Accounting and Finance Report: Cranswick Plc Financial Analysis

VerifiedAdded on 2020/06/04

|17

|3805

|20

Report

AI Summary

This report presents a comprehensive financial analysis of Cranswick Plc, a leading British food production company. It examines the company's financial position from 2013 to 2017 using ratio analysis, focusing on profitability, earnings, and dividends to assess business performance. The analysis includes calculations and interpretations of gross profit ratio, net profit ratio, earnings per share, price-earnings ratio, and dividend per share. Furthermore, the report evaluates financial stability and liquidity through current and acid-test ratios, and solvency using debt-to-equity and interest-bearing ratios. The corporate governance mechanism is also evaluated. The report concludes with an assessment of investment opportunities based on the financial data, offering insights into Cranswick's performance and future prospects within the food industry.

ACCOUNTING AND

FINANCE

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION A.....................................................................................................................................1

Profit, earnings & dividends...................................................................................................1

Profitability ratios..............................................................................................................1

Earnings ratios...................................................................................................................3

Dividend ratios...................................................................................................................5

Financial stability & liquidity.................................................................................................7

Liquidity analysis ..............................................................................................................7

Solvency analysis...............................................................................................................8

SECTION B.....................................................................................................................................9

Critical reflection on the company portrayed by financial reports.........................................9

An evaluation of the corporate governance ...........................................................................9

Identify the assets value per share and the current market share price to assess investment

opportunity...........................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

SECTION A.....................................................................................................................................1

Profit, earnings & dividends...................................................................................................1

Profitability ratios..............................................................................................................1

Earnings ratios...................................................................................................................3

Dividend ratios...................................................................................................................5

Financial stability & liquidity.................................................................................................7

Liquidity analysis ..............................................................................................................7

Solvency analysis...............................................................................................................8

SECTION B.....................................................................................................................................9

Critical reflection on the company portrayed by financial reports.........................................9

An evaluation of the corporate governance ...........................................................................9

Identify the assets value per share and the current market share price to assess investment

opportunity...........................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting is a major area of the business functions which is concerned with the

recording, organizing and interpretation of the historical transactions that took place in an

organization. Finance, on the other hand, is a primary requirement of any establishment because

none of the firm regardless to their sizes can operate and survive in the market with inadequate

funding. Cranswick Plc is a British leading food production company which is listed on LSE at a

constituent of FTSE 250 Index. It offers premium, organic and sustainable food products in

variety of range to the consumers. The thrust of the report is to examine its financial position

through ratio analysis technique for evaluating its investment opportunity. Besides this, its

corporate governance mechanism also will be examined for sustainable success.

100

SECTION A

Profit, earnings & dividends

In order to determine performance of the company in its respective industry, there are

several numbers of ratios are calculated and then analysed. In the present section basically three

types of the ratios considered for assessing Cranswick's business performance which are

profitability, earnings and dividends (Uechi and et.al., 2015). Moreover, interpretation of such

ratios are given as below:

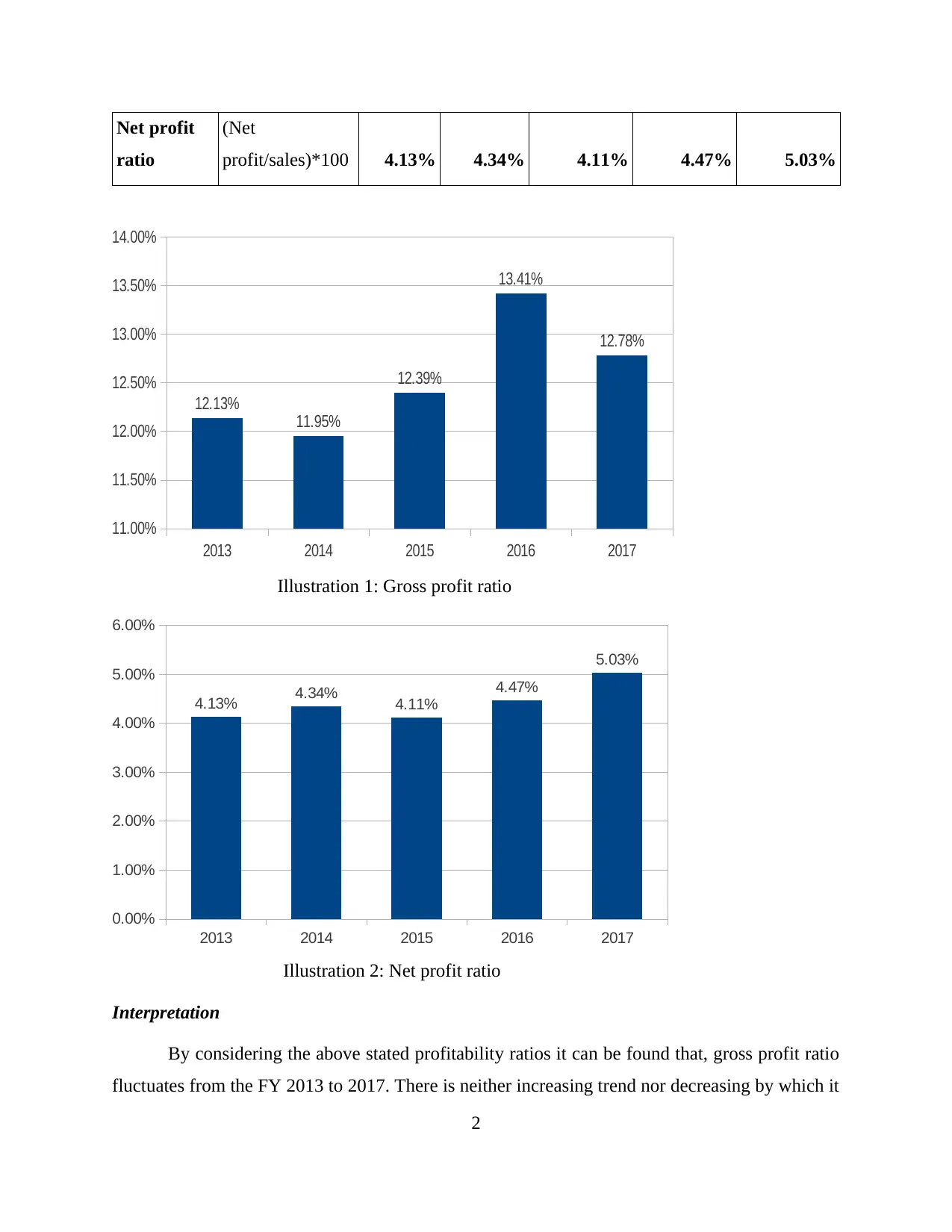

Profitability ratios

Profitabilit

y ratios Formula 2013 2014 2015 2016 2017

Gross

income 106.17 118.91 124.34 136.31 159.06

Net sales 875.17 994.91 1003.34 1016.31 1245.06

Gross profit

ratio

(Gross

profit/sales)*100 12.13% 11.95% 12.39% 13.41% 12.78%

Net income 36.14 43.21 41.25 45.4 62.64

Net sales 875.17 994.91 1003.34 1016.31 1245.06

1

Accounting is a major area of the business functions which is concerned with the

recording, organizing and interpretation of the historical transactions that took place in an

organization. Finance, on the other hand, is a primary requirement of any establishment because

none of the firm regardless to their sizes can operate and survive in the market with inadequate

funding. Cranswick Plc is a British leading food production company which is listed on LSE at a

constituent of FTSE 250 Index. It offers premium, organic and sustainable food products in

variety of range to the consumers. The thrust of the report is to examine its financial position

through ratio analysis technique for evaluating its investment opportunity. Besides this, its

corporate governance mechanism also will be examined for sustainable success.

