram B 5

Total standard usage in

kilograms

C=Bx100

0 5,000

Standard cost per kilogram D $ 2.50

Materials Quantity Variance (A-C)xD 500

Answer to Question no 9

Computation of Direct Labour Rate Variance:-

Particulars Details Units

Actual quantity A 1,500

Actual direct labour hours B 3,200

Actual total direct labour cost C $ 53,000

Actual rate D=C/B $ 16.56

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Standard rate E $ 16.00

Direct Labour Rate

Variance

(AxD)-

(AxE) $ 843.75

Computation of Direct Labour Rate Variance:-

Particulars Details Units

Actual hours worked A 3,200

Standard rate B $ 16.00

Standard cost per hour C 2

Actual quantity D 1,500

Standard hours allowed E=CxD 3,000

Direct Labour Efficiency

Variance

(AxB)-

(ExB) $ 3,200

Answer to Question no 10

Particulars Details Amount (in $)

Selling price per unit A 50

Variable cost per unit B 25

Contribution per unit C=A-B 25

Fixed cost D 40,000

Break-even (in units) E=D/C 1,600

Break-even (in sales) ExA 80,000

Direct Labour Rate

Variance

(AxD)-

(AxE) $ 843.75

Computation of Direct Labour Rate Variance:-

Particulars Details Units

Actual hours worked A 3,200

Standard rate B $ 16.00

Standard cost per hour C 2

Actual quantity D 1,500

Standard hours allowed E=CxD 3,000

Direct Labour Efficiency

Variance

(AxB)-

(ExB) $ 3,200

Answer to Question no 10

Particulars Details Amount (in $)

