Financial Crime: Ethical Implications of Tax Avoidance

VerifiedAdded on 2023/01/13

|19

|1110

|82

Presentation

AI Summary

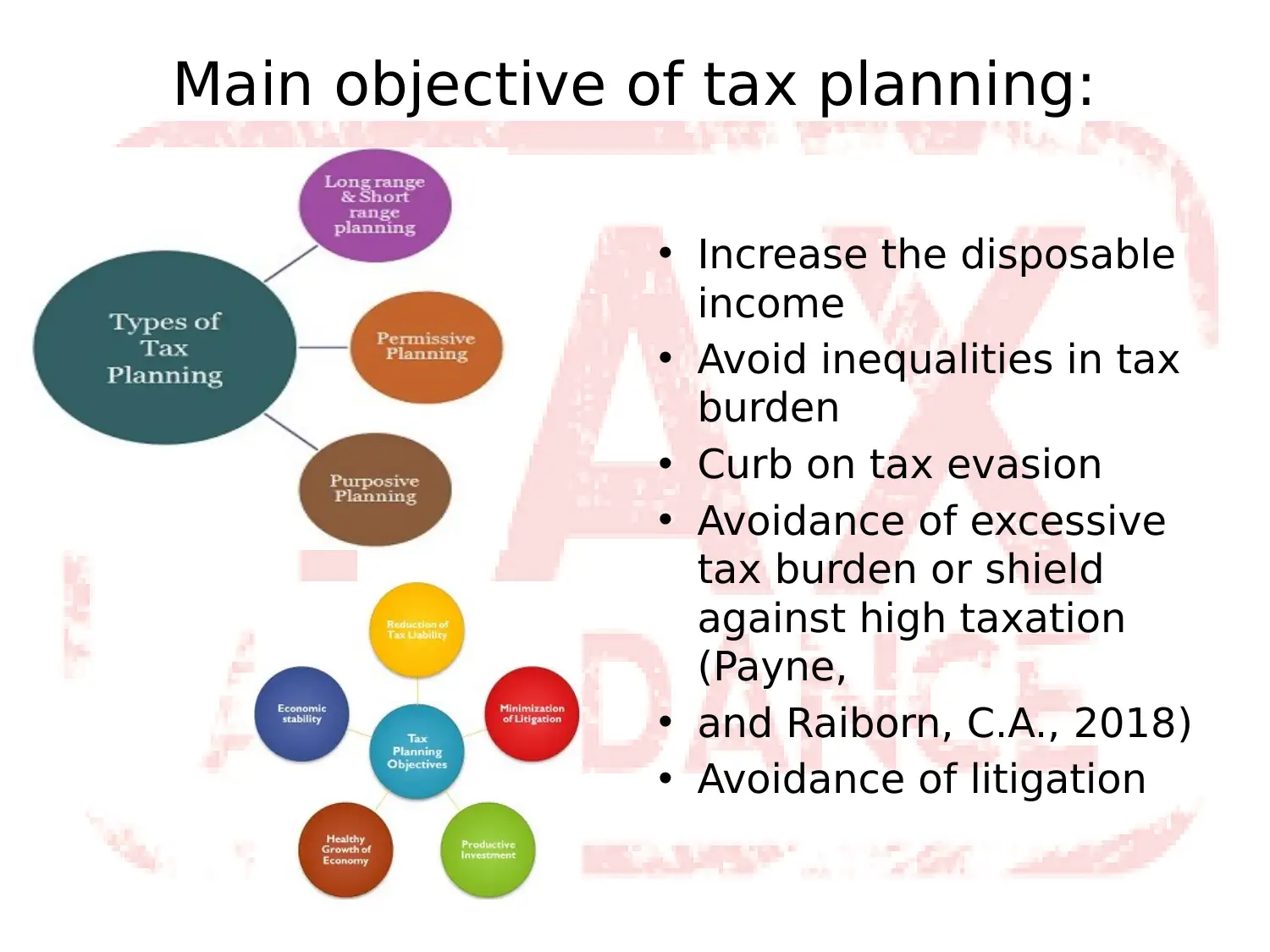

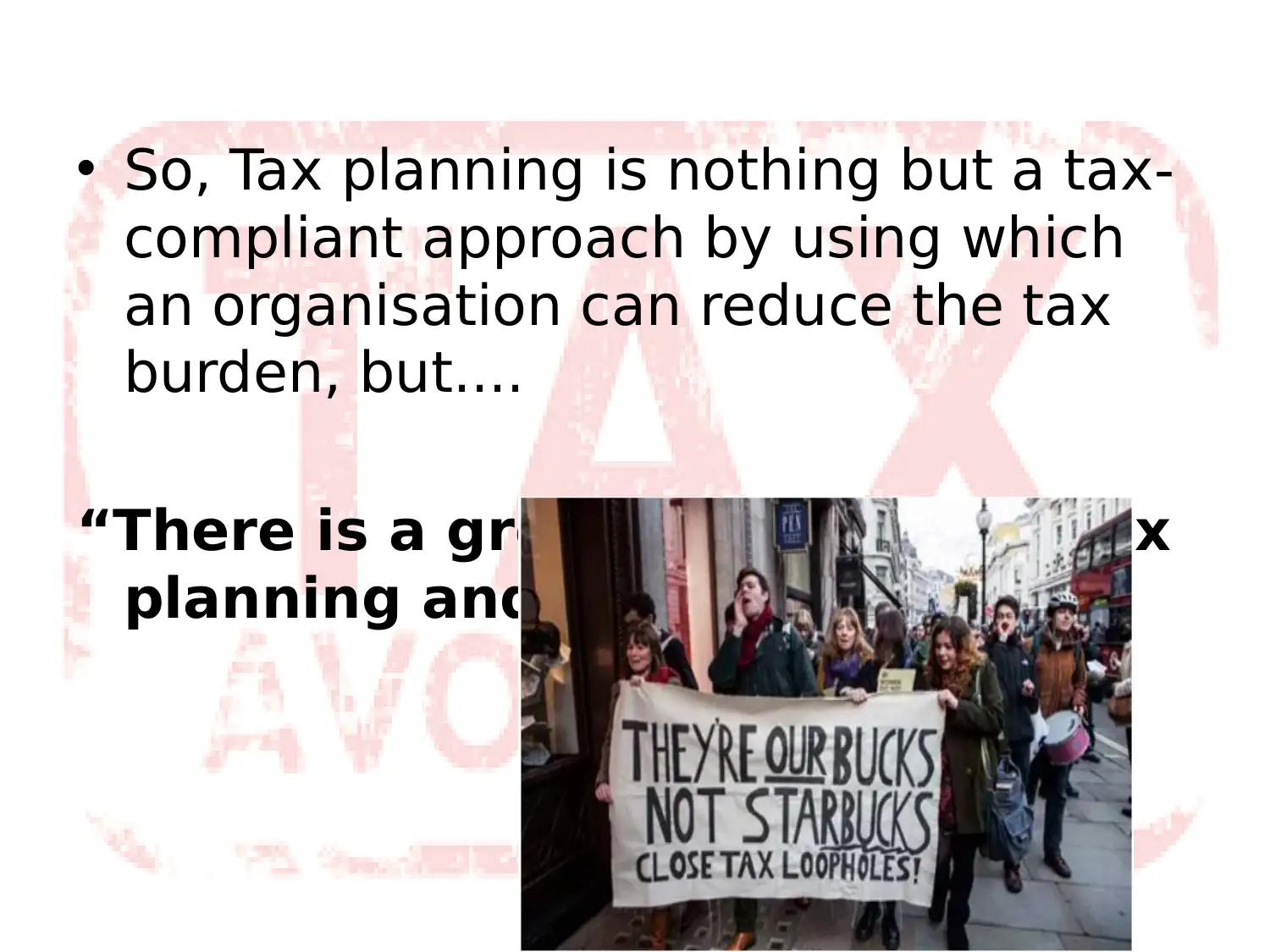

This presentation critically examines the ethical implications of aggressive corporate tax avoidance within the realm of financial crime. It begins by defining corporate tax and tax planning, differentiating it from aggressive tax avoidance. The presentation explores the grey area between legal tax planning and potentially unethical tax avoidance practices, emphasizing the social responsibility of corporations and the impact of tax avoidance on society. It delves into the concept of tax as a social responsibility and analyzes how aggressive tax avoidance can negatively affect a company's reputation. The presentation further discusses the role of governments in ensuring corporate returns and the importance of certainty in tax regulations. Case studies, such as those involving Amazon and Starbucks, are used to illustrate the real-world consequences of tax avoidance. The presentation concludes by emphasizing the negative societal impacts of tax avoidance, including the shifting of funds away from public goods and the weakening of economic stability. References from academic journals support the arguments presented.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.