100

SECTION A

Profit, earnings & dividends

In order to determine performance of the company in its respective industry, there are

several numbers of ratios are calculated and then analysed. In the present section basically three

types of the ratios considered for assessing Cranswick's business performance which are

profitability, earnings and dividends (Uechi and et.al., 2015). Moreover, interpretation of such

ratios are given as below:

Profitability ratios

Profitabilit

y ratios Formula 2013 2014 2015 2016 2017

Gross

income 106.17 118.91 124.34 136.31 159.06

Net sales 875.17 994.91 1003.34 1016.31 1245.06

Gross profit

ratio

(Gross

profit/sales)*100 12.13% 11.95% 12.39% 13.41% 12.78%

Net income 36.14 43.21 41.25 45.4 62.64

Net sales 875.17 994.91 1003.34 1016.31 1245.06

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net profit

ratio

(Net

profit/sales)*100 4.13% 4.34% 4.11% 4.47% 5.03%

2013 2014 2015 2016 2017

11.00%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

12.13%

11.95%

12.39%

13.41%

12.78%

Illustration 1: Gross profit ratio

2013 2014 2015 2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.13% 4.34% 4.11%

4.47%

5.03%

Illustration 2: Net profit ratio

Interpretation

By considering the above stated profitability ratios it can be found that, gross profit ratio

fluctuates from the FY 2013 to 2017. There is neither increasing trend nor decreasing by which it

2

ratio

(Net

profit/sales)*100 4.13% 4.34% 4.11% 4.47% 5.03%

2013 2014 2015 2016 2017

11.00%

11.50%

12.00%

12.50%

13.00%

13.50%

14.00%

12.13%

11.95%

12.39%

13.41%

12.78%

Illustration 1: Gross profit ratio

2013 2014 2015 2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.13% 4.34% 4.11%

4.47%

5.03%

Illustration 2: Net profit ratio

Interpretation

By considering the above stated profitability ratios it can be found that, gross profit ratio

fluctuates from the FY 2013 to 2017. There is neither increasing trend nor decreasing by which it

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be said that, Cranswick not able to manage cost of goods sold in proper direction at the end

of each year. Apart from this, it has not welled strategies for reducing the COGS within each and

every year which lead to fluctuate.

Moreover, declining net profit ratio from 4.13% to 4.11% at the end of FY 2015 indicates

that, indirect expenses like interest and taxation amount are increased. When looking at the

financial year 2017 then it can be found that, NP ratio increases from 4.11% to 5.03%. On the

basis of such figures, it can be depicted that, Cranswick's management utilise resources in

effective manner and decline the indirect costs. As per the profitability ratios, performance of

Cranswick is at the average level. Therefore, the company should boost up sales and revenue and

reduce total cost of selling. It will be highly supportive for it in order to generate higher profit

and raise business performance in food industry.