Selling price per unit A 50

Variable cost per unit B 25

Contribution per unit C=A-B 25

Fixed cost D 40,000

Break-even (in units) E=D/C 1,600

Break-even (in sales) ExA 80,000

Assessment 2

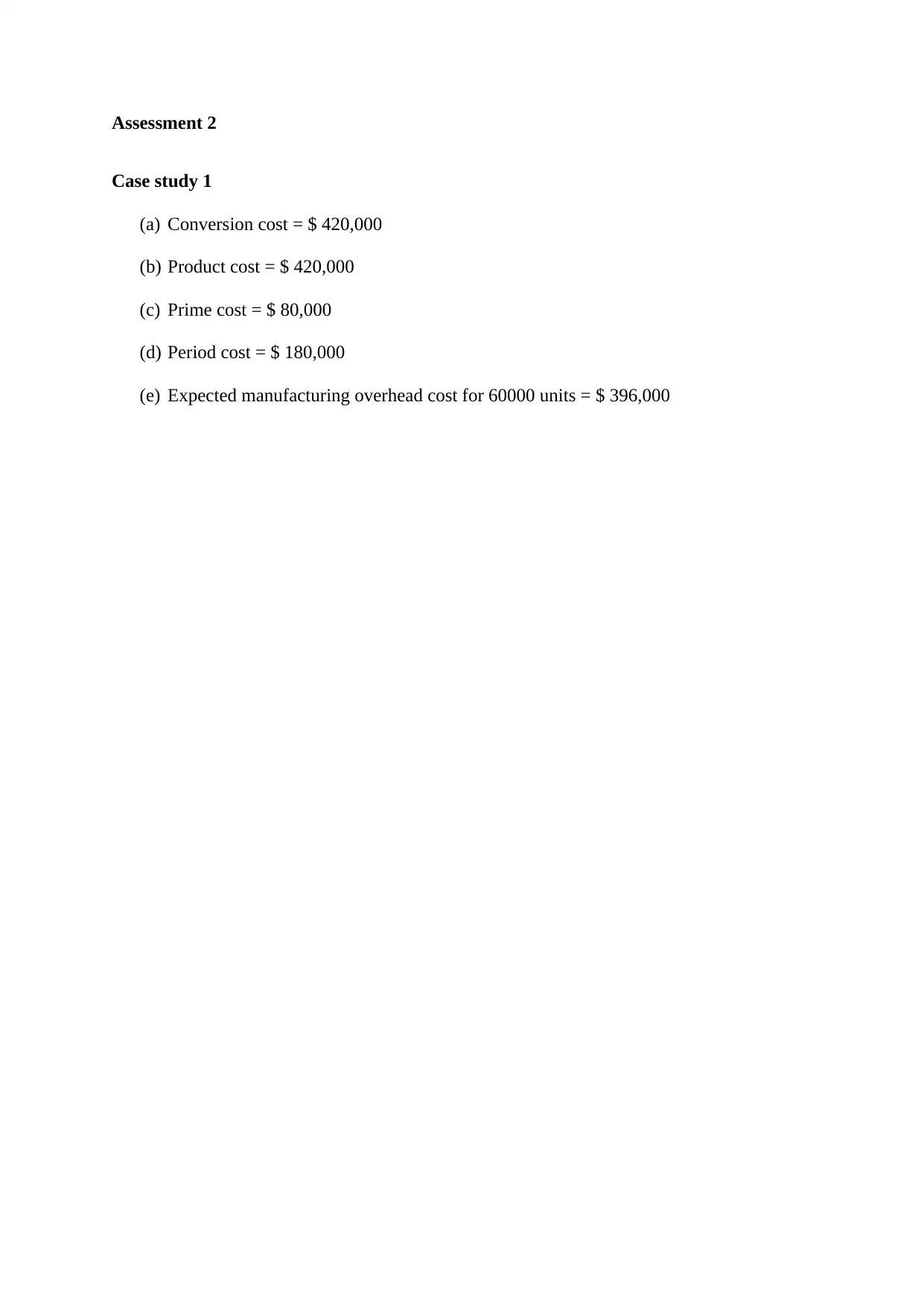

Case study 1

(a) Conversion cost = $ 420,000

(b) Product cost = $ 420,000

(c) Prime cost = $ 80,000

(d) Period cost = $ 180,000

(e) Expected manufacturing overhead cost for 60000 units = $ 396,000

Case study 1

(a) Conversion cost = $ 420,000

(b) Product cost = $ 420,000

(c) Prime cost = $ 80,000

(d) Period cost = $ 180,000

(e) Expected manufacturing overhead cost for 60000 units = $ 396,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