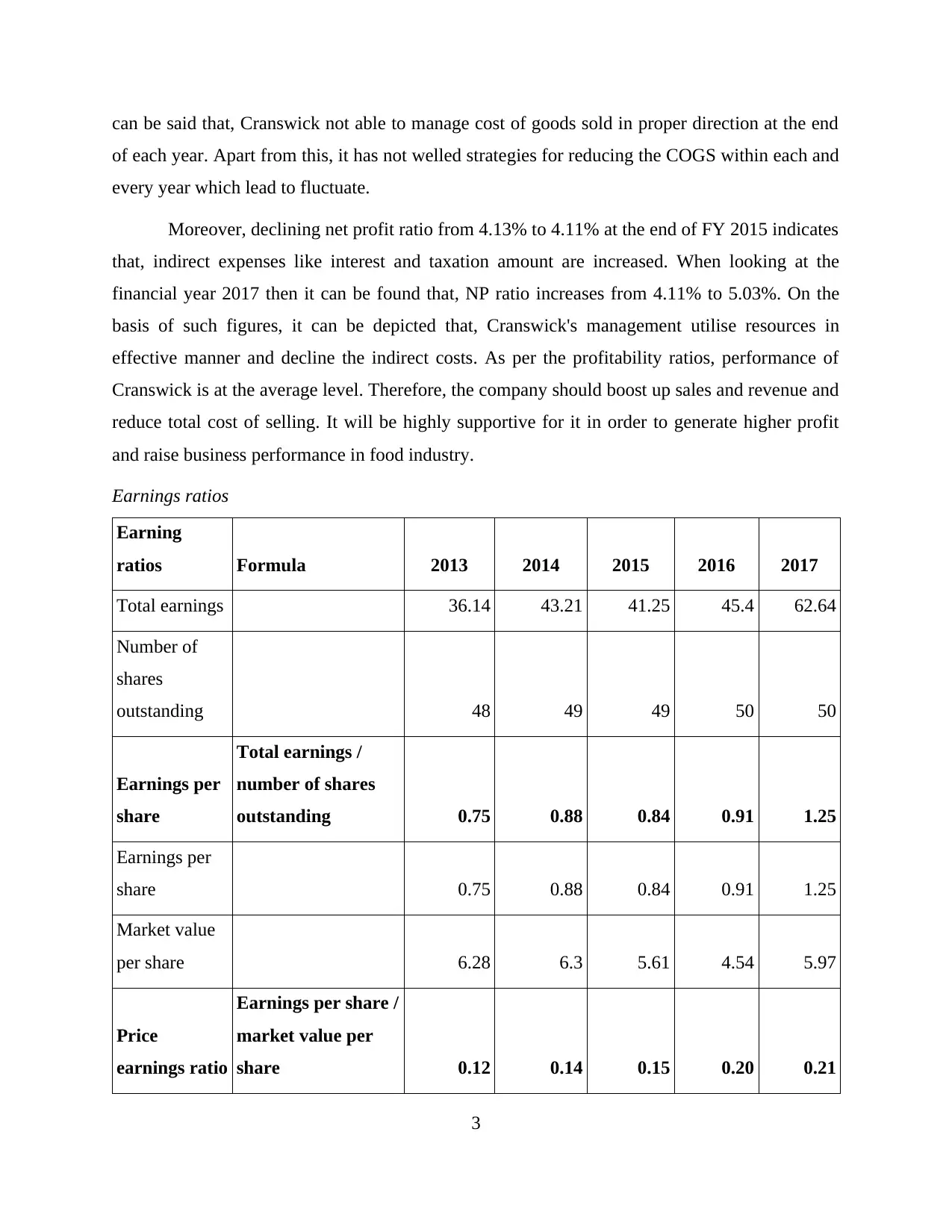

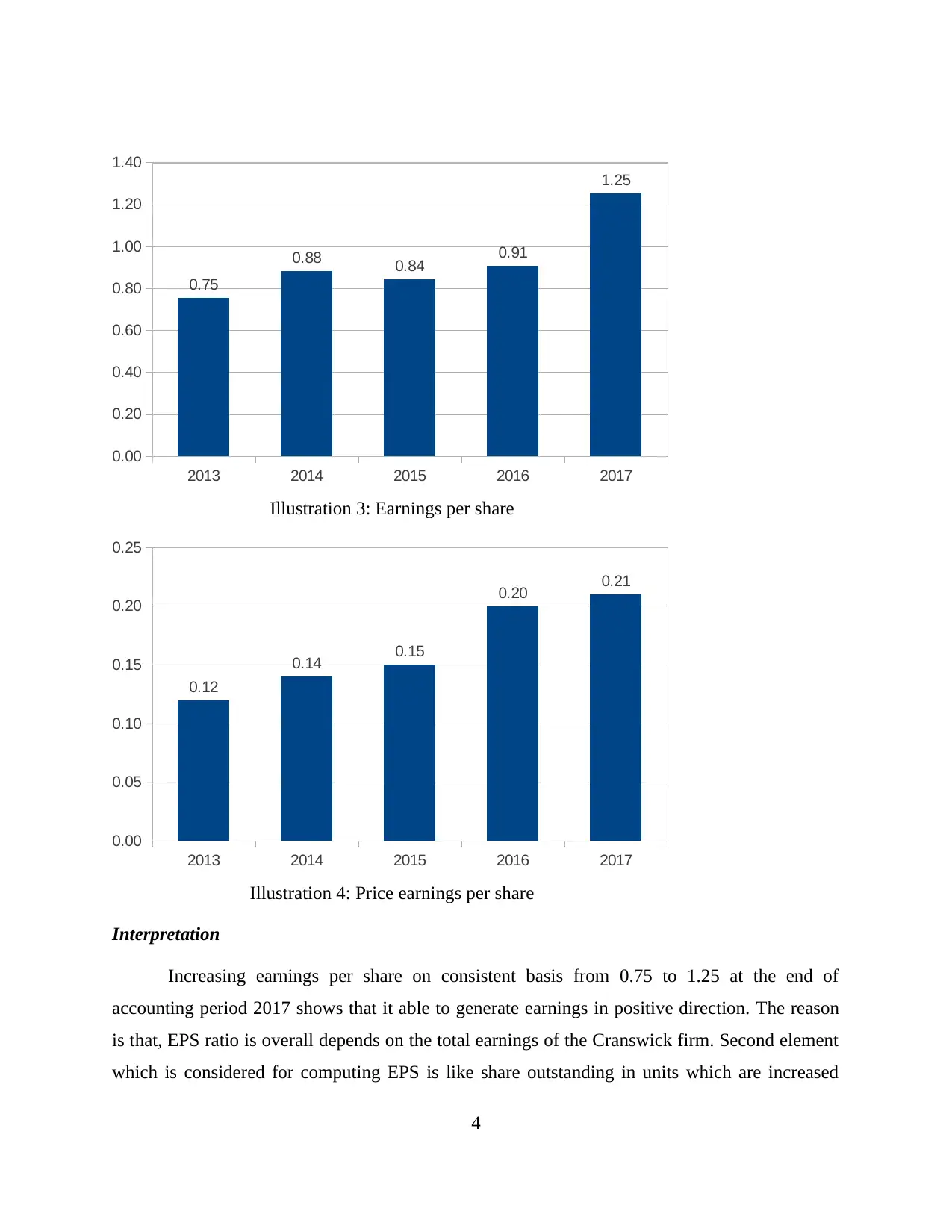

Earnings ratios

Earning

ratios Formula 2013 2014 2015 2016 2017

Total earnings 36.14 43.21 41.25 45.4 62.64

Number of

shares

outstanding 48 49 49 50 50

Earnings per

share

Total earnings /

number of shares

outstanding 0.75 0.88 0.84 0.91 1.25

Earnings per

share 0.75 0.88 0.84 0.91 1.25

Market value

per share 6.28 6.3 5.61 4.54 5.97

Price

earnings ratio

Earnings per share /

market value per

share 0.12 0.14 0.15 0.20 0.21

3

of each year. Apart from this, it has not welled strategies for reducing the COGS within each and

every year which lead to fluctuate.

Moreover, declining net profit ratio from 4.13% to 4.11% at the end of FY 2015 indicates

that, indirect expenses like interest and taxation amount are increased. When looking at the

financial year 2017 then it can be found that, NP ratio increases from 4.11% to 5.03%. On the

basis of such figures, it can be depicted that, Cranswick's management utilise resources in

effective manner and decline the indirect costs. As per the profitability ratios, performance of

Cranswick is at the average level. Therefore, the company should boost up sales and revenue and

reduce total cost of selling. It will be highly supportive for it in order to generate higher profit

and raise business performance in food industry.

Earnings ratios

Earning

ratios Formula 2013 2014 2015 2016 2017

Total earnings 36.14 43.21 41.25 45.4 62.64

Number of

shares

outstanding 48 49 49 50 50

Earnings per

share

Total earnings /

number of shares

outstanding 0.75 0.88 0.84 0.91 1.25

Earnings per

share 0.75 0.88 0.84 0.91 1.25

Market value

per share 6.28 6.3 5.61 4.54 5.97

Price

earnings ratio

Earnings per share /

market value per

share 0.12 0.14 0.15 0.20 0.21

3

2013 2014 2015 2016 2017

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0.75

0.88 0.84 0.91

1.25

Illustration 3: Earnings per share

2013 2014 2015 2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.12

0.14 0.15

0.20 0.21

Illustration 4: Price earnings per share

Interpretation

Increasing earnings per share on consistent basis from 0.75 to 1.25 at the end of

accounting period 2017 shows that it able to generate earnings in positive direction. The reason

is that, EPS ratio is overall depends on the total earnings of the Cranswick firm. Second element

which is considered for computing EPS is like share outstanding in units which are increased

4

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

0.75

0.88 0.84 0.91

1.25

Illustration 3: Earnings per share

2013 2014 2015 2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.12

0.14 0.15

0.20 0.21

Illustration 4: Price earnings per share

Interpretation

Increasing earnings per share on consistent basis from 0.75 to 1.25 at the end of

accounting period 2017 shows that it able to generate earnings in positive direction. The reason

is that, EPS ratio is overall depends on the total earnings of the Cranswick firm. Second element

which is considered for computing EPS is like share outstanding in units which are increased

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

within every two years (Robinson and et.al., 2015). From the fiscal year 2013 to 2016, EPS

enhances from 0.75 to 0.91 only in which growth rate is very slow. From the FY 2016 to 2017, it

able to earn per share with the highest rate due to increasing from 0.91 to 1.25.

When looking at the price-earnings ratio then it can be analysed that, company generates

positive value in each financial period. At the end of FY 2013 value of this ratio is 0.12 which

enhanced up to 0.21 at the end of FY 2017. According to such both the ratios it can be said that,

Cranswick company performs better within food industry up to certain extent. This performance

is gained by the management with the help of EPS because market value of each share is

declining or fluctuating over the years. Henceforth, the Cranswick enterprise needs to boost up

market value on consistent basis which is supportive for increasing business performance at the

end of year.

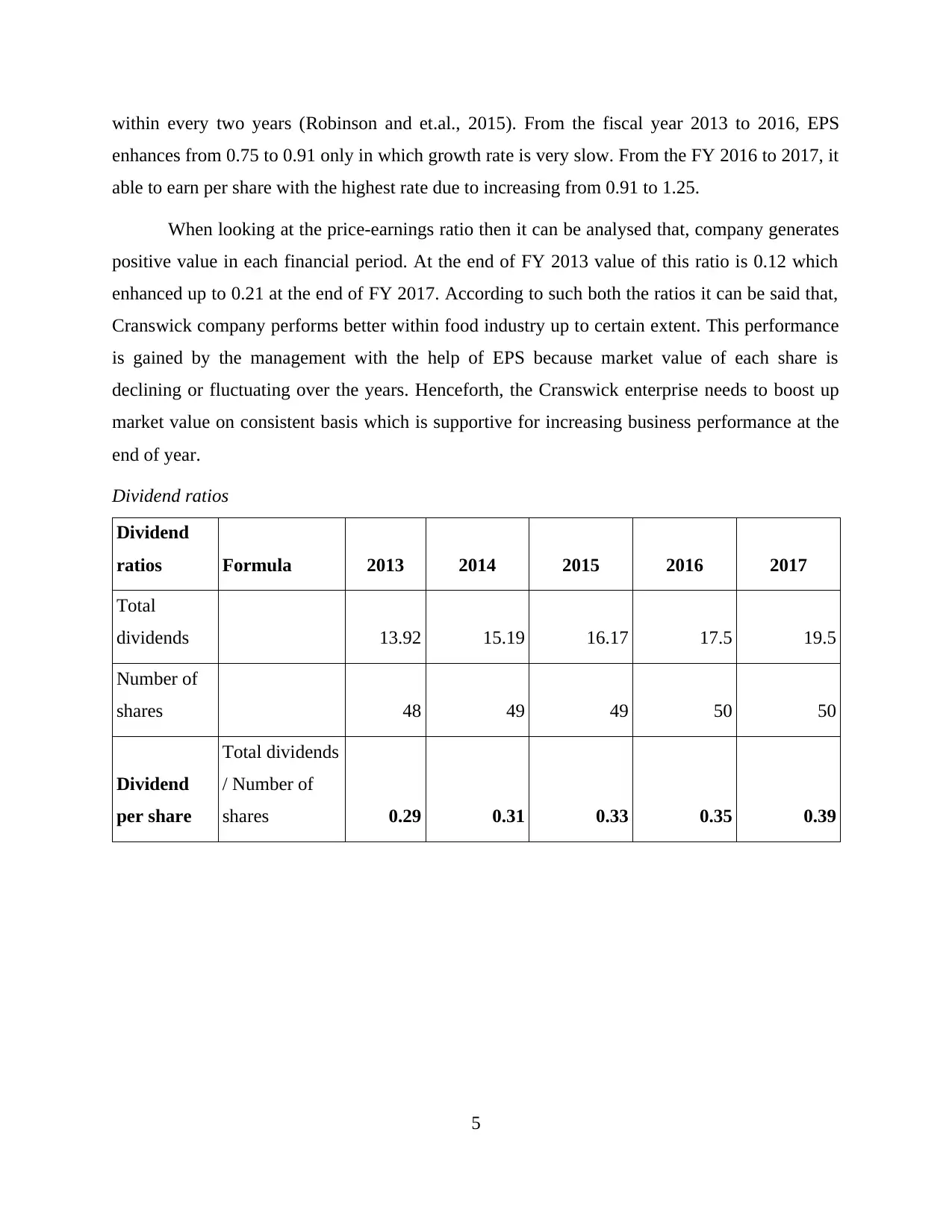

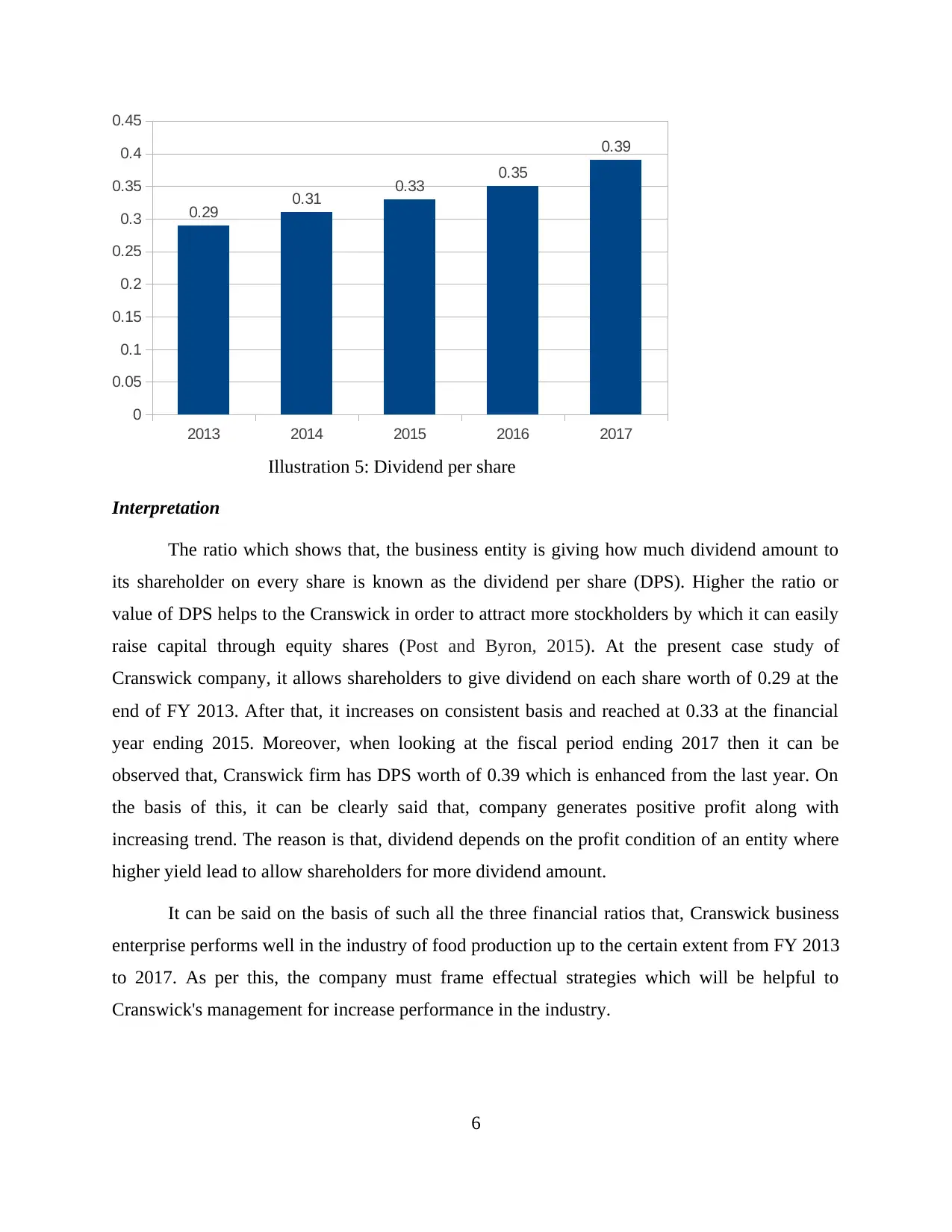

Dividend ratios

Dividend

ratios Formula 2013 2014 2015 2016 2017

Total

dividends 13.92 15.19 16.17 17.5 19.5

Number of

shares 48 49 49 50 50

Dividend

per share

Total dividends

/ Number of

shares 0.29 0.31 0.33 0.35 0.39

5

enhances from 0.75 to 0.91 only in which growth rate is very slow. From the FY 2016 to 2017, it

able to earn per share with the highest rate due to increasing from 0.91 to 1.25.

When looking at the price-earnings ratio then it can be analysed that, company generates

positive value in each financial period. At the end of FY 2013 value of this ratio is 0.12 which

enhanced up to 0.21 at the end of FY 2017. According to such both the ratios it can be said that,

Cranswick company performs better within food industry up to certain extent. This performance

is gained by the management with the help of EPS because market value of each share is

declining or fluctuating over the years. Henceforth, the Cranswick enterprise needs to boost up

market value on consistent basis which is supportive for increasing business performance at the

end of year.

Dividend ratios

Dividend

ratios Formula 2013 2014 2015 2016 2017

Total

dividends 13.92 15.19 16.17 17.5 19.5

Number of

shares 48 49 49 50 50

Dividend

per share

Total dividends

/ Number of

shares 0.29 0.31 0.33 0.35 0.39

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2013 2014 2015 2016 2017

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.29 0.31 0.33 0.35

0.39

Illustration 5: Dividend per share

Interpretation

The ratio which shows that, the business entity is giving how much dividend amount to

its shareholder on every share is known as the dividend per share (DPS). Higher the ratio or

value of DPS helps to the Cranswick in order to attract more stockholders by which it can easily