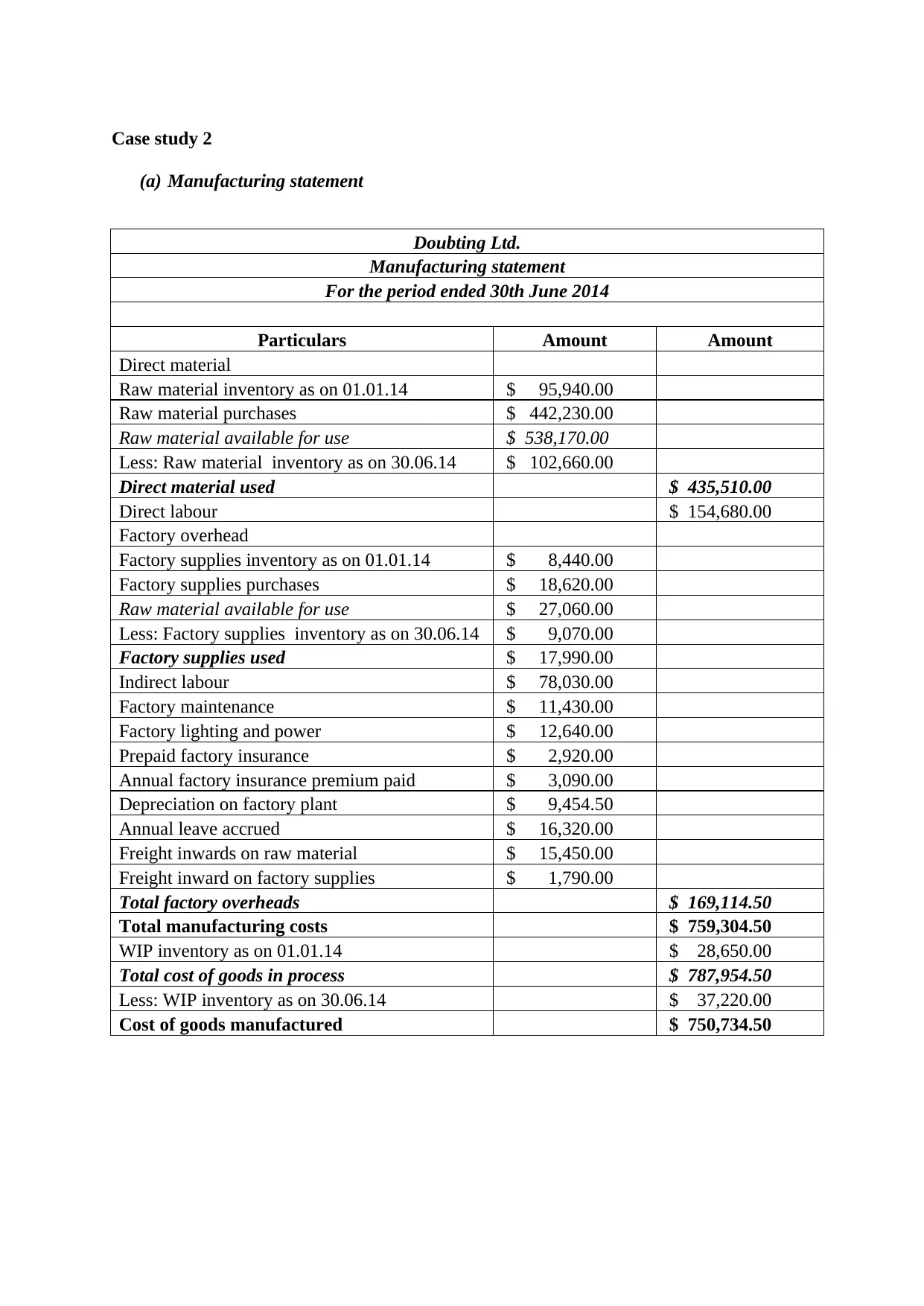

Case study 2

(a) Manufacturing statement

Doubting Ltd.

Manufacturing statement

For the period ended 30th June 2014

Particulars Amount Amount

Direct material

Raw material inventory as on 01.01.14 $ 95,940.00

Raw material purchases $ 442,230.00

Raw material available for use $ 538,170.00

Less: Raw material inventory as on 30.06.14 $ 102,660.00

Direct material used $ 435,510.00

Direct labour $ 154,680.00

Factory overhead

Factory supplies inventory as on 01.01.14 $ 8,440.00

Factory supplies purchases $ 18,620.00

Raw material available for use $ 27,060.00

Less: Factory supplies inventory as on 30.06.14 $ 9,070.00

Factory supplies used $ 17,990.00

Indirect labour $ 78,030.00

Factory maintenance $ 11,430.00

Factory lighting and power $ 12,640.00

Prepaid factory insurance $ 2,920.00

Annual factory insurance premium paid $ 3,090.00

Depreciation on factory plant $ 9,454.50

Annual leave accrued $ 16,320.00

Freight inwards on raw material $ 15,450.00

Freight inward on factory supplies $ 1,790.00

Total factory overheads $ 169,114.50

Total manufacturing costs $ 759,304.50

WIP inventory as on 01.01.14 $ 28,650.00

Total cost of goods in process $ 787,954.50

Less: WIP inventory as on 30.06.14 $ 37,220.00

Cost of goods manufactured $ 750,734.50

(a) Manufacturing statement

Doubting Ltd.