raise capital through equity shares (Post and Byron, 2015). At the present case study of

Cranswick company, it allows shareholders to give dividend on each share worth of 0.29 at the

end of FY 2013. After that, it increases on consistent basis and reached at 0.33 at the financial

year ending 2015. Moreover, when looking at the fiscal period ending 2017 then it can be

observed that, Cranswick firm has DPS worth of 0.39 which is enhanced from the last year. On

the basis of this, it can be clearly said that, company generates positive profit along with

increasing trend. The reason is that, dividend depends on the profit condition of an entity where

higher yield lead to allow shareholders for more dividend amount.

It can be said on the basis of such all the three financial ratios that, Cranswick business

enterprise performs well in the industry of food production up to the certain extent from FY 2013

to 2017. As per this, the company must frame effectual strategies which will be helpful to

Cranswick's management for increase performance in the industry.

6

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.29 0.31 0.33 0.35

0.39

Illustration 5: Dividend per share

Interpretation

The ratio which shows that, the business entity is giving how much dividend amount to

its shareholder on every share is known as the dividend per share (DPS). Higher the ratio or

value of DPS helps to the Cranswick in order to attract more stockholders by which it can easily

raise capital through equity shares (Post and Byron, 2015). At the present case study of

Cranswick company, it allows shareholders to give dividend on each share worth of 0.29 at the

end of FY 2013. After that, it increases on consistent basis and reached at 0.33 at the financial

year ending 2015. Moreover, when looking at the fiscal period ending 2017 then it can be

observed that, Cranswick firm has DPS worth of 0.39 which is enhanced from the last year. On

the basis of this, it can be clearly said that, company generates positive profit along with

increasing trend. The reason is that, dividend depends on the profit condition of an entity where

higher yield lead to allow shareholders for more dividend amount.

It can be said on the basis of such all the three financial ratios that, Cranswick business

enterprise performs well in the industry of food production up to the certain extent from FY 2013

to 2017. As per this, the company must frame effectual strategies which will be helpful to

Cranswick's management for increase performance in the industry.

6

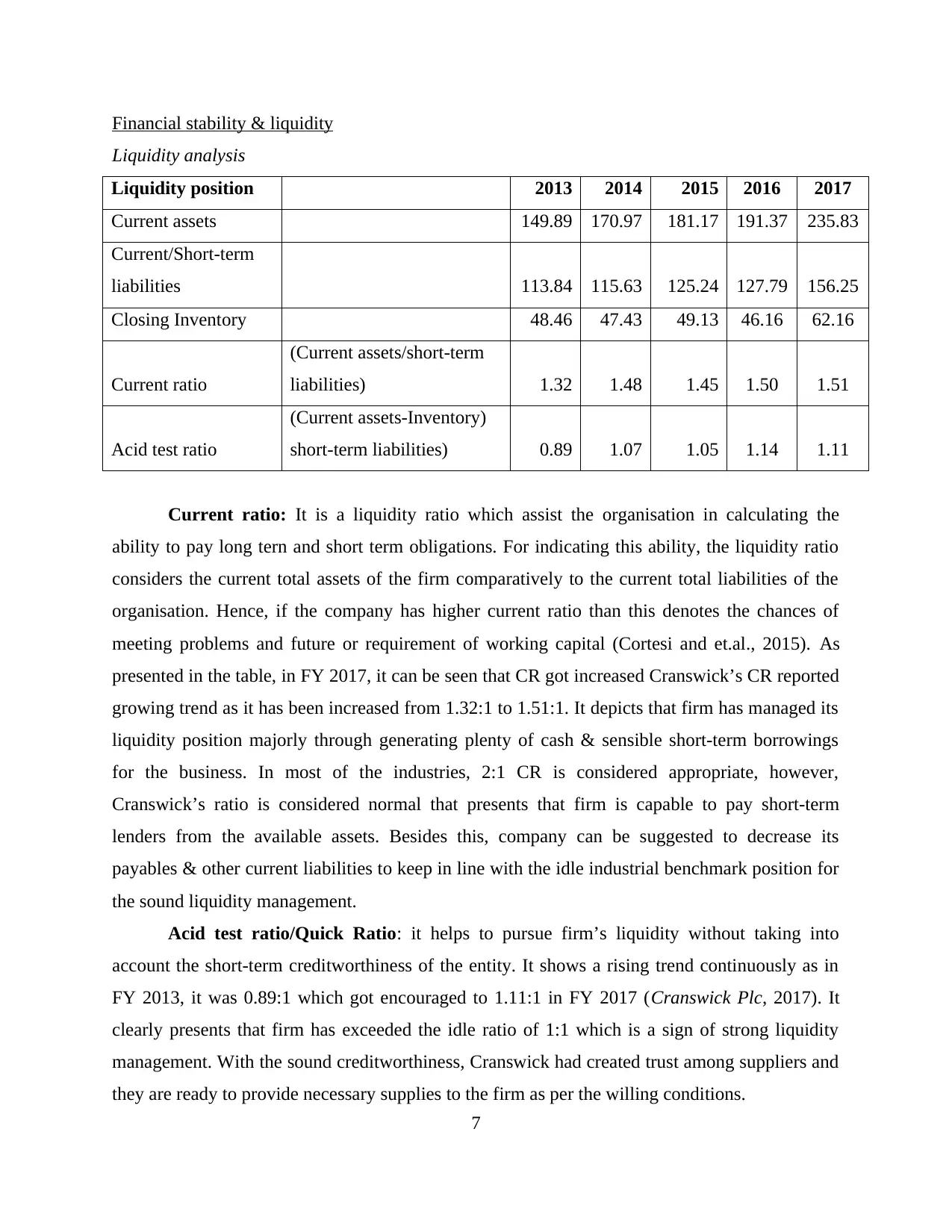

Financial stability & liquidity

Liquidity analysis

Liquidity position 2013 2014 2015 2016 2017

Current assets 149.89 170.97 181.17 191.37 235.83

Current/Short-term

liabilities 113.84 115.63 125.24 127.79 156.25

Closing Inventory 48.46 47.43 49.13 46.16 62.16

Current ratio

(Current assets/short-term

liabilities) 1.32 1.48 1.45 1.50 1.51

Acid test ratio

(Current assets-Inventory)

short-term liabilities) 0.89 1.07 1.05 1.14 1.11

Current ratio: It is a liquidity ratio which assist the organisation in calculating the

ability to pay long tern and short term obligations. For indicating this ability, the liquidity ratio

considers the current total assets of the firm comparatively to the current total liabilities of the

organisation. Hence, if the company has higher current ratio than this denotes the chances of

meeting problems and future or requirement of working capital (Cortesi and et.al., 2015). As

presented in the table, in FY 2017, it can be seen that CR got increased Cranswick’s CR reported

growing trend as it has been increased from 1.32:1 to 1.51:1. It depicts that firm has managed its

liquidity position majorly through generating plenty of cash & sensible short-term borrowings

for the business. In most of the industries, 2:1 CR is considered appropriate, however,

Cranswick’s ratio is considered normal that presents that firm is capable to pay short-term

lenders from the available assets. Besides this, company can be suggested to decrease its

payables & other current liabilities to keep in line with the idle industrial benchmark position for

the sound liquidity management.

Acid test ratio/Quick Ratio: it helps to pursue firm’s liquidity without taking into

account the short-term creditworthiness of the entity. It shows a rising trend continuously as in

FY 2013, it was 0.89:1 which got encouraged to 1.11:1 in FY 2017 (Cranswick Plc, 2017). It

clearly presents that firm has exceeded the idle ratio of 1:1 which is a sign of strong liquidity

management. With the sound creditworthiness, Cranswick had created trust among suppliers and

they are ready to provide necessary supplies to the firm as per the willing conditions.

7

Liquidity analysis

Liquidity position 2013 2014 2015 2016 2017

Current assets 149.89 170.97 181.17 191.37 235.83

Current/Short-term

liabilities 113.84 115.63 125.24 127.79 156.25

Closing Inventory 48.46 47.43 49.13 46.16 62.16

Current ratio

(Current assets/short-term

liabilities) 1.32 1.48 1.45 1.50 1.51

Acid test ratio

(Current assets-Inventory)

short-term liabilities) 0.89 1.07 1.05 1.14 1.11

Current ratio: It is a liquidity ratio which assist the organisation in calculating the

ability to pay long tern and short term obligations. For indicating this ability, the liquidity ratio

considers the current total assets of the firm comparatively to the current total liabilities of the

organisation. Hence, if the company has higher current ratio than this denotes the chances of

meeting problems and future or requirement of working capital (Cortesi and et.al., 2015). As

presented in the table, in FY 2017, it can be seen that CR got increased Cranswick’s CR reported

growing trend as it has been increased from 1.32:1 to 1.51:1. It depicts that firm has managed its

liquidity position majorly through generating plenty of cash & sensible short-term borrowings

for the business. In most of the industries, 2:1 CR is considered appropriate, however,

Cranswick’s ratio is considered normal that presents that firm is capable to pay short-term

lenders from the available assets. Besides this, company can be suggested to decrease its

payables & other current liabilities to keep in line with the idle industrial benchmark position for

the sound liquidity management.