Manufacturing statement

For the period ended 30th June 2014

Particulars Amount Amount

Direct material

Raw material inventory as on 01.01.14 $ 95,940.00

Raw material purchases $ 442,230.00

Raw material available for use $ 538,170.00

Less: Raw material inventory as on 30.06.14 $ 102,660.00

Direct material used $ 435,510.00

Direct labour $ 154,680.00

Factory overhead

Factory supplies inventory as on 01.01.14 $ 8,440.00

Factory supplies purchases $ 18,620.00

Raw material available for use $ 27,060.00

Less: Factory supplies inventory as on 30.06.14 $ 9,070.00

Factory supplies used $ 17,990.00

Indirect labour $ 78,030.00

Factory maintenance $ 11,430.00

Factory lighting and power $ 12,640.00

Prepaid factory insurance $ 2,920.00

Annual factory insurance premium paid $ 3,090.00

Depreciation on factory plant $ 9,454.50

Annual leave accrued $ 16,320.00

Freight inwards on raw material $ 15,450.00

Freight inward on factory supplies $ 1,790.00

Total factory overheads $ 169,114.50

Total manufacturing costs $ 759,304.50

WIP inventory as on 01.01.14 $ 28,650.00

Total cost of goods in process $ 787,954.50

Less: WIP inventory as on 30.06.14 $ 37,220.00

Cost of goods manufactured $ 750,734.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