Acid test ratio/Quick Ratio: it helps to pursue firm’s liquidity without taking into

account the short-term creditworthiness of the entity. It shows a rising trend continuously as in

FY 2013, it was 0.89:1 which got encouraged to 1.11:1 in FY 2017 (Cranswick Plc, 2017). It

clearly presents that firm has exceeded the idle ratio of 1:1 which is a sign of strong liquidity

management. With the sound creditworthiness, Cranswick had created trust among suppliers and

they are ready to provide necessary supplies to the firm as per the willing conditions.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

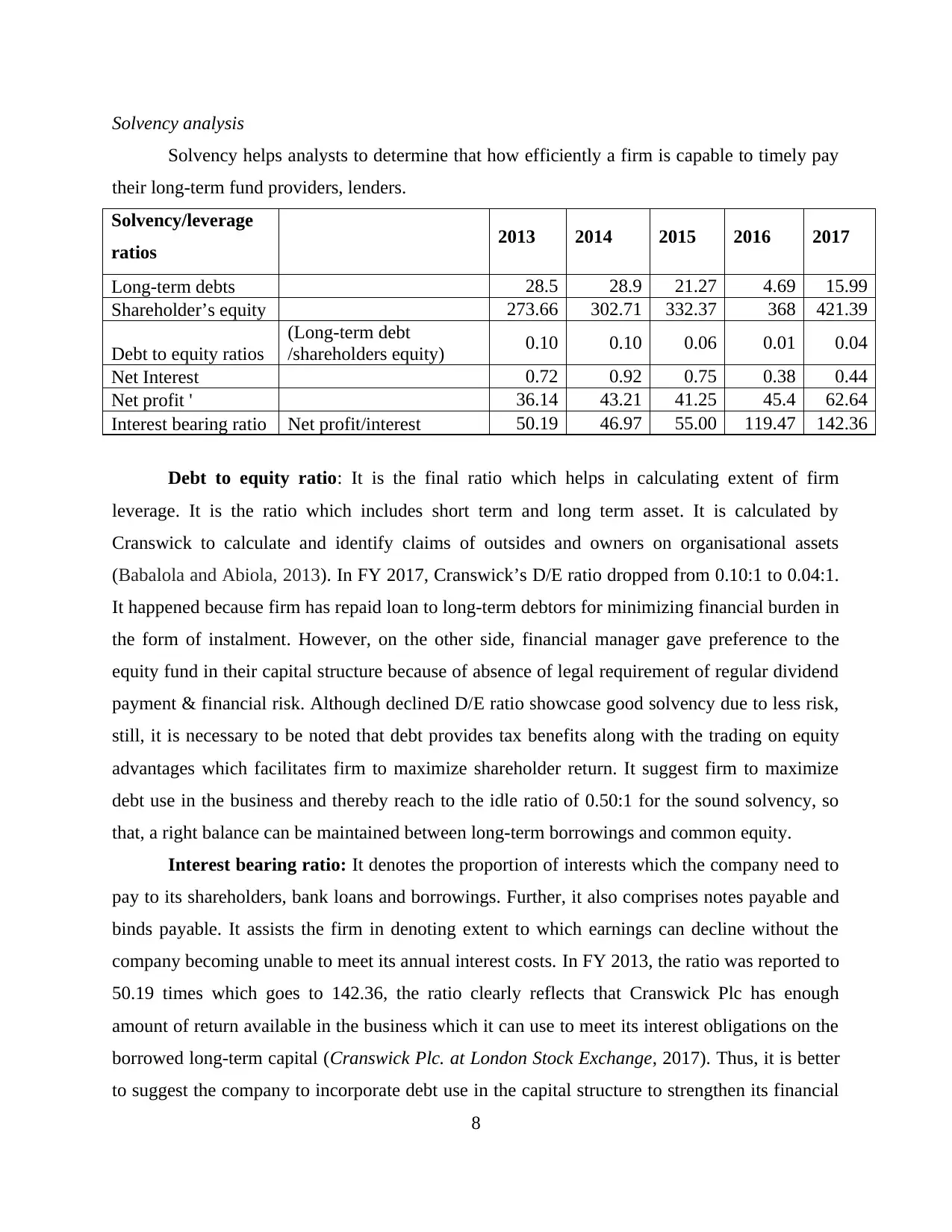

Solvency analysis

Solvency helps analysts to determine that how efficiently a firm is capable to timely pay

their long-term fund providers, lenders.

Solvency/leverage

ratios 2013 2014 2015 2016 2017

Long-term debts 28.5 28.9 21.27 4.69 15.99

Shareholder’s equity 273.66 302.71 332.37 368 421.39

Debt to equity ratios

(Long-term debt

/shareholders equity) 0.10 0.10 0.06 0.01 0.04

Net Interest 0.72 0.92 0.75 0.38 0.44

Net profit ' 36.14 43.21 41.25 45.4 62.64

Interest bearing ratio Net profit/interest 50.19 46.97 55.00 119.47 142.36

Debt to equity ratio: It is the final ratio which helps in calculating extent of firm

leverage. It is the ratio which includes short term and long term asset. It is calculated by

Cranswick to calculate and identify claims of outsides and owners on organisational assets

(Babalola and Abiola, 2013). In FY 2017, Cranswick’s D/E ratio dropped from 0.10:1 to 0.04:1.

It happened because firm has repaid loan to long-term debtors for minimizing financial burden in

the form of instalment. However, on the other side, financial manager gave preference to the

equity fund in their capital structure because of absence of legal requirement of regular dividend

payment & financial risk. Although declined D/E ratio showcase good solvency due to less risk,

still, it is necessary to be noted that debt provides tax benefits along with the trading on equity

advantages which facilitates firm to maximize shareholder return. It suggest firm to maximize

debt use in the business and thereby reach to the idle ratio of 0.50:1 for the sound solvency, so

that, a right balance can be maintained between long-term borrowings and common equity.

Interest bearing ratio: It denotes the proportion of interests which the company need to

pay to its shareholders, bank loans and borrowings. Further, it also comprises notes payable and

binds payable. It assists the firm in denoting extent to which earnings can decline without the

company becoming unable to meet its annual interest costs. In FY 2013, the ratio was reported to

50.19 times which goes to 142.36, the ratio clearly reflects that Cranswick Plc has enough

amount of return available in the business which it can use to meet its interest obligations on the

borrowed long-term capital (Cranswick Plc. at London Stock Exchange, 2017). Thus, it is better

to suggest the company to incorporate debt use in the capital structure to strengthen its financial

8

Solvency helps analysts to determine that how efficiently a firm is capable to timely pay

their long-term fund providers, lenders.

Solvency/leverage

ratios 2013 2014 2015 2016 2017

Long-term debts 28.5 28.9 21.27 4.69 15.99

Shareholder’s equity 273.66 302.71 332.37 368 421.39

Debt to equity ratios

(Long-term debt

/shareholders equity) 0.10 0.10 0.06 0.01 0.04

Net Interest 0.72 0.92 0.75 0.38 0.44

Net profit ' 36.14 43.21 41.25 45.4 62.64

Interest bearing ratio Net profit/interest 50.19 46.97 55.00 119.47 142.36

Debt to equity ratio: It is the final ratio which helps in calculating extent of firm

leverage. It is the ratio which includes short term and long term asset. It is calculated by

Cranswick to calculate and identify claims of outsides and owners on organisational assets

(Babalola and Abiola, 2013). In FY 2017, Cranswick’s D/E ratio dropped from 0.10:1 to 0.04:1.