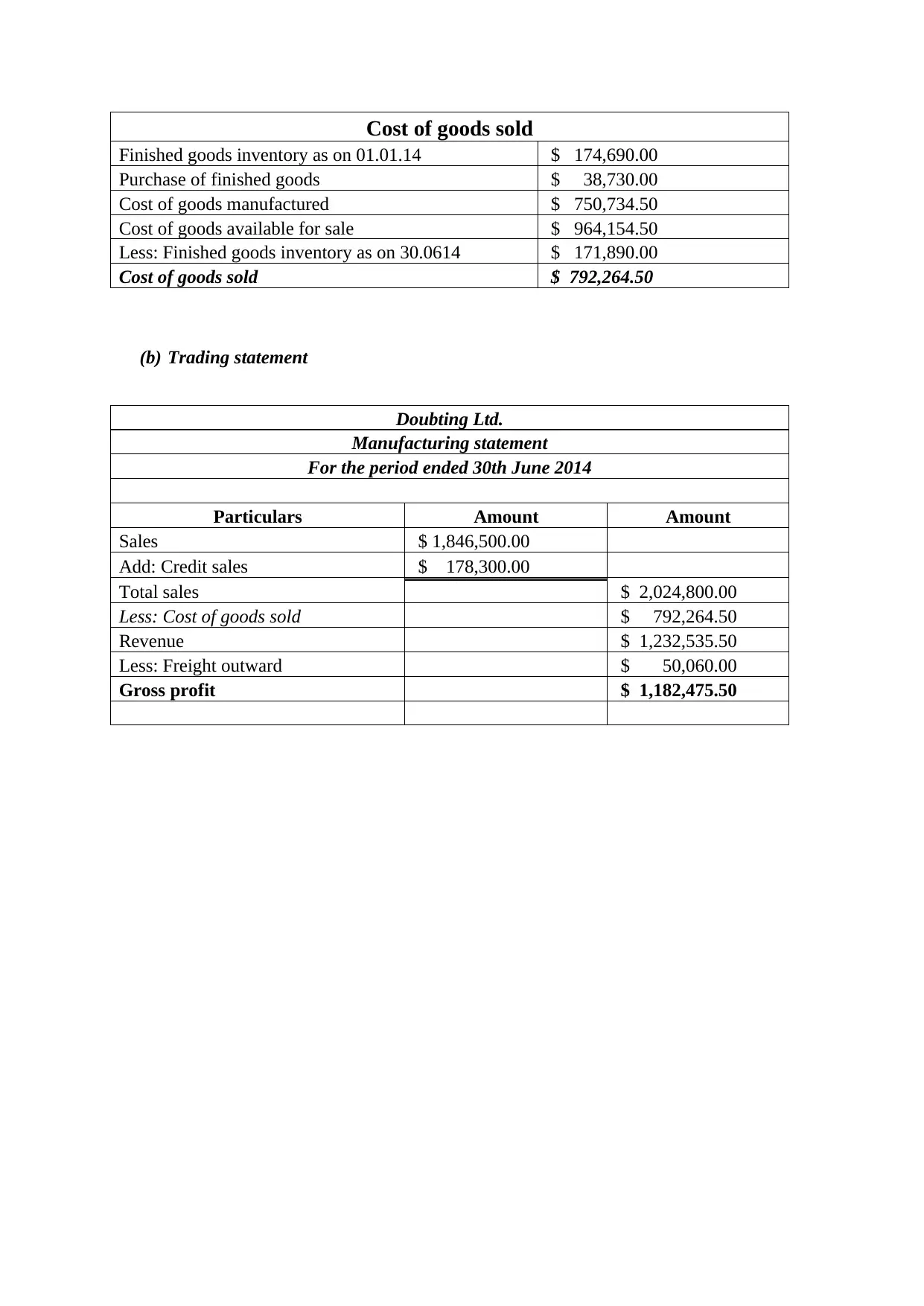

Cost of goods sold

Finished goods inventory as on 01.01.14 $ 174,690.00

Purchase of finished goods $ 38,730.00

Cost of goods manufactured $ 750,734.50

Cost of goods available for sale $ 964,154.50

Less: Finished goods inventory as on 30.0614 $ 171,890.00

Cost of goods sold $ 792,264.50

(b) Trading statement

Doubting Ltd.

Manufacturing statement

For the period ended 30th June 2014

Particulars Amount Amount

Sales $ 1,846,500.00

Add: Credit sales $ 178,300.00

Total sales $ 2,024,800.00

Less: Cost of goods sold $ 792,264.50

Revenue $ 1,232,535.50

Less: Freight outward $ 50,060.00

Gross profit $ 1,182,475.50

Finished goods inventory as on 01.01.14 $ 174,690.00

Purchase of finished goods $ 38,730.00

Cost of goods manufactured $ 750,734.50

Cost of goods available for sale $ 964,154.50

Less: Finished goods inventory as on 30.0614 $ 171,890.00

Cost of goods sold $ 792,264.50

(b) Trading statement

Doubting Ltd.