It happened because firm has repaid loan to long-term debtors for minimizing financial burden in

the form of instalment. However, on the other side, financial manager gave preference to the

equity fund in their capital structure because of absence of legal requirement of regular dividend

payment & financial risk. Although declined D/E ratio showcase good solvency due to less risk,

still, it is necessary to be noted that debt provides tax benefits along with the trading on equity

advantages which facilitates firm to maximize shareholder return. It suggest firm to maximize

debt use in the business and thereby reach to the idle ratio of 0.50:1 for the sound solvency, so

that, a right balance can be maintained between long-term borrowings and common equity.

Interest bearing ratio: It denotes the proportion of interests which the company need to

pay to its shareholders, bank loans and borrowings. Further, it also comprises notes payable and

binds payable. It assists the firm in denoting extent to which earnings can decline without the

company becoming unable to meet its annual interest costs. In FY 2013, the ratio was reported to

50.19 times which goes to 142.36, the ratio clearly reflects that Cranswick Plc has enough

amount of return available in the business which it can use to meet its interest obligations on the

borrowed long-term capital (Cranswick Plc. at London Stock Exchange, 2017). Thus, it is better

to suggest the company to incorporate debt use in the capital structure to strengthen its financial

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stability and solvency. It will offer benefit of TOE wherein Cranswick can reduce its tax burden

through getting deductions and thereby maximize return for the shareholders.

SECTION B

Critical reflection on the company portrayed by financial reports

Cranswick the leading food producer of UK, has earned 1245 million pound in 2017 by

22.5%. Further, according to the scholars, revenue was up by 12.7 percent and before tax profit

was 75.5 Million pound which was increased by 17.2%. Besides, the organisations earning per

share was 17.6%. As per researchers, the earnings increased by 18.1 pens from 2016 to 2017.

Further, the statutory profit before tax while functioning increased by 24.8% in 2017

while in 2016 the share was 62.1 Million pound but not it has increased to 77.5 Million pound.

Moreover, as per the researchers the earning per share during the operations of 2017 increased by

25.6% which was very beneficial for company as in 2016 it was only 98.9 Pens and in 2017 it

increased rapidly to 124.2 Pens. Hence, scholar stated that final dividend of Cranswick has been

increased by 19.7 percent in 2017 which created a revolution in food industry of UK because it

was 25.9 pens in 2016 and in 2017 it increased to 31.0 pens.

Henceforth, from analysis of financial report of the company scholar stated that, the

company is improving its functions and operations every year to increase its revenue and profits.

Further, from the analysis it can be said that the company has continuous growth and has stable

market in UK (Delen, Kuzey and Uyar, 2013). The secret behind rapid growth and increasing

profit is following the proper regulations and serving customer satisfaction in order to maximize

profits.

An evaluation of the corporate governance

Corporate governance is defined as an integrated system of corporate rules, regulations,

principles and practices that is followed in the daily operations for meeting out stakeholder’s

responsibilities. In order to implement quality governing framework for the stewardship,

Cranswick’s board of directors are responsible to overlook the business code of conduct and

regular affairs so as to ensure sustainable value for all the stakeholders (Revell, 2016). The board

member gives respect to their key stakeholders including suppliers, employees, community,

customers, investors and others by complying with the Financial Reporting Council’s

professional code of conduct i.e. trustworthiness, integrity, environmental sustainability and

9

through getting deductions and thereby maximize return for the shareholders.

SECTION B

Critical reflection on the company portrayed by financial reports

Cranswick the leading food producer of UK, has earned 1245 million pound in 2017 by

22.5%. Further, according to the scholars, revenue was up by 12.7 percent and before tax profit

was 75.5 Million pound which was increased by 17.2%. Besides, the organisations earning per

share was 17.6%. As per researchers, the earnings increased by 18.1 pens from 2016 to 2017.

Further, the statutory profit before tax while functioning increased by 24.8% in 2017

while in 2016 the share was 62.1 Million pound but not it has increased to 77.5 Million pound.

Moreover, as per the researchers the earning per share during the operations of 2017 increased by

25.6% which was very beneficial for company as in 2016 it was only 98.9 Pens and in 2017 it

increased rapidly to 124.2 Pens. Hence, scholar stated that final dividend of Cranswick has been

increased by 19.7 percent in 2017 which created a revolution in food industry of UK because it

was 25.9 pens in 2016 and in 2017 it increased to 31.0 pens.

Henceforth, from analysis of financial report of the company scholar stated that, the

company is improving its functions and operations every year to increase its revenue and profits.

Further, from the analysis it can be said that the company has continuous growth and has stable

market in UK (Delen, Kuzey and Uyar, 2013). The secret behind rapid growth and increasing

profit is following the proper regulations and serving customer satisfaction in order to maximize

profits.

An evaluation of the corporate governance

Corporate governance is defined as an integrated system of corporate rules, regulations,

principles and practices that is followed in the daily operations for meeting out stakeholder’s

responsibilities. In order to implement quality governing framework for the stewardship,

Cranswick’s board of directors are responsible to overlook the business code of conduct and

regular affairs so as to ensure sustainable value for all the stakeholders (Revell, 2016). The board

member gives respect to their key stakeholders including suppliers, employees, community,

customers, investors and others by complying with the Financial Reporting Council’s

professional code of conduct i.e. trustworthiness, integrity, environmental sustainability and

9

others. Cranswick prepare their financial statement and publish it to the public to provide them

required information. However, for the employees, the board members believes in blending

varied skills, knowledge and talent of the employees through hiring diversified workers at the

workplace. They are also provided with the training programmes to support their career growth

opportunities.

Figure 1 Risk management & governance of Cranswick Plc

(Source: Business model & strategy, 2013)

As illustrated above, company’s risk committee is accountable to identify various

business risks i.e. financial, operational and regulatory risk and use suitable plans and strategies

to address it effectively. Internal control mechanism is also used for directing and supervision of

the regular activities. Risk committee report possible risks and advise risk mitigation plans to the

Cranswick’s Audit committee (Lee, Sameen and Cowling, 2015). Company also audited their

10

required information. However, for the employees, the board members believes in blending

varied skills, knowledge and talent of the employees through hiring diversified workers at the

workplace. They are also provided with the training programmes to support their career growth

opportunities.

Figure 1 Risk management & governance of Cranswick Plc

(Source: Business model & strategy, 2013)

As illustrated above, company’s risk committee is accountable to identify various

business risks i.e. financial, operational and regulatory risk and use suitable plans and strategies

to address it effectively. Internal control mechanism is also used for directing and supervision of

the regular activities. Risk committee report possible risks and advise risk mitigation plans to the

Cranswick’s Audit committee (Lee, Sameen and Cowling, 2015). Company also audited their

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.