Manufacturing statement

For the period ended 30th June 2014

Particulars Amount Amount

Sales $ 1,846,500.00

Add: Credit sales $ 178,300.00

Total sales $ 2,024,800.00

Less: Cost of goods sold $ 792,264.50

Revenue $ 1,232,535.50

Less: Freight outward $ 50,060.00

Gross profit $ 1,182,475.50

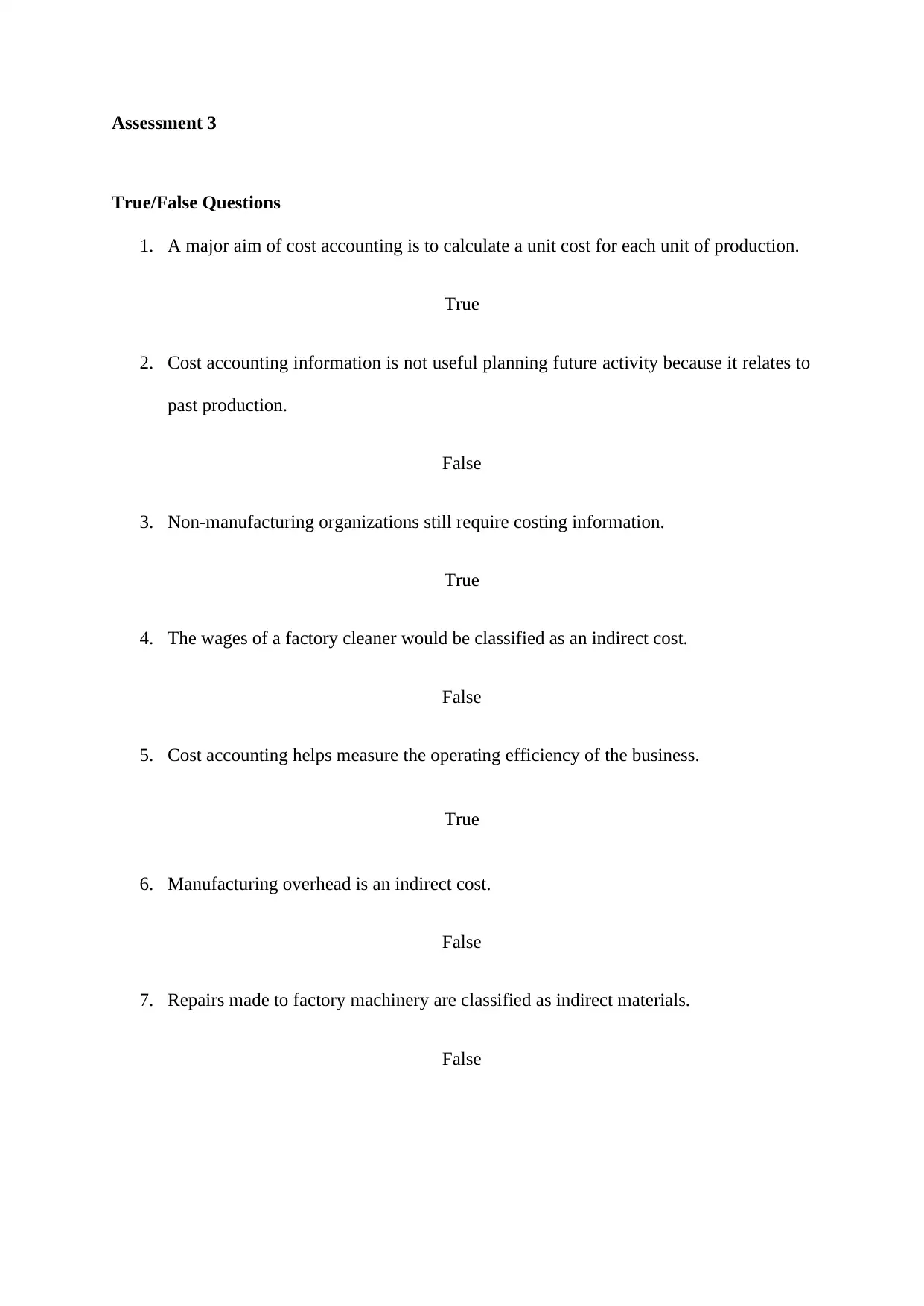

Assessment 3

True/False Questions

1. A major aim of cost accounting is to calculate a unit cost for each unit of production.

True

2. Cost accounting information is not useful planning future activity because it relates to

past production.

False

3. Non-manufacturing organizations still require costing information.

True

4. The wages of a factory cleaner would be classified as an indirect cost.

False

5. Cost accounting helps measure the operating efficiency of the business.

True

6. Manufacturing overhead is an indirect cost.

False

7. Repairs made to factory machinery are classified as indirect materials.

False

True/False Questions

1. A major aim of cost accounting is to calculate a unit cost for each unit of production.

True

2. Cost accounting information is not useful planning future activity because it relates to

past production.

False

3. Non-manufacturing organizations still require costing information.

True

4. The wages of a factory cleaner would be classified as an indirect cost.

False

5. Cost accounting helps measure the operating efficiency of the business.

True

6. Manufacturing overhead is an indirect cost.

False

7. Repairs made to factory machinery are classified as indirect materials.

False

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.